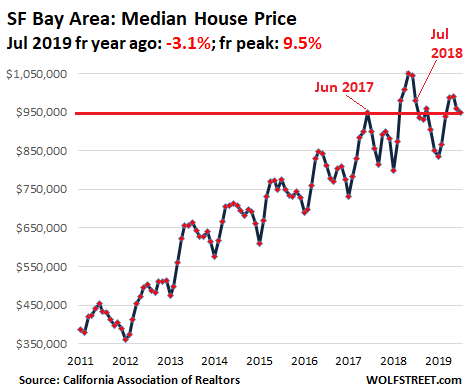

House prices dropped again – and ironically the most in San Francisco and Silicon Valley.

In the San Francisco Bay Area overall, house prices dropped again in July compared to July last year. They dropped in eight of the nine counties on a year-over-year basis: Silicon Valley (Santa Clara and San Mateo), San Francisco, Marin, the Wine Country of Napa and Sonoma, and the East Bay (Alameda and Contra Costa). The only county where house prices ticked up year-over-year was in the least expensive county, Solano.

The drops pushed the median house price for the Bay area 3.1% below where it had been in July 2018, and 9.5% below the peak in May 2018, according to the final data by the California Association of Realtors (C.A.R.). The median price is now back where it had first been in June 2017:

Sales volume of houses in the SF Bay Area ticked down 0.6% in July from the already depressed levels a year ago.

“The market will continue to be challenged by an overarching affordability issue, especially in high cost areas such as the Bay Area, which requires a minimum annual income well into the six figures to purchase a home,” the CAR’s report said.

In California overall, there is now a bifurcation: Condo prices are already falling on a year-over-year basis, and house prices are still rising. The median condo price in California fell 3.1% in July compared to a year earlier. But the median house price rose 2.8%.

The median house price by major region other than the Bay Area, in July year-over-year:

- Central Valley and Inland Empire: Biggest gains in the least expensive regions: +5.2% and +4.1% respectively.

- Central Coast: -2.0%.

- Los Angeles metro +2.8%.

But some parts of the Bay Area are starting to have a wild ride. This is a vast region with a population of nearly 8 million people, separated by the various Bays. The big convoluted body of water with just a handful of infamous bottle-neck bridges has a hefty impact on congestion and commute times, and therefore on the dizzying magnitude of home prices. These prices get less dizzying the more time the commute to San Francisco and Silicon Valley takes during morning rush hour.

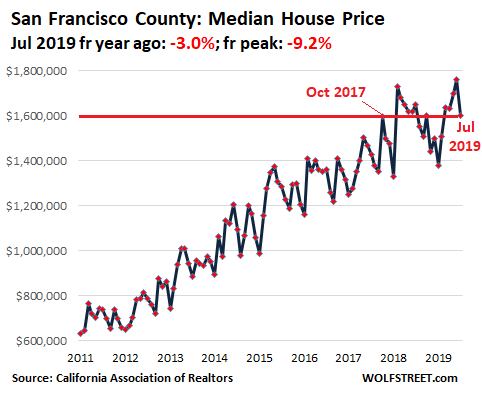

San Francisco

In San Francisco and in Silicon Valley, house prices were supposed to explode, fueled by the lowest mortgage rates in nearly three years and by the IPO billionaires and millionaires from Uber, Lyft, and other companies that would suddenly be buying homes, a time-honored real-estate hype that had been proven wrong before (here is my take: Why the Wave of Mega-IPOs Won’t Bail Out the San Francisco & Silicon Valley Housing Bubbles). And little by little, the results are trickling in.

In San Francisco, the median price of single-family houses plunged 9.2%, to $1.6 million, from the record in June that had beaten by a hair the last record set in February 2018. The median house price is now 3.0% below where it had been a year ago and 9.2% below the peak. It’s back where it had first been in October 2017:

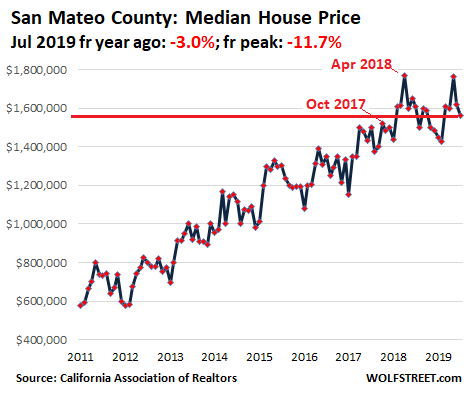

Silicon Valley

In San Mateo County, the northern part of Silicon Valley, the median house price in July fell 3.0% year-over-year, to $1.56 million. House prices are now down 11.7% from the peak in April 2018 and just above where they had first been in October 2017:

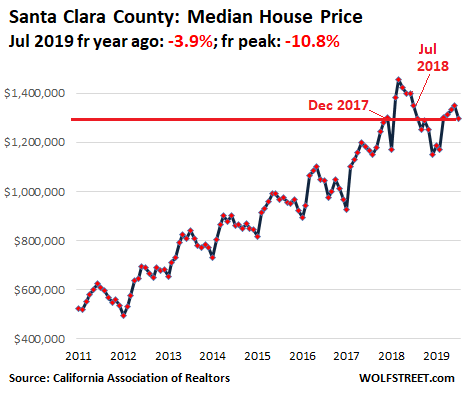

In Santa Clara County, the southern part of Silicon Valley and the most populous county of the Bay Area, the median price of single-family houses dropped 3.9% year-over-year, to $1.298 million. It is down 10.8% from the peak in April 2018 and just below where it had first been in December 2017:

North Bay & Wine Country

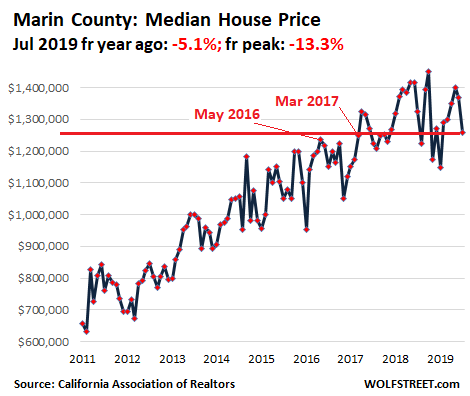

Marin County – think Sausalito, Mount Tamalpais, National Monument Muir Woods, Stinson Beach, and Highway 1 along the Pacific Coast – connected to San Francisco via the Golden Gate Bridge and ferry service, ranks among the most expensive places in the Bay Area. The median house price fell 5.1% in July from a year ago, to $1.257 million. This is down 13.3% from the peak in October 2018, is below where it had first been in March 2017, and is just 1.6% above where it had been in May 2016:

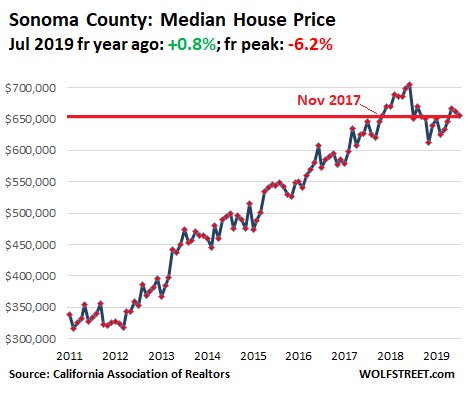

In Sonoma County, which forms part of Wine Country, the median price of a single-family house edged up 0.8% from July last year, to $655,000, but this was down 6.2% from the peak in May 2018 and was back where it had first been in November 2017:

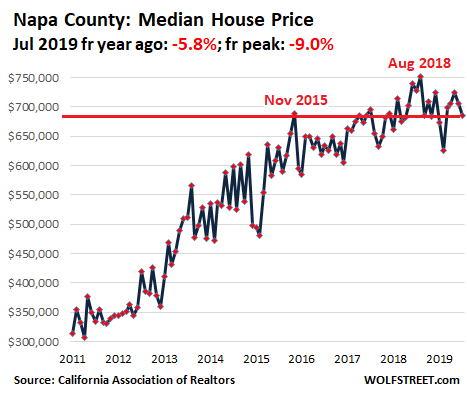

In Napa County, the median house price fell 5.8% year-over-year to $685,000. This was down 9.0% from the peak in August 2018 and was below where it had first been in November 2015:

The East Bay

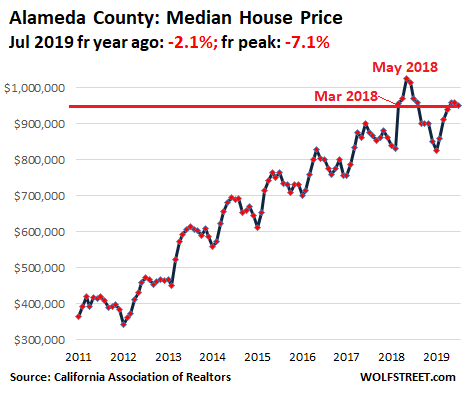

In Alameda County – think Oakland and Berkeley – the median house price dropped 2.1% from a year ago and 7.1% from the peak in May 2018, to $950,000. The price is now back where it had first been in March 2018:

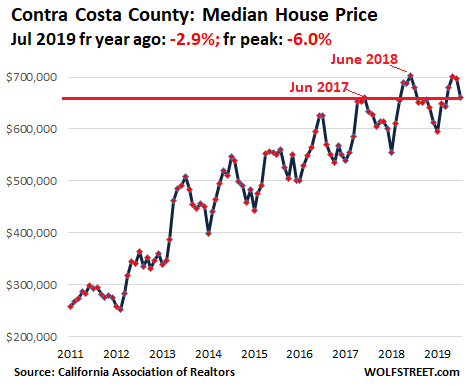

In Contra Costa County, the median house price fell 2.9% from July 2018 to $660,000, and 6.0% from the peak in June 2018. The median price is now back where it had first been in June 2017:

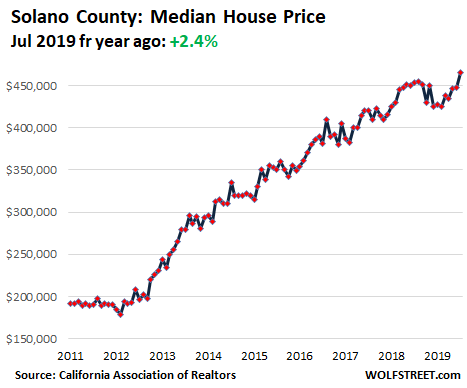

In Solano County, which extends inland toward Sacramento and is the least expensive county in the Bay Area, the median home price rose 2.4% year-over-year, to $465,000, a new record:

Cash-out “refi” hype is back full-blast. And for the first time since early 2006, people are doing it in large numbers. Read… Fuel for the Next Mortgage Bust?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Getting chopping on top line! Not a good sign!

I can’t wait until the housing market bust. It’s going to be fun seeing greedy banks, investors, hedge funds and landlords get slaughtered during the next downturn.

In Socal, am seeing a lot of new pendings over the last week. This market has turned the corner. The fence sitters missed out again. I am even seeing stuff in the 3M and 4M range starting to move. Hopefully, the mortgage rates remain low for a while …

This honestly made me laugh! Thanks for adding a little levity to my diet today of dire economic news. I idea that tapped out buyers in a market ~1.5 million homes about to enter recessionary waters are going to drive it up to double that is hilarious.

I guess if the Fed prints enough money, it’s possible in nominal terms.

PW , in LA, 1.5M in a good beach community is not a problem. Those have been moving. But the above 3M market has been tough for about 8 months. This rate decrease has finally caused a few bidders on the higher priced stuff … some of the better deals are going. For this to keep going, the rates need to stay low for a while.

You can win insignificant battles and lose the war. POTUS is tweeting walmart has good numbers today in the big picture of retail appoclyse published by Wolf for the past two years. POTUS shouted at the crowd saying China is willing to meet half way and nobody cares any more. I wonder what does it do for Socaljim to shout at the fence sitters. I don’t know whether recession is coming or MMT guys in Washionton is going to infrastructure spending/ green new deal the shit out of the economy and stagflate the whole world of zombies. What I do know is that this is NOT 2013 any more. People has changed their minds.

JZ,

WAIT A MINUTE… I NEVER ever said there is a “retail apocalypse” – I said there is a “brick-and-mortar meltdown” and a “boom in ecommerce.”

And we saw today: Walmart’s brick-and-mortar business outside of groceries is melting down, and its ecommerce business is BOOMING (up 37%). I have discussed Walmart here before to that effect.

Same at Macy’s only a lot worse, because Macy’s doesn’t sell groceries, unlike Walmart. And groceries are still doing well at brick-and-mortal stores [“brick-and-mortal,” my classic Freudian slip, as pointed out by brendan dooney below]. Macy’s brick-and-mortar sales are collapsing, and its online sales are booming, up by the “double digits,” as it says.

I have caught HELL here for stating time and again that consumer spending is fairly strong, and that retail is fairly strong, driven by the boom in ecommerce, though brick-and-mortar sales at “mall stores” as I call them, are falling. Department stores at malls are DOOMED. But non-mall stores – gas stations, auto dealers, grocery stores, which are about 50% of total retail – are doing OK. And all the while, the ecommerce boom continues.

We’ll get the new ecommerce numbers shortly. So make sure you read my article about it.

I only have these handy because they were just emailed to me.

