Stock market and corporate bond market are in la-la-land, pricing in an economic boom. They’re not seeing a rate-cut economy. So why would the Fed?

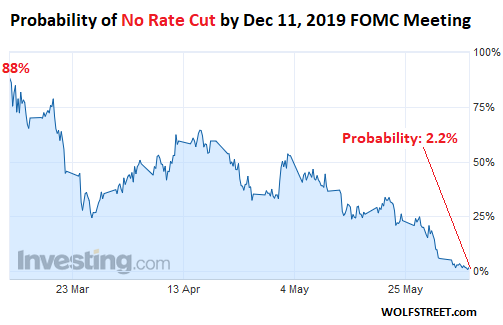

Granted, Wall Street always wants rate cuts, no matter what. But this is getting funny. The probability of three and even four rate cuts by December 11 are suddenly gaining the most favor in how the market are betting on 30-day Fed Fund futures. And the markets are now pricing in practically a zero-percent chance – currently a 2.2% chance up from a 0.8% chance yesterday – of no rate cut by December 11, the day of the Fed’s post-meeting announcement and press conference.

In other words, the market is betting there’s just a near-zero chance the Fed’s target for the federal funds rate will remain at the current range between 2.25% and 2.50% (chart via Investing.com):

Markets were very wrong about this in 2018. In early 2018, the probabilities were stacked for only two rake hikes that year. But the Fed was able to “gradually” walk markets toward the expectations of four rate hikes, and other than yields adjusting upwardly there was no huge reaction in the market – until suddenly there was, starting in October, when the bottom fell out of the credit market and the stock market. This lasted through December 24, by which time the Fed had started to walk markets back from the brink.

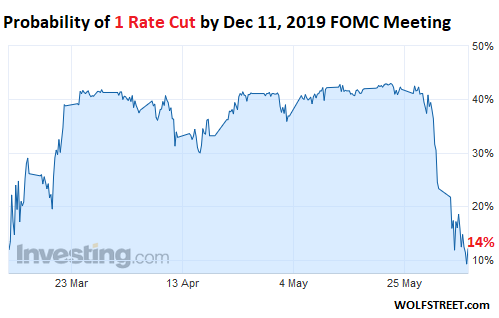

The chance of only one rate cut by December has collapsed to only 13.6% at the moment, according to bets on 30-day Fed Fund futures. That probability had hit a low of 8.8% yesterday. One rate cut would bring the Fed’s target to a range between 2.0% and 2.25% (chart via Investing.com):

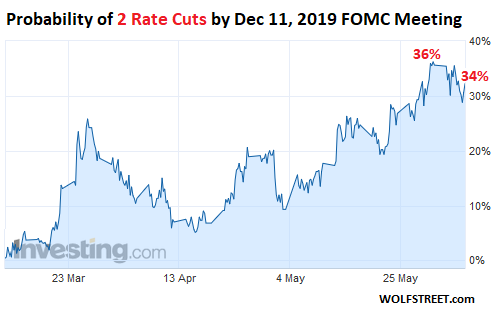

The bet on two rate cuts by December 11 is getting more popular. This would bring the Fed’s target down to a range between 1.75% and 2.00%. That probability had jumped to 36% by the end of May but has since ticked down to 34%, under pressure as three and four rate cuts are drawing more bets (chart via Investing.com):

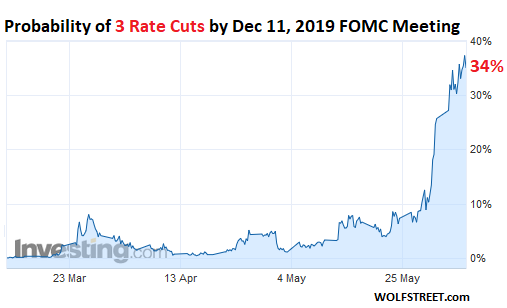

The probability of three rate cuts by December 11 has now soared to 34% at the moment, up from about 0% chance in early May. Three rate cuts would push down the Fed’s target for the federal funds rate to a range between 1.50% and 1.75% (chart via Investing.com):

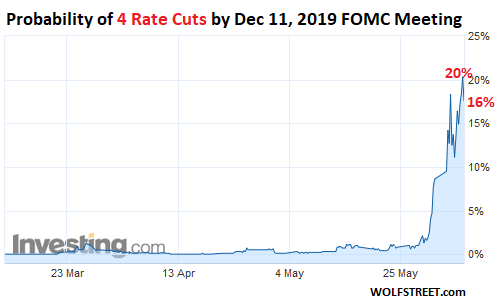

Ha, and even four rate cuts by December 11 – I mean, don’t laugh – has skyrocketed from nothing as recent as May 23, to 20% yesterday, though it has ticked down to 16% at the moment:

But here is the thing: The stock market is near its highs and is predicting boom times forevermore. During a downturn of the type that would induce the Fed to cut rates, corporate earnings collapse, revenues fall, PE ratios go to heck, and over-leveraged companies begin to default on their debts, which tends to wipe out shareholders. Economic downturns can be terrible for stocks that have been inflated like this and priced way beyond perfection. But there are no signs yet that the stock market, which is supposed to be forward-looking, is pricing in any of these risks. It’s gallivanting around in la-la-land.

