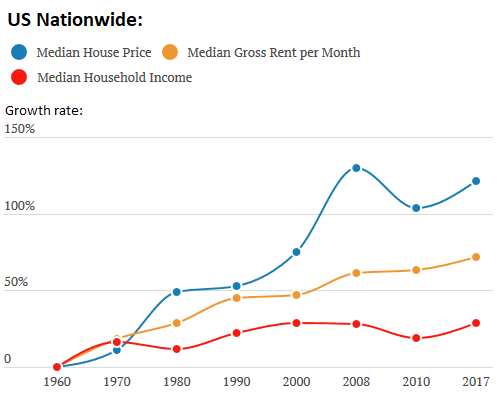

How out-of-whack is the discrepancy in growth between incomes, rents, and house prices?

The “San Francisco Housing Crisis,” as it’s called on a daily basis, is an extreme. But housing costs in major urban areas in the US have been eating up more and more of household incomes, as house prices and rents have soared and as incomes have crept up painfully slowly. In many cities, not just San Francisco, this condition is now called a “housing crisis” where families with median incomes can no longer afford to rent or buy adequate housing, or where too much of their income is spent on housing, with not enough left over for other things. They have no savings, they barely make it to the next paycheck, and they can’t help the local economy because housing saps their spending power.

Just how out-of-whack this discrepancy between income versus rents and house prices has become over the years is depicted in a new study with long-term charts, released by the research department of Clever Real Estate. Based on Census data going back to 1960 for median household incomes, median gross rents per month, and median house prices, all adjusted for inflation, it shows that nationally, incomes since 1960 have risen just 29%, while rents have risen 72%, and house prices have soared 121%:

But the national values above reflect everything thrown into one bucket, from the more affordable areas to the biggest housing bubbles. So we will separate them out by region and metro – and there are stunning differences.

All values in the charts are indexed to 1960. The charts only include data for the depicted years: 1960, 1970, 1980, 1990, 2000, 2008, 2010, and 2017. The data for the years in between those years are not included. For example, if in one metro, the housing bust bottomed out in 2012, the low point falls between the data points of 2010 and 2017 and is not depicted. But you get the idea.

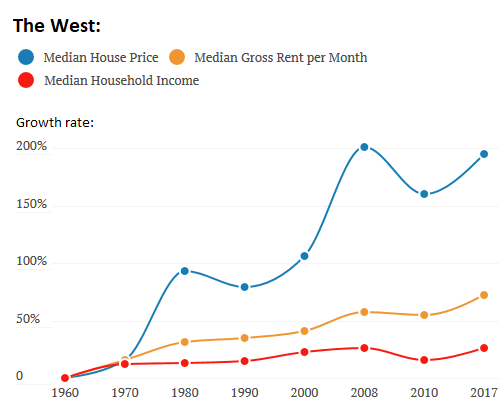

The West: house prices & rents v. household incomes.

In the West — a vast diverse region that spans Alaska, Arizona, California, Colorado, Hawaii, Montana, New Mexico, Oregon, Utah, Washington, and Wyoming — the median house price, adjusted for inflation, soared 195% since 1960. And rents, adjusted for inflation rose 72%. But household incomes adjusted for inflation ticked up only 26%.

The growth rate (vertical axis) is on a different scale in the charts. For example at the chart above it tops out at 150% growth from 1960; in the chart below, it tops out at 200% growth from 1960; in one chart further down, it tops out at 550% (yup, San Francisco):

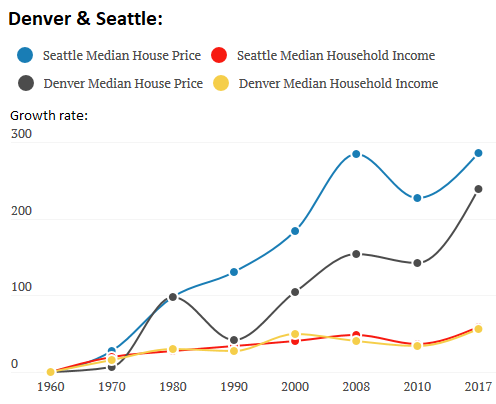

To dissect the changes in house prices and incomes in the West, the study by Clever Real Estate separates out different metro areas. For example, in Seattle and Denver, household incomes, adjusted for inflation, rose in near-lockstep 56% since 1960, while house prices in Denver soared 239%, and in Seattle 286%:

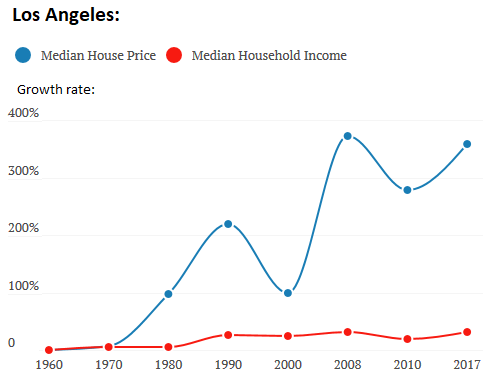

In Los Angeles, the median house price increased 358% since 1960, adjusted for inflation, while the median household income rose only 32%. In other words, house prices increased 11 times faster than household incomes:

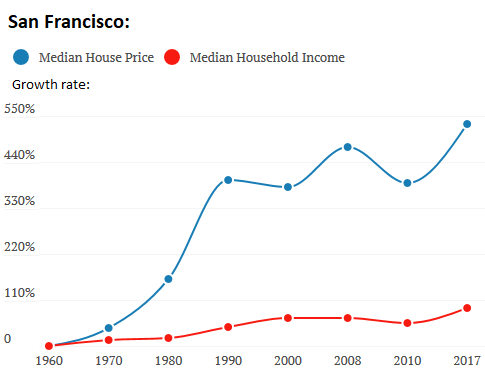

San Francisco is tops, when it comes to house price increases: Since 1960, house prices surged 531% adjusted for inflation. Over the same period, household incomes also rose sharply, but not nearly enough: 91%. In San Francisco – where about 1% of the population is homeless and many others are struggling – the phrase “housing crisis” is in daily use for a reason: House prices increased about six times faster than incomes:

The Northeast: house prices & rents v. household incomes.

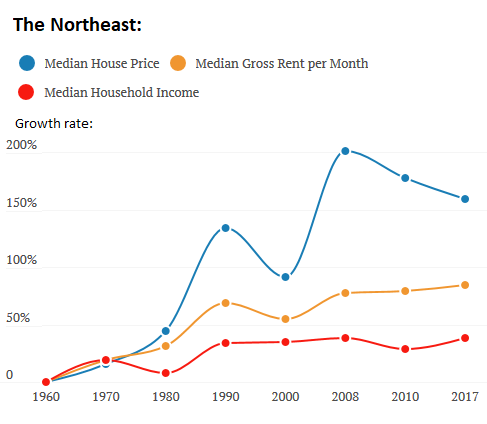

In the Northeast – Connecticut, Maine, Massachusetts, New Hampshire, New Jersey, New York, Pennsylvania, Rhode Island, and Vermont – house prices, when adjusted for inflation, have declined from the peak of the prior housing bubble, and are now up “only” 159% from 1960. They had been up 201% in 2008. Rents rose 84% since 1960 – and they have not declined since the last housing bubble, and have continued to outrun inflation. But household incomes rose only 38% since 1960. They did decline between 2008 and 2010 and are now back where they were in 2008:

The downward slope of the blue line above — a declining median house price since the peak of the housing bubble when adjusted for inflation — is unlike the chart for the West and nationwide. Clever Real Estate’s study explains it this way (all data adjusted for inflation):

However, a surprising trend emerged in our data between 2000 and 2017. We observed an increase of 110% in home prices between 2000 and 2008 (i.e., before the financial crisis), and a decrease of 24% between 2008 and 2010 (i.e., after the financial crisis), which real estate analysts expected. However, unusually, home prices dropped by a further 18% between 2010 and 2017, while household income increased by 9% between these years.

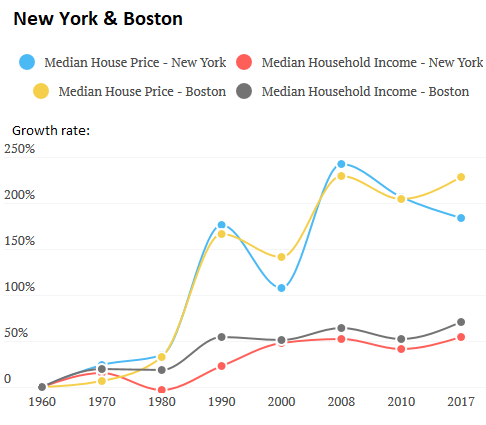

This trend in the Northeast overall is not the case in Boston. Adjusted for inflation, house prices in Boston, after falling 25% during the housing bust, are back where they were during the peak of the prior housing bubble, and are up 228% from 1960. But house prices in the New York metro, adjusted for inflation, while up 184% from 1960, have declined in real terms since the peak of the prior housing bubble.

