In 2013, I called Goldman Sachs a “snake-oil salesman” for underwriting a $1 billion J.C. Penney stock offering. Investors got wiped out. Now the longer-dated bonds, including a 100-year bond, have collapsed.

J.C. Penney, which just took another step toward what will eventually be a bankruptcy filing and likely liquidation of the company, can be summarized this way:

- 860 stores, down from 1,100 stores in 2011;

- 95,000 employees;

- $4 billion in debt, with some coming due later this year and more coming due over the next few years;

- $12 billion in annual sales down from $17 billion in 2011;

- $5 billion in accumulated net losses since 2011.

Sources have told Reuters that the company has hired restructuring advisors. The implication of hiring restructuring advisors is always this: If the company cannot bully its creditors into an agreement on a debt restructuring that will likely cost them dearly, it will file for bankruptcy. It is this bankruptcy threat hanging over creditors that might motivate them to accept losses via negotiations rather than have a bankruptcy court decide their fate.

But even after a debt restructuring, a zombie like J.C. Penney is likely to fail a year or two later. Retailers are notoriously difficult to restructure. Most of them end up getting liquidated. When a storied brand like J.C. Penney fails, it’s not because of one slip-up, but because of years or even decades of mismanagement and failure to adapt to a changing environment – and thereby killing the brand.

Upon the news today, J.C. Penney’s shares [JCP] plunged 17%, from nearly worthless to worth even less, now at $0.90.

What is surprising is not that this is happening. Department stores have been getting totally crushed by e-commerce. Chains, including the biggies Sears and Kmart, and Bon Ton Stores, that didn’t successfully make the transition, have already been dismembered as part of the brick-and-mortar meltdown.

But I’m in awe of how long zombie companies like J.C. Penney keep getting fed new money by investors believing in Wall Street hype and then getting ripped off.

So here is the J.C. Penney example of how Wall Street entities, in this case Goldman Sachs, have conspired with the company to rip off investors. Back in 2013, when I was still fairly new with my financial website and was still using angry but technically correct terms that I might not use today in my now kinder and gentler manner, I wrote an article – “J.C. Penney And Goldman: Lies, Scams, And Rip-Offs” – that started out this way:

Why would anyone buy this crap? No, not the clothes in J.C. Penney’s stores – which practically no one is buying – but the shares it just sold.

Tsk, tsk, tsk, wash out your mouth with soap, Wolf… And then this:

It hired Goldman Sachs as underwriter – snake-oil salesman would be a more appropriate term – and offered to sell 84 million shares at $9.65 per share and granted Goldman a 30-day option to buy up to 12.6 million more shares, for a total of 96.6 million shares. The deal would raise up to $932 million.

The stock offering was planned in all secrecy. And the day before the announcement of the share sale, and in order to pump up the share price ahead of it, CEO Myron E. Ullman III, fully involved in the share sale the next day, said that he didn’t foresee a situation this year where “we’d need to raise liquidity.”

Lies, lies, lies. That’s what keeps zombies funded.

Yup, in September 2013, J.C. Penney, with the help of Goldman Sachs which got richly paid for this, was able to extract by hook or crook nearly $1 billion from new investors via a share offering at $9.65 a share. This money from new investors bailed out old investors and kept the zombie alive, allowed it to refinance its maturing debts in subsequent years, and allowed it to lose the remainder of the above-mentioned $5 billion.

But investors who bought those shares during the misbegotten stock offering in September 2013 didn’t have to wait all that long before they got cleaned out. Their investment is down 91%.

Now we’re getting closer to the end. Another share sale is out of the question. Refinancing the debt that is coming due is likely also out of the question. Everyone knows: It’s now the creditors’ turn to lose money, either in bankruptcy court or outside.

Moody’s rates J.C. Penney Caa3, just a couple of notches above default (my plain-English cheat-sheet of corporate credit rating by S&P, Moody’s, and Fitch). News of the debt restructuring will likely cause Moody’s to perk up its ears. A debt restructuring, even outside of bankruptcy court, is generally considered an event of default.

J.C. Penney has been having discussions with restructuring specialists – lawyers and investment bankers – for weeks, “some of the sources” told Reuters. One of the sources said that the restructuring discussions are at an early stage. The goal is finding ways to restructure debt and raise new money to bail out old investors. This would keep the zombie alive a little longer. Creditors will be motivated by the threat of a bankruptcy filing hanging over their heads, and they get to choose.

In terms of the bonds that form part of J.C. Penney’s $4 billion in long-term debt, there is a slew of stuff out there, some wild stuff too.

