But where the heck is the “U-Turn?”

May was the first month of the Fed’s new plan of slowing QT and altering it in other ways. And suddenly, everything is in flux: It shed Treasury securities at a slowing pace, as announced, but for the first time – and not part of the pre-announced plan for May – the Fed replaced some longer-term Treasuries with short-term Treasury bills, thus doing the opposite of its QE-era “Operation Twist.” And it shed the most Mortgage Backed Securities since the QE unwind started.

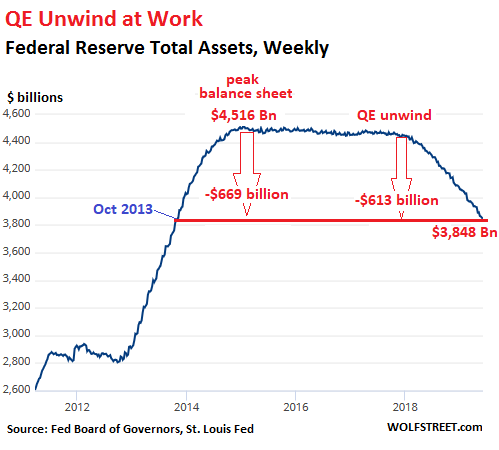

Total assets fell by $42 billion in May, as of the balance sheet for the week ended June 5, released this afternoon. This was the balance-sheet week that included May 31, the date when Treasuries rolled off. This drop reduced the assets to $3,848 billion, the lowest since October 2013. Since the beginning of the “balance sheet normalization” process, the Fed has shed $613 billion. Since peak-QE in January 2015, the Fed has shed $669 billion:

Treasury Runoff slows down.

According to the Fed’s new regime, announced in March, the maximum amount of Treasury securities that would be allowed to roll off when they mature would be cut in half, to $15 billion in May. And that’s about what we got.

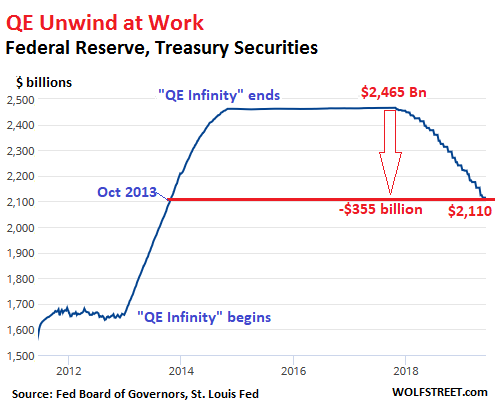

The Fed doesn’t sell its Treasury securities outright. Instead, when they mature at mid-month or at the end of the month, it just doesn’t replace them.

On May 15, three issues of Treasuries matured, and on May 31, three more issues matured, for a total of about $58 billion. The Treasury Department redeemed these securities and paid the Fed for them. And Fed reinvested most of this money into a new batch of Treasury securities but allowed the remainder to roll off without replacement. The balance of Treasuries dropped by $14 billion, to $2,110 billion, the lowest since October 2013:

Here is a new thingy:

The Fed acquired short-term Treasury bills for the first time in years, only small amounts. They crop up on its May-dated weekly balance sheets for the first time. In the current balance sheet, it lists $50 million, which will mature in mid-June. So this appears to be the first baby-step of what it said was still in the discussion stage and would be implemented after September: Replacing long maturities with short-term bills to bring down the average maturity of its portfolio. This is the reverse of Operation Twist of the QE era, when it replaced its short-term T-Bills with longer-term T-notes and T-Bonds to push down long-term yields.

Mortgage-Backed Securities Runoff Maxes Out

The residential MBS on the Fed’s balance sheet were issued and guaranteed by Fannie Mae, Freddie Mac, and Ginnie Mae. Holders of MBS receive pass-through principal payments as the underlying mortgages are paid down or are paid off. The remaining principal is paid off at maturity. The runoff is nearly all due to pass-through principal payments because 95% of the MBS on the Fed’s balance sheet mature in over 10 years.

These pass-through principal payments are erratic and depend to some extent on the movement of mortgage interest rates: Falling rates encourage homeowners to refinance their mortgages, and after these old mortgages are paid off by the homeowner, the amounts are passed through to the holders of MBS. But in times of rising interest rates, refis slow down, and pass-through principal payments dry up.