Since 1960, median household incomes have risen only 71% in Boston and 54% in New York, adjusted for inflation, far outstripped by the surge in house prices:

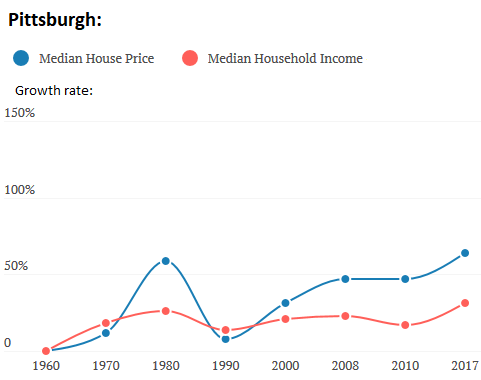

In Pittsburgh, house prices have by far surpassed the peak of the prior housing bubble, which wasn’t much of a bubble, and are now up 64% since 1960, adjusted for inflation. The median household income rose 31% over the same period, a relationship to house prices that seems almost sane compared to the utter madness in the West:

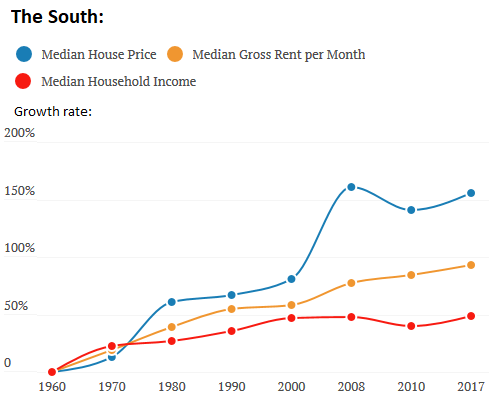

The South: house prices & rents v. household incomes.

In the South – Alabama, Arkansas, Delaware, D.C., Florida, Georgia, Kentucky, Louisiana, Maryland, Mississippi, North Carolina, Oklahoma, South Carolina, Tennessee, Texas, Virginia, and West Virginia – house prices rose 156% since 1960, and rents 93%, while household incomes rose only 49%, all adjusted for inflation.

This region includes some of the poorest and lowest-cost and lowest-income states in the US, but it also includes high-cost and high-income states. In some cities in the region, real estate has gone through some mind-boggling booms and busts. Washington D.C., Miami, and Tampa are examples — and they’re included in my glory list of The Most Splendid Housing Bubble in America. So this here is everything in the big and diverse South thrown into one chart:

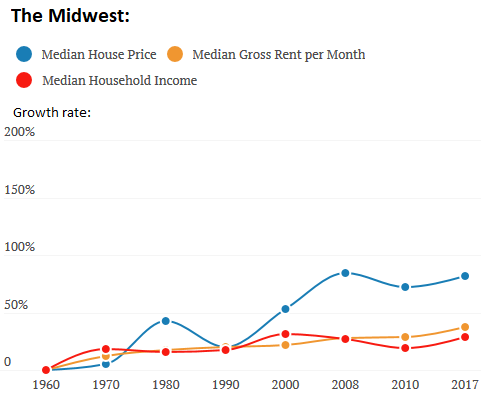

The Midwest: house prices & rents v. household incomes.

In the Midwest – Illinois, Indiana, Iowa, Kansas, Michigan, Minnesota, Missouri, Nebraska, North Dakota, Ohio, South Dakota, and Wisconsin – house prices increased a practically reasonable 82% since 1960 adjusted for inflation, while rents rose 37% and incomes 29%:

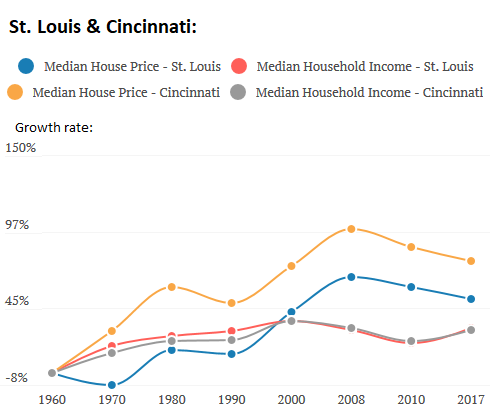

As sample cities for the Midwest, the Clever Real Estate study selected St. Louis and Cincinnati. In both cities, adjusted for inflation, house prices are still down from the peak of the prior housing bubble. And incomes, also adjusted for inflation, are about flat with the mid-1990s:

In some of the hottest most overpriced rental markets, changes are afoot. Read… Apartment Rents Fall in Seattle, Southern California, New York, Oakland, San Jose, Chicago, Honolulu

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Nice charts. Many factors are at play as usual.

– Population growth vs. “attractive location”. Attractive location usually includes factors such as weather, recreation, business activity. Port cities have lots of these things naturally and as a matter of history, thus the bi-coastal thing. Denver has reasonable weather, nice geography, etc.

– Structural economic problem: housing, and basically all other durable goods, have been in decline per capita for decades. This is a structural chicken and egg thing (as often in macroeconomics): housing is a huge (hugest?) part of the economy, and “housing” employment (construction, mortgages, materials, etc.), is huge.

If the demand for housing could go up and commensurate employment in these areas, a new trend could be achieved.

Not so far though.

I will toss some more reasons into the mix.

– People moving to urban areas from rural areas. Land is at a premium in cities and costs higher.

– 30 year mortgages and creation of Freddie Mac. Monthly payments largely determine how much is spent on a house.

– Tax breaks on mortgage interest and other housing costs.

– Tax laws that encouraged ownership of investment property (tax deduction for ‘depreciation’ and house costs). Rather than giving breaks only to owner-occupied houses.

Fannie and Freddie are definitely big factors aka the GSEs (government-sponsored enterprises). Banks would not have been willing to originate toxic mortgages in the last cycle without a place to move them off their balance sheets. Thanks fan and fred. And thanks to the taxpayers for bailing them out.

I never lived it but based on those charts I think I hate 1970.

Lots of people hate 1971, infamous for Nixon severing the last monetary tie to gold.

1970 – Mortgage securitization begins with GNMA guaranteeing mortgage passthrough payments. By 2000, the MBS market was $6T.

This is what happens when your country has a fraudulent, debt-based monetary system.

Over the course of several decades, your currency loses purchasing power and everyone (except the very rich) slowly drowns in a sea of inflation that eventually becomes hyperinflation.

The death of the U.S. dollar — and all other currencies in the Western world — began in 1971 when Nixon took the USD off the gold standard.

The true death of the American dollar was in 1913 with the passing of the Federal Reserve Act. 1971 was just putting the lid on the coffin.

Yep

I was a kid in the 70s.

Lots of uncertainty back then.

I assume I carry it with me now, relative to my kids / millennials who have for the most part just experienced the greAt moderation.

I am both happy to have been through it, so as to be ready for it again, But at the same time, it’s like I got stamped with one scenario in my brain, that excessively effects how I see the future playing out. But that’s biology.

I call ’em the Starving 70s.

Hunger, having only one “good” T-shirt. etc. I’m glad I survived, one of my sisters almost didn’t.

When the economy crashed, I thought, Well, here we go again, but I know more now about foraging, and I’m bigger and stronger now.

@ Alex,

Yeah, my Dad was a pretty successful Landscape architect / Civil Engineer (everything outside the building he used to say),

and for me your Starving 70s were defined by going from a beautiful lime green Dodge Challenger in the early 70s, (which was totaled in an accident), to a baby blue VW Bug that we put ~ 200K miles on — driven to the point where the floor boards rotted out and the battery (which sits under the rear passenger seat) was bouncing on the road. My friend lifted the seat and held the battery up by cables as my Dad drove us home. So the floorboard was replaced by plywood.

Then came Reagan and the 80s, things got better, and my Dad bought a used, gold Porsche 924.

All planned. See the Powell Memorandum. It planted the seed ideas for all of this.

This is very interesting data! Thank you!

