Burning cash is easy; It’s quite flammable and just goes up in smoke.

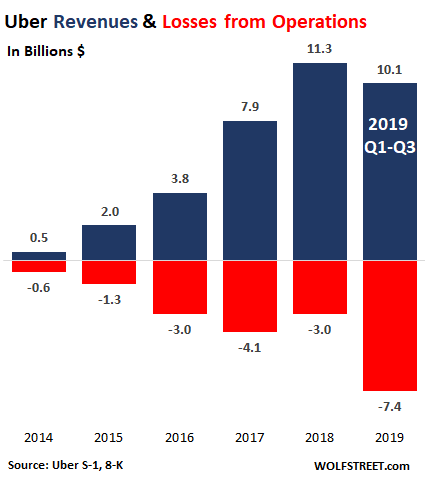

Here it is in a nutshell, the philosophy of “growth at all costs.” Uber’s total revenue increased 29% to $3.81 billion in the third quarter compared to a year earlier, the company reported this afternoon. And that’s very good revenue growth. But to get this revenue growth, the company threw everything at it that it had. So, expenses increased even faster, and the operating loss ballooned.

Revenues by segment:

- Rideshare revenues: +19% to $2.9 billion.

- Eats revenues: +64% to $645 million

- Freight revenues: +78% to $218 million

- ATG and other Technology: $17 million

And here is what it threw at it: Total costs and expenses soared by 33% to $4.92 billion. This includes $401 million the company paid its employees in stock-based compensation. In other words, to obtain a $969 million increase in revenues, the company spent an additional $1.2 billion.

At this rate, when expenses grow faster than revenues, there is going to be a problem trying to get to this mythic breakeven the way the company is structured now.

As a consequence of expenses increasing faster than revenues, its loss from operations soared by 45% to $1.11 billion.

It’s net loss – after interest expense, other income, losses from equity investments, and provisions for income taxes – rose by 18% to $1.16 billion, up from $986 million a year ago.

For the three quarters so far in 2019, Uber has lost $7.4 billion. You really have to try hard to lose $7.4 billion on $10 billion in revenues:

Cash flow from operations was a negative $878 million in the quarter, bringing the cash burn so far this year to $2.52 billion.

But don’t worry: it has plenty of investor-cash to burn, thanks to numerous fund-raising rounds, the cash raised during the IPO, and some monster debts. At the end of the quarter it still had $12.6 billion in cash to burn.

A big part of that cash is borrowed: Uber has $5.7 billion in long-term debt. Those creditors – despite Uber’s deep-junk credit ratings – aren’t worried as long as Uber as enough cash on its balance sheet to service and pay off the debt and a high enough a stock price to issue more shares and use the proceeds to service the debt. Creditors get very nervous when neither cash nor a high stock price is available to bail them out. So that’s what they’re keeping their eyes glued on.

Uber was founded over 10 years ago. It has about 27,000 employees – though there have been waves of layoffs this year, including another 350 folks two weeks ago. It has burned through enormous amounts of investor cash over the years. And yet, it is further away from making a profit than ever before.

In a brief interview on CNBC today, CEO Dara Khosrowshahi said the company is targeting “adjusted EBITDA profitability” in 2021. “We know there is the expectation of profitability, and we expect to deliver for 2021.”

“We haven’t finalized our planning, and it’s going to take a lot of work from a lot of folks, but we are actually targeting 2021 for adjusted EBITDA profitability for the year,” he said.

What does Uber’s “adjusted EBITDA profitability” actually mean? It means if Uber ever breaks even on this “adjusted EBITDA” basis, it will still lose a ton of money.

“Adjusted EBITDA” eliminates a lot of the bad stuff. Unadjusted EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) is a fairly standard measure of operating cash flow, not profit. Creditors use it to see if a company can make its interest payments over the near and medium term.

