The hullabaloo in the repo market torpedoed the function of Interest on Excess Reserves and forced the Fed to go back to the future.

With its announcement this morning, the New York Fed confirmed that the Fed’s Plan A of manipulating the federal funds rate into its target range – now between 1.75% and 2.0% — has miserably failed, and that it will switch to Plan B to control short-term interest rates. But this Plan B used to be Plan A that the Fed had routinely deployed to control short-term interest rates before the Financial Crisis. So back to the future.

The “repo operations” the New York Fed has been conducting since Tuesday were overnight repurchase agreements (ultra-short-term loans), where in the morning, the New York Fed offers up to $75 billion in cash at an interest rate that is within the Fed’s target range. These loans are secured by collateral. The allowed collateral are Treasury securities, Agency securities, and mortgage-backed securities guaranteed by the Government Sponsored Enterprises (GSEs).

These overnight interest-bearing loans unwind the next morning, with the Fed getting its $75 billion in cash back, and the dealers getting their collateral back. As these operations were undertaken every day for the past four days, it’s essentially the same $75 billion that gets recycled every day. The daily amounts are not additive. And these operations have nothing to do with QE.

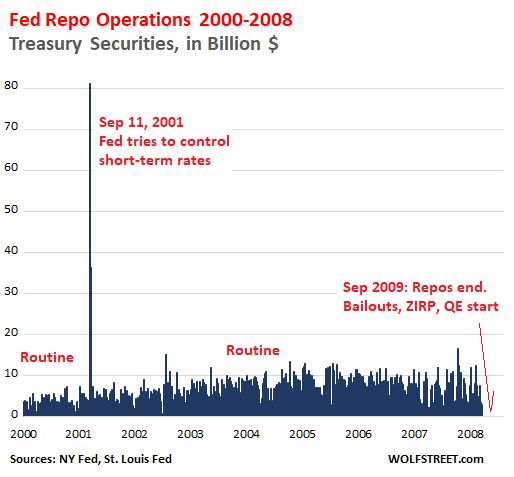

Back in the day, the New York Fed used to conduct these repo operations routinely. But in September 2008, when Lehman and AIG collapsed, the Fed switched from repo operations to emergency bailout loans, zero-interest-rate policy (ZIRP), QE, and other tricks and devices. Repos were no longer needed to control rates.

The chart below shows the tail-end of the era of repo operations through 2008. The spike in repo operations following September 11, 2001, occurred when the Fed briefly injected massive amounts of cash via repos, as funding had dried up, and short-term rates were blowing out:

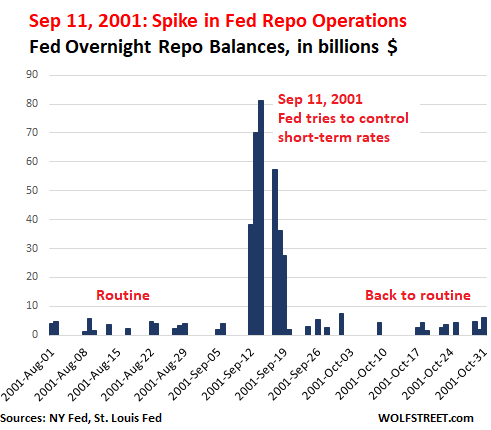

During the September 11, 2001 panic, the Fed conducted these massive repo operations for six mornings in a row. Like all overnight repos, these repos unwound the next day, with the Fed getting its cash back and with banks getting their collateral back.

This chart shows the detail of those operations. Note the amounts, reaching $81 billion on September 14, 2001. Four days later, the operations were over, markets had settled down, overnight funding was plentiful, the Fed got its cash back, and the dealers got their collateral back:

In September 2008, when the US financial system was threatening to freeze up, the Fed developed new tools on the spot, including bailout emergency loans to banks, industrial companies, and market players under a variety of programs, and it shifted to ZIRP and QE. But it stopped the repo operations because they weren’t needed anymore.

Before the Financial Crisis, there were no Excess Reserves, which are deposits that banks park at the Fed to earn the interest, have instant liquidity, and fulfill regulatory capital and liquidity requirements. Excess Reserves started piling up in parallel with QE and peaked in December 2014. Since then, they have fallen by nearly half, to $1.38 trillion.

By paying banks interest on the Excess Reserves (IOER) at a rate equal to the upper limit of its target range, the Fed figured that banks would see to it that the federal funds rate would be less than the IOER. This would keep the federal funds rate within the Fed’s target range. This worked until it didn’t.

Throughout 2018, the federal funds rate hobbled along at the upper limit of the Fed’s target range and occasionally exceeded the limit. The Fed reacted several times by adjusting the IOER to where it was further and further below the upper limit of its target range. That worked until it didn’t.

And on Monday this week, all heck broke loose in the short-term funding market, which is precisely what the Fed is supposed to be able to keep under control.

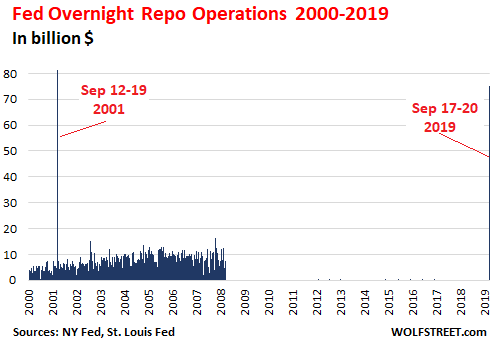

On Tuesday, the New York Fed announced its first repo operation since September 2008. But the magnitude of the financial world has changed over those years: In 2001, the total amount of Treasury debt was $5.6 trillion. Now it is over four times larger, $22.6 trillion. Financialization of everything is a booming business, and the bets have gotten larger, the debt has gotten larger, there is more collateral, and so the amounts have gotten much larger.

If peak-repo day on Sep 14, 2001, is multiplied by four, in parallel with the growth of the US Treasury debt, an equivalent overnight repo operation today would amount to $244 billion. So the $75 billion this morning is small fry. In the chart below of 19 years of repo operations, the thin line on the right represents the past four days:

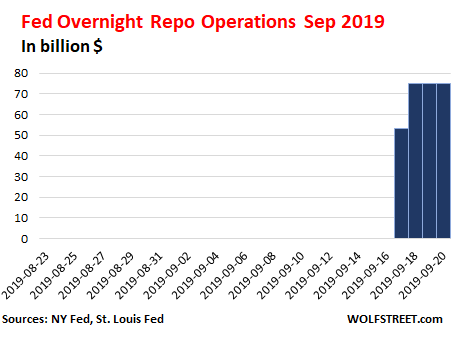

Just looking at the repo operations of the last 30 days:

Admission that Plan A failed; Plan B is now standard.

So here is what the New York Fed, which handles the repos, announced this morning “to help maintain the federal funds rate within the target range”:

- Overnight repo operations will continue through October 10; on Sep 23, for “$75 billion”; on the remaining days for “at least $75 billion.” These repos unwind the next day, with the NY Fed getting its cash back and dealers getting their collateral back.

- Three 14-day repo operations for “at least $30 billion each” (Sep 24, Sep 26, and Sep 27). Each unwinds after 14 days, with the NY Fed getting its cash back, and dealers getting their collateral back.

- After October 10, 2019, the NY Fed will conduct repo operations “as necessary to help maintain the federal funds rate in the target range.”

This third point is admission that the repo facility is now once again an integral part of managing short-term interest rates, as it was before September 2008.

The St. Louis Fed already proposed this months ago.

The St. Louis Fed published two papers on the benefits of a “Standing Repo Facility,” the first paper in March 2019 and the follow-up in April 2019. This standing repo facility is now in operation, officialized by the New York Fed as of this morning.

The two key – but “distinct” – motivations for a standing repo facility are, as cited in the follow-up paper:

First, the facility could be used to support interest rate control by establishing a ceiling on repo rates, thereby guarding against unwanted spikes in money market rates. The use of a ceiling tool for this purpose would be seen as enhancing the monetary policy operating regime of the FOMC.

Second, the facility could be used to reduce the demand for reserves for any given rate of interest on excess reserves.

The first motivation is why the NY Fed uses the facility now: to control spikes in money market rates as seen over the past week and keep the federal funds rate within the Fed’s target range.