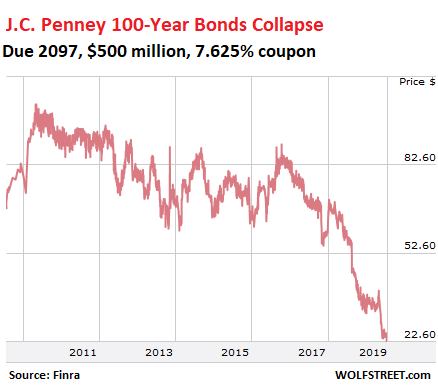

For example on the wild side, in 1997, J.C. Penney was able to sell $500 million of 100-year unsecured bonds, paying a coupon interest of 7.625%. These things have collapsed, now trading at 22.5 cents on the dollar, according to Finra data. This means that investors figure that there is only a small chance of the company ever making it past 2022. The yield is 33% at today’s price, and if you buy at this price, and if the company manages to make interest payments for two or three years, and you get a little recovery in bankruptcy, those bonds might be a great deal. If not, well…

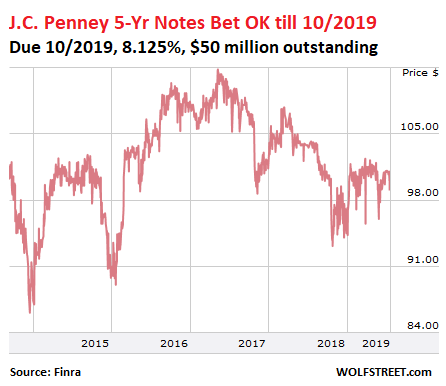

Then the company has five-year notes of $400 million, issued in 2014. Of that, only $50 million are still outstanding, and they’re coming due on October 1, 2019. Investors are certain the company will be able to make it that far and pay off the note with cash it has on hand. It’s currently trading at 99 cents on the dollar:

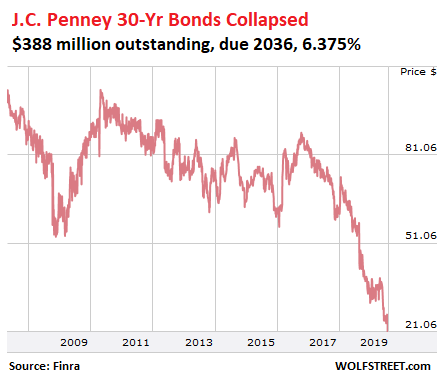

In 2007, J.C. Penney sold $700 million of 30-year unsecured bonds, with a coupon of 6.375%. Of those bonds, $388 million are still outstanding. They have collapsed, and now trade at 21 cents on the dollar, which gives them a yield of 31%. Investors who buy today are calculating to receive two or three more years of interest payments, plus some small recovery in bankruptcy, and then après moi le déluge:

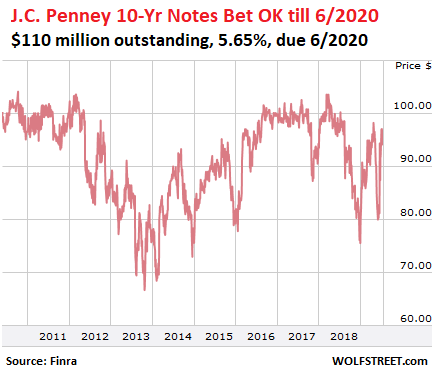

In 2010, the company sold $400 million of unsecured 10-year notes with a coupon of 5.65%. Of that, $110 million are still outstanding, which are due in June next year. Those bonds have gone through some wild gyrations late last year and this year, as investors were weighing the chances that the company would make it through June 2020. They’re currently trading at around 93 cents on the dollar, indicating that investors are pretty sure, but not certain, those bonds will be redeemed at face value on the maturity date, but a month ago, they were less sure, and bonds traded as low as 80 cents on the dollar:

Stock investors have essentially been wiped out, and the remaining $280 million in market value will be mopped up too. Bond investors are giving the company a very limited lifespan — if all goes well, a couple of years maybe. So that might be 2021 or 2022 in a best-case scenario, during which time the company will continue to eat up investor money.

But this was clear in 2013, when I wrote the article, and we’re now six years further into it, and it’s still moving down the same path toward the inevitable, and it has gotten a lot closer to the inevitable, within smelling distance really, and investors have lost a lot of money, and yet they’re are still thinking about feeding the zombie with new money to keep it limping along a little while longer.

Kudos to the private equity firm. These things don’t happen overnight for companies. They happen overnight only for investors. Read... Everything’s Fine Until Suddenly it Isn’t: How a “Leveraged Loan” Blows Up

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I’m no fan of Elizabeth Warren (my dog has more Cherokee blood), but she has a very interesting proposal that essentially eliminates private equity.

Not all (not even most) PE is evil; however, I’d be a lot happier if she could specifically target vulture private equity.

At least this issue may get some discussion.

Yes, but J.C. Penney is the first big retailer in the brick-and-mortar meltdown that was not felled by PE firms or a hedge fund. It did that on its own :-]

they were doing fine until about 5 years ago when they changed their model

from discounting(at cost to supplier) to ONE LOW PRICE brought by new DINGBAT CEO

they lost customers(long long long long time ones) like my wife who quit overnight in search of bargains elsewhere

by time they FIRED and gave nice golden parachute to dimwit ceo

they already LOST COMPANY because customers are FICKLE and won’t return

People love to save money with coupons and sales, even if it costs them more.

