Here’s why — and how that’s impacting truck makers.

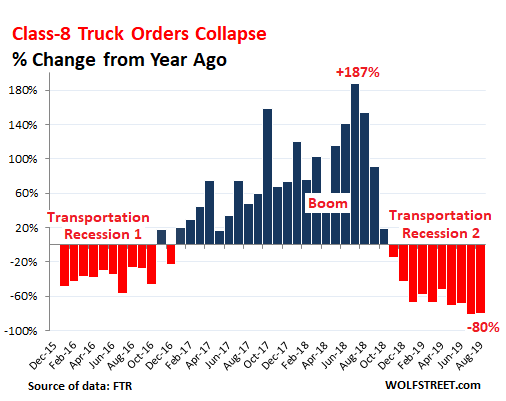

Orders for heavy trucks that haul part of the economy’s goods across the US plunged by 80.1% in August 2019 compared to August last year, to about 10,400 orders, according to preliminary estimates by FTR Transportation Intelligence. It was the 10th month in a row of year-over-year declines, and the second month in a row of 80%-plus declines, with orders in July having plunged 81.2% to about 9,800, not seen since 2010. So far this year, these year-over-year plunges ranged from -52% to -81% off the historic boom months in 2018:

“The Class 8 market is at a turning point,” Don Ake, FTR VP of commercial vehicles, said in an emailed statement. “The huge orders in 2018 supported the robust production last year and through much of 2019. Now the economy has slowed and there are enough trucks to handle the available freight growth. OEMs are cutting production rates, eventually down to near replacement demand levels.”

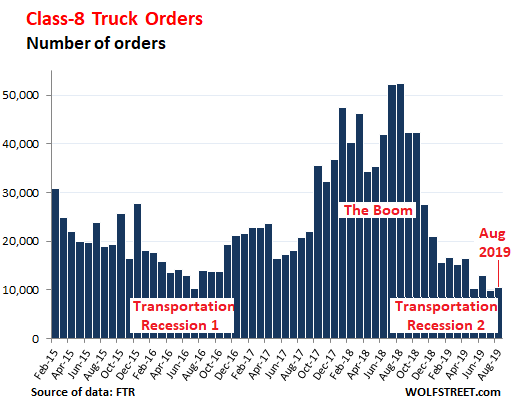

During the ordering boom for Class 8 trucks in 2018, orders had peaked at over 52,000 a month in July and August, powered by fears among trucking companies that they would not have enough equipment to move all the freight resulting from the boom that turned out to be short-lived, caused in part because companies had tried to front-run the expected and announced tariffs by loading up on goods and piling up inventories.

The order volume was mind-boggling in 2018, and as companies backed off loading up on inventories and freight shipments began to decline at the end of 2018, the hangover turned out to be equally mind-boggling.

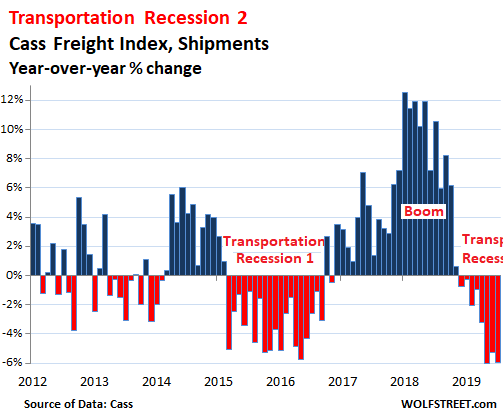

Freight shipment volume within the US by all modes of transportation – truck, rail, air, and barge – fell 5.9% in July from July last year, the eighth month in a row of year-over-year declines, after having already dropped 6.0% in May, according to the Cass Freight Index for Shipments, which tracks shipments of consumer and industrial goods but not of bulk commodities such as grains. Those two declines were the steepest year-over-year declines since the Financial Crisis:

And truckers have been responding to this new reality. FTR’s Don Ake in the statement:

“There is a tremendous amount of uncertainty in the economy right now due to tariffs and the trade war with China. Businesses are holding back on capital investment and our industry is no exception. Fleets are going to be cautious about buying new equipment in the short term. We do expect orders to increase in October. However, if freight growth is still muted and manufacturing sluggish, the big fleets may just place orders for Q1 and take a wait and see approach.”