In Uber’s case, there is “adjusted EBITDA.” And in its earnings release at the bottom, Uber lists all the bad stuff that it excludes from it. Here are the biggies of the bad stuff that is excluded:

- Depreciation of property and equipment and amortization of intangible assets: But “the assets being depreciated and amortized may have to be replaced in the future, and Adjusted EBITDA does not reflect all cash capital expenditure requirements for such replacements or for new capital expenditure requirements;”

- Stock-based compensation expense, “which has been, and will continue to be for the foreseeable future, a significant recurring expense in our business and an important part of our compensation strategy”;

- “Other items” that are “not indicative of our ongoing operating performance”; so shit happens, and it doesn’t count.

- “Certain legal, tax, and regulatory reserve changes and settlements that may reduce cash available to us.” Of which there have been many, given all the scandals and issues with labor laws and taxi regulations in various jurisdictions.

So if Uber gets to “adjusted EBITDA profitability” by 2021, it will still be losing a ton of money, and it will be a long way from actual profitability, and it will be even further away from significant actual profitability that would create some kind of reasonable earnings multiple as appropriate for a taxi and delivery company.

Shares are down 5.2% in afterhours trading currently at $29.49, down 37% from its peak in June.

You’ve got to admire the guts to create something this big that burns up this much investor cash for a decade and on an ongoing basis, and that hasn’t yet figured out how to make a real profit, and apparently has no plans of doing so. Burning cash is easy; it’s quite flammable and just goes up in smoke. Building a profitable business in a competitive environment, that’s hard.

This is a holy-cow moment. Read... Tesla Discloses US Revenues Collapsed 39%. Americans Sour on its Cars, Pent-Up Demand Exhausted

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Well……why are you so hard on the young generation. This company obviously deserves at least a 400x sales multiple in the market. Of course when they go on sale we can swoop in and steal it at 350x sales. This madness of expecting profits from invested capital is so 20th century.

We can also stop with the nonsense of taxing profits…..why not just hit revenue with a 10 percent surtax. Shazaam……I’ve balanced the federal budget. Nobel prize headed my way.

Righteous comment.

I agree. Wolf, you should pick on 100 year old cash burning companies like GE instead of a mere 10 year old…

That is sarcasm by the way….

Since they are loosing money, shouldn’t the various share prices be going up???

But the service is much better, you get new car (even Lexus sometimes), vs duck-taped-rear-seat Crown Vic. And it’s cheaper, unless it’s surge price time, which is always.

And that might be Uber’s main problem (Lyft too). They spend too much money on new cars. Maybe a good cut-back could be to buy slightly used cars including those that were in rental car lots at airports, or were leased for five years or so by other drivers.

They don’t own the cars

But all the hip kids use Uber in LA and SF. How could it fail?

The thing is, it offers a good and popular service. All it needs to do is figure out how to make decent profits doing it — but that’s the hard part.

You realize that making a profit isn’t the job of the current CEO, right? Dara was mission accomplished the moment Uber went public. The investors all got paid off, the schmucks are left holding the bag. Dara probably has his millions in the bank, he just has to make sure the boat stays afloat long enough for him to collect, and then…. adios muchachos.

Profitability is the job of the next sucker.

OK you’ve sold me, all I need is an $800 phone and about $400 a year more in connect costs ($60 plan vs. $30 plan) and I, too, can order a car driven by a hugely overweight incel who’s driven so many hours he’s on the brink of running down pedestrians and cyclists he doesn’t know are there.

(True. I was almost run over by a really fat guy driving an Uber, and he was sorry once I’d evaded him and he’s realized I exist. At least where I am, if you are driving for Uber you’re desperate.)

Cabs are fine with me!

Down here ride sharing drivers are well diversified and provide a discrete variety of products and services inside the convenience of the vehicle. The ride sharing is just a front.

As taxi medallions soared , the only party making money was the investor in taxi medallions,who charged the drivers large monthly fees .

In the current ride share market, only those early investors have made money.

Just like those late investors in medallions , current investors will be “ taken for a ride”

Investors in Lyft and Uber like to think that ride sharing is a disruptive technology , when it is really only the taxi business.

