Seattle house prices fall year-over-year. New York condos flat 24 months. San Francisco Bay Area flat 12 months despite startup millionaires. Los Angeles barely up from year ago. Boston ticks up...

“Home prices in the West continue their cooldown, with prices in Seattle falling for the third month in a row and home price growth in San Francisco falling very close to zero,” said CoreLogic in a statement about the release of its S&P CoreLogic Case-Shiller Home Price Index today. But prices are not cooling everywhere, and “second-tier markets in the South and Midwest continue to lead the country.”

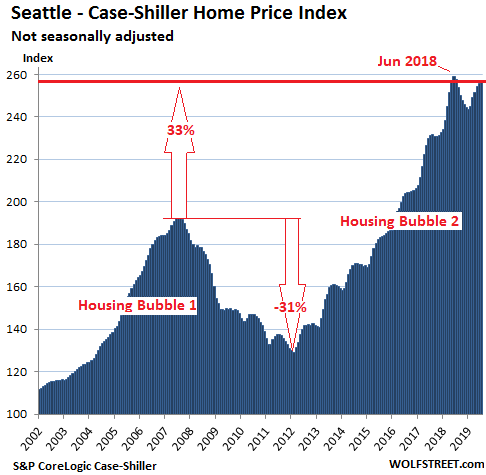

Seattle House Prices:

In the Seattle metro, prices of single-family houses ticked up 0.2% in July from June, but fell 0.6% from July 2018, according to the S&P CoreLogic Case-Shiller Home Price Index. It twas the third month of year-over-year declines in a row:

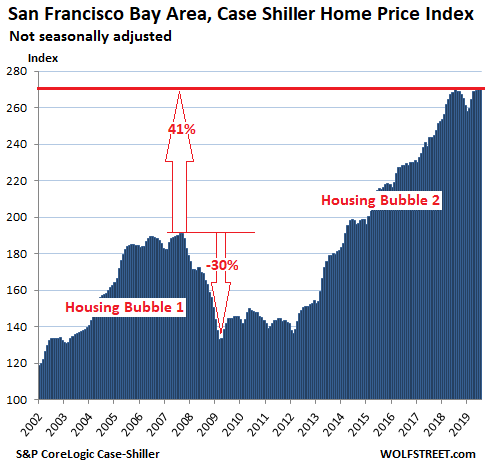

San Francisco Bay Area House Prices

House prices in the five-county San Francisco Bay Area – the counties of San Francisco, San Mateo (northern part of Silicon Valley), Alameda and Contra Costa (East Bay), and Marin (North Bay) – were flat in July compared to June, which whittled down the year-over-year price gain to near-zero (+0.15%), the lowest such gain since the end of Housing Bust 1 in March 2012, despite the countless IPO startup millionaires and billionaires raining down on the Bay Area:

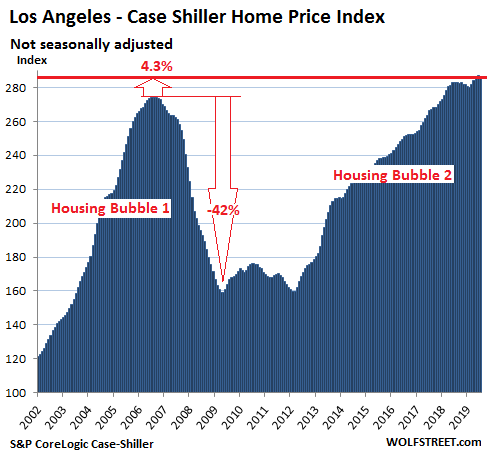

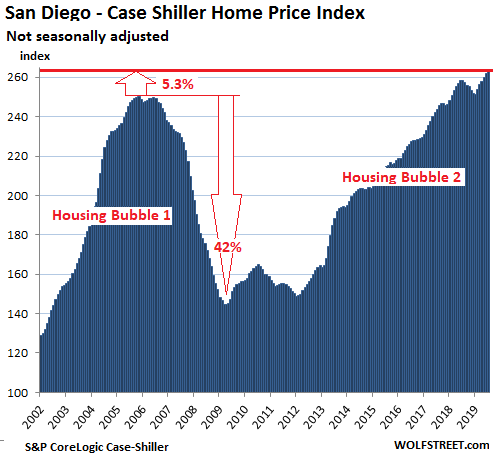

The Case-Shiller Index is a rolling three-month average. Today’s release represents closings that were entered into public records in May, June, and July. The index was set at 100 for January 2000. An index value of 200 means that prices have doubled since January 2000. Every one of the most splendid housing bubbles in America on this list has or had an index value of over 200, either during Housing Bubble 2 or during Housing Bubble 1.

Los Angeles House Prices:

In the Los Angeles metro, house prices inched down 0.3% in July from June, which reduced the year-over-year gain to a mere 1.1%:

San Diego House Prices:

In the San Diego metro, house prices rose 0.7% in July compared to June and were up 2% from July 2018:

The Case-Shiller Index methodology is based on “sales pairs.” It compares the sales price of a house in the current month to the prior transaction of the same house, often years ago. In other words, the index tracks the percentage increase in how many dollars it takes to buy the same house over time. In this manner, the index tracks the purchasing power of the dollar with regards to houses in various markets. This makes it a measure of “house-price inflation.”

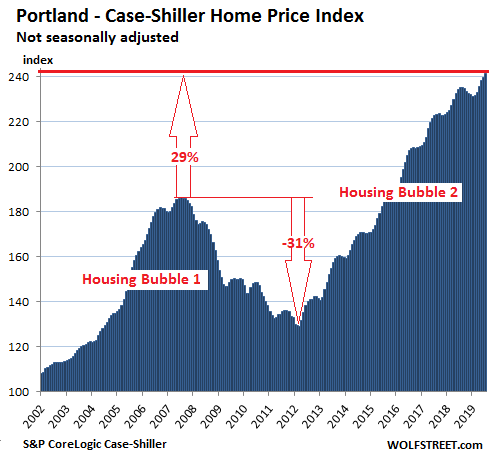

Portland House Prices:

In the Portland metro, house prices ticked up 0.7% in July from June, and were up 2.5% from July last year:

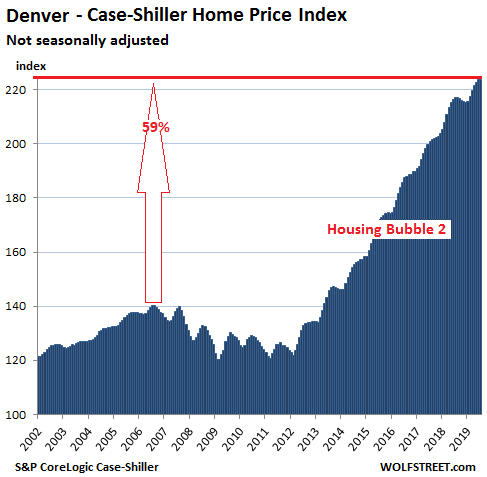

Denver House Prices:

House prices in the Denver metro were flat in July compared to June, which whittled down the year-over-year gain to 3.1%, the smallest such gain since April 2012:

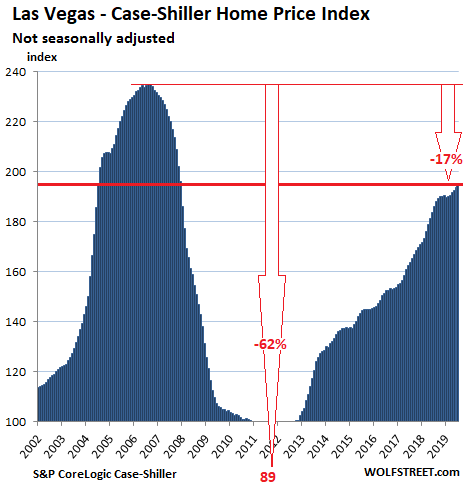

Las Vegas House Prices:

House prices in the Las Vegas metro rose 0.7% in July from June, further whittling down the year-over-year gain to 4.7% — from 5.5% in June, 6.4% in May, 7.1% in April, 8.2% in March, 9.7% in February, 10.5% in January, before which home prices had been increasing at double-digit rates since October 2017. The 4.7% year-over-year gain in July — as large as it was — was the smallest such gain since 2012, when Las Vegas was emerging from the Housing Bust. The index remains 17% below the totally crazy peak of 2006. Gambling in the desert:

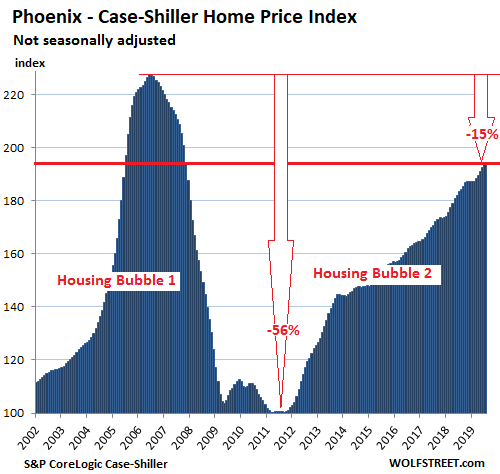

Phoenix House Prices:

The Case-Shiller Index for the Phoenix metro was flat in July compared to June and was up 5.8% from July last year. But it remains 15% below the nutty peak of 2006:

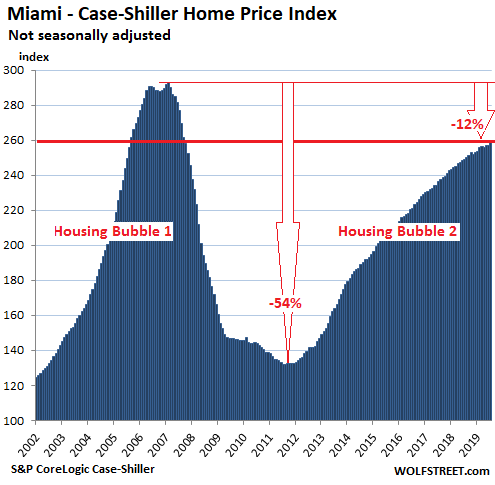

Miami House Prices:

In the Miami metro, house prices rose 0.6% in July from June and 3.9% year-over-year. They remain down 12% from their record-crazy peak at the end of 2006:

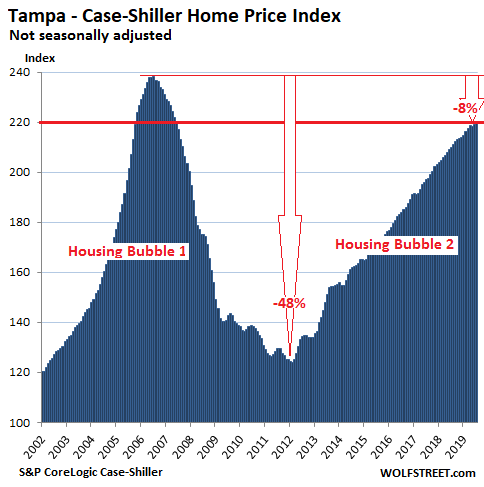

Tampa House Prices:

In the Tampa metro, house prices edged up 0.3% in July compared to June, which whittled the year-over-year gain down to 4.6%, yup, a pretty big gain, but the slowest such gain since August 2012. The index remains 8% below the crazy peak of 2006:

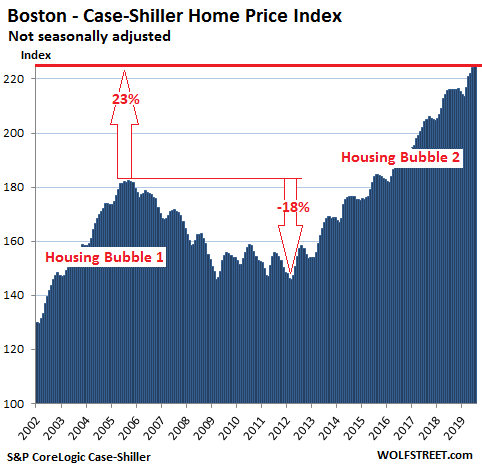

Boston House Prices:

House prices in the Boston metro ticked up 0.2% in July compared to June, and were up 3.9% year-over-year:

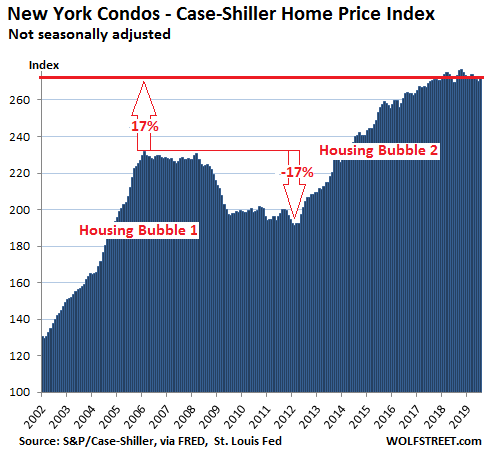

New York Condo Prices:

The Case-Shiller index for condos in the New York City metro rose by 0.9% in July compared to June. This caused the index to be 1.1% higher than in July last year, but still down 1.4% from October 2018. The index has essentially gone nowhere since August 2017:

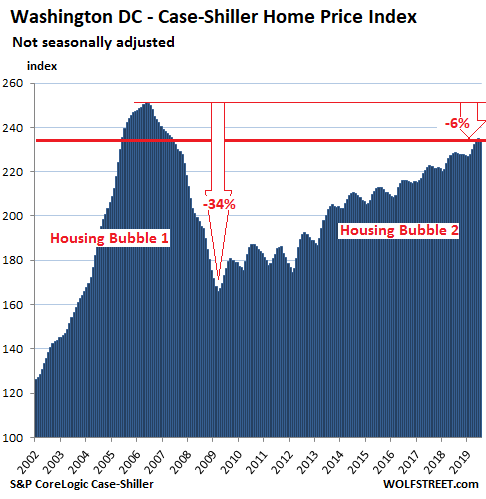

Washington DC:

House prices in the Washington D.C. metro fell a smidgen in July from June, which reduced the year-over-year gain to 2.7%:

“Wiring money overseas is not allowed for the purposes of purchasing real estate or insurance products”: a banker in China. Read… China Imposes New Capital Controls, Targets Foreign Real Estate Purchases, as Yuan Falls to 11-Year Low

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

It will be very interesting to see next year, when mortgage rates don’t drop another 150bp YoY, what happens. Or maybe we’ll have 2.0 mortgage rates and prices will eek out another paltry 3% gain…

Anecdotally, I am seeing the suburbs closest to Boston pretty slow. Lots more price cuts, lot less open house traffic, more and more DoM. The outer belt suburbs appear to still be strong, likely because of their greater “starter home” inventory, and because the inventory that’s cheap closer to the city is just ancient and dilapidated.

