Meanwhile, the Fed relentlessly sheds MBS, replacing them with Treasuries, including short-term Bills.

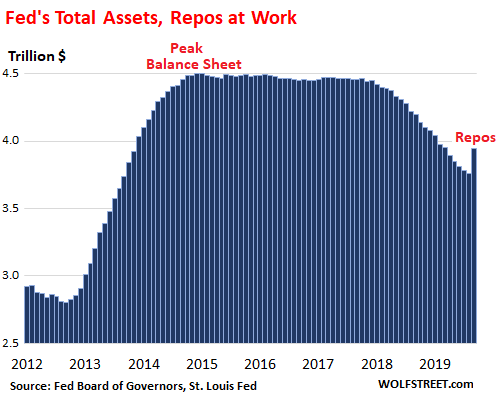

Total assets on the Fed’s balance sheet jumped by $184 billion over the past month through October 2, to $3.95 trillion, according to the Fed’s balance sheet released Thursday afternoon. This increase was mainly a result of the New York Fed’s repo operations – particularly the three repo operations with 14-day maturities that will all unwind next week:

The New York Fed used to conduct repo operations routinely as its standard way of controlling short-term interest rates. When short-term rates spiked following the 9-11 attacks, the Fed responded with a burst of repos for six days, at which point short-term rates settled down, and those repos unwound. When Lehman and AIG collapsed in September 2008, the Fed switched from repo operations to emergency bailout loans, zero-interest-rate policy, QE, and other “tools.” Repos were no longer needed to control short-term rates and were halted. Then last month, as repo rates spiked, the New York Fed dusted off its trusty old repo tool.

The New York Fed currently engages in two types of repo operations: Overnight repurchase agreements that unwind the next business day; and 14-day repurchase agreements that unwind after 14 days.

The overnight repos on the Fed’s balance sheet for the week ending October 2 amounted to $42 billion. The Fed acquired those repos in the morning of October 2, and unwound on October 3. All prior overnight repos had already unwound before the date of the balance sheet and are gone.

Overnight repos are continuing. For example, this morning (Oct. 4), the Fed accepted $38.55 billion, meaning the Fed gave market participants $38.55 billion in cash, in return for securities: It bought $29.5 billion in Treasury securities and $9.05 billion in Mortgage Backed Securities backed by Government Sponsored Enterprises. The repurchase agreements specify that the sellers (such as banks) have to buy them back the next business day (Monday), which is when those repos will unwind. Overnight repurchase agreements, though they’re not legally loans, function like overnight loans.

The three 14-day repos amount to a total of $139 billion. All three will mature and unwind next week:

- 24: $30 billion, matures on Oct. 8

- Sep 26: $60 billion, matures Oct. 10

- Sep 27: $49 billion, matures Oct. 11

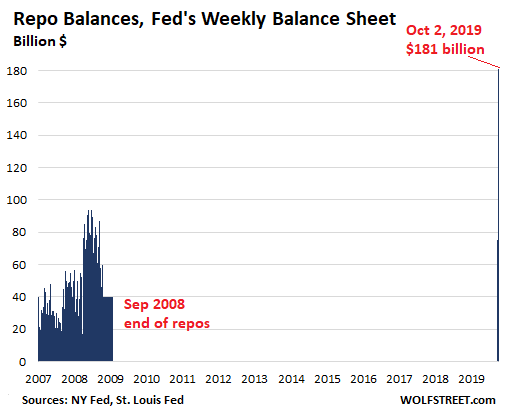

So, on the Fed’s balance sheet for the week ending October 2, there were four batches of repos: one batch of overnight repos totaling $42 billion that unwound on Oct. 3; and the three 14-day repos totaling $139 billion that will unwind next week. This is how the Fed’s balance sheet on October 2 ended up with $181 billion in repos.

This chart shows the balances of all repos maturing within 15 days – overnight and 14-day repos combined – on the Fed’s weekly balance sheets since 2007:

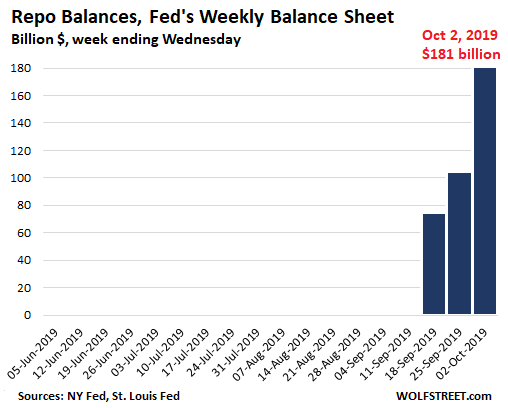

On the Fed’s balance sheet, these repo balances are carried in a separate account, called “repurchase agreements.” For more detail, this chart shows the same balances of repos maturing within 15 days but only for the Fed’s weekly balance sheets since June 2019:

Meanwhile, the MBS run-off continues and exceeds “cap” for fifth month in a row

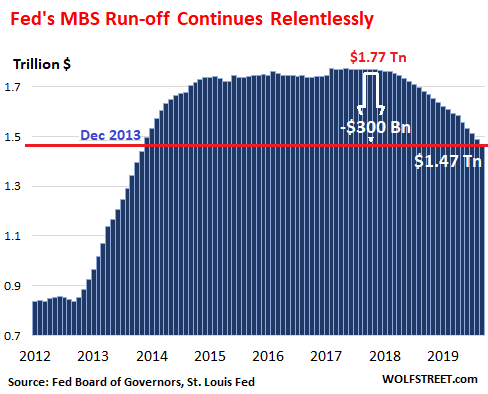

In September, the balance of Mortgage Backed Securities (MBS) from its QE program fell by $22 billion – exceeding the self-imposed cap of $20 billion per month for the fifth month in a row – to $1.47 trillion, below where it had first been in December 2013. Over the last five months, the Fed has shed $116 billion in MBS:

The Fed, like all holders of MBS, receives pass-through principal payments as the underlying mortgages are paid down through regular mortgage payments or are paid off when the home is sold or the mortgage is refinanced. About 95% of the MBS that the Fed holds mature in 10 years or more, and the runoff is nearly entirely due to pass-through principal payments.

