Despite startup millionaires, house & condo prices in San Francisco Bay Area and condo prices in New York fall from year ago. Seattle down again. Los Angeles barely up from year ago. Las Vegas loses steam, Phoenix, others running hot.

San Francisco Bay Area House Prices

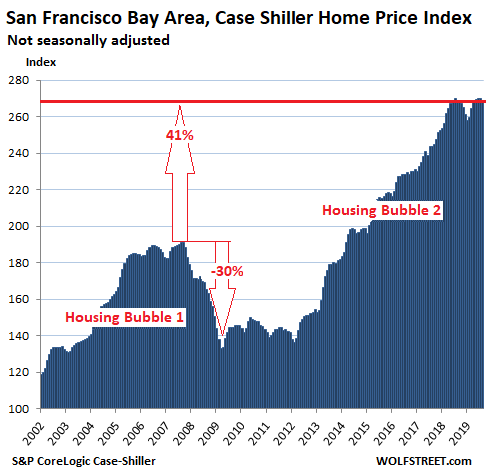

Prices of single-family houses in the five-county San Francisco Bay Area – the counties of San Francisco, San Mateo (northern part of Silicon Valley), Alameda and Contra Costa (East Bay), and Marin (North Bay) – fell 0.6% in August from July, were down 0.1% from August 2018, and were about flat with June 2018, according to the S&P CoreLogic Case-Shiller Home Price Index released today. It was the fourth month in six that prices were down year-over-year, the first year-over-year declines since April 2012.

In other words, despite the endlessly hyped job that the flood of IPO startup millionaires washing over the Bay Area would do to the housing market, house prices have been flat for 14 months, and have now formed a cute double-peak:

The Case-Shiller Index is a rolling three-month average. Today’s release represents closings that were entered into public records in June, July, and August. The index was set at 100 for January 2000. San Francisco’s index value of 281 means that prices have surged 181% since January 2000. Every one of the most splendid housing bubbles on this list has or had an index value of over 200, meaning that house prices have at least doubled, either during Housing Bubble 2 or during Housing Bubble 1.

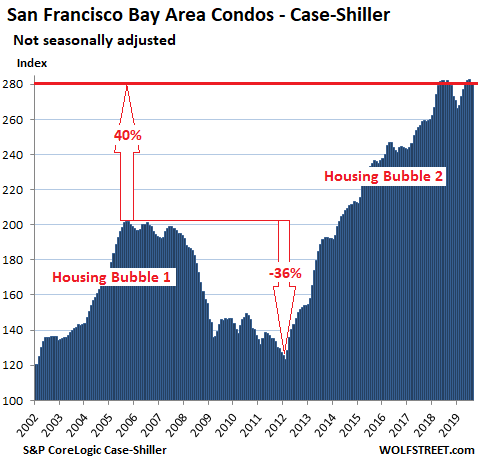

Condo prices in the San Francisco Bay Area also ticked down in August and fell 0.3% below the levels of August 2018, the fourth month of year-over-year declines in the past six months. Prices are now just a tad below where they’d been in May 2018:

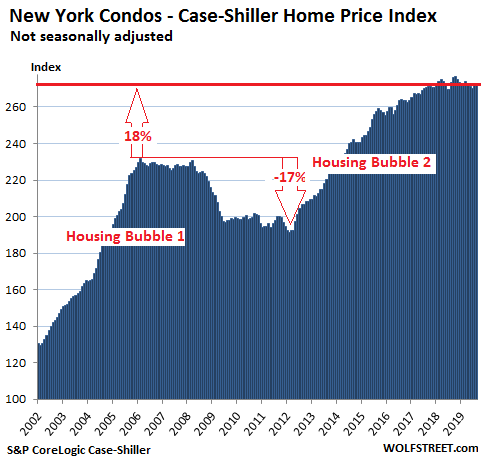

New York Condo Prices:

Condo prices in the vast New York City metro ticked up a smidgen in August compared to July, but fell 0.1% below the level of August 2018, and are roughly flat with January 2018:

While the Case-Shiller Index uses standard Metropolitan Statistical Areas for many of its city indices, its index for New York City is based on a custom area covering numerous counties in New York, New Jersey and Connecticut “with significant populations that commonly commute to New York City for employment purposes.”

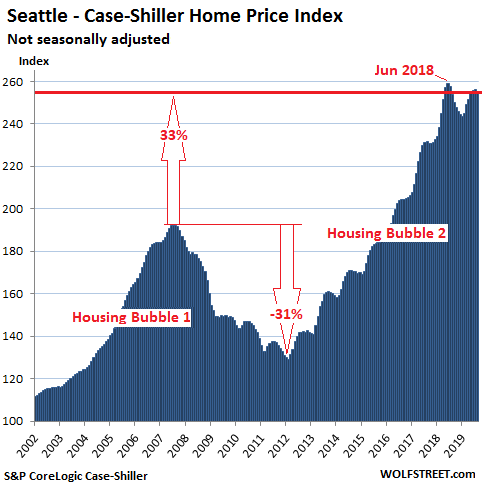

Seattle House Prices:

In the Seattle metro, prices of single-family houses declined 0.3% in August from July, but given the sharp 1.6% month-to-month drop in August 2018, the index was up 0.7% year-over-year. It is down 1.4% from the peak in June 2018:

The Case-Shiller Index uses “sales pairs,” comparing the sales price of a house in the current month to the price of the same house in the prior transaction, however many years ago that may have been (methodology). This makes the index immune to the problem of mix, which can skew “median price” indices, and the problem of a few big outliers that can skew “average price” indices.