Looking a the Los Angeles house prices, it looks like the drop in house prices from 1990-2000 was greater than the 2008 bust.

What caused this? Aerospace downsizing? Urban blight and people moving to the suburbs?

I owned a house in S. CA during this time and remember house prices being very flat in the 1990’s. It could be that high inflation is dominating the chart.

Regarding growth since 1970, any correlation with the rise of two income households? Also any correlation with loss of gold standard?

House price increases leading to Cash-out refi’s providing a source of funds used to bid up prices even more.

“We’ve never had a decline in house prices on a nationwide basis” – Bernanke in 2005

Oops.

I would have thought the rise in 2 earner households would have contributed more to the median household income.

Setarcos-only to the point that the expansion in the labor force, and its inherent devaluation of labor in general, offsets the median figure.

A better day to all.

Tie it to military spending. The west coast was the jumping off point for Vietnam. The 80s were the Reagan military buildup, the dip in the 90s when the war shifted back to the ME, and post 2000 is SV buildout. Like to see San Diego factored out separately, they might be the next SF.

This is some interesting context. But I didn’t know what “SV buildout” meant and this website showed too many options https://www.allacronyms.com/_Military/SV

so were you referring to the greater emphasis in planes and other equipment on electronics?

Phoenix-

My guess is he means some military plus whatever systems are needed for you to post here, and do most every other thing you do, likely the largest part. The milkman at the door is long gone.

Not a man of many words.

Yes, high inflation hides of lot of things.

Seen it,

I bought in 1991 and was upside down for 9 years, only bubble 2.0 (that was the 2nd time i’d seen this pattern, we are in bubble 3.0 IMHO) saved me. Back then the government wasn’t in the business of making banks whole again so foreclosures were everywhere and yes I should have bought as many as I could. BUT when the last bust happened I figured the same patter would play out and holy cow was I wrong. RE is now an asset class that has it’s own plunge protection team to ensure that those prices never reflect reality.

The Oil Crisis and Middle-East politics of the 70s cost the U.S. dearly, ans ushered a dramatic shift to our standard of living that has been masked with increasing debt. The Petrodollar on Wikipedia is a good starting point.

Go South Young Man!

Santiago Chile- -the New York of South America— without the garbage in the streets.

“Amazing Two Bedroom / Two Bathroom apartment in Bellas Artes in one of the nicest buildings in the area. The top floor in the building has an amazing pool, gym and a panoramic 360 view of the city. ”

$832USD per month.”

High end apartment rents are typically from .50 cents to a dollar a square foot.

MAGA!

Same thing in Buenos Aires!

Cienfuegos

The difference between Buenos Aires and Santiago is that Argentina has an unstable economy with runaway inflation, while Chile has a relatively stable economy diversified away from it’s historical copper dependency.

On a related side note, the Russian national debt is among the lowest in the world, at 19.48% of GDP, Chile owes only 24.62% , while the USA owes 109.45% of its GDP to foreign nations and investors!!

Does say something about the way the wind will blow as the USA stands on the edge of losing it’s power to impose the Dollar, unearned and printed from thin air, as the world currency. A privilege historically imposed by sailing it’s aircraft carriers toward any nation that dares object and ramming a bayonet up the ass of anyone who tries to trade oil for gold like it did to Gadaffi.

with or without gastos comunes?

Interesting, the bigger the spread between house prices and income, the more the mortgage market grew. If the data is accurate, they had to know the housing market was heading for disaster.

Isn’t most of the recent price movements the result of “foreign buyers?” It’s a different world out there.

From what I have read, a lot of price support came from sweet heart deals the big banks made with private equity who turned many millions of foreclosed homes into rentals.

This in essence removed houses from the available inventory of homes for sale and put a solid floor under the housing market. Once these large investor groups owned enough of the homes they could also start jacking up the rents.

Just another down side to bailing out the banks and the investors. Big upside for them. Big down side for the rest of us.

Unfortunately, I believe you are correct. Some people even believe it was planned that way.

Remember, “they” were, “……doing God’s work!”

Spot On, economicminor. Capitalism, the ‘Das Kapital’ principles were applied ritually until the banks and private equity raked in their deserved monies. And Supported by government policies with the blessings of the then White House President (Clinton)

Neither of these institutions cared enough about the well being of their own customer base (voters)

Yep, agree with that.

Per sierra7 comment:

Look up Romans 13:4 and then “Seneca on religion”, who was likely alive when it was written, c AD 50.

Some of the most discouraging economic data I’ve seen in a long time.

I think if you were to plot inflation in utilities, home insurance, and real estate taxes the trends would be similar.

If this keeps up U.S. cities will start to look like Rio de Janeiro or Sao Paulo with significant portions of the populations living in tin shacks in “favelas” around the cities.

I don’t have a clue how to remedy this disparity but if something isn’t done pro-actively the set of possible reactive solutions is scary.

When they print and you work, you lose. Period.

They say “If we don’t print, you have no work to do, your vote.”

I reject your reality and insert my own … print the money and give it to me not them

It’s already happening in Seattle. Today, I took a freeway I haven’t in a while and saw a sprawling encampment where even a few years ago none had existed at all. Maybe the next phase will be semi-permanent fixtures. It’s a bit surreal to see technology and manufacturing progress as it has, and yet we don’t even house our population or guaranty a basic level of healthcare.

As for income, it’s also worth noting that women entered the workforce during the time period in question, so median income fell even more relative to housing prices on a per-worker basis than it at first appears.

Btw

The need for two incomes / disparagement of motherhood/ stay-at-home moms is responsible for a boatload of negative societal outcomes.

Courtesy of the political left… viva la revoluccion!

“You’ve come a long way baby!”

How fitting is it that such feminist progress was symbolized in their very own adverts, with the smoking of cigarettes?

Yeah, Ragnar, I totally agree. Both sides though are complicit. Neoliberal Chicago School Economist play lip service to income inequality (like Yellen) but their doctrine requires the de-platforming of labor along with increasing levels of poverty & financialization amongst the masses in order to achieve the Holy Grail of cheap labor. You can toss in the whole immigration issue as well, from the lowliest landscaper/painters to the scam of H1b’s. This Nation could well resemble an Argentina, or other Latin American Country before this is all done. Thos. Jefferson pretty well forewarned us that if we let a Central Bank control the issuance of currency, first by inflation & thence by deflation, that they would rob our descendants of everything.

Most of the federal budget is spent on social programs, but that money circulates within [our] economy. The next largest outlays are foreign aid programs that include diplomatic, military, etc., protecting our “friends.” This is our prosperity going down the drain, and our venal congress insists that this off-shore spending will increase as needed.

NED, this is classic late empire behavior: currency debasement & perpetual war. You and I can’t do anything about it, except maybe try and profit from the coming devaluation. I think a Guy named Harry Browne had some ideas about that.

Easy,

Amusing that you consider the trillion $ per year that the USA spends on endless wars, 800 overseas military bases to maintain full spectrum dominance of the Empire, worthless F 35’s and aircraft carriers, and the multitude of surveillance agencies of the Deep State “Foreign Aid?!!! Exactly how does it benefit foreigners?

The costs of maintaining Empire is one topic that is completely off limits in the American “political” system where there is only one political party— the War Party.

A decade ago China had only a few miles of high speed train lines, just like the US. https://www.youtube.com/watch?v=0JDoll8OEFE

Ten years later China has 16.700 miles of high speed rail lines, equipped with the latest technology 200 MPH trains that serve millions of passengers at a cost per mile about 10% that of air travel. In California we can’t even begin to build a rail line between LA and San Francisco even if we pour many times the Chinese cost per mile down a rat hole.

Thor’s Hammer:

I can see you aren’t a “real red-blooded American who believes in American Apple Pie!” LOL!

We live in an authoritarian state pointedly since late 1940’s and the creation of the CIA…..and the presidents having their own private armies.

We are a “republic” with “democrat(ic) processes; those processes have been thoroughly crushed over the past two centuries.

American, near totally historically ignorant will have to learn how to fight all over again.

I dunno, sierra, sometimes I think “we” are mostly an undereducated bunch of advertising addled morons, and I don’t have to cite why I think so.

Well, finally some good news. The low inflation problem is grave indeed, but at least housing is one bright spot where the Fed has managed to mitigate this serious problem. The price of everything keeps rising relentlessly but we just can’t seem to stop deflation.