The corporate credit market is sanguine. Junk bonds too are once again in la-la land. Junk-bond yields are low, given the risks. And yield spreads – the difference between junk bonds and Treasury securities – are still narrow though they have started to widen a tiny bit, showing that the corporate bond markets, like the stock market, is seeing an endless boom. Junk bonds get hammered in a big way when the economy turns south because in a downturn these over-leveraged cashflow-negative companies are suddenly grappling with existential problems. But that’s not happening yet.

In terms of the economy, first quarter GDP grew at a rate of 3.1%, the best Q1 since 2015. Over the past 13 years, there were only three years with higher first-quarter GDP growth rates (2012, 2013, and 2015). But there were four years when GDP declined in Q1 (2008, 2009, 2011, and 2014). So Q1 2019 was pretty good. Not a lot of data has come in for Q2 yet. So far, it looks a little weaker than Q1, but OK-ish.

Unemployment claims are bouncing along multi-decade lows. The labor market is a heck of a lot better than it was and is the strongest in years. Manufacturing is still growing, if barely, and growth is slowing and might turn negative, but it’s only a small part of the US economy. Services, which dominate the US economy – finance and insurance, healthcare, professional services, information services, etc. – are growing at a decent clip.

Consumers are making more money and are spending more at a decent clip. Consumer confidence is high. Government spending is growing in leaps and bounds, which stimulates the economy too.

So neither stocks nor riskier bonds are seeing a recession. And yet a different end of the market – the one that bets on Treasury securities, Fed Fund futures, and the like, is betting on three or four rate cuts over the next six months.

Based on what? That pressure from the White House will trigger a political panic at the Fed? Could be. But it could also just be market delusion.

Some people are hanging their hat on “low inflation.” Inflation is ticking up again, but as painful as it already is for many people, it’s a little below the Fed’s 2% target as measured by core PCE (1.6%). So maybe the Fed should choose a different inflation measure. One step up might be core CPI (2.1%), in which case the Fed would already be above its target. But there is not a whole lot else to hang your hat on for rate cuts.

I’m not sure how this circus will turn out, but if those three or four rate cuts that are now increasingly being priced in and taken for granted in some parts of the market don’t materialize by December 11, 2019, and if the Fed can’t figure out in a New York minute how to walk markets back “gradually” from those expectations, you might want to fasten your seat belt.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wolf,

I know predictions are ridiculously risky and next to impossible to accurately do year after year – but Robert Rapier does this (for any number of years now) and sort of keeps things along a couple different vectors where his expertise lies. He puts up new ones at the end of the year and posts new ones at the begining (approximately).

It would be fun to see something like that from you – clearly you have experience and insight so it would be a way to communicate that and maybe make a sport out of it.

Here is the action from this new year:

http://www.rrapier.com/2019/01/grading-my-2018-energy-predictions/

http://www.rrapier.com/2019/01/my-energy-sector-predictions-for-2019/

So, if you see some trends at year end you are confident will work out the way you see them within the next year, it would be fun to see your list.

Anyway, nice to see a prediction like this, which is sort of an opinion you put your brand on (so to speak)!

Regards,

Cooter

I like this regarding the market: ” It’s gallivanting around in la-la-land.” Haven’t heard (or read) “gallivanting” in a while. Nice word. Sort of implies decadence.

Simple, Sell at the Rally , Any and everything above Dow 26,000 !

And then Stay away and don’t put anything back in !

Hah! You’re funny. Here’s a prediction for you: there will be one rate cut this year. The Fed will cut rates once, by 3.50% to lower the FFR to -1.00%.

The Fed will need to start creating an additional $200 billion per month to fund all of stuff Americans want Trump buy for us (wars in the Mid-East/Persia, Aircraft carriers, border walls, moon missions and on and on…). We can buy all these wonderful things and more just by having the Fed create an endless supply of money. We never have to increase taxes to pay for stuff so let’s spend, spend, spend our way to prosperity.

We are the deciders, if we tell the world the dollar has value then the dollar has value – anyone who thinks different will feel our wrath, you are either with us (supporting our fiat currency) or against us and you don’t want to be against us.

I no longer work, I’m a patriot. My government and my Fed will provide for me. My country is the world’s only super power and controls the world’s reserve currency so they will print what is required to take care of me.

Paulo it seems they have to keep people in the stock market as banks no longer pay savers anything because they can borrow it from the Fed for almost nothing and lend it to us for a profit . They no longer need depositors money to lend out .

Signs of inflation is stArting to hit main street because of excessive liquidity ,and I wonder if we will be one day be like Zimbabwe with a run away stock market that no one can sell because we have to keep ahead of inflation .

Like I said before… Without ZIRP/NIRP/QQE (and other imaginative weapons of financial and economical terrorism) the PONZI SCHEME – you still persist calling it “Markets” – will collapse in such an AWESOME and FUNNY way.

– “Here’s My Prediction: If the Fed Doesn’t Cut Rates 3 or 4 Times by December 11, Markets Are Going to Crap” ????