Mortgage interest rates have fallen since November, which has triggered a surge in mortgage refinancings, and the pass-through principal payments to holders of MBS have surged as well.

The Fed has stated that it wants to get rid of the MBS on its balance sheet entirely because they’re cumbersome for conducting monetary policy. And it has stated that by holding MBS, it’s giving preferential treatment to housing debt over other forms of private-sector debt, and it wants to end assigning these types of preferences.

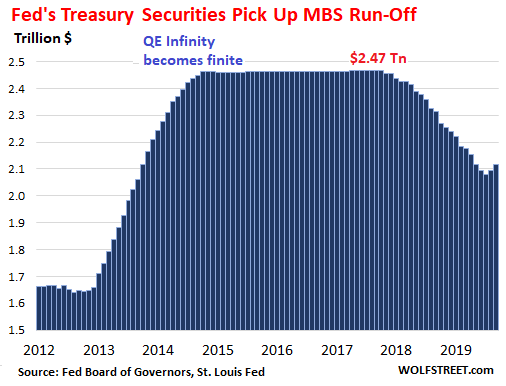

Treasury Securities pick up slack from the MBS run-off

The Fed’s stated plan is to replace all maturing Treasury securities and the MBS run-off with new Treasury securities of maturities that represent the overall Treasury market maturity mix, including short-term Treasury bills.

During September, the balance of Treasury securities rose by $22 billion, in line with the Fed’s plan to replace with Treasuries the MBS that rolled off its balance sheet over the same period. This increased the balance of Treasury securities to $2.12 trillion, including $6 billion in short-term Treasury bills. This was the second monthly increase since the end of 2017:

The thing to watch next week will be how the unwind of the three 14-day repo batches is going. Market participants have to cough up $139 billion and hand them to the Fed. This is a lot of moolah for one week and could put some strain on the repo market. So this morning, the Fed announced that has scheduled new 14-day repos and one 6-day repo, occurring three a week, through the end of October, which would make unwinding the current batch of 14-day repos a lot easier. It also said that it will continue the overnight repos through November 4.

If demand for the coming 14-day repos subsides or disappears, and overnight repos are consistently under-subscribed, we know that the repo market turmoil has settled down for now. If it doesn’t, well, then we can speculate all over again as to who is still out of cash.

If the US dollar loses its hegemony as a global reserve currency, it would be a sea change globally, and specifically for the US economy. So we got the next installment in that saga. Read… US Dollar Status as Global Reserve Currency Slides

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Dear commenters,

My apologies to about 12 commenters whose comments have gotten caught up for about two weeks in a new spam filter that I didn’t know was active.

About two weeks ago, I upgraded the offsite backup service for the server that WOLF STREET runs on. This upgrade came with a package that included a spam filter that I didn’t need because my anti-spam system works well. I deactivated the new spam filter. But it apparently got reactivated somehow, and then proceeded to put about 50 comments, many from long-time commenters, such as RD Blakeslee and “d”, into a spam folder that I don’t normally check.

This morning I checked, and discovered those comments. I fished them all out, and they’re now all there. I also not only re-deactivated the new spam filter but actually deleted it.

My apologies. A lot of good comments were missed.

This is why you have one of the most popular financial sites.. Great insight and all for the price of beer money and all done by a moderator who actually cares..

Amen

So refreshing to have a moderator that is both thorough and diligent. (I’m new here.) More kudos to Wolf!

Amen. On another subject, if these repo transactions do not actually unwind as scheduled, I suspect that we can all say, about the US economy, “Houston, we have a problem.” It would be an indication that another bank just became noticeably insolvent.

With a dry mouth, I wonder if the laws of economics, and of chance, since the banksters’ “casino” banks are not run with the careful computation of odds that Las Vegas casinos use to ensure their long term future, are about to reassert themselves. Can QE to infinity and beyond (which is the tactic left for the “Fed” bankster to pump up the banksters’ banks) work.

Can all of the people be fooled all of the time by the banksters? If the CIA is covertly creating instability in the world, so that investors will flee to the US dollar and maintain its reserve status, as some claim, let me say “kudos” to them. It is sad that the “Federal” Reserve is not run as competently.

I hope that if congress must bail out another insolvent bank, we require that the government/taxpayer’s receive most of its shares, e.g., in a sovereign fund owned by the social security administration, so that all Americans can truly profit from the shenanigans of the “Federal” Reserve banksters.

Is REPO sgort for reaped off?

LOL

Wolf, Will you please do a follow up on the snap back interest rate story you ran a few weeks ago. It appears interest rates have snapped back DOWN. Was the original snap back just a fluke or short squeeze as some have suggested, or do you expect interest rates to snap back up again.

I will, at year-end. As part of a larger year-end piece.

Wolf, I really appreciate this article, but I still don’t understand why they are doing this. Can you explain it in 5th grader language because this bonehead still doesn’t get it.

Thanks.

-Bonehead

“but I still don’t understand why they are doing this.”

You’re not alone :-]

Thst does explain why some articles seemed to have so few comments. Anyway, thanks for fixing things.

I figured some such “Technical” issue was at the root of that problem.

Probably one of those things you have to confirm you wish to delete, several times, as it has something else in it, they are not telling you about “They” dont really want you to delete it.

Why did you delete my last comment on you following up on your snap back article? Did you feel embarrassed by thinking I was calling you out on your massive missed call. I knew you were thinner skinned just like the other economic commentators who think they are infallible. You made a wrong call. You owe it to the readers to own up to it.

