The benefit of NIRP: There’s hell to pay – even the ECB admits it.

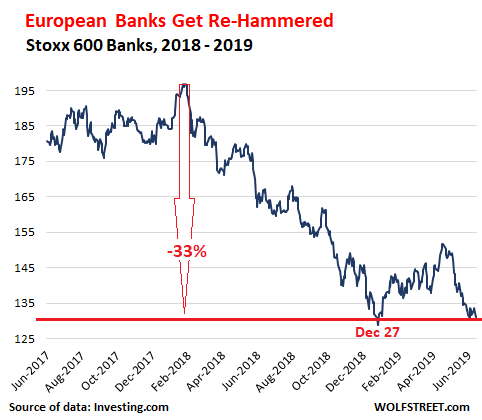

European bank shares – which have been getting crushed and re-crushed for 12 years – are getting re-crushed again. On Friday, the Stoxx 600 Banks index, which covers major European banks, including our hero Deutsche Bank, dropped to an intraday low of 130.5 and closed at 131.2, thereby revisiting the dismal depth of December 24, 2018 (130.8).

European banks did not soar on the first trading day after Christmas, unlike other stocks. Instead they fell further and hit their multi-year low on December 27 (129). The index is down 21.5% from a year ago and 33% from January 2018:

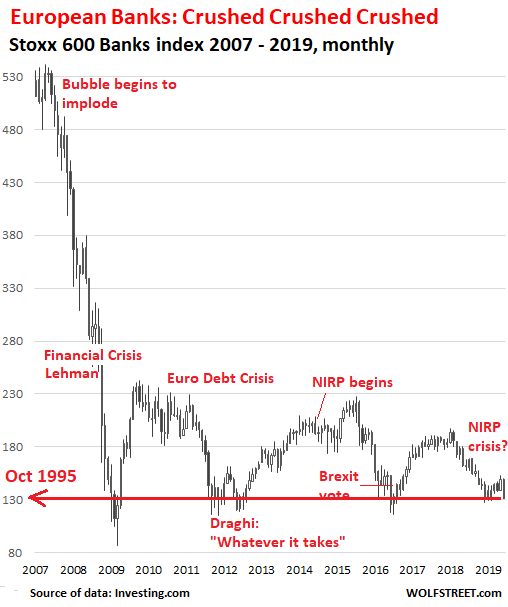

The notable thing about European bank stocks is just how brutally they’ve gotten crushed and re-crushed since May 2007, when, after a blistering bubble run-up, the Stoxx 600 bank index topped out at 534, having quadrupled in the 12 years from October 1995, during the euro bubble when only the sky was still the limit.

Over the twelve years since May 2007, the index has plunged 75%, and is now back where it first had been in October 1995. A confluence of factors keeps banging up these bank stocks, including:

- In mid-2007, euro bank bubble begins to implode.

- In 2008, the Financial Crisis hits. Also, housing market begins to collapse in Spain, Ireland, Portugal, Greece, et al.

- In 2009, euro sovereign debt crisis along with Southern European banking crisis starts.

- June 2014, ECB’s Negative Interest Policy (NIRP) designed to solve these problems hits banks.

- In mid-2015, Italian banking crisis resurfaces because nothing was fixed, and NIRP was making things worse.

- In June 2016, a majority of British voters checked the Brexit box, which caused the Stoxx 600 Bank index to plunge 21% in two days, the worst two-day plunge ever.

- In early 2018, Deutsche Bank and other banks begin to re-spiral down.

So, given these events, that 33% drop from January 2018 in the above chart is a minuscule dip in the long-term collapse-scenario going back to 2007. Buy and hold, indeed. Back to the level first seen in October 1995:

Part of the problem for European banks is NIRP, which was never designed to boost the real economy or make banks healthier so that they could support a vibrant economy. It was designed to boost bond prices and thereby bring yields down, which lowers the costs of borrowing for debt-sinner countries such as Italy, and allows them to borrow for free, which even Italy’s government can do with maturities of up to one year. But there is a price to pay.

The ECB released a paper in August 2018 where it admits that NIRP could cause a financial crisis because it’s terrible for many banks. This is the chilling abstract of the paper:

We show that negative policy rates affect the supply of bank credit in a novel way. Banks are reluctant to pass on negative rates to depositors, which increases the funding cost of high-deposit banks, and reduces their net worth, relative to low-deposit banks.