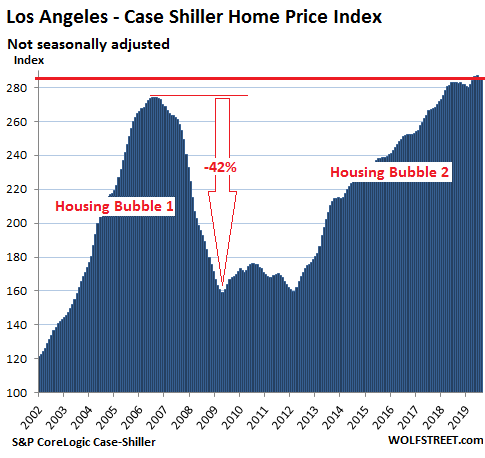

Los Angeles House Prices:

The Case-Shiller index for the Los Angeles metro was unchanged in August compared to July, which whittled down its year-over-year gain to 1.0%. The index has been essentially flat for four months:

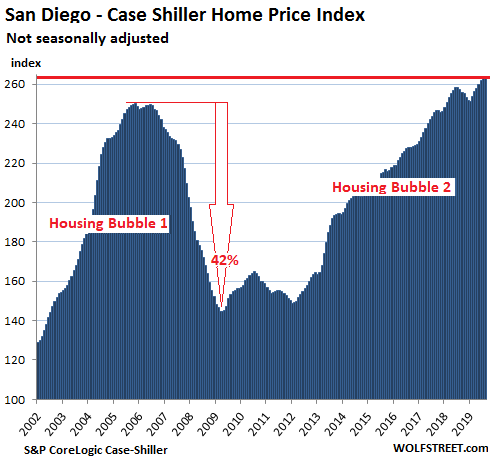

San Diego House Prices:

House prices in the San Diego metro fell 0.2% in August from July and were up 2.3% from August 2018:

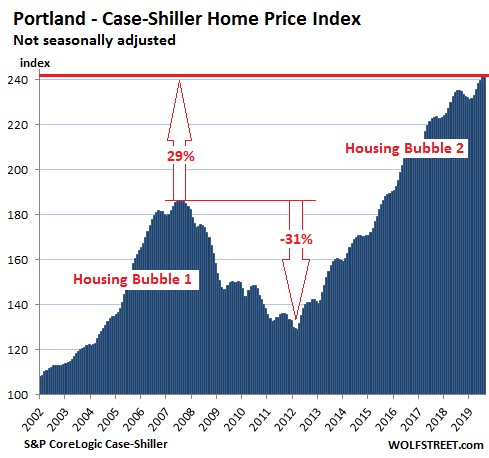

Portland House Prices:

In the Portland metro, house prices were flat in August compared to July, and were up 2.6% from August last year:

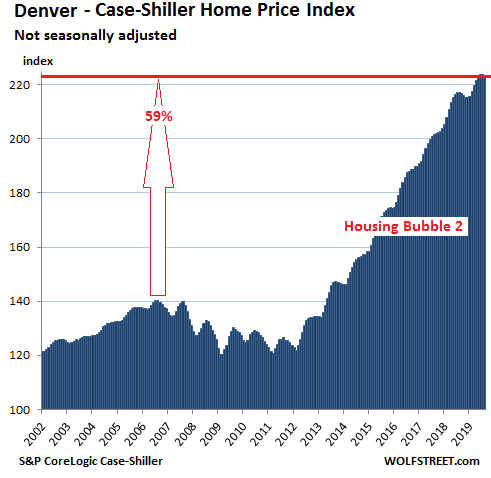

Denver House Prices:

House prices in the Denver metro declined 0.2% in August from July, which trimmed the year-over-year gain further to 2.9%, the smallest such gain since April 2012:

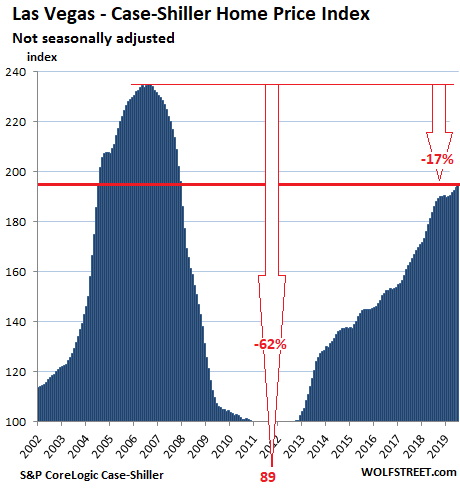

Las Vegas House Prices:

House prices in the Las Vegas metro declined 0.2% in August from July, which whittled down the year-over-year gain to 3.3%, the smallest such gain since August 2012, and was down from a series of double-digit gains from January 2019 back to October 2017. The index is 17% below the nutty peak of 2006:

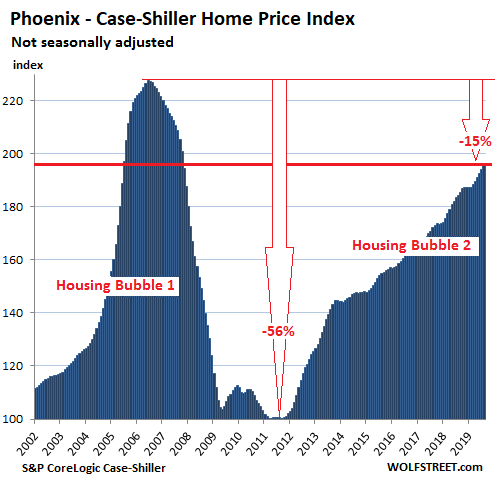

Phoenix House Prices:

House prices in the Phoenix metro rose 0.9% in August from July and were up 6.3% from last year, with a new housing bubble in full swing, though it remains 15% below the crazy peak of 2006:

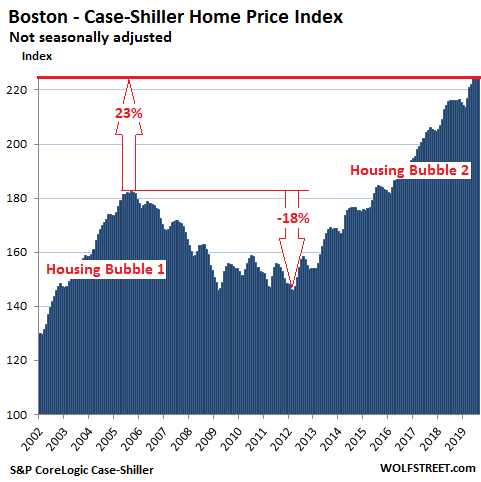

Boston House Prices:

House prices in the Boston metro ticked up 0.1% in August from July, which reduced their year-over-year gain to 3.0%:

Washington DC:

House prices in the Washington D.C. metro were flat in August compared to July and down a tad from June. Compared to August last year, house prices rose 2.8%:

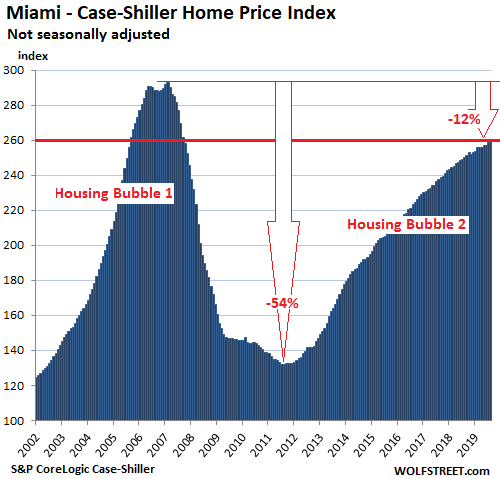

Miami House Prices:

In the Miami metro, house prices rose 0.3% in August from July and 3.6% year-over-year. They’re still down 12% from their dazzling craziness at the end of 2006:

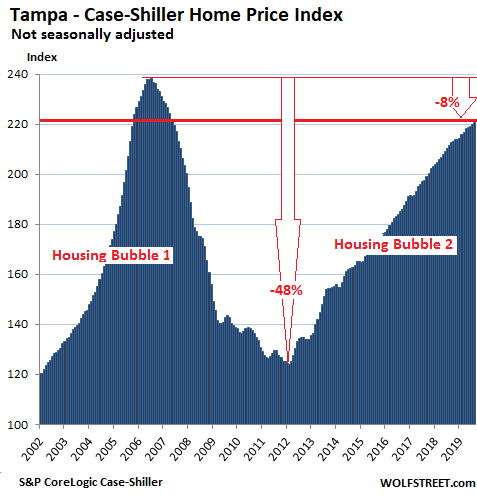

Tampa House Prices:

House prices in the Tampa metro rose 0.3% in August from July, which trimmed the year-over-year gain to 4.3%, the slowest such gain since August 2012. The index remains 8% below the crazy peak of 2006:

The Case-Shiller index, by comparing the sales price of a house in the current month to the price of the same house in the prior transaction, tracks the percentage increase of amount it takes to buy the same house over time. Thus, it tracks the purchasing power of the dollar with regards to houses in various markets, which makes it a measure of “house-price inflation,” which is what is depicted in the charts above because the houses didn’t double in size or become twice as opulent. But the dollar lost its purchasing power with regards to houses, and that’s what is happening here.

By the measure of median prices, ironically, house prices in the Bay Area dropped the most in Silicon Valley. Read... Housing Bubble in Silicon Valley & San Francisco Bay Area Turns to Bust Despite Low Mortgage Rates & Startup Millionaires

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

What happened to the Dallas chart?

Dallas doesn’t fit the bubble narrative so Wolf doesn’t publish the chart.

Please feel free to find analysis somewhere else where I am sure you will like the news better…

I have tremendous respect for Wolf’s analysis. I was being snarky. Are you Wolf’s groupie? If he didn’t like my comment he didn’t have to publish it. I appreciate that Wolf can take a good ribbing without getting his feelings hurt. So let’s leave it to him to moderate the comments and you can mind your own business as to where I can find my analysis.

Chris from Dallas,

Dallas is in the second part of the series, called something like “from the not-so-splendid housing bubbles to crushed markets” — tomorrow (well today, Wed). Includes Chicago, Detroit, Dallas, etc.

I think a more interesting information would be relation of property taxes to losses gains.

How did the tax obligation change as a function of relative value, my experience is when values go down -40%, property taxes stayed the same or went up.

More&More people I know are at retirement age, but its clear to me they can’t stay in their Pacific NW house, where the tax payments is $1k/month rent ($12k/yr tax on homes assessed at $1M), no point of ownership, if your tax payments are near rental value.

I’m not sure how many people flip anymore, I mean that’s how I got rich 70’s to 2010 was buying cheap fixers and turning them into rentals, until I had a huge asset base on 15% fixed, was paid out before 2001, but I sold out at both the peaks you mention in the charts.

My concern is friends & family facing retirement no income, and not seeing these huge tax payments for what they are. RENTING your home from the GOV.

I know I could NOT get rich today as a ‘fixer’, now the kids are more likely to turn your place into a micro-website hotel and fill the closets with tenants, meaning 100’s of occupants instead of two. Not counting officials have far more control of tenant law than say 30 years ago. Rent Control comes and you the owner becomes a slave to the property, got to sell & run long before rent-control. By that I mean, you can’t get rid of bad tenants once rent-control goes into effect, which means your property loses all value.

What is the meaning? Of all this? Many people I know in California want to go live in LV, cuz of the cheap housing, but little to they know of the future water/hydro/power problems ( lakes are dry )

IMHO the only good place to be in the USA, is not to be there :(

The migration of people is the natural process to rebalance the economy. Because it’s a disruptive event, it takes time for people to say it’s better in another city in another state. You see it with Detroit and Baltimore slowly bleeding off people and Nashville and Raleigh booming.

By the way, what is happening to drive Denver housing?

A lot of companies have moved to Denver and brought jobs. We have our own little tech center and people like the mountains, the increasing population has a bit of a feedback cycle because there has been a lot of jobs just to meet the massive demand increase for new hospitals, larger water treatment plants for instance etc. Unemployment has been low for a long time in the larger Denver metro area and I’ve met plenty of people who have moved here from other states where they struggled to find jobs but found one in the Denver area easily. Unfortunately, like many of these boom cities housing speculation is a factor in driving up cost, but largely it’s just good old fashion demand. Supply has struggled to increase as well because in a lot of surrounding cities the utility systems are maxed to capacity and local residents are angry about rapid population growth so restrictive zoning laws are heavily supported. However, people keep coming in as they get jobs here so prices keep going up.

