Making deals where the buyers are. And the buyers are at lower price points.

It’s homeowners and the pros – the homebuilders. Yesterday, we got data on sales by homeowners: Despite plunging mortgage rates and ample inventory, sales fell for the 16th month in a row, but prices rose to a new record. After surging 52% in seven years, prices are too high and are hitting demand. Today, we got data on sales of new houses by homebuilders: They’ve chopped their prices to the lowest levels in years to prop up sales, as they’re loaded with inventory that they have to sell because that’s how they make their living.

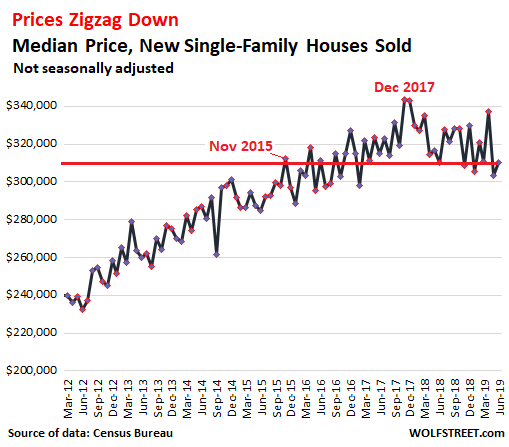

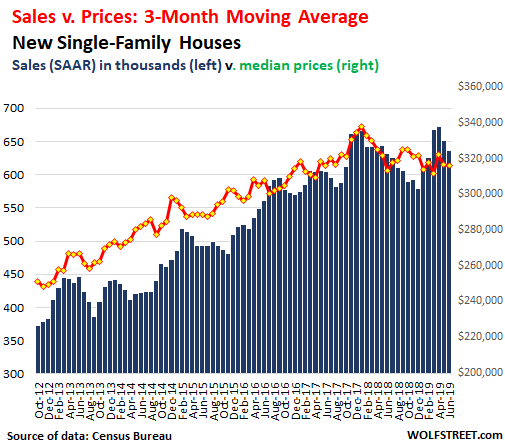

According to the Commerce Department this morning, the median price of new single-family houses ticked down from a year ago to $310,400 in June – below the median price first seen in November 2015, and down nearly 10% from the peak in December 2017:

The price drop starting in December 2017 was the sharpest since Housing Bust 1. But these price changes do not include incentives – the free countertop upgrades, etc. – that homebuilders throw in to make deals. And these lower prices, and whatever incentives homebuilders threw in brought out the buyers – not en masse, as it was hoped after the plunge in sales that started in mid-2018, as mortgage rates had risen to painful levels, but enough to reverse part of the slump.

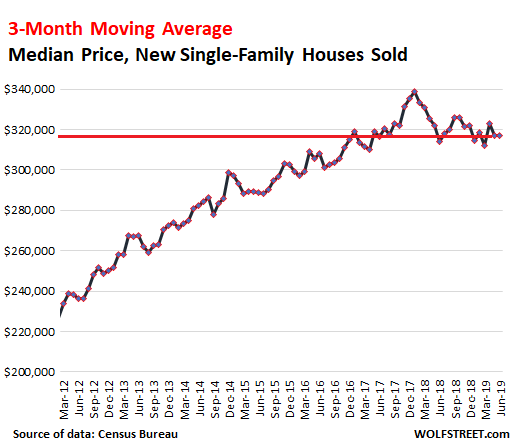

This new-house price data, produced jointly by the Census Bureau and the Department of Housing and Urban Development, is volatile on a month-to-month basis. The three-month moving average irons out some of the volatility and shows the price trends more clearly:

The current price declines of around 10% from peak through June pale compared to the brutal Housing Bust 1 from early 2007 through 2011, when the median price dropped 22% peak-to-trough, before zigzagging higher again. From the range in 2011 and 2012 through the peak in December 2017, the median price of new houses surged by about 55%. This peak was 31% above the crazy peak of Housing Bubble 1 in March 2007. But prices have hit a ceiling:

Homebuilders have to move their speculative inventory. So they’re making deals at lower prices, and they’re also shifting some of their building activity to houses with lower price points. This strategy, along with much lower mortgage rates, had a salubrious impact on sales volume.

