Where is the Fed’s “U-Turn” that Wall Street promised us?

In June, the Fed shed Treasury securities at the slower pace announced in its new plan for QT, but it dumped Mortgage Backed Securities (MBS) at the fastest rate since the QE unwind started, breaching its “up to” cap for the first time. And it is experimenting with the opposite of its QE-era “Operation Twist” – Operation Untwist?

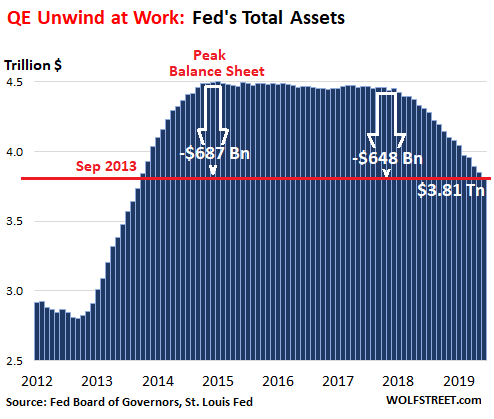

Total assets at the Fed fell by $34 billion in June, as of the balance sheet for the week ended July 3, released Friday afternoon. This includes $15 billion in Treasury securities and a record $23 billion in MBS, for a total of $38 billion, less some other balance-sheet activities unrelated to the QE unwind. This trimmed its total assets to $3.813 trillion, the lowest since September 2013. Since the beginning of the “balance sheet normalization” era, the Fed has shed $648 billion. Since peak-QE in January 2015, it has shed $687 billion:

Treasury Runoff.

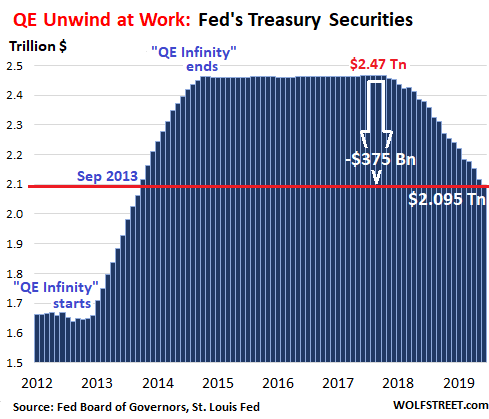

The Fed doesn’t sell its Treasury holdings outright. But when securities mature, the US Treasury Department pays them off, and the Fed then doesn’t reinvest this money in new securities. Instead, it destroys this money in the reverse manner in which it created it during QE. But the Fed has announced caps — the “up to” amounts. If the amount of Treasuries that mature in a given month exceed the cap, the Fed reinvests the overage in new Treasuries. Under the Fed’s new regime, the maximum amount of Treasury securities allowed to roll off when they mature was $15 billion in June. And that’s what happened.

In June, three issues matured, for a total of about $21 billion. The Treasury Department redeemed them and paid the Fed for them. The Fed reinvested $6 billion of this money into new Treasury securities but allowed $15 billion to roll off without replacement. So the balance of Treasuries dropped by $15 billion, to $2.095 trillion, the lowest since September 2013:

“Operation Untwist”

Over the past couple of months, the Fed began replacing longer-term Treasury notes with short-term Treasury bills. It’s the reverse of “Operation Twist,” which had been part of QE, layered between QE-2 and QE-3. During Operation Twist, it had replaced its short-term T-Bills with longer-term T-Notes and T-Bonds in order to force down the recalcitrantly high long-term yields.

Now it is starting to do the opposite, albeit in only small amounts. Short-term bills cropped up for the first time on its May-dated weekly balance sheets. In the current balance sheet, it lists $5 million, with the first batch maturing on July 9, the second batch in August. The Fed seems to be testing what it said would be implemented after September: Replacing long maturities with short-term bills to bring down the average maturity of its portfolio.

If Operation Twist worked to bring down long-term yields during QE – doubts remain – then “Operation Untwist” should do the opposite and put upward pressure on long-term yields.

Mortgage-Backed Securities

MBS securities differ from regular bonds: Holders receive pass-through principal payments as the underlying mortgages are either paid down through monthly mortgage payments or are paid off when the home is sold or the mortgage is refinanced. Any remaining principal is paid off at maturity.

About 95% of the residential MBS on the Fed’s balance sheet – they’re issued and guaranteed by Fannie Mae, Freddie Mac, and Ginnie Mae – mature in over 10 years. So the current runoff is almost exclusively due to pass-through principal payments.

These pass-through principal payments vary with movements in mortgage interest rates: Falling mortgage rates induce homeowners to refinance their mortgages, which means that their old mortgages are paid off, and the principal is passed through to the holders of MBS.

Mortgage rates had hit a multi-year high last November, and mortgage refi applications dropped to a decade-low in December. But mortgage rates have since skittered lower, and refi applications have surged, according to the Mortgage Bankers Association. And the flow of pass-through principal payments has surged too – and the Fed is taking advantage of it.

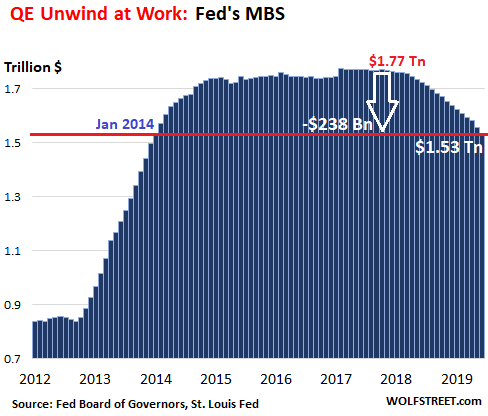

In June, the balance of MBS fell by $23 billion to $1.533 trillion. This was not only the biggest run-off since the QE unwind started but it also exceeded the $20 billion cap – another first! In May, the run-off had hit the cap of $20 billion for the first time, but didn’t exceed it:

The action on MBS confirms that the Fed is eager to get rid of them as soon as possible. Its new plan calls for getting rid of all of them, even if it has to sell them outright if pass-through principal payments slow down too much, as it said. Starting late this year, it will begin to replace MBS with Treasuries. Meanwhile, the Fed is making hay while the sun shines – given the surge in mortgage refis and pass-through principal payments and the prospect that when mortgage rates snap back, this flow of pass-through principal payments slows down.

