Fed Warns about “Elevated” Asset Prices and High Business Leverage.

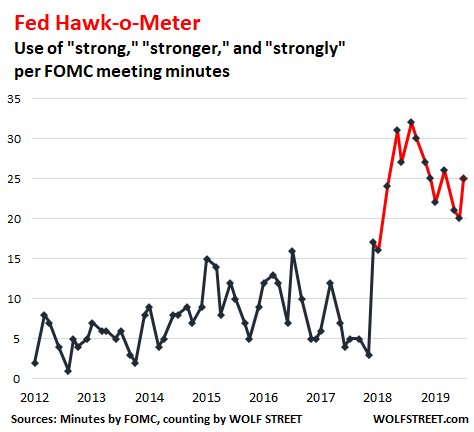

My fancy-schmancy Fed Hawk-o-Meter, which analyzes the minutes of the Fed’s meetings for tell-tale signs of how the Fed sees the economy, jumped 5 points for the meeting on July 30-31, indicating that a further rate cut – even a cut of just a quarter percentage point – was not set in stone during the meeting:

The Fed Hawk-o-Meter counts how often “strong,” “strongly,” and “stronger” appear in the minutes to describe the current economy. The meeting minutes are one of the Fed’s communication channels to the markets to avoid surprises on meeting day. The Hawk-o-Meter attempts to show in a chart what the Fed wants to communicate to the markets.

The words “strong,” “strongly,” and “stronger” appeared 28 times in the minutes of the July meeting. But three of them were “false positives” because they were used in a clearly different context, including a reference that a couple of participants “favored a stronger action.” I removed those three from the tally. Leaves 25, up from 20 at the prior meeting.

“Strong,” “strongly,” “stronger” appeared in phrases such as these:

- “The information available for the July 30–31 meeting indicated that labor market conditions remained strong”

- “Mining output rose notably, supported by a strong gain in crude oil extraction”

- “Real purchases by state and local governments rose moderately, boosted by a strong gain in spending on structures

- “Stronger-than-expected inflation data releases”

- “Gross equity issuance has been strong in recent months” [IPOs]

- “Agency and non-agency commercial MBS issuance was strong in the second quarter”

- “The projection for real GDP growth over the medium term was a little stronger”

- “Participants judged that household spending would likely continue to be supported by strong labor market conditions, rising incomes, and upbeat consumer sentiment”

- “Job gains in June were stronger than expected”

- “Reports from business contacts pointed to continued strong labor demand, with many firms reporting difficulty finding workers to meet current demand.”

Two new terms: “recalibration” and “mid-cycle adjustment.”

Fed Chair Jerome Powell had already used “mid-cycle adjustment” during the post-meeting press conference to the confusion of the markets – instead of the expected iron-clad serial rate-cut promises. This kicked off a 5.6% five-day dive in the S&P 500 from its 3,027-point perch. And the S&P 500 remains 100 points below that perch.

In the minutes, the message, “we’re not on a serial rate-cut binge,” took this form:

Most participants viewed a proposed quarter-point policy easing at this meeting as part of a recalibration of the stance of policy, or mid-cycle adjustment, in response to the evolution of the economic outlook over recent months.

A number of participants suggested that the nature of many of the risks they judged to be weighing on the economy, and the absence of clarity regarding when those risks might be resolved, highlighted the need for policymakers to remain flexible and focused on the implications of incoming data for the outlook.

And trouble in the repo market made it into the minutes.

The minutes described a presentation on money markets and the Fed’s open market operations, and the issues now bubbling up in them (underscore added):

The spreads of the effective federal funds rate (EFFR) and the median Eurodollar rate relative to the interest on excess reserves (IOER) rate had increased some and become more variable over recent months, with a notable pickup in daily changes in these spreads since late March. Moreover, the range of rates in unsecured markets each day had widened.

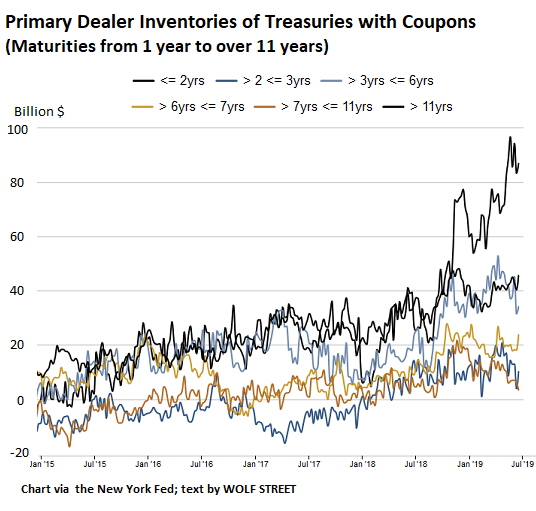

Market participants pointed to pressures in repurchase agreement (repo) markets as one factor contributing to the uptick in volatility in unsecured rates. These pressures, in turn, seemed to stem partly from elevated dealer inventories of Treasury securities and dealers’ associated financing needs.

The New York Fed tracks these inventories of Treasury securities that the Primary Dealers (list) are stuck with. These inventories of Treasuries with maturities of one year and longer have surged from $81 billion in October 2018 to $202 billion on August 7, 2019.

Dealers need to fund these inventories, which may be putting pressure on the repo market, according to the Fed’s minutes. Dealer inventories of Treasury notes with maturities between 1 and 2 years (top black line in the chart) quadrupled from $20.6 billion in October 2018 to $86.6 billion on August 7, 2019:

The Fed warns about business debts and leverage.