As a consequence, the introduction of negative policy rates by the European Central Bank in mid-2014 leads to more risk-taking and less lending by euro-area banks with greater reliance on deposit funding. Our results suggest that negative rates are less accommodative, and could pose a risk to financial stability, if lending is done by high-deposit banks.

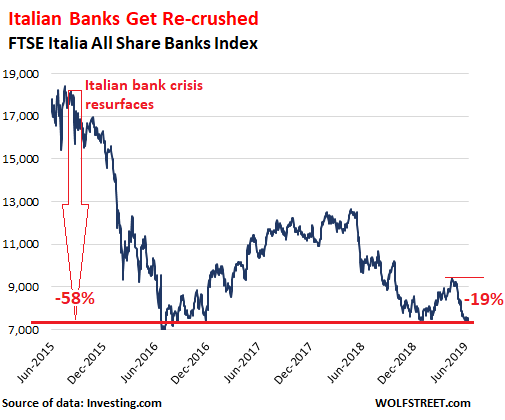

European banks have many other problems, including non-performing loans that after many years of jabbering about them still haven’t been cleaned up sufficiently, and that are now getting a new influx of non-performing loans. Italian banks are king of the hill in that department.

Several of the Italian banks have collapsed over the past few years and were resolved or bailed out, but the problems appear to have just been spread around rather than solved, and the index for Italian banks scampers from one hell to another. The FTSE Italia All Share Bank index fell 19% over the past two months and has plunged 58% since the Italian banking crisis has resurfaced in mid-2015:

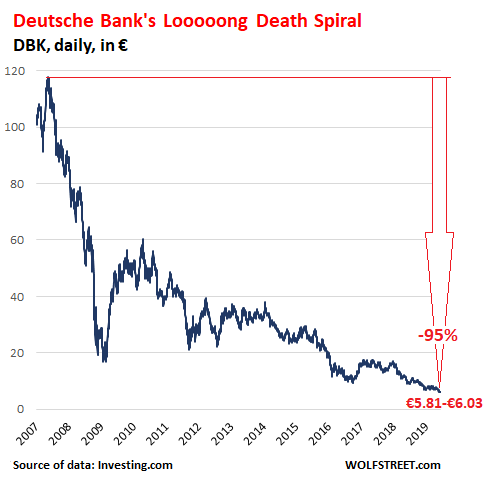

Our hero among European banks, in particular because of its size, is Deutsche Bank. It fell to a new historic low of €5.81 on June 3, and on Friday closed at €6.03. Its shares have now plunged 95% from the peak in 2007:

One thing is clear: Deutsche Bank will not be allowed to collapse in a messy way. It’s too big, and it would take down the German economy with it. It will be rescued in some way, but it is likely that any rescue will further destroy current shareholders and holders of junior bonds, particularly holders of bonds designed to be bailed in under such conditions, such as the contingent convertible (Co-Co) bonds that, when push comes to shove and regulatory capital falls below certain levels, can be converted into equity or can just be canceled. They’re now trading at 86 cents on the euro, pricing in some probability that it might get ugly for them.

The rate cuts for 2019 are a pipe-dream: Goldman Sachs and Deutsche Bank. Read… “The Market is Almost Always Wrong About What the Fed Will Do”: Chart

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Contrary to popular opinion, banks want normal interest rates.

They make money in taking in deposits and paying x interest rates and lending out that money at x + y interest rates. Impossible to do in ZIRP.

####

“Part of the problem for European banks is NIRP, which was never designed to boost the real economy or make banks healthier…”

2banana . Banks do NOT lend out the money they take in as deposits . When you ‘ deposit ‘ money in a bank you are landing the bank your money to use ( as it sees fit ) to run the bank . All money ‘ lent ‘ to customers is money created out of thin air by the bank when it makes a deposit in the borrower’s account which is the ‘ loan ‘ The depositer signs an agreement to say he/she will repay the loan with interest and that promise is the bank’s asset . The Bank of England confirmed that this is how the process works in its first quarter bulletin in 2014.