Mortgage rates have been falling since last November, and mortgage refi applications, after hitting a decade-low in December, have surged by over 50% since then, according to the Mortgage Bankers Association. And the Fed took advantage of this flow of pass-through principal payments.

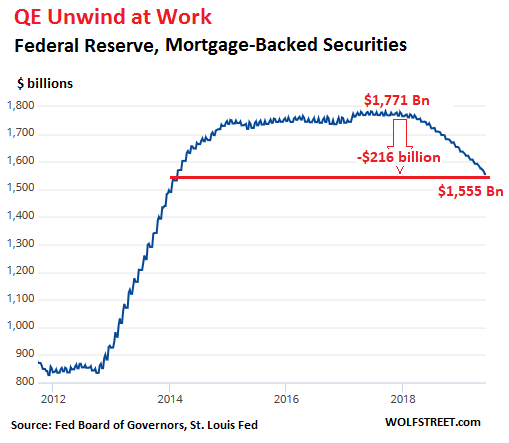

In May, the balance of MBS fell by $20 billion to $1,555 billion. Under the new regime through September, the runoff of MBS is set to continue as before, with a cap of “up to” $20 billion a month. Until May, the cap of $20 billion was never reached. In April, the MBS runoff topped out at $17 billion. The MBS runoff in May, at $20 billion, was the largest so far:

Changes on the asset side of the Fed’s balance sheet – the $42-billion drop in May – also reflect the Fed’s other activities. But in terms of Treasuries and MBS, the Fed shed $35 billion in May. While it slowed down the Treasury runoff, as announced, it is clearly intent on getting rid of its MBS as fast as possible under its announced limits. And in addition, it also now implemented its first baby-step of bringing T-Bills back on its balance sheet, at the expense of longer-term securities.

Stock market and corporate bond market are in la-la-land, pricing in an economic boom. They’re not seeing a rate-cut economy. So why would the Fed? Read… Here’s My Prediction: If the Fed Doesn’t Cut Rates 3 or 4 Times by Dec 11, Markets Are Going to Crap

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The end of May H.4.1 reported that the Fed has 50 million in T Bills.

I could not find any SOMA transaction announcing they bought any T bills for May. I wonder how they got those T bills? Anyone knows.

I know the Fed bought 4 and 8 week Tbills in today’s auction, but not in May.

Iamafan,

I just looked up one of the two issues it has: CUSIP 912796VF3. This is an 8-week bill. So if it bought it at issuance, it bought it in mid-April. I checked, and there are no bills on any of the April balance sheets. They crop on the May-dated balance sheets.

The issue is listed here:

https://www.treasurydirect.gov/TA_WS/securities/search?startdate=2014-01-01%20enddate=2014-02-01%20format=json

Domestic Holdings as of April 17, 2019 shows NOTHING, No T bills owned by the Fed.

I personally own CUSIP 912796VF3 so I have dogging it.

Besides if the Fed bought it as an 8 week, then SOMA should be reported. But on April 11, SOMA was ZERO for the 8 week.

https://www.treasurydirect.gov/instit/annceresult/press/preanre/2019/R_20190411_2.pdf

The Fed probably bought the same CUSIP 4 weeks later so it became a 4 week rather than an 8 week. But still SOMA says ZERO purchases.

https://www.treasurydirect.gov/instit/annceresult/press/preanre/2019/R_20190509_2.pdf

Something is wrong. $100 million appeared from nowhere.

Sorry if this has been asked/answered prior but do you have any idea what the duration is of the Fed balance sheet/portfolio? I see the various maturities for the straight Treausurys but have not found data on the MBS components of the portfolio.

The average maturity of the Fed’s Treasury holdings is over 8 years. It holds $612 billion in Treasuries with maturities over 10 years. And $267 billion that mature in 5-10 years.

About 95% of its MBS mature in over 10 years.

Here is a list by type of security and maturity.

https://fred.stlouisfed.org/release/tables?eid=4422&rid=20

Thanks Wolf. So given pre payments the duration overall would be somewhat lower. Still the Fed at some level would not want to face th duration ey are currently exposed to if possible. Your point in re the MBS sales recently is very well taken.

If you look at the May 1 SOMA Holdings Report, it says the Fed has:

10 Million of CUSIP 912796VF3 and

90 Million of CUSIP 912796VG1 for a total of 100 million in 4 week T Bills.

But if look at the Treasury Direct Announcement Results for these CUSIPS you get a different picture.

Cusip 912796VF3 on May 9 and Cusip 912796VG1 on May 16 reported ZERO SOMA purchases for 4 weeks.