Let me just throw this out there for us to kick around: The Fed has already accomplished more with its verbiage so far this year than it had in the past when it cut rates all the way down to zero and did trillions of dollars of QE. We’re already seeing the first results. Here’s why. Read… The Fed’s Stealth Stimulus Has Arrived

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Could somebody please, please, please explain why mortgage rates have been DROPPING since the start of the year?

https://fred.stlouisfed.org/series/MORTGAGE30US/

Even while all the other fundamental rates (federal funds rate, etc) are rising, and — as Wolf writes — the fed is shedding MBS?

Makes. No. Sense.

I have been trying for a year now to find a reasonably priced piece of buildable land here in northern Grays Harbor — very, very, very rural Western Washington, way too far to commute to anyplace that has a sensible unemployment rate. No vacation homes here either, those are all near the beach.

I can tell you on a boots-on-the-ground basis that things have gotten ridiculous again, progressively more so with each passing month.

I’m a cash buyer and refuse to go into debt for this. But the prospect of bidding against people who are happy to do that, hopped up on central-bank-funded funny money, is not attractive. It’s like being at a sports competition where the other side is openly shooting steroids.

I’m getting really tired of waiting.

Why has 30Y Mortgage Interest Rates been dropping?

Because Long Term Treasury Rates have been dropping lately.

That means there’s a lot of cash floating around.

That extra amount of cash (at a low interest rate) is causing a lot more ASSET purchases.

Wazoo,

Here in my rural nest younger folks are moving in, (NE Vancouver Island). In fact, we hosted a bunch of folks last night to say goodbye to friends who just sold out and are moving back to Australia. Buyers? 35 year old couple….24 acres, awesome new home on a great river. The price was reasonable by today’s standards.

It wasn’t too long ago that Aberdeen and area was in real decline. I think what might be keeping your prices elevated are the softwood lumber tariffs against Canada. This forced BC Companies to relocate into WA for the lower labour costs, and to avoid the tariffs. Places like where I live are now pretty lean and mean. This protectionist trend is temporarially subsidising economic activity and keeping prices higher than they normally would be.

Here is just one example. There are lots of others. Note, the CDN company in Beaver WA. (Interfor)

https://www.google.ca/search?tbm=lcl&ei=1akgXYLKEqiA0wLBl5TIDA&q=Interfor+operations+in+WA&oq=Interfor+operations+in+WA&gs_l=psy-ab.12…87739.93513.0.96175.18.18.0.0.0.0.85.1399.18.18.0….0…1c..64.psy-ab..0.3.240…35i304i39k1j33i10k1.0.hq10i7lvIwE

Paulo:

The rule of thumb for lumber in a typical house is 10,000 board feet. At the peak of the commodity lumber market, Spring 2018, 2×4 SPF hit $650USD. So the peak mill value would have been $6500, and to the retail market, maybe $10,000 delivered to the jobsite. BTW, SPF, the largest specie used in North America, dropped down to $300 this Spring and is now sitting around $380.

Lumber prices have little to do with the price of a home, but cheap Central Bank credit creation and wealthy Foreigners competing against working people’s wages, has everything to do with it.

“friends who just sold out and are moving back to Australia.”

Couldn’t take all the wind and the rain? Wanted to get closer to their friends and family?

The older one gets, the more basic things matter: good climate, good company.

>>why mortgage rates have been DROPPING since the start of the year?

Here is the real answer: Because bond buyers believe (wrongly) that Fannie and Freddie MBS are guaranteed by the US Government, and therefore accept lower interest rates whenever the 10Y UST drops, which in turn happens whenever investors seek a “safe harbor” due to recession fears.

The yield spread between UST10 and and MBS has been hovering around 1.75% for a long time. For example, right now the UST10 yields about 2.05% and the 30Y mortgage rate is about 3.99% (+profit, fees and points so APY is 4.264%) according to Quicken website.

Th higher at-issuance yield for BS versus UST10 mainly accounts for the subsequent yield losses that occur because so many mortgages get prepaid (through refinance) long before 30 years are up. If you look at MBS funding bonds with 1-year left to maturity they trade at yields even below UST1yr yields.

The US system of mortgage lending is completely perverse. It encourage speculation and asset inflation and is a great moral hazard. And it is a Wall Street cash cow at taxpayer expense. It is the usual system of privatizing the profits while socializing the risk and the losses.

>>Th higher at-issuance yield for BS versus UST10

The higher at-issuance yield for MBS versus UST10, feel free to fix typo and delete this comment.

Per my understanding

Mortgage rate is tied to 10 year treasury yield.

Yield drops when demand for treasure is more

Demand for treasury is more when investors want risk averse but low return investments and if you have too much money sloshing in the system

Right now we have too much money and people looking for safe havens

This more demand for treasury and this low yield and thus low mortgage rates

Jon, that’s more or less what I said. Let me try to refine my formulation slightly.

1. Many investors think of the a 30-year GSE mortgage bond (MBS30 for short) as being equivalent to an N-year UST bond, from a credit risk and rate risk perspective, with N=10 being the closest proxy.

2. A yield spread exists between MBS30 and UST10, due to (a) the MBS30 is being repaid continuously instead of at the end, and (b) that MBS30 mortgages may be prepaid in full due to sale or refinance, and that the investor therefore may have to re-invest at a potentially inopportune yield (interest rate risk), and (c) because the middlemen (mortgage brokers, Fannie, Freddie, etc) are taking a cut for arranging each mortgage, insuring the bond, and also for collecting and distributing payments to the bondholders (aka. “mortgage servicing”).

3. MBS30 therefore tend to move at a fairly constant spread from UST10 yields, often 1.75%-2.00% under “normal” conditions.

4. UST10 yields are affected by considerations such as inflation expectations and (especially now) its use as a safe haven before and during stock market crashes and recessions.

5. Investors are wrong in assuming that GSE mortgage bonds are guaranteed by USG. Only true agency (GinnieMae) mortgages are.