Bob Prechter also says this, the short answer is that bank depositors are ‘loaning’ money to the bank, and should the bank fail, you have lenders recourse. This is why they have FDIC. The implication being that USG can simply print enough money to pay off the depositors. If you are vaguely uncomfortable with the explanation being consistent with zero risk, you should consider that small differences in banking interest often reflect large differences in risk, such as the difference between MM funds and UST MM funds in 2008. The next crisis UST funds will protect your principle but the currency will be pulled out from underneath you (devalued). My grandfather got 10 cents on the dollar for his bank account in the 30s. Next crisis you will get NAV but your purchasing power will be downgraded more quickly that it is now. If that does not seem like hyperinflation or even 2% CPI it isn’t.

Very simple, I don’t trust banks. I only use them for payment processing and not to stash savings. My savings are with Vanguard and Treasury Direct. Both are linked to my bank account.

The greatest trick the devil ever pulled was to convince bank customers that they have “money in the bank”. They have only an IOU.

Iamafan, I am curious why you trust Vanguard? TIA.

With all this risk and NIRP; why hasn’t gold gone up?

Merkel 2012

“If Europe today accounts for just over 7 per cent of the world’s population, produces around 25 per cent of global GDP and has to finance 50 per cent of global social spending”

The so-called soft socialism of EUssr nations is just an illusion. EUssr nations are bankrupt, their economies are disintegrating before their very eyes and the promises of lifetime pensions, welfare and healthcare are nothing more than propaganda lies that voters willingly drink. In the end, they will have nothing and be much worse off. Such is the fate of a person who votes for the police powers of the state to steal from another to give them what they want but never earned.

Politics can promise whatever they want, but cannot mend the laws of fisics.

Time to tell the people what they’ve voted for 40 years is not feasible.

In a lie there are 2 culprits:

1 the lier.

2 the one who chose to believe the lie.

Both of them should face up the consequences if EU is willing to give a future to their sons and Grand sons.

I have just a couple weeks ago received my council tax bill here is SW London, UK. It is £2,700 for this year.

It says, 46% of the council’s expenditure is for “social expenses spending for needing adults in the council”. I read it a few times and it really means, 54% of us make money and the other 46% of council’s citizens leech off us taxpayers.

I would not dream of asking for a breakdown of the 46% figure on 1. citizenship of recipients or god forbid 2. how many years payments into DSS the recipients have made in preceding years, before hard times came along. Can’t be bothered to dispose of torched cars from my driveway or clean the isht from my letterbox, together with getting the obligatory “racist unct” sings slapped on my doorstep.

Merkel’s “socialismus”, based on perpetual robbery of low lying fruit targets, namely taxpayers with a fixed residential address, is not confined to the land of DB. It is the main engine of “GDP growth” in our free land of Brexit, too.

Go figure.

Oh Lordy, it ain’t the Germans or the EU suffocating the UK but your dear own tories and their ruthless criminal austerity. (The Germans have their own brand of austerity for Europe to pay hell for.) Brexit ain’t gonna save you from yourselves.

But it will be allowed to collapse in an orderly, efficient and Germanic kinda way?

####

“Deutsche Bank will not be allowed to collapse in a messy way…”

My guess is that in such an event, its shares will collapse and some of its bonds will collapse. My guess is that the bank will issue a large amount of shares and warrants to the German government, whereby the German government injects billions into the bank, and existing shareholders will be diluted to near-nothing. The government will end up with a big chunk of the bank and will likely force the bank to get rid of some divisions and clean up its books. So it would be orderly for Germany, and not so orderly for stockholders and certain bondholders.

Will the existing senior management be able to stay on and still collect their bonuses?

Well, the letter with the checks will probably refer to the Golden Parachutes of their departure deal, but they sure won’t be seen on street corners with signs that say that they Will Bank For Food.

√

Depends on how far left the coalition in power at the time is.

yepp.and even higher bonuses,for “fixing” db.problems….

2banana, “Will the existing senior management be able to stay on and still collect their bonuses?” Sounds like (legalized) organized crime to me ;-)

The elephant in the DB books is their derivative book which stands at over 1 Trillion Euro’s. Various statements from DB say that “most” of their derivative book is hedged, but when you “hedge your bets” someone else is on the other side of the hedge.

