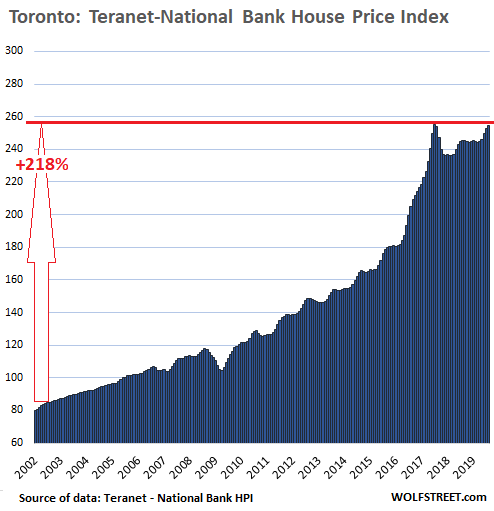

House prices in Toronto still below 2017 peak. Montreal, Ottawa hit new highs. Quebec City about flat with Jun 2013. Edmonton back to Oct 2007. Calgary rises to March 2014 level.

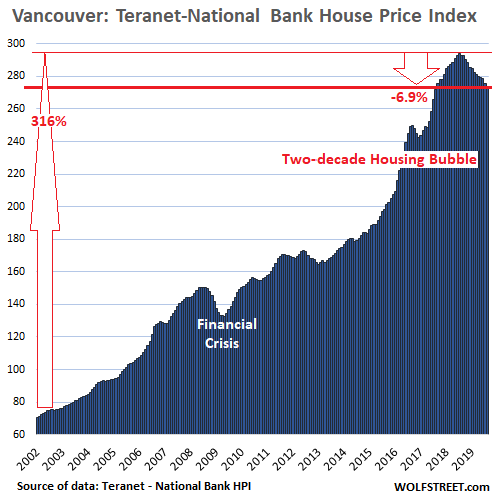

House prices in Canada, as tracked by the Teranet-National Bank National House Price Index, have more than tripled (+204%) since January 2002. But in August, they ticked up only 0.6% from August last year, the weakest year-over-year increase since October 2009. The biggest drag was the market in Vancouver, which is relentlessly spiraling down.

Vancouver:

House prices in Greater Vancouver, once one of the world’s hottest housing markets, fell 0.8% in August compared to July, the 13th month-to-month decline in a row, and were down 6.9% from the peak last July. This comes after the house price index had more than quadrupled over the 16-year period from January 2002 through July 2018. The index is now back where it had first been in September 2017:

The Teranet-National Bank House Price Index tracks prices of single-family houses though “sales pairs,” comparing the price of a house that sold in the current month to the price of the same house when it sold previously, often years earlier. This eliminates the issues of “mix” that median-price indices encounter and the issues of “big outliers” that average-price indices encounter.

A measure of house price inflation

The index tracks how many more Canadian dollars it takes to buy the same house over time. A price increase of the same house is a measure of how much purchasing power the Canadian dollar has lost with regards to houses. If the price of a house doubles over a number of years, it means the Canadian dollar has lost half its purchasing power with regards to houses. This makes this index (and similar indices, such as CoreLogic Case-Shiller Home Price Index for US housing markets) a measure of house price inflation.

But the index generates a softer and lagging image of the market compared to the official MLS House Price Index for Vancouver, which is based on a “typical” house with a “benchmark” price. The MLS HPI benchmark price for Greater Vancouver fell 10% in August from a year earlier and 13% from two years earlier.

Toronto:

In the Greater Toronto Area (GTA), house prices rose 0.8% in August from July and were up 3.8% from August last year, but remain a tad below the peak in July 2017, according to the Teranet-National Bank House Price Index.