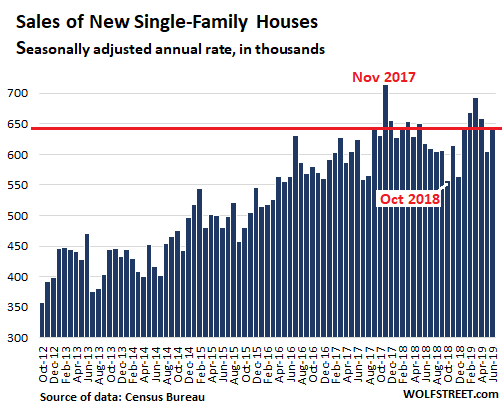

Sales of single-family houses in June rose 4.5% from June last year to a seasonally adjusted annual rate (SAAR) of 646,000 houses. This was about halfway between the recent low point in October 2018 of 557,000 and the peak in November 2017 of 715,000:

The relationship between prices and sales. To get a better sense of the trends beyond the month-to-month volatility, I converted median prices and sales into three-month moving averages, and overlaid them into one chart below (sales volume = blue columns, left scale; median prices = red line, right scale). It shows how the sharp drop in sales that started in early 2018 was stopped and partially reversed by significantly lower prices. But sales volume is now back on the decline, likely leading to further downward price pressures:

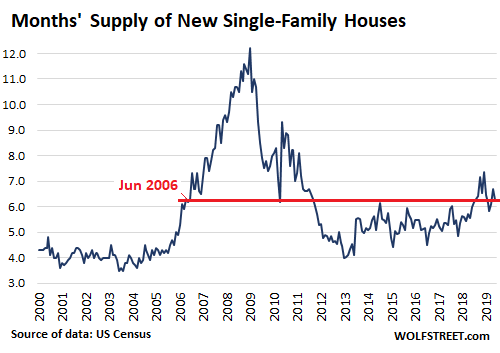

Supply of new houses for sale started to rise on a year-over-year basis in January 2018 and has risen every month since then. In June, there were 338,000 houses for sales. This was up 4.6% from June last year. At the current rate of sales, this amounts to 6.3 months of supply. Four months’ supply would be more than enough. And 6.3 months is the level supply suddenly shot up to at the beginning of Housing Bust 1 in June 2006. If it doesn’t rise further, it’s not a crisis level, but it puts pressure on homebuilders to get busy cutting prices and making deals:

Homebuilders, unlike homeowners, have no illusions. It’s all about building and selling homes, and making a profit doing it. When they build speculative houses in a tough market, they cannot just sit on them and wait for the market to get better. They have to sell their inventory. This might take some time, but they will do whatever it takes to move those properties – not panic-selling, but making deals where the buyers are. And those buyers are at lower price points.

Surging prices are a demand killer, but real estate industry laments the medicine didn’t work. Read... Ultra-Low Mortgage Rates No Relief for Home Sales

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

We’ve added 20M people in ten years (6%) and almost 30% on the home median price. Good job Fed!

Here in the Portland Suburban area Zillow page the listings are about half full of new homes. These are easy to spot because the builders don’t put up pictures of real houses but rendered graphics of what the house will look like when it is done. Ground has broken on most of these homes so the builder is stuck with the floor plan, but they are desperately trying to sell them before they are completed. This builder “zombie house art” as I call it has grown massively compared to 6 months ago.

In Rohnert Park CA a large development was going in a roughly a couple years back.

Was out there (for open flat) calibrating a CB for a friend. Only at street & utility stage plus a few model single family homes, but we guessed it could go to maybe 2-300 (?) if they used all the land available. Also guessing usual bedroom for SF jobs, not a whole lot of tech industry around this area, but a fair amount, plus all levels of gov’t stuff, and std local biz. Anyway, time to go back and see if sale/rent signs are up.