The second motivation would be to reduce the excess reserves presumably needed to control the federal funds rate via the IOER. These reserves and the IOER would become less important, because repo operations now pick up much of the work of controlling money market rates. And the level of those reserves (currently $1.38 trillion) could be reduced further, allowing the Fed’s balance sheet to shrink further:

Why the desire to minimize the demand for reserves? In short, because it accords with the FOMC’s stated preference to operate a floor system with the minimum level of reserves necessary to permit the efficient and effective conduct of monetary policy: “minimally ample reserves” for short.

So this standing repo facility, as we’re looking at it today, takes pressure off those reserves, and it takes the Fed back a step closer to managing short term rates as it used to do before the Financial Crisis.

Nevertheless, the fact that the Fed was forced all of a sudden by a panicky market to abandon Plan A and revert to how it used to do it, rather than implementing the transition methodically, on its own, in its gradual manner, must have come as a shock.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Why does this “repo” works if is just circulating money in a Möbius strip and everyone knows that?

As you know, moving around a Möbius strip you end up exactly on the other side of where you started. As applied to money, that sounds more like the inner workings of a so-called Public-Private Partnership ;-).

Err, no. There is no “other side” to a Mobius strip. Get some scrap paper and make one and see. You owe it to yourself if you never did it as a kid or in college. It’s really weird. It literally only has one side.

No, Alex,. One round and you end upon the opposite side. You have to go two rounds to make it back to the same side.

NARmageddon

If a Mobius strip had two sides you’d be able to colour one side red and the other blue. You can’t. Try it.

I did not say that the Möbius strip has two sides. I said that if (you start at any point) and go ONE round you will end up on the opposite side of the band from the point where you started. If you go TWO rounds, you will end up at the same point where you started.

Well, I just constructed a Mobius strip. I started with a sheet of paper purple on one side, the other side white. (Then cut off a strip.)

To construct the Mobius strip, (after the twist), I had to join the purple side to the white side.

Is this where, Presto-Changeo, dirty money transmogrifies to clean money ? OK, loved the simile; and I found the construction informative.

Looks to me as if unwinding the Mobius strip requires cutting it…..and moving on to the global economy, how do we unwind the Gordian knot of the past decade-plus? BTW, I’m ruling out NIRPs.

The Mobius strip example loses its validity when a large counterparty pukes and then cuts the paper and all paths get severed from the tape joint, that being the foul central banks.

What the heck? I just logged in and there were far fewer comments that I reiterated.

Sorry for the redundancy.

NARmageddon

“I said that if (you start at any point) and go ONE round you will end up on the opposite side of the band…”

Apologies for implying you said the strip has two sides but I was misled by your used of the term “opposite side” when you said, “One round and you end upon the opposite side.” You also use the term “Other side”, as alex pointed out, which (to me at least) implies there’s more than one side.

But I disagree that you’ve gone “One round” because if you had you’d be back to where you started, by definition. AISI, you’ve only gone half way round (and are still on the same side, of course).

I find it best to imagine sticking a vector pointing out of the surface at the start point and equidistant from the edges of the strip. Then move a copy of it around the strip (keeping it normal to the surface and equidistant from the edges). When it gets to the half way point it will have its foot in contact with the foot of vector at the start but they will be pointing in the opposite directions[1]. They are both on the same side, of course. If we continue to make the full round we end up back at the start with the vectors pointing in the same direction.

[1] This informs us why a Mobuis strip is termed a non-orientable surface.

What if Trump decided to change his narrative slightly and blame the Federal Reserve for their failures knowing the markets are on the way down. Sign off on the Hong kong human rights bill and thereby starve China of the US dollars it needs. Kill two birds with the one stone,

The “Federal” Reserve is losing control little by little. As to the very negative effects that its policies have had on Americans, particularly on millenials and on baby boomers with pensions and trying to sell expensive homes, see Danielle DiMartino on youtube at Real Vision Finance, who used to work for the “Federal” Reserve. In very cautious language, she points out the upcoming scandal of what the “Fed” has done to Americans, which most have not discovered yet.

She has various politely phrased issues with the “Fed,” but does not deal with the central issue that in choosing policies for twenty years the “Fed” (run by appointees selected by politicians under bankster’s monetary influence through contributions and bankster treasury secretaries) has always selected from various options the policy guaranteed to benefit the banksters that control major banks and harm the average American. Coincidence? I do not think so.

Taking dirty money and making it clean?

Wonder where I have heard that before…

Illegal is what politicians tend to declare on people not following what they want.

This is NOT dirty money, this is lending money and getting the lend money back the next day, without any interest and doing do every day for a while. At most you can say this is “imaginary money” because it never exists besides on paper and digitally.

Dirty money is money that comes from crimes and illegal acts and rven if this kind of manipulation should be a crime, it is not.

raxadian,

These are like interest-bearing overnight loans. The interest rate the Fed gets for them (determined by bidding) has been within the Fed’s target range.

With what as collateral? Highly leveraged CLOs (over-rated JUNK as shown in recently leaked documents from a ratings agency insider to a YouTube blogger), the CDOs of the next crisis?

Winston,

Treasury securities, Agency securities, and MBS guaranteed by the GSEs. These are all government-backed very liquid securities — among the best, most liquid collateral out there.

Even though the interest is tiny (in the grand scheme of things), what does the Fed do to sterilize it, so as not to be deflationary? Apply it to the national debt?

Rowen,

Yes, sort of. The Fed remits its profits to the US Treasury. This is a number I report on once a year in January. Most of this income comes from the interest paid by the securities the Fed holds, such as Treasuries and MBS, and now interest income from those repos.

‘MBS guaranteed by the GSEs’ – quality of this collateral

Aren’t GSE leveraged 1000:1 ?

$6 billion ($3 billion each) guarantee $5 Trillion in mortgages!

“I will tell you as a safety-and-soundness regulator, when I look at a $3 trillion institution that is leveraged 1,000 to 1, it keeps me up at night,” Federal Housing Finance Agency Director Mark Calabria, the companies’ regulator, told the committee.

zh

Leverage doesn’t matter because the GSEs have the explicit backing of the US government. They’re under US government conservatorship. As long as that relationship is in place, they’re as good as the US government.

Why can’t slobs like me get those interest rates if we put dough on short term IOER with the FED? After all, I busted my butt with very expensive machine tools to save my pittance, while the banksters’ dough is nearly all notional.

Winston, that GSE stuff was all examined for value by Linda Green. Why would the FED buy up multiply defaulted loans on the same houses (up to 33 times) if it wasn’t good as gold.

Repos do pay interest and in the New York Fed’s auctions the highest rate bids are the ones accepted, regardless of the type of collateral. On Friday the weighted average rates on the accepted offers of Treasuries was 1.823%, on agencies – 1.860% and on MBS – 1.866%, the highest rate bids were 1.85%, 1.86% and 1.90% and the lowest – 1.80%, 1.80% and 1.81%. On the $75 billion lent on Friday the Fed (and the American people, since net Fed earnings are paid to the U.S. Treasury) will earn more than $11.45 million in interest when it is repaid on Monday morning.

For accounting purposes repos are loans fully secured by collateral, but legally they are safer than that. Because the securities are technically sold and then repurchased at the opening of business on the maturity date (which for the $75 billion is the next business day) should the borrower go bankrupt during the term the lender already owns the collateral and it is not subject to the bankruptcy. The way the interest is paid is that the repurchase price is higher than the selling price.

Is there anything to stop a bank dumping junk on the FED and not repurchasing it?

Mike,

Yes. Very simple. The Fed doesn’t take junk. Collateral has to be Treasuries, Agency securities, or GSE-issued MBAs. The US government stands behind all of them.

If bidders don’t have the right collateral, they don’t get the money.

Mike, they already did it. FED bought so much defaulted garbage just to bail their pals that they are bound up in their intestines with scheiss that cannot pass.

The FED needs a colonoscopy to find out what’s up from the exit hole. Too bad, they don’t allow an audit on the performance of their fiber ball and barbed wire that is in the taxcow dark.

Something i don t understand is the “maturity date” in the table https://www.newyorkfed.org/markets/opolicy/operating_policy_190920 Do that means the FED loan some money for more than the night operation ? I thought all these operation were for one night to the next morning so this “maturity date” confuse me.

charles,

The table you refer to is a little confusing. On the table, there are three maturity dates listed. All three of them are for the three 14-day repos of $30 billion each. These maturity dates are 14 days out from the data of planned 14-day repo operation.

