“Sell first, ask questions later.”

The $1.2-trillion US leveraged loan market is starting to get downgrade-indigestion. So far this year through October 11, of the 1,460 leveraged loans in the S&P/LSTA Index, 282 issues were downgraded, already exceeding the 244 downgrades for the entire year of 2018, and blowing past the 33 downgrades in 2017, according to LCD of S&P Global Market Intelligence.

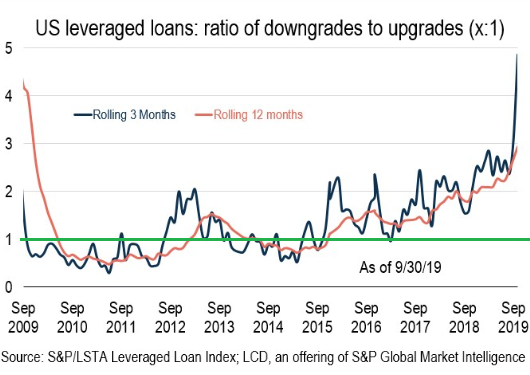

On a rolling three-month basis, the ratio of downgrades-to-upgrades spiked to 4.9, by far the highest ratio since the Financial Crisis. In the chart below via LCD, a value greater than 1 (horizontal green line) means downgrades exceed upgrades. A value blow 1 means upgrades exceed downgrades.

Collateralized Loan Obligations get cold feet.

The hot-button issue at the moment with leveraged loans is a one-step downgrade from B-, or a 2-step downgrade from B (“highly speculative”), to triple-C (“substantial risk,” see my cheat sheet for corporate bond and loan credit ratings by ratings agency).

It’s a hot-button issue because managers of Collateralized Loan Obligations (CLOs) currently purchase about three-quarters of the leveraged loans that banks are syndicating and hold about 55% to 60% of all leveraged loans outstanding, according to LCD. But CLOs have limits as to how much in CCC-or-below-rated loans they can hold.

The majority of CLOs limit their holdings of triple-C or below rated loans to 7.5% of their portfolio. This not a hard limit, but it triggers some mark-to-market rules and other factors. According estimates by Wells Fargo analysts cited by LCD, a CLO could hold up to 12% of its portfolio in these loans before triggering some of the requirement.

According to LCD, the median share of these loans within US CLOs is currently 4.1%, meaning half of the CLO’s already have over 4.1% of these loans in their portfolio, and they need to keep some room available when their single-B rated loans get downgraded to triple-C.

So when loans are downgraded to triple-C, and the CLO buckets for loans with this rating are full, then suddenly buyers are difficult to find, and funding threatens to dry up for these companies, which can push them into bankruptcy. In addition, banks can get stuck with leveraged loans. Both of which are already happening.

Leveraged loans are typically junk-rated loans issued by companies that have too much debt and not enough cash flow. Banks have no intention of hanging on to these loans. Instead, they plan to offload them to CLOs, loan funds, and other investors.

But some banks are getting stuck with the loans.

Investment banks – including Jeffries, UBS, Barclays, Deutsche Bank – have recently gotten stuck holding at least seven leveraged loans, totaling about $2 billion, sources told Bloomberg. These loans were used to fund acquisitions, including the leveraged buyout of Shutterfly by private-equity firm Apollo Global Management.

The banks could not off-load these loans for now and remain on the hook. While the amount is still relatively small, given the size of the leveraged loan market, this – and the stress showing up with single-B rated loans – is happening when yield-starved investors are otherwise still exuberant. Bloomberg:

Worries over a potential downturn have reduced demand for lower-rated loans at risk of downgrades, especially from collateralized loan obligations, which face limits on the amount of debt rated in the weakest CCC tier that they can own.

So CLOs are crucial in getting these loans off the banks’ books. Now all eyes are on the single-B category (B+, B, B-) that makes up 56% of all US leveraged loans outstanding. Loans rated B- account for about 13% of US leveraged loans outstanding, nearly double from early 2017. They’re just one notch away from CCC+.