In the 2008 financial crisis it was suddenly discovered that those companies that “hedged” other peoples bets ie: AIG could not afford to pay when the time came. AIG had assets, but they could not be liquidated in a collapsing financial market and in the time frame needed to meet the calls, hence the large US Government bailout, much of which went from AIG to the Wall St investment banks so that in turn they could pay their calls.

If there is a “credit event” with DB then we will see exactly who was on the other side of the DB hedge. I doubt this will end well!!

You’ll recall that AIG bailout went straight through to the coffers of Goldman Sachs without any mark to market change to valuation. Straight through to the very culprits that created the market and then bet against AIG the insurer of the debt. God’s work.

You might recall Dylan Ratigan on CNBC at the time and thinking how come this guy is the only one telling this truth? Then he got fired.

Ohhhh. That’s why.

AV8R, Dylan Ratigan, yeah I remember him. There’s quite the telling scenario on https://en.wikipedia.org/wiki/Dylan_Ratigan in the subsection “Reporting” and “2011 speech” where he summarizes the behind-the-scenes skullduggery. I’m surprised that he’s still walking around a free man.

Great analysis, Wolf. You are the best and keep speaking out against all the hidden and unreported facts.

How many share and bond holders are themselves guaranteed institutions? So what does this wipeout matter? Japanification.

never forget, that SNB could take over DBK with „out of thin air created „ pocketmoney. germany (and the EU) would never ever allow this. DBK is a major player in the local payment system. to put it in a nutshell, bad for shareholders, but the bank itself will survive, so or so. all stories about DBK are nobrainers. btw, is DBK a primary dealer?

Any casino has its dealers, and Wall Street is no exception. Those dealers allowed to transact directly with the Federal Reserve are Primary Dealers.

And, yes, Deutsche Bank is a Primary Dealer. As were Bear Stearns and Lehman.

Banks will not capitulate until they have exhausted all the debt they can possibly create… at everyone else’s expense. At some point they will need to reset, wipe the books clean, and start over.

Yes that’s right – it’s all about the usury of the private banking sector, all the problems we have and have had since 2008.

Sadly people have been trained so well by propaganda to blame everything on state intervention and regulation [whereas in reality the debt/derivative problems have been caused of course by 30+ years of operation in a DEregulated financial environment] that they will still be parroting this line as we once again go over the cliff edge. led by the reckless greed of the finance sector.

Deregulated but given state guarantees

European banks have been trying to wipe their books clean for over a decade now. Look at how successful they have been. Do those look like the shares of companies that can alter reality merely by snapping their fingers like so many seem to believe? Ellon Musk can get a much better reaction merely by taking to Twitter, and it won’t cost him a penny.

European banks are closer to the Asian (stimulus-driven) than to the American (profit-driven) model in that they exist chiefly to stimulate economic activity above and beyond normal growth rates. That’s why loans extended to both incorporate and unincorporated businesses in Europe keep on shooting through the stratosphere no matter how laughable the business model they finance. I mean… there’s this company in Germany whose sole product is a little rubber mat you put underneath your dog or cat bowl. Who thought that was a brilliant idea worthy of being financed, presumably at record-low rates?

I often blast without mercy the Korea Development Bank for keeping zombies such as Korean Air and DSME alive and rolling into (plenty of) cash but are we really much different? This is not a matter of “bankers” making profits, it’s a matter of stimulating economic activity with no place in the real world.

Well said!

As the folks at Naked Capitalism have been saying for years and years, NIRP is exactly the same thing as ECB saying on Megaphones set at Maximum Volume:

We Expect Super Duper Massive Economic Contraction Of An Unprecedented Scale So Hoard All Your Money Never Ever Spend On Anything Ever Again And Prey You Can Afford To Live To Eat One More Day Before You Die From Starvation From Lack Of Currency.

They never learn – Magneto, X-Men.

Europe, which still behaves tribally, had a few hundred years of experience with individual countries (tribes) having individual currencies. When things got bad, rich guys moved their money out just in time for the devaluation, then they moved it back in. Rinse & repeat.