The Fed now rarely misses an opportunity to warn about business debt levels and particularly leveraged loans, and the “vulnerabilities” these high debt levels entail. Instead of doing anything about it, such as raising rates, it just warns about it. So here we go again:

The staff viewed the buildup in nonfinancial business-sector debt as a factor that could amplify adverse shocks to the business sector and the economy more generally. Within business debt, the staff also reported that in the leveraged loan market, the share of new loans to risky borrowers was at a record high, and credit extended by private equity firms had continued to grow.

And yup, “elevated valuations” show up again

The Fed also rarely misses an opportunity these days to warn about “elevated” asset prices and their potential impact on “financial stability” – meaning financial instability, such as a financial crisis:

Among those participants who commented on financial stability, most highlighted recent credit market developments, the elevated valuations in some asset markets, and the high level of nonfinancial corporate indebtedness.

Several participants observed that valuations in equity and corporate bond markets were near all-time highs and that CRE valuations were also elevated.

A couple of participants noted that the low level of Treasury yields—a factor seen as supporting asset prices across a range of markets—was a potential source of risk if yields moved sharply higher. However, these participants judged that in the near term, such risks were small in light of the monetary policy outlooks…

But there’s nothing to worry. Financial institutions, from bond funds to banks, are “viewed as resilient,” and leverage and funding risk were “still viewed as low despite some signs of rising leverage and continued inflows into run-prone funds.”

The last item – “rising leverage and continued inflows into run-prone funds” – is now regular feature on the Fed’s worry list. These are bond funds and leveraged-loan funds with illiquid assets that offer daily liquidity to their investors, who can buy and sell the funds on daily basis — a liquidity mismatch that makes these funds dangerous in uncertain times. And many of them experienced a run on the fund during the Financial Crisis and imploded. At least now the Fed can say afterwards, we told you so, which embarrassingly, they couldn’t say last time.

Now they’re clamoring for this NIRP absurdity in the US. How will this end? Read… How Negative Interest Rates Screw Up the Economy

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Fed needs to ignore markets and trump and allow a selloff/temper tantrum, because the Fed shouldn’t be a weaponized tool to be abused by casino con-artists. The S&P500 is up like 140% in 10 years, it can take a 20% short-term haircut, because there’s a tsunami of Baby Boomers that will buy the friggn dip …

In Search of Distress Risk in Emerging Markets (IMF, April 20, 2019)

We find that, controlling for firm-specific variables and country fixed effects, the 5-year US Treasury rate, the Fed funds rate, and the VIX are correlated with distress risk

See trend: https://fred.stlouisfed.org/graph/?g=oGbp

Some think the Fed helped torpedo George H W Bush’s reelection. Especially members of GHWB reelection team. :-)

President Clinton had many meetings with Chairman Greenspan. I think Greenspan was quite accommodating to all the Presidents he served. I’m sure Senator Dole thinks that such accommodation contributed to President Clinton’s reelection. Chairman Greenspan was knighted by the Queen of UK. The good Chairman accommodated her too. London prospered and Deutsche Bank share price grew from 40 to 55.

AG said that GHWB was the most meddlesome president he served under,

I believe “Read my lips” Bush lost because he didn’t really want a second term and got out of it by raising taxes.

According to PIMCO, 2019 represents the peak of the ratio of bond buyers to bond sellers. After this year, retirees will start taking money out of the markets faster than they put it in while working. That’s for the US, globally the peak will occur in a few years.

So negative rates may be a temporary phenomenon as the “savings glut” (which is actually a debt glut) transforms into a “savings shortage”.

Right on. It’s a DEBT glut, not a savings glut. Good debunk. We need more such debunking of the official propaganda.

Reversion to the mean expected a hair cut of at least 50-60% at the end of the coming down cycle. May be zig-zag, and then zag- zag – in 2-3 yrs? the last bear mkt lasted 18 months)

If the Fed is worried about rates inverting , why does not the Treasury start issuing only 10 year and longer bonds to fund the deficit?

Rcohn,

Re: why does not the Treasury start issuing only 10 year and longer bonds to fund the deficit?

For the same reason treasury can’t embrace ultra long 50 or 100 yr bonds, i.e., treasury has to have issuance that makes sense across the curve.

See: the financing gap faced by Treasury in coming years is likely to be too large to address with a heavy concentration of front-end issuance. Such a policy would also imply an undesirable decline in the WAM (weighted average maturity) in response to Fed run-off and higher deficits.

http://www.lexissecuritiesmosaic.com/gateway/treasury/pr/sm0070.aspx.htm

” treasury has to have issuance that makes sense across the curve.”

and more issuances in the longer end with an inverted yield curve…..”makes sense”.

The Fed also has a mandate, the 3rd unmentioned mandate….”promote moderate long rates”, and moderate means not extreme. We have 4000 year lows in the long end…and that is extreme.

The Fed could sell off some of their long maturity QE holdings…

why not? If the inverted curve is so bad, why not do something to correct it?

QUOTE: and more issuances in the longer end with an inverted yield curve…..”makes sense”.

Exactly. And long issuance would also punish the wall st speculators that are buying the long end in an attempt to front-run the FRB. So the question is, does FRB dare to punish Wall St?

By the way, implicit in what I am saying here is that the phenomenon of yield curve inversion is man-made by wall st. It is the WS bet that FRB will reduce short-term interest rates, making the long bonds more valuable, with the justification being “recession demands it” “because we say so”.

Not a bad idea really. Set the yield on 10y where it will disinvert the YC, and count on selling bonds at a premium which front loads the proceeds and defers the higher interest payments. In 08 the spread between Refi and Business loans was nearly double digits. I don’t think we want to go back there.

With lower rates, you can be certain bad, careless loans will blow up much faster than the FED assumes!

“Job gains in June were stronger than expected”

___

The “experts” have been predicting a depression since the day Trump was elected. Every month and every quarter it’s always a shock that OrangemanBad is delivering a strong economy. Unexpected!! Unpossible!!

It’s fun to watch.