– My prediction: When (NOT IF) the FED cuts rates multiple times then that is a sign the economy is going to crap.

If the “the economy is going to crap,” stocks and lower-rated bonds are surely going to tank. So that would not be good for markets either :-]

If the current economy is so great, then why are interest rates still so low thus robbing from savers like myself?

Answer: The economy isn’t good, it’s just good political propaganda.

Talking about the BC economy?

Because Paulo, you need to put your money to work in the Ponzi scheme. If you are a saver, then you are a ******… mainly because a war has declared on people who save money. Because if you are saving (for silly things like retirement) then you are not spending. Then you must be the enemy.

I remember when a CD could earn a good 5 to 6 percent. Pretty soon you will have to buy junk bonds to get that kind of yield.

Where is this all going to go.

My guess is that a large armed conflict in the next 30 years or less should smooth things over.

It appears from my research, that in Dec. of 1929 the treasury had it’s first auction. So, I looked up an interest rate chart. In 1930, the equivalent of a 10 year treasury seemed to be around 3.4%…over the next year or so it went up to about 3.75%…then for the next 8 years it slowly made it’s way to around 2.0%. Currently the 10 year is at around 2.1% and a few years ago was 1.5% and seems to be headed back there. So, “we” are barely on a par with the 1930’s….??? How does this make sense in such a “strong” economy ? This sucker must be in a lot worse shape than the powers that be are leading us to believe. Too much debt, too many zombie companies. Money must have a reasonable cost, otherwise, we get hair-brain companies like Tesla. Savings is the backbone of any capitalistic system. What we have is a financial “Mount St. Helens”….will be spectacular when she blows! My lord, how did it come to this? Tough on this middle aged immigrant who believes in saving and under-consuming. Plain disgraceful!

They have to get behind the curve, CPI predictions are sub 2% for the foreseeable future. Can Treasury afford to pay positive real rates to investors, and fund their record debt? To keep markets going the Fed has to reverse their position, and markets know this and are all in. The Fed worries more about deflation so the shift might not arrive soon enough for the margined players, setting up a fall swoon. If the Fed makes an error it will be moving too slowly in response to rapidly escalating changes. If the Fed moves too quickly they could set up a whipsaw effect as well. The Fed cannot rate hike their way out of this. Jerome you do care about fiscal policy, you disingenuous fathead.

O cuts this year…..not one…..fixed it.

I don’t understand how Japan and Germany can sell negative rate 10 year bonds. Are the deeply indebted governments of the world forcing interest rates to stay low to limit the interest they have to pay on that debt? Are the low rates in the U.S. caused by the same thing?

As I see it, the bond market is a game of musical chairs, Scott. Nobody who can do basic maths, except maybe a central bank, buys a negatively yielding bond with the expectation of sitting on it till maturity.

If you simply want to park your capital it’d then probably be cheaper to build a vault in your cellar and stuff it full of paper cash that you withdraw from the bank.

German Bunds too are now speculative bets on relative risks rather than actual instruments people buy in order to secure (or, dare I say, improve..?) their long term purchasing power.

There is a certain bid implied in the guaranteed asset price of that negative yield bond. If you are thinking deflation, a negative yield bond is not a completely bad idea.

“If you simply want to park your capital it’d then probably be cheaper to build a vault in your cellar and stuff it full of paper cash that you withdraw from the bank.”

That was one of the Points of NIRP it was costing the CB’S to provide a secure store for sleeping capital.

A while back German insurance companies were discussing that openly. To keep millions or billions in cash seems to have costs too, like counting the bills and safekeeping itself.

I forgot the threshold when keeping paper currency becomes cheaper then negative rates.

It’s how people too rich for FDIC insurance store money. They pay sevice fee.

So if the Bunds negative -.20% bunds go to -.60%, does that a -.20% bund then sells at a premium?

I don’t understand why any bank would give a negative interest mortgage.

https://www.zerohedge.com/news/2019-06-05/my-bank-denmark-just-offered-me-negative-rate-interest-borrow-money?fbclid=IwAR0Zxf1G4xXW0HxtwGfb4Ef__z3M-OCLrD_TvCBHVu7Hl9TKhPYSKNPaaFk

Maybe someone could explain to me why any bank would want to give a loan where the bank pays you interest on that loan always having the risk of not getting their capital back.

Surely the bank would be better off keeping the cash (Ha Ha Ha) in the safe with no loss of capital and no risk of losiing the capital in to being paid back.

To me it seems very hard to justify a decrease in rates in the face of very low unemployment levels and inflation close to the Fed’s 2% mandate. We really do not want to follow the JCB’s and ECB’s lead to NIRP. Just take a look at $DB’s value for an example of what NIRP would do to the US banking sector.

Is 2% even mandated?

When I was going to school at the University of Chicago, the Monetarists were suggesting a desirable rate of inflation above 2%, if memory serves. More like 3%. Milton Friedman himself said a sufficiently high inflation rate was needed, to allow more flexibility in price changes.

timbers, as I see it any intended rate of inflation is sort of exploitative, however it may be framed.