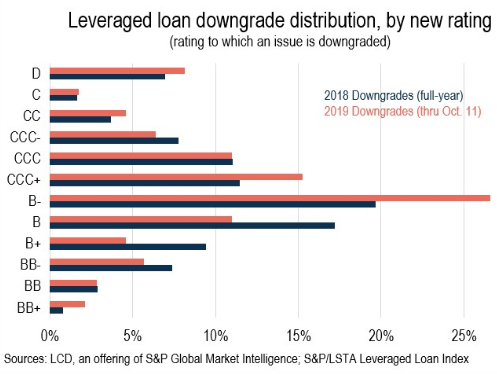

Of the 282 downgrades this year so far, 27% were downgraded to B- and 15% were downgraded to CCC+. The chart below shows the distribution of downgrades in 2019 so far (orange bars) and in all of 2018 (blue bars). “D” stands for “default.” BB+ is one step below investment grade. Note this year’s surge in downgrades to B- and CCC+ compared to last year:

“Sell first, ask questions later,” that’s the current attitude in the market about loans rated B-, LCD says:

CLO managers, however, are not waiting for rating agencies to act. Instead, they’re looking to get out in front of any earnings miss, especially as managers find liquidity disappearing quickly on a number of names.

Double-B rated loans “remain well bid,” according to LCD. The loans that are held by CLOs and that selling off are single-B, and they’re selling off out of fear of a downgrade to triple-C:

- The portion of these loans that are trading for less than 90 cents on the dollar has reached 9.5% of all loans held by CLOs, up from 6.5% in August.

- The portion of these loans trading for 80 cents on the dollar has doubled to 4%, from 2% in August.

For example, Deluxe Entertainment Services Group’s $782-million leveraged loan was trading at around 90 cents on the dollar in July. In August, a proposed spinoff and equity infusion didn’t pan out as planned, which led S&P to downgrade the loan from B- to CCC-. The loan plunged to a range between 36 and 40 cents on the dollar, according to LCD. Then this happened:

The credit is held by a number of CLO managers, many of whom were unwilling to participate in additional financing for the company following the downgrade, as they were hesitant to double down on additional CCC exposure at this stage.

As these existing investors – the CLO managers – were not able or willing to provide additional financing needed to keep the company afloat, Deluxe filed for a pre-packaged Chapter 11 bankruptcy and then obtained a Debtor in Possession (DIP) loan. Its $782-million leveraged loan recently traded at about 5 cents on the dollar, according to LCD.

That’s how a downgrade from single-B to triple-C can push a company over the edge because it can get cut off from funding.

The industry is now wondering, with CLOs being limited as to the amount of triple-C loans they are willing to buy, who will buy them? There will be buyers, including funds set up specifically to buy distressed credits – if the price is low enough. But that price may be so low – and the yield so high – that it effectively cuts off the company from any funding and pushes it into bankruptcy court.

Whose Bets are Getting Bailed Out by the Fed’s Repos & Treasury Bill Purchases? THE WOLF STREET REPORT: What’s Behind the Fed’s Bailout of the Repo Market?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

CLO’S are part of the Junk market and Junk is very slowly starting to Implode.

We know what that =

I think the figurative term to properly describe the future of corporate debt bag holders is blood bath.

Wasn’t burning junk illegal? Yet these companies all have incinerators.

Past history suggests they stay out of trouble by moving it around in their many financial catacombs until those responsible have taken theirs and legally disassociated themselves from the “incinerated money” before ashes and smoke make it too obvious.

A great article and charts, and many of those responsible may still be working out exit strategy for themselves while practicing plausible denial of the present situation…..but time is running out.

I have a hunch they will come out “winners”, as they say.

CLOs can hold as much CCC as they want, but over 7.5% they have to mark it at market, which impacts the over collateralisation tests and WARF test. So like any other portfolio you have to make a tradeoff decision. Most CLO excess returns come from the riskier credits however.

IMO so far this is an LBO equity story. They have been paying 10x EBITDA for companies, with 5-5.5x senior loan funded. The senior loan is taking up 35-40% of EBITDA just in interest. If corp margins fall the LBO equity becomes a zombie.