I moved to Denver from the Bay Area 20 years ago. Colorado has a sunny climate with cold winters and lots of recreational assets (mountain variety). It’s one of the best educated states and has always been a magnet for Midwestern types looking for better weather, but more recently it’s become a back office Mecca for tech companies because the living here is good and far cheaper than the Bay Area. Same reasons that Nashville and Raleigh are booming really, just with a western twist, large livable city with decent weather and fun things to do, with an educated population that supports knowledge industry. Same thing is happening in Salt Lake City on a smaller scale. If you haven’t lived here, the thing about the weather that is hard to appreciate is that it is a very sunny climate even with the cold. People from elsewhere imagine this frigid ski resort place, but the thing that makes it a great place is the sun and the mountains. And summer is amazing, warm and dry, far better summer climate than anywhere outside of coastal California or the PNW.

Used to be also a good place to retire or move away from high tax locales, but changing politically so that long term, Colorado will probably not be a low tax locale. That has been part of the appeal for retiree types leaving CA. I think those people move to AZ and NV more often because they don’t have a real winter there. The majority of the migration is younger people looking for the good life. Hard to find that in the Bay Area unless you have several million dollars.

Also a small number of people moved here for legal pot, but everywhere else is catching up on that quickly.

Does weather really make that much of a difference where people live? I’ve lived all over the place and came to the conclusion that weather is weather. Sometimes good, sometimes bad, no matter where you are. Maybe San Diego is the exception as it’s damn neat perfect every time I’m there.

I’m an avid skier. Denver on paper sounds appealing if you’re into skiing. But the resorts are 2 hours away in clogged traffic. SLC on the other hand is less than an hour to (IMO anyway) much better snow and better overall skiing. I’ve flown into SLC on a Saturday morning and was at Snowbird before the first chair opened. It’s that close. Live on the SE part of town and it’s a 1/2 hour.

But the downside to both SLC and Denver is no ocean anywhere. I’ve lived within a day’s drive to an ocean my entire life. I’d hate to not have that. I know, sounds kinda weird, but I need my beach man!! And it’s also windy AF in Denver. I hate, hate, hate, hate wind. Give me cold, give me humid, give me rain, give me anything over wind.

Anywhere you live you’ll have pros and cons. Florida has the beach but also hurricanes. SF has the mild winters, but rain/fog/wind. Pick any spot on the map and you’ll have both good and weather wise.

Denver missed out on housing bubble one. Denver was more conservative than it is now. The pattern of declining values across the SW is interesting. The one common denominator is Colorado River water. The Ogallala aquifer (which is drying up) also feeds OK and TX. Apparently water is not a renewable resource. Prefer living near the ocean, while the West Coast is part of the Pacific Rim. Trade and goods come through here, is the global economy slowing? Is it secular?

The problem I have with flyover country is that for me, it’d be more expensive than California. Rooms to rent are 80% – 100% – 120% the price, but the min. wage is half as much. And if jobs are hard to get in CA, they’re even harder to get in flyover country.

Saul,

Great insight that higher property taxes are a form of property confiscation. I have long been of the view we really don’t own anything outright in America anymore.

I just heard a CA guy say the insurance companies are starting to pull out of fire insurance coverage in CA. If this is the case, lenders will not lend for un-insurable properties. This will lead to a huge decline in prices in the CA markets where this happens.

If fire insurance simply rises substantially, it will still lead to decreases in affordability, more price declines and more displacement.

Ditto for flood insurance, hurricane and high wind insurance. Will property values decline as semi-arid coastal areas become fully arid as water shortages turn landscapes into rockscapes?

My homeowners policy on my Sag Harbor NY cottage went from 2k a year to 4 in one fell swoop back in 2014 Never had a claim in 30 years Sold the house DONE Taxes were high as well nearly 10k a year for a 1500 sf cottage on a quarter acre Crazy The taxes on my very nice centrally located apartment in Warsaw Poland are around 300 dollars a year

I have a nephew in the Mortgage Business in the PNW. Apparently, he has numerous clients who have alreasdy relocated from CA due to the stress and fear of fire threat. Insurance limitations or rising premiums will seal the deal for many.

A big question for me is PG&E and this ongoing natural result of privatised utilities. Deferred maint and infrastructure upgrades for increased shareholder returns meets climate change and unknown events. Homeowners and taxpayers will pay the price for sure.

My nephew in Novato phoned my sister the other day and told her not to worry as he would have no cell phone coverage for awhile and their power was also being shut off for several days. Imagine, cell phones not working just when people need them most. Many make jokes about Govt bailouts and bail ins. If the truth be told, in this overly complex world the Govt, any Govt, may be incapable of saving the day. I wouldn’t expect or rely on it for security, or economic fixes.

PG&E was not privatized, it was always private.

However, the it was sensibly and heavily regulated (as a natural monopoly/line industry).

The regulation then got crazy: fixed prices => bankruptcy#1. Lack of maintenance and prevented maintenance (! by misinformed environmentalists)=> bankruptcy#2. Also, basic incompetence of PG&E management (they were/are? very arrogant).

I knew a PG&E management/engineer back in the day. They thought the whole state revolved around them.

It takes a village to cause such a mess.

@wkevinw –

PG&E BK#1 was purely Enron. Fixed retail prices were only a boat anchor because Enron was scamming the input costs.

Agree CA power infrastructure (including PG&E) has NOT been sensibly regulated, or Enron would never have happened, line maintenance would have been properly managed, deployment of overhead lines into unsustainable high-cost / high-risk service areas would have been prevented, and so on.

Can’t entirely blame PG&E for doing what corporations do, the regulation is supposed to balance that out. Blame the corrupt schmucks in government for regulatory nonfeasance … and the voters for not caring enough to clear out the corrupt schmucks.

It’s basically a feudal set-up: you may ‘own’, but neglect to pay non-negotiable fees to the lord of the manor and……

Really a very primitive system of taxation, and not suited at all to an economy in decline; unless you are one of those benefiting from the squeezing of the lemon – retired public sector, etc.

