What to do with those messy banks ignites further tensions.

By Don Quijones, Spain, UK, & Mexico, editor at WOLF STREET.

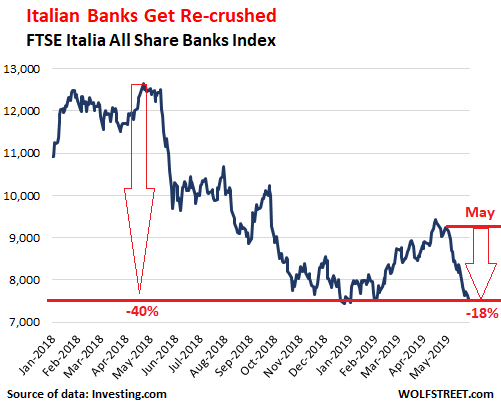

The Italia All Share Banks Index dropped 18% so far in May, almost double the 10% fall registered by the Euro Stoxx 600 banking index during the same period:

Italy’s biggest bank, Unicredit, saw its shares fall through the €10 level for the third time this year. The stock has lost 20% of its value in May, and is close to its all-time low, registered in July 2016 when Italy’s banking system was being shaken and stirred by the slow-motion collapse of then-third largest lender Monte dei Paschi di Siena (MPS). Unicredit’s shares are down 97% since the Italian banking-hype peak in May 2007.

MPS, now 68% state owned following a controversial taxpayer funded bailout in 2017, is already reverting to type. In the first quarter of this year its net profits slumped 85% to €27.9 million euros as shrinking revenues and larger write-downs on problem loans due to Italy’s weak economy took their toll. MPS’s shares, now at €1.07, are down 36% year to date and 78% since the bank’s shares were re-floated in October 2017 at the price of €4.76 a piece.

Ever since pouring €8 billion of public funds into MPS to stave off its collapse, the government’s “investment” has done nothing but lose value. Every now and then, a passing reference is made to the possibility of re-privatizing the bank, but in reality there are no interested buyers, partly because MPS’ balance sheet, still infested with non-performing loans (NPLs), keeps getting messier as the Italian economy stagnates, but also because there are no banks in Italy healthy enough to take on such a burden.

Mid-sized lender Banca Carige, which failed earlier this year and was temporarily propped up by the government, ran out of potential rescuers two week ago after asset management behemoth BlackRock, having seen what it would get into, walked away from the table. If Carige can’t find a last-minute buyer in the next few weeks, European bank supervisors say it should be closed. But that runs contrary to Rome’s plan for a state-funded rescue. And relations between Brussels and Rome could be about to get even more fraught.

Unicredit has its sights set on acquiring Germany’s second largest lender Commerzbank, but labor representatives on Commerzbank’s supervisory board have vowed to do whatever it takes to block the merger.

As for Italy’s second largest lender, Intesa Saopaolo, it is still trying to fully digest the two Veneto-based banks it picked up in a shotgun marriage in 2017. Intesa has seen its market cap plunge 20% in the last month and 40% since May 15, 2018, by which date the formation of the current heavily populist, big spending, anti-EU establishment coalition government had become a foregone certainty. Italy’s third and fourth largest lenders, Banco BPM and Unione di Banche Italiane, are also respectively down 31% and 20% in the last month and 45% and 47% since May 15.

One of the reasons for the latest deterioration is the ongoing, escalating standoff between Brussels and Rome over Italy’s 2019 budget and other matters. For the moment neither side shows any inclination to back down.

On Monday Italian Deputy Prime Minister Matteo Salvini, flush from La Lega’s victory in the European elections, said he now has a mandate to push through tax cuts and fight for changes to EU budget rules. Which went down like a lead balloon in Brussels, which hit back by threatening to fine Italy €4 billion over its rising debt and structural deficit levels.

Since then, Italy’s 10-year risk premium — the spread between Italian ten-year bond yields and their German counterparts — has surged almost 20 basis points to 289 basis points, its highest level since February. Given the constellation of threats and dangers circling Italy’s economy, this is arguably lower than it actually should be. Italy’s current 10-year yield of 2.675% pales in comparison with the 7.56% the Italian government was paying in November 2011, during the peak of the Eurozone debt crisis.

But it’s still three times as high as Spain’s risk premium (95 basis points), 2.6 times higher than Portugal’s (108 basis points) and just 39 points lower than Greece’s (329 basis points). In other words, the price of risk for Italian public debt is rising just as the price of risk for the public debt of just about all other Club Med economies, even that of Greece, is falling.