Most people aren’t financial wizards who know the ins and outs of investment risks, but are people who mostly do some job outside the world of finance and just want to allocate any excess unspent earnings they might have in a way that will not cause them to lose their unspent purchasing power.

If any intentional rate of debasement is baked into their monetary units then they are driven towards risk they are relatively not equipped to deal with, rather than towards real safety.

Essentially, as I see it, any desired rate of inflation is simply a redistribution mechanism designed to benefit financial elites over fixed income earners and savers.

Immigration provides a whole new batch of people, to take on Debt, in a country selling slave labor goods. Those goods, are sold at sky high profits, with lousy quality to people in a “throw away society”. Low interest rates have ushered into existence people with no incentives to save, only watch their credit score until they can take on more debt. In essence, creating a nation of debtor slaves, working for a wage, with no benefits. Profit that only rewards shareholders, not employees. Huge bonuses for the CEO in charge of stealing from the working class. America has become blind to what is really happening. Look at prices of all that junk in Walmart. $200 for some Chinese patio furniture worth about $30. America is the Home of the Ripoff. Wake up people. You are getting ripped off.

Expectations are illogical and a delusion if FED don’t deliver!

Say it ain’t so Wolf. Retirees, pension funds, and savers like myself are already getting kicked around enough already by these low rates. In this borrow and spend economy we have now where it seems like most people and companies are already up to their ass in alligators (debt), who’s going to borrow more to try and pump up this economy? Am I missing something? Other than keeping the zombies alive, what will this accomplish?

On the flip side, pension funds are already fully invested. How are they going to do if the stocks they currently own stop being elevated by funny money? And their bond portfolios – what do you suppose will happen to their values if rates rise significantly? I don’t know what their average maturity is, but rising rates would result in losses on long-dated bonds, no?

As far as I can tell, the easy way out seems to be continual currency debasement – you get your pension, but it buys less than hopiumed.

‘Kicked around’ indeed.

I know quite a few retirees – not super wealthy, many were in small business or self employed – who worked hard and saved to finance their declining years without being a burden on d’ gubermunt (that is, their fellow taxpayers). You know, they have/had stupid concepts like ‘prudence’, ‘independence’ ‘self-reliance’ – old fashioned crap like that…

Now they’re being kicked in the teeth, repeatedly, the conversation at the club is changing to cashing out, private storage facilities & PM’s.

When you’re getting SFA on your TD & other investments with the distinct possibility of ‘bail-ins’, where’s the downside on exiting the totally corrupt system that has been foisted on us..

It’s a ripple now; a tsunami to come.

Good comment. I guess we know why the consumer economy is still breathing- no savers out there anymore. People spending everything they have just to survive and it still isn’t enough. And the FED wants more of this? in order to save some billionaires that invested in unprofitable, poorly run zombie companies, from financial ruin? What a disgrace.

Others have already noted that it’s more than a just billionaires riding the facade. (ie pensions). Billionaires are just a bi-product of capitalism’s feedback loop programming, which says that wealth must be concentrated. Whether the Fed is trying to save them or the entire program is indistinguishable. Symptom and sickness are one.

If we’ve learned anything over the last 13 years, it’s that stocks and bonds have lost their usefulness as a barometer of broader economic conditions.

If it’s possible for the stock market to post double digit gains in the same years wages barely budge, I assume the opposite is possible as well.

The only difference between the two is how much wailing and gnashing of teeth happens on cable news. When wage earners lose their jobs, then get offered a 20% haircut to get employed again, nobody cries on TV. But when the same happens to wealthy “investors”, well now the sky is falling.

I have never seen the outlook so short term. OK, we get market bounces for a few more years maybe. Interest rates near 0% after pleasing investors, a few more trillions.

2022 and beyond, what, we go selling off the national parks to the Chinese?

Counterparties on the losing side of Interest Rate Swaps will get obliterated… Going on a hunch here, but something tells me DB is gonna get smoked like a turkey =)

Probably the bond market believes that the trade wars will cause a general down turn before the end of the year. Which will force the FED to lower rates.

This is an interesting economy. On one hand we have companies looking for workers. Lots of signs for “Hiring!” I don’t think I have ever seen so many businesses looking for help.

On another we have record homeless. A low workforce participation rate. Political chaos/uncertainty. Low commodity prices. Slowing sales of lots of big ticket items. Some from lowering demand, some from ? stupidity/fraud/greed as in Boeing and the stock buy back craze. And what appears to either be fraud, scams, mismanagement or just incompetence in so many areas of our system/society. People don’t trust the government, law enforcement or corporations. And even though it is supposedly against the law, to many robo rip off phone calls. To much Flim Flam.

To much noise and to little concentration on what needs to be done.

It never occurred to wonder why the interest rates were going down. Seemed natural the way I see what is happening in the economy. It isn’t boom times if the workers can’t afford to buy what they are making much less a roof over their heads or shoes to wear. I read an LA Times article on LA’s homeless that had jobs, which said it now took almost $50/hr to live in LA and buy a home and live reasonably.

It never occurred to me to wonder why the interest rates were going down… to bad there isn’t an edit..