I didn’t delete it. I replied to it yesterday. It’s a few comments further up. You just didn’t see it. And then, after not seeing it, you took a big unknowing plunge into speculative BS :-]

Mr. Richter, i apologize if this was addressed in the comments section from your piece last week about the repo rate spike, but is it possible that even though banks still have $1.5 trillion of excess reserves, they are really not ‘excess’ as much in practice because the regulators are quitely telling the big banks they need to have a minimum percentage of their HQLA be in the form of excess reserves for purposes of the LCR even though treasuries, agencies, etc qualify as HQLA? Perhaps this why some of the banks didnt step in right away as rates were rising?

We know there are banks that are awash in reserves, and other banks that are tight. But we don’t know the names. The excess reserves are not spread equally across all banks. There are also other market players in the repo market, such as hedge funds. The banks that are awash in reserves should be lending to the ones that are not. And maybe they are, and something else is going on. Every day, new speculations surfaces as to what is behind this.

Do you think there is a chance DB could be in trouble? Would make sense not to lend if they’ll fail.

In full honesty, this was something that I read at reddit.com/r/wallstbets .

In the movie “the Big Short” there is a scene where Vanett is using the blocks to make a CDS pitch to Front Point. DB is everywhere in that scene. He works for DB. With all of the current problems on WS the price of DB just stays pegged at $7….something smells bad… Just saying…..

Wolf,

Just wondering if you’re contemplating to do this?

“I posted this on an article about the IPO’s crash and burn…”

(Jack

Oct 3, 2019 at 12:01 am

señor Wolf,

I think the time is ripe now to do a dedicated article on “ Softbank “, and delving into its DNA in detail.

A bit of further analysis ( your type of analysis) of it’s so called ( vision fund 1 and vision fund 2) .

The necessity of this will be evident in the market soon.

It will be also great if you look into the recent operations of deutsche bank , these two birds are going to mean much in the next year or so.

I would enjoy reading the contributions to these particular works ( if it materialize) .

Many thanks to everyone that share their thoughts here.)

That was the comment.

There is a Huge Number of comments and I understand it’s hard to cover too many topics, but I suspect that there is big trouble brewing in the banking fraternity now !

You might want to call it “ the biggie that might just crush the proverbial Camel’s back”!!:)

Cheers

In the works :-]

WR,

“awash in reserves…but we don’t know th names”…

I think the following FDIC site might be able to help,

https://www5.fdic.gov/sdi/main.asp?formname=customddownload

Basically, by looking at “equity” capital for each bank (and comparing it to minimum required equity capital), then comparing this scaled up “loan capacity” figure against actual loans outstanding, I wonder if some measure of “excess reserves” can’t be approximated.

I’ve run this analysis in the last year or two and the results were that the vast majority of spare “loan capacity/loanable funds/excess reserves” were located at the Big (Corrupt) Four –

Wells/Citi/Morgan/BoA

Perhaps this really shouldn’t be too much of a surprise – those four are much, much, much bigger than almost the rest of the entire banking industry.

And almost all indications are that the US Government would be much happier really just having 4 national banks to deal with…with the rest going away one way or the other. Easier to control/manipulate the US economy.

On a related note – in 1990 there were about 15,000 US banks…today there are about 6000.

Mr Richter, this may be similar to 2008 when banks wouldn’t loan reserves to each other. Maybe the banks with excess reserves know more than the Fed about the quality of other banks assets? The IOER was supposedly put into place so the Fed would not have to constantly intervene along with the stress tests which were conducted to potentially anticipate questionable assets and there ability to weather a downturn. What happened to the discount window? I guess the Fed doesn’t want to cast a shadow on the banks who need it being this would embarrass those that have questionable assets. When a bank went to the discount window that meant that other banks would not lend to them and the discount window is exactly what the word implies that the bank using it would have to pay a higher rate. Is it possible that we now have a new (temporary?) repo discount window with the Fed facilitating it to maintain the rates with respect to the federal funds rate. The old discount window reflected price discovery to a certain degree.

Mr Richter, this may be similar to 2008 when banks wouldn’t loan reserves to each other. Maybe the banks with excess reserves know more than the Fed about the quality of other banks assets? The IOER was supposedly put into place so the Fed would not have to constantly intervene along with the stress tests which were conducted to potentially anticipate questionable assets and there ability to weather a downturn. What happened to the discount window? I guess the Fed doesn’t want to cast a shadow on the banks who need it being this would embarrass those that have questionable assets. When a bank went to the discount window that meant that other banks would not lend to them and the discount window is exactly what the word implies that the bank using it would have to pay a higher rate. Is it possible that we now have a new (temporary?) repo discount window with the Fed facilitating it to maintain the rates with respect to the federal funds rate? The old discount window reflected price discovery to a certain degree.

The USD is not going to lose its status as the Worlds reserve currency. In fact the USD reigns supreme & will continue to do so as all other world currencies trend to worthless. In the coming age of deflation & depression, those with cash & real stores of value (precious metals) will be able to survive & prosper.

The latest FED actions with Repo’s & interest rates is a warning sign of what’s just around the corner. The FED has 1 tool left & that is to devalue the USD. The U.S. can’t compete with the rest of the turds circling the toilet bowl at a faster spin rate, so they have to keep cutting interest rates in a “strong” economy with a declining unemployment rate. For now, it’s keep the banks propped up because once liquidity dries up & a credit crunch comes to fruition, it’s game over.

Regarding the United States Dollar never losing it’s World’s reserve currency… I wonder if China & Russia would agree?

America has been fortunate to have this advantage, stemming from World War 2, when it was the last man standing, so to speak. But nothing lasts forever. Just check “Great” Britain and pound sterling who were on top before us.

Yet, one wonders, how does this come about? Another world war? Something most leaders would surely wish to avoid with today’s modern weapons. I think, rather, the most likely scenario is a financial panic, allowing the IMF & World Bank to step in, in an effort to “save” the world’s financial system, which after all is now…Digital.