I like parking near Penneys at the mall because i always get a parking space near the entrance. Then I cut through the store quickly because there are no customers to enter the rest of the mall. I used to shop there a lot.

Oh crap. I inadvertently disclosed the only thing in which I’m in agreement with Elizabeth Warren. Mea Culpa.

However, I do see a PE firm in JCP’s future…

It is far too late for a PE firm to take and strip JCPenny

Don’t worry, you only admitted she was financially very knowledgeable. And you did get in a “street creds” sound byte, which only matters the TV addled bunch, anyway. Actually blood doesn’t mean much when we share 50% of our DNA with a banana and 98% with a chimp. ;)

PE worries me, solid public stocks are dropping.

Private equity firms

Before World War II, venture capital investments (originally known as “development capital”) were primarily the domain of wealthy individuals and families. One of the first steps toward a professionally managed venture capital industry was the passage of the Small Business Investment Act of 1958. The 1958 Act officially allowed the U.S. Small Business Administration (SBA) to license private “Small Business Investment Companies” (SBICs) to help the financing and management of the small entrepreneurial businesses in the United States.

https://en.wikipedia.org/wiki/History_of_private_equity_and_venture_capital

Government Giveth and Taketh Away

Removing the ability of firms to buy themselves out with loans (i.e., leveraged buyouts) would reduce the perverse incentives.

But then Mitt Romney would never have made any money.

Then he also never would have become president! – – Oh Noes!!

Private equity isn’t inherently evil. But the ability of a company to buy itself with debt is inherently evil.

I dunno about PE not being “evil”, Dale. I have a chart (by year, excluding investment funds and trusts) that shows 4,775 listed stock market funds in 1975, rises slowly to 7,322 in 1996, and drops fast to 3,700 in 2015, where the chart ends. Can’t all be are explained by M&A (which is also bad, in excess). I forgot where it came from, but can type sources at bottom if ya want it. Wish I could source check it better, and see where we are now. Anyway, once private, not only can most all of us not buy in, but any type of regulation on what they do is very difficult. So PE scares me big-time, not for myself, but for the young’uns.

So just how is a lunatic like Warren any better than PE? They are both parasites, you would be trading one for another. The PE only hurts investors but Warren would DESTROY everyone.

Ooooo!!! Scary!!!! LOL

Yeah, well, you know, that’s just, like, your opinion, man.” — The Dude

So FTI Consulting and Lazard are going to do very well as they “advise” these zombies and make them part with whatever money they have left. Good. At least there are some sectors to invest in.

Wolfe,

Although I don’t understand it clearly, it has become apparent that the banks, financial institutions, and the top 10% are awash in cash, so the principal isn’t really all that important. All that is important is the the monthly vig comes in, cash flow is everything. And the cash flow is so profitable that they will accept pretty high risks of losing some or all of the principal. So that is why they keep throwing good money after bad. The credit card companies are another example. All they want is their minimum principal payment and interest. If you die insolvent and they write it off they don’t care. And if you get behind they seldom demand the whole loan be paid off, they agree to new payment schedules. Payment flow is all that matters, not principal.

I have almost no knowledge of financial theory but I can see the trend. Like you I find it startling, but look at the leveraged loan junkies you wrote about earlier this week. Same trend.

I can only think it is a side effect of the enormous amounts of cash that have been made available by the Federal central committee, but I admit I don’t really know.

What is important is what is the mechanism through which QE and low interest reached zombie companies and not main street.

connections? just spitballing here…

Yep!

When I first decided to try to learn investing (someone at BofA told me that me happily making 5% in T-bills was dumb), it baffled me why all Vanguard’s general index funds (e.g. S&P) showed 30-40% “financials”. Figuring no large corporation could operate lacking its own financial dept (I had worked for a lot of small and up to 1000 people businesses prior) I wondered just what in the hell all this massive “cap-ex” did or produced. I am slowly learning, mostly here.

So, Old Engineer, it’s not just the sheeple living paycheck to paycheck? You’re so right. I believe it’s the new American business model you described. I hate to use the term Ponzi here, but it’s close.

You know, I’m waiting for our wonderful government to do something, and then it occurred to me, they were all bought off… or don’t give a damn.

I’m hope at some point laws gets passed that keeps the PE from awarding themselves with special dividends and such. I know JCP isn’t the case here, but still…..

MCH,

Well the federal government has the same paradigm, from the opposite side. For 2020 income is projected to cover around 25% of the budget, hence the trillion dollar deficit for FY 2020. And god knows what the total debt is. But no one Expects to pay off the debt, EVER. All that matters are the payments on the debt. And as the deficit grows, interest rates require the FED central committee to lower interest rates. Capital is becoming irrelevant. And when interest rates reach zero, theoretically, I guess, the system will be based on interest income and earned income from employed capital will be gone.

I really don’t understand this but you only have to extrapolate from the info in Wolfe’s blogs to see the trend.

i would argue that “capital” is becoming more important than ever before. true “capital” puts you closer to the free money spigot. big club an whatnot…

I thought we are on track this year for $1 T deficit. JP was asked the other day if the debt matters and he said we are a long way from any issues due to the debt. The follow up question which was not asked was “define long way”. Likely it comes on fast and no one will expect it.