All those companies you mentioned looking to hire. What kind of wages are they paying? If you look at jobs in the $85k – 175k range, other than tech, I suspect the economy is not creating a lot of jobs in this pay range. I also suspect that those who have jobs in this pay range that are over 45 are deeply concerned about loosing their job and replacing it in a timely fashion at a similar wage. There are a lot of solidly middle class people today who in 5 years are going to be lower class. You can slice and dice this stuff all you want, a shit storm is coming and make no mistake, it’s going to be ugly.

Any place with a “Hiring!” sign is going to be paying under $12/hr and provide no benefits. I.e. not a wage anyone can live on without assistance.

My prediction:

The (inaccurate) inflations the Fed see and measures is inconsistent with logic of present and/or higher interest rates.

Therefore, the Fed’s logic requires it to cut rates to achieve it to see it’s (inaccurate) inflations targets.

The Fed don’t see no inflations. Therefore it has no choice. It must either see inflations, or change it’s inflations.

If the Fed does not see inflations, logically it must cut rates.

“The (inaccurate) inflations the Fed see…”

Correct. They use GARBAGE inflation figures in their calculations as pointed out long ago in the book, “Greenspan’s Bubbles” and by a few online financial bloggers. GARBAGE figures plugged into GARBAGE economic models based upon simplistic GARBAGE economic theory and you get to where we’re at – trapped.

Of course, those in a position to actually change this, those who actually control governments via lobbying and campaign “donations,” do no want to because they benefit so greatly from it. For the ultra-wealthy it has always been two steps forward during asset inflation, one step back during crashes. Imagine the incredible deals on REAL assets after the crash not to mention shorting on the way down.

Also, the current system as it is allows pols to continuously promise more “free” stuff to voters than tax receipts can cover.

Winston- Right on!

And to add the 2% inflation target is bogus.

1. The last 3 recessions, Fed started to lower rates anywhere from 3-4 months months up to 1 year BEFORE the recessions officially started. Notice also that the Fed Rate reductions started soon after the GDP started to go down.

2. That Q1 3.1% in the GDP would have been half of that value if not for the high inventory buildup and higher that usual deflator they used. Expect that number to decrease considerably in Q2.

3. Many times a recession is seen only after we are well into it – partially caused by the fact that prior quarters GDP figures are revised downward.

Future market predictions on rate cuts are often wrong just like the future earnings growth estimates produced by stock market analysts are many times unreliable.

I don’t really care if they cut rates 1 or 3 times until December. It’s more important to know by how much in total – it’s perfectly conceivable to me that we might see some of the rate cuts of this cycle be higher than .25%.

No surprise to me: a recession by the next 2020 elections is definitely in the cards. The administration knows that and they will try everything they can to avoid it. I doubt their effectiveness – if they pull it off it will only be much worse after 2020.

I care it’ll probably cost me a couple of hundred thousand dollars if they cut rates.

Best comment yet Tony .for all those wishing a rate cut ,hope you understand that your pension is getting eviscerated through currency destruction

Just to clarify: I am not in favor of rate cuts either. I was just stating what I think the Fed will do and that the total value of those cuts is more important.

1. I own too Treasuries. So I know what it will mean to be hit as a saver.

2. Higher rates could be better for some of the borrowers too – fewer people will do stupid things with almost free money.

I’d rather see rates not be controlled and be established freely by the market, which would likely mean they would be higher.

Sandu I have no idea what the blue curve in your plot is or why you’re massaging your GDP so much, but given your point (3) I think you can throw the whole blue plot out. The GDP that is in the database now is not what was reported in real-time.

If you’re going to use a highly manipulated (and quite possibly goalseeked) metric, and you want anyone to pay attention, you have the obligation to explain what it is and why you chose it.

Sure, here is the full disclosure:

The data from the FED’s website – I am not massaging anything. I interpreted the blue line as a close approximation of GDP growth rate.

https://fred.stlouisfed.org/graph/?g=cN69

You can find the full descriptions for all metrics used there at the above link.

I zoomed in to the last 3 recessions to make it easier to see when the Fed Rates started to decrease in relation to the start of the recessions. The patterns are really not that different if you look at prior recessions too.

You didn’t answer the question. What FRED data is going into the blue line – it’s not strictly GDP, you are adding and subtracting and dividing and therefore “massaging” the data to get a particular look – and why do it that particular way?

And I again point out that the data reported on FRED is not what was available to policymakers in real-time and therefore leading/lagging indications are meaningless in terms of anticipating policy choices.

sandu,

The Fed cannot cut much. FFR is from 2.25 to supposedly 2.5%.

We are on a different spectrum now. Also the Fed already has a bloated Balance Sheet compared to 2008. Trillions more.

It’s hard to comprehend these funny numbers.

Right Iamafan, a lot less room to move this time.

BTW when I say the recession would be even worse if it happens after 2020 I just inspire myself from thoughts of other people that know a lot more than I do and articulate this argument much better than I can.

Page not found!

