A gigantic spike in 3 years. The UK dominates.

By Nick Corbishley, for WOLF STREET:

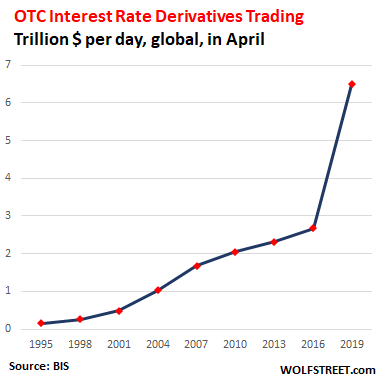

The volume of over-the-counter (OTC) interest rate derivatives traded globally soared by 141% in three years to $6.5 trillion per day in April 2019, according to the Bank for International Settlements’ new Triennial Survey of Global Derivatives Markets. In the prior survey period, April 2016, $2.7 trillion per day in trades were executed. Since 2001, the magnitude of trading volume has multiplied by a factor of 13, from $490 billion per day to $6.5 trillion per day, with a gigantic spike over the past three years:

OTC derivatives are securities that are generally traded through a dealer network rather than on a centralized exchange such as the London Stock Exchange or the New York Stock Exchange.

Some derivatives can be explosive, such as the credit default swaps (CDS) that brought Lehman Brothers and AIG to their knees in the last crisis, and which still remain a threat today, especially with the U.S. government this week bowing to Wall Street pressure to dilute regulation that had been designed after the crisis to reduce the risks of these instruments.

Interest rate derivatives, whose value rises and falls depending on the movement of interest rates, or sets of interest rates, tend to be more straightforward. They are often used as hedges by institutional and retail investors, banks and companies to protect themselves against changes in market interest rates. If managed properly, they shouldn’t pose undue risks to the financial system.

The BIS attributed much of this 141% three-year surge in trading of these instruments to increased hedging and positioning “amid shifting prospects for growth and monetary policy.” It also cautioned that some of the turnover in April 2019 was in shorter-term contracts, which are rolled over more often, leading to higher volume of trades. The 2019 survey also featured more comprehensive reporting of related party trades than in previous surveys. After adjusting for these trades, the actual increase in trading volumes since the 2016 survey is more likely to be around 120%, the BIS concluded.

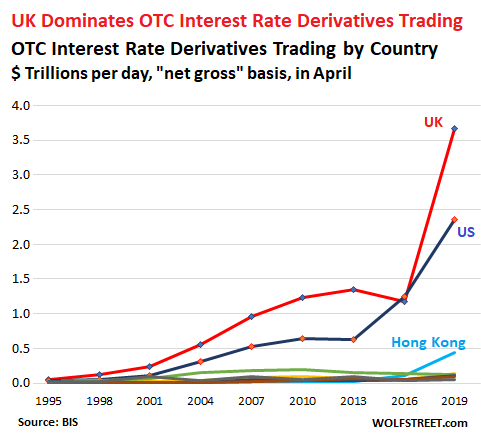

Here’s where most of the trading OTC interest rate derivatives took place:

- The City of London: $3.7 trillion per day or 56% of global trades were executed at trading desks in the United Kingdom, a 213% leap from the $1.18 trillion of average daily turnover in April 2016. Most of those trades took place in the City of London.

- The United States: $2.35 trillion per day, or 32% of the global turnover, up 9.8% from $1.24 trillion in 2016. Back in 2016, the U.S. had been for a brief moment the world’s biggest market in these instruments with a share of 41%.

- Hong Kong SAR: $436 billion per day. This was up almost four-fold from $110 billion per day in April 2016. Driven largely by increased turnover in Australian dollar-denominated contracts, this growth in trades takes Hong Kong’s share of global turnover to 6%, from 3.6% share three years ago. In mainland China, by contrast, an average of just $16 billion of interest rate derivatives were traded daily in 2019.

- The Eurozone. Turnover reported at sales desks in euro area countries remained relatively meager this year, reaching $256 billion per day, or 3.5% of the total turnover in April 2019.The largest euro area trading center, France, saw turnover fall from $141 billion per day to $120 billion per day in the last three years, taking its share of global turnover to 1.6% from 4.6% in 2016 and 8.1% in 2007.