How can the Fed on May 1 report something that has not happened???

They auctioned the CUSIPs the 9th and the 16th of May, weeks later. Looks like clairvoyant Superman right? Of course, they are ALWAYS right.

Unfortunately, it looks like Powell is more like Bernanke than Volcker. Selling out America. Too bad he is weak.

Iamafan,

is it possible that FRB/SOMA took possession of 100M T-bills that were part of a repo-loan that failed and did not get paid? That’s another mechanism for acquiring “assets” that does not involve an explicit purchase, at auction or otherwise. Or maybe some primary dealer bought the T-bills at the auction, but then could not pay, so FRB/SOMA just took the T-bills after the fact?

Thanks, Wolf and Iamfan, for keeping track of the minutiae. I have occasionally done so myself but have not had time recently. Good work.

You can pretend the Fed is not warming up the printing presses and preparing to do “whatever it takes” but pretending is not a good investment strategy. The Fed has pivoted to full on dovish inflation policy.

The Fed is kicking off their latest easing cycle and this one promises to be the biggest ever, endless in fact. Jerome (the free put) Powell has promised to take all measures necessary to keep growth on track – downturns are now banished because the Fed knows, after having pushed debts to enormous excess, even a tiny downturn could bring total collapse.

It’s inflate or die from here on, there will never again be a “tightening cycle”. Buy hard assets (stocks and productive assets) or be left impoverished by inflation and taxes.

The FED is trying to ease the market by telling them what they want to hear. Remember “subprime is contained”

The Fed and all Central Bankers have become Central Planners…and they have taken on the task of preventing cycles.

Cycles serve a purpose that the academics seem to miss.

Cycles periodically flush excesses….they “reset” the markets..

By preventing cycles, the Central Planners create MEGA CYCLES, the ones that bring systemic risk.

Cant agree more. I expect dow to be over 30k one year from now.

Given the amount of debt, it is simply inimaginable that the fed will allow any sort of asset deflation to happen. Except zero to negative interest rates, helicopter money, QE ad infinitum, whatever it takes, the Fed will not allow dow below 20k anymore.

It’s already baked in that the Fed will get the blame when the cycle wakes up. They’re damned no matter what they do.

What other game is there left?

Whatever the FED does it can never please more than 40% of the population.

This is what makes it such a soft target for teh FED bashers. They can always find a FED bashing angle that will fit in the anti FED media.

What is VERY AMUSING is watching the personal positions of the bashers change.

No matter what the FED does, the bashers are correct and the FED is wrong.

FED chair person on eof teh most thankless tasks on the planet.

Whats amusing at the moment is all the clutzes at the moment demanding interest rate cuts to of sett US tariff effects, any excuse to demand MORE FREE MONEY by paper asset profiteer’s.

FED BASHERS = WALL STREET CRY BABIES

Truer words never spoken. Nobody will ever save again and why should they at 0-1% and it will only go downhill from there. Inflation ticks up adding another generation of homeless living on the streets of every major US city. The FED created this “policy mishap”.

Whatever happened to that big fat ugly bubble?

You know they say the strong eat the weak but what about parasites?

Napoleon said, “Religion is what keeps the poor from murdering the rich.” I have observed we are getting more and more poor and fewer are religious. Ego….

@curious: words to take seriously, in what is now, more than ever, a post-ethical world (if it indeed, ever was…). The power of a general public conscience now appears to be in steep decline…but as long as one has theirs, Jack (be sure to research the term ‘noblesse oblige’), may we all find a better day.

I have no idea why the market dropped from all time highs when it was clear the market knew the FED would cut all along? Wolf stated the market was forward looking, yet if that was the case, the market would never have dropped in the first place.

What’s happening now ( in my guesstimation) is that you really can’t keep a secret in today’s world and that hundreds of economists inside the FED already know what the rate cut plan is. The info has leaked, plain an simple. I just watched the s&p torture itself to drop a 150 points yet, suddenly the markets, all rise in unison and have lost all their fears in two days?

No way. All the big guys now know exactly what’s going to happen and that is why they buy with such conviction. Gordan Gecko is alive and well inside the FED.

Something called the “Japan Affect”. America is doomed!! All the Fed’s feeble charades will only make things worse. In an ageing population with a falling birthrate zero interest rates hurt more people than it helps. This ins’t the baby boom era from the 1950’s each successive generation will get smaller and smaller as the birthrate falls.