@Wolf: since you label it housing bubble 2, are you convinced a correction/deflation is coming?

sc7,

I’m not “convinced” of anything.

I’m not close to the Boston market. I’m a lot closer to the Bay Area market. And I have been seeing a noisy stream of data all year that indicates that this bubble here got as big as it’s going to get and that it is now unwinding. But unlike last time, this time, there is no crisis, and the unwind is very gradual, with lots of ups and downs.

Every market runs on its own time table. So I don’t think that we will see the Bay Area, Chicago, and Boston, for example, move in lockstep. This is just not going to happen unless there is a national crisis, such as Mnuchin going up to Congress and telling them that he needs unlimited powers and means to bail out the biggest hedge funds or else the world will end :-]

I remember 2006 being a long slow leveling out/slow unwind, then mid-2007 the wheels fell off at the Brits say.

It ain’t a bubble if the result is loss of dollar purchasing power. It’s called inflation. Why is that so hard to understand? Home prices are not going down permanently. Your purchasing power is.

Reality,

Please read the article. It’s hard to discuss things you haven’t read. As I pointed out in the article, if the same house goes up in price — the Case-Shiller index works that way, being based on “sales pairs” — it is HOME PRICE INFLATION, yes loss of purchasing power of the dollar. See the paragraph right under the San Diego chart.

There is nothing complicated about it. This is at the CORE of a bubble. It takes more dollars to buy the same thing, whether it’s houses or stocks or bonds or classic cars. Once that gets to a certain level, it’s called a bubble. Bubbles reverse. See the charts in the article. Pure and simple.

You’re just wrong, Wolf. If it were a real bubble rather than inflation, then when Housing Bubble #1 burst, prices would have retreated to year 2002 levels. And when your so called Bubble #2 bursts, prices will not go back to year 2008 levels. Price keeps going up because of inflation.

Heard inflation is like additional taxation. The housing price increases have outpaced and exceeded tame inflation (per government) but more I think the clincher is wage increases not keeping up. Also 1 sure way to fight out of control inflation like in the late ’70s is interest rate boost to counter it – counter-thinking as the CBs of the world spiral toward ZIRP.

One cannot rule out another Great Recession either with bigger asset bubble across the board as look what happened to Japan in the late 80’s followed by years of deflation and poor economy.

Reality,

You just don’t WANT to get it. A housing bubble IS inflation. Say this out loud three times in a row until it sinks in. It’s house price inflation taken to an extreme. Once you get that, look at the charts again. And now they will make sense.

“Price keeps going up because of inflation.” LOOK at the frigging charts: what did those prices do during the housing bust? They PLUNGED.

I’m in East bay and made a big mistake by selling my house 3 yrs ago upon hearing Chinese buyers pulling back. Been renting since and the market was really hot this spring when I looked in case the landlord does not renew the lease. Then the market cooled a lot this summer.

I don’t think there will be the price collapsing like 2008-2011 in SF Bay area but slow decline over next 3-4 years retracing the 50% lows of 10 years ago even with a recession next year. I plan to stay another year till youngest graduates from JC then I’m leaving for NV or back to WA with no state income tax and tired of this land of uber-liberals running amok against the 1st and 2nd amendments with sanctuary cities and free medical care for the illegals.

Thanks for this report Wolf, like you, I live in the Bay Area. Antidotally, it appears that some of the really nice houses generally still get their asking price, but if the home is viewed as needing any work whatsoever, or lets just say is not turn-key,.re-landscaping needed for instance, it will sit, and usually within 20-30 days will experience price reductions, and in several cases multiple reductions. One house I ran across, That would easily pass as a fixer-upper, with some price reduction already, the owner is clearly just in denial, that it could easily require 200K in work to get it to a decent state. It’s like the sellers have not yet figured out the light switch has flipped over to a buyers market. Many, like myself, are just sitting and waiting, because it will likely be just cheaper this time next year.

Your “housing bubble” term is as over used just as the word “recession” is over used right now by the extremely uninformed media. Since when is a large demand and very low supply of housing a so called housing bubble? The ridiculous spike in housing prices in the Seattle/Bellevue area due to a high level of the increase in employment and the resulting

in-migration was an extreme anomaly. Easy math; lots of buyers, and a minimum of homes to purchase = price increases to the highest pricing possible in that market moment. The last dumb arse housing bubble was caused by many, many ingredients including stupidity by home buyers and lenders. Certainly the most significant of those failures was buyers buying way above their normal mortgage credit qualifications, no proof of income, no cash downpayments, and the insane theory that housing values would never loses value and always increases in value. What we have now is an unaffordable market for 70% of the potential home buyers due to the spike in housing prices, and state and local zoning regulations that prevent the production of many more and feasibly affordable housing units. This particular housing market needs to have more homes available for sale to meet the market demand. Unfortunately not only does the local government restrict the ability to produce more housing, the boomers are not about to sell their homes and get stuck having to pay the high price for their next home. This is a housing quandary, not a housing bubble.

Housing Bubble 1 wasn’t called a housing bubble either until afterwards, when it imploded.

The implosion was the result of totally unqualified buyers buying up anything and everything available due to very easy access to home loans and an endless supply of available homes for sale at the time. Vancouver BC and Toronto have had their housing prices spiked by foreign investors such as mainland Chinese, and they are bound to have an implosion of pricing now that the foreign buyers have disappeared. So where is the implosion going to occur in the Bay Area with the housing demand in the stratosphere and the supply completely just not available anytime soon? The buyer public will have to just keep moving further away for their own affordable housing and a decent lifestyle with the few $$ left over every month. Thanks for the modern computer systems and phones many, many of those folks, including me, can work remotely and have a great life without the high priced urban in city living that’s portrayed in the Friends and Seinfeld fantasies

>>very easy access to home loans and an endless supply of available homes for sale at the time.

Huh? So in 2007, say, there was an endless supply of homes in SF Bay? Is that what you said yourself in 2007, or were you preaching “shortage” then also, but have changed your tune now?

>>where is the implosion going to occur in the Bay Area with the housing demand in the stratosphere and the supply completely just not available anytime soon?

But in 2019 somehow there is somehow no supply? How did this imaginary shortage come about?? And by the way, you are aware that San Jose median price is down by about 10% in the last 12 months as of June or so.