Wolf, how much longer does SIG have, 3-4 years? Golden Gate Capital took Zale to the woodshed before they pawned in off on SIG a few years ago. Now SIG is sleeping with Leonard Greene.

PS – thoughts on that CLO that just blew up, LG deal. Clover Technologies apparently lost 30% of its value in 48 hours.

Stop, you are depressing me. This blog has too many people who know the score, especially the Wolf. But they out flank us at every turn.

The gyrations that the ruling parasites go through to achieve a rentier economy for themselves is a sight to behold, isn’t it? It seems using standard economic thought to divine the future is no more applicable than throwing a hand full of bones on the ground like the witch doctor in a Tarzan movie. What can one do?

@Endeavor — Adam Smith knew that rentiers are the downfall of a capitalist society. You are right that the government (and, yes, I’m including the Fed in this) seems to be working entirely for the rentiers. It’s a bad trend.

Dale:

It’s because that class successfully changed the narrative.

They’re no longer rentiers; they’re “job creators.”

They’re no longer robber barons; they’re “legendary investors”

My mom said during the ’29 crash bankers shot themselves all over the country, people jumped from Wall St. buildings, etc ,etc.

Only one I know of in FC, one European noble feeding friends to Madoff.

No honor/responsibility/ethics now, the ultra rich are playing hardball.

You are correct. Not just wealthy investors and financial industry types want income but anyone with any money to invest is hungry for income. The Fed and other central banks have all but snuffed out investment income in favor of granting capital gains to wealthy speculators.

Those bonds may seem like a gamble, but are they really? Obviously the early bond investors did alright. If you bought 100 year bonds that paid 7.625% back in 1997 you did pretty good over the ensuing years during which the Fed cut any hope of earning income anywhere else but high yield (even that no longer pays inflation adjusted income).

The rule of 72 still applies and those bond holders made all their money back a long time ago and money collected now is gravy not to mention they could still get back $0.22 of original capital if they sell now. Never mind getting paid for 100 years, in a world where central bankers no longer tolerate investors earning a positive yield, the buyers of these bonds have done, and continue to do, well.

Couldn’t one, if one was someone with connections to both the regulated and the unregulated financial markets as well as FED financing set up some kind of financial Perpetum Mobile?

Where each round of new financing is really the prime mover of derivatives and leveraged side bets on the various bonds?

So they sacrifice perhaps a billion (more than half is not their money) while making, say, 1.3 billion on the side bets. Plus more derivatives can be originated with the new bonds.

Who “The other side” is, is the mystery.

I think that the term you are searching for is “Bondzi”.

Let’s fast forward to 2018-2019. Instead of investors buying bonds of retailers, they are buying stock in IPOs of companies which have NO chance of ever being cash flow positive and already established companies like NFLX, TSLA which have little chance of being cash flow positive

The same thing will happen to these stocks as happened to the bonds of retailers

Well you could have bought INBev IPO raising 10B with a 100B debt. Immediate suicide that it failed.

450 of 500 largest malls are predicted to lose 2 anchor tenants in the next year or so.

Imagine the vast empty reaches of those places–the effects on landlords and second-tier tenants will be crippling.

In the NYC metro area the largest Mall/ Entertainment complex — “The American Dream” will be opening near the Meadowlands Sports complex in NJ, meanwhile Nordstrom is opening a huge new store in Manhattan, and Neiman Marcus opened first store in Manhattan in Hudson Yards

Meanwhile retail sales are white hot in the NYC area. Sales tax collections are up by over 15% year over year.

“

Those retail sales are obviously taking place in the empty storefronts that are everywhere in Manhattan, especially along traditionally high-end avenues.

It reminds me a bit of the old baseball announcer’s quip, when team management would make ludicrously inflated attendance claims for hopeless teams, the announcer would say that most of those paying fans came disguised as empty seats…

Restaurants and bars are still doing well in NYC, and there’s a construction boom that’s transforming the city, but storefront retail is dying.

You do realize that ecommerce also pays sales taxes?

Lakeside Mall, a large mall north of Detroit, has a Macy that is moving to a new upscale outdoor mall a mile away. The Sears and Lord and Taylor have already closed an the last remaining anchor is a J.C. Penny. The curtain will probably come down on this store and the entire mall.

I’ve always thought Detroit needed an upscale outdoor mall.

In my burg, the local mall lost its biggest tenant. And the space was retrofitted and now houses a call center. And another mall in the suburb next to mine, a closed Sears was converted to a mega gym. There is life post retail for these locations, if done right.

Wolf

I take it that the 10 year and 5 year bondS that are trading closer to face w value is somewhat illiquid, is that correct? So investors still believe somehow that JCP will last possibly that long, whereas no one believes the company will survive for 30 or 100 years.

I guess it doesn’t make a lot of sense when you have the whole picture, but I can see how bond holders being attracted by higher yields could jump into those bonds without paying more attention to the fundamental of the company.