BTW, good online tag. Being Seneca fan, am guessing observation might have been sparked by the once Greek dominated Mediterranean when Rome took over?

Here’s a cultural headwind for new home sales…

My recently immigrant family members will never buy a new home if it’s part of a HOA, which is usually a selling point for the mega-homebuilders. Way too restrictive for even their authoritarian backgrounds…

Good point. HOAs are usually PITAs.

People move to HOA’s after bad experiences in free-standing homes without regulations. Once you have a neighbor on one side with 6 barking dogs 24/7 and the guy on the other side with 6 partial Edsels up on blocks in the yard because restoring them is his “passion”, an HOA seems a welcome place. The rules and regulations are spelled out in detail before you buy. You must sign a paper saying that you have read and understand them and intend to comply before the closing is over.

They have more clout than any city or state ordinance or law. They are a legal contract. You have agreed that if you violate the regs, you will pay a monthly fine of X dollars. After 60 days, usually, the HOA has the right to take your property in foreclosure. And they do. They always win.

Laws and ordinances can be ignored for years, and courts drag on forever without results. That’s why people with similar interests live in HOA’s.

I rent a house in an HOA. There are dogs barking 24/7, and nobody does anything about them, but they forced all the homeowners to get new roofs (not a bad thing, the old ones were all shake).

You have a point: The HOA violates the city’s lawn watering restrictions regularly and AFAIK no one has taken them to task. The city sends violation notices to me, but I have absolutely no control over the sprinkler systems.

Put in an offer in Tucson with ex girlfriend 2009 for 1K ft/sq single family in mixed (many upscale) housing, completed, all occupied (over 3-5 years?) Nice area (Ram-N Oracle) with HOA dues only $30/mo just to keep it nice per realtor. Unadorned rock landscaping fine there. ( Maybe put out couple cacti and unofficially AZ req’d Pele. ;) ) Anyway, don’t mind that as long as boomer+ neighbors don’t have anything better to do than run around with a clipboards, as I’ve seen in sister’s roughly similar $200/mo HOA with pool, tennis, clubhouse, largish amount of open area grass and landscaping, etc.

I never get the HOA hatred. Do you want your neighbor across the street to park 5 cars – 2 of which don’t run – in the driveway? No you don’t. In an HOA he can’t do that. In a non-HOA he can.

HOAs don’t necessarily prevent any of this. In Florida almost every house is in an HOA and they can be a nightmare. People get entrenched on the boards and the power goes to their heads. The board members and their friends get special treatment, as do their business associates, and the rest get ignored or harassed.

I’ve lived in 3 HOAs and never had any issues.

HOA rules are common sense things: don’t park your RV on the street, can’t own more than 2 dogs, can’t paint your house purple, you have to mow your lawn, you can’t leave the garbage bin out on the street for days and days after garbage day.

The vast majority of people look at those rules and think, yeah makes sense. And then there’s a small group who think 2 dogs? Eff that, I’m getting 5 dogs. Or I’m not paying for storage, I’ll damn well park my RV on the street. And when the HOA comes knocking, they whine about how unfair and fascist HOAs are. No they’re not fascist, they’re enforcing rules YOU AGREED TO!

If you don’t like the rules, fine. Buy some property in the woods and do whatever your want. But if you agree to live by a set of rules, don’t whine about the rules being enforced.

Yep, that does happen.

Instant delete. No thanks (minus the thanks).

Foreign buyers , especially the Chinese have disappeared. When the stock market tech rally implodes , start ups along with hiring will dry up. Look for a real estate depression and a 2/3 correction in SF,LA, NYC, MIA, BOS prices before this is over in 5 years.

Prices in those area have been dropping already…without the tech bubble burst or recession. Just think what those will do the prices when they do happen. Just wait until China forces money launders to bring back stolen money or their families will be executed, that’s when the fun really starts!