- Other worthy mentions: Japan saw daily trading volume rise to $135 billion per day (from $56 billion), and Singapore, to $109 billion per day (from $58 billion), taking their share of the global total to 1.8% and 1.5% respectively.

The U.S. and the UK combined accounted for 82% of total turnover of interest rate derivatives in April this year, up from 79% in 2016. Even after three years of regulatory tussles with its biggest trading partner, the EU, the UK has not only maintained its grip on the vast and fast growing OTC derivatives markets, it’s strengthened it, pulling away from New York and leaving Paris in the dust.

“London is the capital of capital and this report shows that despite challenging times, the fundamentals of the City remain strong,” said Catherine McGuinness, policy chair at the City of London Corporation, the municipal governing body.

The UK trading also dominates in global currency markets, albeit not quite as much. In April 2019, its FX trading desks generated a turnover of $3.58 trillion per day, up from $2.41 trillion per day in 2016, taking its share of total global FX activity from 37% to 43%. By contrast, the US share of trading declined during the same period from 20% to 17%.

In France, the UK’s biggest EU competitor, the trading volumes also fell, from $181 billion per day three years ago to $167 billion per day in April 2019, tiny compared to the $3.58 trillion per day on London’s exchanges. In Germany, the average daily FX trading volumes are even smaller, clocking in at $124 billion per day, up from $116 billion per day three years ago.

That London has also managed to increase its share of trading euro-denominated interest rate swaps, accounting for 86% of the global total, up from 75% in 2016, will be of particular concern to Brussels. For years, the French government, together with the ECB, have sought to wrest control of the trading and clearing of euro-denominated transactions from the City of London, for mainly justifiable reasons. And Brexit was supposed to provide the perfect alibi. But alas, as this BIS report emphatically shows, it hasn’t happened yet! By Nick Corbishley, for WOLF STREET.

Ginormous numbers, FX swaps and spot trades, USD, EUR, JPY, GBP, Australian & Canadian dollars… but where the heck is China’s CNY? Read… Foreign Exchange Trading Soars to $6.6 Trillion a Day, US Dollar is Total King

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Greenspan said these instruments make markets safer. You may assume that these numbers reflect more “registered” derivatives, and of the two types of derivatives, interest rate and currency, that almost no currency derivatives are registered. Those derivatives in the City of London may have a lot to do with Brexit. Additionally the cost of borrowing is at all time lows making derivatives less expensive. However it does bother you that if this market expands, these counter parties are becoming compromised. I would also say that dollar holders are nervous about their currency. I continue to see the Eurozone and their currency as a winner here. NIRP helps buttress their currency. If you consider this chart as a risk graph consider HK will probably disappear in the next decade, what does that say about the US?

Hmmm… “Eurozone and their currency as a winner”? I’d say mighty USD.

Apparently not much options other than resorting to the derivatives that sunk LTCM (once noted as experts in investing in derivatives to make above-average returns and outperform the market), Orange County CA and Bear Stearns/Lehman/AIG? Guess market is short on learning from history with the Fed bailing out everyone again except this time the global bubble is so big that it will be different this time.

The entire article screams LTCM to me.

>> Greenspan said these instruments make markets safer. <<

Well, Greenspan said a lot of stupid things, but this one may be one of more memorable…

Powell ‘we will not deploy NIRP’

I suspect that will one day be trotted out as memorable.

I don’t know the context in which Greenspan made that statement nor his whole statement.

But I agree with the gist – risk mostly dissipates in the marketplace … except there always seem to be a handful of parties who accumulate risk and end up holding the bag.

Think AIG. If they had done proper risk assessment, they wouldn’t have loaded up on the CDOs.

Same with oil price hedging.

Same with currency exchange rate hedging.

Same with interest rate hedging.

Bets in each of those categories create winners and losers everyday and that’s perfectly normal. We only hear about massive tail risk events.

Are we suggesting there shouldn’t be any derivative trading? That’s nonsense.

My reading says the notional value of the world wide derivatives market is now about $1 quadrillion.

Good article, particularly in mentioning the deregulation of derivatives thanks to the fat cheeto. Also, the real terms of these derivatives often vary. They are not disclosed, so the risks to the banks are opaque to investors and the public.

Profits are huge and tempting. Banks give discretion to their officers as to many derivatives’ terms which may later come back and bite them.