Hahaha if only they knew at the time the books were cooked by 500k…

https://www.marketwatch.com/story/us-created-501000-fewer-jobs-as-of-march-2019-than-previous-reported-2019-08-21?siteid=rss

The whole Obama media never told the unemployment story though much much worse than now so why prattle on like this.

Right now, it is very very easy to get a good job. Easiest I have seen it in 20 years. Almost too good. People know this and the 501000 story is just noise.

I just don’t understand the case for a rate cut … the only negative item glaring to me is people are still not stepping up and buying homes north of the mid 2Ms … but, they want to live in them. The high end rental market in SoCal is red red hot … I see stuff for 8K a month going, and even some demand for stuff north of 10K per month … but people are refusing to buy these homes. But, the cheaper stuff is flying off the shelf … lots of buyers.

I live in small town outside of Raleigh and my looking around meter tells me the economy is hot here now which I am guessing means we are near end of cycle. Lots of house swapping and building. Jobs easy to get. Best I have seen it in a while.

Old-school – you know Boomers are retiring in huge numbers after having made lots of money on the coasts, and are looking for cute sleepy little towns w/o extreme weather to retire or semi-retire in, right?

Most trump fanatics are blind to reality and obviously you missed the revision today, or just have difficulty processing reality. I suggest you read the Labor Dept revision story at a mainstream media place, if you have time of course.

“8 hours ago – The Labor Department revised down total job gains from April 2018 to March 2019 by 501,000, the agency said Wednesday, the largest downward revision in a

Easy come, easy go. In the end Labor Dept don’t know. Watch the ship, train, and truck traffic. Burning fuel transporting stuff is real. I think some multi-nationals are hiring for political reasons or because they believe a China deal is going to happen and cause a boom. US will have a hiring frenzy if Hong Kong takes out China Inc. Lots of funny money is going to be shifted and burnt through.

Quite a while back I read a study of what percent of revisions are downward. I don’t remember the exact percentage, but it was huge.

That should tell you something about their methodology just as “more accurate” CPI calculation methodologies always result in lower CPI figures.

LOL 500K revision. Deep State gotta Deep State I suppose.

Meanwhile in the real world anyone with a pulse can have 5 job offers within a week. No matter how much the left wants a recession, it ain’t happening.

I came to this site about a week ago and was impressed by the comments, I didn’t understand all of them, not being particularly well-versed in financial theory, but they sounded very interesting.

But now I’m reading comments that make me wonder. Garbage comments about ‘deep state’ are seriously giving me pause.

Zantetsu,

I stumbled upon this site recently, looking for housing data. I’m also put off by the “anti-MSM, deep-state, illogically pro-trump” propaganda. It just doesn’t meet reality. I’m a moderator on a website where comments like that just get destroyed….hoped for the same here. *shrug* Russian bots gotta bot???

Yes, Wolf has this mysterious tolerance for the “deep state” kooks on this site.

That’s why I keep reading other sites. Everything on the internet comes with a POV. Figuring out what that POV is key to sorting out the level of believability of any internet blog, post, or news story.

Agree. I read Dmitry Orlov’s site but he very recently went on this jag about the moon landing being fakes, like wut? He was serious too.

Likewise the “OfTwoMinds” Guy, it’s a little ad-dense and I’m not sure why I bothered, and he solved my problem for me by going on some weird rant about the “deep state” and so I don’t need to visit his ad-fest site any more.

Let’s keep this site about real facts, you know, the real kind.

Knee-jerk jerks gobble down conspiracies without chewing. And there’s some burning desire to spread the b.s. – a Paul Revere fantasy… ‘the British are coming’. But the ‘deep state’ aren’t people in red uniforms, they’re whomever Bannon thinks they are.

You’d think that with the avalanche of lies by Trump, there’d be some degree of questioning of the b.s., but no, his worshipers are ready to blow up the system and spread the gospel that there’s a deep state. If Trump loses at something, he’s the biggest victim in history, and it’s always a conspiracy against poor Donald. “The election is rigged”. Want a history lesson on “real” conspiracies: The Birther Movement.

Here’s an article from informed, knowledgeable people on the deep state bogeyman. Too bad “Just some random guy” probably won’t read it and let the light of reality spoil a spooky, sinister story-line. https://www.govexec.com/feature/gov-exec-deconstructing-deep-state/

Better not get on the wrong side of the orange one: you’ll be a deep state operator yourself!

I’d like to see Wolf nip this crap in the bud.

We all know the BLS and other FED agency numbers are cooked and the stats are fake. It’s a running joke on this site when sometimes referring to triple seasonally adjusted downward revisals.

Zantetsu: Nobody cares about your opinion of the comments section.

Hi everybody on both sides of the “Deep State” debate: a teeny-weeny bit of tolerance goes a long way. Just don’t try to preach or proselytize.

I come to this site to educate myself by reading what Wolf has to say. If you are reading comments here and other sites, you should consider them entertainment.

Wolf, sorry. I’ve been on the “now now children, be nice” side of moderating. I should know better.

As an aside, have you thought about having commenters create a profile so we can check replies easier? I guess that would be much more of a commitment for the comment section for you workwise. But I was noticing how much your comment section has ballooned in the last few years- you’ve got yourself a legitimate community here.

GirlInOC,

“… have you thought about having commenters create a profile so we can check replies easier?”

Can you clarify that? I’m not sure what you mean. Do you mean that there is some kind of link under each commenter’s name that when you click on it takes you to all his or her prior comments?

Or do you mean email notifications of replies? I used to have that, but I turned it off because some commenters used this function to get into endless arguments with everyone that tore up the comment section and made it very hard for me to deal with. That’s off the table forever :-]

But I’m open to looking into some kind of profile link, if that’s what you mean.