Downgrades also mean they get pulled out of the borrowing base for their individual credit lines and/or warehouse lines from banks (which provides the CLO its own leverage to go out and acquire paper).

So one loan downgrade shuffles the whole deck, as the CLO has an operating ratio to abide by with its own equity investors, plus the borrowing base for its own line of credit; you get a bunch of downgrades at once, and you really start to see a lot of shuffling.

The warehouse is only there before the CLO is priced, so a few weeks. Unlikely a CCC loan would get downgraded within a few weeks of being syndicated…

For sure as loans get downgraded most holders cant sell so just have to weather it out.

But there is a reason these are senior, secured loans and not high yield bonds, they have assets and other security behind them.

Interest rates for C rated loans have been rising compared to higher rated bonds.

S&P 500 company 2019 Q3 earnings reports have been showing negative average earnings growth. Weakness is expected in Q4 also.

As California’s utilities are fessing up to have started most of the recent (2017-2019) wildfires there are going to be serious financial consequences for share and bond holders of these major companies to say nothing about what this is going to cost ratepayers.

Mr. Richter’s decrepit PG&E pole outside his home is any indication of the true state of California’s electric grid, public safety power shutoffs are going to have to be far more extensive and perhaps more pervasive than what anyone is ready for.

“…there are going to be serious financial consequences…”

Exactly. We certainly all know us proles are just going to have to suck it up. How else are we going to fund the CEO’s annual $9M+ salary? (Not to mention the other board members well into the million dollar club too.) We certainly can’t expect the executive class to suffer. Heaven forbid. Quality management like this is just hard to come by.

Especially not when that Executive class can shut of power to people to force them to complain to legislatures to get them to grant a Big Bailout of Public Money. PG&E seems to have a lot money available for lobbying, but little for repairs.

In the American crony capitalism system, shorting the money for repairs and operating expense to create fake profits is a very old game.

Certainly your missive is worth a couple articles. The immediate fallout is insurers pulling out of the market. Those with mortgages, what is the blowback on that count? The Ca Insurance Commissioner just threw his hands in the air. He is “waiting” for authority. Most assume something akin to CEA will develop but that could take years. CEA only this year has the autonomy to write policies. It could be that the courts will clear the utilities and limit judgments, or the legislature will weigh in. If you build a house in a flood plain, or hurricane zone, you should assume some of the risk. Courts are being increasingly libertarian on this. Ca often leads the way in complex social issues, what does it mean for red state America? Is everyone supposed to live in a high density urban development? The country used to be where the poor lived, is there a demographic shift going on?

Earthquake and wildfire damage is ( not yet) a rich versus poor issue though I agree, if firefighting assets get deployed to Malibu or the Getty Museum at the expense of a trailer park in San Bernardino the political firestorm will begin.

What is unknown at this time is how did such a dire situation develop. Did California push too hard for ‘renewable’ energy and divert resources away from less glamorous activity such as renewing existing infrastructure and maintenance? Grey Davis was removed from office when he couldn’t keep the power on and people’s homes were not being incinerated. Gavin Newsom is going to have blackouts and homes burning down. Not good!

A century of tree-hugging to preserve “pristine” forests results in a humongous pile of tinder distributed everywhere. Otherwise known as shooting yourself in the foot. What do folks expect when they “nestle” their homes into highly flammable pine trees. PG&E’s next move may be to adopt the slogan “Only you can prevent forest fires.”

I think a state takeover of PG&E is becoming an increasingly likely scenario – and I would certainly expect investment firms to think that way.

In many ways it makes sense. CA pushes a lot of renewable energy agenda through the utilities and expects significant infrastructure upgrades without spiraling costs, yet investors seek as high a dividend as possible.

Interesting enough, we just witnessed a Liquidity Squeeze in the secured, government instrument, overnight lending market. Why this same problem has not shown up in junk or near junk bonds with very thin covenants is surprising. Wonder why there is no contagion like a forest fire? Maybe the yields spreads are mesmerizing. Lenders run away from making overnight loans but aren’t worried to get stuck for years in real junk. Weird. Ask the Taiwanese insurers and Mrs. Watanabe as they have loaded up in so called AAA tranches of CLOs.