Irvine, Tustin home sales fall 11%; countywide pace slowest since 2014

https://www.ocregister.com/2019/07/08/irvine-tustin-home-sales-fall-11-countywide-pace-slowest-since-2014/

Santa Ana home sales tumble 16% in Orange County’s worst first half since 2011

https://www.ocregister.com/2019/08/14/santa-ana-home-sales-tumble-16-in-orange-countys-worst-first-half-since-2011/

During this next downturn you will see deflating prices and decreasing mortgage rates. It will be very painful for those that are highly invested in real estate. I have seen this all before. Those who deny the loudest are usually the ones that are invested in RE the most.

Apologize for confusing brick and mortar with retail. My point stays, one can always find one good number to talk about as if it is a “true” representation of the state of market or economy. What’s more, everything else is “fake news”. Beach community in LA moved, so everything else does NOT matter.

JZ, I can only tell you what is going on in better LA and OC beach cities, and in parts of Boston. I watch those very closely. I don’t know what is going on in other markets … too much for one guy to watch. But, in the areas I know, the jump in pendings just started one week ago. It was a significant jump. I would guess the same pattern exists in many other zip codes. This will be an upside surprise.

Just one anecdotal Sonoma Co. rent flash hot off landlord’s presses;

5.1% Aug bump has been completely rescinded as of 2 min ago.

Over 55, appx 200 apts, mostly 1 bed, maybe 10-20% 2 bed. LIHTC totally non-luxury 3 story hotel style housing, but great location. Think it was part of letting developers build all the Fountaingrove stuff. Which mostly burned in fire.

Far out!!!! I’m damn lucky to be here.

Boston area here, south of.

My neighbors homes is 2 down from me was on the market. I saw new cars in the driveway yesterday. It was listed for $346,500.

It sold for $356,500. I calculate that to be $10,000 above asking.

You suckers really missed out. Those $3 and $4 millions shacks are done, gone, see you later! You snooze, you lose. Better luck in 10 years after housing bubble 3.0 POPS! LOL

qt, your comment … I made a mistake. I should have said the fence sitters looking for low end homes in good areas ( i.e. starter homes ) missed out. Those are hot But, the jury is out on the $3M and up homes. In that price range, there is some interest, but high end fence sitters are still OK.

I live in LA … well, kinda – I’m staying in hotels during the workweek now and staying with friends and family on weekends.

You’re right that the market is still crazy now for anything people can reach. Rents are so expensive that it can seem worthwhile to buy almost anything.

It’s funny how personally some take the housing data, like we’d somehow win a crusade for lower prices through argument. The market is what it is, and it certainly seems tilted against buyers down here.

Uh-huh.

They are gone because instead of being 3-4 million they have been reduced as much as 50%. Chinese money launderers have disappeared and coastal CA is experiencing that impact. High end crashes first and from MY local observation, it is crashing. Realtors and investors may say to the contrary but they have no evidence to backup their pipe dream of to the moon real estate.

That is not what I am seeing. Seems like beach close homes north of 3M, and especially north of 4M are selling for less than they were last year. But the little 1950s homes near the beach that are under the low 2M mark are selling for more than they were. That is what I see.

I’ve seen a jump in pendings in Boston in the past few weeks, too. Since maybe about the weekend after July 4. Existing homes seem to be moving much faster than new construction, which are still seeing prices getting slashed and sawed. Most closing data I am seeing shows houses are going for or below asking, much fewer bidding wars at a premium over asking.

Still not a great sign that it took a plunge in rates to get volume back up, just going to push the bubbles up a bit more before the fall that comes with a recession.

San Diego is the next San Francisco only with some buffer against rising sea levels. Most of SF will be ruined. So much of the recent development is on old mud flats when the water seeps in underneath it will be like a dozen earthquakes. I am hearing that Hawaii is going downhill fast, and with a few weather shifts could be a desert island. Maybe the $99 airfares did it.

” Maybe the $99 airfares did it.”

Don’t know about now, but back when I was a young buck, 65 or so, I snagged on of them-there bargain airfares, on the way out to Denver to accept an award for the quality of some of my steers on the rail.

The plane was STUFFED. Poor stewardae sweating like porcines and muttering about “Hollywood Hillbillies” under their breaths (got’ta be careful not to make a spelling mistake there …).

But, anyway, I got a freebie drink for killing a wasp got loose in loose the cabin.

That was in the days before PITA and there were no repercussions.

Thanks for the great sense of humor.

I used to go to Hawaii every couple of years for scuba diving, etc., but after a 15-year hiatus I only returned again last year (Kauai and the Big Island).

There seemed to be no new development on Kauai. In fact, the infrastructure from 20 years ago was severely degraded, nearly unusable in many places. But 2-3x as many tourists. Apparently the people making the tourism profits and the people paying for infrastructure don’t meet much. (The Big Island was a different story.)

San Diego will NEVER be San Francisco. In any respect. I do agree that building on landfill may be a disaster (for a minor portion of the city) if the big one hits but culturally and aesthetically there is no comparison. And if you’re just comparing price…I would love to see you put up some numbers. Good luck.

Totally agree.

Same old story. Same result. Prices will continue to increase. Don’t believe me

Go back several years and it’s the same old same old. Sorry folks

Yeah. I agree. Look at the charts. They go up and down all the time but mostly up. The latest drop doesnt seem to signify anything other than the same zigzag to the sky.

Nope. Not “Same old story.” These are the first year-over-year declines in Bay Area house prices since the housing bust. It’s not the same anymore. Something is broken. Actually, a lot of things are broken.

Ill tell you for sure that owners are finally price concious of repairs. Ive been selling upgrades for the past five years like gangbusters in sf. Now the owners and prop managers are getting real picky and requesting multiple bids and nit picking. One guy accused us of ‘extortion’ (haha nothing is further from the truth) and then accepted my quote. I get the distinct feeling this guy is gonna lose his shirt if he hasnt already. Too much dumb money in real estate who musta went to a seminar and thought it would be easy to own rentals. There are hoas that cant afford $500…In SF! I have hoas late on payment all over the place and developers who seem to be losing their minds. Seriously. Im truly concerned for them because they’ve become friends over the years. I definitely feel what you are saying, Wolf but scratch my head at the meaning of the charts. Brace yourselves? Is this gonna be like 08?

My strategy is keep the shades drawn, stick with the best customers and stay away from any potential quagmire projects. No new hires until after something breaks

bungee,

NOTHING is going to be like 2008. Everything is different. These events don’t duplicate. I don’t see a crash like that — though maybe I’m blind to it. What I see is a long quagmire that prices sink into very gradually with many ups and downs, just like the charts.

I was a big believer in a 2008 type crash coming but I am starting to believe the coming crash will not be as bad, most likely a crash in rentals and a 25% max drop in housing prices.

2008 wasn’t much worse than 25% in most areas. The national average was 34%. We won’t see a crash as big as 08, the run-up this time hasn’t been nearly as insane and speculative.

I’m betting on 15-20%.

What about particular markets like Seattle/Portland/Denver?