6. All of the above implies that mortgage bonds are one of the most doctored, manipulated and un-free markets there is.

>>from a credit risk and rate risk perspective,

from a credit risk and DURRATION risk perspective,

Congress took over Fannie and Freddie during the 2009 GFC. Therefore the MBSes were or are guaranteed by the US taxpayers.

Nope. USG is a majority shareholder, that is all. Shareholders are not responsible for debts. Nowhere is there an official document that says USG guarantees Fannie and Freddie MBS bonds.

DebtWazoo,

I too am in Western WA and am in the industry. We are a week or so from a final plat of estate lots and are trying to sell another entitled plat + engineering. The projects are located in active markets in north Pierce County and SE King County. The market has slowed from what would have been immediate liquidations a year ago even though there are very few finished lots available. I consulted for 8 banks in 15 municipalities during the last downturn involving their non-performing assets and REO’s. What is now hindsight for then is foresight for now. You are located in the upmost tertiary market and are witnessing an echo-bubble of the GFC, imho. When asset values drop again, nobody will be issuing loans for land and the banks will be unloading assets for amounts you can easily afford! Be sure to check the difference between a Statutory W Deed and a Special W Deed which they may need to convey with. Not a big deal but look for unwarranted encroachments, etc. Be patient my friend.

> Be sure to check the difference between a Statutory W Deed and a Special W Deed which they may need to convey with.

Thanks. I had one seller try to tell me a quitclaim was okay, was having none of that. Warranty deed with title insurance, tax deed (straight from the county) with a title report I understand, or keep waiting; those are the only options.

> Be patient my friend.

Thanks, it’s not easy. Tired of living in town with all the noise but that’s where the rentals are.

Not until the effects of operation untwist take effect, should start seeing small rises in the 30 yr bond rates happening simultaneously with the drop in shorter rates; at least theoretically

Doug Noland’s group is going to do a conference call “What’s Behind the Global Yield Collapse?” CBB July 18th.

@Debtwazoo:

Financial markets are globally interconnected. Central Banks world wide have produced “Funny Money” – that is buying bonds – in order to speed up growth and investments or at least prevent set backs in the economy. Prevent Deflation ..

I live in Denmark. I have the same concerns as you.

Last week we saw negative interest rates on all Danish Treasury Bonds.

Mortgage rates are now 1% on a 30 year loan ..

The basic question is : What has happened to the INFLATION.

Many economic text books should be re-written ?

“The basic question is : What has happened to the INFLATION.”

That’s easy to answer: There is a TON of inflation. But not in consumer prices (consumer price inflation). The inflation is in asset prices… houses, stocks, bonds, commercial real estate… you name it. It is called “asset price inflation.” It has very pernicious consequences over time. The books don’t need to be “re-written.” This phenomenon is well known and documented, including on this site.

There are different types of inflation, the three most important are: wage inflation, consumer price inflation, asset price inflation. They’re impacted by different things in different ways.

The cure for inflation, like most cures, consists chiefly in the removal of the cause. The cause of inflation is the increase of money and credit. The cure is to stop increasing money and credit. The cure for inflation, in brief, is to stop inflating. It is as simple as that. Henry Hazlitt

And the cure for getting old is to stop aging.

> And the cure for getting old is to stop aging.

Well-known trick among dead people.

Wolf:

Use the Big Mac inflation index. In 1970 the Big Mac Meal gave you change back from $1. Today’s Meal is not bigger, and no better in “quality”. Essentially the same meal. Depending on where you live in North America, that same Meal is $7 to $8, so inflation is 700% plus.

From the Caterpillar Performance Handbook on Fuel Consumption for Cat machines, #1 Diesel Fuel was 16 cents per U.S. gallon in 1973. Depending on where you are in North America, Diesel costs 20 to 30 times that now. Inflation at 2000% to 3000%.

Government benefits hugely from inflation as they tax consumption items on an ad velorem basis and collect more income taxes as they push you into higher tax categories. Conveniently for government, they can tell you that your new TV has more value/utility, ergo, that $800 price tag is really $400. As if government has a precision instrument to measure the excitement and utility baseline to an individual when they first experienced TV (black and white) in the first place.

It might seem quaint, but I still remember in 1972 my father haggling with a farmer before they settled on the price of a 100 pound sack of potatoes at the princely sum of $1.

kam,

There is no place in the US today where diesel costs “20 to 30 times” what it cost in 1975. Back then, a gallon of highway diesel (No.2) cost about $.60 a gallon. Times 20 would be $12 a gallon; times 30 would be $18 a gallon. Today the actual average cost in the US is $3.05 a gallon.

In 1980, #2 diesel cost $1.20. Today, almost 40 years later, it costs 2.5 times as much ($3.05).

Also, the couch set that I bought in 1982 (cloth) was more expensive than the beautiful leather couch set we bought a couple of years ago. I bought my first computer in 1984, with a daisy wheel printer, for about $4,000. It didn’t even have a hard drive. Now look what kind of computing power you can buy for $4,000. Not to speak of smartphones, which are super computers by 1985 standards that would have filled an entire room and cost many millions of dollars.

Consumer Price Inflation is a broad mix of goods and services. That Big Mac Index is fine and dandy for Bic Mac eaters but is irrelevant as an inflation measure.

Here is something you should read before you spend another second thinking about the Big Mac index:

https://wolfstreet.com/2019/06/14/my-personal-dive-into-the-murk-of-official-retail-sales-inflation/

Caterpillar Handbook 1973, does not include road taxes, etc. Cost was 16 cents/US gal.

I used to sell Cat Iron and those were the fuel costs, ex-taxes.

The cheapest fuel, ex-road taxes, for my machines that burn diesel fuel is just shy of $3.00 US. gal. And Diesel prices can be pushing $4.00, depending on location.

$3.00 divided by .16 is 18.75 times.

The cheapest tax-in cost Diesel for trucks travelling thru Canada is C$1.21/liter and lots of truckstops are at C$1.40. This translates to $3.43USD per U.S. gallon minimum to an top end of $4.00UDS per U.S. gallon.

So, 20 to 30 times the cost is not out of the ballpark.

Ask anyone with a hundred highway trucks on the road or with diesel-fuel sucking machinery.