The EU has now blessed us with not-so-altruistic politicians, plus EU bureaucratic control freaks, plus a population absolutely drained by 200 years of almost continual war (from Napoleon forward), plus the single-currency (ie euro). This may have helped civilize Germany, but at incredible cost in almost every other dimension of society.

Now that EU’s (unelected) “leaders” have thoroughly beclowned themselves in front of the world (among other things, trying to supersede the USA economy and US dollar), it’s time to come up with a survivable process to leave at least the euro currency, allowing tribes to get back to their own currency and individual devaluations.

Italy, with a stagnate GDP of $2.3T is estimated to have an ECB Track II debt of over $1T (translated to the USA economy, that’s about $10T).

This would be laughable but for the magnitude of the risk to hundreds of millions of EU citizens (and the rest of the world).

“This may have helped civilize Germany”. Otherwise very much agree with your comment though on this point: let’s not forget that France/Mitterrand agreed to the German re-unification only under the condition that Germany join a currency union. The rationale being that this would sufficiently weaken a fortifying enlarged Germany.

As probably intended from the beginning, and contrary to the assurances given to and naively believed by the Germans, the Euro soon started its steady decent in value. Germans saw their multi-trillion pile of cash savings dwindle (pre ECB, a trillion was a very big number). Adding lost interest come with ZIRP, a collective loss of wealth into the hundreds of billions. Now that’s some losers!

Are painful losses civilising? Voting results point in the opposite direction: right and left wings dramatically strengthening, the stable post-war two-centre-party order demolished. A growing part of the votership willing to back anybody with a hardline anti-EU position.

Deutsche Bank shall not be allowed to go under. Money launderers have rights too!

[Excerpt from an June 7 article in the Washington Post by Tory Newmyer]

…The bank is already facing intense scrutiny from congressional Democrats over its ties to Trump’s business empire. It has been the only major financial firm willing to back Trump over the last two decades, after a string of bankruptcies rendered him persona non grata on Wall Street. It still holds $300 million in outstanding debt from Trump — and it continues to make headlines for allegations of misconduct and money laundering on behalf of its clients.

Much more interesting imho is which are the most “NIRP” vulnerable US banks?

Another nice piece on bashing Deutsche. I’m long DB. It is hard to ignore DB’s fundamental improvements. Let’s not forget TBVPS is almost $30 a share. TBVPS is a proxy that is used to determine liquidation value. The bank is sitting on almost 1T of cash, has 279B of liquidity and their Tier 1 capital ratios improve with each passing quarter. Let us revisit this discussion in 1 year and compare your short vs my long position. Now is the time to go long. The time to short this stock is over.

According to their own Q4/19 presentation they sat on 184 bill. in cash and cash equivalents. In Q1/20 they earned € 200 mill.

So where did those 850 bill. of cash come from?

Last time I looked they had just over €500bn in “depositors funds” and around €200bn in cash or cash equivalents at the Bundesbank. One assumes that the €300bn difference between what the retail banks clients have deposited and DB’s “cash in hand” is accounted for somewhere inside the Investment Banking division.

A very large percentage of the derivative book is under water and some of their maturities/obligations run for 20+ years.

My local bookmaker will cover my bet on the 2.30pm at Ascot next Wednesday, based on form and the Gods! but taking a bet on any event over 20 years time is just a non-scientific wild assed guess, but the guy who wrote the derivative will have had his bonus and retired long before the brown and smelly hits that rotating thingy on the ceiling.

Rinaldo and Covey:

That’s not a how a bank works. Here’s DB’s balance sheet in the most simplified and abbreviated manner (complete balance sheet linked below):

DB has €1.44 trillion in Assets — where the money went and where revenues and earnings came from. Here are 3 of its assets:

– Cash and “central bank balances” (deposits at the ECB mostly): €187 billion (13% of total assets)

– Loans outstanding: €410 billion (29% of total assets)

– Other assets €130 billion (9% of total assets)

DB has €1.37 trillion in liabilities – where the money came from, and where the cost of funding (an expense) came from. Here are 3 of its liabilities on DB’s balance sheet”:

– Deposits: €575 billion (42% of total liabilities). When you put $100 in the bank, the bank records this with two entries: a “deposit,” a liability of $100 (what it owes you, and that liabilities stays there until you withdraw this $100); and “cash,” an asset of $100, that the bank then invests, sends to (lends) the central bank for deposit, lends to a customers, or keeps at hand to be used later.