Wolf,

Well, if your goal is to DECREASE arguments via less replies, then my idea won’t help. ha ha. But yeah, have members create a profile (or like a membership, I don’t think it needs to be mandatory to comment), so we can check replies and our comments. We can also message each other through our profiles…which is sometimes helpful. But this all might be a can of worms you want to avoid. Understandably. Especially if you want to avoid being the Reddit of the finance world. ;-)

Oh and under our profiles you can link the articles that have new comments. Sometimes it’s hard to tell which article has new comments because I basically have to remember how many comments were on each article. So that way if someone comments on an older article (like us here), then members can get a notification:

*New comments on “Repo Market Problems & Ballooning Inventories of Treasuries at Primary Dealers Make it into the Fed’s Minutes.”

I just read an article about the last recession. The system reporting doesn’t handle recessions well and basically tells you things are good the first fee months you are in a recession and then massively revises to the downside. I don’t think it’s intentional. A recession is finally called about a year late.

I think we are heading for recession unless interest rate cut or another tax cut to keep the juice flowing. Not good for long term I don’t think as there is already enough distortion in economy.

You ALWAYS keep forgetting to add, “Let not your heart be troubled”. But then I guess that’s why you aren’t worth $100M+.

– A new rate cut is already set in stone. The only question is WHEN.

– When primary dealers are stuck with Treasuries then they could try to sell them at a discounted price. And that means that the yield on those T-bonds have to go higher.

– And WOLFSTREET still thinks the FED is able to control the interest rate on those bonds (e.g. T-bills) ?

How are dealers “stuck” with something that is rising in value as the rates are cut?

Because it is election season. The opposition party is throwing all the mud possible.

Yeah, the dealers picked a really appropriate time to hang onto those Treasuries, they’ve shot up greatly in value.

No one on Wall Street ever seems to be stuck with anything… that job belongs to the taxpayers, the retail investors, and those who take out mortgages without reading the fine print.

– Quite simple. It means that maturities of 1 year and longer will be cut in price (= rising yields) and maturities of say 6 months and shorter will fall in yield (= rising value).

– If funding costs (for those bonds) go higher than the yield on the bonds then those dealers will be forced to sell those bonds.

“Quite simple.”

But rates have dropped while the dealers were “stuck”….how did they do?

If fund costs go higher….

But did they, and will they?

The dealers made money holding treasuries all year…

Please include in the:

Not Hawk-O-Meter (because everybody knows Hawks do not exist)…

And remake it the We-Are-All-Super-Ultra-Dove-Deluxes-O-Meter:

Asset Purchases and Lower Bound.

Thanks

Hawks exist, it’s just the relative line between Hawks and doves that’s moved.

The slow push of rates higher over the past couple years is hawkish vs the dovish view of no hikes ever. Similarly, Fed hawks like to throw out any consideration of NIRP, some even advocating a line of 1% as the bottom rate.

There are articles out today saying that the recent 0.25% cut was a lot more controversial behind the scenes than previously thought as many didn’t want to cut. The vote wasn’t unanimous.

>> high level of nonfinancial corporate indebtedness

financial vs nonfinancial – what is the significance?

Pelican,

“Financial debt” is debt that was issued by banks and non-bank lenders. They all borrow money to lend money. That’s their business model. They’re just intermediaries or conduits. This is very different from borrowing money to invest in a building or oil production or whatever (“non-financial” debt). So the two are separated.

Financial debt is used to measure leverage in the financial sector.

If you count financial debt and non-financial debt together in one number, you end up double-counting a lot of debt. For example, if my bank borrows $100 million from the bond market and then lends me that $100 million to build a factory, then the actual debt is $100 million that has been handled via a middleman, the bank. Not $200 million.

So my $100 million loan would be “non-financial” debt. And the bank’s $100 million bond issue to fund this loan would be “financial debt.”

“For example, if my bank borrows $100 million from the bond market and then lends me that $100 million to build a factory, then the actual debt is $100 million that has been handled via a middleman, the bank. Not $200 million.”

From where does the bond market get the $100 million (to buy the bonds) in the first place?

From investors wanting to buy bonds, from your bond fund, from pension funds, from foreign investors wanting to buy bank bonds, from Apple and Microsoft wanting to invest their cash that they get from their profits…. There is huge demand for bonds, as you can tell from the low yields.

“Wolf Richter

Aug 22, 2019 at 9:35 am

From investors wanting to buy bonds, from your bond fund, from pension funds, from foreign investors wanting to buy bank bonds, from Apple and Microsoft wanting to invest their cash that they get from their profits…”

Yes, but from where do the investors, my bond fund, the pensions funds, the foreign investors, those that bought stuff from Apple and Microsoft so as they made a profit get the money in the first place? It has to have originated from somewhere, right? I’m just asking you from where it came?

I reckon all money is loaned into existence by private banks but you, I believe, don’t agree. So where does money, that’s not loaned into existence, come from?

medial axis,

You don’t care where your beloved bitcoin and other cyptos come from. They’re created by computers, called mining rigs, that churn out these digital entities. Anyone with access to electricity and a big enough a computer can do it. And you still love them and believe in them. You’re in good hands there. Then why would you care where “money” comes from?

@Wolf – Completely disagree re: “there is huge demand for bonds, as you can tell from the low yields”.

It’s not like bond suppliers are cranking up production to meet demand because customers are lined up around the block, demanding more opportunities to lend from their savings.

Nobody “wants to buy” bonds at yields between -2 and 2%. They are buying because they are stuck with credit they cannot put to any better use immediately. The central banks have pushed so much zero-maturity, zero- to negative-interest credit into the system that no one wants to sit on it. That created the illusion of demand for everything financial gave us the Everything Bubble.

But it’s all a massive game of hot potato.