But isn’t it only popular because it is subsidized and violating various regulations (e.g. most drivers do not have commercial insurance and of course pay not gov’t fees) allowing it to undercut cab rates?

I have been to multiple cities that have excellent ride hailing services that cab drivers subscribe to. That’s what I use because I will not support a company (Uber) that is basically operating a dirty business

Yes, cab companies have been using good apps for years. I know a cab driver here in SF who has been using it. But his business got gutted nevertheless.

Do they sit there and talk on a conference bridge with all the other cab drivers or whatever they’re doing on the phone the entire ride every time?

The existing taxi system was a monopoly.

This I think is the crux of the matter. Cabbies are victims not so much of Uber (and thus of Wall Street) than of the app stores. If you have ever visited one, you know discoverability is nil. With millions of apps, only the few with the most marketing muscle manage to put their apps in front of user eyes; everybody else sinks without a trace. This is a manifestation of the winner-take-all nature of online markets, so that the user-per-app curve takes on brutal Zipf law characteristics.

It doesn’t matter how slick the competing ride hailing apps are if users don’t even know they exist. I must say I don’t see a way out of this quandary, short of spending tens of millions on marketing, which of course traditional taxi companies can’t afford to.

I am going to NYC to await hailing the Cash Cab. I am good at trivia as long as they stay away from pop-culture questions. What is missing from Uber and Lyft is the lack of Checker cars.

This is my exact thoughts about Peloton – its a really cool product that could be in any high end hotel, service apts, executive lounges / clubs but just like Uber all they are doing is burning cash. I haven’t looked at their financials closely but it looks like all these unicorn are taking on the same strategy.

I keep getting Peloton mixed up with Juicero.

We took a ride in one & it is no better than the old standby “YELLOW CAB”

So who cares if they go bellie up!! They have drained enough money.

I use Uber primarily to get to and back from SFO airport and some destination airports in US. Honestly the price Uber charges are low and wish they raise prices to pay the drivers more who barely makes $20/hr with the known expenses and lot less with hidden expenses. Most drivers I’ve come across are nice people in between jobs or supplement their income though I’ve seen some serious drivers who equip their cars like a vending machine and interior more like a beat-up cab.

What gets me though is how an app company can lose $1.1 billion or $120 mil per day while paying their drivers peanuts.

Here’s on example of how they burn cash. They had a normal meeting at corporate. Instead of using a video messaging app like Skype, they flew all the people to Fiji for three days.

Article in the Chronicle a couple months back. Uber spent over $200,000 on balloons for birthdays at the HQ in SF.

Maybe they pretend to only lose money so they don’t have to pay any taxes.

Companies that would spend to avoid paying taxes know the minimum profit numbers allowed before taxes hit and spend anything over that mark. Successful companies don’t run in the negative unless they have tons of free money to keep them going down the toilet.

Ubers value may lie its ability to demonstrate there is a useful purpose in it services that have a demand . As often happens Uber may not be the entity to make it profitable. The collective will benefit no matter their future.

Does the 27,000 figure include drivers, who i thought were independent contractors? With all of those employees, you’d think they would have great customer service. But you can’t reach them by phone.

That 27k does not include drivers!

Uber had 3 million drivers in 2018.

SZ,

“That 27k does not include drivers!”

That one fact goes a long way to explaining the admin overhd cost insanity that must be destroying the unit level economics.

What in the hell are those 27k doing? The system is almost entirely automated – hello internet.

I can also imagine a shit ton of ad spend abuse…

They have gotten this far by punishing labor, which is a trend that has limits. They are swimming against the current. Minimum wage laws, and state and city regulations will at the least prevent Uber from gaining an economy of scale. On a similar subject Google is coming under fire for directing traffic around freeway slowups through secondary roads, which has residents on normally quiet neighborhoods up in arms. The system has to get a whole lot more sophisticated, or they have to admit they cannot solve the problem of centralized transportation with decentralized systems.