Some of the same ‘primary dealers’ getting to drink at the Fed’s free money spigot are the same banks that are stuck holding the big leveraged loans that they can’t move. 2+2=?

Python,

I think you may have nailed it here. The repo market is pretty much the province of the mega-big boys – it only seizes up when that small club has a pretty good sense that one or more of its members is sitting on a lot of shitty loans about to go bad.

Now, about 45 days later, we start hearing that some big boys can’t offload the shit loans they manufacture for syndication.

Python, I think you nailed – insider word on the street is that one or more big boys are already in dangerously bad shape.

Wolf, how about a pool for guessing the right mega-bank? The LBO data is largely public so educated guesses should be possible.

In the daisy chain Fed throws money at Repo, which keeps dollar funding in Turkey going, whose debt is owned largely by Spanish Paribas, who owns American Bank of the West outright. There is also the uncomfortable notion that dropping rates narrows the Euro/US bond spread and foreign (hot money) investments, which probably took a hit when the admin delisted Chinese firms. I see Powell bailing THEM out on several counts. Last months impeachment selloff is this months impeachment rally. LW ticker tape parade. Your concern with the banks (who never answered to anything a decade ago) is “dually” noted. There is a new populist in town.

What @Python said, 2+2=4. There was/is a squeeze in USG and GSE repos at least partly because of the squeeze in CLOs.

I guess CLOs and Frackers have something in common.

I am not sure WeWorks and Softbank should be added to the comparison.

Re PGE… Forget the new CEO and get back the 100M+ severence from the last guy. What a crock that is. No one wants to hear about his decades of service. We have some of the same performances everyday everywhere and are getting realllly tired.

America needs a corporate death penalty. After all, corporations are considered people, and if a person killed tens of people in a single town they’d be deemed a horrible mass murderer. And we are regularly told by the talking box that capital punishment is needed as a deterrent to make people act correctly.

Seize the assets, and all the stock if value=$0. PG&E and Boeing as the first serial killers to be used to make an example.

“capital punishment”, he he. That phrase just took on a new meaning.

It’s criminal to lay waste to the lives of thousands or millions of people for fun and profit – unless you use a corporation to do it. Then it is lavishly rewarded. Mass destruction is highly incentivised.

Largely true, but not quite fair: if you do it with a Five Year Plan that’s cool to, or so the 20th century taught us.

Or to establish a Thousand Year Empire; and so on…..

If I am not mistaken Bill Johnson the new CEO got a 100 million $ parachute when he was forced out of DUK. It’s a small club at the top.

Wolf,

The hired lobbyists really have done their jobs well in buying politicians to change laws to protect the massive amounts of fraud in this current system.

Protect the money and to hell with the citizens paying the bills at inflated currency costs. Rewarding for deception while the honest gets incarcerated.

Is it a wonder the people are pissed and hate Congress.

After the last crash, didn’t we learn that these ratings agencies are all crooked? I don’t remember any massive reforms or public executions of their executives to teach the lesson to stop doing that. Thus, nothing’s changed, right?

So, I take it that the loans being downgraded to CCC are from companies that have reached the point where they can no longer afford the bribes to be considered “not junk”?

Thunar,

The problem was and is — given the conflict of interest you mention — that the ratings agencies downgrade too little too late. So when that downgrade to triple-C comes, it’s too little too late. So investors can brush that off at their own risk. Others know it’s too little too late, and they buy these securities only at an appropriately low price.

With cross global finance don’t you suppose that agency fealty in a sovereign market, or even between markets might get tested? What would happen if China downgraded USG credit rating? Agencies are nice when you own them, not so much when your competitors own them. There was an unspoken rule against knocking the other guys credit, and delisting Chinese ADRs is far less serious than competing ratings downgrades. The global players act like a bunch of doctors, they stick together, and it is in everyone’s mutual interest to pretend. Until it isn’t…

Ambrose Bierce,

China’s credit rating agencies are in much worse condition. A big one, Dagong, was just taken over by the government because of all the issues. That’s the one that downgraded US debt to BBB+, that’s two notches from junk :-]

I know, let’s have govt takeover the rating system. Govt does everything really well, is corruption free and super efficient. Amirite?