Central bankers have courageously made massive sums of money available to the investor class at low and even negative interest rates but even this valiant effort has not saved us from the scourge of prices that just don’t go up fast enough. I’m so disappointed when I see my grocery bill has only gone up 25% in one year – I know the Fed can do better than this. They have the courage to act, they will save us, they just need more time. I just hope soon I will no longer be able to afford groceries at all.

These are dark days but don’t lose hope, prices will rise more rapidly in the future. The Fed is intelligent and courageous they will delivery the higher prices we all hope for.

I’m a rapidly fossilizing historian of the UK, so maybe my antiquarian knowledge may be of some assistance. In the UK for decade after decade from the Napoleonic Wars on the purpose of investments was to live off the dividends. You made your pile, then you invested it so that your children, and your children’s children, could live a comfortable and highly respectable life as rentiers. You did not “sell the silver”, i.e. the stocks and bonds on which the family fortune rested.

Today, in America, the purpose of assets like stocks and bonds is to buy cheap and sell dear. No one who is really wealthy is prepared to live on the annual income of returns on his or her investments. They all want to “make it grow”, and can’t leave a nickle on the table. The idea of living like a character in a Regency or Victorian novel (“he has a country seat and 1200 a year”) is alien to most wealthy Americans. So they adore asset inflation, because they are not living on a fixed income and want their fortune to grow via said asset inflation. This has led to an inflationary bias at the top, which is unusual as historically the wealthy don’t like inflation because it eats away at the value of their interest, fixed rents on land, and dividends. But that’s not how Americans get rich and stay rich. They do so via speculation. Therefore, they love asset inflation.

As a rule, money does not last more than three generations in America.

Money has lasted in my family – Franco Spanish – since 1100. Yes, you read correctly.

Actually, since c 600 AD, but that was based on force, not commerce, so I don’t really count it.

From that perspective, the US is a plaything and fantasy of mere adolescents in terms of real civilisation.

I say this just to give you a sense of historical perspective, not to boast, because ‘wealth’ is mere dirt.

I myself only value what I make with my hands, not the rather ignoble game of speculation and manipulation which is what you all get so excited about.

Direct your thoughts to God,because that is all that matters in the end: a pure heart and a love of the best in your fellow men.

No one will ever remember you for being rich: but those who knew you will recall your goodness and decency if that is how you have lived.

@Cynic

Thank you for your sharing comment.

Since you come from generational wealth, please tell us what role if any, physical gold plays in preserving that wealth through the ages.

And yes, God bless, directing our attention towards the Almighty carries us through eternity.

Cynic – The US is all about being radically, perniciously, individualistic.

I have relatives here in California sitting on millions. I wiped out the few hundred in savings I had buying medicines, and somehow I’m too poor to get Medi-Cal so my only access to healthcare is the emergency room. I was keeping one relative updated, and it never occurred to her to offer to pay the $275 for one medicine; my employer eventually kicked in $200 and I sold something to come up with the other $75. As for the bill for the ER itself, a mere $1600 this time, it’s far more than I can imagine having in one place now, as things continue to get worse.

Wealth lasting more than a generation or two would imply people in a family giving a damn about each other or about the next generation, which is most Un-American.

alex in Detroit, I am one of those sitting on millions. But, you know something? As long as you are alive and have good friends and family, you are winning. Millions are nice, but not that important. Money is just a game. Being alive with friends and family is winning.

@ cynic

Why do you place so much importance on being remembered after death?

How is that different from all the egomaniacs our daily life is full of?

Hollywood Dog, very true. Those who had what it took to make and accumulate it, followed by those who knew what it took and managed to keep most of it, followed by those simply took it all for granted and learned the hard way that a fool and his money…

It is sad to see a 1st gen live long enough to realize their grandchildren will squander their labor.

But the above scenario only applies to “ eff’g up” money as opposed to “eff you” money like Cynic describes below. Eff you money lasts longer, but requires a sword to make … and defend.

Cynic’s comment also reminded me of Plato, who said that all the gold upon and under the world is not enough to exchange for virtue.

The pursuit of happiness requires virtue. Envy has always been a pauper and greed dies an ugly death.

Socal Jim – Did it not penetrate? My family, like any conventional American family, is useless.

Friends, well, my boss kicked in most of the cost of the medicine because as I got sicker, so did the business I work for him in. That $200 is putting thousands back into his pocket.

I am getting away from Americanism, Christianity, “The American Way” etc as far as I can, as soon as I can, given my age and resources.

As nearly as I can tell, America, and Americanism, are my biggest enemies.

Cynic is the least cynical amongst us?

Great comment, Mr Levy. Interesting.

In the John Galsworthy novel, “The Forsyte Saga”, Irene Forstye was left 15,000 pounds in her father-in-law’s will in 1892. With the income that was generated by the inheritance, probably invested in British consols (perpetual bonds) and giving piano lessons, she was able to maintain a middle class lifestyle, which included having a a maid. Under the gold standard rules, 15,000 pounds would have been worth about $72,000 US. Needless to say, 15,000 pounds wouldn’t buy much today. World War I and II and the Arab oil embargo of 1973 seriously weakened the pound. Since the gold standard days, the pound has declined in value from $4.80 to about $1.25.

15000 gold Pounds is worth 4,979,000 in today’s dollars.

(15,000 x .2354 oz per pound x $1410.00)

@ James Levy

As a student of History myself, I find your generalization of Americans, typically British and quaint.

The American People do not get to decide about asset inflation. That is a top down decision made by American Royalty in the Central Banking community and Financial classes. By borrowing against the earning power of the entire nation – essentially sending the bill to others and especially future generations – asset inflation is the free, unearned ticket to ride, for the very few.

The rest of Americans are not privy to, nor are they generally aware of the corrupt instruments of wealth stripping concocted by the few at the expense of the many.

Britain and Europe have led the way in stripping private earnings from the working class via Asset Inflation.

p.s. Excellent work Wolf.

That’s why I said the bias was “at the top”, which precludes the average American.

Interesting and arguably very valid take from a country whose power once rivaled that of Rome (in it’s time). And you still have “The City” and all it’s tentacles.

Van,

Post of the f’ing decade right there. Touche ~!~

Yes, we MUST keep the Fed faith fellow Chris Farley fan!

Van Dweller and MAGA citizen,

+1

Exactly…this absurd notion that we “must” generate more inflation is never even questioned by the political class and the lapdog press anymore…it’s just a “fact,” repeated ad nauseum by Central Bankers, and then regurgitated by the chattering class. There is plenty of inflation, especially in things that are not optional.

Since 1% of San Franciscans already live on the street just where does this all end? Just who does benefit from not having enough housing for so many people?

Are we all waiting for the Great Depression/Recession/Civil War 2.0 to hit before we deal with this?

On the more immediately practical side, would ending the effectively free money for Rentier Class and taxing or restricting empty housing help?

1% are on the street and obviously homeless, but another 9% are living in cars, in garages, “stealth” homeless if you will, but homeless all the same.

People sleeping in their cars or RVs are included in the homeless count (the 1%) by definition.

My guesstimate, and it is just that, is that just over 1% of San Franciscans are homeless with maybe another 1-2% are the couch surfing or spare space vagabonds.

I don’t want another serious dip or an actual depression, but the whole area felt like it was going to seize up and just stop functioning in 2000 and 2007 before the recessions came and froze/dropped rents and increased vacancies. The re-emergence of mini-studio apartments and dorm rentals again suggests that another big dip is coming again.

Down the drain goes American Dream

Data seems to agree with Case – Shiller. Since 2000, LA home prices has gone up more than any other area in the country.

And Boston will repeat that for the next 10 years.

Boston’s price growth has been mild sics the large spike in the late 80s. It has always been expensive, but YoY growth has not been subject to wild swings like CA.

Between 1970 and 1980 we had huge demographics. Afterward they were reasonable until the last decade, with boomers now aging out of prime buying time. Not 100% sure on the housing bump between 1970 and 1980 (besides demographics), but much of the remainder of the increase is explained with a long term chart of US mortgage rates.

https://fred.stlouisfed.org/series/MORTGAGE30US

Very interesting chart, “LessonINT”. I’m wondering what a chart showing relative affordability would look like with respect to: the decrease in mortgage rates, nearly stable income, and increased house prices. Would this be close to a “wash”? (I can’t imagine that mortgage rates could off-set that much price inflation.)

It’s important to remember that Shiller, a behavioral economist, blames inflation on “stories” that we tell each other and the “expectations” of inflation. They create a feedback loop. So, for housing prices to increase dramatically, there has to be huge demand; for prices to remain stable, there’s a balance between supply and demand. There must be a fairly stable “supply” because the rate of ownership hasn’t changed much since 1960 (supply naturally increasing relative to the increase in the population). In fact, the current U S home ownership rate is approx. 64% compared to 65% in 1960, only a 1% difference.