I was listening to an interview of Morris Berman, the “Why America Failed” guy, and he talked about how people in other countries don’t pay these insane property taxes. Some little guy in the US paying $10k a year on their little shack is just as weird and US-only as the same guy going bankrupt and homeless because of a medical problem.

The message here: Get out!

Petunia, it’s happening all over CA. I’m in San Diego and since the local West Fire last year (about 20 high cost homes lost) insurance companies have raised their prices significantly.

My neighbor has a modest home valued at about $475K. She told me last week her fire insurance went up and is now $5,000 a year. I know another family in the rural part of the county that is paying $7,000 Annually to insure a much nicer home.

On top of already expensive mortgages, taxes, gas at over $4.00/gal I don’t think this is sustainable. Luckily my house is paid off so I’m in relatively good shape. I pity the young folks today just starting out in life!

Alex in San Jose:

So, who pays for all the infrastructure including roads, schools, energy delivery, etc……????

The money has to come from somewhere.

Nothing is “free”……..somebody always pays.

To others who have commented about PG&E power shutdowns and the property insurance fiasco….I’m smack dab in the middle of all this.

Yes, most all insurance companies are pulling out of direct fire coverage of property in the “hi-risk” areas. They will insure your property for most everything except fire. You will have to turn to “two coverages”. One for non fire (regular insurance companies) and the fire coverage to what is known as, “California Fair Plan”. Subsidized coverage. And, your policy costs will increase dramatically sometimes even more than doubling. And, of course it will effect property sales, county revenues etc.

PG&E used to be a more strictly regulated utility back in the day. Ever since the emergence of more and more deregulation became the mantra of the financial/political world it has not been under such scrutiny. The CPUC (Ca. Public Utility Commission) has not exercised enough oversight. Just as in the GFC the SEC had contributed to much of the mess by not exercising it’s oversight responsibilities.

Shutting off power according to PG&E’s plans has plunged this state where this is happening to lots of despair. So many parts of the areas of the shutdowns involve older retired and dependent individuals. I suspect more will die from the cold exposure, poor access to medical care and just plain depression and panic resulting from these traumatic experiences.

PG&E kiting it’s own stock and proven neglect of infrastructure upgrades/repairs over the decades are all the responsibilities of upper management. I say they have failed abysmally. I’ll stop here because this post is long enough.

If they lived literally next door to brush and forests.. then yeah… but homes a few streets away won’t see their costs rise until the homes across the street burn down and they are the new front line.

Dude, like 5 homes were destroyed this year… out of millions… they can eat those losses easily.

Clueless millennial here who works a full time job and somehow owns a cheap home in our area ($1.4 million), I have a serious question because we live in a high property tax state…during a recession when there is a shrinking tax base, do they increase taxes in other areas? Property taxes, even if home values go down? What about federal and state income taxes. I think all I do is work to pay my income to taxes, commuting and childcare.

Your property taxes will never go down.

Every penny has been spent and earmarked for insane public union benefits, salaries and pensions.

Even if your house price crashes, you will not get lower property taxes.

It is for the children.

The property valuation for property tax purposes is just a means of allocating your share of the budget. When values go down the rate goes up and vice-versa.

Alison,

For the sake of your family, get the hell out of there. There are plenty of places where an income under 100K goes a long way, with shorter commutes and more time with your family. I left NYC in the 90’s and still don’t miss it.

Re: property taxes in real estate collapse.

I was in south FL when the real estate prices collapsed. Some counties in south FL have portable tax basis where you can trade up but still contain the rate of increase of the new property to about 3% a year. So it takes a while for the new property to get to full assessment.

Real estate prices did drop but not by much when properties were reassessed down. I think the 3% a year cap on rate of increase goes both ways, up and down.

Solution MOVE there’s a great big world out there

I have a beautiful home on San Juan Island and my property taxes are only $200/month.

Moderate property taxes (and/or some other form of carrying cost) are essential to ensure that property is put to productive uses and not simply idled. Otherwise you get “investors” wasting land and resources on vacant cities filled with see-through buildings (hello, China).

But a lot of property taxation is far from moderate. And some is rigged to be completely unfair, sometimes in ways that would have the Founders up in arms all over again.

Agreed, but you don’t have to overtax everybody just so you can punish some Chinese investors who want to keep their property vacant. You can make a law to target that kind of behavior, no collective punishment is needed.

The thing is real estate tax is the easiest to collect and hardest to avoid so taxes will be going up, and all you have to do is shut up and pay.

A couple of thoughts:

It’s kind of amazing that looking back at the bubble bursting a lot of people got a 50% haircut on their house and 50% on their 401k at the same time. No wonder the Fed tried to reflate with the wealth affect.

Is where we are at right now where the Fed wanted us to be? Housing bubble and stock bubble reflated. Seems like the Fed’s goal is to try to maintain asset prices about where they are by carefully trying to jiggle monetary policy.

If I remember correctly the consumer has not returned to his debt level height due to poor household formation. That probably tells you who got hit the worst by Fed policy. The young with no assets. Today housing and stocks are very expensive compared to wages.

Final thought is the current asset bubble is all built on Fed and fiscal policy being nearly maxed out in the eleventh inning of the ball game. We were in bottom of ninth, but tax cuts got us a couple of extra innings.

My house in SW Floriduh sold for 60% less about two years after I vacated and I was on a beach with a canal. Inland there were 80% drops all over. I sold in summer of 2005 which turned out to be good timing.

I expected boomers to retire en masse in 2012 based on demographics when I bought in ’96. To my surprise that never happened and they couldn’t retire. In 2007 when it became apparent that FL houses went hard bust I looked into the actual wealth of that generation and it was comprised of 2/3 real estate. I can’t remember the amount of liquid assets but it was shockingly low and not enough for a two person household in a big house to last long enough to not die poor.

That house bubble and the next were both due to financial engineering, primarily with Fed interest rates that were set far below the risks associated with the underlying asset creating massive distortions that persist.

I can’t even guess when demographics (or incomes) will factor into real estate demand and prices after the last 20 years of engineered prices but one thing is certain; we all die. I foresee a “liquidity crisis” looming for elderly (looking at you booomy) who need to finance their consumption and tax burdens that will only grow out of control in all the popular cities along with cost of living and medical necessities.