You can be sure that the banks have been betting that interest rates will not go up, because the banks are profiting so greatly from the ultra low interest rates, which they are charged to borrow from their “Federal” Reserve, while they can charge huge interest rates to the average American. They want the gravy train to continue.

Additionally, in light of the transfer of its wealth to the banksters since 2008, the US. is already in deep trouble from its over $130 trillion in liabilities (per Forbes), upcoming baby boomer quasi-retirements and would have a hard time servicing its debt and keeping up with its other budget priorities if the rates went up. However, interest rates are like forest fires.

You can control them up to a point, but at some point, the lenders will panic and they will go up. The vast wealth controlled by the parasites that have gained power over our governments will not be risked.

When the risks exceed a certain level, the normalcy bias will not be able to overcome the fear. Interest rates will surge.

NIRP in Europe certainly buttresses the currency in the short term, at the cost of institutional and societal – erosion not very smart at all (as you, of course, appreciate).

Why Brussels can’t allow the UK to escape from the Eurozone.

Others will see that all the predictions of really bad stuff happening just didn’t come true. Not even close.

“And Brexit was supposed to provide the perfect alibi. But alas, as this BIS report emphatically shows, it hasn’t happened yet! “

There is also a growing list of countries that are and have moved away from the SWIFT system and from being blackmailed with tariffs from the US. No doubt many companies will follow as well.

Seems like only yesterday that Warren Buffett was headed to prison for derivatives fraud, but then Spitzer saved the day.

“Under investigation are a number of reinsurance transactions — insurance purchased by insurance companies — that regulators contend were designed to improve AIG’s financial statements without the transfer of risk. Risk transfer is necessary for a deal to be an insurance transaction and determines how it’s carried on a company’s books.”

The world is so much better off with less regulation and fewer crooks, fewer derivatives …

(snark)

Buffett, at a Berkshire annual meeting in the early 2000s, declared derivatives were “financial weapons of mass destruction”. He spent the next several years closing down his derivatives trading desks. When the 2008 meltdown came, he was hurt but not brought to his knees. One reason the FED has been tip-toeing through the tulips with its interest rate increases and cuts is the size and fragility of the vast interest rate swap market. The fixed rate is pitted against the variable rate, and steep, quick changes in rates could lead to the blow-up of one side of that equation.

interest rate derivatives do not eliminate interest rate risk.

They just transfer it from one party to another.

Nil sum game.

Thats what insurance policy’s do.

The insurer bets that he will make a small nett vig, on the majority of deals. lots of deals, lots of money.

Long term The insurer is generally correct, unless he has very bad actuary’s working for him.

As long as he and his underwriters, have enough capital to weather any short term storm/black swan events. The insure stays around and makes good money, long term (Lloyd’s).

The issue with derivatives arise from “Naked” or “non/short underwritten” derivative writers, many of those in ccp china.

One never really knows who the ultimate counter party’s/underwriters are in so many Derivatives.

Ultimately a derivative, is an insurance policy, thought of that way, they become much easier to understand.

My understanding of which I admit could be totally incorrect is that the problem with derivatives in the sense of insurance is that the thing that is insured can be insured more than once, if not many times which is fine unless as with AIG they have to pay up.

After all, is this a possible explanation for the fact that derivatives actually dwarf in amount that which they are attached to ? So therefore is it not logical to assume that only a few misplaced stones could cause a landslide ?

Deutsche Bank – $ 47 trillion etc.

>for mainly justifiable reasons

Not sure I agree there.

People can trade euro-denominated interest rate swaps wherever they like but they choose to do so in London because of ease of doing business..

London can also trade in dollar-denominated interest rate swaps. You don’t see the US getting all uppity about it at all.

Must be doing fall yard work, so rather than taking time to study the following 2 posts, and trying to understand the relationship (if any), I will ask:

re Wolf’s number of 9/18, Foreign Exchange trading “soars” to $6.6 Trillion per day

AND,

re Nick Corbishley’s number above, 9/19, Interest Rate Derivatives trading “explodes” to $6.6 Trillion per day

is there a connection, preferably understandable, between these 2 measures of the global economy ?? or is this just a coincidence ?….(my espionage fiction reading tells us that true coincidences are rarities).

leveraging?