After which all transactions, by universal law, will be carried out digitally. All currencies will be a part of it, but cash will be a relic.

Call the digital currency…”Jibits” if you like, but don’t think for a second it will be the dollar.

We are going to be dethroned.

I believe the new world currency will be the “bancor” and it will be illegal to have this currency in the US ….

A few issues with your comment, Double D. Reserve currencies have come and gone, and I suspect the US dollar will not be any different over time. Your definition of ‘Real Stores of Value’ when everything tanks and we enter some kind of cataclysmic Depression pre-supposes people will be able to safely cash in and take advantage of the situation. In other words, use their wealth to take advantage of others.

In such a situation I would imagine anyone obviously wealthy will have big big targets painted on their backs. People have been killed and skinned for a lot less than being rich.

My own feeling is that real wealth (beyond health and family) is community and arable land. Community is nurtured and reinforced by sharing and being one with others. Like-mindedness. For example, in our rural community several folks down the way make note of who drives down our one way road. Sometimes they phone others about a suspicious vehicle. I have shops, tools, and stores that all my neighbours have access to if they need something. If they need something built or fixed they just have to ask. I haven’t locked my shops for the last 15 years because I don’t have to. About a mile away a friend operates a local sawmill. I have free reign to all of it with the only requirement of leaving a list of what I have taken……paid for, whenever. How do you put a price on this? If I was in some kind of trouble or needed help I wouldn’t phone the authorities, I would phone a few friends. People that don’t share and take advantage of others in tough times don’t have friends or a support network.

Side note: Russia just announced yesterday that all future oil transactions will be done in Euros.

Paolo you are doing it right. I’m all for skinning the rich and feeding them to the pigs lol.

I tried the rural/semi-rural “survivalist compound” thing and I just got stuck with the lion’s share of the work, endless drama because the guy who owned the place invited all kinds of freeloaders to live there, etc.

Since I am not of the land-owning class myself (one’s class is just about carved in stone in the US) all I can do is hope to find a better lord to work for in the future. And thank my lucky stars that we’re not at the point yet where one is bound to the land – I was able to simply leave.

Alex you are so right. BTDTDWO. (Been there, done that, didn’t work out.)

Idyllic, Paulo! Wish we all could live in such a community. But behavioral economists have shown (empirically) that over time (short times, at that) people will game the system. Attempts with communes usually fail because of what alex in SJ mentioned: when it comes to sharing the hard, dirty work, few will contribute. Communism may be an ideal, but it sure ain’t real – not for human beings, in any case, with the exception of religions where the fear of God’s retribution keeps order in the court.

And if you consider the drift of American politics today, it’s almost diametrically opposite of the scenario you’ve described. We are more divided against one another than almost any time post-Civil War. And, we have a “leader” who has called for civil war for his own political benefit. How long will it be before we can leave our doors unlocked with that kind of rancor?

Yes of course all these things are real wealth. But this blog is about finance. The wonderful things you mention cannot be divvied-up, traded, hidden, transported….

The reserve is gold, people. No ifs and or buts.

Hi Paulo,

I felt compelled to respond to your comments. I think anyone who has anything of perceived value will have a target on their back. It’ll be the haves vs. the have nots, only on an exponential level.

In a “Kumbaya” world yes a tight knit community is very desireable. But in times of desperation when your neighbors are getting increasingly desperate, the nice, freindly community you describe may no longer be as nice, freindly & safe.

BTW, I day trade Crude Oil Futures & all oil transactions are done in USD. I doubt Russia is going to contradict OPEC. The Euro is going to worthless once the EU collapses, so I can’t imagine any country outside of the EU wanting to trade the Euro.

Well stated as I think EU’s policies/experiments and Euro may unravel sooner than later. Better to accumulate gold and silver using stronger FIAT currency USD as “competitive” currency war might be the next phase when ZIRP flounders.

I can’t tell if you’re being sarcastic.

The latest Fed actions with Repos is a warning sign that government deficit spending is in a feedback loop/death spiral and the dollar is going to be debased to zero to pay back the debt the government owes. The primary dealers were getting crushed by the treasuries they were compelled to purchase.

It’s not just the debt that is structural, it’s not just the deficits that are structural, it’s not just the growth of the deficits that are structural – it is exponentially expanding deficits that are now structural and the Fed has given the government the green light to print as many treasuries as the want. The Fed has signaled they will buy and buy and buy treasuries no matter how much the government vomits out. DEBT MONETIZATION.

The fact that the Euro, Yen and Renminbi are being debased is not going to save the dollar. People around the world who hold currency are all going to be crushed.

Since when do overnight, interbank, treasury collateral loans extend for 14 days and roll over forever? This is a giant pile of stinking BS. The Fed is monetizing government debt through the Repo market and their balance sheet is ballooning.

The government’s answer to out of control deficits was to cut revenues and dramatically increase spending while demanding a weak, compliant Fed pay for everything with loose monetary policy. The King is not wearing beautiful robes, he is walking around butt naked – and his nakedness is hideously grotesque.

Powell said he would be increasing the balance sheet “organically”. The organism he is feeding is an out of control monster – good thing Powell has an infinite supply of currency to feed the monster.

How can the debt be bad if it’s “organic” – thank-you for the free put Mr Powell.

What are the real world ramifications of this? Less OPM for speculators to pump into the asset bubbles?

You’re funny.

The mechanism the Fed uses to fund the government (currency creation and loose bank oversight – also currency creation) is not an efficient government funding mechanism. Much of the money does go toward funding wasteful out of control government spending but, again because the mechanism is a ridiculous Rube Goldberg contraption, much of the currency flows into assets (the pockets of Warren Buffet and other wealthy parasites).

What you see as an “asset bubble” is actually a currency bubble. The currency is way overvalued given it’s reckless stewardship – fiat currencies are a confidence game and central banks appear hell bent on destroying the confidence.