– “Financial liabilities”

– Long-term debt (bonds it issued).

Deposits are its largest single liability and its largest source of funding, accounting for about 42% of its total liabilities.

Assets have to be larger than liabilities. The difference is capital.

If there is not enough capital, the bank collapses. If too many of the assets (loans, etc.) are bad and have to be written off, eating up too much of the capital, the bank collapses.

We don’t know what the quality of the assets on DB’s books is. They include derivatives. We have NO IDEA what is buried in them. That’s where all the uncertainty comes from.

Details on pages 11 and 12:

https://www.db.com/ir/en/download/FDS_Q1_2019.pdf

It has less red than Tesla? That’s amazing!

Joking aside, when will this stop? Banks can’t keep going like this infinitely. Unless you want Europe to end with a monopoly were just five or four companies own all banks.

Not much has changed in the 40 years since I sat my banking exams, except the size of the numbers and the complexity of where those numbers come from.

As you say, we have no idea what is buried in the “asset” side of the bank. The Zero Hedge article today on the “bad bank” idea makes mention of a bunch of legacy issues ( €60bn est) that have been costing the bank some €500m per year in losses, and until John Cryan mentioned them, nobody outside the bank was aware of the issue. DB developed a taste for long dated derivatives, which should be profitable over the 20+ years of the bet. The problem comes when those positions start to produce losses which might go on for 20+ years

How do you value a derivative that is loss making and has 10-15 years to run!!

Wolf

No worries, I have a pretty good idea of how banks work. My remark was a reply to BUTLER FOR YOU, who claims that DB is sitting on 1 Trill. cash pile.

If you went long DB at Fridays €6 per share you stand a good chance of making some money.

Ten years ago DB was at €20, rose to €60 and then wilted down to its present value of €6. An ideal opportunity to lose some serious money.

BUTLER FOR YOU,

I’ll take the other side of your proposition. We shouldn’t turn WOLF STREET into a betting parlor, so it’s your forecasting reputation vs mine; we’ll check back on Fathers Day 2020 to see how DBK does.

After 11-12 years of an almost straight-down 95% loss of valuation, one would certainly hope DBK had hit rock-bottom…but investors obviously don’t believe management’s opinion of asset quality, boilerplate TBVPS calculations, regulatory compliance or turn-around strategy.

My view: At this point, vultures are lurking in the trees to see how the EU or German state (AKA taxpayers) recapitalize this turkey. The following state actions invalidate the bet: MATERIAL ECB and /or GERMAN STATE RULE CHANGES, CAPITAL INJECTION, DEBT-TO-EQUITY CONVERSION, MERGERS WITH SMALLER HEALTHY BANK(S) or FAVORABLE PURCHASE OF DBK “BAD ASSETS”.

PROPOSITION: 06/14/2019 DBK.F market cap of $12.54B will be lower on Fathers Day 06/21/2020

TRACKING METRIC: DBK.F (Frankfurt) market cap in USD

– DB shrank, the new smallness is the result of the failed “ether” DB traders.

– In the last x3 days, SPX daily candles shrank to the smallest size

on the chart. They look like miniature candles.

SPX, after breaching a very important swing point, from May 2(L)

@ 2,900.50, – the day day that followed the all time new high, – is

currently taking a break to fill the tank, to get few cups of strong coffee, before moving on.

– When the SPX breached this important swing point @ 2900.50, it

was a thud, a small upthrust.

– In the last x3 days, SPX is under the 2900.50 line, but above the

dma50 and the Buying Climax of Jan 26 2018 peak @ 2872.87.

– There is an important debate what the market will do next.

– – Some people think that the SPX will jump to a new all time high,

just 67 points above, showing its strength and extended power.

– – Other view the June 11(H) as wall street tech guy work of art, bringing the chart to a point just 2% below peak, before the mark down start.

– During the summer time, the chart will move to the right and the

markets will do what they are suppose to do and nobody can stop

the next move, not the Fed and not Trump.

“Much more interesting imho is which are the most “NIRP” vulnerable US banks?”