This is what I have been saying. These areas are showing significant signs of slowdown (moreso on the west than east, but east tends to lag by ~1 year), and things are very good in terms of unemployment and household debt service. When a recession comes, the bottom will drop out on these markets. In Boston, I’ve noticed a sharp uptick in homes dropping out of escrow (due to financing), and there are reports of sharp upticks in foreclosure prevention activities. The DTI ratio of buyers is pathetic, they may not be liar loans, but we are setting up for another round of subprime borrowers that will be in serious trouble the first time they go a few months without a paycheck.

But Larry Yun and Danielle Hale (aka David Lereah 2.0) told me it was “to the moon Alice!” She literally said “its different this time” last week. Whatever econ program granted her a degree should lose its accreditation.

That will be the new asylum classification – Real estate based asylum for Chinese tax evaders.

I could almost see this, as it’s a half-mil for insta-citizenship (it’s even less for some countries, a bit more for a few) and usually at least a mil for a house …. USA might not want that money leaving.

I’m extremely bearish on the next 5-10 years of real estate, but what do you mean by 2/3 correction? Losing 2/3 of their vaue? I doubt it. 1/3? Very possible. I say less with a long, long period of home value stagnation while inflation eats away at the value of it.

Also, in before the Timbers’ Neighbor Home Price Index, which is far more valuable and accurate than Case-Shiller.

Rcohn Growth of US Tech Job Listings has slowed:

https://www.axios.com/the-growth-of-us-tech-job-listings-has-slowed-1bab5b19-6917-452d-bc81-a426bd91761d.html

When housing permits—particularly for single family permits go negative for Texas, it means bad news for housing. Permits are down for 38 states through June 2019. United Rentals cut guidance, today CAT reports dealers have increasing inventory. It does not look like a good 18 months for housing despite good employment numbers and low mortgage rates. The price of housing has climbed too fast, and younger buyers having trouble with debt and down payments.

Permits in TX down? Coincidence?

https://oilprice.com/Energy/Energy-General/Job-Losses-Hit-As-Shale-Slows-Down.html

Bob, in the oil sensitive markets of Midland-Odessa up 50% and Houston up 6%. Dallas seeing the biggest declines at 7 percent down. For single family permits, Dallas is down 5 and Houston down 3%.

Wolf,

You should one of your well researched posts on the recent drastic decline in RV sales. I am in the camp that this is one of the best leading indicators to a recession. Back in the 2000’s I owned a company that made parts for Class A ( over $750,000) motor coaches among other things. In late 2007 we started seeing order sizes get smaller and more sporadic. I took this as a bad sign and in early 2008 dumped all my holdings in the stock market, dumped my house, and wound down my business in the motor coach market. We all know what happened to the market and homes in 2008, but my motor coach customer went bankrupt in early 2009. I shared the same welding supply vendor with my Motor Coach Customer and when I tried to convince the owner to taper his business with this huge customer he sounded just like house pumpers do today. I quote,” the market for RV’s for the average guy may slow down, but Class A coaches are purchased by wealthy people with assets and a recession won’t slow down their spending at all. ” He lost $1.2 million in the bankruptcy and I lost $79.

Has ther ever been a 67%, 2/3 correction in real estate?

Not nationally.

Yes, in specific local markets as a result of specific local events, such as an oil bust in oil-based cities. I no longer have numbers for this, but I think Tulsa (where I used to live at the time and where I bought a condo in the late 1980s), experienced this following the oil bust of the early 1980s. This was when local banks dropped like flies, including my bank, when the FDIC became a major homeowner in town, and all the oil companies that were headquartered in Tulsa moved to Houston. It was devastating for the local economy. The city didn’t come out of it until the last five years or so.

I enjoyed living in Tulsa, though. My condo had a gorgeous view of the river, great running along the river too. I belonged to a cycling club that was active and fun. Doing business was tough, but I never noticed what a depressed place it was until I started spending time in other cities. I even sold my condo at profit in 2000 because I’d bought it for so cheap from a collapsing bank.

BTW, a decline in real estate prices of 67% is NOT a “correction.” It’s a bloody crash.