I used 1973, before the big jump in Opec induced pricing, but that is the only old Cat book I have left.

I get your point on the mix of consumer goods that go into the mix of what constitutes consumer price inflation.

Inflation is rampant in many of the absolute necessities of life. Including food.

Best regards,

K

@Wolf. Thanks for enlighten me.

I’m sorry that I asked the wrong question. It should have been asking “when will we see substantial economic growth coming from all this stimulus”?? Especially here i Europe. And subsequently some wage and price inflation.

One could fear that this QE is good for nothing – except asset prices

Yes, and asset inflation was, and still is, a manipulated market created by the US Treasury with the assistance of the Federal Reserve, aka Ben Bernanke.

asset inflation benefits capital holders.

wage inflation hurts capital holders.

wonder which inflation the Fed and FedGov worries about…

ding…ding…ding…step on up, your the winner….

To make it even more confusing, everyone has their personal ‘inflation’ rate. Most people don’t even know what ‘inflation’ is.

I’m living cheaper than I did 20 years ago.

The amount of bonds in the aggregate is overwhelming new issues. USG has not passed a budget, and probably won’t until 2020. The current bond market is the pricing mechanism. ZIRP will be with us for a long while, and when bonds need to correct, bond principle will be the catalyst.

Are you or your friends currently investing in Danish bonds?

I wonder who is buying .

https://www.bloomberg.com/news/articles/2019-06-19/in-land-of-sub-zero-debt-a-whole-yield-curve-may-turn-negative

Anyone or entity who holds the bond to maturity(someone has to)

is GUARANTEED to lose money .

Negative interest rates also mean that there is very little demand for money and low rates of return on investments.

Europe is going to have a moribund economy for decades. A secondary effect of a moribund economy is increased probability of social unrest. Added to this is the EU policy on immigration and the EU is a powder keg just waiting for a match

Has the Fed stated on which market they intend to sell their Mortgage Backed Securities (MBS) when the time comes? Because it’s not a matter of if but of when. Maturities are way too long and they still have way too many MBS on the books to count on refinancing alone to clear the balance sheet in under five years as they seem set on doing. That liquidity can then simply be struck off the books, meaning sent back to whence it came.

I think this puts an end to any talk of “QE Infinity” here and now and given payroll figures (and wage growth) the argument for another rate hike is extremely strong. 90% it will come to nothing but it also means any talks of rate cuts are wishful thinking at best and downright lunacy at worst.

Next up: Europe and Japan. Europe is where the US was in 2015 and Japan about six months earlier. Neither cannot avoid a stagnation but they can avoid a real recession (macrodata are easy to doctor… but the Devil is in the details, see China) if they can resist the temptation of igniting another 2017-style mini-boom and start down on the path of tightening before the end of the year.

I am not holding my breath, so I think I’ll just go out and buy another bike to add to the collection. A better investment anyway.

> on which market they intend to sell their Mortgage Backed Securities (MBS)

I believe that MBS are traded OTC (over the counter). Like, nobody trades less than hundreds of millions of dollars worth at a time, so it’s done the old-fashioned way with telephone calls between brokers.

I read an article about ten years ago about how it was actually a minor clusterfuck when the Fed suddenly wanted to start buying these things it had never bought before. Nobody working there knew how to do it. Quite a bit of scrambling.

B/c Fed had NEVER bought MBSs in it’s entire history since 1913! One can see the distortion in the global banking system in order to bailout the Banksters!

The principles of investment matrix is up side down! Bad news is good and vice versa!

First, the Fed has not yet stated that they will sell MBS. Instead they said “It continues to be the Committee’s view that limited sales of agency MBS might be warranted in the longer run to reduce or eliminate residual holdings. The timing and pace of any sales would be communicated to the public well in advance.”

When and if they do start selling, it will be in the same market they have been buying (and occasionally selling as part of small value exercises) which is called the TBA (to be announced) market. You can find out about the market at:

https://www.sifma.org/wp-content/uploads/2011/03/SIFMA-TBA-Fact-Sheet.pdf

MC01,

“Has the Fed stated on which market they intend to sell their Mortgage Backed Securities (MBS) when the time comes?”

The Fed has not said anything about the modalities of selling MBS. When it announced the new regime earlier this year, it only mentioned in one phrase that it might actually sell its MBS because the natural runoff would take too long. I’m sure Fed staff is pouring over this question right now. The last thing they want is creating turmoil in the MBS market.

Thanks for the replies (to all of you, I don’t want to spam the comment section).

Allow me to say my thoughts are with all you people in California due to the ongoing earthquake swarm.

Toxic waste, toxic debt, which is worse? Which will ruin the planet first?

I wonder if there are more dollars than bits of plastic floating in the sea, and which has the greater value!

Everybody knows that printing money is the key to prosperity.

Also, it’s the moral thing to do.

What took us so long ? We could have done this 30 years ago.

Why the emphasis to get rid of MBS so quickly?

Make private Freddie and Fannie once again?

######

“The action on MBS confirms that the Fed is eager to get rid of them as soon as possible. Its new plan calls for getting rid of all of them, even if it has to sell them outright if pass-through principal payments slow down too much,”

Why? Because the FED is primarily NOT a Housing Agency.

Had Congress not take over (nationalize) Fannie and Freddie, the Fed would not have bought PRIVATE securities, but they did so the Fed bought MBS just like they did other Government securities such as Treasuries.

What’s interesting is the Fed is holding only $5 billion T Bills, down from $100B and $50B. Wasn’t the idea to replace a certain level of pre-maturing (those paid off early) MBS for T Bills? How come the Fed has LESS T Bills now? The also have less MBS.

Iamafan,

“only $5 billion T Bills, down from $100B and $50B.” I read those numbers as millions, not billions. But yes, the amounts are down.

Yes you are right 5,000 in thousands is just 5 million. I get confused since the Fed SOMA holdings are grouped into thousands only whereas the Balance Sheet H.4.1 is reported in millions.