As I pointed out earlier (different post) Uber develops massive amounts of software, so at least some hundreds of these people are software developers. And I know that many of the others are recruiters of sorts, i.e., their job is to sign up drivers (I imagine there is high driver attrition and that they need to be constantly looking for new ones). But 27K seems crazy nevertheless.

27,000 lawyers fighting each and every local unique taxi commission in every municipality it serves; all cities, fifty states, protectorates and countries.

I still think the whole ride-sharing thing is a desperate race for monopoly power. If UBER fails to achieve it in significant markets, the lack of pricing power probably means these business models, as currently operated, will never reach GAAP profitability. WHAT UBER IS ACTUALLY SELLING HERE IS TAXI RIDES, NOT SOME TECH MAGIC.

To me, “adjusted EBITDA profitability” just translates to “we’ll be profitable if you ignore most of our expenses”.

The VC model of start-up funding, allowed UBER 10-years of operations with $10+ billion-dollar-losses just demonstrates UBER management is not strong enough to manage its appetite for dream projects (freight, eats, AVG et al), and they don’t have the chops to operate at a profit in any sense of the word.

They’re grasping at straws…

Monopolies of any kind cannot exist without some kind of government backing.

Uber has been playing with fire in that respect: remember the Greyball and Ripley software used by Uber have been specifically employed to deal with law enforcement agencies where Uber is illegal. Last year a police raid on the Uber offices in Brussels (the staff panicked and tried to flee instead of using Ripley to wipe and lock their computers) netted an internal document called “unexpected visitor protocol” instructing Uber employees on how to deal with law enforcement agencies in countries where the service is illegal.

Where Uber is legal however, so are their competitors: Lyft, Free Now, Turo… plus the good old taxi companies that are getting beaten into a pulp precisely because they trusted their politician pals to keep any competition off their back and got stabbed in the back at first occasion.

All these rideshare companies are happily burning through mountains of cash provided to them by investors desperate to find the next Amazon and FaceBook. If bicycles and e-scooters are anything to go by, these companies seem to have a nearly endless supply of investors willing to lose money: as soon as one folds (leaving behind piles of rapidly rusting bicycles and vandalized scooters), another takes its place.

So I don’t see Uber developing a monopoly anytime soon, ironically for the same reason the company can keep on throwing money out of the window so carelessly.

You say “burning billions” like it’s a bad thing. Get with the times, Wolf. It’s different this time!

/sarc tag omitted :)

I go to Walmart and purchase Uber gift cards, since I’m particular about who I give my credit card number to. They still owe me $50.43 of rides. It looks like I might be safe for a few more months.

The point of the credit card is you don’t have to care.

Oh, these Millenials!!!…all these guys have done is change the entire freakin’ world of hailing a cab in the rain, and in the lingua of Thomas Friedman flatten the world to the benefit of drivers and users alike. Pity, though, poor central cities across the globe like New York, that can no longer auction off their rip-off ‘medallions’ to the unsuspecting young men & women trying to earn an honest dollar!!!… PJS

There are baht bus, tuktuk and motorcycle taxi businesses here in Thailand that will still be making money long after Uber has gone bust. Just as convenient and almost as safe (sarc).

Problem is automobiles depreciates at a fairly rapid rates. In the first three years of a new car, it has already depreciated 30% to 40%. Then you write off labor, driver costs and it’s almost technically impossible to generate profits such as Uber!

Lyft is doing better but both bleeding cash!

When the crash happens, nothing will be left!

Uber owns very very few automobiles.

They did say they were going to buy 24,000 Volvo XC90 SUVs next year to make them self driving vehicles.

Suzie Alcatrez,

The third-party anti-spam algo found you too, it seems. All your comments are automatically sent to the moderation queue. Many commentors are getting caught up in it. I have no idea why. Eventually, this will go back to normal. So be patient.

Far from whingeing, you Americans should be grateful that investors remain happy to fund American companies. They still have fight and hunger!

Contrast it with the UK, where UK investors bail out of UK firms at the earliest possible moment and do not give a hoot what happens.