I no longer have numbers for this, but I think Tulsa (where I used to live at the time and where I bought a condo in the late 1980s), experienced this following the oil bust of the early 1980s.

If you hadn’t waited 30 years to start blogging I could have advised you to short Arbusto. You know, where Dubya made his reputation as an oil tycoon.

Ah, naked shorts, never to be covered. Those were the days.

Hey you guys, no snickering.

Wolf:

Helping home builders with cutting prices has been a large drop in prices of the commodities used in building.

2×4 SPF-the bellweather of framing lumber peaked in Spring 2018 at $650USD/1000 board feet, now bouncing around $300-350. Cedar decking peaked around $1850, now struggling for sales at $1300-1400. North Central OSB 7/16 Sheathing low $400USD/1000 surface feet last spring, now struggling at low $200’s, and plenty of sales in the high 190’s.

And all the rest of pricing in housing components are negotiable.

Truly amazing what a free market can do.

I closed on a new construction condo in CT in 1988. I had locked the price a year earlier. In three years the price was up 50%. By 1993, when the bank sold the property in a foreclosure, it was down 58%. I was a Realtor back then, and had gotten licensed as an appraiser. The prices were dead on, following the market back then. House prices in suburban towns, especially East Of The River, dropped 50%. They took a decade to retrace to the 1988 levels.

It wasn’t 67%, but pretty close. CT is not exactly Rust Belt, either. It can happen.

Southwest Florida had that kind of drop ’08-’11 or so. At one point, our house was appraised at less than our car. (And it’s not that small a house or that nice a car.)

Wolf, Thanks for the encouraging heads up. Us folks out here that got burned in 2008, we’ve been recovering and waiting for the chance to own a home again. This is the most encouraging news I’ve had in years.

I was looking in realtor dot com at homes for sale in another town. One ad showed the most recent sale was in 2012. They are now asking three times the price it sold for in 2012. That area was foreclosure city in 2012. Home prices cannot triple every seven years, can they? According to one local real estate statistics site, current asking prices are more than ten percent above recent selling prices. Some of these houses are not attracting multiple bids as they have been on the market for months.

salubrious – nice!

Can you use “plethora” in your next column?

If you check https://wolfstreet.com/?s=plethora it pulls up the WOLF STREET articles with “plethora” in them, about two dozen of them, some written by other authors, some written by yours truly :-]

Thanks, that means a lot.

(Not my original, but a good one.)

I haven’t seen Builder spec single family home developments for years, anywhere. I see new homes built for clients who have organized up a construction loan/mortgage, and I see the occasional development site plan complete with billboard graphics and “coming soon”, but I think the developers are waiting to build the big projects. They never show any progress other than some sewer going in. There is a new sub-division opening up just south of a nearby city close to where I live. The zoning is in place, a shopping plaza is planned and announced (with a request for approval for a larger sq ft anchor tenant grocery store), and the sewers and road infrastructure is going in……,but after that the prospective homeowners choose and buy their own lot, contract their own builder, and move in when it’s done. I just don’t see empty single family new homes sitting because builders are busy and already contracted for by living breathing clients.

There are also many new apartment houses going up; 4-6 stories and they fill up right away. I walked by one today on the way to the dentist, semi-waterfront, 6 stories with the wrap on and new windows just installed. There is a big sign on the front wall saying, “Now Renting”. I bet it will be pretty well filled up before it is even completed. Years ago existing apartment buildings were refurbished and upgraded and sold off as condos. Now, those apartments are being replaced with new projects because there is a huge demand in the rental market.

A year or so ago my niece bought a few acres around Bellingham Wa, after ascertaining they had water use/availability with the land purchase. (There is no new well drilling allowed for new homes in that County). They then shopped around and had a big house building company build their selected design; (modest and definitely not custom swank). The bank paid off the builder upon completion.

I just re read the article and it sounds like there are just too many builders. Perhaps this is just a normal shakeout.