The only thing here for which there is insatiable demand is the Financial Free Lunch. The Zombie companies think they’re getting a Free Lunch, as do the bankrupt governments who cannot afford higher rates. As rates drop, investors see their portfolio valuations rising and think they’re getting a Free Lunch too.

So whenever the price-momentum breaks and people start to wake up to the reality of years of zero-to-negative returns from those dying zombie-companies and bankrupt governments, the central banks hit them with another “credit stimulus” and push the bubble ever higher. But it’s all unsustainable.

This is a reply to Wolf Richter’s most recent comment:

‘Then why would you care where “money” comes from?’

I am not sure why this commenting system doesn’t allow me to reply directly, although I am guessing that it only allows reply chains so many levels deep …

There is a big difference between ‘the money supply’ in cryptocurrency, which controls the creation of currency via published algorithms that cannot be deviated from, and fiat currency that is created at the whim of a government that can game that system however it wants.

I am not personally saying that I have a problem with fiat currency, I am just saying that there is a big difference there and that could easily explain why someone would think ‘care’ (i.e. not like) how money is created in fiat systems but be fine with how money is created in cryptocurrency systems.

Hm, but I can respond to my own comment so I guess it’s not a comment depth issue …

Sorry for the garbage posts, but it appears that it *is* a comment depth issue because my previous post was at a level one higher than Mr. Richter’s comment, and my reply at the same comment depth as his comment, cannot be replied to.

@ Bryan “cryptocurrency … controls the creation of currency via published algorithms that cannot be deviated from”

That statement is flat out brainless. First off, algorithms are not fundamental, they are human constructs and can be changed just like any other constructs. Second, there’s no limit to the supply of algorithms themselves. Some crypto systems will endure longer than others, but there are so many cryptos out there now, forking this way and that, that it’s blatantly obvious that “creation of currency” is absolutely not under control.

“Wisdom Seeker

Aug 22, 2019 at 6:30 pm

…Second, there’s no limit to the supply of algorithms themselves. Some crypto systems will endure longer than others, but there are so many cryptos out there now, forking this way and that, that it’s blatantly obvious that “creation of currency” is absolutely not under control.”

That’s right. It’s not just innovation it’s evolution too – so no one’s in control – that’s exciting. You cannot do better than the combination of those two. The amount of work going on in the space is remarkable and most of it not driven by the normal investors, they are only just waking up to it. Those that ignore, or simply don’t see, it are missing history in the making.

Wisdom Seeker – I think you’re going to have to use a little more subtlety in your thought process than you seem either willing to or capable of to understand the point I am trying to make.

Of course *any* statement about the permanency of *any* human system can always be simply refuted with “but all people in the world can suddenly decide to undo it all so there is no permanency of anything”.

But is it really useful to talk about infinitesimally small chances as if they are a real possibility?

For example, I could say, “one thing is certain, you’ll always have to pay your taxes”. If I said that, a rational person would simply agree, because the chances that all taxes are suddenly going to be abolished is like 0.0000000001% or less, not even calculable. But I guess you are the kind of person who would disagree with my statement because of that infinitesimally small chance? You’d argue that, “actually, you might not always have to pay taxes, if everyone in the USA agreed to vote in politicians who would be willing to abolish all taxes, we could do it.” I mean sure it’s theoretically possible, but it’s not going to happen. So for the purposes of conversation, it’s just much smarter to simply assume with certainty that there will always be taxes than to constantly have to provide disclosures in every conversation discussing why this economic theory or that economic theory doesn’t make sense if there are no more taxes.

Bitcoin is the same way. It is a huge system with millions of participants and it works because the collectively run algorithm is locked in and cannot practically be changed. Sure, millions of people could simultaneously decide to run different software with a different algorithm for distributing new bitcoin, but the chance of that is so infinitesimally small as to not be worth even talking about as a possibility.

If Bitcoin loses popularity (which I hope it does because I think it is a farce, we need a cryptocurrency that can actually scale to a useful number of transactions per second and bitcoin is not it), then eventually, it may be used by so few people that a coordinated change could happen. But by that point, it won’t even be relevant, and it really won’t even be the same thing that I am talking about now — I am talking about “the bitcoin that is used by millions of people”, not “the future bitcoin that is irrelevant because it is used by hundreds”.

“Zantetsu

Aug 23, 2019 at 10:50 am

If Bitcoin loses popularity (which I hope it does because I think it is a farce, we need a cryptocurrency that can actually scale to a useful number of transactions per second and bitcoin is not it), ”

Have you heard about the Lightning Network? It’s a second layer solution that sits on top of bitcoin that enables unlimited number of transactions at near instantaneous speed at very low cost. The base layer, bitcoin, being decentralised cannot be both fast and secure – Bitcoin Cash (BCH) and BitcoinSV are examples of what happens if you try to have both (in the base layer). Bitcoin is evolution, we’re all learning by our mistakes. That’s why it’s so exciting.

Yes, I know about the lightning network. It is also a farce because it requires participants to sequester coins and allows any party to close the transaction at any time, which means that each party must constantly watch the entire block chain for completion transactions. And if you chain your transaction to a third party via the lightning network you now have even more to watch for. It doesn’t scale.

Thanks, Wolf! That makes sense. But don’t financial companies also have plant/equipment kind of expenses that they may use the debt for e.g. bank’s building/renewing new branches, cost of IT infra etc. Are they typically a smaller/negligible proportion of their debt or do they come under the other head?

I think the FED should go stochastic: Instead of all the waffle, then every 3 months they have a lottery on what the interest rate should be.

They could even fix a desired mean and then bump the rate around it by randomly pulling positive and negative numbers out of a sack of coloured balls or something making a normal distribution.

Televise the damn thing, with some celebrity picking out the balls, like a real lotto.