The Fed plan to replace the first $20 billion in MBS principal payments received with Treasury securities does not go into effect until October. At that time, up to $20 billion each month will “be invested in Treasury securities across a range of maturities to roughly match the maturity composition of Treasury securities outstanding” which means that all of it will be reinvested in Treasury notes and bonds. The T-bills on the Consolidated Statement of Conditions are only from “small value exercises” that the New York Fed conducts for practice (the NY Fed is a weird place where $5 billion is a “small value”). In October the Fed will go back to rolling-over all maturing Treasury notes and bonds, allocating the purchases in proportion to the size of the new Treasury offerings of notes and bonds issued on the maturity date.

For the Fed, MBS are a hassle because the principal pass-through payments are erratic. And the market for MBS is not very liquid and not nearly liquid enough for the amounts the Fed has to move around. In addition, the securities are not useful in conducting monetary policy. The Fed has stated these reasons for getting rid of the MBS, and those reasons make sense to me.

Wolf, I have a question.

Why are foreigners loading up on GSE securities?

Looking at the last TICDATA Transactions release:

https://ticdata.treasury.gov/Publish/s1_99996.txt

It looks like foreigners have bought about 75,415 (in millions) or more than $75 Billion of NET GSE securities from Jan to Apr 2019.

If the Fed is reducing their MBS, why are foreigners loading up?

What are they seeing?

I’m not even going to try to divine what foreign investors are thinking. But the MBS market is now dominated by GSE issues, and it’s big, and these bonds pay a slightly higher yield than Treasury securities and carry explicit or implicit government guarantees. So there are reasons to own them.

Iamafan, I think foreigners are loading up on MBS because they have better yield than Eurozone govt bonds and USG bonds (sometimes).

Also, I think Fed is unloading GSE(*) MBS because they are about to lose a lot of value and Fed does not want to be stuck with them. Nobody seems to talk about this possible explanation.

Remember what happened in 2008 after many foreign investors loaded up on private label MBS? Those MBS went to heck. This time it is GSE MBS that will go bad, I think.

(*) As always, I feel the need to point out that Fannie and Freddie are GSE and ARE NOT GUARANTEED by USG. Only Ginnie is a true agency and guaranteed by USG. The term “agency MBS” is used fraudulently every day by Wall St.

Fed not interested in buying Treasuries and helping interest rates drop further.

Fed selling MBS because it knows there will be a need to buy huge amounts of MBS down the road when housing fails again.

(in thousands)

Month-over-Month As of June 26, Note and Bonds Change -8,186,334.2

Week-over-Week As of July 3, Note and Bonds Change -15,000,000

Month-over-Month As As of June 26, MBS -22,679,108.6

Week-over-Week As of July 3, MBS – No Change

So yes, they are still cutting. But that will change in August, since, there’s a lot maturing to reinvest.

Iamafan,

“Week-over-Week As of July 3, MBS – No Change”

Yes, but that is how it always is: one or two weeks of no change followed by one or two weeks of big changes. The chart below shows the weekly MBS balances over the past year. I marked the week you’re referring to:

Yeah and 22.3 billion is a big number.

What surprises me is HOW the Fed intends to replace the maturing MBS with T Bills.

Since I can’t add up the SOMA purchases in auction reports to 100, 50 and down to 5 million, it looks like the Fed is simply taking maturity payments directly as T Bills from the Treasury or Fannie and Freddie. I can’t find another explantation.

The payoff money is destroyed except for the amount over the Designated cap as stated:

“If the amount of Treasuries that mature in a given month exceed the cap, the Fed reinvests the overage in new Treasuries. Under the Fed’s new regime, the maximum amount of Treasury securities allowed to roll off when they mature was $15 billion in June. And that’s what happened.”

Perhaps all of the 6 billion (21b-15b from June has not been put to use buying treasuries yet.

> In the current balance sheet, it lists $5 million, with the first batch maturing on July 9, the second batch in August

Should that read 5 billion?

Nope. H.4.1 is in MILLIONS of dollars.

Therefore, a million, million is TRILLIONS.

On the CUSIP level, it is reported in actual dollar value.

You can check actual SOMA reinvestment amounts to the exact dollar at every treasury auction announcement.

The Fed report on SOMA holdings is in thousands.

For July the reported maturing TREASURIES is: $21,399,179,700.0 or $21.339 billion.

MBS is a different matter since that is PASS-THROUGH and borrowers can prepay their loans.

On the 3rd of July:

4 week Treasury investment rate was 2.251% (taxable)

IOER was 2.35%

The Effective Fed Funds Rate (the rate banks trade reserves at the Fed) was 2.41%

SOFR (Secured Overnight Repo) was 2.56%

So the favored banks make more than Joe Blow short term.

What’s wrong with this picture?

It takes up to two months for reinvestments of MBS principal payments to close and be reflected on the “Mortgage-backed securities” line of the Consolidated Statement of Conditions. For example, for the last month before balance sheet reduction began, September 2017, the Fed reinvested $26.486 billion, in 470 transactions that had trade dates from September 15th to October 11th but settlement dates from October 12th to November 20th. The to be announced market only has three settlement days each month. Portions of $3.0 billion that the Fed is reinvesting for June may close on July 15th, 18th and 22nd and August 13th, 19th and 21st, so all of the reinvestment may not be reflected on the weekly Consolidated Statement of Conditions until the one released on Thursday, August 22nd.

Starting in October the first $20 billion of MBS principal payments will be reinvested “be invested in Treasury securities across a range of maturities to roughly match the maturity composition of Treasury securities outstanding”.

This page:

https://www.newyorkfed.org/markets/ambs/ambs_schedule.html

supposedly has the schedule.

June 14, 2019 – July 12, 2019:

The Desk plans to purchase approximately $3.0 billion in its reinvestment purchase operations over the noted monthly period. The next release of tentative purchase amounts in agency MBS will be at 3 p.m. on July 12, 2019.

Note the last purchases had much smaller amounts, about 220-300 million per month.

The largest purchase was approximately $44 billion on September 14, 2016 – October 13, 2016. It has gone down considerably (by a lot).

I wonder where the housing money is gonna come from.

I also wonder if the retirement of Simon Potter (Head of NY Fed SOMA) was hastened by the end of normalization.