I’m just shaking my head at the amount of incoherent rambling propaganda you can generate.

As soon as the job market turns south. I’m not sure where the huge incomes are coming from to overpay for shanties. Once the prices quit going up by greater fools overpaying will people still be willing to buy overpriced houses? $350K product for $650K where I’m at.

House of cards!

Not a RE Bubble?

Do u not think there is a correlation btwn west coast housing prices and the multi billion dollar valuations of earnings negative tech companies?

Wolf u must have a lot of smashed keyboards and lcd screens in ur junk room. And megabytes worth of unsent draft emails with lots and lots of colorful language.

Otherwise I don’t know how u do it. Even so

I don’t know how u do it.

Thanks!

LOL

Not far off the truth.

Housing bubble 1 —> the poor NINJA them self’s into homeless.

Housing bubble 2 —> “qualified” middle class mortgage themselves into poor or bankruptcy.

You think those TLSA, NetFlix, Snap, Uner, Lyft, WeWork employees are “qualified” buyers creating explosive demand?

Let’s wait for the day when market asks the question they should NOT ask, “ can we make a profit?” Once the stock and bond market start to hold back, let’s see how many qualified buyers are left.

How many people are stretching themselves thin buying at these prices this time? I mean…we know wages haven’t kept Pace with home prices so….without a hard recession and subsequent job losses I don’t see much of a home price correction. I wonder if this is a permanent jump in prices due to QE and other Fed shenanigans that I don’t understand but what do I know

Wolf – there were a couple of sites hardly anyone read that were calling it a bubble, one was even called “Dr. Housing Bubble” or was it “Mr. Housing Bubble” another one was pretty hilarious, making fun of columns, the various people hanging out in realty photos, red arrows in ads, etc. It was a good ol’ time.

But you are 100% correct in that you’d never find anything pre-2009 about a housing bubble in the Murky News.

Thats not true.

There were plenty of stories in the print media and on cable news shows. All had quotes from investment and real estate experts about how there is no bubble, but the stories were there.

CNBC even held a 1 hour town hall type show in early 2007 hosted by Bill Griffeth where they debated the possibility of a housing bubble. I recall the consensus was that there might be a few bubbles, but real estate was local. The thought that the entire US would experience a decline in housing prices simultaneously, was quickly dismissed. This was right after the collapse of New Century Financial ( a company that specialized in sub-prime mortgage origination and was #2 in the industry).

Dr housing bubble is still around. He even uses Wolf’s charts in some articles….I’m assuming by permission.

I definitely remember you posting a ton back in the day.

Dr housing bubbles was great… until he became a real estate agent. Somehow he lost his sharp wit about the same time. Too bad.

The best was Housing Panic. Keith was years ahead of the game, the blog is still online going back to 2005, giving a complete timeline of the entire clvsterfvck. He would post several times a day, calling out the entire banking system.

Once it all crashed in 2008 he closed shop. Bravo Keith.

“Extremely uninformed media”?

“News is what somebody somewhere wants to suppress; all the rest is advertising.” – Lord Northcliffe (1865-1922)

√

John Snider, you are trying to argue the “shortage” angle for Seattle. And that the current price level is somehow natural and organic.

What a load of rubbish. Seattle is massively overbuilt with new apartment and apartment-to-condo conversions galore. All there is is a lot of speculation, frontrunning and disappearing China-money buyers. Case-Shiller index peaked in May 2018. Active for-sale inventories are rising again.

Come back in a year and try to explain how this supposed “shortage” suddenly disappeared.

PS: Inventory hour-by-hour

https://twitter.com/coqumragep279/status/1175420918669012992

The CBD of Seattle may be over built with very high priced apartments, but not condos. However, in spite of those high priced apartments in SLU, the overall supply for any rental or “for sale” housing within any reasonable affordability is nonexistent. You can play with the numbers all you want, but the supply and demand issue won’t be solved anytime soon. You may not know this for some reason, but residential real estate is very localized, so your national Harvard computer averages are only appropriate for your coffee klatch BS discussions about the world in general.

What one earth are you rambling about?

“your national Harvard computer averages are only appropriate for your coffee klatch BS discussions about the world in general.”

Huh????

“Supply and demand”. Someone shows numbers demonstrating supply increasing in Seattle, prices decreasing and sales decreasing (aka demand decreasing).

“Numbers and data are fake news for them Harvard elites”

Look out below next year when there’s no big drop in mortgage rates like this year to stimulate another bit of demand.

I agree with some of your comments. The limited supply (Government regulations, systems development charges, and zoning laws being a major constraint.) I’m a long time realtor. I was floored in 2003 when I realized that our government (House and Senate banking committees) changed the rules for lenders permitting the creation of “No Doc Loans” (AKA Liar Loans). Those lending rules became effective social engineering rules as banks were threatened legally if they failed to process these loans. As a realtor at the time, I decided to warn buyers beginning 2005, to consider NOT buying. The hoax was extremely disheartening. One of my last clients (whom I warned) lost at least $150,000. When I voiced my concerns they told me that they had “never heard such a thing” and decided to buy in spite of my warning. After the crash, rather than permitting market forces to correct the mal-adjusted government interfered with housing market, the government got involved again. Interest rates should be the corner stone of any free market economy. The market should be the only force able to affect interest rates. The cost to borrow money must be a free market function. Otherwise, we may find ourselves in the very extreme and dangerous “market” situation we find ourselves in. What happens now? What happens to the housing market if mortgage rates rise to say 5.75 %? (Well below historic rates formerly established by market forces.) Remember to that struggling taxpayers must pay the interest to service our government debts as well as their own.

John Snider,

If 70% of the potential home buyers cannot afford this spike in housing prices, then where is this large demand coming from? Does this mean that the 30% who can afford these prices are buying up everything available en masse?

I would say in the Phoenix metro this is a definite possibility considering the amount of flipping (or rental conversion) I see going on. Half the houses in my old neighborhood are getting bought up at ~$250K a pop then relisted at $500K+ after serious renovations. Thing is, I don’t see any of them selling for these insane initial asking prices. Only after they’ve dropped $20K-$40K do they seem to sell. Maybe people think they are getting deal at that point…

Uniformed such as the meaning of what a recession is and what a housing bubble means. They use those terms as simple easy throw away explanations of economic conditions that they know nothing about, yet they are able to put fear into their audiences and have no accountability for their bloviating about whatever the crib notes tell them to say.

LOL, if the shoe fits….then look in the mirror.

Someone didn’t save his commissions checks. Dont be angry at the messenger. Just tell your sellers to drop their Bubble high prices.

I moved in Silicon Valley last year and every article I read was about writing love letters, offering 100k r 200k over asking, skipping home inspection, etc. I guess this was responsible during the Bubble but now talking about it not? Now prices in San Jose and San Clara are down 10 to 15% YoY. It was this blog that saved me from making the biggest purchase of my life during the biggest housing bubble 2.0. This blog and Ben Jones one.