Even more interesting to individuals (most of whom are ignorant about it) how and to what extent are we vulnerable?

To add to this Gigantic (“Titanic?”) Comedy Farce, I suggest that the government of Germany re-capitalize Deutsche Bank by transferring the German Target 2 balance to Deutsche Bank, in exchange, perhaps, for a new issue of bonds. Thus the Uncollectable becomes the asset of the Uncreditworthy.

That should boost the price of Deutsche Bank shares, and prove, once and for all, that the Germans do have a sense of humor.

my mother is German….sense of humor? maybe not so much , but they do appreciate irony…..

Brilliant idea, should propose it to Weidmann.

AI, Your suggestion that “the Uncollectable becomes the asset of the Uncreditworthy” is pure ironic gold. In my book, you are giving Chip a run for his money.

Morning Wolf readers.. HFD… Good article.. As featured in “The Big Short” the world’s bag holder of CDS is DB. Never got fixed and therefore cannot be allowed to implode. More can kicking..

“One thing is clear: Deutsche Bank will not be allowed to collapse in a messy way. It’s too big, and it would take down the German economy with it.”

Could the collapse of Deustsche Bank trigger another Lehman moment and trash the global economy? Isn’t Deutsche Bank intertwined with the global economy via trillions in derivative contracts?

I don’t think merely ‘saving’ the bank would be enough to calm the markets.

DB must survive because of its wide global exposure as well as the domestic retail market, so let’s all first agree this point.

Two things need to happen;

1. all DB bad loans, underwater derivative exposures and the like must be transferred from db books to the german government/taxpayer

2. once this is completed db can now issue convertible bonds and apply raised funds to reorganise the bank and reduce their headcount in particular at the MD level.

As a previous DB Director who is passionate of the 150 y/o bank, provide the Board the resources to succeed instead of bringing what was once the envy of the financial services industry down. Bank of America and Goldman Sachs should have also failed, DB needs a lifeline, the share price will rise, investor dividends will recommence, german taxpayers will get their money back. DB has some great people but it also has a lot of baggage it must eject, those self serving, machiavellian managers need to be moved on and allow internal fresh blood to rise from within the DB ranks and focus the bank on the path of sustainability. I promise you it can be done!

Amazing suggestion, “All DB bad loans must be transferred from DB books to the German government.” A criminal act akin to the US TARP in 2008.

It’s quite bizarre that the MSM has managed to brainwash the masses into accepting such moral hazard and destruction of their financial futures for the benefit of some bankers’ hides. Sheeple indeed. The bankers must be saved at all costs.

Certiainly hasn’t worked betting in ‘new blood’ in terms of the challenger banks in the UK, a promised ‘new dawn’.

Greed is greed is greed, and greedy people are attracted to working in the world of finance.

Nothing’s ever going to change that. You just swap greedy 50-somethings for greedy 20-somethings…

Rah efiin’ rah.

Update:

Doug Watson,

You are definately a banker with:

“DB needs a lifeline, the share price will rise, investor dividends will recommence, german taxpayers will get their money back. DB has some great people ”

Didn’t Gordon Brown tell the UK tax payers that?

It’s really astonishing to me just how disproportionately huge the European banking systems are. France, Spain, UK, Germany, Portugal, the Netherlands, and Switzerland each have net banking assets of more than 300% of their respective GDP, and believe it or not France leads the way with more than 400%. For comparison the US is only at about 100%. That takes too big to fail to a whole new new level. Here’s a graph if anyone’s interested in seeing the big picture. Granted it’s from 2013 but I doubt it’s improved since Europe has largely stagnated since then and they don’t seem to have delevered.

https://www.zerohedge.com/sites/default/files/images/user5/imageroot/2013/05/Global%20bank%20assets%20%25%20of%20GDP.jpg

Don’t understand how US banking stocks can rise without regard for the NIRP that the stock market so anxiously awaits. It could be that (secret) rate hikes are waiting around the corner? Rates high enough to kill of the already anemic rate of bank lending would certainly be much more difficult for banks that zero rates. There is no goldilocks for this group, and no policy to reign in shadow banking practises, or bad corporate debt. In the runup to 2007 weren’t they promoting Fannie Mae as bulletproof? GSE guaranteed?