There is going to be hell to pay in the housing market eventually based in the income mismatch alone. There could be massive inflation with continued wage deflation, saving house prices but making affordability worse.

So, what prevails? Demographics, affordability, or fiat financial engineering?

All three seem stretched too the limit.

Old School. I mean boomer in the cosmic sense, not personally. I’m old genx so not that far removed. It’s more of a mentality that encompasses cultural changes.

Only mention because I don’t want to start a descending spiral of generational gripes among commenters and after reading my comment I didn’t want you to take me the wrong way. I appreciate your comments.

I expected these figures to get much worse in California as the fallout from the wildfires and the current electrical power debacle becomes apparent. Numerous people without power, internet and even cell service with these outages dragging on in some cases for almost a week. This is third world stuff. I’ve heard many reports of lifelong Californians fleeing to Idaho. How can a business survive in this environment? The Governor blames PG&E. Throwing stones from a glass house.

I would like to see an in depth story on the wildfires, the utilities and the public regulation. In some ways the utility is directed by the public utility commission. Has the public utility been making requests for more aggressive tree removal program only to be denied by public utility commission. I think it’s about a 50 / 50 shared responsibility of blame without knowing facts.

Yes, I know a guy that moved to Idaho and he said there are lots of retired Cali gubbermint workers like police and firemen in his area. My duddies have moved to Washington, Montana and Colorado. Anotehr moved to outside Reno, but that was to follow his GF. Not mentioned yet is the 405-Freeway was open yesterday, but many offramps were closed. The Hollywood Freeway was closed due to police activity on an overpass (jumper?). What a mess. I had to drive through LA yesterday heading north and was out the door by 4:15am. I am still tired today, and al so I can pay taxes out the ass and $4/Gl gasoline. Wait until the water restrictions bite. We are looking, but I will keep a place here. Too many have left and are unable to come back

Yes, Idaho is full of rugged individualists who migrated from CA with their fat gubbmint pensions and hate socialism.

Shhhh! Repeat after me, Idaho sucks, don’t move here…..

Rural AZ the same; I lived out there and everyone’s on welfare, it’s hilarious, just as you describe. They hate Socialism but the running joke is that if you live in X area which may or may not be Chino Valley, you have your “ID card” which is an EBT card. And they all foam at the mouth about “socialism”.

Unless-N-Until the government starts accurately gauging

the inflation rate of the inner-city poor who are

increasingly being put out on Seattle’s streets,

the bad option will be keeping short-term rates at Zero,

and the worse option will be housing them, gratis.

Treat these people poorly, and they will bite your ass.

I don’t understand why we can’t turn the clocks back 1/2 hour on Sunday and leave them there.

But Berkshire Hathaway on the continued retreat of property insurers from risk. Why raise rates when you can stop taking the bet entirely.

Ahh. Uncle Warren, who rode the demographic wave up with GEICO, deciding to pull the plug now?

How would that serve the purpose of showing how much the gvmnt can jerk you around?

If you visit wine country and the North Bay area, and you look up at all the power lines, the problem becomes very obvious, dilapidated power lines and poles and equipment everywhere, lines draped over tree branches everywhere, a complete and total mess. It is a massive problem, and it would take a huge force of people and equipment (and cooperation from land owners) to fix it. Even if this was started, the problem is so massive and wide spread it would take a decade to fix it. Watching the blue PG&E trucks cutting a few tree limbs away from the power lines here and there makes me laugh. The attempts so far are hopeless. The economic and personal costs being shouldered now by the good people of Sonoma County are huge. It is unlikely we will see a solid plan from the county or state to fix it.

All electrical lines must be buried underground as is the case in most developed countries, not only are they a terrible eyesore but a public hazard too. Problem is California is run by a bunch of incompetent bureaucrats.

They fly the Transmission lines with LiDAR twice a year. Do an analysis and any tree or limb that is with a set distance based on the kV is trimmed or removed. That’s been going on for about 4 years now.

The tree “mess” you are seeing in landowner that are refusing to allow PG&E to cut or remove the trees. Or dumb Tree Municipal Tree Ordinances.

Everything within their know Right-of-Way or Easements is removed.

Say a tree is 120-ft tall and totally dead, but the easement is only 50-ft wide. They need landowner permission to remove that tree. There is database they maintain of “refusals” and it’s massive. Entire cities and counties will be on the refusals list. Palo Alto, Burlingame to name a few.

Also, PG&E doesn’t own any bucket trucks for tree trimming, it’s 100% contracted out. If you see a blue bucket truck, it’s because that is a Lineman doing work.

Hope that helps.

I can see into some of the backyards in Palo Alto and Atherton when I take the CalTrain and ride on the upper deck, and there’s a real “Grey Gardens” vibe going on there.

Bottom line is that disaster is profitable. Do you know how much FEMA money is poured into disaster areas? I used to work for a utility and was involved in a couple of firestorms and I can tell you the money I made during those disasters was obscene. Imagine doubling your wages, then double them again for the 16hr days and multiply that for 4 or 5 weeks.

That is what everyone involved in disasters looks forward to. While some lose everything, others profit hugely. The problem is, some of those who profit, are also the ones who are tasked with preventing the disaster to begin with…..

Interesting, you could hand a child those graphs and some crayons and the little fella could finish them for you. And of course he wouldn’t be saying but, but , but……. Good work Wolf, appreciate you.

Everett: LOL! As anybody who has raised kids can tell you, the little guy, with crayons, would be saying “Why?” “Why?” “Why?” !!!!

And the more you try to explain, the more “Why’s?” he will keep saying!

Once you deep dive down to the molecular level driven by “Why?” to the nt degree, you will finally give up trying to explain what can’t be explained!

The joy of kids!

My community has a Facebook page. A Florida lady had her home insurance cancelled at the start of hurricane season. Home insurance costs are higher here. Auto insurance is higher as hurricanes dented cars. It seemed to me like bubble prices have been forming as housing prices rose faster than income, however mortgage rates are lower than any decade I can remember.