Yes, that page is my source. A link is provided to a spreadsheet with the details of all the transactions made for the month including the settlement dates. The information I provided for September 2017 came from the spreadsheet for that month. By the way, the reason that the periods run from about the middle of the month is that since the New York Fed is the agent for Ginnie, Fannie and Freddie, they know by the middle of the month the amounts the Fed will receive by the end of the month.

When the normalization began it was anticipated that the principal payments, which mostly come from prepayments, of MBS would never exceed the $20 billion maximum reduction in reinvestment. That was true for the months from October through May but by June rates had unexpectedly dropped low enough that homes were again being refinanced (and more were being sold) so payments exceeded $20 billion. The investments between October and May were “small value exercises”, not reinvestment of principal payments. (Only at the Fed is $300 million a “small value”.) One of the reasons for the exercises is the introduction of the new “Uniform Mortgage Backed Security (UMBS). Initially only Fannie Mae securities are included but Freddie Mac issues will be modified to more closely match Fannie so eventually either Fannie or Freddie UMBS can be included in the same TBA trade. I’m not sure about Ginnie Mae (the sister that stayed home — Ginnie is a government agency not a GSE).

The Fed stopped making additional investments in MBS in October 2014 so I would expect that “where the housing money is gonna come from” will be the same sources that have supported expanded mortgage lending for more than the last four years. Don’t forget that the liability side of the balance sheet has also been declining. Since balance sheet normalization began depository institutions (thrifts and credit unions as well as banks) have reduced excess reserves by $787 billion. Over the same time deposits in transaction accounts at the depository institutions increased by about $516 billion. That $1.3 trillion had to be invested somewhere.

I suspect the Simon Potter left because, while the regional Federal Reserve Banks set their own salaries and pay better than federal civil service, the top pay at the NY Fed for 2019 is $252,200. By comparison, the Chief Wholesale Banking Officer at the 50th largest bank in the U.S. received total compensation of $1,230,583 in 2018.

– And in spite of this tightning the ETF called JNK (junk bonds) kept rising. The yields on T-bonds kept falling. What do you mean “Quantitive Tightning” (QT) ?

– In spite of the nonsense that’s being spouted in the media, the fact remains that QT is NOT “tightning”.

Large deficits are adding more money than the Fed is removing.

Corporates are solid, despite the hysteria, it’s the treasury bond funds which are under distribution, investors are using the rally to unload shares. Government is broke and fiscal stimulus is not happening. The accompanying rise in rates outside the US did not happen. Fed can drop rates and still maintain a premium over foreign yields. Purchasing power of the dollar in steady decline, makes foreign bond buyers nervous, Weimar inflation in assets. Bond investors will drop the bid, USG will set interest rates too low, and they will break the bond. The dollar will follow. Falling dollar value in forex, means dollar is worth more, and there is your tightening.

QE untwisting makes no sense when the US has to pay higher interest rates on their debt assuming interest rates will go up in the future. With these extremely low interest rates, it makes sense for the government to sell long term bonds to finance its debt, unless they plan to drive interest rates below zero.

Do you know how the reinvestments are suppose to happen. Tracking maturing Treasuries are easy. But what about MBS. I don’t think the NY Fed has explained it.

Hey Wolf, maybe you can answer this for me – I can’t find an answer to this question.

What would Treasury yields be at the long end of the curve if the Fed were not running its QT program?

It would seem to me that if QT were stopped, 10Y and 30Y yields would have to drop to some degree. That would deepen the 10Y/3M pair inversion and probably also invert the 10Y/2Y pair. If QT had never been run, the first yield curve inversion would also have occurred earlier than 3/2019.

So, in the world as I see it, if free markets were totally in control of the long end of the curve, the yield curve would be even more deeply inverted today, and probably inverted for longer than a quarter now…

Wolf,

Here is a reference on the topic of the small ($5M, etc) T-bill transactions that Fed/FRB/FOMC have been doing. Since people have been asking about the topic I’m posting it here for reference:

———————————————–

he New York Fed undertakes certain small value open market transactions from time to time for the purpose of testing operational readiness to implement existing and potential policy directives from the Federal Open Market Committee (FOMC). The FOMC authorizes the New York Fed’s Open Market Trading Desk (the Desk) to conduct these exercises to test its operational readiness in the Authorization for Domestic Open Market Operations and Authorization for Foreign Currency Operations.

In connection with these authorizations, the Desk intends to conduct a small value Treasury sale operation, which will occur on Wednesday, May 15, 2019, beginning around 10:15 AM ET and ending at 11:00 AM ET. The sale will not exceed a face value of $50 million and will be limited to Treasury bills maturing between 3- and 5-weeks from the date of the operation.

As announced previously, this test is one of three small value exercises to test operational readiness for transacting in the Treasury bill market.

Results will be posted on the New York Fed’s website following the completion of the operation. The results will include the securities and total amounts accepted and submitted.

https://www.newyorkfed.org/markets/opolicy/operating_policy_190509

Thanks, I get it now. These are small value purchases and not part of SOMA reinvestments that are “bought” in Treasury auctions.

Let’s see if I got this right ,the people’s money in the treasury pays the fed at maturity, and the fed destroys the people’s money by not re-investing which is the reverse of the original Q.E. Is not the source or liability of this money the peoples taxes that are paid to the Treasury not the IRS or the fed? The impact on Every-Day person during the past 10+ years of this scheme are thus.They have been robbed of the natural rate of return on investment for their security in old age or infirmity, Denied fair compensation for labor. Endured de-basement of their money,and by the use of additional schemes transferred that loss into the cost of shelter. The effect of this scheme has greatly hindered ownership of basic shelter and has instead forced the people to accept the high rents of the schemers modern serfdom which has now become a generational pox on their innocent off-spring. Completely corrupted an already corrupt political system to insure this travisity be continued. Promoted usery financed schemes to enrich the political class . Devised education based schemes and shelter ownership schemes that offers loans that cannot be paid back and then remove the protection of bankruptcy.The words of the post are benign to the ear but their impacts have bevastated Every-Day man and women .