The Toronto index has more than tripled (+218%) since 2002, a huge increase in 17 years, but it pales against Vancouver’s 316% increase from 2002 through its peak in 2018. I put the charts here on the same scale as Vancouver’s chart to show how large the house price increases were in each metro compared to the other metros, and particularly compared to Vancouver. As we go down the list, the white space gets larger and larger:

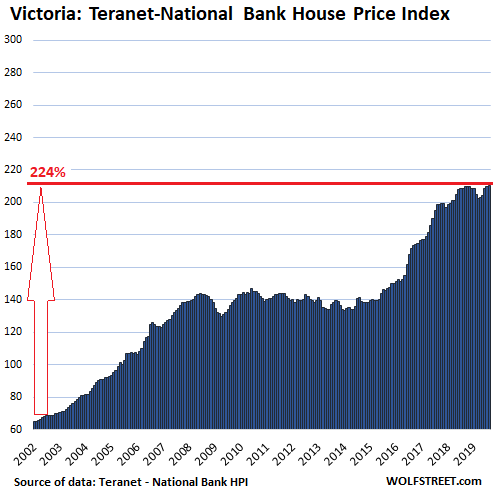

Victoria:

House prices in Victoria, which more than tripled since January 2002 (+224%), inched up 0.2% in August from July, and were up 0.7% year-over-year. The index eked out a new record, squeaking past the old peak set in September 2018 (chart is on the same scale as Vancouver’s):

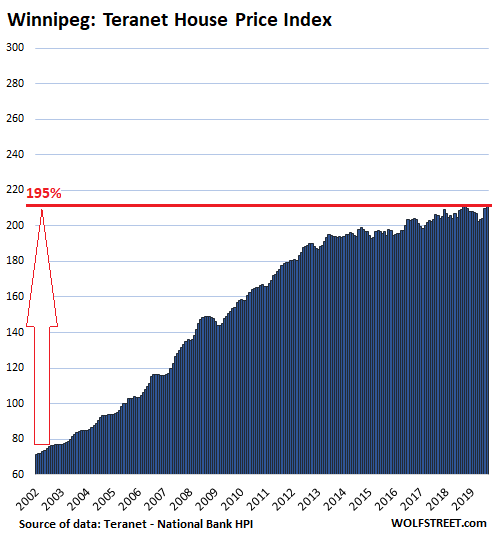

Winnipeg:

House prices in the Winnipeg metro rose 0.7% in August from July and 1.1% from August last year, but remained a smidgen below the peak in September 2018. The index had nearly tripled between 2002 and September 2014, and then stalled. The index is now 6.3% higher than it had been in September 2014:

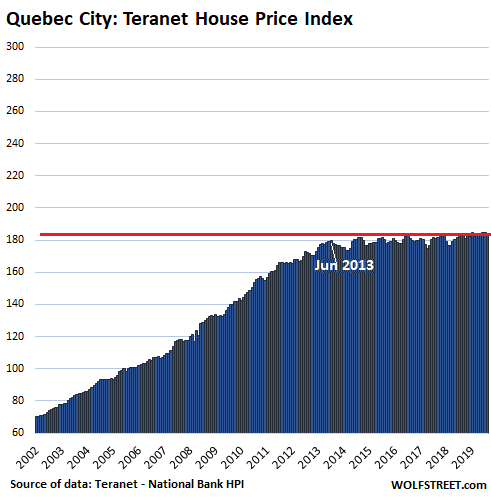

Quebec City:

The House Price Index for the Quebec City metro declined 0.4% in August from July and was flat compared to August last year, having been essentially flat since June 2013, a hangover from a 160% gain in the prior 12 years:

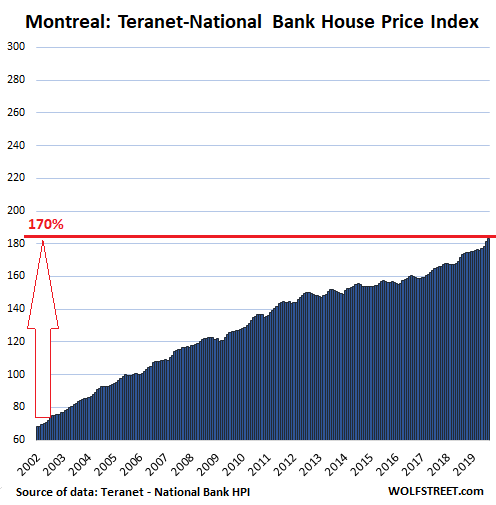

Montreal:

House prices in Montreal jumped 1.1% in August from July to a new record and were up 5.8% from August last year. The index has risen 170% since 2002 without even hesitating during the Financial Crisis:

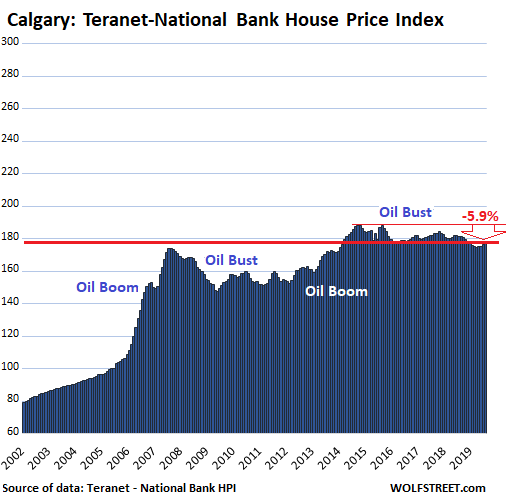

Oil Boom-and-Bust:

The housing markets in Calgary and Edmonton are dominated by oil booms and busts. In the two-year period during the oil boom before the Financial Crisis, house prices in Calgary soared by 78% and in Edmonton by 87%. But then came the oil bust, and these house price bubbles deflated – over the long term!

In Calgary, house prices rose 0.6% in August from July to their March 2014 level, but remain down 2.3% from a year ago, and 5.9% from the peak in October 2014:

In Edmonton, house prices inched down a smidgen in August from July and were down 3.1% from August last year and down 5.9% from the peak in October 2007:

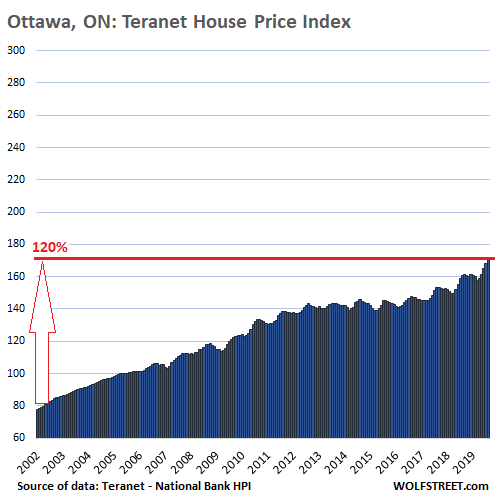

Ottawa:

House prices in Ottawa rose 1.7% in August from July to a new record, and are up 6.4% from August 2018. Since January 2002, the House Price Index has risen 120%, which is a big increase by any measure, but given the splendidness of the other housing bubbles in Canada, Ottawa ranks in last place on this list in terms of price gains:

“Wiring money overseas is not allowed for the purposes of purchasing real estate or insurance products,” explains a banker in China. Read… China Imposes New Capital Controls, Targets Foreign Real Estate Purchases, as Yuan Falls to 11-Year Low

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Buy now folks, it’s only up to the moon from here! Don’t be priced out.

I hate to admit it but I think you’re right. I can’t believe I’m saying this but it really is different this time.

How bad will Canadian banks implode when the Canadian housing market implodes?

And, FYI, Canadian banks already have a built-in TARPish bail-in scheme.

“Beginning in 2018, all unsecured long-term senior debt issued by Canada’s largest banks — those that are deemed systemically important domestically — will be convertible into equity should a bank need to be “resolved” or unwound, according to David Beattie, a senior vice-president in the financial institutions group at Moody’s Investors Service.”

https://business.financialpost.com/news/fp-street/new-bail-in-regime-for-canadian-banks-will-ease-burden-on-taxpayer-in-case-of-crisis

What is unsecured long term debt, are customer deposits exempt?

Shorting Canadian banks because of the real estate price decline is a terrible idea. Don’t do it.