Here’s some anecdotal ‘data’ for you:

Last April I closed on this house in NW San Jose:

https://www.zillow.com/homes/1070-keltner-ave-san-jose-ca_rb/19604504_zpid/

I accepted an offer a day after listing for $1.3M; that buyer got cold feet but my agent had another in a day with an offer at $1.305M (he was very sharp, did all the promo in social media and charged only 3% commission as he handled both sides of the transaction).

This is a nearby ‘comp’–with the exact same late ’50s tract house floor plan–that I see finally has a contingent offer. It was on the market for over 50 days and has many upgrades and improvements–including a ‘lap’ pool–over the house I sold (but is located close to a park the locals affectionately call ‘Needle Park’):

https://www.zillow.com/homedetails/1111-Boynton-Ave-San-Jose-CA-95117/19604559_zpid/?

There is 50% chance that you will regret you did NOT buy in 2018 or 2019 when you have 10% down. And yet, you have 50% to pick up something 40% cheaper.

Wolf and Ben Jones can both be wrong big time and yet they can be correct. The rule #1 of speculating is to be able to absorb either outcomes. Yes, house is a speculation now says opposed to stable price well justified consumption item. We are all forced into the casino.

qt – You are talking about the Bay Area which is unique with insanely high prices driven largely by Chineses money launderers. This area is also getting hit very hard by the change in the tax reform act.

The rest of the country is not overvalued because there was no large scale foreign investment speculation or material impact for the change in tax law.

There is no national housing bubble. Housing prices change based on interest rate fluctuation and supply/demand dynamics. The weakeness in the market last year was due to interest rates going up to 5.0%. Now that rates are back down to 3.5%, it seems to be full steam ahead for housing prices again.

The Fed still has plenty of ammo also. What do you think will happen to Bay Area real estate when mortgage rates are negative?

These Shiller Index charts are not inflation adjusted, correct? With let’s say an average CPI for housing of 2.5% over 10 years, that would account for 28% increase. The other way to look at it would be indexed to the cost of a mortgage, i.e. for a fixed $ payment for principal and interest, how much house can you buy.

It is easy to agree that it is a bubble. It is much harder to forecast how it will unwind. So far it is inflation that has only affected asset prices, but not people’s incomes. Deflating the bubble requires a crisis, but we could see in ’08 that the deflation was short lived.

So consider the scenario that is not currently priced into the markets, and that is a return of inflation. The current inflation breakeven priced in is 1.65% for 30y. Is it still a bubble? Maybe, but much less so.

Tony,

“These Shiller Index charts are not inflation adjusted, correct?”

The Case-Shiller data IS a measure of inflation, namely house price inflation. If you adjust this data for CPI, all you see is which is greater: consumer price inflation as measured by CPI or house price inflation as measured by CS.

What you’re asking for is an affordability index – a formula based on local wages, local home prices, mortgage rates, insurance costs, property taxes, etc.

I look at the affordability index for the Bay Area on a quarterly basis when the C.A.R. comes out with it. It’s terrible. A decline in home prices causes this affordability index to improve, as does declines in mortgage rates.

Those charts are scary. A lot of those properties are probably financed with 10% down. A 50% – 100% ride on that slim piece of equity is not a sustainable situation.

Old-school – Why is this not sustainable? What if the Fed drives mortgage rates from 3.5% to -0.5%? Negative interest rates are very real and are coming to America. The banks are going to start charging depositors interest and paying people to take out mortgages.

Houses in major metro areas will cost $4M in ten years.

Ed,

Negative mortgage rates long term means that most other interest rates are negative as well. This will wipe out the US banking system.

In countries with negative interest rates (they’re only slightly negative), the banks are in DEEP trouble already, and they’re begging the central banks to give them a break on negative interest rates. And they’re getting a break. The ECB, the BOJ, and the SNB have all introduced “tiered” policy rates that exempt a large part of the deposits that banks have at central banks from negative interest rates. That didn’t resolve the banks’ problem, but it stopped making it worse.

Not even Japan and the Eurozone have negative mortgage rates.

In the US, the banks own the 12 regional Federal Reserve Banks. The Fed’s job is protecting and enhancing the banks since most of the Fed is owned by the banks. So what makes you think that the Fed suddenly would want to kill the banks?

Dream on about negative mortgage rates. Not happening in the US.

Wolf – The economy is addicted to rate cuts. It’s the only thing that props up real estate values which drive consumer confidence and spending. Many corporations are also dependent on the ability to constantly refinance debt and borrow cheaper than previous years.

The Fed has no other option. It will continue lowering rates until the entire banking system collapses. If they don’t, the economy will collapse first.

I have been helping a widow and her neighbor redo their lawns. It’s a fall thing around here. It’s kind of painful to watch the money flow out. Between city taxes, HOA, utilities maintenance, lawn maintenance and watering I doubt if people really know the monthly cost of home ownership. It’s OK if your nest is your top priority, but it’s not mine any more with kids all grown.

Perfectly said. I can’t afford my home with a full time job. How do I expect someone else to. Our school system is lousy and city charges for everything. And delevopers get tax breaks but residents get inceases on over assessed properties. If not enough housing than why so many empty houses? Because buying property isn’t a sure investment as once was. Cities without big increases have prices to high for average person to afford. Just wait a few years and foreclosure will be their biggest issue. Real estate for profit isn’t a easy anymore. You’ll make your money back on purchase but not holding costs. I’ll sell my for more than it was purchased for but not costs of interest on mortgage and other costs of ownership. My taxes are like buying my house every one and half years if you use the original purchase price it had 1951. Took 30 years to pay off. We don’t have mortgage and can’t afford to keep it with full time job on costs to maintain and taxes which doesn’t include water, sewage and garbage. It’s ridiculous hidden costs of ownership that you aren’t told. Only people that make money are the ones that can build when demand is there not people trying to emulate pass market trends for profit. Here’s a thought: what’s the difference between high-end housing and low cost housing? Where I live it’s the neighborhood. Built the same but with different zip codes.

“Here’s a thought: what’s the difference between high-end housing and low cost housing? Where I live it’s the neighborhood.”

Ta-da! Once the craftsmanship has been lost, the only way to produce mid-high end buildings is “Build in a better area, bigger, and with more expensive finishes”. But same garbage underneath.

re: “We don’t have mortgage and can’t afford to keep it with full time job on costs to maintain and taxes which doesn’t include water, sewage and garbage. ”

Well, to be fair, you’ll pay for ‘water, sewage and garbage’ if you rent, too (ask me how I know).

I got lucky and found an old home as part of a farm to rent. It’s kind of built up around the farm and down to 14 acres. Taxes that owner pays are around $1000 per year. He rents out the two old homes on the property. Everything is automatic draft. He leaves me alone, I leave him alone. Rent is $450 with water and electric it averages about $575 all in cost. It’s a man cave and that’s exactly what I want.

But all of those things you talk about are knowable before purchase. Who buys a property without being very aware of what it will cost every month? And more importantly, how much is it going to cost me this time to help bail out their poor decision making?