Why? Because the dumb AI’s that are “Markets” have come to rely too much on a precision and certainty that doesn’t exist and now the FED has become sucked into it too, where the merest noice from the FED sloshes trillions around in seconds.

We need to bring back some resilience to the game, blow up some beautiful crystal castles of leverage by surprise. To teach the others!

South Park already did that, literally.

Season 13, episode 3 “Margaritaville”.

However replacing all the chicken blood with a blindfolded Kristen Stewart pulling numbers out of a hat would probably be much more Nielsen-friendly. ;-)

Thanks! You know we are in some kind of trouble when South Park and The Simpsons turns out to be prophetic :)

I am pretty sure Athenians were saying the same when watching Aristophanes’ plays.

A classic. Especially with the non-Fed economic theory side story going on at the same time. Definitely in Aristophanes league.

Who will chuck the first squirrel??

Thanks for restoring some class to an exceedingly tiresome, boring, and futile “debate”.

Interest rates should be a blend of rates occurring in the economy, not set at a closed auction to primary dealers. My credit card rates are 25%+, nothing in the fed rates comes close to reflecting this, and I am closer to normal rates than they are. The rates should filter from the bottom up, from payday lenders charging 50%, from car dealers charging 24%, from utilities charging 1-2% a month late charges, etc. These are the real interest rates people are living with.

Savings rates are a joke because most people are one paycheck away from homelessness, and the well off are two paychecks away. The banks know higher savings rates won’t make a difference attracting money that doesn’t exists.

“Pour encourager les autres” for finance? Why not?

It’s time to get interest rates back to a historically normal 6-8 percent and get asset prices back into the stratosphere.

Come on Jerome, get it together.

The norm would be 3.5 to 4% here with an inflation rate around 2%.

Everyone seems to forget, and the effort to help people forget is all around us, that Fed Funds historically equal or exceed the inflation rate.

AND that would bring the annual interest payment on the national debt close to one TRILLION dollars.

Central banks worldwide are trapped due to their own hubris and stupidity. Provide the easy money heroin or everything collapses.

Who cares ?? That debt is NEVER EVER going to be paid back !

“annual interest payment “

Wolf – great article

What do you make of Robert Shiller’s view that effectively it is the direction of animal spirits we are watching , reacting to all of the sign posting and effectively freaking out? He came on Squawk box and espoused the view that the market itself is a bigger risk than the yield curve or any other tangible evidence because effectively all of this recession talk could be a self fulfilling feedback loop

When I balance this alongside Jeff Gundlach’s views to be invested in gold and short term treasuries I feel fairly confident with about a 20-25% weighting to equities.

To me markets are entirely rational. They add to monetary supply, that depreciates the underlying, while putting upward pressure on prices necessitating a more risk on strategy, in order to avoid be left behind, like pensioners and subnormal types with huge annuities.

If people could buy 5% short term CD’s, they might sell speculative asset classes.

The 2 yr – 10 yr inverted again yesterday. The inversion was shallow.

Come on, David. Navarro says it is a Flat Curve, not an inversion. :-) Spoken most likely from a Flat Earth location. Flat Curve?hmmmmm These people are crazy in their explanations.

I have been shouting and warning about these metrics for weeks here.

The primary dealer Treasury inventory has been very high approximately $250-280 bil. That’s a signal the Fed has to do QE to buy the new massive amounts of Treasury issuance since the rest of the World don’t want it.

EFFR or the effective Fed Funds Rate (the market for reserves) is now consistently higher than IOER. So too is the collateralized overnight repo (SOFR). The IOER was designed to also be a high cap, but now it’s acting as a floor in the bottom only.

SOFR is gyrating crazily in a 3 day cycle. The interest spreads and gaps are large. More weirdness.

The Fed may have lost control of rates. Long term yield has never been this low. If the Fed has 2.1% IOER for 1.5 trillion of reserves, then it better earn that much interest on its assets or it will likely reduce IOER more. If they lower rates, then IOER goes down, too.

“The primary dealer Treasury inventory has been very high approximately $250-280 bil. That’s a signal the Fed has to do QE to buy the new massive amounts of Treasury issuance since the rest of the World don’t want it.”

That’s not how I’m reading it. To me it says they could sell those Treasuries in a snap at higher yields, but that would mean at a lower price, and perhaps at a loss for the dealers. So they sit on them and hope that prices rise further (yields fall further). So they clamor for more rate cuts to make that happen.

I think we already saw that inventory drop from 7/24 to 7/31.

Notes and Bonds Inventory dropped from 246,319 to 205,942 (in millions). Prices increased so the dealers won.

The effect was more pronounced with T Bills. On 7/3 they had 41,425. On 8/7 it was -2,101 (in millions). Dealers won again.

So yes, they could be HOARDING thinking interest will drop and price will rise. But the amount of NEW Treasury issuance might be too much for them to deal with. Net new bills alone will already be an additional $212B till end of year. That’s why I think the Fed will help in buying new Treasury Issuance. I am not sure the World’s NIRP demand is enough to offset our increasing deficit.

Exactly right Mr. Richter. There was a treasury trade this week on Tuesday where an unnamed entity bought 60000 contracts. Whether it is a hedge or a bear position was not clear. The bet was made for Friday- today. Is it a speculative hedge or a protective play?

The Fed is largely responsible for this bubble. It started to do something about it by raising interest rates, but then the billionaires and their vassals howled and that was that. All this stuff they write is just so much nothing. They just want to shift the blame, like Trump, like Congress, like the Financial community to someone else when all this debt turns into the garbage it is. So sad, that no one wants to do the right thing, what’s best for the country…

“Coming into Jackson Hole, economists are grappling with a major issue: Can central banking as we know it be the primary tool of macroeconomic stabilization in the industrial world over the next decade?” – Larry Summers, 22 Aug 2019 tweet

“Coming into Jackson Hole, economists should be grappling with a major issue: Was central banking as we know it the primary cause of macroeconomic destabilization in the industrial world over the past three decades?”