Hmmm, in fact, if the 5 and 10 years become liquid, it would be pretty horrible given the current circumstances… right?

MCH,

Toys R Us bondholders were riding high (95 cents on the dollar) when the news came out that it was hiring a restructuring team. And those bonds just plunged from one day to the next. So all kinds of things can happen in situations like these that really mess with bondholders.

The J.C. Penney bonds I listed are unsecured. So there isn’t a lot of recovery at the end of the day if the company goes bankrupt.

So with bonds that mature over the next 12 months, investors are betting on getting paid face value on the maturity date plus interest. They’re betting that the company makes it to that date and pays up. If it does, it really doesn’t matter if the bonds become liquid.

In terms of the bonds that mature years or decades down the road, there is no hope the company will make it to the maturity date. The math for buying that bond today goes like this very roughly:

If you bought the 100-year bond today, you would have paid about $225 for a bond with a face value of $1,000 that pays annual interest of $76.25. So your yield is over 33% if the interest payments are made.

This means that after three years of collecting these coupon payments (3×76.25 = $228), you got your money back.

If the company files bankruptcy after the third year, bondholders will get some claim to the assets. This bond is unsecured, so the recovery will be small, just guessing here, maybe 10% or 20% of face value. So if your recovery is 15%, you get an additional $150 for the bond.

So you paid $225 for the bond, and your received $228 in interest and $150 in recovery for $387 total, or a profit of $162, or 73%, in three years. The math is a gamble. But if the company makes it four more years before defaulting, you more than doubled your money.

Wolf,

Ah, thanks for the math on that. I hadn’t known that’s how it worked. So, there were good rationale initially to buy the bond, as long as you believed that the math will outrun the time to default.

Then the math that is the basis for the current price must also work to some extent based on assumptions on when JCP will go belly up. And if by some miracle, they found some other suckers to keep JCP afloat a bit longer, the guys holding the current bonds might actually make money.

It’s really kind of perverse how all this stuff works. It really is who gets left holding the bag when the music stops. But for sure the guys who work there are not going to make out.

YES!

Thanks very much for WR simplified version of why anybody would get into such bonds in the first place.

Like Sears, it’s been over 20 years since I visited J C Penney. Visiting, not buying. Unlike Sears, I have no idea what Penney’s sells. It might be 30 years since I bought anything at JCP

Does that sound weird? A slice of Americana and I don’t recall what they sell. Maybe it’s my age or just a memory hole that’s been filled with Wal Mart, Lowes and Costco.

Maybe it’s symptomatic of the Brave New World of marketing where every product in the known universe can be delivered by Amazing.con drone or Uber Eats in one hour or less

I guess I’ll just be a consumerist luddite, wandering the malls in search of a store that have something worth buying. Like most Boobus Americani consumers I have enough useless crap to last 2 lifetimes.

I do remember something of the product lines at Sears. Tools, batteries and tires. But those were sold off years ago. I still have a discount coupon for a Craftsman tool chest that I might use this weekend.

Uh, darn, Sears closed all their stores when they went bankrupt. Oh Well . There Harbor Freight and their cheap Chinese Craftsman knockoffs.

It’s probably for the best that J C Penney goes Tango Uniform. Most of America is holed up in their pod homes, ordering everything from their Iphone apps while immersed in Netflix, Hulu, Roku etc, getting comfortably numb and entertained to death

AGXIIK:

Zounds! I thought I was alone in the world!

Corporate and Household Debt about DOUBLED from right before the Financial Crisis till today.

So the Fed’s balance sheet topped at about 4.5 trillion and is now about 3.8 trillion, with about 1.4 trillion of that is still stuck as excess reserves. So about 2.3 trillion of that leaked out somewhere. Multiplied by fractional reserve banking then bingo! You got the cheapest and most debt ever. Too bad they all can’t make money. It’s easier to borrow.

My little town has a sears and a J.C. Penney’s. So I guess ciao to those two soon . That leaves just Costco and Ross to buy clothes or a 1 hour drive to the nearest mall. I will just keeping wearing my t’s and Levi’s Clothes now a days (Nordstrom, Macy’s ) are cheap made, poor materials, and most down right ugly or laughably ridiculous. Sure I will pay 300.00 for jeans that have artful rips and tears in them. Eye roll.

Although Paulo ,when in Victoria last spring I saw some pretty decent stuff and almost 30% less in Canada using the dollar. Worth the BlackBall trip over

Bet,

“…to buy clothes or a 1 hour drive to the nearest mall.”

Start buying your clothes and shoes online. RD Blakeslee, a long-time commenter here, lives out in the country, and he says he gets almost all his stuff online. He, according to his own description of himself, is not exactly a young whippersnapper anymore. So you don’t have to be a millennial to buy your clothes online. Even I buy them online :-]

If there is a Goodwill near you, try that. I bought a $300 three-piece suit for $12 bucks. Fits great and looks great. Of course, many don’t like buying used at a place like Goodwill, but for me that place is fine.