And that is particularly bad news for Italian banks, which are notorious hoarders of Italian treasuries. After the Bank of Italy, they are the second largest holders of Italian debt. Italian government bonds make up 20% of the banks’ entire asset base. While other Euro area banks, including even those in Spain, Germany and France, were net sellers of domestic government bonds in April, Italian banks doubled down on their purchases, buying up €7 billion more.

Over the last 12 months, Italian banks have increased their holdings of domestic government debt by €62 billion. This issue has been termed the “doom loop,” the interdependence between shaky banks and shaky government debt: When one gets in trouble, it will make the condition of the other even worse, thus creating a feedback loop.

As the ECB has gradually exited the market with the ending of QE, and with other market players unwilling and able to take up the slack, Italy’s banks and other financial institutions made up the difference. But they do so at huge risk to their already fragile financial health. By Don Quijones.

Just bumping along the bottom, from hopeless to hope and back to hopeless. Read… Deutsche Bank Death Spiral Hits Historic Low. European Banks Get Re-Hammered

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The idea that Unicredit might be allowed to acquire Commerzbank is just kite flying. Unicredit would love to get its hands all those lovely German deposit accounts just bulging with Euro’s, but I doubt the Bundesbank or BAFIN would relish the idea of all those Italian treasuries appearing on any German balance sheet.

Fraternal German/Italian relationships within the EU are one thing, but German depositors propping up Italian banks is quite another.

They are not after deposits: they are looking for a solvent government, like a parasite looking for a new host when the current one is about to die.

The EU needs a bankruptcy process for area banks that will allow them to write off bad assets and simultaneously lower liabilities until the banks are solvent. It’s been a decade since the Great Recession and euro banks are still a mess.

I want a process for myself where I can lower liabilities by some method other than the traditional one of giving someone else money. Sounds like a great idea.

yes it’s called ‘bankruptcy’ and it’s as useful as you imagine

I understand that trying to take control of “pledged assets” taken as security for Italian secured loans, is the triumph of hope over certainty.

In the UK it takes between 12 and 18 months for a UK lender to get their hands on whatever assets are pledged as security on a loan in default, and where the assets are in the UK.

I understand that in Italy you can plan on waiting a minimum of 5-7 years and 10 years is not regarded as unusual. Meanwhile, the borrower carries on as before!

I LOVE Monte dei Paschi di Siena (MPS)!

That bank rocks…it raises capital, it breaks EU regulations, its government is a comedian. Everyone who comes near the place is required to steal handsful of euros.

There is no bottom to this bottomless pit.

Yet after all these years and all these bail-outs, we’re still pretending this is a venerated institution.

WHOOHOOO!

Catching up. This post made my day. Thx Chip.

“labor representatives on Commerzbank’s supervisory board have vowed to do whatever it takes to block the merger”: This is likely the government speaking via the Labour (‘SPD’) part of the coalition which is closely tied with the unions.

After persistent but so far unsuccessful attempts to merge two coming bail-outs into one (DeuBa+CoBA), it seems the government doesn’t want to accelerate the CoBa collapse by infecting the bank with UniCredit.

It seems more and more like they should pull off an inverted bad bank in Italy, ie move what little of sound banking that they have left into a separate unit and leave the rest to fester ….

In a certain way it’s amusing from a view of Black humor, because bith Lega and M5S both did heavily condemn the previous government(s) for precisely the same thing they are now going for, ie rescuing the banksters with taxpayer funds …

Once more an excellent piece by DQ.

Reminds me of South Korea in the 1990’s and those chaebols holding massive debt (supported by Korean govt). The banks will be saved by the Italian govt… the game goes on just a different country,

The Italian government can do nothing about Carige since the bank is directly regulated by the European Central Bank (ECB): any bailout plan would need to be approved by the European Council, the true ECB taskmaster.

All Italian politicians can do is promise excessively generous tax breaks for any “investor” so brave or more likely so stupid to enter the fray and pledge up to €1.3 billion in guarantees and direct cash injections, money which has not been appropriated and as such money which doesn’t exist.

Part of the reason the ruling M5S party lost so many votes on Sunday is because their promises to “get tough” on shaky banks and “economic godfathers” openly flaunting rules have been sacrificed on the altar of GDP growth. So far they have shown absolutely no sign of understanding this lesson. Beatings will continue until they either “get it” or they become a political non-entity in spite of their brazen pork-barrel.

The longer they try to keep these pieces of lead floating the worse qill be when they fall over people heads.

God bless…Wolf….and….Son.

Should have read….Don..

MMT will “cure” every ill in the financial world, brace yourself, and buy some precious metal.

Hi Don, with reference to Carige bank since their deal with BlackRock falling through has there been a run at all in relation to people taking their money out?