Pottersvilles are the rage of modern day fed serfdom…..don’t forget to wink to PE, Hedge, Foreign PE and Shysters who get homes for pennies on the dollar and rent them in a scheme to all the serfs until broke…..

its a wonderful life in 2020 huh

I ponder the notion that the entire bond market has become a much more complex casino and the bets up and down literally make no sense at this point and thus valuation is not predictable. I would bet the average person interested in bonds have very little understanding of IRR, CTD and the treasury future game and how that relates to bets with collateral. I assume this mess will implode, because the super smart guys never fail to screw up.

From CME:

In years past, it was commonplace to evaluate the volatility

of coupon-bearing securities simply by reference to maturity .

But this is quite misleading . If one simply examines the

maturities of the current 2-year note and 10-year note, one

might conclude that the 10-year is 5 times as volatile as the

2-year .

But by examining durations, we reach a far different

conclusion . The 10-year note (duration of 8 .794 years) is only

about 4-½ times as volatile as the 2-year note (duration of

1 .978 years) . The availability of cheap computing power has

made duration analysis as easy as it is illuminating …

I think the real issue here, is that this whole bluff, counter-bluff, counter-counter-bluff-bluff, etc., etc, etc., can drag on for decades, and it’s getting nauseating living through it.

I think most of us would like to see things break one way or the other, just so we can get it over with. (i.e. either get tight all-around, or just start super-printing as fast as possible)

The Fed is an enigma, but the 10Y chart isn’t.

The 40Y chart had a bubble and a bubble collapse.

On Sept 1981 10Y peaked @ 15.82.

On May 1984 10Y was @ 13.873.

The low in between, on Feb 2983 @ 10.218, is an important swing point.

Once the 10Y fell below the swing point, the 10Y made lower highs and lower lows for 30Y, until Oct 2018 !

A resistance line, on a monthly linear chart, is coming from Feb 1989(H) @ 9.323 to Nov 1994(H) @ 7.906.

The 10Y failed to breach resistance, until Dec 2016, a year and a half ago.

Since Dec 2008(L) @ 2.04, there is a shortening of the down

thrust.

July 2016(L) is nadir @1.321.

This month, on July 2019, the 10Y (L) @ 1.941 dropped on top of the resistance line . It came from Oct 2018(H), from above.

But the 10Y is an enigma :

1) A log !!! monthly chart show that the resistance line is currently around @ 4% and well above Oct 2018(H) @ 3.261.

2) TA 10Y weekly is Negative, telling us that the trend is down !

3) A new cluster of rates, between 3M to 30Y, formed a bottleneck,

possibly to start a new zone of crazy lower rates.

Or to jump on a spring board, with higher inflation.

Re: “These pass-through principal payments vary with movements in mortgage interest rates: Falling mortgage rates induce homeowners to refinance their mortgages, which means that their old mortgages are paid off, and the principal is passed through to the holders of MBS.”

Fed says: “… mortgages amortize and carry prepayment risk, the duration on the 30-year MBS is around 7 years and is thus more comparable to that of a 10-year than that of a 30-year Treasury or agency bond”.

I’m getting a strong feeling that the King of Debt is up all night playing with fire! Sadly, this MBS/debt thing is rocket science…

Also see: Tired of fetching water by pail, the (Sorcerer’s) apprentices (trump/mnuchin) enchants a broom to do the work for him (them), using magic in which he (they) is (are) not fully trained.

There are many misconceptions here about MBS pools. I worked on MBS many years ago, so I will try to address some of the misconceptions.

Creating MBS mortgage pools can be an extremely complicated process. Most pools are not a bunch of 30yr bonds waiting for pass thru money. Most MBS pools are a bunch of tranches in a myriad of maturities.

For example, I may want to buy a continuous stream of $1M in MBS that matures every 30 days. My MBS salesperson will be happy to chop up pools to include these tranches. The pools will be generating 15/30yr yields, I will pay for tranches paying 0.5% over 30day bills. My tranches will come from many MBS pools and will mature every 30 days. I will be making a premium over 30 day yields, but the pool is making a 30yr yield over the same 30 days. I make more, they make more.

An MBS pool will have a large number of tranches of varying maturities within the pool, all going to different customers. If you are wondering why the fed is going to shorter term securities, it is probably because the demand is in those maturities. MBS will tend to track treasury maturities because they are easier to price, but they also go ala carte for big customers. It really is a complicated business.

I think I get it.

The FED might sell MBS to banks.

Banks then repackage them into ? and sell them to the usual suspects.

In exchange the FED gives the banks something they want that being ?

Why? Because this is not Europe. the American FED is to make banks make more money.

Hmmm?

To get to its all-Treasurys goal, Dudley says the Fed should seriously consider outright sales of MBS to meet its monthly cap of $20 billion, which it rarely hits now. Last month, Fed Chairman Jerome Powell said on Capitol Hill that such sales were at the “back of the line” when it came the central bank’s thinking.

Regardless, the Fed’s shift away from mortgage bonds could present a risk for the MBS market if 10-year Treasurys — the benchmark for 30-year mortgages in the U.S. — fall below 2.25 percent, according to Walt Schmidt, head of MBS research at FTN Financial. Those levels could trigger an influx of supply as lower rates prompt homeowners to refinance their mortgages.

“There will be no Fed to sop up supply,” he said.

https://finance-commerce.com/2019/03/trillion-dollar-bond-dilemmas-emerge-for-fed/

Where best to put your dosh so as it doesn’t lose value over time? Personally, I’m opting for bitcoin as it’s most likely the only thing not in a bubble. Ironic or what!

This is hilarious. Thanks for making my day :-]

($ thousands)

30 year UMBS FNMA

2.5 4,881,798.5

3 218,227,648.9

3.5 215,600,741.5

4 132,832,402.7

4.5 29,923,644.9

5 8,808,637.5

5.5 3,754,437.7

6 542,760.1

6.5 56,392.3

UMBS FNMA Total 614,628,464.0

The largest type of MBS settled holding by the Fed is this 30 year UMBS FNMA.

Though they are all 30 years maturity, the interest (yield) varies.

I think this is what we mean by TRANCHES (difference in yields) in what the Fed bought.

I don’t think each tranche will mature faster than the other for the same type of MBS.

I’m not sure what pre-payment will actually do the “maturity” date and whether this is distributed uniformly.