What I don’t understand, and what I haven’t seen anything definitive on, is why things suddenly went out of control and why the repos solve the problem. I think I understand that the four big banks in NY have dramatically reduced their short term lending. But it isn’t clear why. So I guess the repos just give them the Fed’s money to lend, so they don’t have to use their own? What changed over the weekend that made them all simultaneously reduce their lending?

No. Most likely it is the weak banks that enter into repo loans with the Fed. See below.

Old Engineer,

There were some well-understood factors taking place at the same time, some of which sucked cash out of the money market (such as corporate quarterly tax payments) and others needed funding (such as large amounts of Treasury securities that were issued and buyers needed funding for them).

There was no surprise in these factors. The surprise was the market’s reaction — there was sort of a panic. Powell admitted that at the press conference too: everyone expected these factors, no one — not the market and not the Fed — expected the market to panic.

“….such as large amounts of Treasury securities that were issued and buyers needed funding for them….”

So the Fed had to step in and buy Treasuries….as if here in the short term, the Fed is taking down the new federal debt. This can be added to their balance sheet (federal debt portfolio)..

So, the Federal Deficit grows and the Fed is taking the overage.

Also, let us not forget that the arbitrage between ECB ZIRP NIRP rates and US rates requires the obtaining of dollars. One can guess that the dollar shortage maybe a direct result of this arbitrage…the ECB fake rates.

Doesn’t the high overnight rates eliminate the arbitrage between ECB negative rates and US rates

Similar to 2008 – banks with excess liquidity don’t want to lend to banks who don’t. Either they are worried about other party’s ability to pay back, or wanted to lend out cash at market rates.

Fed once again is undertaking a major misstep – by lending out at target rate. If it lets repo market decide the rates, borrower banks would raise cash by selling off assets, closing trades etc. It will be short term pain but equilibrium will return soon.

But because now Fed is lending at cheap rates, short on cash banks can continue whatever behavior ended up making them short on cash.

P.S.: I don’t buy the ‘lack of cash’ narrative.

There isn’t enough collateral in the world to force liquid banks/dealers to loan overnight to those who holding metaphorical FORD 2046 trash and derivatives on said trash…

`curl ‘https://nga.finra.org/bondfacts/api/bond/345370CS7’ | python -m json.tool`

GP,

“I don’t buy the ‘lack of cash’ narrative.”

Me neither. There was lots of cash, but it wasn’t there at 2.1%. It came out of the woodwork at 3% and then at 4% and then at 5% and finally at 10%. All these deals got done at high interest rates, so there was cash and liquidity. So the market was able but not willing at 2.1%. We don’t know why. This is the hallmark of a market not functioning rationally. This happens quite a bit, in different directions, flash crashes and the like. And someone makes a TON OF MONEY during these events.

I think it is wework. Everything is about wework and uber recently, they are breaking the unicorn fairy tales. Imagine you lend one of the unicorns 1B$ over night and next day unicorn died. Or you know some banks lend unicorn that money and the lending banks is trying to fund those in the repo market. Time to hold back. Let FED lend to unicorns, day after day, week after week, year after year, to keep them alive. Not me.

PS: I know nothing about repo market other than they are treasury pawn shops. I just want to dump more dirty water on a wework and uber. It is these MFers who hired so many people to jack up house prices.

Wolf said: “This is the hallmark of a market not functioning rationally.” But…could it just possibly be that the anti market Fed interest rate suppression rate 1.75% is THE Hallmark of irrationally, not the market rates the Fed is suppressing? Why isn’t the Fed suppressing credit card rates? Why should the Fed suppress overnight rates that are used by ultra extremely super wealthy & sophisticated actors and not give a f**k about everyone else?

Wolf,

I understand the usefulness of the fed stepping in to establish a cap when irrational loans are being made. At what point does having a “standing repo facility”, capping the rate, diverge from the natural rate and how will the feds know?

Also, is it possible to see who made the loans at 10% as well as who stood on the sidelines? If there was enough liquidity, then perhaps there were not enough lenders in the market?

Scot,

“Also, is it possible to see who made the loans at 10% as well as who stood on the sidelines?”

I’d love to know that too. The NY Fed is now investigating these very issues.

That was market working perfectly rationally. Supply vs demand determines the price. In this case cash was in short supply and did command a higher interest. 10% is perfectly reasonable.

Banks aren’t obligated to lend at Fed target rate. They are only required to keep the reserve.

As Petunia said/speculated, a big bank got in trouble – Fed stepped in to rescue it by artificially suppressing interest rates. That’s irrational and thuggery.

If free markets seek their own level, the Fed should realize that perhaps rates are TOO LOW.

Why we must cut rates to be in line with the ECB and it rescue operation to save failed socialist nations who overpromised benefits and pensions is beyond me.

Maybe the US is where all the money is flowing because we are doing it right?

Or is this just a giant exercise in globalization?

Also, the “Fed” has reportedly not entered the repo market in this substantial way since it entered it with $800 billion during the 2008 crisis. Moreover, Goldman sucks is saying that there may be something going on with the market in October.

The Chinese communists have propped up state owned and communist cadre owned companies, so many now have become effectively insolvent (absent continuing subsidies) and have debt levels that are not sustainable; major US banks and many US corporations are in similar positions.

Even major companies that have not received direct US government subsidies have effectively been subsidized by the unreasonably, ultra low interest rates. Those rates enabled excessive, stock repurchases, stock dividends, and over use of leverage, while these companies were not investing in R&D or major asset purchases in the US. They have slowly grown weaker due to these low interest rates.

Now, a recession may come due to a very understandable fear of what will happen when the inevitable recession occurs: fear of recession may reduce purchases, reduce consumer spending, etc., and bring it about. The recent, Fed actions in the repo market (and spikes in repo rates) indicate that too many people who are lenders in that market are worried about future, much higher interest rates and recouping the funds which they lend out.

Hence, the spikes in repo rates are like tremors that may indicate a coming major earthquake. I would wish that this was not true, if I did not fear more where the re-election of a certain orange fuhrer may lead our country.

Why can’t the banks use their excess “funds” to fall back upon instead of this rejuvenated scam?

“Operating in a region of ample reserves” is Fedspeak for “We have been monetizing a boatload (yes, 3.X Trillion) of UST bonds such that even the weakest bank will end up with at least a minimum reserve balance.”

It does not mean that ALL Fed member banks have “ample reserves”. Some of them do. But some other banks are hovering near the bare minimum. And that’s how you get RESERVE SHORTGAGE and RESERVE CRISES, which is what is really going on. Not “dollar funding shortage”, not “liqudity crunch”, but a RESERVE SHORTAGE at certain banks.

The numerical value of the reserve balance of each of the Fed member banks is one of the most closely guarded secrets in the universe. If the numbers became known, all hell would break lose (with the weak banks in particular). That;s why the Fed NEVER talks about individual bank reserve balances. Only the aggregate number.

Just in case anyone wants to quibble, instead of UST I should have written UST + GA + GSE.

I am not about to quibble. At least in 2006/2007 you had some superb sites to check at least the “Texas Ratios” of banks. Several others had good coverage of the rotting RE markets.

I went to my bank that I knew was in trouble and made an ass of myself trying to calmly explain to my favorite lowlife tellers why they should dump the bank stock that their impending retirements overly relied upon. My annoyance to them was when their retirement nut was at 63.00/60.00 It dropped to 3.00 within months. The FED bailed them out for a few billion but they never recovered and were sold to BMO.

Needless to say I used the good info on the net that is much harder now to come by to switch to a very local bank that had some iffy debt, but not much.

Bad banks need to go bust. The problem is that the banking laws and rules do not allow any decent insight into their financial condition.

DYODD.

Erle – I hear you.

Oddly, if you actually read the Bank’s Annual Report, especially the footnotes, you may see some very interesting stuff.

There was a bank in Northern California who put in their annual report the fact that more than half of their loans were to an “affiliated” Construction/Development company. (More accurately, to a thicket of corporations with names like “1234 Main St., Inc.”)

One day, the FBI raided the place. The people waiting for the front door to open at 9:00 pulled guns and started shouting “Drop the mouse!” and “Step away from the computer!”

It was really, really funny.