Some researchers are saying that Housing Bubble 2 is actually worse than Housing Bubble 1 in terms of the price/income ratio. Search “The Supply of Housing Has Become LESS Elastic”. Of course, this is national, and real estate is local, so YMMV.

We sold our house in Contra Costa April earlier this year in PH and feel we did pretty well on price at the time,.but since then we are already seeing a fair number of price reductions on zillow / redfin, etc. really since then, and pretty much across the board. Given Wolf’s recent data, do we wait until later this year or next year to even consider buying our next home? Where is all of this headed? Seems like SALT, House prices that are way out of whack to salaries, and SF having turned into literally shitsville, are giving me pause right now, to say the least.

Based on the attached graphs, I wouldn’t personally describe the bubble as having “popped”. Looks more like that the bubble has stopped growing.

I think it would be appropriate to use the term “popped” once a definite downtrend can be observed.

Wolf tries to be 6 months ahead as opposed to be “right” 6 months later.

There is no value to publish something that is agreed by everybody with scientific evidence.

The price may well turn north and Wolf will be proven wrong. But I think the odd that he is right is more than 50%.

Go back to the start of this “Housing Bubble 2” series (I’ve been following for almost 5 years) and you’ll see the same story. Valuations are through the roof!!! No wait, x months of lower x,y,z values so the house of cards (pun intended) is starting to come down!! No wait!!! It’s up again. Are they nuts? And on, and on, and on.

A year-over-year decline is a downturn in prices, no matter how you twist and turn it.

There is such a thing as manipulating the data too much of course, but you can also do too little. It would be much easier to draw conclusions from your graphs if you showed seasonally adjusted numbers. As it stands from a quick glance the last year does not look particularly interesting.

Max,

Year-over-year comparisons by definition eliminate seasonality because you’re comparing July to July, June to June, etc.

So I show both, YOY and “from peak.”

“From peak” is also important as we go forward. YOY only looks back 12 months. But “from peak,” after three years, will show where we were three years earlier. I introduced this measure now to be carried forward, so you can keep track of the total cumulative moves from those “peak” prices over the years until we bounce off the trough (which we will know only a while after the fact when that occurred).

BTW, “seasonally adjusted” numbers (where they exist, and they don’t exist here at the county level) are only as good as the seasonal adjustments. If the seasonal adjustments are wrong, the numbers are off too. But you can see the seasons here just fine, which is important. And YOY comparisons take care of that seasonality.

Wolf, pick a peak, any peak. Again, it’s a repeat the last n-teeth peaks. We’ll eventually hit red if we bet the same long enough

America will be much better off after the bubble pops like a nasty zit, prices return to the long run average and speculators are taken out to the woodshed and given a proper beating.

I wonder how much of the $25-30T in pension investments are in real estate, stocks, bonds, and other bubble assets. In other words, it will not just be the (semi-)aware speculators that will have their clocks cleaned.

Exactly. So called ‘savers’ have it coming too. So just trash the dollar and everyones happy.

Here in Sonoma County it depends on the town and the price tier.

I mostly work the Western part of the County and I’m seeing more days on market and more price reductions with turn key properties still selling quickly and often with multiple offers.

But it depends greatly on the location.

A week ago I was talking to a Broker who has been in the biz here for more than 30 years.

He listed a prime property in Jenner this spring at $995K, it appraised at $975K in early 2018.

No offers.

He dropped the price to $825K.

No offers.

Dropped again to $775K and I believe it will sell for that or a little more.

Jenner is just a little too far away from SF to be an easy drive.

Real Estate is priced at the margins, and corrections start at the margins…

Oh oh, somebody dropped the soap. A 30-year interest rate below 2% tells you the recession is coming full steam ahead. It’s no time to be buying a big house, unless you are the CEO that lays everybody else off.

Well known wise ass James Carville once said, “When I’m reincarnated, I don’t want to come back as Jesus, I want to come back as the bond market, and then I can scare the hell out of EVERYONE”. Is a 2% 30, and a 1.5% 10 year, of interest at all to anyone here? Who is doing that QE, anyway?

if you look at the charts, that is a seasonal drop on a long term trend that is definitely upward. You can see the same drops for other years once the summer selling season is over. So I expect the prices to keep going down till spring where we will reach another high. Especially with the yield on the 30 years breaking below 2%, house prices will be on fire again. Not saying it’s good policy, but wishful thinking doesn’t make for good decision. Prices are high but rents have almost doubled since the recession so don’t expect that we are going to see 2012 prices again, you will be renting all your life.

Agreed, anyone holding out for 2012 prices (especially nominal prices) will never buy a home. I think lowering mortgage rates from here is going to have diminishing returns. A retrace to inflation-adjusted 2015 prices seems plausible if there’s a severe enough recession.

2012 prices could happen again. All it takes is some job losses (possible) or higher mortgage rates.

I also 2013 real values are very likely in SF during the next recession. If it’s particularly long and deep, 2011 real values or lower.

The charts would be easier to read if I could tell which dots were which months. Even if just e.g. every January dot was a different colour it would make a big difference

Income is the major problem and it’s unlikely that a few rate cuts will have any impact on housing. If people don’t have increasing sustainable wages and a good feeling economy, why would a slightly lower mortgage rate matter? It’s easy to see this play out in Europe where lower rates are not stimulative and when production is decreasing and wages stagnate, people don’t give a crap about placing huge bets on expensive homes.

You omitted That San Jose the city of over one million people, the urban center of Silicon Valley, 3rd largest city in the western US and largest city in San Francisco bay area is in Santa Clara County.

San Jose is in Santa Clara County. And all data in this article is by county. So all cities in the 9 counties are included in the 9 counties. Not sure what your question is, if there is a question, but I tried to answer it anyway :-]

I live in Marin and many 2+ million $ homes are coming way down, 10-20 percent. Almost anyone who can afford the price level is probably being impacted by the SALT tax law changes. That’s why I’m sitting on the sidelines until all this settles down. I am seeing people owning their homes for 15 years in Marin and taking $500,000-$1 million loss on their sales right now. I think every person on earth should be very concerned that no central bank can raise rates to a historically normal level. Such a sketchy market. After owning five homes, I have been renting for 11 years. And I can’t really find a financial sound reason to buy a house.

I sold my house in NJ in 2018 and moved to Solano County. Theoretically the SALT changes would mean I would lose my deduction for sky high real estate and state income taxes. But because of the ALTERNTIVE MINIMUm calculation , I was not able to deduct these taxes before so the loss of SALT deduction was irrelevant .

I have one question for SF real estate professionals.How many all cash purchases are happening?

Alternative Minimum is one of the major reasons why SALT doesn’t impact the higher end incomes, but it definitely affects many others.

A friend of mine is paying $8000 a year more in taxes due to SALT.

Brilliant play by Trump to stick it to the Coastal states that are all blue.