For example, Just Eat UK (much bigger than Uber Eats UK) is about to be sold off to a Dutch rival (Takeaway) that is 3 times *smaller*. UK investors have just thrown their hands in the air and said “we give up”. We surrender!

Net result = Uber Eats US continues to grow (longterm)… Just Eat is toast, and all the best jobs will shortly be closed in the UK and moved to the Netherlands…

You US guys shouldn’t really be complaining about loyal shareholders with strong faith. You don’t know how lucky you are :-)

Far from whingeing, you Americans should be grateful that investors remain happy to fund American companies. They still have fight and hunger!

Mostly they have loads of money and no where else to invest it because they’ve been squeezing loads of money out of every possible market with all their other investments, which is how they got loads of money in the first place that they can’t invest.

So they’re going to piss away their money on every new fad that comes along, which isn’t a problem because they have loads more.

You don’t really think these guys go broke when the market crashes, do you? Don’t be silly. They just buy up loads of temporarity impaired investments at bargain-basement prices, figuring on making it rich when the markets come back, and will continue this cycle until financiers finally burn the whole thing down. Figuratively speaking, of course.

Believe me, I don’t ever complain when investors are subsidizing my rides… it’s not my money.

Logically, ride shares are at a point where it’s so much cheaper to take than long term parking in most instances. The only situation where ride share is not cheaper is if you are doing a one to two day hopper between LA and SF.

I remember the days when I had to take South Bay shuttles between SFO and San Jose, I was shelling out $30 to be stuck in a van for two to three hours while a bunch of people got picked up on the peninsula. Now, I can save time and get the same service for about $20 more. Who wouldn’t take that option.

Meal delivery services are if possible the best way to burn cash: I am actually surprised the whole business hasn’t been discovered to be a sophisticated scheme to launder money coming from tax evasion and other illegal activities.

I’d like not to draw your attention to your phrase “Uber Eats continues to grow”. So do their dozens of rivals: in Bilbao alone I stopped counting at six different meal delivery services and in Metz (population 117,000) I counted three, but there may be more. As a business owner I can tell you it’s so easy to grow when you don’t care about profits and losses.

Delivery Hero managed to get through the IPO door in 2017, laying bare for all how much money it costs to grow: in FY2016 they had revenues of €297 million and lost (EBITDA!) €107. In FY2017 they grew revenues to a whooping €544 million, up 83%. But losses grew to an equally whooping €190 million, or up 78%. Assuming this trend continues Delivery Hero should break even in FY2037 or so. ;-)

Delivery Hero, like all these meal delivery outfits, buys and sells brands and divisions with passion. In 2018 they sold their German operation to Takeaway.com, but immediately announced the purchase of Hipmenu (active in the Balkans) and a few months later of the food delivery division of Zomato. Oh, and Delivery Hero owns about 15% of Takeaway.com, making them the second shareholder. ;-)

Takeaway.com is a Dutch-registered NV, explaining their seemingly minuscule size and shopping binge (why do you think The Netherlands are a corporate haven?), but they have lost money every single year since their IPO in 2015, meaning not even the wonders of Dutch incorporation can help them.

not even the wonders of Dutch incorporation can help them.

And that doesn’t seem to be a problem for them.

Classical Capitalist Thinking says that Schumpeterian ‘creative destruction’ will necessarily take over and put them out of business, to make way for a more worthy business model. All well and good, other things being equal.

But it doesn’t happen, and the waste continues. Why? Obviously there must be something seriously wrong with Classical Capitalist Thinking. But what could it be?

That leads to other questions, harder questions. And it is clear that the failure to answer those questions constructively has dire consequences. Problems screaming for solutions should not be ignored as background noise.

Classical Capitalist Thinking does not provide for a central bank and the banking rackets that create “capital” from nothing.

If this is capital from real savings, none of the horror shows would be possible

Takeaway has achieved monopoly power in the Netherlands. And the Dutch market is not minuscule compared with the British.