Thank you for that last paragraph. Finance is a confusing mess to me, money shooting all over under many names, disguises, features, etc. This article was simply beyond my grasp, even though I just looked up money market and repo, and tried to grasp how they fit in with the other moving financial pieces. Other articles here are not, no complaints, I’m here to learn.

So, “bad financial engineering”, then seems to me similar to bad automotive engineering where the design of, say an A-arm, is cut too close and they eventually begin to fail and kill people. But before that occurs, the cars have to be on the road a while, maybe several years, and weaken enough. By that time, the profits have all been pocketed, the bonuses given out, and the shareholders rewarded. A few profiting at other’s expense.

The “laws of our land” evidently allow the “killing of people” economically, which is seen clearly in ever growing income and net wealth inequality.

Dead people from car accidents are obvious to the public, as are bank runs. Swifter consequences for excessive greed.

Taking chances and profiting on other people’s misfortune are very well rewarded “professions”, in both cases.

Banking is just one example of many, no wonder that for the first 20-30 years of our country Corporations were strictly regulated and abolished when a job requiring the formation of one was done.

The “borers” (now called lobbyists) “enthroned the corporations”.

Not my words, Abe Lincoln’s.

”Finance is a confusing mess to me, money shooting all over under many names, disguises, features, etc. This article was simply beyond my grasp, even though I just looked up money market and repo, and tried to grasp how they fit in with the other moving financial pieces. “. You are in good company. There are a few presidential candidates in the same boat.

And a sitting President, conspicuously absent from your post.

My definition of money:

Money is a token of value in a recognized accounting system which tracks the exchange of promises for goods and services.

The token, of course, must not be easily counterfeited.

Our problem, of course, is that there is no token, i.e., no thing existing in space and time to represent the promise. Even the cash and trinket coins can be manufactured at will by the privileged institution.

The recognized accounting system we have is just imaginary accounting (no thing), with nothing to prove its honesty and accuracy.

It would be OK if this this imaginary accounting system was honest and accurate in it’s tracking of the promises, but we all know it is not, and that is the problem. Imaginary accounting with no thing to prove it always lends itself to fraud.

If you cannot follow the meaning of what the Fed is doing it is because it was designed that way. It is fraudulent accounting.

Think of Enron. One day it was worth $70 billion. Two weeks later it was worthless.

Nothing burned down. They did not suddenly make bad investments. What happened during those two weeks is that it was recognized that the accounting was fraudulent.

Does this remind you of a financial crises?

Money, obstensibly, as a token of echange, implies that there is no store of value in money. I agree with this notion.

Electronic money has only transactional value. That transactional value is huge. It represents the force with which people are compelled to transact in a certain currency. This power to compell you to transact is at the root of all currency machinations by governments.

When you consider money like game credits in an arcade machine it all starts to make sense.

Somebody’s talking because just yesterday, I heard on the news, the 4 largest banks make up 75% of excess reserves and IOER is 20% of their profits. The big 4 are usually considered to be JPM, WF, BOA, and Citi.

The cash crunch didn’t come from them, but it came from some bank big enough to pick up the phone, ask the fed for money, and big enough to get it too.

Petunia:

So, the “bazooka” is still being wielded in the “background”!

@Petunia, whoa, that’s very significant info. I did a web search and cannot find anything that mentions these numbers. What is your best attempt at a reference for the info (the name and time of the tv or radio program if nothing else)?

This also inspired me to search in the annual reports of JPM (and BAC). I could find no breakout of reserves in their balance sheet. The only inkling of reserves was “cash reserves” (greenback dollars) of 22B, but that is just a pittance relative to the 1181B loan portfolio and 2623B total assets, so clearly it does not include all reserves,

Could one possibly back-calculate/estimate reserves and/or excess reserves from IOR and IEOR? Sure, but of course JPM (and most likely no other bank) will break out IOR nor IEOR from the big interest income bucket item in the income statement. Why? Exactly because people would then be able to estimate R and ER since IO(E)R are published by the Fed.

It all goes back to what I said before: The numerical value of the individual reserve balance of each of the Fed member banks is one of the most closely guarded secrets in the universe.

So how did the aforementioned estimates leak? Fed employees are the only ones that should really know these numbers.

TYPO CORRECTION: will break out IOR nor IEOR …..

SHOULD BE: will NOT reak out IOR nor IEOR .

I heard Danielle DiMartino Booth discuss the 75% number in a utube video done 2 days ago. I don’t remember if I heard the 20% number there as well. Video is 1:16:24 look at about 1:10+.

Most of us understand that money as manifested in our currencies isn’t worth what it ‘claims’ to be worth if we look further ahead at e.g. pension scheme promises.

These extended repo operations seem to indicate that it maybe isn’t worth what it claims to be worth even in the very short run, and I suspect that is the near term worrying aspect in the need for their implementation.

I guess it’ll be something that blows over again, but it’s possibly at least a warning sign that the time of realisation is getting nearer.

Pure and simple to explain this hogwash;

The trickster also going by the name ( the Fed) is running out of gimmicks, Not many bunnies left in the old ?!!!

Note : the funniest thing I read here was a comment under another article that goes this way

“The Dow @ 30k by end of next year”!

Well I tell you sunny: you don’t know what’s coming your way.

Cheers

I think the Dow will get to 30K soon. I think Gold will get to $2000 as well.

Cheers.

“These are overnight interest-bearing loans that unwind the next morning, with the Fed getting its $75 billion in cash back, and the dealers getting their collateral back.”

Admittedly I am a bit of a novice on Repo, but as I understood it a key part of Repo was that the dealer could freely decide not to pay the money back leaving the collateral behind and to make this palatable the collateral was priced in a way that the repo originator (in this case the Fed) was fine if there was no repurchasing.

Obviously in a healthy repo market almost all the collateral should be repurchased the next day… but not necessarily all of it (what is a few billion here and there?) Moreover given the sudden state of this liquidity issue is the repo market currently all that healthy? Is there any way we can see how much of this repo is actually repo and how much is actually effectively a secret emergency QE running under the cover of repo with no repurchasing?

>> but as I understood it a key part of Repo was that the dealer could freely decide not to pay the money back leaving the collateral behind

Not true. If a bank did that it would be in default. And Fed would promptly deny them any further repo. Not a good thing. That bank would go under quickly, with some other bank buying it for cheap with taxpayer susidy from FDIC.

And think about it, if banks could just dump UST+GA+GSE bonds at FRB then the banks would in effect be running QE in any amount they wished.

Can you imagine having banks deciding for themselves day-by-day how much QE there should be? They would kill the value of the USD in one big race to the bottom. The Fed has to be the semi-adult in the room that controls these things.

Even scarier: Imagine Italian banks entering into repos with ECB, using Italian Gov Bonds as collateral, and then defaulting at will. That would go bad very quickly.

>> “Not true. If a bank did that it would be in default. And Fed would promptly deny them any further repo.”

I thought that is why repos are often over-collateralized, so that the reverse-repoer isn’t bothered by a default, and thus why repo-defaults aren’t considered even worth mentioning.

>> “And think about it, if banks could just dump UST+GA+GSE bonds at FRB then the banks would in effect be running QE in any amount they wished.”

Exactly, though not any amount, their is a daily cap set by the Fed that is decreasing. But yes, that is what the thrust of my post was about. I was wondering if this is free secret QE to the tune of however much banks want up to the Fed repo-cap each day, but it is well disguised as a totally legitimate short term loan process. An interesting question: this all started when the banks with excess reserves at the FED decided not to lend for Repo even though they would be getting a better return on investment by participating on repo then leaving money in the excess resevers at the Fed. The Fed cut made this even more true – try to force the banks to lend very much including things like repo but even the rate cut wasn’t enough to force repo to get as many money-lenders despite their massive excess reserves.

The only two explanations that come to mind are: 1. said banks are afraid of repo defaults and thus don’t want to be bag-holding tens of billions in treasuries even if over-collateralized, 2. these banks are just mysteriously afraid of making more money. Now I know option 2 can’t be right, but I do allow there might be other possibilities to option 1 … but what are they? Please do tell.

>> Can you imagine having banks deciding for themselves day-by-day how much QE there should be?

Well the repo is capped at 75B for now and decreasing going forward, so they can only decide up to the cap really.

>> They would kill the value of the USD in one big race to the bottom.