Private insurance is a scam. The only reason I carry fire insurance is that my lender requires it, otherwise I will never by one, the probability of fire where I live is so small that it makes more sense to insure against some ufo falling from the sky and damaging my roof than fire.

I would only buy insurance if the insurance company was non profit and all premium money not used at the end of the year was refunded back to members.

You old socialist you.

BTW, extraterrestrial UFOs do not exist, so you should be able to get UFO insurance for very reasonable rates.

Actually, UFO just means “unidentified flying object” and can be any, well, flying object that you … can’t identify. Meteors certainly qualify and once in a great while one damages a house.

Water follows money, there is almost no chance of large wealthy western cities in the US running out of water. Read “Cadillac Desert” for the full story.

I guess you’re not familiar with the Anasazi, or all the other Puebloan Indigenous Tribes that had their civilizations collapse over the millennia due to southwestern & western droughts lasting 500+ years or more.

I don’t think the tribes had de-desalination and pipelines, or water treatment plants.

Relatively speaking, neither does CA.

Infrastructure always lags development by decades because it’s expensive and everybody thinks the government should pay for it, and not taxpayers.

Great article. Lots of nice graphs. But I have no idea how to digest this news? Only that house prices are going down. Maybe my sons can afford them after a few years of price decreases.

What else is happening? Tomorrow the Fed will report its balance sheet.

I calculate that Repo will print 215.5 billion in the balance sheet. But the real story is the Fed actually went through 482.084 billion that week ending Oct 30. In addition the Fed bought 15.002 billion in T bills.

Only one day (Wed) of the overnight repo will end up in the balance sheet. The rest (Mon, Tue, Thu, Fri) will expire and not hit the balance sheet. The term repos will hit the balance sheet. So if you are looking at the balance sheet to tell you the whole truth, then look again.

So half a trillion dollars was used this week. Does it shock you anymore?

Considering 85B a month for QE, yeah it is pretty shocking. QE is forever, but Repo is like a swarm of cyber mayflies. It is perilously close to a direct monetization of spending, and is a hit to our credit rating which in turn fuels selling in bonds, and a self reinforcing cycle. Debt paper loses value, requires more of it service the debt. One thinks intuitively that another rate hike would NOT be a surprise. That would keep a bid under the buck, foreign investment liquidity and make this shell game to pay the rent less obvious.

What it means for housing? The banks will have to cut a deal on mortgages and eat the profits they hoped to gain on a steepening yield curve. Gawd I hate the banks.

By any objective measure, would it have been better to rent for the past 10 years or invest in real estate?

What about 20 years? 30? 40?

The answer is no.

You just elucidated the reason that renting going forward might be a good idea.

Short term. Maybe, maybe not. Long term, probably not.

Renting is almost never a good idea when it comes to a home for your family. Take i from an old man that has gone through many economic cycles.

Do yourself a favor and stop reading negative, end of the world is near internet blogs for investment advice. Reading such material is good for entertainment purposes only.

Any such blogger will have some inherent bias toward negative reporting as it attracts more readers. It is the same with the TV, no one will be watching but for the constant sensational bickering.

Do yourself a favor and stop reading negative, end of the world is near internet blogs for investment advice.

The world isn’t ending. In fact, I expect it will eventually recover.

The particular problem I think we have in the bay area is that homes are only fairly priced if they include a built-in return on investment. It makes no sense to buy anything around here unless you are going to get a reduction on the cost of ownership through significantly increased valuation later on when you go to sell it.

I can rent for $4,000 per month but it will cost me $7,500 per month to buy. I do not want to throw away $3,500 per month just for the good feels of owning instead of renting. So much of that $3,500 per month has to come back to me later in terms of profit when selling or else it won’t have been worth it.

Therefore, I cannot buy if I do not have strong confidence that the $7,500 per month home will increase in value by at least $36,000 per year on average over the next N years (I’m targeting around 7).

This is complicated a bit by the fact that that $7,500 per month isn’t *really* $7,500 … it’s more like $5,000 per month when you factor in the fact that some of it is principal so it’s not really money I’m spending, more money I’m putting into the savings account that is my house, and also tax write-offs, and also the lost opportunity cost of the large downpayment.

But in the end, when houses are this expensive and displace almost all of your investments, the house itself has to be a good investment. And when it looks like we are near the top of a bubble, or maybe even just a permanent leveling off, it becomes very hard to justify the financial risk of buying a home in the bay area.

Location, location, location. Yours is such a blanket statement on renting vs buying it is meaningless.

Yes Wolf great article as usual. If you look at the whole, a pattern forms. Basically, no matter where one lives, municipalities and insurance co. are strapped or worried about being strapped for cash in the coming years, so property taxes and fees are rising. I rent but I’ve noticed my friends who “own” homes are getting strapped to the max with property taxes. Here in TX the governor is attempting to pass a bill to corral/limit the cities and county’s ability to increase property taxes by greatly “increasing said Value” of a property in one year. Houses in Little Elm and Aubrey that just 5 years ago were at 140,000 to 185,000 are now “valued” (taxed) at 285,000 to 370,000. So the taxes these folks now pay rose from 2000 to 8500 or more. These are NOT McMansions, these are 1600 to 2000 sq ft homes. Texas has no state income tax but it taxes its citizens to death through increasingly rising property taxes. It’s why as I approach retirement, I’m thinking I may have to move to a state with low property taxes in order to keep from being taxed out of a home. I look forward to your Part 2 with Dallas.

The Texas legislature doesn’t meet again until 2021.

There is already a law that limits taxable value of a homesteaded property to a maximum increase of 10% per year.

You do realize that is 100% in 10 years…. right?

Happy,

Yes “Water does follow money.” but what is money?

I’ve read “CAdilacc Desert,” a good read about how LA and politicos

siphoned off water from the Colorado river, along with AZ to not only provide water to LA homies, but mostly forlarge agri farms!

The book also gets into the total inefficiencies and screw ups of the

US Army Corp sof Engineers providing water to farmers to grow hay to

raise beef, a very inefficient and IMHO non-sustainable business model.

But that said…you are I think sadly misinformedabout water, a vital resource which is becoming less and less available in the West & the world.