In FY2018 Takeaway.com (TKWY) reported revenues of €204 million. That’s minuscule compared to competitors such as Uber Eats ($620 million) and frenemy Delivery Hero (€540 million), especially considering TKWY controls a large network of companies which include Lieferando, Foodora, Oliveira etc. As said you don’t incorporate a company in The Netherlands just because you are a fan of Floor Jansen. ;-)

And from what I have been able to piece together TKWY will merge with Just Eat. Unless this is a Japanese-style “merger” (meaning a thinly disguised acquisition to save face) it will be interesting to see the details, such as where the resulting company will be incorporated, what will happen to Delivery Hero’s large equity investment in TKWY and how much money will they able to lose.

The founding business of Takeaway.com is thuisbezorgd.nl so incorporating in the Netherlands is to be expected. Thuisbezorgd started out as purely a website to connect consumers with restaurants that home delivered. Their own delivery service is only a recent additions and they claimed back in 2018 that it can’t be done profitable. My expectation is they will close the delivery service when Uber.eats etc. go belly up

FY2018 does not include the German part of Delivery hero And Uber includes the delivery costs so merging with just eat (TKWY get 47.8% and the CEO position) makes sense.

ps. Thuisbezorgd.nl gets 13% for connecting the consumer with a restaurant with restaurant operated delivery. This should be highly profitable

Burning cash is easy; it’s quite flammable and just goes up in smoke.

And here you thought Uber was a taxi and delivery company, when it’s really in the disposal business.

Taxi and delivery companies are regulated because they should be, for practical reasons. A firm based on evading provably necessary regulations should be prohibited.

Well, seeing that the definition of “adjusted EBITDA” in most credit documents is now 4-5 pages long full of baskets, carveouts, addbacks and run rate/synergy exercises, I expect by 2021 we may be at the point of “screw it – just take your best day and multiply it by 365” when defining Adjusted EBITDA.

Investors prefer to be lied to by con artists out to rob them, apparently because they have money to waste and really just want to be stroked.

A fool and his money are soon parted, but you have to wonder how they got together in the first place. What’s even more wondrous is that they really don’t seem to mind.

“You’ve got to admire the guts to create something this big that burns up this much investor cash…”

Doesn’t take guts, just takes chutzpah and access to stupid investors, which seem to be available in endless supply.

Don’t forget a credulous business and finance media, which invariably tout these transparently non-viable, and often fraudulent, companies.

Please, pardon my density (and maybe it’s been explained but I’m too dense to have noticed) but how does a company that owns no depreciable equipment (the cars), doesn’t pay its frontline employees as W2 employees and is basically automated can manage to nor make a dime in profit! I’m seriously in the wrong business!

A disciplined taxi company with that kind of business that is not blowing a fortune on self-driving car development, fancy headquarters and other offices in the most expensive places in the US, and the “growth at all cost” method to pile into new trajectories that might never pan out would make a decent profit. But it also wouldn’t have a $50 billion stock market capitalization.

Even expensive places like SF needs low wage services. The only difference is how the Valley is able to add in the software layer to monetize those services and projected across the rest of the planet and slap the label technology or innovation on it to sucker investors.

Companies like Google and Facebook aren’t tech companies, they are glorified ad companies. There have been very few tech companies in the Valley for a long time, the last really interesting one was Tesla.

The funniest thing is all of the so called socially conscious advocates in these ad companies who don’t do much real work and are literally hovering up money while whining about the hand the feeds them. The latest gem is this petition by Googlers against Google…

https://www.google.com/amp/s/www.vox.com/platform/amp/recode/2019/11/4/20948200/google-employees-letter-demand-climate-change-fossil-fuels-carbon-emissions

I especially like how some of these people are also busy protesting mass surveillance when they work at some of the biggest mass surveillance organizations in the world. Yet most of these petitioners and protestors don’t ever follow their own convictions because they are too busy looking out for their own economic interests. Utterly hilarious.