I totally see the term repos getting renewed (fresh batch issued same day as the unwind date).

Narrative was that there was end of quarter cash-crunch. But Fed has been publishing daily repos everyday even after End of quarter has come and gone.

Fed can keep this going on for a long time. Providing cheap liquidity without calling it QE.

That’s right Just don’t you dare call it QE This is very good for precious metals assuming as I do that it will continue to infinity or default whichever comes first

When we reach this point:

Turning and turning in the widening gyre

The falcon cannot hear the falconer;

Things fall apart; the centre cannot hold;

Mere anarchy is loosed upon the world,

The blood-dimmed tide is loosed, and everywhere

The ceremony of innocence is drowned;

The best lack all conviction, while the worst

Are full of passionate intensity.

Gold will probably spike dramatically — and it will be next to impossible to purchase any (think about how many trillions of dollars will be attempting to scream for the implied safety of gold)

But that will be short-lived.

Because when the system shatters, we will effectively be bombed into the stone age.

Nearly 8B people without food, medicine, oil, etc.

Oh but some will have their gold. And it will be worthless.

“The best lack all conviction, while the worst

Are full of passionate intensity”

Anyone come to mind?

Looked at that page – so we will get that perpetual term repos after all.

When I speculated about Fed stacking up these term repos I was told “getting a little over-enthusiastic here with your QE theories.”

Do you still feel that way?

The Fed now effectively has once again what it used to have before Sep 2008, which is a “standing repo facility.” The Fed has gone back to controlling short term rates the way it used to control them, namely with repos. Until Sep 2008, the Fed always used repos to control rates.

I thought I read elsewhere that the term repos were a new thing, that the prior-to-2008 repos were all overnight-only. Am I mistaken?

My theory, such as it is, is that the fed originally thought and claimed that QE was unlike printing money because once money was printed it was difficult to unprint, whereas QE could be unwound. But the fed’s experience with QT has shown that QE/QT is not symmetric – the market goes into a hissy fit over QT much more rapidly and strongly than the market responds to QE stimulus. And they were able to unwind only a small portion of the QE before the economy started rolling over.

So now they are trying yet a third variation, the term repos. Which are not quite like outright purchases of long-dated treasuries, which don’t unwind on their own for years, since the 14-day repos unwind automatically unless rolled over.

My first guess is, if they decide the economy needs more stimulus, that rather than restart QE officially, they will just ramp up amount of 14-day repos they are regularly offering. And they won’t call it QE, though the market will.

And my second guess is that looking way out, once they have built up a large regular rolling purchase of term repos, they will discover that the market breaks if they don’t keep rolling it over, and it’s just as hard to unwind as the other things they’ve tried.

Its a lot easier to get people to take free money than it is to get them to give it back. I don’t understand why the fed keeps working so hard to try and disprove this obvious truth.

@Eastwind – Term Repos are not a new thing, they were used in the past. We’re just not used to them because of the policy changes since 2008.

Here’s historical data on Term Repos since 2000:

https://fred.stlouisfed.org/graph/fredgraph.png?g=p4XM

There are separate data series for overnight repos and for various types of collateral.

“The Fed has gone back to controlling short term rates…” This statement is inconsistent with logic and empirical evidence because the Fed does not seek to control rates when they go below it’s target only when they go about it. Therefore, a more accurate statement is: The Fed is suppressing rates when they go over it’s target rate suppression.”

timbers,

The Fed uses “reverse repos” to keep the rates from going below target. Reverse repos are currently a $290 billion line item on the fed’s balance sheet (on the liability side), but that’s down from $500 billion a few years ago. Reverse repos are a liability, so they’re the opposite of QE and repos, which are assets.

Except… this is not a run of the mill repo program as was done in the past to set (manipulate) interest rates.

This is not temporary, overnight lending with collateral being repurchased the following morning. This appears to be longer term debt that is being perpetually rolled over and growing to funnel currency into the treasury market.

I will admit to being wrong (and relieved) if the Fed’s balance sheet drops back down from its recent surge – in other words I will not have to admit to being wrong.

QE acquired a bad connotation after it became synonymous with money printing. Problem is, everything the Fed does is money printing – the moniker they attach really doesn’t matter.

Confidence in their electronic digits is waning.

Ok I’ve gone over my allotted number of posts and I’m only repeating myself “their debasement program is out of control” so scrub this message, really just typing to myself at any rate.

@wisdom seeker (not sure why I can’t reply directly to your post)

Thanks for the link, that’s interesting. I must have consumed some fake news. Looking at the graph, the highest it ever was back then was about $12B, a lot less than the amount of 14-day repos they’re doing now ($45B of term repo on 10/10)

A turd by any other name is still a turd. Behold, permanent open market operations.

Fresh as opposed to stale ( money) !!

Hahaha :)

What will they think of next ?!

Federal Reserve announced today that the Term Repos will continue.

Rolling inventory looks like $150-200 billion.

https://www.newyorkfed.org/markets/opolicy/operating_policy_191004

Fed also announced that Daily Repos of $75B+ will continue for at least another month:

“The Desk will continue to offer daily overnight repos for an aggregate amount of at least $75 billion each through Monday, November 4, 2019.”

Yes, see the paragraphs below the last chart for details.

Hello Wolf

You have a fantastic site. One of my favourite daily reads. Please continue!

I would be very interested to see the Fed balance sheet over time from here on out. Specifically if the collateral (Treasuries and MBS) continues to grow. In other words repo failures. That would mean the banks are just keeping the money and it is QE via the back door.