Regarding whether I can invest in short term Fannie or Freddie MBS; this is what I saw that was maturing earliest in Vanguard:

Federal Home Loan Mortgage Corporation Callable 06/20@100

Maturity- 06/24/2022, Coupon- 2.150

I am not sure how you can invest in MBS, SHORT TERM, without intending to trade them.

The earliest maturing agency security that Vanguard sells is:

Federal Home Loan Bank maturing 11/15/2019 with a 1.375 coupon.

My simple mind tells me to just auto-reinvest in 4 week at Treasury Direct. At least the Investment Yield was 2.251% last week.

Please read my previous comment.

You are mistaken in your assumption that the tranches(slices) of the pool all mature at once in 30yrs, they don’t. The yields of the trances track treasuries plus a premium for the risk. The lower the yield, the faster they mature. The higher the yield, the longer is their term. Notice the highest dollar amount is concentrated in the middle range, maybe 5-10 year range. This is around the average life of this pool, the point at which most mortgages will have been paid off. As you go further out, there is less debt outstanding.

Are you sure you are not referring to CMOs? My family has been buying rather large amounts of these from banks and they are often pooled Agency MBS of various types. I shortest I can remember is about 2 or 3 years on average. I don’t remember buying them from Fannie or Freddie and they seem to be products of the banks already.

CMO is a type of MBS, not much different because you can create MBSs by segregating collateral any way you want.

This whole article and comments especially have left me literally “dizzy”!

“Simplicity Clarice. Simplicity!” (From Silence of the Lambs movie)

There’s a big seller of MBS, out there? I’m still digesting the locomotives stacked and piled high in the desert.

Wolf,

Thanks, as always, for keeping score. Much appreciated.

If the Fed wants to rid itself of MBS entirely why do they continue to buy them? Granted, it’s in small amounts lately, $200 million to $300 million per month. This is a far cry from the peak madness back in 2013 when they were purchasing more than $100 billion per month.

Purchases should have been suspended long ago.

The big purchases stopped. They were called “Reinvestment Purchases.” These small-scale purchases — the Fed calls them “Small Value Exercises” — have a different purpose and are not an indication of monetary policy but are considered “exercises” to test the system and keep it functional. By Fed standards, the amounts are minuscule. The New York Fed explains:

“The Desk conducts agency MBS small value exercises from time to time as matter of prudent advance planning by the Federal Reserve. The exercises are conducted under the annual authorization for domestic open market operations for the purpose of testing operational readiness. They do not represent a change in the stance of monetary policy, and no inference should be drawn about the timing of any change in the stance of monetary policy in the future.”

What we need to know:

(in $thousands)

On 22-Feb-17, the Fed held the highest amount of MBS = $1,773,621,269.9

By the end of June 2019 (June 26) the Fed only had = 1,532,726,162.0

In other words there was a reduction of 240,895,107.9 (thousands).

That is almost about $241 billion.

How did the Fed reduce this? They had a NORMALIZATION Program.

Starting Sept 20, 2017

Monthly Caps on SOMA Securities Reductions

Agency Securities*

Oct – Dec 2017 $4 billion

Jan – Mar 2018 $8 billion

Apr – Jun 2018 $12 billion

Jul – Sep 2018 $16 billion

From Oct 2018** $20 billion

*Applies to combined principal payments of agency debt and agency MBS.

**Once caps reach their maximum amounts, they will remain in effect until the Committee judges that the Federal Reserve is holding no more securities than necessary to implement monetary policy efficiently and effectively.

However, the Fed Pivoted. On March 20, 2019

Monthly Caps on SOMA Securities Reductions

Agency Securities*

Oct 2018 – Apr 2019 $20 billion

May 2019 – Sep 2019 $20 billion

From Oct 2019 $20 billion**

*Applies to combined principal payments of agency debt and agency MBS.

**The first $20 billion of any agency principal payments received will be reinvested in Treasury securities.

Any additional agency principal payments above $20 billion will be reinvested in agency MBS.

Before March, they were going to roll-off up to $20 billion MBS per month. But after March, starting October, the first $20 billion of MBS maturities will be used to buy Treasuries. The amount above $20 billion maturing will be reinvested in MBS.

The reason why these MBS actually mature is because they constitute pass-though payments and borrowers pre-pay their mortgages and not stay the 30 or 15 years their mortgages were designed for. Since the AVERAGE LIFE of an MBS is about 5.28 years, then in order for the Fed to keep the balance they intended to keep, only $20B was actually allowed to mature and any further amount was REINVESTED. It was the NY Fed’s Open Market Operations that bought the re-investments from the Primary Dealers (open market).

The actual holdings can be found here. (Excel):

https://markets.newyorkfed.org/soma/download/856/mbs

As they say when your that big you have to sell into strength…. Of which I’m sure a lot of people should follow/.

Isn’t this info about the Fed’s assets primarily interesting because of the value of the Fed’s liabilities. I know that the quality of assets is a serious issue to a bank, but even if we leave that aside for the moment, have Fed liabilities been reduced as assets are reduced? I ask because I have some in my pocket and wouldn’t want them to be devalued. Or is this a special bank where assets and liabilities don’t matter?

Fully,

The two largest liabilities on the Fed’s balance sheet are:

1. Currency in circulation (the stuff in your pocket you’re worried about), currently at $1.75 trillion. This just keeps rising with demand for paper dollars. This demand has been very strong, mostly from overseas. And banks have to have enough paper dollars on hand to meet this demand.

2. ” Excess reserves,” which is money that banks deposit at the Fed for liquidity purposes and to earn a return (interest on excess reserves = 2.35%). This is the part of the liability side of the balance sheet that is falling — and sharply so. It had peaked at $2.7 trillion at the end of QE in Dec 2014 and has now fallen by almost half.

So yes, asset on the Fed’s balance sheet will always equal liabilities plus capital. Assets are falling and liabilities are falling at the same rate. But within liabilities, currency in circulation is rising, hence excess reserves are falling faster than assets are falling, keeping the whole thing in balance.

“The Committee intends to conclude the reduction of its aggregate securities holdings in the System Open Market Account (SOMA) at the end of September 2019.”

-Don’t worry, the pain of liquidity withdrawal will soon be over.