– The long recessions (NBER) :

1) Oct 1873 – March 1879, total : 5Y + 5M. GDP fell 33.6%. After a short relapse, the next one rolled over :

2) Mar 1882 – May 1885, total : 3Y + 2M. GDP fell 32.8%.

3) Aug 1929 – Mar 1933, total : 3Y + 7M. GDP fell 26.7%.

– Is it possible that we are going to get a recession.

– Can it be long, deep, and in repetitions

– The (-)5.1% GDP, 1Y + 6M recession from Dec 2007

to June 2009, was the longest since the depression.

– No we can’t according to the FANG. Yes we can, according to Sir John Glubb PDF, “The Fate Of Empires”, because our nation is old, we are 250 years old, on the crosshair.

– All symptoms are there, every day. According to Sir John, we are already in deep troubles.

Up to Their Neck in Inventory, Homebuilders Cut Prices to November 2015 Level to Boost Sales

They might like to start giving them away before they bury themselves in their own production.

As usual, one of the primary deficiencies of supply-side capitalism is the lack of balance with the demand side. Which is to say, if you build it, they’re not going to come, unless it’s some fictionalisation starring Kevin Costner.

For a compendium of secondary deficiencies refer to all previous posts.

Unamused

Supply and Demand are dynamic forces (except where Big Government dictates via the price of borrowed money and regulations) which struggle with each other around the fulcrum of price.

At $50,000 for a house, Demand would far exceed supply. At $500,000, Supply exceeds Demand.

There was a lot of air in the prices of free market inputs into housing costs and that air is being squeezed out. Mills and production is shutting down to keep prices from collapsing further.

Really? I couldn’t have guessed.

The Boston Globe keeps publishing “no inventory!” “get in now or never” articles. Should be interesting

The Boston Globe is utter trash. They’ve always put up that kind of stuff as long as I can remember. Someone there must be heavily invested in RE and wants it to go “to the moon Alice”

I wish it would hurry up and crash. I’m getting tired of waiting!

Same here, what we have right now it’s not sustainable. These inflated assets will have to deflate. Here in North Texas looks like properties prices are up about 40%, 50% in general. I would be happy with a 20% to 30% decrease. But the 1% or 2% I am hearing, I will pass.

I’m for a healthy economy, but QE Infinity artificially inflated is not healthy. It will hurt the working class the most when is all said and done. Young families are priced out of the housing market. Not because of supply and demand, but bad monetary policies and too big to fail.

Look at our National Debt… It won’t end well, for us.

curiouscat I agree with you… but the whole thing is manipulated so it will trigger when it triggers.

The stock index is super high. The economy is supposedly great. 30y mortgage super low at 3.81; yet homes have a hard time selling. Something is not right. The buyer can’t afford.

Let me explain what has happened in a way you might just appreciate.

And w/o all the obfuscation of tiny variations in stastical minutia which distracted rational thinking and conflated the exit of foreign purchases, rather enlighten us on what is happening in our own economy.

In Dec 2018, Super Ultra Dove Deluxe Powell did a U-Turn.

Powell’s U-Tern thru a Tidal Wave of liquidity at assets.

As a result asset prices have soared.

Super Ultra Dove Powell succeeded.

This was Sssssoooo easy to see for anyone paying attention to their neighborhoods NOT CASE SHILL. Super Ultra Dove Powell has completely re inflated asset bubbles, starting in December at his U-Turn.

The economy? Not.

Because we all know that the polices of Super Ultra Dove Powell and his ilk do not benefit the economy, only his Ultra Rich Friends.

Because Super Ultra Dove Powell, like all his fellow Super Ultra Doves, does not and will never ever get that the fact that inflating assets is the opposite of helping the economy.

IMO its not that they cannot……its that they don’t want to…….home ownership is maintenance, real estate taxes, insurance and lots of additional work. They compare the costs of a 1600 sq foot apartment that includes access to a beautiful gym, pool, common entertainment area to owning a 3000 sq ft home and say……how stupid do they think we are. Kids don’t play much outside anymore. Its games in the rec room. So the back yard means little. They change jobs every three years so decorating is for suckers. The tepid numbers in the face of the demographic strength is just evidence.