Not at all – they generally consider treasuries at or approaching the status of “cash equivalent” and they could freely sell them on the open market if they were truly cash strapped and the Fed wasn’t offering an out. Such a sudden liquidation would do way more damage then secret QE that has a daily cap. By your logic cash-strapped banks can just destroy the USD at any moment on the open market – secret QE that is done via over-collaterilized repo would be so much less damaging to US debt market and USD then letting a bank liquidation run of US treasuries occur on the open market by frenzied cash starved banks.

If the repo is over collateralized then they are making less money then they could be just selling the the treasuries on the open market, which they are free to do at absolutely any time. If this hypothesis is true (and I fully accept it might not be) this would be like a secret QE bailout that prevents both a liquidity crisis and a US treasury snap back from a mass treasury liquidation that would blow-up the financial world. Sounds like a really good and useful idea to prevent a two-prong disaster – i.e. it would be *EXACTLY* what the Fed would do to be the adult in the room under such conditions.

>> The Fed has to be the semi-adult in the room that controls these things.

Which would be what the Fed would be doing in this hypothetical situation, preventing a financial crisis.

>> Imagine Italian banks entering into repos with ECB, using Italian Gov Bonds as collateral, and then defaulting at will.

But they can’t and it isn’t part of what I am discussing here, that is a digression.

these banks are just mysteriously afraid of making more money…

I think the problem is a shortage of eurodollar funding (overseas loans in USD), and that some banks prefer to loan at IOER (interest rate on excess reserves) which is the lower rate provided. You rarely if ever see banks passing on opportunity to do a free arbitrage… So what is scaring them?

Generally, I agree with your thinking. If I was a suspicious person, I would be looking for an entity with a large foreign exposure in Asia, as my first choice.

@Nat

>> 1. said banks are afraid of repo defaults and thus don’t want to be bag-holding tens of billions in treasuries even if over-collateralized,

I think 1. is the correct answer. The banks who (today) have excess reserves are afraid they might need them soon(*), and hence do not want to use their reserve for a big repo (which may end up as a permanent purchase :)) of UST+GA+GSE from some other bank. The formerly reserve-rich bank would then be the one having to go begging to the Fed at another repo auction.

(*)probably because these banks are concerned about impending defaults and losses on corporate debt, but that is just my guess as to the most likely culprit. Jerome Powell did state that corporate debt was one of his biggest concerns in the Weds press conference.

@nat – i agree. no one wants to be stuck with agency or mbs in the event of a liquidity crisis. inmho, the ioer should be zero. i’m tired all of this.banker welfare.

Here you go:

“An central development in the 1980s that spurred the growth of repo was that repos received an exemption from automatic stay in bankruptcy (Garbade (2006)). This exemption allows the cash lender in a repo to sell the collateral immediately in the event of default by the borrower without having to await the outcome of lengthy bankruptcy proceedings, thereby reducing the counterparty risk exposure of the cash lender.”

From: Garbade, Kenneth D., 2006, The Evolution of Repo Contracting Conventions in the 1980s, FRBNY Policy Review, 27–42. May.

Repos are popular in part because their defaults don’t have to have any significant consequences (depending on the particular agreement). Its why they aren’t called “overnight loans” or “extremely short term loans” they are “a repurchasing agreement” – this keeps the whole bankrupcy court and similar complexities and repercussions out of the situation. If you have the liquidity to mop up a large amount of securities (like say the Fed), you can just sign up to be a reverse-repo party and take whatever you are given and just shrug at those who don’t pay you back. Even a private bank with no ability to print its own money can profit on that: set the over-callateral hair-cut to 5% or more (i.e. lend only $950 for every $1000 worth of treasury collateral – this is a pretty standard %), and if the counter party never pays you back for the (not-a-)-loan you still made 5% overnight in highly liquid assets – no need to be concerned, no need for anyone to go through bankrupcy proceedings, and no need to even “ding” the counterparty’s creditability – just shrug and move on with your overnight 5% profit.

The info about the finer contractual points of repo is good stuff. These contractual clauses exist to avoid a contagious cascade of defaults when one counterparty goes bad, obviously. It is worth mentioning that the *proceeds* that bad bank C got from a repo that it subsequently defaulted on, are not exempt from bankruptcy law :).

As for common haircut (A.K.A. “discount” ) size, I could not find any recent numbers, but I saw some 2009 number such as 1% for UST and 2% for GA+GSE and as low as 0% in 2007 before the great financial crisis. Haircut sizes may vary considerably, I think.

There is a measure of failed payments in these REPO agreements. collateral pledged that is never delivered, or delivered late. When that number gets a bit high that’s another symptom the system is broken.

Nat, good questions.

I have some questions too. What if the collateral offered to the FED has a wad of undisclosed derivatives associated with the collateral. How in heck can the FED do a chain of command on this paper to take it for overnight collateral? Two or three days of Lehman fouling out revealed a little bit of what the Deplorables were to pony up to save their sorry asses.

We taxcows found out that the junk offered for collateral the last time had vast amounts of derivatives written against the trash so the boyz put taxcows on the hook to bail the counterparties like Goldman Sachs.

It is part of a pattern. Some 2000 years ago, Cicero observed that if there was a liquidity problem in the eastern provinces, it would eventually hit Rome. The financial capital.

Earlier in the year, Argentina and Turkey discovered their money markets had run out of liquidity. Their central banks soon followed and money market rates soared.

Then it hit the big outlying markets–India and China. I was following the latter as their currency weakened, thinking it was policy stuff. Then in early August realized it was the next credit crisis moving through outlying exchanges.

Now it is hitting New York.

And this is just the first hint of trouble in what was considered a risk-free world.

“Risk free world” ha that’s something to give me a good laugh this morning Thanks I needed it

d

So a repo is basically exchanging treasury securities for cash. The question that comes to mind is that the parties (banks) were unwilling to do this among themselves because they don’t trust each other’s collateral, unless the transaction took place at 10% interest rate. What do they know about each other’s collateral?

The obvious risk in exchanging cash for collateral would be that the collateral would be worth less in the future and the other party nigh not buy it back. Now if bonds have a negative interest rate, wouldn’t this be the default case? No one would like to hold a security that is worth less the next day. How do they do it in Europe or Japan?

This is not as innocent as Wolf shows. It’s an admission that banks can’t manage their balance sheets and keep running to the Fed to plug their holes and this money should come with a penalty rate from the Fed.

Why doesn’t the Fed require that they sell some of those assets on the free market so they can get the cash they need? Savers would love a treasury bond with 10% coupon.

I personally think some big guy is about to go bankrupt somewhere, we will see.

>> “The question that comes to mind is that the parties (banks) were unwilling to do this among themselves because they don’t trust each other’s collateral, unless the transaction took place at 10% interest rate. What do they know about each other’s collateral?”

That is what I am wondering too, *BUT* its not necessarily that they don’t trust the other banks collateral, the other option is that they could be worried about mass defaults and end up with way more assets to liquidity then they are comfortable with. So either 1. they think the collateral is junk, or 2. they worry too much of the liquidity they would loan out, just won’t come back even if the collateral is fine. (… or 3, both: they are worried about the collateral and a high risk of being left to bag-hold it).

Good stuff, Nat. Thanks.

All it says is that THEY prefer cash now over promise of cash in the future. We should do the same.

Momento That was my first thought DB comes to mind but that may be too obvious

Repos are the essence of the monetizing scheme, (and the state of government spending is the issue at the moment). Treasury issues bonds, the Fed accepts them as intermediary, and passes them on to the Primary Dealers, who are supposed to find buyers, but who can also access this REPO market and turn those borrowed bonds into cash, and provide the Treasury with collateral. Bob Prechter calls it a “check kiting” scheme.

“No one would like to hold a security that is worth less the next day.”

They would if it’s better than the alternative. I’m not suggesting anything more than the face value of that statement, mind you, that a small, known loss is better than a large loss. For some reason we’re all convinced that profit is the natural state of things. Do repos say anything about that?

Re: “By paying banks interest on the Excess Reserves (IOER) at a rate equal to the upper limit of its target range, the Fed figured that banks would see to it that the federal funds rate would be less than the IOER. This would keep the federal funds rate within the Fed’s target range. This worked until it didn’t.”