Nobody else in the world will do what Japanese did. Most of the world will most likely go yellow vest.

The FED is doing what they are doing until the YWD, the yellow vest day.

And for yellow vesters to be, please don’t go against politicians or police. Go to the FED and take a dump at their door.

Book….your comments are spot on…… in addition the administration manipulates the markets with its timely announcements when weakness occurs to retain the wealth effect. Free markets are a thing of the past.

The big guys have the economy wired. Recessions are no longer allowed…..for now. The transfer of wealth from small savers to the wealthy will continue until there are no small savers. Then the wealth leaves for Switzerland and the collapse occurs.

Book and Fred nailed it. Just reading “Predator Nation” and agree with the premise that wealth transfer has been going on for decades and will continue to do so until every last drop is squeezed out for the ‘club’ and accepted members.

It could be worse and more blatant. Easy enough to imagine just past the 75th anniversary of D day. It gets worse and worse and more ramped up and the next thing you know there’s another war or trade dispute starting up. And more resources get siphoned off to the select.

Fred nailed it. The billionare class is treating Americans like colonizers treated Africa. Extract all the wealth, leave the people destitute, then transfer the wealth back to China or Switzerland and laugh about it for a hundred years.

We have to fight back against the billionares before it’s too late!

LMAO. Fight back? The peons thought electing Trump was fighting back. Let’s face it. The sheeple are going to get screwed and they deserve it.

It was not about electing Trump. It was about not electing the status quo that allowed the country to deteriorate over the last 30 years.

No need to fight. All you need to do is go to Eccle’s building and take a dump. When they crunching numbers and think by setting the numbers they will get you to spend or transfer your wealth or force you to do he things they want you to do, they will get shit!

I don’t really understand what happens with the MBS. If they’re not maturing for another 10 years, how does the fed get rid of them? does someone buy them? I’ve always heard that these things were garbage because the fed bought them at face value during the crisis. Didn’t a lot of the underlying mortgages get defaulted on?

Mortgage owners prepay and half of mortgages are only expected to last less than 10 years. In fact, most MBS were expected to pay out in a little more than six years. Remember MBS is pass thru and the monthly payments include interest and principal. Owning MBS can be confusing. My dad and older brother have been buying MBS for decades and I never completely understood what was going on.

By the way, the Fed does not sell their securities before maturity. The keep them till they mature. But MBS can mature rather quickly and can be prepaid before their expected original term.

Maybe they can be prepaid in T-Bills even? Perhaps that’s how the Fed wound up with some, without buying any.

Could also have arrived via one of the currency swap lines?

Point being – they have more activity than just SOMA.

They were garbage at the time because the mortgages included liar loans, alt-a, etc. and real estate was dropping like a stone. But, by buying MBS, they put a floor in on the collapse.

So all the soldiers trapped in the field got big time air cover just before being wiped out. If they are your friends, which they like to appear to be, it feels like big mojo because it is.

I knew an elderly women who worked as a clerk and amassed almost a million dollars over a lifetime of saving which she had “invested” mostly in CDs. She had no idea who the Fed is and yet they transferred tens of thousands in wealth from her every year, year after year … and she really didn’t understamd how or why. That’s big mojo.

bungee, during the time of Quantum Everything, the Fed decided that it should hold $X amount of MBSes. Each month, some $Y amount of those MBSes mature. To continue holding the target $X amount, the Fed then buys $Y of new MBSes.

What has changed is that the Fed is reducing the $X amount so instead of buying $Y of new MBSes in May, they bought $Y – $42 billion. Over time, this should lead to them “rolling off” all of their MBS holdings.

thanks JonTX and everyone else who chimed in!

While central banks go on juicing their Ponzi markets and asset bubbles with Keynesian monetary fraud, the oligarch-looted real economy continues to shed living-wage jobs. IBM is laying off another 1,000 – gotta relentlessly chop headcount to boost that “shareholder value” (CEO compensation) and concentrate even more wealth in the greedy hands of the already super-wealthy.

Citizens have only one defense against central bank currency debasement: buy and hold physical precious metals.

How’s that working for you? Gold made a run at 1350 today and then folded like a cheap lawn chair. We’ve got another 4 to six years before PMs make a real lasting move upwards.

There’s an old saying: “We can’t stand prosperity”. Hubris sets in.

Pumped-up, false prosperity will eventually fail, IMO, pumping to the contrary notwithstanding; actually, I think, making the fall more calamitous.