They hold very little mortgage securities. Almost all Canadian mortgages are insured by Canadian Government CHMC, so the risk to the banks is nil. The government will simply print the money to bail out CHMC , just like the Fed did here during the recession with Fanny and Mae.

A better bet would be the CAD , but it’s hard to predict how it will move if such crisis happens.

Even back in the late Eighties, I had a mortgage officer tell me that if a homeowner made two payments, he was happy. After that, the mortgage was sold and they didn’t have to worry any more. It was wrapped into some kind of investment vehicle and off their books.

Go LONG banks. Just wait until the 50 year mortgage, real estate will take off like a rocket ship, and this, the banks.

Thanks for all your input Wolf.

My on-the-ground view as someone looking for a single family home in Toronto–

Prices in our preferred neighbourhoods are testing record highs (the Annex, Seaton Village, Danforth Greektown).

It is really depressing to be a renter having amassed a sizable downpayment, with a value-minded orientation, to be watching these year-after-year price increases. Already in our early 40s, we don’t want a 1M+ mortgage hanging over our head for a small house in one of these neighbourhoods. Many of the houses priced just under 1M don’t have parking, and require substantial renovation. And participating in this system requires sizable payment to morally questionable dealers and go-betweens in the RE industry. Salt in the wounds.

Much of the rental stock is owned by individual investors, some of whom are are not professional. Landlords are evicting tenants for personal occupancy, requiring 12 months, before they can re-rent at much higher rates. Very destabilizing for people with young kids. Few new purpose built rentals in decades, although some is being built now.

Torontonian’s fetishize homeownership like no where else! It isn’t clear where all the money is coming, because even with low interest rates, most of the population can’t afford these prices. Politicians don’t want to allow price discovery to occur, and would rather loan first time homebuyers 15% for an equity stake. Political calculation, but there is a lot of pain and suffering along the way for everyday Torontonians seeking a better housing situation.

The past 10 years have been a bad time to be a saver or value investor. Will this tide ever turn? I can’t change my money orientation and throw out my upbringing about money.

One correction: Chart for Ottawa is mislabeled as Quebec city.

The politicians profit from the rising prices because they bring a higher tax basis. No offense, but you would be crazy to invest in the current market. One average correction and your deposit will disappear. I already hear stories of people that don’t qualify to refinance their own homes, that’s crazy. Hold on to your money and/or move. Your down payment may buy you a home outright in another city.

The tide will turn when the central banks desperate policies aimed at keeping asset prices inflated push on a string, or cause the kettle to explode.

When that happens the tide will turn into the mother of all tsunamis.

In the meantime, one can look to the people of Hong Kong for inspiration. They are protesting about the insane cost of housing as much as the CCP.

When will more people stand up and say ‘Enough’

yeah!!!!

Well these are the numbers but there is no hard evidence as to what is actually happening in the Toronto market. It would be interesting if it hit 280 or closes in on 300 by next year. There is a lot of anecdotal evidence I’ve been reading for years, but that is useless when you talk about a housing market as large as MTA. The people talk about immigration, but with no hard numbers. I can speculate that the world is going to pot and all the rich from all over the world are landing in Toronto where they invest in housing. But then, I don’t have any hard number either.

Living the dream in Toronto, harsh never ending winters, traffic jams everywhere and one million dollars for a piece of garbage.

The world is big, take your money and move , you won’t regret it.

Yeah, it seems like there is a willful effort to obfuscate what is going on by either not measuring important information about the market, or not promoting transparancy in what is available. Shouldn’t governing bodies want to make market information abundant and clear to all market participants?

Brett,

Thanks for the correction. No, that chart was not “mislabeled.” It was labeled correctly “Quebec City,” but I’d stupidly stuck it into the paragraph about Ottawa. Now the Ottawa chart is in that slot, correctly, and it looks very different than Quebec City.

@Brett: Take your down payment cash and buy a little 2,000 sq ft 3/2/2 on the Florida Gulf coast like so many of your compatriots. You’ll be there in 15 years or so anyway.

I’m not a realtor (happy to say), but I see this a lot.