That stupidity is what has screwed the economy up more than anything! Who dreamed up the concept for taxpayers to loan banks money and then pay them to hold the loan, instead of them paying back taxpayers. The Fed gave banks a Yuge incentive to sit on reserves, making very easy money, which at some point became normal and predictable cash flow for banks that should have gone bankrupt long ago! Extending this pathetic charade is criminal and banks should pay back every penny of interest that they stole, and then they should be assessed massive fines and or pay massive interest back to me and my fellow Americans.

It is a lock for the banks…

they get the high end of the Fed Funds rate, and pay their savers half…if that.

The argument for paying IOER was partly backed by Friedman’s opinion that banks should get paid for reserves. I never saw Milton say “excess reserves”. Did he?

Also, don’t forget, the Fed pays banks 6% on their required stock ownership in the Fed. If only the people had this lock, instead of rates pegged below inflation…and a promoted inflation at that.

The only thing I’m wondering is which bank got caught with their pants down playing the oil market and now needs payday loans to cover their losses. If I was a betting man, I’d say JP Morgan chase.

Or did the arbitrage between ECB rates and US Treasuries sop up an incredible amount of liquidity in the dollar?

Centrally controlled interest rates are a centrally controlled market.

There are no free markets in the US, or the EU.

Stalin would be proud to own this system.

YES!

Central bankers are now central planners. Economic decision making by committee behind closed doors. This is a tenet of Socialism.

With $1.4 trillion in excess reserves, how can there be a problem with overnight funding?

Beneath the crisis is my observation that companies are using overnight repos, continually, to fund normal operations. Parties no longer trust the collateral.

It took a mid-month crisis to flush this out.

The Fed’s alleged solution is to give companies at least $30 billion “14-day” lending, repeated of course, indefinitely. This is on top of at least $75 billion daily.

Excess Leverage

I smell an excess leverage, borrow-short, lend-long scheme of some sort that has seriously gone awry.

https://moneymaven.io/mishtalk/economics/us-banks-have-1-4t-in-excess-reserves-yet-need-daily-emergency-fed-actions-PyTpv9xMuka3cHgLC7N2UQ/

Borrow in Europe, convert to dollars, buy US Treasuries.

The massive conversion to dollars may have strained the liquidity.

The ECBs attempt to save failed socialist endeavors in the EU is to blame. IMO

As an old bond trader ,who has seen so many panics ,this sounds like some kind of counter

party problem. Perhaps some major repercussions from the bond sell off ,some leveraged fund having margin calls,and setting off a daisy chain of counter party risk assessment.

At 10% repo rates someone should be all over loaning their excess reserves. But few takers.

Question:

Is the party seeking the funds identified?

Who turned down a chance to lend at 4,5,6,9%….?

Those who could must have decided the party involved too much risk.

Now, who might that be?

“At 10% repo rates someone should be all over loaning their excess reserves. But few takers.”

The Fed is wondering about that, too:

https://www.zerohedge.com/markets/clueless-new-york-fed-examining-why-banks-excess-cash-failed-halt-repo-panic

Slightly tongue-in-cheek but largely true:

If bad bank B agrees to pay good bank G 10% interest on a repo, then bankB must be in very serious trouble. So bankG had better not lend them anything ;). Even with a nice haircut. Heck, maybe BankG should just wait for bankB to become totally insolvent and then buy it for cheap (with taxpayer subsidy)? In which case bankG will need the reserves, so definitely don’t lend them out.

That’s how credit freezes occur.

Long Flux Capacitors!

The music is about to stop, and we are about to be left holding the largest more odoriferous bag in the history of capitalism…

So, how much leverage is dead?

The biggest failure of 2008 was to not kill so much leverage, but instead to save the gamblers and allow more leverage into the system.

And yet, how will the rest of the system outside of the control of the US deal with deleveraging?

The Chinese are the biggest wildcard as the paper pyramids go up in flames. How can they deal with the political fallout of allowing capitalist morons to fall into the abyss?

LoL- what happens when housing prices begin to fall in Hong Kong?

Think the unthinkable, and watch it happen…. how much leverage is beyond our shores, and only held up by paper promises?

Someday this war’s gonna end…

I’m certain housing prices in Hong Kong are already dropping At least the high end

This twitter thread below was popular lately in explaining some of this weeks FedSpeak, there are about 20 posts that are fairly succinct and educational. The following is one of the main points:

17h17 hours ago

The problem is,by making a requirement based on intraday liquidity “resolution liquidity adequacy” is discouraging gross flows. The big banks are now incentivized to hoard liquidity.14/N

https://twitter.com/NathanTankus/status/1174992669040422912

The People’s Fed would do this:

“The two key – but “distinct” – motivations for a standing repo facility are, as cited in the follow-up paper:

First, the facility could be used to support interest rate control on credit cards and student loans used by working folks and students by establishing a ceiling on interest rates, thereby guarding against unwanted spikes in credit card rates and student defaults, with to terminate credit card rates that are running 24% and more. The Fed will buy credit card debt until credit card interest rate stabilizes at the target rate of 1.75%.”

Ain’t it great we have a Fed that acts as a credit card at massively subsidized rates for the Ultra Rich and Rich Gigantic Corporations?

The only way it makes sense for the banks to me is if they can prepare for the cash/asset trade in advance by setting up short term loans at a lower rate than presently available, but higher than the repo rate. It seems like it would take a while to make it pay off. It would be a colluded corodination of known frequent borrowers and lenders taking advantage of the lower rates,therby creating more liquidity movement.

Come on you guys. We all know the financial sector is the source of all wealth and so must be propped up at all costs. Indeed, if it weren’t for the banks from where would we get our money. I mean we could hardly issue it ourselves, could we. That’d never work, would it.

The parasites are getting long in the tooth People are sharpening up their garden implements as we speak I’m sure Long Gold and pitchforks here

Very nice explanation of how repo works. Plain and simple and easy to follow.

“And these operations have nothing to do with QE”:

If repo is sustained, then it does represent an extension of the FED balance sheet, as is the case for QE. The real question is why is this suddenly happening and the answer to this question would shed light on whether this repo operation will have to be sustained and expanded, which if true would be the first step to officially re-introducing QE. As long as the stock market is near or at ATH, the FED can hardly call it QE, so they call it repo. If the true cause for this repo action is the federal deficit, the legal requirement that PDs buy all the issued USTs, the pancaked (and inverted) yield curve that prevents profitable carry trades, and the high FX hedge cost that prevents foreign CBs to buy UST, then the only resolution will be lower rates, much lower rates. A sustained and increasing repo action is another leading indicator for lower rates. Maybe another risk-off episode would temporarily alleviate the repo issue by soaking up excess UST, but that would’t make things any better overall.

The 9-11 attack on the World Trade Center towers and Pentagon produced panic and a spike in repo. This recent spike came after an attack on oil infrastructure in Saudi Arabia.

Last year Robert Shiller, Nobel Prize winning economist, stated the US is in its third worse housing bubble since 1890.

As a practical matter in case of this being an indication of a real emergency in the US Banking system, the best place to hold cash instead of in bank would be?

–other currencies? Euros, AUD,CAD?

–Treasuries?

–Mattress?

–PM’s?

Australia is on the verge of passing a bill to ban cash, so don’t go there, Canada will probably follow in short order.

Good luck with that one Petunia, bartering is almost back now.

Never use a mattress! House could go up in flames. Buy yourself a home safe. Then, cover it with a cardboard box and mark the box, Extra Kitty Litter.

one can only hold cash in cash, by defenition.

1) HSBC, a bridge head to the world, to freedom.

2) China richest are selling HK RE, and moving out.

3) HK & Brexit, a spicy salad, mixed by HSBC chefs.

4) HK highest RE/ GDP, Consumer debt/ GDP and Gov debt/ GDP

ratio in the world.

5) HKD is still pig peg to the USD, but dollar reserves are gone.

6) Oct 1st within ten days. Brexit next.

7) HKD will jump to Xi bed. China will absorb HK, but China

will absorb HK debt, adding dollar debt, a bone in their throat..

What is the point of these overnight loans? I mean, if a bank needs to hold more reserves then presumably it hasn’t enough (according to the rules?), right? But next morning when it gives back the reserves, in exchange for the collateral, it’s going to have even less reserves (as it has had to pay interest) and it’s back to the state it was in the previous night – it hasn’t enough reserves!