Can you provide url of these supposed $500000 price reductions/losses? Zillow or Redfin will do.

This data is great and the insight on the article is much appreciated although sometimes I think it is twisted by wolf to the negative side. Example it’s not fair to compare a current month to a different prior month because of the seasonality in sales. Some months are naturally busier than others. Similarly we can’t compare the current month to a “peak” because that peak may not be the same “apples to apples” month. So the 9-10% decreases above are not realistic. The only thing that matters is the year over year comparison.

With that being said, it is shocking to see negative year over year comparisons in the Bay Area of -3% to -5% already and we haven’t even started the recession. Imagine when things really go south, this is going to be a blood bath. I think the tech sector has overheated and while they somewhat missed the brunt on the last recession (thus heating up faster than other sectors) I’m thinking they are going to be at the forefront of this one just like the dot com crash hit SF harder than anyone else. This Bay Area data should be a warning sign for the rest of the country.

I live in LA and have been shopping for a home for nearly 2 years so I feel I probably know the market better than even some realtors! Housing here took a turn south in the summer of 2018 with price drops becoming steeper and more noticeable and houses lingering on the market for 100+ days. Starting this year I’ve noticed resales of houses purchased in the 2016-2017 period having to go for prices lower than the 2016-2017 price. One house in particular was purchased over asking at $4.2m in 2016. It was relisted at 4.5m and after 200 days on the market and multiple price drops it was dropped to 3.9m. Still no takers. Ouch!

There is no way this bubble is going to end well. The gig economy is misleading the unemployment numbers. Corporate debt is too high. Millennials can’t afford anything, much less a $3m house, and even if they could they don’t even care to own a house. The tech sector is living a lie in “hopes” that future revenue will eventually offset expenses. When everyone and companies are forced to rein in spending (already starting to happen) and home purchases slow we are going to see the real prices for houses and my guess is that they are 25-30% lower than what they are now.

60-70 % lower. Too bad the bug payments don’t go down with the market. Pure stupidity being displayed.

+1000

They will make sure gig income will be treated as “stable”. Just wait and see.

Typo in the Santa Clara graph: the July *2019* dot should be titled July *2018*.

Also I would note that the 6-month lockup for Uber, Lyft, Zoom, etc. hasn’t hit yet, so we don’t know what effect that might have. (I’m assuming there’s a 6-month lock for not selling shares after the IPO date.)

The lockup period for LYFT has been moved up from 9/24 to 8/19 .Watch out tomorrow and next week

It’s a pity the NAR doesn’t release the median square footage along with the median price. That would really boost the informative power of this dataset.

Median price, by itself, is susceptible to changes in the sales mix.

Suppose, for instance, the Chinese investment pools have stopped buying, but new-parent US families are still buying. That would skew the sales mix towards lower-priced homes and lower the sales median. But it wouldn’t necessarily changing the price of any particular home, especially those below median being bought by those families.

A loss of money-laundering foreign “investment” demand is not a bad thing. Houses are built to be lived in, not collected.

Anyway, as an owner with no intention of selling, I hope prices do drop a bit, because it’d be nice to finally get a break on property-tax inflation, and I know a lot of young working families struggling to find an affordable place in a good location… Zillow shows an ongoing decline in our area and maybe the assessor will finally catch up?

If the lenders have done their jobs this time around, a small price dip won’t kill anyone, but it will curb the craziest of the speculators, and discourage the cash-out folks from stupidly spending equity that may not be there when they need to sell.

San Francisco made the international housing bubble lists sometime ago. They looked at price/rent and price/income ratios. It is still listed as overpriced. If rents can’t pay monthly mortgage payments, taxes and insurance, is it a bubble? Home repair bills are not cheap. If a tenant stays two years, the place may need new paint. Carpets were replaced after a few years or sooner if there was pet damage or stains.

Fundamental metrics like price/rent never matters for the past 7 years. The houses are used as a tool to receive the printed money. While rent can NOT cover mortgage, add 4% appreciation in price a year. Cover mortgage now? The thing is, the game has changed from economic analysis into “what can I do to get into the Fed money shower?” Owning houses can. Owning any “asset” can. Start up Telsla, wework, snap, Uber, Lyft, can. We dob’t need to “make money” any more. We just go where Fed showers.

Just for rant, Fed wanted to lift house prices for obvious reasons after 09 bust. Fed wants to flood the stock and bonds market so that people like Elon, wework can creat businesses to hire people. Hey think by making the the appearance of prosperity the economy will get going.

They think by heating the corpse of Epstein to 98F and he will start to talk.

A sound economy run under good rules will bring prosperity. Not a prosperity brought out by corruption will heal the economy.

But no matter how much I rant, they will do what they do and they always think it will be the next guy when the shit hit the fan.

JZ – Exactly. The Fed is giving away free money. This is the only way to get people to keep spending and investing. The Fed has given me so much free money I’m actually considering buying a nicer house or a Tesla. Why the hell not? I didn’t earn half of the money i have. just bought a house and clicked the “buy” button on my brokerage website.

Even crazier then free money is impossibly cheap goods and services. Electronics, clothing, and food is basically free at this point thanks to globalization and ecommerce. The cost of raising a child has certainly increased but excluding that, life is pretty incredible now thanks to technology and the Fed.

Everyone needs to stop complaining about a system that has generated free money and cheap goods.

Cisco just cut 500. Uber cutting a few Engineering and Marketing positions. Huawei cut…so not a good sign for confidence to buy homes. IBM cut as well as it digests Red Hat. Who would want to pay $2000 a month alone in property taxes to buy a Single family home in Mountain View or Sunnyvale or Cupertino.

Palo Alto, Menlo Park, Los Altos home sales continue to be flat to slightly up though the multiple offers have declined.

Do these smart tech folks not realize that to live in such a place is a huge pay cut? Some will scream about all the glorious equity, but that will disappear overnight when the next big tech shakeup appears. To live in these place for these jobs is folley. Big tech needs to remotely open up hubs in a few affordable places and let their employees actually realize the gains of their labor.

Jim N – Add NYC, DC, and LA to that list. Why would anyone live in a big city at this point. Migration patterns affirm our opinion that Americans are bolting from large high cost metros to the Sunbelt. The flight of Americans is being offset by importing people from crap countries to fill the apartments and do lower income service and corporate jobs.

So when is a house a house, or a money pit? Modern construction gives only about 20-25 years of life to a structure. After a score of years, it’s time to replace the roof, HVAC, bathrooms, floors, kitchen, windows, you name it. When I lived in Seattle, real estate was more about lots than houses. Buy the lot, bulldoze the house.

When is a house a home? And they only last 20-25 years? As a carpenter, construction is not that shoddy as suggested by your comment. Sure, roofs wear out as do appliances, but that’s about it. With proper maint a modern home should/will last hundreds of years. Of course I only use galv fasteners, and standard plywood sheathing as opposed to modern OSB air nailed crap, but still, your comment is off the mark.