Good idea — I like the space coast. I’ve been wanting to do just that (as a dual U.S./Can citizen), but my wife is resistant to buying real estate elsewhere until we own a home in Toronto, so it will require some more persuading.

Show her what a $1M will buy in Toronto and what $1M will buy in Florida.

P.S. There is a lot of money laundering in Canadian cities, do you really think all those empty crap shacks are good investments? Consider they are really vehicles for moving money around until they get to a bag holder, potentially you.

Buy in Toronto and a vacation home, yet scared to buy at the peak prices. Which is it? Either you are frugal and buy in an appropriate market or you go all in. Being in Toronto will most likely leave you “house poor”, if not you can afford both and don’t have to worry about depreciation over the next 5- 10 years

As interest rates go lower, people looked for more property to buy. A house is the highest value asset many families will own.

Wealthy Hong Kong residents established dual citizenship by investing in Vancouver and Toronto. Asians are the largest Toronto minority. Toronto is nearly half minority. Population growth demands housing.

Canadian real estate prices in Vancouver and Toronto are inversely proportional to the number of U.S. and Canadian factories.

As the China Dictatorship got into bed with the hot Global Money crowd, foreign, heavily Chinese, hot money looked to invest in their personal Plan B.

I suggest you lower your expectations, by a lot. I grew up in a Toronto row house in what is now called the Lower Annex, which for many years, provided inexpensive houses for recent immigrants. In 1929, my father bought the house for about $1,250. Web site Listing.ca currently values the house at $1.4 million, although it appears to have undergone significant upgrading in the 40 years after we sold it. In the late 1950’s and 1960’s, there was a steady exodus of families from the neighborhood to the suburbs, as people’s economic situation improved. The late Jane Jacobs’ home at 69 Albany Avenue in the Annex is currently valued by the web site at over $2.1 million. Sorry to burst your balloon.

Ok, a few points about the Teranet-National Bank National House Price Index from their website:

1) The measurements are based on the property records of public land registries, where sale price is available.

2) Is estimated by tracking the observed or registered home prices over time. Properties with at least two sales are required in the calculations. Such a “sales pair” measures the increase or decrease of the property value in the period between the sales in a linear fashion.

[Wolf here: I deleted the remaining three points because they were promo material from their website]

Shawn,

I’m not sure why you posted this here. The first two points were OK, though I said most of it in the article.

The remaining three points I deleted because they were copy-and-paste promo materials from their website. I don’t allow promos here.

Resale apartments and resale townhouses are rising in price in Edmonton. They’re still down about fifty percent from their October 2007 peak. Rent is about triple what it costs to own and as interest rates fall it will cost about 4 times more to rent than to own a resale apartment or a resale townhouse in Edmonton, Alberta.

I just raised my tennants’ rent by 70% this year. Told them if they don’t like it, I had 56 unsolicited offers to buy the place cash at 120% market value.

You mean your mom raised your rent by 70% for you to remain in her basement, because you keep exceeding her bandwidth cap. Sorry Jim, but actual wealthy property investors have neither the time nor the inclination to troll bearish sites and trade opinions with us plebes. Real landlords are also loathe to brag online about how much they raised someone’s rent. It makes them look bad, and incites the ire of municipal politicians and local activists, Wuxi can ultimately bring more regulation and rent control down on their heads. You jumped the shark with that post and exposed yourself as a fraud.

One can always tell the difference between the real landlords and the wantrepreneurs with way too much time on their hands. The real landlords, if they show up at all, which is rare, will gripe about tenants or some onerous regulation that makes it impossible to evict a bad tenants. The pretendlords tell us how awesome it is to buy properties and “watch the money role in.” Anyone who’s ever owned a rental will tell you that’s NOT how it works.

Oh, and Tony, rents are not triple the cost of ownership, not even in Edmonton. Such and imbalance cannot exist. If that were the case, the return on a rental property in Edmonton would be so enormous that people from all over the world would be snapping them up. A return 4x the cost of ownership????? Socaljim would buy the entire city! In both Calgary and Edmonton, prices have fallen, but rents have fallen faster. I know people in Calgary who bought investment properties because they thought the price-rent metric had improved. Well guess what- as soon as the existing leases expired, they either offered the tenant a huge discount, or the tenant moved. The adjustment to rental rates is lagged and non-linear, because it happens as leases expire. Since most leases are one year, any imbalance between price and rent evaporates quickly. It never lasts long enough for rent to become an absurd quadruple the cost of carrying the home. Not unless prices plunge 80% in less than a year.