Yes, but I live in San Francisco, and nowadays, as head-honcho of my media mogul empire, I wear a suit only to weddings and funerals. So the one that is left over from my East Coast days — a so-outdated Brooks Brothers that it will be fashionable again in 10 years — probably represents a life-time supply of suits for me :-]

Actually, Goodwill has a store a wealthy area of the city I live in. Dad likes shopping there.

For those not familiar Goodwill in eugene and probably other places has an electronics department. Used laptops, monitors, full size computers, games, speakers, that all are checked out, reconditioned and guaranteed. Laptops with win 10 and dual core probably only 2 – 3 years old run 135 – 250. Fast gaming units with ndiva chips 250 +. Amazing values. Staffed by geeks that know there stuff. Rest of store we’ll stocked, organized and great values, Macy’s it’s not, but amazing. In palm desert the American cancer society or Eisenhower resale stores are so upscale resale you are likely to find any number of very high level clothing names. Final example are China sets typical 120 piece 100 – 150 for perfect that cost 1000 + new, course millenials don’t want them. So resale really varies widely.

Sure “drive to the mall” lol you are putting mileage on the car (you should always drive less than 1,000 per month or 12,000 per year — rent a car for longer trips ) , traffic, and not to mention that are just rude and move so slooowllly these days especially those 5’1″ etc.. 180LB pear shaped women….

It is different for men, Wolf. For women, the sizing online is not consistent and the quality is ridiculous. Men’s jeans don’t have rayon yet. Women’s jeans do.

Yes, I see that. I never have to send anything back. My wife, who buys nearly everything online as well, sends lots of stuff back. She will actually order two or three things, knowing that she’ll keep only one. Some retailers are starting to crack down on this practice, so she has be a little more prudent about it, she says.

Lol another clueless millenial who pays $300 for jeans, do you also spend $10,000 on sleeve tattoos and get secret hard on checking out other guys tattoos?

By the way Costco & Target are showing stellar results and have both said that they have never seem such a sustained economic boom like now..

By the way anyone with half a brain would know that clothes are the dumbest thing to buy on revolving credit. The depreciation curve for clothing is greater than driving a new car off the lot. But of course millenials (despite what the media says) has this pathological obsession with buying stuff (you are still amassing credit card debt buying online at 28% APR)

If your $300 jeans comment was directed at Bet, think you missed the sarcasm.

NickL, congratulations. You win the misogynist clueless bingo today.

Yeah, Bet…it makes huge good sense for US citizens to wander up north and buy stuff, spend the weekend, the whole shebang. But what I always wonder is why Canucks are still buying anything beyond fuel south of 49? Even with cheaper dairy, poultry, gas, eggs….it still doesn’t make much sense if your time is worth anything. (Those border delays!!!) And basic food, plus restaurant meals seems to be the same regardless of currency levels.

Our discounted dollar is one reason why the BC economy is doing so well these days. Ottawa just tweeks the interest rates to keep it around $.75.

When I was a little kid my mom shopped at Penny’s. This demise is like so many changes we see. I suppose one day WalMart will decline and be replaced by something else that comes along, at least in scale.

I don’t mind seeing stores and chains miscalculate and go under. What really bugs me is when financialization and manipulation drives them down. Retail and all small business is a tough challenge, anyway. When I find a good business I like dealing with I stay loyal to them even if it costs more sometimes.

I was in Canadia recently. There are no bargains to be had. Gas is about $5.50 CAD. A Big Mac meal at McDs is $10 CAD. Sales tax is 12%. Essentially whatever discount I got on the CAD vs USD exchange rate was eaten up by the higher price on everything.

My wife and I retired in 2013, after 10 years in JCP’s supply chain. The company’s demise is a chain of ignorance and neglect. Its policy of mostly promoting from within made management top heavy with people who had no idea of what was going on in the business. New management with college degrees in supply chain management give up after a few months and look for another job. Their supply chain is state-of-the-art 1982, and so is the software that runs it. It is run by a lot of hammerheads who worked their way up from the loading docks.

The inefficiency means that it costs the company more money to bring a product from China, Cambodia, Vietnam, or Bangladesh than other retailers. If this wasn’t a big enough deterrent to profits, add in the 4 billion of debt.

No matter what kind of product mix they decide on for the stores, it sells at a net loss.

JC Penney wasn’t brought down by private equity. It really hurt itself when they went from discounting items for sale to the one low policy which long-time shoppers hated so much they quit shopping there. The CEO who took over after the other CEO plummeted the company into the ground has tried to make things work, but it was probably way too late to turn things around. They tried selling appliances and opening up mini-Sephora kiosks, but those didn’t work, and they gave up on appliances earlier this year. It’s only a matter of time before they declare bankruptcy and liquidate all of the stores.