Buying a house set our family up for retirement. 1st purchase a 60 year old shack when I was 24, 2nd…only 20 years young, but needed work to repair rental damages, etc. 3rd? renovated and I retired shortly thereafter at age 57. No money from folks…..just from workingman wages.

People often make the mistake of buying a destination home for their 1st purchase, when they should be living below their means and using money to pay off their mortgage asap. Get the house paid for and use the mortgage savings to buy another…and away you go.

Just imagine not having any living expenses beyond minor upkeep and taxes, plus regular costs of being alive. It’s called freedom. Paying rent and/or making mortgage payments is a form of debt servitude, imho.

New construction that is affordable is very poorly constructed, at least in the areas I’ve looked at. Combine that with families that don’t have the additional income to keep up with repairs, and communities that were new 10 years ago look very depressed these days.

Papa Geo – Totally agree with you. Anything that is “affordable” is priced that way for a reason….Anybody that can “afford” not to live there buys somewhere nicer.

Having to interact with the neighbors in “affordable” areas is a giant headache as well. I pay the premium not only for nicer houses, but for better neighbors as well.

There is no shortage of affordable housing in this country, just a shortage of good places to live.

No, I’m not knocking owning a home. I own my home and repair it myself, love no payments. It’s the only way to go. Just saying, paying 1.5 million for a home twenty plus years old is going to need work and updates most likely in the near future.

When one builds one’s own house, the whole picture changes.

It can build to last more than lifetime.

Paulo, we fastened the T11 underlayment for vinyl siding to the studs with aluminum alloy screw nails.

The architecture was our own, fashioned in the light of prior generation’s lifetime of living experiences, as well as our own.

For example, all the entrances (three) are on grade and the house was built in a stable rural area. My mother’s father had to leave his house late in life because it had stairs to every entrance and it was located in a populated area which was “overtaken by events” as the lawyers say.

It simply doesn’t occur to most folks how much real control they could have over their lives, if the put their minds to it.

20-25 may be on the generous side. I’ve been looking at homes in Novato’s Hamilton Field area built in the early 2000s and the unrenovated originals are looking very tired.

dwf – Yes, unrenovated houses built from 1990-2010 are worthless to me from a buyers perspective. The majority of houses from this period need to be completely leveled. Ugly exteriors and large, cheap dysfunctional interiors.

At least half of these houses are occupied by boomers who are going to start dying off in huge numbers. I wonder if the lot with the existing house actually becomes less valuable than a vacant lot in some areas over the next 10 years.

I call that a minor correction.

Your charts show that houses are still 200% of 2011 prices.

If that is a pop, it is barely noticeable.

More so, because your graphs also show, that such minor corrections are the norm, these last 8 years.

OF COURSE this is a historic bubble and it WILL pop.

Bhut why this correction will be it, I cannot make out.

Ultimately, Proposition 13 is the issue.

The entire state of California has had its tax base shift dramatically over the last 1.5 generations. Before, the state derived 2/3rds of its income from property related taxes.

After nearly 50 years of Proposition 13, that proportion is down to 1/3. The shortfall has been made up with income, sales, and other taxes.

The problem is that the local governments can’t really raise other taxes – and these are the organizations that fund schools.

Established areas which are wealthy in property price terms have really poor schools because the tax base has been eroded by homes with 1980s era property valuations (1970s era homes, after 45 years of Proposition 13, are valued at 1980s levels). Combine that with inter-generational valuation passing, the tax base will never recover so long as Proposition 13 is in place.

Go to Zillow and browse around San Francisco, for example. You’ll see that many of the $5m homes pay $2K to $3K a year in property taxes – meaning they’re valued at $170K to $250K.

If the same home were purchased today, the lucky new owner would have to pay $60K a year in property tax.

Is it any wonder that the public schools in SF are abysmally bad?

Unfortunately Repealing Prop13 will never happen because so many current homeowners benefit from it.To me the most ridiculous and unfair part of Prop13 is the inheritance of the original(adjusted for the small annual increase) price .

My calculations result in similar $ taxes as yours. I figure that new houses in Northern Cal pay about 1.125% of market value in property taxes.

I just posted a link to an article talking about a Proposition 13 repeal ballot proposition that has qualified for the November 2020 ballot, and how the ballot sponsors are clearly looking to split the opposition.

I actually disagree that current homeowners matter. The percentage of voters with significant Proposition 13 subsidies is likely not very high by the very nature of how it works.

California home ownership is also a lot lower than national average: around 55% vs. under 65% nationally.

While people who have purchased a home more recently might vote in order to preserve their future benefit, it is just as possible they’ll vote to stick it to those people so transparently benefiting from Proposition 13 – especially if lower property tax rates are now on the table as a consequence.

In any case, the ballot sponsors are clearly being very pragmatic in their political positioning – excluding small businesses and likely at least lower valued properties.

Prop 13 also impacts commercial properties, such as Intel’s campus that it bought decades ago and for which it now pays peanuts [well, almonds maybe more appropriately] in property taxes.

So this will be an interesting debate. Commercial interests, landlords, and companies of all kinds are solidly lined up against a repeal, and they’ll spend to preserve that benefit.

The bubble will pop when the herd says so. Right now, the herd is on alert, and some within the herd have already started running to a new location. The 30- year rate just hit its lowest point, EVER. It won’t be long before the rest of the herd wises up, and the change of direction will be unstoppable once it starts.

This is the time that separates winners from losers. The winners are open-minded and nimble. The losers keep clinging to that patch of pasture that has performed well in the past, with their head down.

Ironically, just read this article about a ballot initiative to roll back Proposition 13, on the November 2020 ballot: https://nymag.com/intelligencer/2019/08/2020-property-tax-battle-in-california-could-be-epic.html

From the article: “By some estimates, more than $7 billion a year in tax revenue for the state is at stake, and the war will most definitely be waged at a cost commensurate with the stakes:”

To put this in perspective: Total state education funding is $78.4B for 2018-2019, with local property taxes comprising $23.5B of that.

An earlier article by the above author listed an estimate of $11.4B per year.

What is particularly interesting is that this is very much a progressive effort in a supposedly liberal political state.

And as can be seen, the proposed ballot measure isn’t actually killing Proposition 13 completely. What it does is allow assessors to treat some properties different than others. It seems clear that the ballot sponsors will look to isolate 1% and large business owned property from everyone else in order to prevent these wealthy groups from pushing forward grannies and mom & pop businesses as fronts: small businesses with less than 50 employees and $3M property values are excluded. This is likely why the 2 articles showed different impacts: $11.4B vs. $7B.

First, if this passes it is inevitable that many businesses will either pass on the increased taxes to their customers or will move out of the state.

Second , if this passes residential home owners will be fearful that they will be next .