Sorry, try this:

https://www.theinstitutionalriskanalyst.com/single-post/2019/06/05/Aftermath-Interview-with-James-Rickards

Clearly there’s a scarcity of 2-10 year Treasuries, so Congress needs to spend more (forcing up issuance) and / or the Federal Reserve needs to accelerate QT and initiate sales in that maturity range!! \snark

BTW, the term the Fed itself uses for the rate path implied by the bond market is not “prediction” but merely “expectation”. Expectation is probably the more appropriate term – especially given the routinely-demonstrated utter lack of predictive capability in macroeconomics.

But one big question not addressed in Wolf’s article is the extent to which the Treasury yield curve actually represents genuine expectations about the Fed’s future actions, as opposed to reflecting concerns about Other Central Banks’ actions. The Treasury Bond is a global financial instrument. Someone in China, the UK, Turkey or Europe, concerned about the future of both their local economy and their currency, might prefer a US$ bond but be unable to invest in shorter- or longer-term bonds for various reasons.

There are probably other potential sources of anomalous demand right now, which may have nothing to do with economic expectations. For instance in the March FOMC minutes the “Balance Sheet Normalization Principles” indicated a shift towards a portfolio which would match the maturity composition of all outstanding Treasuries. But in the May 22 FOMC minutes it’s clear that they are comparing this approach to an alternative in which the Fed holdings are weighted towards the short end of the maturity curve. The Fed’s modeling says the latter approach yields a lower Fed Funds rate, which might be of considerable value to the US Government for financing the national debt. If this approach is gaining traction, then market participants might be front-running the Fed’s potential purchase of trillions in short-term Treasuries over the next 2-5 years. (I leave open the possibility that simply floating this option was designed to trigger this response, in order to invert the yield curve prematurely and trigger a Fed easing which would have high political value between now and the 2020 elections… well-known public economist David Rosenberg has floated similar ideas.)

This probably helps the primary dealers get rid or make money of their bulging treasury inventory. Lowered interest makes older purchases look nice.

I just can’t make sense of this. If you look at TICDATA foreign transactions, they have been selling of Treasuries and US Corp. Stocks. 2019 selling accelerated. Normally, when foreigners buy LESS, we have to increase yield to make it more attractive to them. I don’t think American savers are enough to gobble down the deficit or Treasury auctions. Therefore, if this continues, then a round of QE is called by the doctor – and that is with record high stocks and debt. When that happens, there is no more excuse, we are simply monetizing debt.

It was the Swiss national bank that caused the big sell-off on Wall Street from October to December. The U.S. Fed and the U.S. central bankers didn’t want to make the Swiss central bank look stupid by rigging the U.S. stock market back up immediately after they sold so they waited until near the end of December on the last taxation day of the year for taking losses. Interest rates had nothing to do with it at all.

Got any evidence for the Swiss Bank Hypothesis, Tony?

gimme a day. I’ll analyze Swiss TICDATA transactions tomorrow and report.

Switzerland (Country Code 12688) showed NO SIGNS of extraordinary trades last December 2018:

(in millions)

US Treasury: -739

US Govt Agency: -116

Corporate Bonds: -214

Corporate Stocks: -266

This across the board selling is nothing new. It was much worse in May 2018. From April to December, only Nov was slightly positive.

Switzerland has been dumping US securities. But they are not the only one.

I don’t understand how people can put a probability on these phenomena. Statistics only describe groups of events.

That’s why you can’t get rich tossing coins. You know what the odds are. It’s 50/50 for any given toss of the coin.

However that gives you no predictive abilities regarding what any individual toss of the coin will be. All you can say is it if you flip a coin a thousand times you’ll get approximately 50 % heads and 50% tails. For any given toss of the coin you can’t predict what it will be.

If you toss heads 10 times in a row the probability of the next coin toss being heads is still 50/50.

That’s why predicting probabilities of single events is absurd.

You can prove anything using statistics to people who don’t understand statistics.

A probability of 50% attributed to a statistical issue must assume no partiality – as with a coin toss. No one, not Uncle Sam, not even God, audits the FED – but I can tell you that probability doesn’t enter into their decision making. Even the attributed probability vectors between zero rate cuts vs three or four is merely the opinion of people who have money to lose. It has no basis in whatever imaginary reality the FED uses to make decisions.

The economy as an aggregate functions on very simple premises: economic growth must always exceed interest rates, otherwise companies will not take out loans they cannot repay. Real growth is anticipated to be anemic, so the rates must fall. The Fed has decoupled this mechanism by providing ever cheaper loans, but all it has achieved is asset price inflation and malinvestment, because there is no increase in productivity. This will last for as long as foreigners keep buying the dollar, which is America’s main export and asset.

Dude – not quite:

The economy as an aggregate functions on very simple premises:

economicmonetary growth must always exceed interest rates, otherwise companies will not take out loans they cannot repay.Here’s some questions in my mind as an IT guy with very limited Financial knowledge.

Are the Fed interest rates what the banks pay the Fed or each other to lend money? So if that rate goes down, then everyone who borrows money to buy a car, house,iPhone etc gets a lower rate? Or companies get a lower rate to buy back their own stock? Where does the Fed get this money cheap to give the banks? If the Fed cut the interest rate does that mean all the Feds previous loans get reset to a lower rate, thereby reducing the Feds monthly bill? Finally, isn’t this currency manipulation?