The chart shows the sharp drop-off in orders for class 8 trucks from the phenomenal boom in 2018, down to historically very low levels where they appear to have gotten stuck for now:

But the manufacturers of Class-8 trucks have been reporting big revenue increases. For example, truck and engine maker Navistar International [NAV] just reported that revenues in its third fiscal quarter, ended July 31, had surged by 17% from a year ago, to $3.0 billion, “primarily due to a 28 percent increase in volumes in the company’s Core market (Class 6-8 trucks and buses),” as it said.

But, but, but… two weeks ago, Navistar had announced the first set of production cuts of medium-duty Class 6-7 trucks at its Springfield, OH, assembly plant. The company blamed “the cyclical nature of the business.”

Big increases in revenues but production cuts? Yes, eating through the backlog.

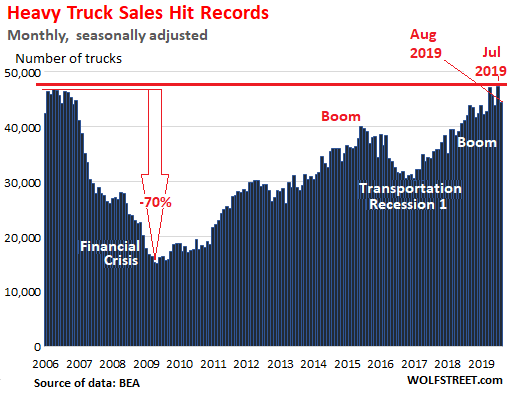

It takes a long time for manufacturers to build out their historically large backlog. In terms of Class-8 trucks, 2018 generated a record backlog that truck makers are now building and delivering. And for the industry overall, truck sales surged during much of 2018 and into 2019, past the record levels set just before the Financial Crisis to over 47,000 units (seasonally adjusted) in April and July 2019.

But in August, according to the Commerce Department today, sales of heavy trucks fell from July’s record levels, to 44,500 units (seasonally adjusted). These are still all sales of 2019-model-year trucks, for which orders closed some time ago (larger chart):

Truck manufacturers don’t disclose their order backlogs. But they have been shrinking at a rapid rate as truck makers pushed production and sales of those orders in their backlogs even as new orders have been plunging.

Sales follow orders with a long lag. And unless a miracle happens and orders begin to re-soar soon, truck makers – Peterbilt and Kenworth, divisions of Paccar [PCAR]; Navistar International; Freightliner and Western Star, divisions of Daimler; and Mack Trucks and Volvo Trucks, divisions of Volvo Group – will eventually cut production, as Navistar is already doing with medium-duty trucks, which leads to declining sales; the legendary boom-and-bust cycles of the industry.

For Trucking and Railroads, it’s Hangover Time. Read… Freight Shipments Suffer Steepest Drops since Financial Crisis, Overcapacity Balloons

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Fed far too tight. Strangling

Fed far too loose, having caused overproduction and overcapacity.

Well yeah but two wrongs….

on average, it’s right on mark?

I totally agree with Wolf. The Fed and the low rates have continued to erode price discovery. The free money has allowed companies with flawed business models to access billions of capital. Anyone can sell a dollar for 50 cents.

Lowering interest rates going into a recession results in over leveraging resulting in credit problems and bankruptcies when the slowdown takes effect. Lowering rates for the purpose of improving business lending (while Powell said interest rates were not an issue – so why did he lower rates?) is and was a classic interest rate policy mistake at this point in the business cycle, prior to a recession.

Let me offer a different perspective: the California CARB rules were being enforced in 2018 by local municipalities, which led to perfectly functional trucks being sold to other states in the aftermarket. NOW there will be much less demand for new trucks because of the replacement cycle AND the used truck market getting supply replenishment. Not to mention, as Wolf stated on Kaiser’s show, the Fed is done with rate dropping cycle. Profit margins will plummet in truck manufacturing, just like with CAT. The law of diminishing returns will ensure equity valuation destruction–higher rates and less demand due to regulatory required capital spend.