For those out of the loop on Fed repo, here yah go:

Two Little-Noticed and Self-Inflicted Causes of the Fed’s Current Monetary Policy Implementation Predicament

Bill Nelson (bpi)

October 1, 2019

“Thus, it is concerning that the decisions to allow massive growth in the Treasury General Account and Foreign Repo Pool may not have been made with sufficient deliberation. As described above, the Fed and Treasury elected to leave Treasury cash balances in the TGA rather than in deposits under the jointly run TT&L program even after interest rates began to rise, but there is no record of that decision in any FOMC minutes. Similarly, the Fed decided in 2015 to remove constraints on foreign official counterparties’ ability to vary the size of their investments in the Foreign Repo Pool; again, though, we cannot find this decision reflected in the FOMC minutes. Thus, as the Fed grapples with numerous adverse consequences of its continued operation of a floor system, it may be worth a wholesale review of the decisions, or non-decisions, that led it there.

I dare to speak for others here, as for myself, when I say that even if we don’t agree on all things, we all appreciate everything you do. I’ve been reading and posting here since testosterone pit (how long has it been?) and enjoy it very much.

I think it’s time for kitten lopez post!

Off to formulate an “on-topic” comment.

Kim

“I think it’s time for kitten lopez post! ”

Seconded.

Count me in ,

We’ll need more than a strong coffee or brew to control the headache that the Fed is causing us By their” Wiley Coyote language shenanigans “! :))

Seems to me the Fed has some banks ‘swimming naked’ if they have to rolling and expanding these repo operations. Why won’t other banks lend to them? If the Fed doesn’t want to reveal which of their primary dealers are crippled maybe the FDIC should and force the banks to pass the hat to shore up deposit insurance before there is a big failure.

In other news. I would suggest anyone involved with The Lending Club exercise extreme caution. Over the past month this ‘peer to peer’ lender has contacted me repeatedly about my loan applications. I have told them repeatedly these applications are fraudulent ( something the big 3 credit agencies would have verified had they bothered to check). Apparently making the loan is how people get paid and getting the loan repaid will be YOUR problem!

Unit472 that looks quite interesting! LC’s stock is probing fresh new lows and is in danger of becoming a single-digit stock. It’s already down over 90% from its IPO about 5 years ago. Desperation breeding shenanigans?

The FDIC forcing ‘good’ banks to beef up their contributions to shore up bad banks (i.e. the ones that offer the highest deposit yield and charge the lowest interest for loans) is just further confirmation that the philosophy of society is to punish success and reward failure.

Banks know about each other, and not pouring money down a sinkhole is one of the rules of proper* banking. That’s why they don’t lend to some other bank, and that the bad bank should just pack it in.

*(proper banking does not include central banks).

About the Lending Club, just looking at their site, for ‘investors’ they are offering lower yield on higher risk. ????

Mortgage debt is expanding, even while housing is tepid, perhaps the drain of Chinese cash buyers has opened up this market. Reckoning that even with lower rates the mortgage market has probably bottomed. The spread between MM and savings rates has something to do with reserves. If they want NIRP this is the way to go about it (cramdown on savers) Obviously it creates problems. Why do they need reserves? Kinkos has one hour service?

Repo & collateral. No collateral, there is no Repo.

In 2008 RE collapse and MBS was no longer accepted as

collateral. There was a big hole, a financial vortex.

That’s how Lehman was gone.

Some banks could be using the repos for growth. Getting repo cash may be easier and quicker than raising deposits or CD money. It enables a bank to make loans quicker, doesn’t it?

Or, maybe a bank is experiencing a run or other cash management problem. Who really knows.

By golly I think I have a nice repo chaos clue; this wraps it all up nicely and perhaps shows this unusual activity is related to the deficit, who woulda guessed there was something going on?

Chicago Fed Letter, No. 395, 2018

Second, as the figure shows, the Treasury occasionally reduces the account balance below the $150 billion minimum that it ordinarily targets. These reductions generally occur when the Treasury approaches the debt ceiling—a limit set by Congress on the amount of money the government can borrow. Similar to a household that wants to pay its bills without taking out a loan, the Treasury, when it faces a tight debt limit, must spend down its checking account until Congress allows it to borrow more. These factors mean that if the Treasury maintains its current approach to cash management, the Federal Reserve’s liabilities to the Treasury in future years will be both larger and more volatile than they were before the financial

Second, while the Fed remits virtually all of the earnings on its assets to the Treasury, it historically has retained some earnings as capital. Until 2015, the retained surplus was set equal to the capital paid in by commercial banks. Thus, the Fed’s total capital—the amount paid in by commercial banks plus the retained surplus—grew in proportion to the size of the banking system, as shown in figure 4. However, in 2015 Congress passed a law limiting the Fed’s surplus to $10 billion, and in February 2018, Congress further reduced the limit to $7.5 billion. To comply with the limit, the Fed transferred some of its surplus to the Treasury, reducing the amount of total capital. Going forward, the retained surplus will remain at $7.5 billion, while capital paid in by commercial banks will continue to reflect the size of the banking system.

https://www.chicagofed.org/publications/chicago-fed-letter/2018/395

If it doesn’t, well, then we can speculate all over again as to who is still out of cash.>>>

Banks can’t lose money in the repo market and thus won’t to do business with an insolvent bank. The question is, which bank(s) has a capital shortfall? I speculate it is a European bank that starts with a D.

There are many rumors about who is low on cash. I think it’s a bank in Hong Kong. A guy in Australia thinks it’s a bank in Australia. Others blame Goldman, and still others JPM. Only thing for sure is the fed is doing this for a reason.

It’s could be all of them.

Funny/strange that banks don’t seem too disturbed about the time value of money until it’s their money being lent out overnight in the repo market.

The repo market appears to be that last interest rate business model hold out.

The global plan is to power through this upcoming recession with printed money. They did it in 16 and all Yellen had to do was dither a bit. There is no communication there, so anything is possible, just nothing really good, that’s all. Even if JB does make good on his threat not to be threatened, Liz Warren could be his VP and that would make Wall St nervous.

It’s the very nature of fractional reserve banking, borrow short and lend long. The instability is built in to the system which requires intervention by the central banks.