Our main export asset is not the dollar.

Our export assets are land, businesses, IP, education and debt, which are all purchased with dollars.

@Stinks:

1) Yes.

2) Yes, eventually, if the banks pass their lower costs on to borrowers. (Notice that your checking or savings account still isn’t paying interest yet, even though rates have risen? But at least CDs and money-market accounts do.)

3) The Federal Reserve has been granted by Congress their constitutionally-derived power to create money from nothing. (But not sure if they get their chicks for free… h/t Dire Straits :)

4) The Federal Reserve controls short-term interest rates and this does affect the borrowing cost of the Federal Government, but rates on other, longer-term Treasury bonds (FedGov borrowing) are set by the market not the Fed.

5) Finally, isn’t this currency manipulation? Yes, and it’s a dirty job, but someone’s got to do it, and it’s so important that the power to regulate the national money supply is defined in the Constitution.

Thx… I thought currency manipulation was illegal on the world stage, isn’t that why we dont like China?

Some things really don’t change… recessions always start –

AFTER the yield curve has inverted and already begins to steepen

After consumer confidence has reached its normal cyclical peak

Once Corporate debt to GDP reaches a cycle peak based on historical peaks

Once House price growth starts plateauing

Unemployment rate stops decreasing and stabilizes at a low rate for a short time

…All these are obviously pointing to an upcoming downwards trend in the business cycle. While the economy is still robust today, these signs are all pointing to the party coming to an end in the next 6-12 months.

Only problem is that we are starting all this at a Fed funds rate of just 2.5% and an already bloated central bank balance sheet, oh and an already large fiscal deficit (certainly for what are considered ‘good’ times).

Watch out.

When your in La La Land everything is great!

It feels Great

It looks Great

The market just keeps going up!

And as long as it’s going up

La La land exists.

It’s Dream Land!

Until one day you have a Nightmare!

Thanks for the info..

I never even knew those probabilities existed

but i don’t know if you need them for sure cause

if you look at the Utilities, REIT, Insurance, treasuries, and Foods that pay a good dividend ..you’ll see there all in La La Land already

There Scared!

Scared of a Nightmare

where interest rates are gasping for life

and yields are rarer than Flying Saucers

How come you always hear Baaaa… Baaaa..Baaaa

in La La land?

I don’t see how this ends well…. So now whatever is bad for the economy (and leads to rate cuts) is good for stocks? What kind of bizarro world is this?

Hey did anyone else see the LA times article a week or so ago about the glut of megamansions that aren’t selling in southern CA? Apparently they’re throwing parties instead of more simple open house events. One was stated to have a Great Gatsby theme. The irony was monumental and apparently lost on those holding the event…

I saw it … on top of that, another feature of the party was a lady floating inside a BUBBLE :]….

A few years ago I came to the realization that there were no longer any free markets anywhere.

Interest rates are whatever central banker’s say they are!

Trying to analyze anything is a total waste of time.

Central banks use derivatives to control everything.

The price of everything is what the central banker’s say it is.

End of story.

Yes, now the market is trying to dictate interest rates and the Fed has no choice. With 3 month bills higher than 10 yr Treasuries, bond funds will drive down the 30yr more, steeping the yield curve.

The Fed in their comments certainly seem to be trying to walk the markets back. But I also see that the Wall St press always distorts and exaggerates what they say. So, when someone who sets the policies says something like they are neutral and patient on rate cuts, suddenly the websites are celebrating the Fed’s massive U-turn and the stock markets jump upwards in happiness.

So, the Fed seems to be trying to walk them back gently, but the markets aren’t listening. At some point, this Fed which doesn’t like to surprise people might decide there is some value after all in shocking the markets. And right now, a little, tiny 1/4% rate hike would shock them silly.

Once interest rates have reached 0 for an extended period, any attempt to raise them consistently and restore sanity will fail. See Japan, Europe and now US.

Whether US rates fall now, in 6 or 12 months is pretty irrelevant. They will go back to 0 in the not too distant future.

Silver now is about the same as it was 10 years ago. Gold is about USD 200 above its 10 year old price. Pennies.

So tell me, where’s the price gonna go…..as the economy/currencies/d’ entire world goes to crap thanks to the PhD geniuses/criminals running the joint.

But what would I know as much smarter than I have said… “Gold is just….gold..”

There are a bunch of gold mines with VERY HIGH recovery costs per OZ.

Mostly Russian and ccp chines owned and operated.

The Gold buying groups supporting these miners, are allied to the Russians and ccp chinese.

This holds gold at its current insane selling prices.

Should the russians and ccp chinese be unable to hold the selling price above $ US1100.00 OZ the will be forced to close their MANY mines that have a recovery cost of around than.

Then the selling price of Gold will drop toward its true value and start to resolve the divergence from silver.

There are many gold mines in Western AU and other places that abruptly closed in browns bottom and have never reopened there is plenty of Gold left in them.