Maybe the Fed could buy those loans and waive the coupons, so the almighty recovery can continue to steam ahead.

Should we debate about this?!

https://www.marketwatch.com/story/this-couples-161000-in-student-loan-debt-was-forgiven-heres-how-they-did-it-2019-11-04

It sounds just like Bernanke, when first started printing free money, promised to be only 1-time, short term. And then it went on and BIGGER, transforming Fed’s mandate to Stock Market.

I worked my butt off in graduate degree, get work-scholarship to pay for tuition and stipend. Make sure I picked difficult Electrical Eng to guarantee a job after school. Nowadays these leeches just get a big loan and enjoy 4 years University life without lifting a finger, enjoy their daily starbucks while my BEST treat was only $1 McDonalds.

And now these leeches loan are paid off, bought by Federal Reserve. No wonder the University facilities and student housing are becoming a 5-star resort.

Being a teacher is NOT the same as “doing” a charity. They still earn decent salary, and 3-months summer off, and guaranteed job and pension for life. School Principal could earn more than Senior IT professional.

Pretty soon, Fed gonna own up Stock Market and your houses, the bigger the mortgage the better, because they gonna pay you back monthly through negative rate.

Not much to debate. Socialism sucks.

Next topic.

Any -ism sucks.

Altruism?

Atomism?

Prism?

I might “vote” for pre-Hamilton conservatism circa 1760. The only “-ism” we appear to have now is “schism.”

I get a little teed off at public employees put on a pedestal. Is their job more important than someone who builds homes, produces food or produces toilet paper.

Up yours old school. I worked as a public employee for almost 5 years. I agree there is a lot of dead weight in public employment but private industry subsidizes a far more vast herd of Dilbert bosses. There are many loyal public servants who keep their heads down for benefits while vesting their small pensions in exchange for low pay and the illusion of job security. I spent the last few months helping a coworker through his permitting nightmare as he jacked up an unfinished basement to become a 3 bed + family room space. The permit lady kept ticking him off until she finally snapped under his abuse to explain that the basement window well modifications she insisted on were to keep his toddler daughter from burning to death 6 years from now if daughter couldn’t evacuate a smoke-filled basement up dad’s narrow basement stairwell. In terms of pay, when I switched to private industry with the same skill set I received an immediate 25% increase in salary but crummier benefits and no pension benefit (instead 401k matching). I have witnessed state agency corruption & inefficiencies before my switch but private industry hijinx I witnessed after the switch from public to private made State of Oregon corruption look like Our Gang shorts from the 1930s. American capitalism works best when predatory capitalism doesn’t get to chew holes in the regulatory playing fields. Sorry for the ad hominem attack but I worked with a lot of hard-working folks who were ethical public servants.

You should’ve worked in Chicago where they have no low paid public workers and the benefits are stellar.

Really big, bad things, start out small.

Remember ground zero 2008 and sub-prime mortgages?

Well guess what? Theyy’rre baaack! With a new name.

“Non- Qualified Mortgage”! lmao

The amount of non-qualified mortgage bonds, that have been bundled – $18 billion just this year alone! A 44% increase from 2018.

A crises starts somewhere, usually small in the background. Just another one of those ‘pesky’ fundamentals.

Mean while indexes are shooting up and Fed opened the spigot for ‘easy-peasy’ money! 250 B in two months increase in balance sheet! No fundamentals or NOTHING matters! Bigger bubble in process!

Except that money is horded by the banks which do nothing with it. If anybody wants an example of overleveraged, it is the big banks with trillions in derivatives. I suspect all the federal reserve is doing is making sure its member banks don’t fail.

Wish we could say the same for China. According to a recent Zero Hedge story, overleveraged Chinese banks are starting to fail.

No one really knows what’s going in Chinese Banking system including their bloated ‘shadow’ banking! Their GDP involves non-evonomic activity. Their accounting is more than suspect.