I gave up on my housing search in the south bay. Of course I wish I’d bought any time between 2010 and 2016 when I was sniggering at the concept of paying so much for so little, whereas now I am faced with paying much more for that so little. But that doesn’t mean that now is the right time for me to buy either. I think that in the bay area, a year from now prices will be about the same or slightly lower than they are now, with a 10% chance of something really wacky like a huge crash happening … so I feel no hurry anymore. I can put up with my tiny apartment for another year.

My general feeling is that many buyers feel like I do. And there are alot of sellers who also will not accept the concept of lowering prices, so I have seen many places that sat for 3 months with little to no price reduction, then were simply taken off the market and listed for rent instead. As far as I can tell, those people aren’t getting the rent they are asking for either (most reduce the rental price before taking the rental off the market) but they probably feel it’s better to take some money in rent while waiting for a return to boomtime than taking less egregious profit now.

The rent owners are actually getting is implying the value of the house/unit. Purchase price and rent have a direct relationship and if they can’t get the asking rent, they won’t get the asking price.

I learned from real estate professionals in NYC to never pay more than around 10X rent. One rental I lived in in Florida was sold immediately after we moved. It sold for 11X the rent, and it took 3 months to sell.

Sorry just so that I understand what you are saying Petunia … your rule is to never pay to buy a property for more than 10x the yearly rent of that property?

If so, you’d never, ever be able to buy in the bay area. A place that rents for $4,000 per month will sell for $1,400,000, which is about 3x your rule.

Just imagine paying $500,000 for any livable property in the bay area … what a dream that would be.

Zantetsu,

You can pay whatever you want for a property but no real estate professional(owner/manager with hundreds to thousands of units) will pay much over 10X. That 4K per month house is not worth more than 500K, but you can pay whatever you want.

I was just having this conversation about rental prices and home prices today so interesting to see this comment.

A house mortgage should be somewhat justified by the rent the same house would receive. I can see someone paying a little bit more if there is an emotional connection with a specific place but in many west coast markets the numbers are completely out of wack.

In LA, units that are purchased by investors for rent (duplex, triplex, etc) can easily sell for 40-50% of what a single family home with similar square footage in same neighborhood would sell. This tells me people are grossly overpaying for single family. When the SHTF, and people realize that for whatever reason they have to sell in a down market (job change, divorce, moves, etc), they will desperately try to not lose the equity of their home by not reducing prices (already happening), then they will try to rent it next and will quickly find that no one is willing to pay $15000 in monthly rent for their 3bedroom house they paid $2.5m for because a unit of similar utility is in the market for $5-$6k. That’s going to be a tough wake up call.

Also add to that that rental prices are also weakening in some markets. It’s not going to be pretty.

Petunia – the thing about the bay area is that housing is a speculative investment market. If you make a sophisticated spreadsheet calculating your overall cost/return over 10 years when buying vs. renting, housing can easily come out ahead even at 30x housing cost vs. yearly rental cost, *if* the house value appreciates at 6% per year — which bay area houses have done over the past 9 years.

Of course, you are also terribly, terribly screwed if you lose on that bet and your leveraged $1,200,000 mortgage loses money instead of growing at 6% annually.

So it’s a risky investment, but lots of people are still bullish on future prices which is why they continue to prop these inflated prices up.

I personally am not bullish — if I was, I’d just sink every possible dollar I could into leveraging myself into the most expensive bay area home I could and, like my friends who did so in 2010, find myself several million dollars richer 10 years later. But I don’t think that’s going to be happening over the next 10 years, that ship already sailed, and I missed the boat.

re: “… the thing about the bay area is that housing is a speculative investment market …”

Only partially true. People buy homes in the BA because they have high-paying jobs in the BA. The alternative is commuting from Gilroy or Morgan Hill–also expensive–or the Central Valley; I’ve known quite a few people who do this: up at 3am, on the road by 4 and home by 7pm it you’re lucky and there’s no fender-benders on Hwy 580 (‘telecommuting’ isn’t really a full-time option for most).

The couple who bought my house were Asian-American, but not speculators; they both worked at Apple HQ about 3 miles away as the crow flies (a half-hour or more ‘commute’ nonetheless).

Petunia – This rule was probably used when interest rates were much higher. It probably makes sense to buy if the property would sell for 20X-25X rent. i’d rather buy a $800K-$1M house than rent the same property for $4K.

@Dian and Zan,

I agree with your comments but would add that is exactly the reason why some individuals chose a particular profession or specific location to buy, before reality bites. Those choices self-sort people into where and how they live.

For example, I live rural in a very nice home on a river. (Taxes $900 per year). If I was a doctor or lawyer I could not live here because there would be no work for me. But a carpenter, welder, logger, truck driver, even teacher, can all live here and live very well. If I took those (working/hands on) careers to a city where the higher paid professions find employment, the carpenter, welder, etc would be forced to live in subsidised housing, or worse…maybe renting a real hole, while the highly educated will thrive.

My electrician son lives a far nicer life and has a much better home than his accountant/engineer/teacher cousins who all live in US cities, one of which is in the Bay Area. It is all relative amongst the relatives, I guess. :-)

Stuck and/or screwed is spelled the same way, everywhere. Gotta plan ahead and hope the pieces fit.

Once the 2.0 dot com bubble bursts then watch home prices fall on both seaboards. It finally looks like unicorn valuations are starting to reflect the need to make a profit. Lay offs at the unicorns are starting.

Wolf,

I’ve been in the building industry for the last 40 years. House building and contractor stuff. Moved to loghomes and timberframes and watched that collapse along with the small mill suppliers…

Over the decades, the regulations and safety requirements along with the workers rights are astronomically unreal to anyone wanting to start in the business.

We have lost a whole class of hands on crafters of buildings for the cheap slap together, last 40 years buildings.

So much infrastructure is going to decay and disarray as the buildings used to take multiple years to build are replaced with the cheap slap together and ugly buildings.

This downturn will be long slow and painful.

The housebuying craze has gotten so nuts that my old hometown which is way out in the boonies are over 100,000 dollars overpriced due to the speculation craze.

I personally value homes built in the 1970’s, 1980’s and early 1990’s over anything built since then, because I believe that the craftsmanship and expense put into build quality was markedly higher then. Maybe I’m wrong, but I believe it to be true. I tend to shy away from anything built since the mid 1990s and absolutely will not buy anything made in the past decade, the latter because I don’t want to cook in my living room which is what the current crop of ‘open concept’ new builds want you to do.

I find that places built in the 1980s generally resonate with me. So many interesting angles, unique flows, split level interiors, just cool stuff all around. The only downside is the bathrooms tend to be kind of meh in anything built in the 1980s for some reason.

In Florida you want to buy only houses built after 1992 when the building codes were upgraded to withstand hurricanes. This was done after hurricane Andrew, a Cat 5, blew away the town of Homestead. Nothing will survive a Cat 5, but the new standards are really strong. I survived 5 hurricanes in my 2002 house.

Zantetsu – The 80’s and 90’s houses certainly have better lots, not so sure about design or build quality. 80’s and 90’s houses are incredibly ugly and most would need a gut renovation to be livable.