My thinking about Uber has been that the idea was likely to establish a broadly used app/service that could transfer to driverless vehicles, without at that time having to start a fight for customers on equal footing with competitors, and that they’d just eat the costs of paying drivers in the meantime, whilst subsidising rides in order to capture market share.

I suspect that the’ve miscalculated the time frame, though, but handily the company instead admirably fulfils its other function of being a capital transfer mechanism.

I think that’s a good point. It’s likely Uber, Lyft, etc could do very well is they didn’t have to pay drivers.

But automated vehicles are still a few (too many?) years away.

So the right idea, but too early. I wonder if Google (or Apple for that matter) are just waiting for Uber/Lyft to flame out so they can take over smoothly and easily. Right now they can just sit back and watch what Uber does right and wrong and adjust their own future business model accordingly.

I believe Waymo begins to run fully self automateed cars in certain restricted areas in Arizona next year. Fully automated, no drivers.

There are some pretty crazy big rig trucks moving in Arizona for UPS facility to facility. Video of it on youtube driving in the rain. Not a Tesla sensor package of a couple of cameras, they have full LIDAR and such in addition to stereo vision cameras and such.

Apple, maybe…. with Google, who knows. Have they had any successful project outside of their core search and YouTube business?

Android.

But you are right

Drivers tell me I have the oldest profile they have seen whenever I ride in an Uber. I downloaded the app in 2011 when it was still called Ubercab because it was impossible to get a cab in SF at certain times and Yo Taxi! was the only competition. At the time, you could either get a yellow cab or a black car that took you home at 1.5x the fare with no tip to calculate, no cash to fiddle with, and you could split the fare on your phone among riders. You knew you were paying more than a cab but it was for a reason.

This entire model (Uber/Lyft) has morphed into a race to the bottom until you replace the driver with a robot. It’s just a race against time and cash burn to get there. Either Uber and/or Lyft will be around to reap the rewards, or someone with more cash or time will pick up the carcass and the technology.

If i sit outside my house and chart for an hour the cars that pass by, in a given morning rush, I would estimate that half are Uber/Lyft; traffic is a nightmare. 5% of the traffic are the Cruise/Waymo/self-driving prototypes going around the neighborhood.

Uber’s philosophy, top to bottom, is:

(mighty) cash flow now, (stupid) bankruptcy later.

Ordinary people want (mighty) cash now, today;

they don’t care about their (stupid) credit rating.

It’s wrong to horde yard-sale booty and body fat;

yet, somehow, hoarding financial “assets” is a good thing.

Remember seeing a theoretical curve of the growth rate vs life span of a typical company. I prefer to stay away from early lifespan investment as it is too much speculation for me. At some point the growth rate will slow to a more predictable and sustainable level where you can make a rational decision about future cash flows and figure out a price to pay.

Can we please stop talking about drivers being poorly paid? Uber drivers are doing this as part time work. I take Uber to the airport often and it’s always a college kid or a retiree working a few hours here and there. I’ve yet to encounter anyone whose primary job is Uber driver.

The stories you read about, drivers only making $1.27 an hour or whatever are the morons who buy a brand new 12 MPG SUV with a 7% loan to specifically drive for Uber. WhicH is I-N-S-A-N-E!! And it’s impossible to be profitable doing that.

The sweet spot is drive a 30+ MPG, 6-7 year old car that’s in good condition and already on the flat end of the depreciation curve. Other than gas, tires and brakes there is no vehicle cost. And that can be very profitable to drivers. As for insurance, I looked into it, and my insurance charges $10/mo to add an Uber/Lyft supplement.

My experience has been entirely different. I live in deep LA and use Uber either for a hedonistic night of 80’s music or to get back and forth from the airport. The Uber driver almost invariably is an immigrant with a relatively new, high-end Japanese car–often with leather seats and tinted windows. (Some offer complimentary mints, water, and phone charging.) They’re working the road all day.

But I totally agree with your analysis: it can’t be profitable for them. Like Uber, they lose money with every ride.