That the Fed has to engage in what for all practical purposes are discount window operations is troubling. Maybe the economy isn’t so robust after all, despite years of propaganda.

Hard for the central banks to reposition themselves to respond to a real crisis when they can’t reduce their balances and banks cannot shed excess reserves when times are good; when stock- and bond markets are at highs and there is full employment.

Discount window, without the transparency of the discount window… best of both worlds!

Maybe the economy isn’t so robust after all, despite years of propaganda.

Things are not as they seem. The whole thing is supported only on the continual increase in debt in all important sectors. The cost of perpetuating the illusion keeps increasing as well, paid for by bleeding the real economy.

The old cracks are still there, and new cracks are forming. The Fed’s finger in the dike isn’t going to be enough when it bursts. As Powell himself has warned, it’s not a sustainable situation. All to keep from having to write off the phony paper wealth of financial asset inflation so the investing class can continue their profiteering.

At least you know where the excesses of the last meltdown went to: those were converted into Fed assets. Or maybe they’re liabilities. These days it’s not so easy to tell.

I need to print digital USD out of thin air today buy securities, too

Which you can’t do unless you’re a financial industry insider. Hence the emergence of cryptocurrencies, aka prosecution futures.

Don’t confuse the words finance and industry with fraud. “Central banking” is actually not banking it’s just fraud. But there are insiders you are correct about that.

1) Trump & Dem might become friends again. Trump really need Biden.

2) The “Golden Week” is over, the dragon hangover,

bloody hand will unite them.

3) A trade deal ==> forget about it.

4) Dollar strong> 104.

5) SPX up today, on lower volume, but the 10Y is down.

6) Soon we will know which collateral is swimming naked,

So much global debt, the Fed cannot help.

7) If the market will dive, the chance of vortex

is growing. RIP repo.

8) An energy blowup can lift up NR, $17T, so far.

9) US & Canada have energy. Russia does. A ME blowup

will hurt the Giging dynasty the most.

This is the consequence of excessive lending everywhere and resulting collapse of interest rates leading to a ‘problem’ with the buy- and sell sides …

//“There is no point denying we are faced with a looming liquidity mismatch problem,” said Pascal Blanque, who oversees more than 1.4 trillion euros ($1.6 trillion) as the CIO of Amundi SA, according to Bloomberg’s Mark Gilbert who in a Bloomberg View piece writes that Blanque told him that the prospect of melting liquidity is one of “various things keeping me awake at night.”//

When the greater fools (pension funds and money managers) have already bought, who is left to sell to?

Now we see runs against money managers and banks:

//”As an aside, while the above is 100% correct,we find it ironic that it comes from none other than Deutsche Bank, a financial institution which due to a similar considerations among its clients, has itself become the target of a mini “bank run” one targeting the bank’s prime brokerage assets, and which as we explained last week, is reportedly draining roughly $1 billion per day from the German lender.”//

https://www.zerohedge.com/news/2019-07-24/16-trillion-fund-spots-new-ticking-time-bomb-market

“This increase was mainly a result of the New York Fed’s repo operations – particularly the three repo operations with 14-day maturities that will all unwind next week:”

Jimmy crack corn and I don’t care.

“Meanwhile, the MBS run-off continues and exceeds “cap” for fifth month in a row…”

HALLELUJAH

Inside the New York Fed …

https://www.institutionalinvestor.com/article/b1hf1ts2xs9vtc/A-Secretive-Committee-of-Wall-Street-Insiders-Is-the-Least-of-the-New-York-Fed-s-Concerns

“The Fed’s stated plan is to replace all maturing Treasury securities and the MBS run-off with new Treasury securities of maturities that represent the overall Treasury market maturity mix, including short-term Treasury bills.”

Not quite. The Fed’s plan is to reinvest up to $20 billion of MBS principal payments each month in Treasuries. For September about $6.4 billion of MBS principal will be reinvested in MBS, but it takes up to two months for the reinvestment transactions to settle so the money comes out of the MBS category on the balance sheet and then back in. For example, there were August principal payments for which the reinvestment transactions will not settle until October 21. Only the $20 billion in MBS principal is being reinvested in open market Treasury purchases in proportion to amounts outstanding in 11 sectors, including 15% in T-bills. Principal payments from Treasury securities will continue to rollover at maturity in proportion to the amounts offered by the Treasury on the maturity date. So of the $12,985,000,000 in principal from Treasuries that matured on September 30, $3,324,319,300 was reinvested in 7 year notes, $4,259,153,100 in 5 year notes, $4,155,274,300 in 2 year notes and $1,246,582,200 in nominally 10 year (actually 9 year, 10 month) Treasury inflation-protected securities. The amounts don’t exactly add up to the maturing principal, because of discounts, premiums and in the case of the TIPS, accrued interest.

If the cost of producing money is less than its value then there’s an incentive to forge it.

One just loves the phrase ‘melting liquidity’ (Steve from Virginia’s comment).

It would indeed keep one up at night: who says finance can’t be entertaining? !

It’s a mad world, my masters, a mad world…….

Learn to laugh at it all, or you’ll be weeping to Doomsday.

Repos are only “new”‘ to those “new” in the game.

They play an important function in the market, assisting banks with larger holdings of long term hard collateral T’S, to use some of it in times of liquidity need .

Which is better:

1 The FED holding huge chunks of long term T’S, with inflated balance sheet. Inducing excess liquidity in the Market Etc, and everything else that goes with that.

Or.

2 Banks investing large chinks of THEIR liquidity in long term T’s and REPOing against them in times of liquidity need.

As long as the FED does not allow MBS back into the REPO market, FED and the TAX payer can not loose.

The FED Balance sheet, EX MBS is around where it should be, for the size of the US economy and the Physical US $ in circulation.