As an aside, do the guys that carry out these operations sit on tall stools behind tall desks and record it all using quill pens?

medial axis,

Normally, these overnight loans and ultra-short-term loans are the cheapest form of borrowing. If you have access to this market (the money market), you can borrow essentially at a rate that is within the Fed’s target range.

If everything works, you should be able to borrow at 1.9% currently, and you should be able to borrow billions of dollars at that rate, and you can buy long-term assets with this money and roll over the debt every day, which is great until it isn’t — which is why GE almost went bankrupt in 2008-9 because it suddenly couldn’t borrow overnight anymore as the money market froze up, but it was relying on this form of debt to fund its operations and make payroll.

Very informative Mr. Richter. It would seem that the abnormal fluctuations that occurred may have been the market trying to price in actual risk. Is it possible that we may have actually seen a little bit price discovery going on? If I remember correctly no one, not even JP Morgan, wanted anything to do with Lehman’s commercial paper so the Fed had to directly intervene. There should always be market liquidity at the right price and the right coverage when there is real price discovery. When there isn’t, well the Fed intervenes.

The point of the overnight repo used to be to bring a bank back to its required reserves before the fed closes for the day. In the old days the fed didn’t like lending to any bank and encouraged them to support each other. It was a good business for banks with excess reserves to lend to those short of cash.

The math was only done once a day at the close, and the traders who did these deals would usually start looking for cash about the time the banks closed for the day. At that point the banks still had a few hours of fed time to settle up. The next day was a clean slate.

Now with IOER the overnight lending business is gone. The fed is the only lender.

Petunia:

Simplicity…..perfect. I thought I might have been the only one that thought as you have written.

Somehow the system of “overnight” repo lending which was so simple has been twisted into some kind of monster?

And, WR asks the question: “Why did WS panic?”

That is the question and we have multiple answers but no definitive ones.

If WS is so sensitive then it’s like a tooth with nerve damage: It needs a good root canal!

To sum it up, too much debt issuance. We are one wafer thin mint away …

You guys are reading way too much into this. Clearly this was a case of bidding wars in socaljim’s neighborhood sucking liquidity out of financial institutions.

People had to withdraw a lot of cash after deals closed @ %20 over asking price.

Too much talk about trees. Not enough discussion of the forrest. The fact is one week after Mark Carney ANNOUNCED a coup against the US dollar interest rates soared. The only play the US has is higher rates.

This repo thing is above my ranks to comprehend but it occurring recently may portend liquidity issues to arise and canary in the coal mine.

I think there is a simpler explanation for the sudden reappearance of Repo by the feds. The 10 year treasury moved 50 pips over night. This reduced the collateral value of the bank to bank repos. Banks did not want to hold additional treasuries while prices plummeted. The Fed to the rescue

Yeah, and in fact over 5 days this week, UST10 yield dropped 15bips (0.15%, 150pips).

Which means (a) Someone was selling a lot of UST10, including perhaps ad bbanks that needed net more reserves. (b) As GSH said, those good banks that held UST as repo collateral started to get nervous that collateral value was dropping, and quite possibly decided not to lend anymore on repos. (c) Two mutually amplifying factors driving up interest rates.

Interesting comment NARmageddon.

Does anyone know who takes the loss or gain from the collateral?

Let’s say that BigBanc dumps several billion in trashuries to the FED and the interest rates spike higher in the overnight. Does BigBanc have to pay back what they borrowed or just pay for the newly depreciated collateral?

Wolf, I listened to your podcast over on PP with Chris Martenson, and I’m trying to digest everything I’ve been reading and listening to regarding repo markets. Here’s what I’ve got, and I’d love to hear any tweaks to my understanding from you or your readers. I teach a high school Econ course, and a few of my brighter students are asking wtf is going on. I need to lock down my understanding before I teach it to them:

1) Repo markets are the places where banks can borrow money on a very short-term basis from one another in order to cover regulatory requirements, etc.

2) The interest rates in Repo markets usually hover around the Fed Funds Rate, and the Fed hasn’t had to commence Open Market Operations in repo markets – a tool it utilized all the time prior to the Great Recession – since 2008/9 because the combination of QE, low interest rates, and the use of the Interest on Excess Reserves function have served to keep credit markets stable and interest rates where the Fed wanted them.

3) For some reason that isn’t clear, the IOER system broke down, and supply-demand dynamics in the Repo market caused some holders of dollars to NOT lend out at interest rates near the Federal Funds target area, but rather, at much higher rates. I’ve seen much speculation on Twitter as to why that is, but no one seems certain.

4) The Fed stepped in to stabilize the repo market, but needed to do so in increasing amounts and has now declared it will do so until October 10th, and beyond.

Assuming im getting all this correctly, it feels like there’s something big moving underneath that we aren’t seeing, and that something somewhere might have broken, but we won’t know for a bit who, where, or how much. What I have heard in unison out in the Twitter Space is that if the Fed’s efforts fail to keep repo rates where the Fed Funds target area is, and rates go higher, shit starts going very south very quickly.

My gut doesn’t like this, though. That much I’m certain of. It feels bigger than the MSM or Fed is letting on.

Bebe Robozo said it above. Too much talk about the trees and not enough about the forrest. Forget teaching the trivial details of how the fed works since it is deliberately designed to be deceptive.

Teach them the history of banking and the illegal creation of the Federal Reserve to embezzle wealth from the people and fund the wars.

Of course you will probably not be allowed to do this if you work at a government run school.

Oh, I do. I teach them what fiat is, the history of US currency (Breton Woods, Nixon’s taking us off the gold standard, etc. I’m trying to teach them to think and see economics as it is.

Ditto your questions, Snydeman, and those of “brighter students” in your Econ class.

I hope you’ll give us an update, sometime soon, what you and they are thinking.

In the meantime, I think it’s safe to advise them that keeping their silver coinage under their mattresses always works nicely.

Thanks, I will. I had a devil of a time teaching them the textbook answers on how to save for retirement, because the brighter ones said “but aren’t IRAs below the inflation rate? That would be stupid!”

These are not invalid conclusions…

Snydeman,

First let me tell you that I think you’re doing an awesome job trying to cover this topic in class. I wish I’d had teachers like that!!!

Your students need to understand that everyone is still trying to figure out WHY this happened. There are all kinds of speculations out there, including my own that you heard on the podcast at Peak Prosperity with Chris. But the actual documented reasons — who did what, or more importantly who didn’t do what, and why, and who profited from it — haven’t been revealed yet.

So I’ll give your questions a quick shot, in the order of your list:

1. Yes and no. The banks can borrow in this market, but they normally LEND to this market (except when they don’t, which is what happened over the past week).

2. Yes.

3. Yes. Note that your “holders of dollars” are the banks that did not lend near the normal rate, but only lent at much higher rates. They ultimately did lend. But why did they wait till rates hit 4%, 5%, or even 10%? Still, lots of speculation as to WHY, but no real and documented answers and names.

4. Yes and no:

– Yes, the Fed stepped in.

– No, the amounts have not increased. Its first repo operation was supposed to be $75 billion but got screwed up, and it ended up lending less. The remaining three were all at $75 billion. But remember, these are overnight loans, so they unwind the next day, and the Fed gets its money back. So it’s the same $75 billion that is circulating, and the amount has not increased so far.

– Yes, there is a chance that the amounts WILL increase in the future, as the Fed has taken off the $75-billion limit for operations starting on Tuesday and after. And it added the three 14-day repos, which would remain in the system for 14 days each, and this would increase for this 14-day period the overall amount.

– This assumes that there are takers for them. If the market calms down, those amounts would be heading toward zero.

– After Oct 10, it’s an open-ended standby facility, so if repo rates go out of whack, the Fed will use this facility to bring rates back in line. This could be done normally with very small amounts, until there some kind of problem, like we had, and the amount would jump for a few days until the repo market settles down.

Wolf,

Excellent, thank you! I’m going to put together a quick addendum to my lessons on monetary policy incorporating this info!

-S

IOER is Reverse Repo, and typically applies when you want to set rates higher. The process provides liquidity, like a payday loan. Markets (calm) see the transition (back) to Repo as being bumpy, but no real worry. 4) says they are ready to “do whatever it takes..” http://creditbubblebulletin.blogspot.com/2019/09/weekly-commentary-no-coincidences.html

When everything fails, start QE4! Just a matter of time

POMO ( Permanent Operational Mkt++) is nothing but QE – Lite!