Joe,

I’m equally disgusted by the modern housing construction techniques. I used to think I’d hire a craftsman to build my final residence. I look at the brick and timber buildings from years past, and I can still feel the pride of their creators.

But this has changed as of late. Now I’m thinking: “why would I want to spend a huge chunk of my savings on something that just invites parasites to bleed me to dry with their ever-increasing property taxes?” A stationary target – like a house – is an easy one to hit.

And so now it just might end up being a “whatever works”, not a priority anymore, like the Old School says above.

It will be nice to see affordable houses again in 3 – 4 years like in 2009.

Another bubble comes to mind—the 1929 stock market bubble. It bottomed out in 1933, and took until 1954 to reach the peak again. Market analysts in 1954 were probably showing charts to indicate a most splendid bubble was upon them. Was it really a bubble? Only time would tell…….

I have always heard for years the Bay Area, but mostly San Francisco, San Mateo and now many parts of Oakland are immune to housing crashes, bubbbles, major reductions etc because of all the high paying jobs that revolve around tech and computers. There is just to much money. YOu have stated that you dont predict and I do agree every region is different, but the question of the economies being all connected remians real. If there is a slowdown, recession in the ecnomony, in theory this means people will spend less. As people spend less, advertising will go down. Compaines that push the hard economic line in the Bay Area like Facebook, Twitter and Google make most of all there value on people, companies advertising on thier free websites. If and when ad revenue slows, does this translate iin loss of value in the company? And if this true will this have an impact on the overall Bay Area economy which could only weaken the hoising market?

I work in tech and the Tech Bubble 2.0 is probably bigger than the Housing Bubbble 2.0. Uber has 24k employees, not counting the drivers, and they are losing billions hand over fist every quarter. How long can this continue? Probably longer than anyone here can imagine but at some point it will end. They need to be profitable and this requires raising prices and cutting costs. This applies to all the unicorns out there like Slack, Juul, Lyft, WeWork, EB, Crowdstrike, Tesla, etc.

“This applies to all the unicorns out there like Slack, Juul, Lyft, WeWork, EB, Crowdstrike, Tesla, etc.”

May as well scratch WeWork. It’s WeWorthless now…

If the CA ruling on gig employees holds, that might be the end for Uber and Lyft unless someone finds self-driving cars pretty quickly.

Amazon lost money for a lot of quarters too. Lots and lots and lots of quarters after going public. How’d that turn out for employees with stock options?

Frisco Lens –

The Bay Area is the opposite of what they tell you. Pull out a chart of Bay Area home prices going back to the 1950s, and you’ll see it’s a boom-and-bust region that is MORE prone to sudden declines. Precisely because the tech economy is a boom-bust economy, more so now with so much of people’s wealth tied up in stock options and startups rather than long-term sustainable businesses.

The dot-com recession had a huge impact on Bay Area prices, as did the housing bubble leading up to the 2008 financial crisis. The next one will hit the Bay Area hard too.

Yes my dad used to always say, the higher you go, the further the fall. The next one will be a doozy.

The Case-Shiller housing data is supposed to be adjusted for inflation. Official inflation is below 3%. I have seen housing price appreciation above the inflation rate for years. It supports a theory of a housing bubble.

Florida has seen an influx of newcomers. We do not have the high paying jobs of San Francisco, San Jose, Washington D.C. metro area, Boston, or Manhattan. As I checked realtor.com listings for property history, I saw house flipping activity. I do not know if there will be a housing crash, but am wary. What happened in 2006-2012 had not happened in decades. There were foreclosures during the Great Depression.

Shiller says housing market will crash: https://seekingalpha.com/article/4292700-robert-shiller-says-housing-market-will-crash-one-else-seems-think

Did you not read the article? The author states the exact opposite and backs his statements with compelling data.

His data would be more compelling if 2008 allowed prices to properly deflate. A crash is definitely not coming this time, but a gradual deflation seems likely. Good for owners and the economy, but difficult for anyone trying to time their entry point.

Did you not see the article has Shiller point of view and then the author’s?

Just an FYI: Dallas Market from an observer in N. Texas region. House for sale signs still going up, but the houses are remaining on the market longer. Been watching a house in a very nice neighborhood in the Little Elm/Frisco area. It went up for sale late June, it is STILL on the market. Houses in the Providence/Savannah area are not moving as fast and a lot of the signs are having “REDUCED” signs tacked on additionally to the for sale sign. Seems the slow down is happening in N. Texas area as well. Clearing of land just north of me for new houses continues, but the building has slowed dramatically. Builders in the new Union Park 380 area, are sending out tons of flyers and price reductions to induce buyers. I think the “repro” news with the banks, is reminding the consumers of the bad days of the GREAT RECESSION. Consumers are strapped, spooked and taking cover financially.

If consumers are strapped and spooked then you’d see consumer spendng going down and nobody buying these expensive homes..

I don’t see it happening yet..

Jon,

The consumers ARE strapped, they are using their credit cards just to stay afloat and put food on the table. The whole global markets are having this same issue…. it’s just the U.S. is in a little better shape than they are, so global investors are getting on what they see as the U.S. market lifeboat.

see this link: https://www.itmtrading.com/blog/the-bazooka-experiment-bigger-monetary-experiments-and-their-chances-of-working-by-lynette-zang/

Conclusion:

The Titanic has hit an Iceberg of Reality and the bilge pumps are not working as they did before. Expensive homes here are NOT selling and many are having for lease signs out front. I’m seeing this first hand here in the DFW area.

re: “… a lot of the signs are having “REDUCED” signs tacked on additionally to the for sale sign …”

Wonder how many are slapping ‘REDUCED’ signs on their lawn signs as soon as they list? Like stores that mark up prices 10% before having a ‘10% Off EVERYTHING!’ sale.

Some homeowners are having their fire insurance cancelled in my area of SoCa. So far they are finding other carriers. We are in peak fire season so maybe they are trying to avoid the seasonal hit, and there is blowback from PGE for cause. The entire US southwest is an ecological/geologic disaster in the waiting. The BLOB sits off the coast, sooner or later a harmless Baja hurricane finds a path to LA. Then state mandates are pushing up the supply of new housing, (much of it on the rural fringes where fire danger is higher) and probably not at a good time for the economy.

Ground report from San Diego North County: No slow down in sight. The price rose 100s of percent sin last few years even if it stays same or goes down couple of percent.. doe snot really make any difference materially..

ON top of this, govt is hell bent on maintaining the asset bubble.. they’d either bring the rates to zero or even do NIRP… to sustain the bubble..

Cant’ fight the system..

Whose government? Ca gov wants to repeal prop 13, that would take a big chunk from RE prices, (he wants to raise taxes) USG wants lower interest rates, and deficits, which won’t affect mortgages much. Nobody is going to write a 2% home loan in the middle of a bubble and nobody is going to put up collateral at the Repo window in the midst of a stock market bubble. Such is the nature of bubbles, they go pop.

Do you think repealing Prop 13 is politically possible ? I don’t see it happening in my lifetime..

USG is successfully able to brought down mortgage rates.. just look past in the last few weeks..