Keep in mind that “$3,000 in upgrades” probably cost the developer about $1,800.

$3K is retail, $!,800 is (More or less) wholesale.

Countless ads for “new construction” here….nothing, not one, under 500k. The majority seems to be closer to 1M. I get higher profit can be made in upper-end units, but why did so many investors/builders not foresee a glut of million dollar homes in an area without a glut of millionaires? (we aren’t quite at SF levels of income).

I talked to an agent this weekend who represents “high end” Newport Beach clients. I asked if there was a correction coming and he said no way, not in my price point (500k), but maybe in the upper end of the market. God, I want him to be wrong. But even with this slowdown, I’m not seeing it come down enough right now. Unless this is the quiet before the storm?

They are just waiting to be the new suckers for PE and distressed funds.

On the list of people whose opinions I value on assessing the real estate market, agents are about at the very bottom, for me. For one, they take 6 or less months of classes to become a certified “REALTOR(TM)”. They have no knowledge of economics, and frankly, when I hear some of them attempt to talk about the economy in any meaningful way, it’s cringe city. It is a field ripe for disruption, they are basically used car salesmen. Would you ever think a used car salesman is going to honestly and accurately tell you about carmageddon that’s going on right now?

I’ll say it again, the housing market is like a cruise ship, it does not turn around very quickly. The slowdown from last year to now is dramatic in most markets. If you look at the rate of decelleration (in some CA markets +20 to -10), it’s striking. Doubly so on the backdrop of record low unemployment, and mortgage rates 100bp lower than this time last year. If the market is stagnating to slightly down now, when unemployment ticks up and we hit a recession, the bottom will drop out. Especially so if those dried up foreign purchasers end up liquidating the assets they have now. Look out below Boston, LA, SF, NYC, etc… if that happens.

Lol. Asking an Agent who wants a commission, If houses are declining is very “Not smart”.

Why would he/she say yes? They want to sell you now.

“Always be Selling”

It’s possible I may be “not smart”….I assumed being candid with him by telling him there was literally nothing on the market we could afford, he wouldn’t see me as a $$$customer$$$ (since I’m not, in his area/price point anyways). It’s more likely that I erroneously assume the best in people (even Agents) and hoped he might have an opinion I haven’t heard beyond mainstream housing market articles. I asked every agent I saw last weekend when we went house hunting what they thought….answers varied to “wait a year before you buy” to “no one knows what’s going to happen!” to “buy now”.

To be sure, I’m not going to let one person’s advice make the decision for me either way. *shrug*

Tough time to be a builder, particularly when every piece of land under the sun has been artificially inflated with endless trickle-down liquidity. I was looking over Meritage Homes’ 2nd quarter earnings release, and it provides a good example of the dilution going on in the home building space. I happen to live in one of their new communities in the DFW area, so I have been watching them water down their product to keep sales volumes up. Here in DFW it’s all about hitting the sub-$400K price point.

They are shifting a large chunk of their product to the LiVE.NOW series, which in Laymans’ terms means watered down. Lower ceilings, fewer bells and whistles, and generally not as appealing as their other product. This is how builders end up screwing their customers who buy at the higher price points. When the going gets tough, they will dilute product to keep sales going, even within the same community. I watched DR Horton do it in Houston.

Recent batch of earnings from builders highlights another significant problem…the party from their big tax cut windfall last year is over. Year over-year earnings comparisons are now more challenging.

I’ve been looking at houses in Collin County for over a year now. Almost 2 years. I have yet to find anything worth the money. Everything in every category is inflated. I did like many homes I saw, but not for the price. Builders are offering huge incentives, but nothing substantial to bring it back to sanity. It’s like getting a $10 off coupon at Neiman Marcus to use it on a $200 T-shirt. It’s still ridiculous. Renting is not cheap either. Same issues, you get nothing for your money.