The Fed’s “flooding the economy with money”, resulting in surplus money going toward the inflation of assets (specifically home prices), may not be true. The bidding up of prices may be a behavioral event rather than monetary – the greater fool theory at work. No??

“Animal spirits”… (title of an Akerlof & Shiller book)

One more thing: the key reason that housing prices in major cities have gone up so much is the supply of land hasn’t increased. but the demand has exponentially. Some zoning changes have allowed increased housing density on some lots, but not by much (NIMBY pressure on planning depts.)

Another thing that’s possibly overlooked is RMD’s. What is the effect of all these Boomer homes and portfolios flooding the market in the next recession?

A Shiller housing price to median household income ratio historical chart shows a bubble. Over the decades home prices have kept up with inflation. More recently real estate outperformed govt. bonds, inflation and gold bars. It was rising at double digit rates for years. The average size of a new home built in the US has been increasing. Benjamin Franklin observed a house with two chimneys burns more fuel than a house with one. He recommended cost control, thrift and diligence as a way to wealth. A big house will bring more property taxes, insurance expense, utility expense, maintenance and repairs. It might not bring a better job or pay raise. Home owners got heart disease and cancer same as renters.

Seems like something happened in 1971 ,what was his name? Nixon, lets print our way to prosperity top move.

Yeah, that and allowing his right hand man, Henry Kissinger, to make a deal with the devil (Headchopper & Dismemberment Central) in the form of the Petro Dollar.

A home’s median value……but what is a home? In 1960 the average size home was 1300 sq ft. Now 2700 Sq ft. Air conditioning, granite counter tops, covered patio, fencing, three car garages, jet tubs, dual head showers, heated floors, sound systems,under cabinet lighting, third bathrooms, fireplaces, pantries, decorated driveways etc etc were all much rarer than today. So adjusted….not much change……sorry……but true…….unless someone can provide this old man some other reason. Always willing to learn.

Comparing house prices and house amenities to 1960 prices doesn’t explain the notion that Wolf described earlier: how some house prices can increase so dramatically within short time-frames, maybe only 2 – 3 years.

Credit cycles causing volatility.

Thanks for this post Wolf. I’ve forwarded it to several friends who are struggling to buy that first house. It doesn’t help them buy the house, bu5 it helps them understand the insanity of it all…

Next time you want to blame the “Reaganomics” remember that this started in the seventies.

So yes, this is yet another thing you can blame Nixon about.

But please do remember that Richard Nixon, Gerald Ford and Jimmy Carter were president in the seventies, so is not just Nixon.

Don’t forget LBJ and his costly Viet Nam war.

The Viet Nam war was great for military contractors. But as Eisenhower would have pointed out, it was awful for the American commonweal, as it took money away from building schools, hospitals, etc.

Another thing that we can blame Nixon for, is that his good pal and huge contributor Kaiser, of Kaiser Permanente, talked him into allowing Health Insurance Companies, Hospitals & Clinics, which heretofore had acted as pretty much public utilities, to act instead as pure profit driven entities going forward. That Dicky sure was a swell guy!

Sorry I’m killing the Comment Board here today. I’ll cease & desist and crawl back into my safe space now.

I thought the HMO act of 1973 was sponsored by Ted Kennedy, so I don’t think it was a republican vs democrat bill but bi-partisan. If I recall correctly this bill allowed for the profit motive to be introduced in healthcare where previously all hospitals were non profit. Otherwise your observations seem to be correct.

Kaiser Permanente is a non-profit health care system.

“Founded in 1945, Kaiser Permanente is one of the nation’s largest not-for-profit health plans, serving 12.2 million members, with headquarters in Oakland, California. It comprises: Kaiser Foundation Health Plan, Inc. Kaiser Foundation Hospitals and its subsidiaries.”

https://www.google.com/search?client=firefox-b-1-d&channel=tus&q=Kaiser+Permanente+non-profit

The Kaiser Family itself seems to have since regretted the ball they likely started rolling, and has a foundation (Kaiser Health News) which is separate from and very critical of “managed health care”. It is good reading, to me anyway.

Years ago I lived in Fontana, where their hospital supplied health care to workers at their huge steel mill. It may have been one of their first.

financialization .

second van post for saying it purdy.

Thanks wolf, if the data went back further it would show even more of the American dream. It’s criminal what has happened and I commend you for putting out real data!

We need to think of further generations not what gains we can personally gain…

Due to having been significantly under valued………with all the upgrades and more than a double in size homes should cost more if they are only selling for a 125% more. The issue is that millennial’s are not willing to deny themselves things that their parents either never purchased or only sampled in retirement. They want trips to Maui every year and the house that Dad had to work for 40 years to buy when they turn 35. Saving is becoming something only suckers do in this country. Unfortunately, without savers our capital base is the money printed by the fed and what is borrowed from China/Germany. Of course there are some saving millennial’s but the majority think going without Starbucks is a real sacrifice.

Fred my man… Why should the costs of building a home remain constant over time? Do flat screen TVs still start at $2k? Deflation is your friend bud. Homes should be cheaper to build today.

Land/house prices in cities have become uaffordable due to insane financing (5% down, interest only, etc.), urban revitalization (fair point), corporate profiteering (housing is big business), and most importantly, ~40 years of declining interest rates.

Remember, every time interest rates go down, it’s actually a bail out for current asset owners (old people), and a slap in the face to potential asset buyers (young people). It just ain’t fair.

Finally, as a millennial, I feel obligated to suggest y’all stop marching out Starbucks as your insult of choice. We youngins have moved on to 3rd wave cafes and local roasters because we are informed consumers and recognize real value (quality/price). Ironically, that’s also why many of us are refusing to buy into the current housing ponzi. Enjoy your precious living boxes though, you can like my photos of my Maui vacations from your finished basement.

I agree. It’s like the boomers telling us ‘stop being so irresponsible travelling and enjoying life. Instead you should work hard, do nothing fun, and pay 70% of your income into providing returns for our pension funds over the next 20 years. At the end of that you’ll own the leaky hovel in that crime infested neighbourhood and we will have lived out our golden years in style.’

What a scam. Young people are waking up to the ponzi scheme. The next step will be smart talented young people choosing not to become doctors or engineers as they see that it has become nothing more than a giant rentier trap.

Jon,

I mentioned in my reply to Fred about son putting in a trailer pad for a watchman. This is a couple who did as you guys recommend, they didn’t buy a home and lived for the day. Now, in their 60s, they were just evicted due to the property being sold where they rented. If my son did not make them a landing place, these two would have been screwed. I also did this, and built a small cottage for a friend which I rent to him for $350/month. Call it what you want, but many many rural people take it upon themselves to watch out for local seniors.

If you don’t have a place by the time you retire, you had better have a damn good income that will match rent trends, and be prepared to always move on. I recommend to people to buy a lot somewhere affordable, and just pretend it doesn’t exist. One day, there is your safe haven and you can tell the World to pound sand and kiss your a$$. A good used fifth wheel is cheaper than a condo, and is bigger and more comfortable. You can pick up a fifth wheel 400 sq feet, top knotch quality used, for 40-50K, and often for 1/2 that price. But, you need a place to park it and that can run $500-$700 per month. But hey, no problem because you bought you 1/2 acre, zoned right, years ago and now own it free and clear. right?

Aesops Fable covered this situation generations ago. Look up, “The ant and the Grasshopper”. My oldest brother was a grasshopper and just before he drank himself to death he hounded all his relatives for money to pay off debts. He didn’t go to Maui as he lived in France, but he skied in Grenoble and skindived off Egypt while the rest of us saved. He died misreable, penniless, and left a lovely family behind who are wondering, “what the hell happened”?

regards

OK, I wasn’t sure what a ‘watchman’ was–some type of security guard?–so I googled it and the first five pages, at least, of results were all about some sort of heart implant. So, I still don’t know …

Exactly, this is why we refuse to buy a home in the Bay Area. I’m not handing over my hard earned dollars to some mediocre NIMBY baby boomer. Let’s see how ‘y’all are doing’ when the next recession hits, the Chinese buyers run away due to Trump and the hospitals put a lien on that crapshack for your surgery.

We’re saving every penny to retire as soon as possible.

PNWGUY – Those of us living in the real world are brewing our own damn coffee.