I work at a health insurance claims processing company which is located across the street from what was the major mall in my hometown (it still technically is the major mall in my area, but not for long), and since the beginning of this year the following stores have gone out of business or are about to close:

Sears

Gymboree

Crazy 8

Payless Shoe Source

Bare Minerals

Things Remembered

Charlotte Russe

Dress Barn

Charming Charlie

Add those to the stores which closed last year (Bergners/Bon-Ton, Teavana, Vanity, Vitamin World), and it looks like my neighborhood mall is about to become a ghost mall very soon.

the reason is because of the stores themselves nothing to do with consumer spending.

Vitamin Shoppe

Target

Costco

TjMaxx

Whole Foods

Ulta Beauty

These are stores that are seeing booming top line revenue growth and who are opening stores everywhere….

NickL,

” booming top line revenue growth” —

OK, I just fact-checked the top 2 lines of that list. You need to start looking at the actual numbers before making claims of “booming top line revenue growth”:

Vitamin Shoppe revenue in its fiscal 2014 was $1.21 billion; and in its fiscal 2018 (last year), it was $1.11 billion. Revenues FELL 8% over those four years!

Target revenue in its fiscal 2015 was $72.6 billion; four years later in its fiscal 2019, revenue was $75.4 billion. That’s less than 1% growth per year. That’s less than the rate of inflation. And ALL of that growth plus a whole bunch more in revenues came from its online operations, and its brick-and-mortar revenues actually fell.

Target even conceals the same store sales losses to online by bundling online sales to local stores and quoting that figure as YOY same store sales.

Target is also in vigorous buyback mode to boost YOY per share earnings.

Fraudulent reporting wherever they can get away with it. It is stupefying.

Not Me

Target’s financial reporting not being EXACTLY the way some individual (perhaps not even a shareholder) prefers it to be in no way makes it fraudulent. Not completely transparent certainly, but definitely not fraudulent.

If I accurately understand your description of how Target reports YOY sales for stores (B&M + on-line), there is business value in knowing which legacy geographic locations (AKA stores) provide a suitable nexus for future re-configured sales/distribution at given locations.

surely the new season of stranger things will help resuscitate these moribund emporia!

“was still using angry but technically correct terms that I might not use today in my now kinder and gentler manner,”

If a kinder and gentler manner implies not calling a crap a crap, then I for one would prefer (at least some of the time) an angry but technically correct Wolf!

Speaking of crap, I see GS more as University.

Arguably the best for obtaining a PhD in white collar crime.

Good for Private, Gov’t, Stay with the University and teach, or become a self employed entrepreneur. Their graduates are everywhere.

They’re coming for you Barbara .

Apart from the mismanagement, there is nothing wrong with a little wealth redistribution the capitalistic way imho; the 95,000 employees probably didnt feel too sorry either…

13’artical nailed it,

there those smarty’s are!

I’m in my sixties so I remember when shopping in Union Square in San Francisco was a pleasant experience. The well heeled headed for I. Magnins and I headed for Macy’s. There were benches in the square you could sit on and watch the scene. Then the derelicts showed up. I headed out to the Stonestown Mall for shopping expeditions. Now the malls are full of rough looking people.

I wonder if this coarsening of American life is not related to the income divide. If you don’t have credit you can”t shop on line so the ‘cash’ customers, of necessity have to head to the mall so the ‘mall’ has come to more resemble the seedy stores that lined Market Street more than the credit card carrying customers who went to department stores.

I try really hard not to go shopping alone, it doesn’t feel safe or pleasant anymore, hasn’t for years. It’s not just the rough looking people, it’s the mall workers as well. The kiosk sales people are the worst, they accost you through the entire mall, adding stress to the shopping experience. If mall managers knew what they were doing, it wouldn’t be this bad.

unit472

About 80% of adults have credit or charge cards; not sure have to factor in the 18-21 crowd (Credit CARD Act of 2009 bans approvals for anyone under 21 years old unless they have an adult co-signer or can prove they have sufficient income to pay the bills). Let’s go with anyone who wants one more-or-less has one.

I’m with Petunia on mall visits: a certain segment of society seems to go there for “entertainment”; this 72-year-old doesn’t want to go there to become the entertainment.

Young people get a debit card the minute they sign up for college, all student loans and grants are electronic payments, no checks. The credit card offers are sent to these kids like water over Niagara Falls, just sign here.

On a holiday to the USA last September my wife and I ended up in JC Penny New York store.

My wife decided on a piece of costume jewellery,after 10 minutes waiting in a queue to pay for it we put put it back and walked round to Macy’s.

Totally different experience,plenty of staff,plenty of stock and a real vibe happening,DJ going for it.

Didn’t bother going anywhere else for shoes,clothing,and baby wear after that.

People have been buying apparel online. It is a paradigm shift.

I always hated going to the mall. Bad enough being trampled by a herd of humanity suffering “mall fever”. Usual symptom is being run down by one pushing a stroller who just doesn’t realize what they’ve done They tended to have the thousand yard stare. I guess that was replaced by the smart phone distraction…not sure if there is a term for it yet.

My jeans? They are $15 on sale Wranglers, they last a very long time before wearing holes in the knees. Anyone remember the iron on patches you used to be able to get to extend the life of your jeans?