Yeah, and Japan worked out so well

Heavy Truck sales hit record highs in the third graph down… Where is this 80% drop??

How come NONE of economic data is showing any slowing in Consumer Spending or Business capital investment???

First chart shows the 80% drop in orders.

Concerning your second question: Services are hot, and 70% of what consumers spend is for services. Retail is strong too powered by soaring online sales. This is an inventory issue and an industrial issue, not a consumer issue. Consumers are doing fine.

Online sales make up around 11% of total retail sales. Whether they’re “soaring” or not matters little. Online retailers employ very few people relative to bricks and mortar and therefore do not add much to the economy.

Easy to show a “Soaring” increase on a small relative percentage. Let me know when online hits 30% of total retail, then it might matter a bit if sales are soaring.

Ken Wu,

About half of retail is sales at gas stations, auto dealers, and grocery and beverage stores. Those have largely been resistant to online sales for more or less obvious reason. Ecommerce is already over 22% of the other half.

The retailers I call the “mall retailers” — department stores, clothing stores, and the like — are getting crushed.

Total ecommerce retail sales will reach $600 billion this year. A 14% increase in 2020 would mean an increase of $84 billion — and this is big enough to move the needle. Check this out to get a feel for how powerful a driver ecommerce is:

https://wolfstreet.com/2019/08/19/how-the-ecommerce-boom-plows-down-mall-retailers-one-by-one/

For example, department store sales peaked 19 years ago and have been declining ever since, as department store chains are getting wiped out:

Online retailers do, however, employ a lot of trucks!

P.S. Online retailers free up people from low-wage sales-clerk jobs so they can do something more productive. They also free up consumers from having to waste time slogging through stores to not-find what they need, enabling them to spend money and/or be productive in other ways. There’s much wrong with them, but that’s how they add to the economy.

As a trucking company I can say we feel the slowdown, freight rates are way down, keeping everyone rolling is a daily challenge. I see owner operators and small freight hauling fleets really struggling right now and think there will be some consolidation among brokers who rely on owner operators and small fleets.

Thankfully my fleet is paid for and I really do not haul basic freight so I will ride this out like I have many times in the past.

RW, can you provide insight as to what types of freight customers are providing you with less revenue and which are holding steady. Trying to understand if there are specific segments of the industrial economy slowing faster. TY

There is a another reason for the drop in truck orders. Due to the wet, cooler summer the Agricultural reports coming out of Canada and the Northern U.S. is a much lower yields on wheat, soy, corn and other farm crops. Examine as well the canning factories that are closing across the U.S and Canada. If there is no product to transport, the trucks are not needed. See the Ice Age Farmer, Adapt 2030, https://www.zerohedge.com/news/2019-05-27/crop-tastrophe-midwest-latest-usda-crop-progress-report-signals-nightmare-scenario and this https://electroverse.net/official-canadian-crop-estimates-wheat-soybean-and-corn-in-sharp-decline-due-to-adverse-seasonal-conditions.

Its a much larger encompassing issue than just over supply of trucks there are other factors at work in this.

Txhumingbird,

As shown in the second chart, shipments of freight by all modes of transportation are down about 6% year-over-year, the largest decline since the Financial Crisis.

There are two parts to this equation: decline in demand from shippers (industrial companies, etc.) and soaring capacity of trucks.

Last I heard the order backlog was about 10 months, and I doubt that truckers are going to place orders farther out in such a cyclical industry. There are a lot of economic alarm bells and fat ladies singing, but not here. Thought I was reading ZH for a minute.

Did you read any of the data in the article, or was this some preconceived notion that you were going to post anyway? If you did actually read it please rebut the data and let us all in on your insight.

“ACT analyst Kenny Vieth said the backlog is the biggest since May 2006”

New orders have collapsed largely because of the backlog. No one disputes this. I’m not contradicting the article data, just adding to it.

You are quoting a WSJ article from 5/13/18. Actually making my point that it is different a year later. Please try harder next time.