There, fixed it…

Weasel words employed by bureaucrats of all stripes are tough to parse, being as how they are designed to cover the speaker’s ass, rather than contain a definite, attributable meaning.

RD Blakeslee,

“Weasel words” doesn’t do justice to the minutes. Reading the minutes is the most unpleasant thing I do as part of my job. It’s the most mind-numbing repetitive awful prose ever written. It’s sheer torture for the brain. And they’re long. Not counting the endless list of names of all the people that participated, including staff, and not counting the footnotes, the minutes amount to nearly 10,000 words. That’s about 12 average-length articles on WOLF STREET.

They’re designed NOT to be read. I hate them. And yet, in between all this torturous mind-numbing repetitive endless verbiage, they say important things. So I try to save you the anguish of having to read them yourself and give you some digestible morsels along with a soothing drink to wash them down with :-]

Thanks, Wolf – “… not easy to parse …”, that’s for sure!

Thank you, Wolf for your effort!

We here, all benefited from your insightful opinion!

“They’re designed NOT to be read. I hate them. And yet, in between all this torturous mind-numbing repetitive endless verbiage, they say important things.” Which reminds me of regulations that I read in the military. Unfortunately, I’m cursed to usually remember what I’ve read, and always to remember where I read it. Convenient to my fellow service members, they’d just turn to me. Mind-numbing is a good description of FOMC notes, too. I used to go read them. Thankfully, yes, I have you to save my brain the stress!

I occasionally muse about the job qualifications for positions such as a FED elite. Academic pedigree, suaveness, alpha type personality and projecting absolute certainty quickly come to mind. Wolf’s comment here clearly shows that skills in Gobbledygook should be added at the top of the list. P.S. : Those with common sense need not apply.

sp500 is 3% off the all time high. This is after a month’s worth of OMG OMG OMG the sky is falling hysterics in the MSM.

Three whole percentage points!

And that price is a whopping 1.3% higher than a year ago which means total returns are probably negatory.

Add in dividends and it’s more like 4%. Which isn’t great, granted. But the way the MSM is talking you’d think it’s negative 25%.

(In billions)

The Primary dealers REPO about —

Overnight:1,770.0 Term: 716.3 Total: 2,486.3

About 1,701.2 are secured with US Treasuries.

Source: https://www.sifma.org/resources/research/us-gcf-repo-index-triparty-repo-and-primary-dealer-financing-reporeverse-repo/

That means they need COLLATERAL !!!

In the week ending 8/7 they had a total of 226,249 (millions) of US Treasury NOTES and Bonds (G.T. 1 yr). That’s about $226 billion.

Sure <= 2 yr peaked on 7/10 to $96.574 bil. It is now about $10bil LESS or $86.824 bil.

How the Primary Dealers manage their inventory is not easy to understand. You can take a stab at it reading this (Warning Wonky):

https://www.newyorkfed.org/medialibrary/media/research/staff_reports/sr299.pdf

*The regular issuance and redemption of securities creates a different inventory management problem for government bond dealers versus equity or foreign exchange dealers. We assess how U.S. Treasury dealers manage their positions and in fact find that underwriting plays a key role. As explained by Madhavan (2000), “[J]ust as physical market places consolidate buyers and sellers in space, the market maker can be seen as an institution to bring buyers and sellers together in time through the use of inventory.” Our findings emphasize the key role of dealers in the intertemporal intermediation of new Treasury supply.

Specifically, we find that Treasury dealers absorb a large share of new Treasury supply by retaining securities bought at auction instead of immediately selling these or similar securities to other investors. Moreover, dealers retain this exposure for at least a week, offsetting only small shares of their auction week purchases in adjacent weeks. Further results show that dealers still hold large shares of issues at maturity, especially issues with short original maturities.

We also find that dealers adjust their response to new inventory differently depending on the source of the trade. In particular, we show that Treasury dealers engage in selective hedging, offsetting a much smaller share of spot position changes in the futures market when such changes are explained by issuance and redemptions. Presumably there is less need to hedge these inventory changes because they are not information-based. Such behavior is consistent with that of U.K. government bond dealers, documented by Naik and Yadav (2003b), who also adjust their hedging depending on the perceived level of asymmetric information.

Lastly, we identify patterns in Treasury returns related to dealer intermediation of new Treasury supply, thus explaining a component of Treasury yield predictability not previously explored. These patterns suggest that dealers are compensated for their intertemporal intermediation of Treasury issuance, consistent with the prediction of standard microstructure models. That is, dealers tend to buy Treasuries during auction weeks when prices are depressed by the new supply and are then compensated by price appreciation the subsequent week. Our results therefore add to the evidence from equity markets (Hendershott and Seasholes (2007)) that inventories have significant asset pricing effects at a multi-day horizon, and show that such effects can exist even when the inventory changes are publicly known.

Me again… I am not sure how we can make sense of these numbers. The only thing I can say is the Primary Dealers inventory PEAKED at $287 billion. It is now $224.148 billion (so they have room now).

Whether they can afford to keep more than that depends on the REPO market where they offload these (and of course the foreigner's or INDIRECT buyers willingness to buy). For that reason alone, I think the Fed may have to restart QE as the buyer of last resort. I think the word for that now is STANDING REPO FACILITY or SRF an idea coming from the St. Louis Fed. Yes, Bullards group. This means the Fed can increase reserves whenever it wants to. Watch out for its activation. Interest rates do not have to go down to near Zero. The Fed can QE anytime and increase money supply.

I think Congress might take an interest in the Fed restarting QE, especially in an election year. The power shift back to Capitol hill should not be underestimated. Fed traditionally greases the reelection skids, bipartisan mandate, it’s possible they might get called on that.