I also feel bad for the sheep who bought a few years ago at a lower price, and think they are rich because their house is “worth” so much now. Property taxes of their artificially inflated property “value” is killing them. It’s like tax hike but everyone is happy about it because they think they are rich.

This market is insane. That being said QE infinity was a success. The goal was to inflate asset prices. It sure did!

Wow. Texas. What’s the property tax in those counties? 2.5% – 3% PTax paying on your house equity. That’s a great scam.

The only people making money are the transactions people: realtors, brokers, banks, flippers…

cause the average home owner is paying high property tax, high utilities, high insurances, high maintenance… all under the illusion that their home is worth $$$$$ according to Zildo. Until they sell… it all fees.

I listen with amusement to the myriad of real estate radio shows on sundays in the austin/round rock area pushing RE. They have never mentioned the (about 10 year) cycle that housing goes through in this area, ie 1968, 1979, etc. Most of them are only 10-15% drawdowns except for the humdinger that trashed RE about 50% when over 3000 bankers/realtors, etc went to jail in the central US. (Keating 5, etc) late last century. I have some tenants moving out in early Oct and will be putting that house on the market. Love this site but the sarcastic side of me is still amazed that the exact same crimes involved no jail time when the meltdowns occurred in the 200-7/8 time frame on both coasts. Politics anyone???

I live in a community where the median household income is a little over $100,000 per year, house values are around $450,000 to $600,000, and has been one of the fastest growing places in America for the last 10 years. Over 70 percent college educated, top public rated schools in the nation, and property taxes that have went up 50% over the last 8 years, from around $8,000 per year to $12,000 per year per house. I noticed this past year, searching online public tax records, that many of my neighbors (in $500,000 houses) have started using credit cards to pay their property taxes, and are paying them late. It cost an extra 4% to use the credit card, and they are paying them late which adds another 3% per month. “Something” broke in this area over the last 6 months, and I am guessing the loss of state and local tax deductions was the last straw. I suspect that the huge rise in credit card use is somewhat tied to property tax and income tax payment issues for the middle and upper middle class tax payers in higher property tax areas across America. The loss of the “SALT” property tax write-off to punish blue states is backfiring IMHO. The irony is I live in a red state, soon to be blue (pun intended).

Where do you live FedMAdeMeFakeWealthy?

I had no idea you can look up public tax records and have it show that they paid with a credit card.

The OC Register just posted an article about bankruptcies increasing for the first time since 2011 in Southern California.

here’s the byline: “Local filings rose 2% as the nation ran essentially flat. Statewide, bankruptcies rose 1%.”

I follow that author closely, he’s pretty good. But he doesn’t seem concerned about that stat.

A 2% increase in bankruptcies doesn’t worry me either. This data is volatile. I look at the national data every month. There is a bankruptcy season even, when they spike every year. Bankruptcy levels are currently very low. So a 2% increase off low levels is still low. But bankruptcy will spike — meaning they will double or triple off today’s levels – when the credit cycle turns and credit is harder to get, and when the economy goes into a recession.

Bankruptcies are a lagging indicator. In other words, you know when they’re coming.

Nationally, consumer bankruptcies in June were up 8% from June last year, but are still at very low levels. So when you look at the long-term chart, an 8% increase barely registers. All commercial bankruptcies were down a smidgen.

Wolf:

There has been a 20 year trend that affects formal bankruptcy numbers. Banks are using “soft receivership” and extending the lives of the walking dead. Something that was very rare in years gone by.

I believe it has a lot to do with the Central Bank money printing where the banks no longer have to “cash out” of bad loans, since the bank’s own liquidity is less of an issue.

In June this year a Houseboat business here was put in Receivership. Bank owed $ 8 million, unsecured creditors

$5 million (which will be entirely wiped out). Biggest asset? Land which tripled in “value”- that you couldn’t sell for 1/2 price today. The Bank kept the business going for the past 4 years, on hopium. This season when peak deposits were received, the Receiver was appointed, the doors were locked and customers were handed a crying towel.

K