Today;s Morning News:

Treasury Yields Tumble on Payroll Miss.

Boy did I get a laugh.

Bad news is now good news.

Yep I thought the same. We have entered the ‘bad news is good for the market’ crazy place once again. Seen that movie before.

– Despite bad job report, the DOW best week.

– The job report don’t report that high tech jobs are moving from

high cost Palo Alto to Pittsburgh, because the housing cost in Pgh is 1/3, and for the same jobs pay less.

– The job report don’t report that many of those new 1,000,000 illegal immigrants will never go back home and might be employed assembling AAPL components in US + PR, at lower cost than in China, competing with expensive robots.

– In the Gilded Age 1865 – 1896 German, Irish & Italian immigrants replaced high cost union workers and made America work & great.

Nobody liked them, fearing they will bring the Pope in. Chinese workers

building R/R were hated the most on the west coast.

– When the new immigrants demanded improvements, Freedmen moved in.

– The globalist are in a state of shocked, because tariff are imposed on China and a new 5% on Mexico, from Mon. Few weeks ago the end is near that because 10% tariff on China, but they recovered.

– Economist are shocked when warehouses purge reduce jobs.

– Since Europe and Japan rates are underwater, the next “heat wave” will sink Europe, dragging US 10Y with them to 1.25% – 1.5%.

– The DOJ hitting FANG + friends might rectify the Nasdaq and US Pareto top income & wealth.

– Rotation will not replace the bubble, but the economy might be doing well, in the next 4-5 years, in phase III since Mar 2009 and with higher inflation !!

– When the DOW is up Trump hit in pulse modulation.

Michael Engel-please cite the ‘high-cost’ unions you reference, as well-paid unions didn’t really exist until well into the 20th Century (indeed, the period you refer to was the gestation period of the union movement worldwide and the oft-violent struggle that brought unions to their eventual, now-vanishing, prominence-recommend Barbara Tuchman’s ‘The Proud Tower’ for a more detailed look). In this case I think you might be referring to the in-place (for over a generation), mostly WASP, U.S. citizens resisting the influx of ‘pauper labor’ (see any similarities with our current southern border issues?) comprised of people of differing religion, language, and/or ethnicity/color at a time when many Americans were also ’emigrating’-leaving the farms for the cities and those new factory jobs.

No one living a stable, happily-located life likes to see their labor devalued, any more than someone who finds they are not valued by their society/country who will pull up stakes to migrate to a place with perceived better opportunities. Business will always take, nay, be forced, to take advantage of the subsequent windfall cost of surplus labor. (How much immigrant-blaming can we really do when we’ve looked the other way on enforcing an employer card-check program for two generations, now? Work ‘Americans’ won’t do’? Well, not at THAT pay…).

In any case, despite the expensive buy-in, robots will eventually be much cheaper for business in the long run than human labor (especially as the product spread and needs of an increasingly impoverished world society are reduced to basic survival levels), rendering even more of growing world population surplus. As many have said on this blog, one can’t have a successful consumer-based society without successful consumers-what will world corporations and market/financial institutions do to seriously address this other than picking at the bones of a slowly-rotting corpse?

TANSTAAFL, and the race to the bottom continues. In the smoke, may we all find that better day.

If the Fed drops rates they drop energy prices, and that leads to global deflation. Energy is still the primary economic driver. Not sure why gas prices are stuck (same old price gouging I guess) but while truck shipments drop you know demand is also falling. Falling demand means even lower prices. Move over matrix, hello vortex.

It looks like we are going to ZERO then NEGATIVE.

This “forever bubble” could last for decades. Scary.

“This “forever bubble” could last for decades. Scary.”

I opened my first online trading account in late 1996. At the time Greenspan said that the stock market was frothy.

Owning stocks and real estate has paid off very handsomely. At this point a 50% drop in valuations would not bother me too much. It would present a chance to seize opportunities.

However it looks like globally coordinated Central Bank Liquidity will elevate assets at least until the next elections.

Invest early and invest often. The best way.

Not a U-turn but an About-Face. Currently marching the same direction only facing backwards. The Fed has a history of crashing the US economy to save its precious dollar, the only commodity it produces. But they capitulated in ’08 so they may figure the jig is up. Trump will bash them relentlessly if they don’t. So everybody in the pool for a bubble blowing bonanza to end all. Marching backwards for now but then its full speed… Behind!