Dems helping Donny, re-elected!?

Wow!

Me thinks they will PRETEND but not really!

Meant to say Congress might block more QE in an election year. That would set up a partisan battle. If the Fed is pressured into holding a lot of Treasury paper Congress has precedent to monetize those reserves.

CNBC reported Germany can not sell all its new bond issuance. Negative interest rates are as popular as square wheels. Official inflation is low as their economy recedes. I do not see Weimar Republic conditions.

It will be T bills that have massive increase in issuance for the US Treasury.

You can do a little math. These T bills are issued WEEKLY.

The ADDITIONAL Amounts auctioned are:

4 week +20b/week

8 week +5b/wk

13 week +6b/wk

26 week +6b/wk

Dealers buy about 60% of these for themselves. You can estimate this with the weekly auction announcements.

In the last 13 week auction, the foreigners bought little, so the dealers ended up with ~70% of the auction.

That means that the dealers need to buy about 23 billion MORE PER WEEK. This is additional to their normal purchases of Notes and Bonds.

If they get overwhelmed in T bills, the Fed has to help.

That’s why last June 6th, there was a SOMA Reinvestment testing for T BILLS. I would not be surprised if FOMC steps in and does a QE like move (named differently of course).

I hope I’m mistaken but this math is easy.

They’re nowhere near “overwhelmed”.

Although Wolf doesn’t believe it, the Primary Dealers can de-facto pull credit from Excess Reserves (or “wherever”) to buy Treasuries, then sit on the Treasuries and wait for Uncle Sam (or his payees) to deposit the credit somewhere else in the banking system, at which point it flows back to Excess Reserves and can be borrowed again by the bank.

It all nets out, just ask the Italian banks for whom this is a way of life…

That’s not that easy. Reserves can be exchanged for new Treasuries when the Fed rollsoff or allows their Treasuries to mature. But that ended Aug 1st. There has been massive rollover SOMA add-ons since then.

Besides primary dealer liquidity is not limitless. They need to fund new auctions.

The primary dealers usually get new cash to buy new Treasuries in the repo market – the wholesale capital markets, primarily tri-party. This is the plumbing many folks don’t understand. This plumbing is limited unless the Fed steps in and becomes a lender or permanent buyer of Treasuries.

Some of the reserves bleed out as currency in circulation. You can do the easy math as the Fed’s asset is more than excess reserves. That’s an exchange from reserves to cash.

can someone explain to me repo market,ioer and dealers inventories

Ogg, each of these topics is complex

I highly recommend you read Zoltan Pozsar’s work for repo and primary dealers. He worked at the Fed and is now in Credit Suisse. The NY Fed has old videos in YouTube that’s very helpful.

For IOER, I suggest you read George Selgin. You can find him at Alt-m.

I follow these 2 guys a lot as well as listen to podcast guests at Macro Media. They are very helpful in understanding more than the basics so you can think for yourself.

LoL, welcome back to the land of depression economic growth. Wages must rise…..and assets fall….

Usually great wars are the only way that happens involuntarily.

ill play wolf, jp stands pat.

Hi Wolf,

While drinking a bock beer I noticed a couple of questions about financial terms and mysteries in the comments. When I was twelve my uncle gave me an S&P Blue book (1970’s) and told me to find every stock priced at $10 with a PE less than 10. I had no idea and my search for financial term definitions began.

For the Present day I may suggest the appropriately named https://www.investopedia.com/ for those new to the topics and ideas presented here.

A question for Mr. Wolf. You regularly publish data from reports on who is buying USG debt. I’m assuming that this growing inventory of treasuries in the hands of the official dealers is a subset of the amounts you publish as being owned by American investors and institutions. Is that correct?

And a further question, if you don’t mind. Could these be considered inventories of those dealers, with relation to an analogy to the way inventories build up in other businesses and lead to future reductions in purchasing as they now feel that their inventory is becoming too large?

Question 1: Yes.

Question 2: Nyes? Yno? The dealers have a reason why they keep this inventory. Unlike certain physical merchandise (for example, dresses at a retailer that are out of fashion trends), these Treasuries could be sold quickly, and there is enough demand to absorb them. But the price might be lower at which they would sell. Also, the dealers might expect that prices would rise and they would sell later at a higher price. And they might have other reasons. So it’s not exactly like an overstocked retailer that has to do a “70% off sale” to clear the merchandise.

Interesting viewpoint on negative interest rates by Von Mises.

https://seekingalpha.com/article/4287532-disaster-negative-interest-policy?isDirectRoadblock=true

The Von Mises article is interesting.

States at the top , something to the effect that negative rates are impossible, i.e., they cannot exist, or something very close to that; following with some good bullet points, and closing with something to the effect that the philosophical economic model that the ECB has made, to justify NIRPs, is not justifiable, and is, in fact, deeply flawed and harmful.

Hey, it’s refreshing to read that Dragi and company have even felt like they needed to construct a model to justify their behavior !

Seems like a good place to pose the question: how can a bond ETF like IEF move up +15% in a year? The underlying bonds can’t possibly have moved that much. Are these the “bond funds” Fed refers to? If so what is the basis of their valuation? Or are they traded like closed-end funds with no correlation to price of holdings?

Broken Clock Capital,

When yields fall, bond prices rise. So short term, there can be big gains. But you have to sell the bonds pretty quickly, because as they get closer to maturity, the value of bond moves toward its face value because the last guy holding it on maturity date, when the bond is redeemed, will get paid face value, and that is it.

So a bond that matures in five years and has a premium of 30% will give up the entire premium as the bond approaches its maturity date. Bonds are NOT like stocks. Bonds CANNOT retain their premium. They’re ultimately worth face value at maturity, unless they default before.