This is going to get very interesting next week. National Guard troops being sent to Jordan as we speak.

What’s the chances of these overnight Term Repos will morph into Open Repos. If they do will they be additive,and how long after the fact will we learn of this ? Will the phrase Breaking the Buck be in our future ? Nah …… This fiat money system is working great.

“With its announcement this morning, the New York Fed confirmed that the Fed’s Plan A of manipulating the federal funds rate into its target range – now between 1.75% and 2.0% — has miserably failed”

After working extremely well for ten years and nine months. We really don’t know how well the old Plan A worked because prior to October 20, 2015, there is no accurate data on the effective federal funds rate. Prior to that date the Fed was only aware of fed funds transactions that were placed through brokers, a very small segment of the market. Since that date all U.S. banks and thrifts and all branches and agencies of foreign banks, except the very smallest, must report on fed funds borrowing, Eurodollar transactions and CD issuance on a daily basis.

The other part of the old plan A is that since the low end of the rate target was raised above zero on December 17, 2015, the New York Fed has been in the repo market every day offering to borrow through overnight reverse repos limited only by an overall limit the size of the uncommitted system open market account securities, originally about $2 trillion and still more than $1 trillion, and $30 billion per day in loans from any individual counterparty (there are more than 150 counterparties).

Fed is actually derisking the fixed income market by moving away from QE and back to standard REPO market operations and even POMO. Unfortunately Aleve is no substitute for Heroin. The market got the chills, but stocks took no notice, instead dropped on the failure of China’s trade delegates to visit Montana? The trouble could be that massive liquidity has overwhelmed a system designed for recycling a static pool of cash. I don’t buy the revenue neutral argument, and 50B a day for how many days? its a lot like stock day trading, you put your capital into a trade that lasts a couple seconds, and hope the market doesn’t lock up between the buy and the sell, and that 50B is only margin, not pledged collateral, as one writer put it that could easily turn into a trillion.

‘The trouble could be that massive liquidity has overwhelmed a system designed for recycling a static pool of cash’

Don’t forget the LEVERAGE factor and the quality of ‘collateral?

Do Banks trust each other?

The formula is as follow, higher wages implies higher inflation, the compensation costs–wages plus benefits–faced by employers is stuck at an all time low of around 2%.

When the tide goes out, “we” will see who is bare-ass naked of any real wealth …the trick is that “we” will not be allowed to look, i.e., “they” will obfuscate “our” view, essentially by claiming “Trust us. We are your friends.”.

If the banks were properly capitalized, there would be no need for a repo operation.

So does this mean banks have been enticed so far out to lend that they don’t have the over night cash necessary to avert a possible FDIC closure party?

Been awhile since we witnessed that kind of fun… but clearly being strapped for cash when you are supposed to be a bank (full of cash).

I think there’s more to this story than what they are really saying. Fool me once shame on you… fool me twice? I don’t think so.

“Financialization of everything is a booming business, and the bets have gotten larger, the debt has gotten larger, there is more collateral, and so the amounts have gotten much larger.”

Sounds great!

But what’s the QUALITY of these ‘collateral’? Are they valued at Mkt to Mkt or Mkt to fantasy#? Do the parties trust these collaterals?

—

Total reserves and excess reserves as a fraction of total bank assets. Compare these to pre-crisis history. To imagine that recent repo spikes reflect some inadequacy of reserves or the need for more QE is to misunderstand the nature of the constraint.

(h/t John Hussman)

Smoke and mirrors – statement appears to give control where there is none. Do not believe the fraudsters. They are gaming you. Choose not to be their game. Play your own. Be free. Exercise your choice. Give up your programming. Think for yourself. Be unpredictable. They hate it.

I think the explanation for the need for Fed funding of overnight lending is simply due to the fact the Fed is charging too low an interest rate. The Fed caused this problem by suppressing rates. The Fed can correct it’s mistake by raising rates. Nobody wants to make 1.75% when they can make more elsewhere, that’s theft. So even though big banks a drowning in liquidity, they can make more money elsewhere than the Fed suppressed rates.

So, let me get this straight. The Fed used to have a plan. The plan stopped working. Then they did something different for awhile. But now that has stopped working as well. The Fed now goes back to what they used to do.

Does anyone see a problem with this? What they are now doing has stopped working in the past. And now, what they did to fix that has also stopped working? So, what do they do when what they used to do stops working again, like it already has before?

Repos didn’t stop working in 2008. The Fed started doing QE, ZIRP, and various bailout programs in 2008 and didn’t need repos anymore. Repos work, don’t worry.

But I am reading repos have stopped working now. I am reading big banks had massive liquidity but avoided repos because they felt they could make in currency markets. Ergo, Fed needs to raise rates because they are suppressing them. Why would big banks avoid repos? Isn’t obvious? Because the Fed is suppressing rates.

timbers,

You’re mixing up the Fed’s repos with the repos done by other parties.

Those who need to access the market were being priced out. The demand for cash did not overwhelm supply, despite Fed response, putting more money into the system. They are pushing on a string. If a bank could borrow at below EFFR they would, the demand is not there, which is short hand for a credit event. The market in aggregate is boycotting the line of credit, and it has nothing to do with rates. Powell said that, business tells him, rates are not a deciding factor in new investment. If Treasury supplied the Repo window with collateral to hold rates at the market that would be QE. Their official explanation, a blip in the markets doesn’t jive with their response. We are about two seconds from QE.

One of the reasons why big financial firms have gone bust in recent decades is that the guys who know economics assume that there is an infinitely big pool of money, that has infinite numbers of buyers and sellers, and that flows of money are nice and smooth and can be approximated by infinitesimal intervals used in calculus to take derivatives and integrate integrals.

This is a great way to construct a mathematical model of the markets, but it’s wrong.

One reason why Long Term Capital Management went bust is that they assumed that the market would behave just like their macroeconomic equations said it should behave. They didn’t fully realize that there were a small number of big players who could dominate the market until it was too late. These traders didn’t care about macroeconomic equations written by Nobel prize winners. They saw a chance to stick it to LTCM and drive a competitor out of business, and they did just that.

It was stated above that four big banks dominate 75% of the market for the type of operations that are linked to overnight inter-bank lending, repos, and other ultra-short term flows of money.

I can’t help but wonder if the big four are quietly colluding to get rid of a competitor like they did when a hugely over-leveraged LTCM was gutted like a fish.

Giving up 10% interest on an overnight loan is a tiny amount of profit to forego. It’s a small hit that is worth taking for the chance to kill an opponent forever, even if it’s a small chance.

The real question is, who is the pigeon at the poker table this week?

I think you’re on to something, Ensign Nemo. Economics guys have been using higher math to make it look like economics is a science. Ha ! I have reached the conclusion that economics is a sub-category of theater. You know: you got your tragedy; you got your comedy; you got your economics.

Why was IOER at the top of the range before? Shouldn’t it have been below Fed funds or GC? Was it to try and keep the velocity of excess liquidity low?

this October should be very interesting to say the least. You never know which snowflake will start the avalanche but my bet is on the backup in the 10 year. The whole street was short. We calmed down a bit( 1.90 back to 1.75). But the next push might do it. I heard one trader say if we take out 2.07 then there will be a panic let alone if rates get to 2.70 as Wolf suggested.

Doesn’t sound like a robust money system. Sweep it.

Wow. There are a lot of comments on this one.

Is it a record?

Dave Chapman,

No, the record is over 300 comments. Here is an article with 315 comments (this is the one I could remember – but there may be others):

https://wolfstreet.com/2019/02/18/why-wolf-street-is-still-free-and-not-behind-a-paywall-though-you-have-to-put-up-with-ads-and-i-make-less-money-maybe/

There are some articles with over 200 comments. Here are some recent samples I could find without spending too much time digging:

218 comments: https://wolfstreet.com/2019/09/08/the-wolf-street-report-what-to-do-about-the-student-loan-fiasco-student-loan-forgiveness/

205 Comments: https://wolfstreet.com/2019/08/04/the-wolf-street-report-is-the-everything-bubble-ripe-yet/

274 comments: https://wolfstreet.com/2019/07/24/i-got-it-nothing-matters-tesla-boeing-stocks-like-the-whole-market-has-gone-nuts/

Dear Wolf

Possibly an indication of your growing readership.