If the FED could dump its MBS holdings at Par plus costs it would probably jump at the opportunity to do so, and I for 1, would be extremely happy, as the MBS is something the FED should NOT BE Holding.

Then the Fed and the US financial sector, would both be 1 step closer to “Normalisation”.

The FED should not still be backstopping the US Govt and the US housing market, 11 years after the 2008 event.

The Fed “acquired” all those MBS because they’d become worthless, but the Fed paid full listed price for them. So, there was never a snowball’s chance in Hades of getting back “par” cost for them. This is the debris still left around from the last big banker scam job that stole $trillions before it crashed and then got bailed out by Mom and Pop when the scheme crashed.

The US is a socialist country. But in a new way in that only bankers and billionaires get supported by the government. Ordinary people are told to go starve and that somehow its their own fault so they should hate themselves just like the billionaires hate them.

Mad Max,

The Fed acquired some private label (not backed by Government Sponsored Enterprises) MBS during the financial crisis as part of the bailouts. Some of those went bad. But the MBS the Fed has been acquiring since as part of QE, which is what it now has on its books, are all “agency” MBS, that means they’re issued and guaranteed by the GSE or by government agencies such as Ginnie Mae. On those, the Fed hasn’t lost a dime because the credit risk is with the US government entities.

Not sure why Fed just doesn’t let market set rates. Next they”ll be setting the price of Salmon in San Francisco. Not really, but I think there are a lot of investors out there who would like to know who these exposed counter parties are? The Fed is not only covering but covering up. In a real market, the Street would know and let their clients, and thus, the world know who are the weak hands here.

Supposedly the Dodd-Frank law was supposed to require such disclosures to Congress after the Fed handed out $Trillions under the table the last time the bankers screwed up. But, the day Dodd-Frank passed, the floor of the NYSE erupted in cheers. And since we’ve seen why, in that it is the most ignored law in history. The bankers and the regulators have simply just agreed to pay no attention to it. So, we are left asking questions about just which banks are so badly needing this emergency money.

Nothing but more QE coming…

I suggest we start referring to any form of government debt purchases with newly created money as “monetization of debt” or “money printing”.

That’s what it is.

“Is breaking the buck ” the next talking point in our future or has the fed fixed forever the money market liquidity problem. This is just a way for the fed not to say QE.

Wasn’t the original con job behind these Fed Repos that it was due to a cash crunch at the end of Q3. My calendar says that’s a week behind us, but still the Fed keeps handing out money.

Why did the banks stop lending to each other, forcing the Fed to step in? They have large reserves, or so we are told. So, why?

An article that mentioned the 2008 depression mentioned that the banks stopped lending to each other because they didn’t know which other banks were exposed to the massive losses at Citibank? Who’s in trouble this time? Deutsche Bank?

Why has JP Morgan lowered its reserves on hand with the Fed by a whopping $150 billion? Does this have anything to do with its “Metals” desk being indicted under RICO racketeering statutes that were designed to go after organize crime? This is the same bank that already pleaded guilty on two felony counts related to being Bernie “Ponzi” Madoff’s banker, and another from another desk being convicted of also rigging the LIPOR markets.

The banks are all connected by derivative schemes. Right now, it appears somebody is in trouble, and the banks don’t know which other banks are connected to that by derivatives.

“Meanwhile, the MBS run-off continues and exceeds “cap” for fifth month in a row…”

The one thing the Fed has no control over is Mortgage ReFi. Sure they want to limit the roll off to control a gradual depletion of MBS on the balance sheet but if a MBS Homeowner wants to ReFi or sells the house outright and a bank writes the mortgage that “asset” is transferred to the Banks balance sheet. Now the bank needs to shore up its overnight liquidity position and thanks to the Fed the money is there.

To my way of thinking this is a massive improvement to time healing the MBS wound. Its a blight, at long last the private sector (and rates) are financially healthy enough to re acquire these loans and increase the trajectory of MBS roll off to ZERO.

Great post Wolf, very encouraging.

The one thing the FED does not control over is demand in the real economy as well as for money.

The biggest point the mainstream economist alsways leave out of their analysis is the fact that the economy follows the credit cycle. It is not something that grows on itself.

When the FED enlarged the credit in the aftermath of the financial crisis it accomplished that people were borrowing more and spending it thus creating demand.

However the other side of that medal is that people who live of the interest on their principal received lower income. For a while the lower interest rates didn’t effect their demand too much, since their principal wasn’t touched.

However somewhere along the line the price increases and the lower and lower income required them to reduce their demand.

As long as the borrowers demand growth outpaced the demand reduction of the savers, there is no problem.

I think that in the last year that balance flipped and demand started to drop. In my opinion the trade war is merely an exacerbation not the cause.

I think that we are now in a situation where lowering rates only accelerates the recession. Borrowers are not going to borrow more and savers will even spend less.

And the consequence is that when companies cannot sell their stuff, the odds that they cannot pay off their debt is growing.

Also QE will have hardly any effect. Even on assets, since pretty much all the gains are the direct consequence of buy backs. Often financed with debt. Banks will not be too willing to lend to companies of which they are not sure they will pay it back.

And ultimately I think that the deterioration of the business and housing outlook means that the quality of collateral is being questioned thus resulting in hightened reluctance to lend between banks.

The FED might try to do some repo’s to control the rates, but with the amount of debt now in the world and the slow down, each passing day more and more debt starts to become non performing. There is no way that the FED can do anything about it.

QE1, 2 and 3 combined was like 2 trillion dollars. They already printed like 200 billion in two weeks and that in a booming economy. I cannot even imagine what they would have to print with the slightest uptick in the default rate.

The FED is f***ed. Anything they do will have adverse effects popping up and they know it. Jerome must be crying at night why he ever took this job.

Is it possible the whiff of smoke is coming from the derivatives theater?

This FRED chart explains the repo chaos

https://fred.stlouisfed.org/graph/?g=p5hX