BTW, for most of the mortgages, USG is on the hook via freddy/feddy .. not the banks… they simply issue mortgages and sell it out to these gov entities..

Bottomline, as long as USG is behind the asset bubble, it won’t burst..

LA Times says, citing CoreLogic Data:

“The Southern California median home price was flat in August [year-over-year], while sales dipped from a year earlier as buyers struggled to afford sky-high housing costs”

https://www.latimes.com/business/story/2019-09-25/

I see housing starts are up in the West, how much of that is state mandated? Supply may contribute to a lower median price but somehow I doubt it. The housing market is as broken as the bond market. (How is the bond market continues and the Repo market doesn’t?) By analogy the home mortgage insurance covenant might form a parallel to interest rate derivatives. or the two markets are joined at the hip, though mortgages seem to be a consumer anomaly to real rates.

Many of the newly minted stock option millionaires from the unicorns over the last several years have been able to buy property in the bay area using the book value of these instruments as collateral or the actual payment for loans on real estate. What happens to the loans of WeWork and Juul stock option real estate buyers as the stock value of those companies craters and perhaps goes to zero. Do we see some kind of real estate loan margin call resulting in foreclosures?

Wolf, care to draw a trend line through these graphs? My eyes and my read compression are in disagreement.

I’ll draw a trend line through these charts in the middle of Housing Bust 2. You’ll be shocked by the trend.

Would be interesting to see these charts reflected in inflation adjusted monthly payments and (possibly) down payments.

The real question is what payment can the consumer bear? If the prices are flat even with a sharp drop in mortgage rates, that is a much more unhealthy market than the chart tends to show. And unless you buy into the negative interest rate garbage, the monetary interventionists are about out of ammo.

My assumption is we are really overdue for a mean revision in the pricing of bay area homes. While I do not know when that will happen, it has the potential to be a significant. Maybe Wolf could create an article on possible scenarios of where the mean might be based on the chart . If 2007 was a bubble, then this one is far worse.

This is weak analysis. First, 40 percent appreciation in about 10 years from a market TROUGH does not indicate a bubble. You’re using linear scale instead of logarithmic which is inaccurate and always falsely shows things “accelerating recently”. You use nominal dollars, not real, which properly account for inflation. Having a few percent decline doesn’t show a bubble popping, just don’t get used to year over year 10-20 percent growth. For better analysis of all relevant factors, better to look at the following data (I have no stake in this research house) https://seekingalpha.com/amp/article/4293633-housing-market-bubble

Daniel,

Please note that there is nothing in this article about a “national home price,” which is the data point your linked Seeking Alpha article discusses.

The reason I don’t discuss a “national home price” is because there is NO national home price.

There are local markets. Some are bubbles, others are crushed, or just emerged from being crushed.

That’s precisely why I do the whole series — so everyone can get used to the idea by just looking at the charts, which all look totally different, that there is no national home price.

So yeah, if you average out San Francisco and Cleveland, there is no bubble in San Francisco and no crushed market in Cleveland.

Having just moved to the Bay Area (& renting), I’m grateful for your posts about the housing market.

The average income in Los Angeles is $63,000.00. The average home price in LA is over $600,000.00.

Tell me this is not a bubble.

If there are 3 houses to buy and 25 buyers, the average salary of the buyer is irrelevant. Even more irrelevant if the average buyer isn’t in LA (plenty of out of town/foreign speculators, especially in the big west coast markets).

Not that we’re *not* in a RE bubble – I believe we very much are. Simply that these particular numbers aren’t necessarily evidence of it.

Lots of the West Coast were pumped up on China money fleeing to RE. That drying up will have just as big of an effect as interest rate movements. Will be interesting to see what happens – saw China home-buying is at a seven year low. Usually that would put a floor under CA real estate if job losses/recession/more fundamental US factors weaken, because incoming Chinese money has been omnipresent since 2011 around here (Bay Area).

It’s tough to sit on the sidelines and watch right now, but I just feel like if you can wait a bit longer and see this play out, it might be best.

Famous last words, I know.

There’s definitely something wrong with China right now, but we don’t know what it is.

To stay in theme it’s getting extremely hard for Chinese firms to get capital out of the motherland: see how both HNA and Fosun were not allowed (or were not able) to prop up their failed investments in Europe any further resulting in carnage and mayhem.

Right now the Chinese government has adopted a line of “only technology and the capital goods we cannot manufacture, yet” as guidelines for allowing the export of capitals. Granted: deep pockets and even deeper political ties can obtain a waiver, but the days of “buying” EB-5 visas by buying quotas in US luxury hotels are clearly over. The new EB-5 rules coming in being in November will complement much tighter controls by Chinese regulators.

But…

Real estate markets worldwide are completely nuts right now, and that’s in spite of diminishing returns. I’ve kept a weather eye on CRE in the German market (healthcare sector) as an investment and margins are getting thinner by the quarter: purchase costs are off the scales for what you get and the effective annual yield is getting thinner through a combination of factors, last but not least the huge number of brand new CRE coming on the market. And that’s in spite of record-low CRE loan rates and Chinese buyers making themselves scarce.

Even a small dip in percentage terms (say 4%) can wipe out a whole lot of equity with such sky-high valuations, and since Sod’s Law is infallible when it’s time to sell you’ll be stuck in a typical Italian/Spanish/Greek/Portuguese scenario: a sky high paper valuation but zero buyers.

Where are SoCalJim’s buyers ruining each other with extravagant (and obviously all-cash) bids when you need them…

Fair enough, Wolf. But you are only responding to the last point/link. It just shows there is way more to bubble assessment than just the housing price. For example, how would you say income/mortgage payment has changed over the last 13 years since the last Bay Area peak? The nominal index had gone up 41% (in 13 years!) and about 80 since the trough (!) In 11 years. I would suspect that income growth is similar or higher to both those numbers. So all you’re showing is scarcity of supply given demand, or that houses are properly priced. And I do think you should use log or semilog scales and real dollars. Finally, one year of flat (or things just looking normal for a change) doesn’t mean bubble popping… I apologize if the comment, especially the first phrase was harsh. I take it back and appreciate your dinner response and certainly I’ve been checking you’re analyses when you’re posting. Thanks

Dinner -> sober :-) … But now that makes me hungry…

With the exception of Washington DC, all of them look like classic bubbles. Washington DC looks like it had the 2006 bubble pop, but the rest of the graph looks like the normal gradual appreciation of real estate with the seasons clearly delineated by the “rolling hills”.

Every city but Seattle was positive. And Seattle was the #1 city for housing for 2 or 3 years. So it makes sense it’s the one city that’s slightly down.

Overall housing is just fine and all the talk of crashes and recessions from 6 months ago seems silly.

https://www.sfgate.com/news/bayarea/article/Bay-Area-Home-Sales-Slip-To-9-Year-Low-14471743.php

IS this the top of the bubble?

No. The top was last year. Prices in the Bay Area are already down year-over-year.

https://wolfstreet.com/2019/08/15/housing-bubble-2-in-san-francisco-bay-area-silicon-valley-is-cooked/