Now, some of us might be buying ‘custom’ beans, where others of us are fixing up some nice Japanese UCC instant* into a nice iced coffee in this hot weather, but in all cases it’s far cheaper than SBUX burnt beans.

*Taster’s Choice is full of some kind of filler, clay or something.

I run on the cheapest store brand, I’m in it for the caffeine in a coffee tasting hot drink.

Who knows what else is in there besides that.

Fred, the house my parents bought in Los Angeles went from $22,000 back in the day to $1.4 million currently (just sold according to Zillow). Square footage remains the same! So… according to your way of thinking about this, the upgrades have made the difference. So, owners, over the years, must have put gold counters in rather than granite, and the cabinets must be made of African Blackwood and are no longer pine.

Fred Flintstone,

My 35 year old son, who works as an industrial electrician for a major machine maint company, puts away 50K per year off his pay cheque including an employer match….to fund a future retirement. He is also paying off a house and has a business on the side. All millenials aren’t as you describe, eating avocado toast at Starbucks, but then again he is a rural guy like his old man. :-) His friends are also focused and well on the way, but they are also rural.

Having said that, his ex wanted granite counter tops on a breakfast and kitchen island. I talked them into “granite tiles” at about $7 per square foot, and showed them how to lay tile using epoxy set and grout. they bought a $100 tile saw. For a few hundred they got the granite counter top instead of spending thousands, plus they laid their own kitchen tile floors and installed 3/4″ hardwood in the rest of the house, did their own wiring (obviously), plumbing, etc. I did their trim and window casements, and repaired their crappy drywall job. :-) Original purchase price for 3 acres and an old rundown motel on a river, 270 K 6 years ago. Converting motel to 2400 sq foot rancher, post and beam, 10′ ceilings……another 70K and lots of sweat equity. The original shack home on the property was rented but now serves as a tool & stores storage building + he is installing an rv pad for a watchman who doesn’t have a place to live.

City living is expensive, pure and simple. Plus, many (not all) people chase in their vehicles at the slightest whim; picking up this and that, items forgotten on the last grocery run. If you’re rural you have a list and don’t forget anything because a town trip is an hour each way and a waste of time and fuel. Life quality? It isn’t for everyone, but in my later years I find we can cook whatever meal we want, knowing that what we eat is only 20-30% of what a restaurant would charge and better quality. For treats we have an awesome local seaside cafe that is wonderful. Yabbadabbado.

Cali Bob (last comment for me, honest)

Sorry….a watchman is logging camp term, a live-in security guard usually a retired logger. The phrase used is, “going to watch camp”, when the regular crew heads for days off, he (with sometimes wife in tow) moves in for a bit of a paid holiday and steak dinners. In this case it’s a free pad with sewer and water…they pay their own hydro and phone. It works for everyone.

I have a son who lives in New York City. We thought he was doing OK because he had a decent job. Turns out he was about 30k in debt with his credit card and his girlfriend took a rather new $140k school loan. They have joined the debt hunger games like so many young people. There’s only one solution, Dad and Mom to the rescue. We’re now making only 2.2% in Treasuries so helping them get out of debt is a no brainer. I am now teaching basic budgeting to two brainy people. Debt is like smoking. It can kill ya yet so many are addicted to it.

Debt addiction is widespread today and can be devastating. Though most experts in the field advise parents against actually paying off their children’s debts. (Like puppies, they will be conditioned to repeat the behavior for more treats.) Teaching them budgeting, as well as how to leverage their education and experience for more income, is a better path. A total of 170k in non-secured debt is not insurmountable, especially for a schooled couple in NYC. Good luck!

>”…so helping them…”

Helping the girlfriend too?

a no brainer? The kid got himself in the hole. His GF is not his wife. Getting debt free including mortgage free is one of the more satisfying things I have ever done. The most satisfying is raising independent thing, self-sufficient son and daughter.

It’s not my rodeo, but a good lesson on budgeting is how to budget to dig out of that hole. They won’t die. IMO, you are not teaching them what you think and the lesson they are learning is diametrically opposed to your goal. 2 cents worth.

Demand v.s supply.

Keep voting for the NIMBY folks.

I live in flyover the country, and its insane the costs

& paperwork to build a d*mn house!

Propose a development? The price per/lot to make it to

final plat will cost more than that 1980 house.

I can’t even imagine what it costs on the coasts.

I’m sure they have govt. committees for “affordable housing” set up.

In 1960 the price to income ratio was ~2.6 to buy a median new 1,200 square foot home. In 2019 the price to income ratio is ~4.0 to buy a median new 2,400 square foot home.

What’s the big deal? Home ownership rates are the same at ~65%. There is none if you compositionally adjust for increases in size and appointments (more bathrooms, garages, etc.) over the two periods.

Anecdotes about owning in the right (wrong) location in the right (wrong) city in the right (wrong) state are meaningless.

So compare millennial to boomer home ownership rates. The lead edge boomers in 1982 (36 years old) rate was ~41% and the lead edge millennials in 2018 (36 years old) is ~35%. The difference can be attributed to compositional changes in race/ethnicity and marriage rates and delayed buying due higher student loans to capture the college wage premium.

Financialization: What It Is and Why It Matters

December 2007

http://www.levyinstitute.org/pubs/wp_525.pdf

Financialization is a process whereby financial markets, financial institutions, and financial elites gain greater influence over economic policy and economic outcomes. Financialization transforms the functioning of economic systems at both the macro and micro levels.

Its principal impacts are to (1) elevate the significance of the financial sector relative to the real sector, (2) transfer income from the real sector to the financial sector, and (3) increase income inequality and contribute to wage stagnation. Additionally, there are reasons to believe that financialization may put the economy at risk of debt deflation and prolonged recession.

https://www.oftwominds.com/photos2014/piketty-saez-top10a.jpg

http://media.peakprosperity.com/images/chs-inflation12.jpg

Winston: (4) design&implement the game so those taking the impacts of (1), (2), & (3) are required to play with no real alternatives (until public sensibilities similar to 1796 France/1917 Russia, et al, come to the fore…). Royalty of all types, eventually, do seem to overplay their hands, but with a dark age ensuing while the wreckage is sorted out.

Thank you, Wolf, for continuing to call out the nakedness of the various emperors, and citizens, all…

May we all find that better day.

1) 500 miles, 500 miles away from home.

2) From June 1949(L) DOW @ 161.60, til Jan 1966(H) @ 1000.55, the trend was very strong, providing great dividends for good health & life.

For 16.5 years, til Aug 1982(L) the DOW had a crooked smile on its face (Parabola) and jumped from 769.98 til 2000(H) and

from there to 2007(H), making x2 corrections in 2002(L) & 2009(L), but the trend was still very strong, providing dividends.

3) Since the DOW swallowed an AAPL things have changed.

4) Billionaires hate success and waste their money.

5) FB fell from a cliff, recovered after falling $96.60 to a swing point, and made a lower high, on Fri.

6) GOOGL is trembling like a leaf, opening huge gaps near its peaks.

The largest open gap followed Apr 2019(H), a new all time high, to start a huge downdraft.

7) AMZN one trillion built on hope, made it to a swing point and up to the last point of supply.

8) SPX mission accomplished, closing > 3,000, in an Ending Triangle, with RSI(5) triangle.

9) The DOW made a new all time high on Fri, stamped a clean number > 27,000, stopped by a resistance line coming from Jan 2018(H) to

Oct 2018(H).

10) The next correction will tell if the long time uptrend is still

intact. Since the stock market predict the economy strength in advance, we will know if we are going to be 500 miles away from home with just shirt on the back, not a penny on investors name, can’t go home the ole way.

The most colorful technical analysis ever!

Where the American Dream goes to die … well how about where it can go to live?

Voice crying in the wilderness (again, sorry): Get the hell out of the city. Buy a piece of land you can use and care not what the city slickers are doing to/with fiat money.

Housing prices could be better controlled if insurance companies would only insure houses for the cost to rebuild the property instead of the market value. Banks require the property to be insured for the price of the loan… in other words, fewer people would have the ability to purchase a home that is priced higher than the cost to rebuild the home.

Our last house (sold for $1.1M), the structure was insured for about $450K. The rest was land value. IMHO, there is no correlation between home prices and insurance limits.

Keep in mind that is possible to be under insured to the point that the settlement from the insurance company is insufficient to rebuild the structure. Many people in CA who were burned out in the past few years found that out the hard way.