In my rural area we have Walmart, Tractor Supply, and Family Farm & Home. If I had to buy a suit now, I’m not sure where I’d go. I think my last suit, BBC (before business casual), was from JCP. I have a blue jacket, some gray slacks, a few white shirts and some ties for whatever event requires them, weddings and hopefully rare funerals.

Guess I’m just an old guy since I don’t understand investing like this, or in stuff like TSLA or any of the other cash burners. I’ve always asked “whose cash are they burning”?

Credit,

Here’s a fashion tip for older gents.. At least it works in my redneck rural enclave. I had to attend two memorials this past year. I wore a new black tee with some newer jeans. It didn’t look any worse than guys 10 years older than me wearing 40 year old suit coats that seemed to bulge. I have going out for dinner ‘good jeans’, and over time they recycle down into everyday work jeans. No rips or tears. However, my wife is starting to develop wardrobe impatience and has started making comments of late.

My buddy just remarried, yesterday. I thanked him for not inviting us (and I meant it). His reply, “No worries, I didn’t even invite my girls (daughters). If I invite them , I have to invite those, and where will it all end”?

Paulo,

You just need to get a pair of black jeans to go with your black tees. Black on black is a cool look for any occasion.

Get Lee Double Black jeans. They fit, and it takes a long time for them to fade.

“I guess that was replaced by the smart phone distraction…not sure if there is a term for it yet.”

Phone Zombies is what I call them and I hate their clueless, imbecilic shuffling with a white hot passion.

Here in the Midwest my go to jeans place is Menard. Paid 14.95 for their Old Mill brand and they wear as well as any other brand short of working trade grade. Also have Fleece lined for the cold months for about $20.

I own a small on-line retailer with low single digit growth, 20 years old. $16 stock price, $1.08 div, $5.00 cash on books, zero debt. It is priced at only 9 PE and 1.2 x sales because market currently values growth in sales no matter how much debt and how little profit.

@old engineer

I really think you’re into something.

Looks like you hit the nail on its head.

Many details seem to be minutiae.

But I believe you struck gold in your thread.

As money gets recycled in whatever format, fees, margin and spread together with cash flow is really what matters. The music keeps on playing until it stops.

I’d need more like 20% to buy a JC Penny bond.

I think that I finally figured out where all the money to inject financial adrenaline into zombie retailers is coming from.

The shopping center REITs and shopping center owners are terrified of losing their anchors. Macy’s locally held a major regional shopping center hostage to getting nearly free rent when it threatened close. The other two anchors in the center are (drum roll) Sears and Penny’s. Likely the banks and center owners are so terrified of losing all their anchors that they must keep the zombies moving at any cost.

Of course across the freeway are a moribund 30 year old shopping center and a freshly finished strip mall mall, all two miles away from a Montgomery Wards converted to Kohl’s shopping center.

Luckily, locally the cost of housing is so high, that the likelihood is that it will be plowed under to make way for condos. If they can find anyone to buy them, since the Chinese are rolling up and blowing away.

We are the road runner off the cliff as shopping centers RE. Still waiting for gravity to wake up.

The Chinese are being driven away by deliberate government policies. And of course, this is instead presented as some sort of natural phenomena…. they just blew away. In the modern propaganda sphere, the negative results of deliberate policies are always represented as stuff that just happens, usually as if it is some sort of natural phenomena. The economy just naturally crashed after the bankers rigged it for their benefit and stole trillions. But never mind that, the crash is just a natural phenomena.

Here in Oakville Ontario (supposed richest town in Canada) local mall just as major reno, Sears closed being replaced by PetSmart, GoodLife fitness and a Baby store. Pulsiteri’s a high foodie shop closed up after a couple years.

The Bay renovated but you can still fire a canon through and not hit anyone.

Lots of empty smaller stores.

The owners The Bay and Riocan REIT have been shopping it for years and just keep pouring money into it hoping and praying it will turn around (it won’t).

Landlords need to wake up,THE RENT, TAXES,COMMON AREA EXPENSES ARE WAYYYY TOO HIGH.

Going to be big hits taken.

Who on earth would buy a 100-year, unsecured bond? On its own, it seems silly. As the great philosopher Morrison once said, “the future’s uncertain and the end is always near.” It seems likely that given the way the world changes that someone who bought such a bond at the start of the 20th century would likely end up praying that a Bradley’s Fine Horse-drawn Buggies would still be in operation and paying its debts at the end of the century. Or that Hick’s Horseshoes would still be a going concern?

Who would buy a 100-year bond? As the wolfman indicates, the JCP ’97 bond is trading at about 22 cents on the dollar. I’m buying it because in bankruptcy all bonds of the same seniority are merged based on face value regardless of maturity or interest rate. So if they file soon, near-term bondholders are big losers while long-bond holders at the same position in the stack may do well. The issue isn’t that anybody expects JCP to be paying coupons for another 80 years but that recovery in bankruptcy (i.e. equity in NewCo) will exceed current bond prices.

In a democracy people get the leaders they deserve

In financial mkts and ponzi schemes people get what they deserve.