Third, turnout for this presidential election will be the lowest in years. As you mentioned there is no real contest for President, Senate, or Congress in most districts. The amount that Republicans will spend on media is expected to be at an all time (inflation adjusted)low,so spending by corporations to defeat any changes to Prop13 will dominate any media buys.

Prop 13 has contributed to the lack of supply of houses in Cal.Even though you are correct that this affects fewer and fewer numbers of houses each year, it does remove potential sellers from the market. This reduction in sellers combined with the all cash foreign buyers has been the main source for price increases in recent years.

I would disagree with the 1% talking point that businesses will pass on increased costs to customers. For one thing, businesses face competition: only a business with either local only competitors or monopolies would be able to make price increases stick.

Secondly, most businesses operate from leased facilities. It is debatable whether lease costs will increase quickly should a Proposition 13 split roll pass.

Thirdly, companies like Intel (as Wolf noted above) – the increase in property tax makes no difference whatsoever to their corporate bottom line.

As for “fearful homeowners” – again, this is wishful thinking. I noted that home ownership in California is barely over the 50% level; of those who do own homes, I would pretty much guarantee that a majority of them have purchased their homes relatively recently, so are not affected in any significant way. I base this on the nationwide number of 20% of homeowners owning their homes outright – a roughly proxy for the Prop. 13 gainers in California.

Lastly, turnout. A low turnout is worse for the 1% – it means the significant number of ballot signees will have a disproportionate impact on the election. Equally, a low turnout likely means the conservative voters will be less present than normal – because California is rock solid, all or nothing Democrat. And conservative owners are, reliably, far more against “more taxes” based on principle vs. liberal voters basing on “fairness”.

If you look at the graphs at where prices were in 2011, that’s where they’re headed back to when the bubble deflates. At least 50% or more devaluation when the Deflation wave explodes.

Fat fingers typed “brick and mortal”……I think I will use that.

The RE pumpers here seem to be like someone stuck in the 5 stages of grief and are at the denial stage. Instead you should learn from Wolf’s methodical reporting of the bubble unwinding and accept that the next big downturn in RE is coming. History shows that no “special place” will be spared and it will come to where you live. Unload your dicy property now and hunker down to do what you have to to service the debt on the good stuff that will have future value when the dust settles.

Also keep in minds that different areas/cities are in different stages of the bubble. For example, Vancouver, London, and Sydney are a year ahead of us while New York and Miami are a year ahead of them. Silicon Valley and Seattle are a year ahead of southern CA and southern CA is a year ahead of the US east coast. I remember last summer in San Jose, price increase slow while inventory jumps with sales collapsing. Very similar to SoCA right now but with higher interest rates! If interest rates are low now with job market strong and sales still drop 20% YoY, imagine the carnage if layoffs start happening.

Senecas,

People like you have been predicting a housing crash for, what, 5, 6, 7 years? Any day now…..

It’s cute how you accuse others of living in a stage of denial.

I’m no RE pumper, I’m a pragmatist. There’s no evidence of a housing crash. Could one happen in the near future? Sure, why not? Is one happening right now? Not even close. And if/when it happens, I’ll be there to buy myself some cheap property that will double in value 10 years later, just like the last 5 or 6 bubble/bust cycles.

However, waiting a decade to buy a home, waiting for the absolute best price seems like rough way to live life. You’ve given up a decade of your life to save, what $100K? $200K? Is that really worth it?

The lack of Chinese cash buyers is causing prices to come down. It will ensure that they crash and stay down

There actually is plenty of evidence to indicate that Silicon Valley is headed for a major realignment. I’m not talking about charts – those are made by economists who try to treat Silicon Valley as yet another abstraction.

Google and Apple and Facebook aren’t going away but they also aren’t making anyone particularly rich anymore. They are all looking outside Silicon Valley for cheaper talent. IPOs this year are awful, and it feels like they were rushed out in order to head off an expected recession.

Rank and file employees, even those with good salaries, are basically forced to rent. Silicon Valley stopped minting 1%ers a few years ago in favor of making the rich (even by local standards) richer.

The Bay Area has a long way to fall, there’s nothing about the local economy to indicate a run of new wealth being created for people who weren’t wealthy before.

Just Some Random Guy – NYC and the Bay Area are certainly crashing. A $4M house a few years ago in either locale is now worth about $3.2M and your taxes have gone way up. This is a big problem because it will eventually compress housing prices down to the lower tiers. And unless they have figured out how to defy the economic cycle and avoid a recession forever, unemployment will go up. Baby boomers are going to start unloading unprecedented numbers of crap shacks onto the market that nobody wants to buy.

Is it possible the Fed burst the housing bubble a year ago?

Here’s where the Fed screwed-up last year, switching it up … raising rates, when their model said to stay put. Inflation was never an issue and they, along with trump paved the way for a recession!

“Participants also discussed a staff presentation of an indicator of the likelihood of recession based on the spread between the current level of the federal funds rate and the expected federal funds rate several quarters ahead derived from futures market prices. The staff noted that this measure may be less affected by many of the factors that have contributed to the flattening of the yield curve, such as depressed term premiums at longer horizons.

https://www.marketwatch.com/story/heres-the-new-recession-indicator-presented-to-fed-officials-2018-07-05

Wolf,

All these charts show the same pattern. Ups and down short term with a long term up trend. One example is Marin Co which went from $1.2M to $975K in 2016 then up to $1.5M in 2018. Now it’s back down to $1.25M. By this time next year it will probably be $1.7M.

Just Some Random Guy,

We will find out right here where it will be this time next year :-]

Also, let me remind you that there was no year-over-year decline in the overall Bay Area median price during the entire period from the bottom of the Housing Bust in early 2012 through 2018. So these are the first year-over-year declines, indicating that something has broken….

In my flyover neck of the woods anything under $300K was gone in a day or two earlier this summer and anything over $500K was sitting. Now it seems to have reversed itself. The cheaper stuff is sitting while $500K+ is flying off the shelves. 3.5% mortgages has made the expensive** stuff more affordable and people are moving up.

** Yes I know by LA standards, $500K is not expensive.

500K in LA? You are talking a rundown property with major gang activity plus bars on all windows and doors on a busy busy street.

US economic prints remain strong while corporate profit margins appear to be under pressure. In my opinion, some of this pressure is inflation related … inflation from the supply chain. This is a fly in the ointment may cause the drop in mortgage rates to be temporary … the US recession scare is unfounded and much of the scare is political. “Russia, Russia, Russia” has been replaced by “Recession, Recession, Recession” … another political hoax. While worldwide growth is slowing, the US may escape the bulk of the slowdown because of de-globalization policies put in place by the president. The low mortgage rates may prove to be short lived.

SocalJim – if mortgage rates increase the housing market and stock market will both collapse just like last fall. The Fed is preemptively slashing rates to help minimize the impending blood bath. Why do you suppose the Fed is cutting and the market is pricing in economic disaster? You’re smarter than the Fed and the bond market?