I worked in insurance for years and saw first hand that a vast majority of homes were insured for market value, not replacement value. Simply put, if the standard replacement cost estimate didn’t cover the value of the loan, the banks would hire a person to appraise the house for the value of the loan… lots of fraud in the entire process.

I’m not 100% sure, but most county property tax values end up being based on median market rates and then insurance rates also follow that hazy valuation approach — hence, property taxes are a nice source of revenue that seem to go up and up and then, when the market drops, those taxes (and insurance rates) are very slow in reflecting lower market value. Meanwhile, we all need better streets, higher paid teachers, better libraries, police, fire and all those things that help us with cost of living.

I doubt that. AIUI, you can under insure and over insure (besides getting it right). If the former you’ll not get enough to cover the cost of a full rebuild (if you make a claim). If the latter, I doubt somehow they’d pay out enough to build two houses (or what ever), nor would they be likely to refund the excess you paid. All the insurance firm is interested in is the cost of a rebuild (or whatever) they don’t care the market value, why should they?

Mind you, it’s interesting that the cost of a rebuild can differ so much from the market value of the property (it can vary both ways). Where does that extra value come from? Conversely, the same house built in a less salubrious neighbourhood can have a market value less that the cost of rebuilding it! Seems to me the market is skewed such that houses are best built in areas where they sell for more than their real worth.

Don’t kid yourselves.

The rentier class suppresses wages and manipulates prices higher, including real estate, as a matter of course, to increase profits.

It’s not just monopolistic practices, tax evasion, and government corruption, but by any means possible – and new ways are invented all the time.

How out-of-whack is the discrepancy in growth between incomes, rents, and house prices?

Not nearly as much as RE specialist rentiers would prefer, but they’re working on it. It’s not easy to weasel home prices higher when your competitors are already squeezing your intended victims dry with their own scams. College graduates, for example, are already indebted up to their eyeballs before they can even get into the housing market, and you know that can’t be good for business.

ah! THERE you are….

Yes, glad you’re back… although I don’t buy into the conspiracy theory.

I don’t buy into the conspiracy theory.

Don’t be naïve. It’s business as usual. Let’s just say it’s not a secret conspiracy, because the rentier class operates pretty much in the open, except for money laundering, tax evasion (the world’s biggest industry), government corruption, and so forth, for obvious reasons. No ‘conspiracy’ needed, not for such a common business model.

Besides, sometimes a theory is also a fact. Depends on the quality and quantity of supporting evidence, and naturally, for that, you come here.

1) Judges 16:29 : Let me die with the Phillistine, Samson pushed the two pillars and the wall came tumbling down.

2) In June 1967 the Suez canal was closed for over a decade.

Onassis became a multi millionaire and married a grande widow.

Energy supply from Iraq, Iran and SKA to Europe & Asia was

constricted for over a decade.

ARAMCO, still in American hands, cheated their Saudi partners,

about price they get per barrel oil in the open market.

3) In 1973, following another war, the desert kingdom imposed an

embargo and confiscated 100% of ARAMCO in several tranches.

4) Oil supply was further constricted until the early 1980’s deep recession.

5) From 1967 til 1982, oil supply had the sharpest drop, making USD strong, until James Baker Plaza accord, who also threatened Germany in Oct 1987, causing a pop…

R/R kicked Japan out of UST, because he didn’t like

Japan immoral flirt with rising China, promising Deng Xiaoping a fist full of dollars.

6) Money from US vaults to Tokyo, Rockefeller Center RE and the Japanese stock market. Nikk225 came tumbling down.

The good ole way inflation didn’t lift the global deflation.

Michael Engel,

Suez canal closure helped secure Onassis fortune. That’s the first I heard of it. Thanks for the history lesson.

>3) In 1973, following another war, the desert kingdom imposed an

>embargo and confiscated 100% of ARAMCO in several tranches.

This 1973 war was the tipping point for huge increases in U.S. diplomatic and military spending in the region that continue today. The middle-east is costing us our prosperity, e.g., universal health care, alternative and/or renewable energy, space exploration, smart national electrical grid, etc., but instead we are going deep into debt selling houses to each other.

To understand what has happened to income, the better starting point for analysis would be 1970, not 1960. The 1960’s were a time of relatively good income growth. By the early 1970’s however, it became obvious that employers in basic industry were intent on de-industrializing the American economy. Starting the analysis in 1970 captures the extent to which the malign intent behind out-sourcing was successful, from the point of view of industrialists and employers. 1970 as a starting point also removes roughly half of the increase in income over the time period, compared to 1960, and starkly demonstrates how the intentions of the few translated into reduced living standards for the many.

Some would argue that is where religion/ philosophy / morality / Christianity comes in. With some plausibility.

Where as I don’t think, communism/ socialism have yet to have a successful long term cycle to prove their viability.

Anyway, these are philosophically mortally bankrupt concepts anyway. Pro Slavery concepts couched in platitudes of “goodness”.

It’s not just the US of course, you can see very similar trends play out in Europe.

Netherlands has its “Herengracht index” for housing that goes back four centuries and tracks the price to average income ratio for the same homes, similar to the US Case-Shiller repeat sales index. Home price to income has varied strongly over the years due to good and bad times, but it always was within a clear band with the tops of the ratio 4-5x the bottom values. On average home prices simply tracked inflation for several centuries. Big adjustments usually took many years and often more than a generation, but they always occurred out of necessity. From the late nineties (first worldwide financial bubble) index prices have been outside the historic band almost continuously, even the small dip after 2008 didn’t change that and current prices are by far the highest in 400 years, not just absolutely but also relatively to incomes.

If you look at actual prices, the Dutch had their last housing crash in 1981 (average home price down ~50% in 1.5 years, after a relatively modest five year housing bubble). From the late eighties it was off to the races around Amsterdam (financial center) and a few years later for most of the rest of the country. In my remote hometown, home prices have increased 1500-2000% (15-20x) from the early nineties, without any significant upgrades apart from irrelevant stuff like newer kitchen appliances, ISDN or cable TV. Note we are talking about prices for the same homes here, not bigger or better homes! Only basic apartments have increased significantly less. Even the most remote locations in the country (with no good jobs or services) are many times more expensive than 30 years ago. Land prices have increased even more, in my area 50-100x compared to the eighties, mainly thanks to government policy (zoning).

Over those same 30 years, Dutch incomes have increased maybe 100% and household incomes a bit more because of more women joining the workforce. Rents have increased way more than incomes and as a result free market rents are now so high that many renters spend more than 50% of their income on rent alone (highest for all of Europe). But Dutch government thinks this is great because it forces renters to buy a home.

In Netherlands foreign buyers were not a factor at all until a few years ago and they are still irrelevant in most of the country. The main driving force for the huge price increases was zoning (severely limited supply) plus financialization, “easy money”: 100% mortgages for everyone with a pulse (in the nineties you could even get 120-200% mortgages), the most generous mortgage tax deduction in the world, a free government put option for the average buyer (i.e. you can’t lose money if you ever have to sell the home) and probably the most important after the start of the Euro: near 0% interest rates. Despite ridiculous price increases of 10-20% per year for many years, most Dutchies still argue that home prices can only go up and young people will have to accept much smaller homes or rent forever. Older canal homes in the cities owned by boomers are being converted into many very expensive tiny apartments in order to keep homes “affordable”.

People in social housing with low income are lucky, their rents have more or less tracked social security incomes and they pay only around 15-20% of the free market rent for a similar same home. If you have a normal job you are less lucky and you either have to spend most of your income renting, or swallow the ultrahigh home prices and hope prices keep climbing forever.

An additional problem that is brewing is that the government will force homeowners to upgrade their homes to low energy use with taxes and draconian price increases for the natural gas that most Dutch homes are running on now. Estimated cost at least $75.000 per home (solar panels, heat pump, insulation etc.). Because most people do not have this money, they can borrow this for almost zero cost, on top of their 100% government-guaranteed mortgage … why worry, prices can only go up …

It’s interesting that the figures for Pittsburgh are relatively sane and, a quick look on wikipedia says, they have a form of Land Value Tax there.

The wikipedia article also suggests higher land value taxation leads to increased construction.

I heard that American Dream and European Dream have been decaying and diminishing for quite sometimes since 2000. In contrast, someone else particularly in Asia and Africa have been eating out more and more of Americans and Europeans pies.

In my opinion, the risers in Asia mainly China, South Korea, India and perhaps dozens of other Asian and African countries such as Indonesia, South Africa, Thailand, Malaysia, Singapore, Vietnam, and Nigeria will become new economic driving forces in the future.