Portland has both Daimler’s Western Star Factory and North American Headquarters for All of Daimler Trucks. In transportation recession 1 they didn’t miss a beat because Western Star was busy building shale oil trucks and the R&D cash burn were propped up by Daimler’s then robust car and Sprinter Divisions. Things are very different now and I expect we will soon get a big announcement of layoffs in the W.S. factory and the headquarters (engineering). I predict this to be the kickoff for the oncoming recession here in the Portland Area.

This is TERRIFIC news for Socal and Boston real estate!

LOL.

Just so that everyone knows, this is a spoof of the real “SocalJim,” our RE enthusiast.

:) :) :) :) :) x 10000000000000000000000000

Neighbor had a bidding war and sold over the asking price?

Was worried there for a minute after having earlier read that “SocalJim” had left the building…. Lol

What am I missing here? Why everyone is ganging up on SocalJim?

She/He has been on the ground reporter of RE matters in few cities. I doubt his observations have been proven wrong any more than other’s here. Why make her/him a punching bag?

It’s similar treatment to what Paulo receives, the 2 informative folk both have great insight to their world. But their world compared to everyone else’s world are not all the same. So when a report says one area of the economy is hurting, their comments of how well they are doing just comes off as grandiose.

A simplistic analogy would be – “The sun was out all day today, why are you complaining about that tornado in your backyard?”

What does this mean for the Tesla Class 8? I suspect that it will never be made. There’s not much market for a vehicle that cant be refueled on all major routes; that loses carrying capacity due to the weight of its “fuel tank (battery)”; and that has no service organization in place. Promoters like Musk drive their share price through grandiose “announcements.” That is what the Tesla Class 8 should be called: The “Announcement.”

In the 1990s that sort of thing was called “vaporware”. Microsoft could destroy legions of competitors simply by announcing that they were working on something. Even if they weren’t.

Ahh, the good old days!

Another Musk doubter. He’s revealing more details of the truck this month!

Nikola Motor Co. is still trucking along just fine with 14,000 orders for its hydrogen fuel cell trucks. The main advantage of hydrogen fuel cells are for long haul truck routes – the hydrogen refueling can be accomplished at the same speed as current diesel refueling, and the system is much lighter than the large batteries needed for all electric truck.

https://www.forbes.com/sites/alanohnsman/2019/09/04/nikola-ceo-trevor-milton-is-now-a-billionaire-thanks-to-hydrogen-truck-startups-fundraising-drive/#5ffbe2855b0f

They have the orders I have yet to see one, our company spend a lot of money on research and development ,so where are they

Union Pacific reported railcar loadings down 7% in Q3 as of 9/1/19 compared to Q3 2018.

Not a good time to waste money.

How will this affect American auto stocks, esp. those companies that depend on their truck market?

Wolf,

Many thanks for continuing to keep score with Class-8 trucks.

At this pace, when does the real pain start to throb with the truck manufacturers? Somewhere between Dec ’19 and Mar ’20?

Rail grain shipments way down for the class 1’s. Watching the secondary rail freight market, UP is -500/car under tariff, BN around -350/car. And this looks like it will be this way through the end of the year right through fall harvest. Crazy!

For the first time being in trucking business for 12 years. I have received a blank form from DMV to turn in your tags. I guess their data showed that a lot of trucking companies will go under due to over capacity. Already 650 companies went under this year.

I’ve read that the tax reform act of 2018 offering accelerated depreciation may have pulled forward some truck purchases/demand.

It’s the same in any capital good industry worldwide: it’s now time to pay for the insane growth in order books we had in 2018 and 2017.

Whether it’s lorries, 5-axis CNC aluminum cutting machines, jetliners or even humble hardness testers, all of these are expensive capital goods designed to last for many many years while working and earning their owners a living. They are not gadgets, to be replaced when a more fashionable model appears after a couple of years.

But we deluded themselves they were, that what we saw in 2017 would go forever and ever and once order books stopped growing we threw the mother of all temper tantrums to get “moar” (thanks a lot 4chan).

Trucking is cyclical business, that’s fine, but triple digit order book growth for four months in a row in a highly mature economy like the US is the very definition of insanity. It means the otherwise very intelligent people running these companies acted like complete idiots: hopefully they will now be forced to live with the consequences (read: overcapacity) and thus learn some valuable lessons but I am not exactly holding my breath.