I’m 70 and I find these comments of ‘I’ve seen all this before’ ridiculous. There are lot of experts out there who disagree but they agree on one thing: we’ve never been here before. These are uncharted waters.

Re: San Fran house prices. They look cheap compared to Vancouver. It just got its ONLY house listed under a million, an unlivable shack on a 33 ft lot. And prices are plunging here at a rate NEVER seen before. One guy who bought in 2018 sold for a 30% kicking: bought for about 3 mil and sold for 2. Why don’t sellers just live there? They don’t live there. Many live in China.

Everyone agrees that the single family house has become ‘financialized’. They have become an investment vehicle, like the stock market. This is not just another wave. It’s never happened before to this extent. The closest US version is the Florida Land Boom and Bust of the 1920 s, that saw raw land in Florida treated like a stock, with folks all over the US investing in without ever seeing it.

It went up and up and then lost more than 90% of its value.

Not all waves in the economy have a ten- year wave length. There is a whole field of economics about long waves, the ones from 60 to 90 years. 90 years ago we had the last stock market as richly valued as this one.

And yes, it did recover from the Great Crash 90 years ago. If you were in the market in 1929 you recovered by 1954, also the first year the Empire State Building, completed in 1933, finally broke even on an annual basis.

I agree some people are overlooking a potential correction in the long term debt cycle. There is the short term cycle and the long term cycle. Everyone thinks a recession will come and go just like the others and everything will be fine and keep going up. Let’s not forget we are due for a correction of the long term debt cycle and that could be as bad as the last depression.

Two factors that will be affecting Sonoma County home prices this fall and winter are the increase in supply, builders have been going all out not just replacing the 5,000 odd homes that burned, they have also pushed forward quite a few new home developments, Condo and apartment buildings.

Inventory and the perception that it is growing has a large psychological effect on buyers.

Another important factor is that the insurance companies have been paying market rent for thousands of people who were burned out.

That ends after two years, so starting in October a lot of the $ that has been supporting high rents will go away.

Just keep placing your bet on red.

It’s not a bubble therefore it does not pop. Traffic jams are still long. Number of Californians still growing. Companies still hiring. Still IPOs. Maybe it will grow less or stagnate a bit. But calling it a bubble is nonsense.

Nah,

It seems you don’t even understand what a real estate “bubble” is. Sure, there can be doubts whether this bubble “popped” or didn’t “pop.” But there are no doubts that prices — $1.6 million of a median house??? — are in a bubble.

But, in the bay area, the median price is not 1.6M .. it is around 800K. It is 1.6M in select areas, but overall, it is 800K. Same in SoCal … in select areas, like the west side, it is somewhere around 2M, but overall, the median is lower. I am not sure if 800K is that big ov a problem.

SocalJim – You are so smart. Tell us what the median income is and then explain how the median house is 10X the median income if it’s not a bubble. Who are buying the houses if it’s not the people that live and work in the area? This is a big mystery but it seems like it’s the combination of elicit foreign money and local people leveraging to the max to buy a shack. Foreign money is gone and the economy cannot get any better in California. The prospect of increasing values is gone, so the fundamentals don’t make sense and nobody is buying. Sales are WAY down.

Ed,

The way the housing typically works on in blue chip east and west coast cities is, more often than not, people below the median income rent and people above the median income buy. I know this from my days as a mortgage trader. We did these calcs to determine affordability. This concept that the median income needs to purchase the median home applies in many cities where the percentage of renters is low, for example Detroit and Atlanta, but where the percentage of renters is high, your buyers come from higher than the median. If you do your calcs with these adjustments, things look much more in line, and a bay area median of 800K is not that crazy.

It is very much a bubble when incomes are not keeping pace with house price inflation.

The combination of Fed interest rates and Proposition 13 is the primary reason why prices are loathe to drop. Fed rates are constrained in a band for the foreseeable future (neither significantly higher or lower), unlike the 35 years after Proposition 13 passed – up until 2008.

Proposition 13 itself is going to undergo a very interesting test next year.

Not sure what traffic jams have to do with it – a region can be both crowded and poor. Most of the people on 101 or 280 have absolutely no hope of buying a home even if prices crash.

Companies are hiring but they don’t pay anywhere near enough for most workers to get into homes if they are currently renting.

IPOs are doing awful this year and in any case most of the shares were allocated to a tiny group of founders and VCs. Rank and file employees haven’t benefited from IPOs in a long time.

Your comment represents a common theme with residents of the Valley – there’s plenty of denial because so many have sacrificed so much to be there, despite most having their standards of living reduced.

Retail apocalypse and a brick and mortar collapse is essentially the same thing .. most people know retail is brick and mortar

I know the Bay Area market well….well enough that I sold my RE there in early 2018….literally ringing the bell on the top.

The core problem is that not enough new wealth is being created. IPOs are not doing well, but even worse than the price is the distribution. In the 90s, rank-and-file employees made real windfalls off of IPOs…now its just a select cadre of founders and VCs. Even early employees who are not founders are being left with scraps. Many of the winners on the other hand are already rich, so their gains tend not to translate into consumption.

Silicon Valley has simply topped out. It will never be dirt cheap but it has a long way to fall from here.

The bubble finally popped. It’s done. I am in the real estate game since 20+ years and unloaded what I could recently. Waiting for the 40% correction to buy back in. Rinse and repeat. Done this multiple times now

bubbles (and predictions of awful upcoming local crashes) often neglect to remember this. Still, dwindling affordability is certainly a symptom of overheating, of a market being pushed perhaps too high. Looking at the charts above, it is interesting to note that the markets of all Bay Area counties hit similar and historic lows at previous market peaks in 2006-2007, i.e. the pressure that began in the San Francisco market spread out to pressurize surrounding markets until all the areas bottomed out in affordability. This suggests that one factor or symptom of a correction, is not just a feverish San Francisco market, but that buyers cannot find affordable options anywhere in the area. We are certainly seeing that radiating pressure on home prices occurring now, starting in San Francisco and San Mateo (Silicon Valley) and surging out to all points of the compass. Significant increases in mortgage interest rates – as happened in the second half of 2018 (before then subsiding again in 2019) – affect affordability quickly and dramatically, as interest rates along with, of course, housing prices and household incomes, play the dominant roles in this calculation.

I bought a house in Oakland late 2017. I sold it this spring for personal reasons, but am glad I ended up selling. The estimated sale price while I owned it was consistently much higher than what I paid, and was pretty accurate to the price I actually got for it. Since selling, the estimated price has gone down, and homes in that neighborhood have sat longer and sold for less. I’m now on the fence as to whether I should buy again in light of the impending recession and residential real estate forecasts. But I will be very happy if/when this ridiculous housing bubble bursts AND if many of those responsible for driving up the prices (techies) leave to go ruin Texas and the like.