The Fed has taken NIRP off the table. “Zero lower bound” (policy rate of just above 0% = lower limit) is in all its scenarios, not NIRP. The Fed does not like the side effects of NIRP. The Fed works for the banks, and banks have a problem with NIRP, as you can see.

According to shadowstats and the Chapwood index, nitpick is already here in a big way, whether they call it that or not.

When interest rates go negative, it is no longer an economic system, and economic fundamentals no longer apply.

The economic system today is like a jet aircraft that is not aerodynamic and cannot fly. If you have a fast enough computer to control the thrust and control surfaces you can get it through the air, but even a minute failure of any system gives catastrophic almost instaneous results.

Those going long DB much braver than this observer.

If DB is such a fine risk play, why then is the company proposing the cordoning off of yet another “bad bank”? The company went this route before (back in 2012) to rid itself of 125 billion euros of “non-core” assets and booked nearly 15 billion in losses after winding it down. This time it’s ONLY 60 billion euros in assets but might take much longer to wind this one down if this includes many longer-dated derivatives.

In Q1 of this year, the company earned 1.3% ROE. Leadership is promising to get that to 4%, which is still pathetic. DB will get nowhere near that level unless the ECB raises rates dramatically. Seems unlikely but Draghi is gone in just a few months so who knows what his successor will propose.

Any meaningful rise in Euro interest rates is unthinkable as it would soon be followed by wholesale collapse of Southern Europe’s private and possibly at some point also public sectors.

That reliable indicator of the establishment’s plans for us, The Economist, is cheerleading for Erkki Liikanen as next ECB head. His main attraction being his vocal support for “unconventional measures”. He won’t raise rates, he will take Euro money printing to a new level.

With regard to Erkki Liikanen as next ECB head.

I wonder what he will discover taking over from Mario Draghi knowing Mario Draghi’s banking deals/relationships in the past.

You spoke to soon re the 4% profitability target! :)

—

Market Chatter: Deutsche Bank Temporarily Cancels 4% Profitability Target for 2019

17 Jun 2019 15:04 ET

03:04 PM EDT, 06/17/2019 (MT Newswires) — Deutsche Bank (DB) will cancel its 4% profitability target for 2019, Handelsblatt reported on Monday, citing two sources familiar with the matter.

The cancellation of the target is only temporary, as the bank expects higher returns achievable as a result of its planned restructuring, the report said….

MT Newswires

Nice to see stocks fall on bad earnings and bad news unlike their American counterparts which rise on bad earnings and all bad news.

Bear in mind that DB survived WWI and WWII (modulo break-up and re-unification). That’s not to say it would serve to be its shareholder.

In my opinion, Deutche Bank is more like an investment house with lots of tentacles and not really a retail bank with Mom and Pop depositors. In fact, you’ll likely bump into them in other countries more than Germany. Given what I said, what makes them any different from Lehman?

Right now my current average share price is at 6,22 Euro and I will commit even more capital in $DB if there is another significant all time low! PS: When it comes to profits DB is going through a restructuring and hardly showing any, but it’s reaffirmed 2019 guidance does imply a 2.4 billion EUR net profit. Furthermore, when you consider that the EU interest rate environment won’t last forever I do think that DB is currently a screaming buy. Long DB

So with all this risk with banks with regard to shareholders and savers; why hasn’t gold increased in value?

In Switzerland, we have negative interest rates of 0.75%.

In Switzerland we have personal tax on capital (includes bank deposits) of 0.2%.

As a result there is a waiting list of 2 years for bank safe deposit boxes and a shortage of 1,000 chf notes (1chf is approx US$1).

There is a funny country – economy is growing 3-4% a year and lots of swiss and german taxpayers like to retire to this country. Eur has devalued in a year a whopping 12% there plus natural inflation there.

There is a really bright future for european retirees – yes, EUssr delivers their pensions no problem but…with some hefty tax. At the same time there is clamoring about EUR inflation rate not hitting the target – from the other side of the globe they seem to hit it fine

You can smell the fear – Merkel uncontrollably shaking today.

The solution will be taxing cash by implementing an exchange rate between paper and digital currency and allow paper currency to depreciate relative to digital currency. It is as simple as that.