Exactly how much growth were these shipping companies expecting is hard to gauge, but I suspect like my colleagues in Switzerland and Germany they expected a steady yearly 8-12% increase in volumes, which is absolutely unsustainable mid-term, let alone long-term.

The companies in the manufacturing heart of Switzerland (Jura, Solothurn, Neuchâtel etc) have already started to cut shifts (usually on Monday) as their thick order books dwindle and the predicted continuous big orders from India, China, Germany or wherever fail to materialize. The blame game is on, as is the scaremongering in the press. A few are doing the right thing and looking into the mirror to find the culprit but that’s not as popular as screaming the R word and look for the most inmprobable culprits.

Next up: did the Freemasons and the Martians conspire to cause a recession?

Stay to tuned on Rock ‘n’ Roll Radio.

Just in time for the new China tariffs to take effect and consumer sentiment to take a step back. There may be some cynical impulse for the marionette of Wall St to force people to buy now ahead of the price changes. 43 told us to shop and defeat the terrorists, no idea he mean domestic, and church attendance down? Maybe Fed will lower CC interest rates in two weeks?

https://www.aar.org/data-center/rail-traffic-data/

A lot of truck traffic is dependent on rail traffic. When you compare the overall annual rail traffic for US, the peak was 2014, which wasn’t much over 2011- and overall cumulative production per Rail data isn’t too rosy since before the latest FC, “so-called……”

consumption of soft goods doesn’t leave much of anything real, even for data-mining of today’s consolidating platforms.

Hydrogen fuel cells could be a sure winner though over anything Musk comes up with. He’s just cherry picking for himself, just like his buddies.

Printing money and putting IOU’s on the Fed balance sheet. People do not want T-bills. They want to flip houses. Housing prices go up as bond yields go down. Who could remember a time when housing prices ever went down?

Sorry, the above was posted by mistake under wrong topic.

Hi Wolf.

Who are the weakest mall retailers?

Thank you.

This feels like a continuation of the transportation recession that began a couple years ago.

$FLY has been one of my favorites.

With all hype over EVs, hydrogen trucks, etc. anyone can tell to what extent the US rail network is electrified? US is a big country and it needs to carry most of freight by rail. But from what I here, this is not the case.

DV,

So why don’t you come to the US and look at US freight trains. Go ahead and look at a busy rail line and watch the trains that are over 2 miles long get pulled by several huge diesel engines. Or drive along I-80 and watch those engines haul these long trains across Donner Pass (7,050 ft or 2,151 m) in California’s Sierra Nevada. The train line goes right by the ski area and through Truckee. It’s a fascinating spectacle.

Here is some data.

In the US, trains can double-stack containers. In the EU, overhead electrification prevents double-stacking of containers.

In the US, trains carry about 40% of the total freight; trucks carry about 34% (ton-mile). In the EU, trains carry only about 17% of the freight, and trucks about 77% (tonne-km).

In the US, freight trains can be over 2 miles long (3.5 km). In the EU, freight trains are limited to about 750 meters (less than one-half mile).

In US, the weight per axle is usually 30-35 metric tons. In the EU weight per axle is limited to 20-23 metric tons.

The thing is, EU rail systems are designed for passenger transport, and passenger transport has priority. So passenger travel is slick and fast. But freight is not.

In the US, rail systems are privately owned and are designed for freight transports. Passenger transport, where it exists at all, is not a priority, except on a few dedicated lines (such as between Boston, NYC, and Washington DC. So for you to cross the US by rail will be an expensive adventure (it’s possible on a couple of lines, and it’s gorgeous, just make sure you have a lot of time). But shipping a container across the US is cheap and fast.

Accrual basis revenue will stick the revenue in an “unearned” balance sheet account until matched with production. I assume the unearned revenue accounts for these firms will dry up and leave these companies showing no revenue in a few quarters.

Truck makers recognize the revenue on the income statement when the unit is delivered. So deliveries drive the top-line revenues. Deliveries are going to slow sharply this year, once the order backlog has been built, and so will revenues.

Thanks for sharing the worthy information.