This issue underpinned by covert ccp chinese money printing is what has been manipulating the ridiculously high gold selling price for over a decade.

One day the mechanism manipulating the high sell price of gold it will fall over. The existing divergence from silver tells us that as does browns bottom. The peopel who say not, are also the peopel who told me I would never live to see $80.00 oil again.

Gold is just Gold- You know nothing about Gold.

I don’t see any rate cuts this years unless the things get really bad.

Fed: We may do rate cuts if things go to shit.

Markets: Yay! 3 rate cuts this year!

Fed: ?

OMG, from today’s WSJ… PJS

Analysis: It may be time for investors to stop worrying and learn to love the current economic boom

Wolf, I think you are on record as believing the December sell off was to be the end of this bubble?

In the carnage of March 2000, you were one year off having expected it in 1999.

In Oct. 2008 you were one year off, having expected it in 2007.

I see no reason to believe you won’t be one year off this time too.

He (we) are not wrong.

1 Caution

NOW we are still in a QE Economy, so the old rules and time frames, do not necessarily apply.

Although the end result, WILL be the same.

– The FED is going to cut (very) soon. The 3 month T-bill rate took a dive today (june 7, 2019).

I go for a walk in the mornings … have to get exercise. But I observe the real world beyond internet rhetoric.

The economy is strong in my area. For the first time in years, there are no houses for sale in my small Riverside County neighborhood. Just one for lease sign. Been that way for the last three months. I’d say this is the best I’ve seen it in a while.

In 2010, there were a dozen of homes for sale and half foreclosed. Add to that for lease homes.

Another note, the home price never recovered back to bubble highs here. People have moved into those foreclosures and fixed them up.

It’s a different world and rates are back down. I’m surprised by that. Perhaps, in the Bay Area/NY its all priced in. Have to watch out in this market because the politicians seem to time their announcements to the stock market TA.

You’re right. I’m incredulous just reading this. It’s absolutely the silliest and stupidest thing I’ve ever witnessed in the history of the central bank, centrally planned, financed, debt-monetized phony baloney economy. It’s embarrassing actually. The only thing left now is the bottom falling out of full faith and credit in, and total collapse of, the US finance system itself.

In a non-manipulated world would this be the case

Economy Good ==> Rates should go up.

Economy Good, might be slipping ==> Rate hike pause.

Economy Not Good ==> Rates should go down.

Economy Not Good, but getting better ==> Rate cut pause.

Central Banks controlled all markets, even bought financial assets in past years pulling tomorrow’s growth forward. We are in for years of little GDP growth worldwide.

Stock market is up big today – they know Jerome is going to help them out. Gold tried and failed to breach 1350 miserably and is now headed back down to its lows. To infinity and beyond!

Wolf, you talk a lot about junk rated debt. I suspect a fair chunk of the BBB is actually junk w lipstick on it. Thoughts on what % of the BBB debt should be rated as junk today?

I wouldn’t want to put a percentage on it, but it’s a pretty good portion. A lot of people are worried about that since there is such a large pile of BBB-rated debt out there right now. And if some of it gets downgraded, that’s still a large chunk.

That said, a downgrade to BB isn’t the end of the world during good times (right now). But when credit gets tighter, and companies being to buckle under their debts, an investment-grade rating can be a life saver.

The FED is making NO mistakes… The FED is keeping the dollar

alive as weakly as possible, while it kills as many other currencies

as possible… The FED is preparing the dollar to coexist along side as crypto carbon currency that will be demanded by a

monopolized world market place… the dollar will die slowly

as the carbon currency slowly fills in the gap…

Putin is being fed billions in digital counterfeit by the US, to complete his pipelines and other industrial expansion projects..

Russia has been depopulated, the US will be depopulated.

The powers that be have NEVER been as powerful as they

are right now… and the American people, never so dumb and useless… the movie “bird box” is a dead accurate analogy of

what will happen when the American idiots are pushed out of their fantasy world , and FORCED to look at the reality they

chose not to see… that movie and “The matrix” should be a double feature .

The lost fiat mine is open for business.

A couple of comments

1. POG this is not high at the moment because most of the cash is invested in shares/the markets .

Hence when the markets do take a hit , the money coming out will need a home.

2. It makes sense that the FED know before anybody else that GDP is down trending and hence the need to lower rates so I agree with the graph provided as a decent representation of what is likely to follow soon.

3. OIL led the way before xmas as it crashed , followed by a market decline. Looks like it is happening again BUT this time the FED is wise and rate cuts are planned to minimise OIL damage.

4. Rates can be cut only so far , at 0% you have to start giving $’s for free

One day it could happen

5. Sock markets and commodity markets are rigged …. sure they are … but they always have been

Let’s fix the problem and spin the dial back to 1913. Repeal the 16th Amendment. Disband the Federal Reserve. Bring back the gold standard and arrest the every Federal Reserve member for conspiracy to defraud the United States. Nice dream. Will never happen. The hoards of Americans are too ignorant to understand the fraud perpetrated upon them.

https://archive.org/stream/pdfy–Pori1NL6fKm2SnY/The%20Creature%20From%20Jekyll%20Island_djvu.txt