I have no idea what, or who, ‘Wuxi’ is. That should have been ‘which’.

@Alistair: socaljym is a parody account of socaljim the shill … he got me the first time too. Otherwise your points are well spoken.

enjoyed this!

Damn, I should have known better. I only noticed the ‘y’ instead of an ‘i’ in his screen name after I hit reply. He was decent enough to signal that he was a parody, and I fell for it anyway. Well played Jym. My apologies to the real socaljim.

They are in the case of resale apartments and resale townhouses in Edmonton today. Like I stated mortgage rates are falling so in the near future it will cost 3 times more to rent than own. The list prices on mls mean nothing its what they sell for. Many apartments sell for the same price as a new car or new SUV.

Spot on.

Alistair, FWIW, one of my sisters just sold her place in GP to move back to Calgary, to their long time hobby farm/home. The GP house sold for C$460,000 and sold within 2 weeks of listing.

On the other hand her daughter, going through a nasty divorce, has 2 houses in GP, that once were valued at over C$1.5 million each, that are now on the market at less than C$800,000 and they aren’t even getting looky-loo’s.

All secondary businesses that live(d) from the excess dollars from the oil and gas business in Alberta, including tourism in B.C. are the walking dead.

Dear parody accounts … it’s time to end the parody. This is getting confusing for readers who are not familiar with the story. Thank you!

I think I’ve gotten my laughs out of everyone. SocalJYM, signing off!

Thank you!

about time, the dead horse was starting to smell.

Last time I raised my tenants rent they moved out after 5 and 1/2 years of renting my home. It took me 4 months to get it rented even with a 10% reduction on what the previous tenant was paying. In the 5 years of this tenants rental, int total we Had a 5% increase on the rent which was below inflation and the rent control percentage of 2.5% per year in my CA area. Moral of this story is if you have a good tenant keep your them happy and make sure to be upfront about any increases. As great and profitable as Jim makes being a landlord sound, he is very wrong and undoubtedly has a high tenant turn over. Good luck with your investments and long term ROI with your strategy Jim.

your tenet should take you to landlord and tenants board for this ill-legale raise

Kurt,

Please note that socaljym is a parody account that has now officially signed off as you can see from his comment a little further up because it’s getting too confusing.

Wolf – the last chart you have is Quebec City (again), you’re missing Ottowa.

My daughter lives just north of Toronto. A few years ago she bought a home in a middle class community. Within a few years, the neighbourhood was transformed from homeowners to renters. The Trudeau govt. allowed in a mass of immigrants who needed housing and the corporates have been more than happy to buy up houses to service the demand. My daughter has just sold out to one of those landlords and moving on.

Canada is an immigrant nation, our rate of immigration is three times greater than the USA. No matter which party wins the election, neither will alter the status quo. It is our country’s greatest strength.

Canada is a nation with a population of 37 million (last census), slightly smaller than the population of California (39 million plus). Canada has even stricter immigration rules (which are also enforced much more strictly than those in the USA), and has struggled to meet the immigrant goals set by the current gov’t.

The USA has (at best, last count) 47 million immigrants, or 19% of the entire worlds total. The US receives an average of 500,000 ILLEGAL immigrants yearly. (Note that just the idea of accurately counting all of these law breaking individuals causes political chaos throughout the North American hemisphere.)

If America enforced it’s immigration laws the way Canada does it would cause such outrage that the entire world would be printing horror stories on the front page.

Third world immigrants drain all our social systems dry. All the rich Chinese have already emigrated to Canada. Virtually every immigrant coming to Canada nowadays is of the third world. Now you know why income taxes keep on rising.