I read that the current Chinese president publicly announced that China will become super power and replace America by 2050 in many areas such as military, economy, education, world’s trading currency, media, filmmakers and etc. There are currently more African students studying in China now than in America and Europe combined such that almost all of the African students in China have been receiving scholarships from Chinese government.

Looking at how much monies Chinese government have put into their military’s development these days, they’re huge. Eventually, there will be wars between China and America in the long future. Whoever will win both the soft and bloody wars of these two countries becomes the superpower of the new world’s era.

Today the population of Africa is just over 1 billion……by 2050 it will be 4 billion. Asia will increase by 2 billion by 2050. That is where the growth is happening.

I am probably dead or nearly dead by 2050 LOL considering my current age. By that time, I would hope that my future pensioning payments from my personal savings and investment combined with small money from the Canadian pensioning system would be able to catch up with my living expenses around the years 2050.

The Okies went west in the 30s, which way are we going to go?

Think global. One can live like a king in many countries for a million dollars.

Does laundered cash, foreign and domestic, count as “Household Income?” ;-)

Years ago I was banished for mis-timing comments and moderation of same, so this likely will not appear. Just as well, I get too opinionated.

But I would like to say this is by far the BEST dialogue I have ever read here. Thanks, Wolf.

If allowed, one final comment; “Give me just one truth to stand upon and I will deduce a world” Can’t recall the ancient fellow who said it.

Faithful/Reader Ad Clicker,

You were never “banished.” Your comments were sent to moderation for some reason I cannot remember (this was 2017). This means that I get a chance to review them before they’re public. That’s not “banished.” Just follow the commenting guidelines.

https://wolfstreet.com/2017/10/07/finally-my-guidelines-for-commenting/

I’m so impressed you reply to everyone. Truly VIP treatment. ?

Thanks Wolf. I realize now that a lot of people here can type, and fast, plus have mobile “smart phones”. I have a dumb flip phone and a desktop because it’s all I need/can afford, whatever.

By the time I post, 20 comments have gone by, and nobody seems much interested in an older dialogue, even if it’s good. I’m not even sure you look this far back, and must also have some good algorithms or some extra help.

Anyway I have a pretty significant old notion stuck in my head, and that is that Vietnam cost 2/3 of WW2 in todays dollars. All that cap-ex just blown to hell, and resulting fallout if that notion is true. Anyway, could you look into that if it isn’t too well hidden? And thanks again.

NBay,

Don’t worry about commenters not replying. There is only a small number of active commenters. But there are many readers that read these comments. For example, this article was read over 12,000 times so far, and it’s still active, and people still read your comment. Some articles here are read over 80,000 times. If you want readership, it’s the readers who matter: and 99% of them don’t post comments, but many read comments.

The late and great George Carlin said: “The American Dream – because you have to be asleep to believe it”.

If you remember way back to the 90s, the belief was that housing prices in cities were going to drop. The belief was based on advances in communications technology meant people were going to work from home, and they would start living in far flung place meaning the demand for housing in cities would go bust. Were they wrong.

Yes, interesting how this never worked out like expected.

I remember how second half of the nineties self-employed people in IT in Netherlands started talking about working from home thanks to the web and moving to Belgium, France or even further away with their much lower home prices, more nature and “slower” life. For the price of a small Dutch home you could then buy a real castle or a grand villa with a huge garden in France and have some kind of permanent vacation. Some really took the plunge but most of them were back within a few years. Clearly it doesn’t work out in practice for the average person and even after retirement relatively few people are moving.

I’ve written a fair amount here about this. It turns out that working remotely just plain sucks. You *have* to be in the same room together or things will go horribly. I mean, projects torpedoed, careers ruined, companies even going under.

The US gov’t has been pushing “teleconferencing” since the 1980s, since it costs a fortune to fly people around but if they don’t fly people around, things end up in a shambles.

People would love to get out of “Silicon Valley” because it is indeed insanely expensive here. There’s a very strong motive.

So when you see a strong motive to spread out, and see it not happening, that should tell us that there’s a very strong reason that spreading out leads to failure.

So you can’t afford to leave until it’s time to retire. Then you can move to bumfuct nowhere and set up your little machine shop etc. as a hobby retirement thing.

An interesting insight to this is, if you want one of those carved wooden signs, there are TONS of guys on Etsy with engineering degrees and CNC setups. You can get an absolutely beautiful sign done. The shortage is in people who’ve put in the 20 years to get good at brush lettering, because these are guys who’ve put in decades of 60-hour weeks, ain’t got no time for handicrafts.

Simply untrue. In the consulting firms I’ve worked with, a typical skype business call will have individuals in half a dozen time zones. We have the technology, it works splendidly — and it’s more efficient than spending time and resources on international flights/hotels/per diem ect…

I foresee a collapse in office parks in the not-so-distant future.

I agree that despite the technology, it usually doesn’t work out. Maybe it takes 1-2 generations to get accustomed to new social structures?

As to the reply from Nicko2: yes, some technology is available and in a way you could see outsourcing as something similar. Why let people work from home (or further away) when the technology can just as well let the work be done on the other side of the globe in a low wage country? This was a trend too for some time but it failed in many cases, and only with carefully structured and managed projects it works out. Otherwise, the time and money spend in correcting all the bugs, misunderstanding, language problems, support problems etc. from outsourcing isn’t worth it. Many IT projects are still “local” to some extent and a lot of that apparently doesn’t translate well through skype and similar means.

I would like to see these same graphs with interest rates added. I have a pretty good idea of how it would look.

After reviewing this data closer, clearly something is not right with the income data. Income has risen so much more than stated in the graphs. The only explanation is perhaps the income graphs represent real wages instead of nominal wages … i.e the income is reduced for inflation. However, wages are so much higher than 1960. At the same time, the house prices appear to be nominal … include inflation. Something smells here …

SocalJim,

ALL data in these charts is adjusted for inflation, including incomes. This was pointed out about 16 times in the text to make sure readers didn’t trip over it :-]

Real income “FRED” from government shows more income growth from 84 to 2017 than these graphs show from 60 till today. Something is off.

I just checked. FRED chart (annual) goes from 1984 through 2017. Real household income increased 22% since1984

https://fred.stlouisfed.org/series/MEHOINUSA672N

Supposedly one of the strengths of the American middle class workforce is mobility.

Lots of businesses moved to the sun belt starting in the 80s. California and Illinois are losing businesses.

But when the businesses move I’ll bet the management goes too but not the mail clerks or janitors. Their value in the workplace diminishes. Not surprised at all that with clerk/janitor demand reduced and supply steady clerks and janitors might not see wage increases.

Perhaps we have a mobility problem? Just a thought for a Sunday afternoon.

Speaking of mobility, if you’re pooping in the streets of SF, my advice is to go Mexico, disguise yourself as a Mexican (or African I suppose) and then get caught crossing the Rio Grande. Instant improvement in your food, clothing, and shelter.

We have people dying in the camps, adults as well as children. And you think conditions are great there?

You first.

Something to ponder, but clerks and janitors will easily be replaced by AI and robots over the next twenty years. ;)

Nick02 – there’s a wide gulf between “things that compute” and “things that move around in the real world”.

Anyone who’s worked with things that have to work in the real world knows, it’s a matter of constant repairs. Anything working in the real world wears out, and fast.

Plus, all of this AI stuff takes just gobs of energy to run. Energy we literally won’t have.

Clearly inflation numbers or BS. There’s no way prices could go up that much adjusted for inflation and not affect inflation itself so that wages didn’t go up at all basically.

The y-axis of the chars should not be called “growth rate”. The y-axis is simply cumulative price change (in percent). Someone should tell the original author. There is no comment section on the referenced blog.

Unrelated but relevant: The term “price growth” that I see get bandied about in REIC press releases gives me the willies. It is Price Change not “Price Growth”.

By the way, I can’t find what is the source of the price data. Wages are self-reported from decennial census and ACSD data. Median prices are from ????

Other than that, quite interesting.

Interesting information on Fannie and Freddie.

https://www.americanbanker.com/articles/trump-team-wary-of-fannie-freddie-fix-before-2020-election

This topic has been better described by economist Michael Hudson who has pointed out the inevitability of these data due to shifting to finance and away from manufacture. The logical outcome is raising the cost of housing by lowering the standards for mortgages, thereby increasing demand.

Eventually, the cycle will be impoverished by greedy rentiers and most people who will be unable to buy stuff and the entire economy will collapse.