The Fed has a history of crashing the US economy to save its precious dollar, the only commodity it produces.

Not so. The Fed, in concert with its Wall Street grifter accomplices, uses engineered boom/bust cycles every 8-10 years to effect the looting and asset-stripping of the vanishing middle class and the transfer of their wealth to the Fed’s oligarch accomplices. The Fed isn’t “saving” the dollar; it is debasing every dollar in existence with the trillions of “stimulus” it is creating out of thin air so its financial sector partners in crime can hoover up the distressed assets of the increasingly pauperized proles.

Forward, into the past!

If you cant trim the balance sheet, if you cant remove the stimulus with and inverted yield curve, record employment and a 26K Dow, when can you?

The real question no one seems to ask is

Why isn’t the Treasury raising ALL their money in the Ten Year Note and out to the 30 yr?

The record low rates in the long end are attractive, and it would reduce or eliminate the inverted curve.

shouldn’t the chart of the Fed balance sheet start at 800 Billion (2008 level) rather than 2.6 Trillion?

And should not charts pertaining to inflation show the accumulation and compounding, rather than mere incremental increases?

historicus

No. People who say that the balance sheet should be at $800 billion now to get us back to where we were don’t understand what the Fed’s “balance sheet” is and how it works. So let me help you with this. Read this carefully so you don’t have to post that kind of question again:

So here is the first fact: In the five years between Jan 2003 and Dec 2007 (a year before QE), the Fed’s balance sheet grew by 25%, from $712 billion to $890 billion.

Why? Because the balance sheet always grows — and it can never go back to $800 billion, or to $400 billion or to $200 billion – for these reasons:

The Fed’s balance sheet has two sides, like all balance sheets — assets on one side, and liabilities and capital on the other side. These two sides have to be the same to the penny (“in balance,” got it?).

On the Fed’s liability side, the biggest items are “currency in circulation” (the actual paper dollars in your pocked) and bank reserves (money that the banks park at the Fed and that the Fed owes the banks).

Cash in circulation was $815 billion in 2007. Reserves were small. And there was not a lot else on the liability side of the balance sheet. Total liabilities amounted to $860 billion. There was also a little capital. And hence total assets amounted to about $860 billion too. That’s the $860 billion you’re referring to (well, you called it “$800 billion”). It was mostly a result of the amount of “currency in circulation.”

Now currency in circulation is $1.74 trillion. This is determined by demand for currency, mostly from overseas (stash under mattress, illegal enterprise, etc.). Banks have to have enough currency on hand to meet this demand at all times, and the Fed makes sure they do. This is market driven. During times of uncertainty overseas, there is more demand for paper dollars. This is why during and after the financial crisis, demand for paper dollars surged.

So assets can never drop below the liability of “currency in circulation,” now = $1.74 trillion and growing. So just forget your idea of an “$800 billion” balance sheet. People who say that this is where the balance sheet should be today are just clueless about liabilities on the balance sheet.

Here is my discussion on “currency in circulation,” including long-term charts of the kind you would like:

https://wolfstreet.com/2019/01/11/feds-powell-balance-sheet-to-be-substantially-smaller-how-small-he-gave-big-clues-my-dive-into-dynamics-w-charts/

The other big item on the liability side are bank reserves (“required reserves” and “excess reserves”). Those amount to $1.54 trillion now, up from very small amounts in 2007. This is the one item the Fed can actually reduce. And it has been reducing it. At the peak of QE, they were $2.8 trillion. So it has already cut them by nearly half. And it will continue to reduce them.

Here is my discussion on the dynamics of those reserves:

https://wolfstreet.com/2019/02/21/what-the-fed-actually-said-about-ending-the-qe-unwind/

So the balance sheet will always be a function of “currency in circulation” and “reserves.”

Central bankers, panicking over the incipient implosion of their Ponzi markets and asset bubbles, are trying to forestall the approach of the long-deferred financial reckoning day by unleashing another tsunami of Yellen Bux funny money to levitate these rigged, broken, manipulated “markets.”

https://www.scmp.com/business/banking-finance/article/3013594/central-banks-set-flood-market-cheap-loans-trade-war

Why? Why? Why? Just get the MBS out. This wasn’t supposed to be hard. After blowing out the balance sheet and then bailing out the MBS holders you do the same in reverse to return to “normal”.

Cut ties with the MBS now. First. Forever. Then strive for normalization.

I don’t understand why this has become such a Magilla.