Canada’s peak immigration year was actually in 1913. Two of those immigrants that year were my older relatives, one on each side of the family. In the past four decades, Toronto has been the destination of many thousands of former Montreal area residents, because of Quebec’s draconian language laws. Immigrants whose first language is not French prefer to move to Toronto vs. Montreal. Toronto has in many respects become a victim of its own success, although it continues to rank very high in livability surveys of major cities around the world.

Interesting article, stats, and comments. For those talking about shorting cdn banks, I sure wouldn’t do it. Mortgages are insured for those with lower down payments, and cdn banks are notoriously conservative and well protected by regulation and govt influence. (I deal at a Credit Union, that is doing just fine, by the way).

Anecdotal comment from Vancouver Island:

Victoria is on a plateau, but other places on the Island are not as they have taken over the destination(s) for cdn retirees that Victoria once held. Vic has now priced and grid-locked itself out of that equation. Campbell River, with its views of the ocean and new homes priced at 40%? of Victoria is booming. There is a very high growth rate with new sub divisions and local shopping areas under construction. Places are often sold before completion.

I live a 45-50 minute drive west of CR and my opinion/observation is that prices have plateaued. Many many older crappier built homes are sitting with signs, and blingier homes will just not sell. My friend, down the street from me, has what we call a ‘Surrey House’, too big…dormers…well appointed, big garage, landscaped, etc and he has tried to sell it numerous times, always pricing at the high end because that is what he thinks it is worth, “Look what this would sell for down Island”. Just like a shack doesn’t fit with a sub-division, a mansion doesn’t fit with rural, and has to be priced accordingly. Those with big bucks can buy a fancy house anywhere, and certainly places where there are more amenities. People buy here because the costs are lower. If they don’t fit in, they usually leave within 2 years. It is almost predictable.

There are absoutely no rentals available. God help someone who is forced to move. There are waiting lists. One fellow I know had many many folks looking for him and it still took 6 months to find a place he could move to. An outsider will have little hope and will certainly be well screened.

Your friends story sounds familiar, I hear similar justification from sellers out my direction. When they can’t afford the monthly bills the banks will take these houses, the greater fools have been found already. They all bought in up until late 2018, now the buyers all know they have the power with rents being fairly affordable as they hold out.

The second of the only 2 local mansions is for sale for $2.5 million down from last years price of 3.2M. The owner’s issue is only 5 or 6 locals have the funds, but they all have homes and are feeling content. His house stands out on the market since there are 20 other listings all under 500k.

Mortgage fraud is rampant in Canada, and the biggest banks are exposed. Anyone with more than a 20% down payment doesn’t need CMHC, and there are billions in mortgages that are not insured. And many of those 20% down payments were borrowed from alt lenders who don’t report to credit agencies, so the bank has no way of knowing the money was borrowed. Uninsured portfolios at the big Canadian banks are as large as or larger than the insured portfolios.

Brampton, Mississauga and Milliken Mills are 1, 2 and 3 in Canada in that regards.

Just like everything you buy in life…wait for it to go on sale…*cough, cough* recession* cough* cough* “Be greedy when people are fearful and fearful when people are greedy”

A few years ago there was a very apt Internet meme: a human skeleton covered in cobwebs sitting on a park bench accompanied by the caption “Waiting for my date to arrive”. It was quickly adapted to other purposes such as “Waiting for the Indians to win the World League”, “Waiting for a good Ben Affleck flick” and so on.

We won’t be seeing another recession in our lifetimes, albeit how this will come about is open to interpretation: India announced a package of extraordinary monetary and financial measures after estimating their GDP would grow between 5 and 6% in 2019. The Reserve Bank of Australia panicked after the government in Canberra predicted 3.5% growth in 2019. China being China they have been firing round of financial and fiscal stimulus after round of financial and fiscal stimulus after announcing the usual GDP growth in the 6-7% range. And the less I say about the pathetic farce of the German “technical recession”, the better.

Of course one may say that GDP data are embellished at best and completely fanciful at worst, and failing everything else population growth and inflation will save the day (Australia I am looking your way), but I have been hearing people sounding the recession alarm for so long to get freebys I have become very cynical on the matter.