Of course, new wave progenitor Gary Numan saw all of this coming in 1979 when he piped “Nothing seems right in cars”…

Morning… Everything comes back to the ponzi of selling the IPO to the shepple and taking the money off the table. There are so many of these now my brain hurts. There used to be actual companies in SV that were not based on the current mind set.

Expenses growing faster than revenues sure does not seem to be a problem for the US Government (aka taxpayers). I know Uber cannot print its own currency. See WS recent comments on the debt and deficit.

Maybe that is the “successful” model many companies follow today.

In the 1970s in Freeport, GBI the taxi system seemed to be literaly anyone with a running car. Great, happy people. Frequently, had to wait for, or help the driver at the market for bread or milk, but was otherwise real efficient and fun.

Rare to find them working on Sunday, but did find a guy who was doing some family errands. Got to meet his family and had lots of fun. Couple of hours of stops here and there for a few miles journey.

One guy explained, when I tell you I’ll be there Bahama time, that means I’ll be there….anytime I get there…… Don’t worry, be happy.

Maybe this will be the ultimate evolution of the Uber type services.

\\\

All this money for nothing, truly a sad system.

\\\

Good article, but maybe you miss the point, Wolf: their objective may not be to become profitable with their operations, they intend to establish Uber as a “household name” and then sell it to one of the big (German) car companies, that are too slow/ too conservative/ too cautious in establishing a car sharing company

see for instance:

https://www.handelsblatt.com/meinung/kommentare/kommentar-die-mutlose-deutsche-autoindustrie-ueberlaesst-uber-das-feld/25188444.html

(“the-fainthearted-German-auto industry-leaves-the-field-to-uber”; may need google-translate for reading it in English)

Ha, that’s funny. I read that thing months ago. It was published around Uber’s IPO. Hype, hype, hype.

Why would a profitable German car company in the middle of a very expensive transition to EVs pay $50 billion to buy a money-losing taxi operation? Well actually, they’d have to offer a premium, so they might have to pay $70 billion if they did it today.

VW, the German automaker with the largest market cap, is now worth about $100 billion. It would be nuts for VW to waste $70 billion on a money-losing cash-burning taxi operation.

Bayer bought Monsanto for a lot less — overpaid and got screwed massively. Germans don’t forget. This nonsense is fabricated by Wall Street hype organs trying to boost Uber’s stock price by hook or crook. No one should take this stuff seriously.

If I were VW I would stay away from most American business rackets after getting stabbed for a small violation of the arcane regulations when producing super efficient Diesel cars.

There are perfectly good cars rotting away in desert parking lots, and VW had to buy them back with an enormous fine to boot.

Maybe the goal for Uber is for it to own everything it touches, to ensure monopoly and price control. Uber Eats could buy all the restaurants everywhere and allow food only to be purchased through Uber Eats. The ride sharing service Uber could begin by purchasing all the airports and require all passengers to and from access only through Uber. Eventually it could own every conceivable starting point and destination everywhere and apply the same rule. Prices could be raised continuously and profits ensured. (sarc)

Can’t wait for Wolf’s article on SoftBank’s dismal results today. Incredibly the Nikkei reported,

“The Japanese investment giant recorded an operating loss of 704 billion yen ($6.46 billion) in the July-September quarter.

The loss compared with an operating loss of 48 billion yen forecast on average by four analysts…”

Who were these “analysts”? They obviously don’t read wolfstreet.com. You called it, Mr. Richter.

Apparently the insider stock lockup for UBER is expiring today or possibly already expired yesterday. Reports are not clear on the distinction. It may or may not mean that the shares are salable today, in other words.

“Shares of Uber Technologies Inc. UBER, -4.23% are down 3.1% in Wednesday morning trading after a lockup expiration that Wedbush analysts had said would result in more than $20 billion in stock, or 763 million shares, becoming available for sale.”

Venting my Spleen — I just read this article and would like to share with everyone — https://lfb.org/uber-ceo-says-murdering-a-guy-could-happen-to-anyone/