You mentioned the connection between $ and H20.

What are you going to do when the US dollar is no longer the World’s Reserve Currency? What are you ogoing to do when the SHTF?

Do you really think all the folks in the city out West will be able to “buy their way” out of a water shortage or break down in the delivery and purification water systems?

You had best think again and check out Peak Prosperity.com and start to wrap your head around sustainability and how to create resiliency.

You could always just pick up sticks and park you mobile home at Slab City

Looking at SF Bay Area houses and condos, I’m wondering if we are going down the same road as the Toronto Metro Area (see Wolf piece on the Canadian housing bubbles) where prices fluctuate up and down near the peak? Has the dynamics of the housing market changed where the new norm is somewhere around these peaks given that we all might be heading toward negative interest rates? Or would a bout of job losses like we had in the Great Recession be the spark that causes these bubble to deflate, all but slowly, in a significant way.

When the .com bubble burst, real estate in SF dropped by 10%. Tons of jobs lost and real estate market barely noticed. And this was after prices doubled in the 90s.

There are some cities where it’s really expensive to live. New York, London, Paris, Tokyo, etc. Hoping to buy a cheap house/apartment in one of these cities is a fool’s errand.

Sure prices may fall a little here and there (before ramping up again). But all that means is the 50 year old 1100 sq ft house costs $1.6M instead of $1.8M. And 10 years from now it’ll be $2.5M. The same pattern has held true from the 80s on.

There is a limit. House prices cannot increase faster than wage increases forever. I suppose what happens is that the home-owning class becomes a smaller and smaller part of the population, mostly people who bought in long ago or are super wealthy. The rest being renters. The back pressure on this is how much less people view the bay area as a good place to live when you know you have no hope of ever owning a home.

Right now until proven otherwise I am going to assume we’ve hit the permanent peak (increasing prices from here on out being only at the rate of inflation) that Shawn describes until something convinces me otherwise.

“I suppose what happens is that the home-owning class becomes a smaller and smaller part of the population,”

Precisely, this is what is happening in San Francisco. 22% I think and of that a good chunk of that is bought by big investors.

One thing that is notable about the housing bubble graphs Wolfe has shown us, is how different areas of the country are affected differently.

The reflation of the housing bubble by the Fed has been very uneven.

Some areas have been grossly over inflated while other areas have hardly felt the the surge in money supply at all.

Beware the day when the fed cuts rates……and the markets drop instead of rallying.

I welcome that day… I love recessions, it is when I am able to buy everything I want on sale…..

Happy days are here again because they never ended and never will so long as the Fed’s Inflation Fraud Report is fraudulated like it is:

“I think we would need to see a really significant move up in inflation that’s persistent before we even consider raising rates to address inflation concerns.”

(well, not counting asset inflation)

Jerome Powell, Chairman of the Super Ultra Dove Deluxes.

Dat Fed don’t see no inflations, so there don’t be no inflations to see.

I wonder how much of the rise in prices is due to the depreciation of the US Dollar? We did print like $3 Trillion of them buying up the bad assets from 2008 and a 2% interest rate peg since 2008 is more than a 10% devaluation in the US Dollar by itself.

NoCrazies,

“I wonder how much of the rise in prices is due to the depreciation of the US Dollar?”

All of it, or nearly all of it, as explained in paragraph under the last chart (Tampa). It’s called “house price inflation.” It takes more dollars to buy the same house — means the dollar is losing its purchasing power with regards to houses. That’s what is going on here. Then there are periods when the dollar gains purchasing power with regards to houses, namely during the housing bust.

Most of it. The official 2% inflation is just fodder for the ignorant masses…

Yeah, house prices are up 100% in the last 10 years but they fell 0.2% this year, time to go and get a great deal on that million dollar shack.

This is probably true for the rest of the world also. I don’t think there is anywhere to hide. As I age, I just give my kids more and more. At least, I want them to have a house (with less debt) – something I am able to enjoy.

The prices rose ~100 percent in the last few year.. IN most of the places prices still going up albeit slowly.. in some places, it went down tiny bit.. inventory still low.. housing market still hot..

how is this a news.. I am just trying to understand,

I’d be attentive if it drops by 10% or so.. don’t see this happening..

The 2017 fires in Sonoma County destroyed a large number of homes and prices jumped big time in all price tiers.

2019 is different, only (!) about 100 homes destroyed, but a big change in attitude.

People are now accepting that fires like this are the new normal, and in a market already beginning to see price declines…

I expect the declines to happen a bit faster than they would have otherwise.

If Sonoma County = Wildfires in peoples minds it will have a long term and significant effect on the market here.

It doesn’t matter that the Sierras are a tinderbox from one end to the other, or that many other cities and towns are at similar risk.

If Sonoma County = Fires we’ll see some genuinely affordable housing again in just a few years.

Disclosure, I am a Licensed Real Estate Broker in Sonoma County and the opinion expressed above is solely my own.

You are seeing declines because the demand for housing in CA is declining along with the population. The fact is that liberal politics have had a negitive effect on living standards in CA and people are leaving, at least the productive ones who have the choise. They are being replaced in large part by the unproductive people who are attracted to liberal welfare programs that benifit the unproductive. CA will follow the path already blazed by the liberal crapholes from which most of CA inhabitants fled to begin with….

They are being replaced in large part by the unproductive people who are attracted to liberal welfare programs that benifit the unproductive.

Dang them cripples and orphans and old people. The sooner sensible tycoons have ’em starving in the streets, the better.

There but for the grace of God goes jdog…except not to CA, apparently.

The only thing making people leave is housing prices. All the rest of it (including wildfires) are just news headlines. Yes, a few people will leave for that reason, but not many.

And high housing prices are a consequence of the state being a very desirable place to live.

In short: people are leaving because the “liberal politics” have done *too good* of a job, not too bad of one.

Actually, to be honest, I think politics have little to do it with it, it’s more economic and environmental factors that are only minorly affected by politics. But if you want to argue any political angle on this, then you’re just wrong, because whatever CA has been doing, has led to the problems caused by *too much success*, not too little.