But the investors believe whatever PBOC states their ‘health’ No one really knows the % of non-performing loans or the required capital ratio? The Germany’s DB Bank’s accounting is a mystery no one explain!

‘The Deutsche Bank Death Watch Has Taken A Very Interesting Turn’

zh

OK so where is all this money coming from?

See how the beast is fed.

Net New Cash Raised from Treasuries in 2018 and 12 mos. ending Sept 2019

In 2018, we (in billions)

issued 7,246.0 bills and 2,192.0 notes

retired 6,872.9 bills and 1,682.8 notes

In 2018 we (in billions)

raised 373.1 from bills (34.8%) and 509.2 from notes (47.6%) and 188.3 from bonds (17.6%)

for a total of 1,070.5 of net new cash.

In the last 12 months ending Sept 2019, we (in billions)

raised 137.0 from bills (13.1%) and 696.1 from notes (66.6%) and 211.6 from bonds (20.3%)

for a total of 1,044.8 of net new cash.

We have plenty of cash to burn. Until ???

…Until we get too much debt. Then we burn the debt, wipe out some investors, and go right back to burning cash again. Try to find a long-term counterexample in any country.

Maybe that’s why Powell is shattering QE records with his “not QE” QE4 in the repo market, swelling the Fed’s balance sheet.

CNBC: If Trump wins in 2020, stocks up 15% in 2021. If Warren wins, down 25%.

I think he’s being way too conservative on the Warren front. More like 35-40% is accurate.

So there it is bears…vote for Warren and your dreams of a great crash will come true.

Just Some Random Guy,

They said the same thing about Obama in 2008 and about Trump in 2016. Both were going to wipe out the stock market essentially, according to pundits. Trump was even himself talking down the market during his campaign, said he sold all his stocks, and that the market was fake, and that interest rates were too low, etc.

They weren’t wrong about Obama. The day after he was elected, S&P500 lost 5.3%. It lost another 25% over the following 5 months.

He took office in January, and two months later, the collapse that Bush handed him was over — and was followed by 10 years of rally.

The only credible bet I could think of on the election would be a spread (put+call) in specific stocks you think might be affected.

Ideas of industries where their policies might drive divergent responses: Coal, solar/wind, defense, etc.

Expecting an overall market crash or spike is a bit much – I’ve heard that all my life about candidates and it doesn’t really work that way.

Will DB of Germany be the first domino (Lehman for this on going everything bubble) to pop this bubble? Can Powell prevent this?

if Deutsche Bank goes down, it will be even more catastrophic for the global financial system than the collapse of Lehman Brothers was in 2008. Germany is the glue that is holding the EU together, and so if the bank that is right at the heart of Germany’s financial system collapses, the dominoes will likely start falling very rapidly.

Deutsche Bank has been going down for a while. It will be death by a thousand cuts – though not so much for the DB as rather for the taxpayers and holders of Euro fiat which the ECB keeps inflating, and eventually perhaps also cause some long faces among bailed-in account holders. DB has significance as a national symbol to the German gov’t which tries to prevent a public collapse for that reason.

DB “the glue that holds the EU together” – why so?

DB will not be allowed to blow up in a disorderly manner. The German government won’t let that happen. DB is already a lot smaller than it was years ago. And it will continue to get smaller. If push comes to shove, the government will step in and take a big stake and shareholders might get diluted to death, and heads might roll, and divisions will get spun off and assets will be sold, but there will not be a disorderly collapse of DB. Not in Germany. You can take that out of your scenario.

√

DB as you say, will not be allowed to implode, however a, shareholder, bondholder, or large depositor, I would not wish to be.

Is there a connection between leveraged loan instability and the sudden unwillingness of the primary dealers to provide money to the repo market?

Do people with leveraged loan portfolios run to the repo market when the loans get in trouble? Can junk rated companies access the repo market?

Starting out in the small loan business in 1974, my Region Manager told me in my first review, that…. “you made a bad loan here, and all the collateral in the world cannot make it into a good loan”.

Seems many should have followed this basic truth.