Just bumping along the bottom, from hopeless to hope and back to hopeless.

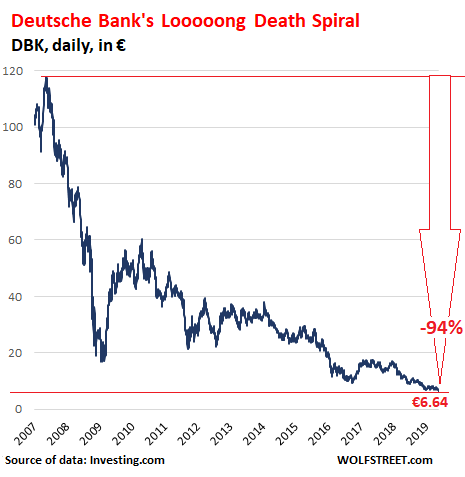

The amazing thing with Deutsche Bank shares is this: Since 2007, so for 12 years, bottom fishers have been routinely taken out the back and shot, every time, with relentless regularity – as have big institutional investors, from Chinese conglomerates to state-owned wealth funds, that thought they were picking the bottom. A similar concept applies to European banks in general. May 2007 was the high point. And it has been brutal ever since – 12 years of misery.

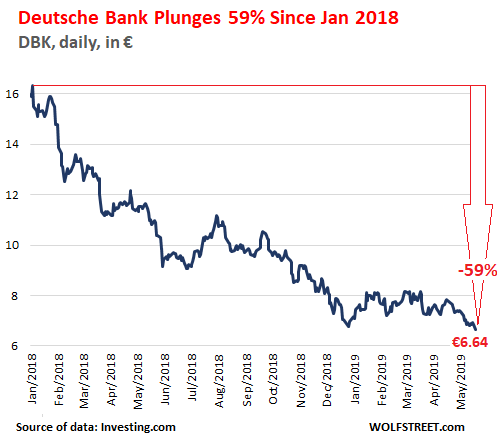

Deutsche Bank shares dropped another 2.9% on Monday in Frankfurt, and closed at a new historic low of €6.64 after hitting €6.61 intraday. This time, the blame was put on UBS analysts that finally stamped “sell” on the stock, replacing their “neutral” rating. Deutsche Bank’s market cap is now down to just €13.8 billion. Shares have plunged 39% over the past 12 months and 60% since January 2018 (data via Investing.com):

The bank has been subject to years of revelations of shenanigans that span the palette. Once a conservative bank that primarily served its German business clientele in Germany and overseas, it decided to turn itself into a Wall Street high-flyer that caused its shares to skyrocket until May 2007, when it got tangled up in the Financial Crisis that then led to a slew of apparently never-ending hair-raising revelations, settlements with regulators, and huge fines.

Since their death-spiral began in May 2007, Deutsche Bank shares have lost over 94% of their value. The UBS downgrade to sell came just in the nick of time:

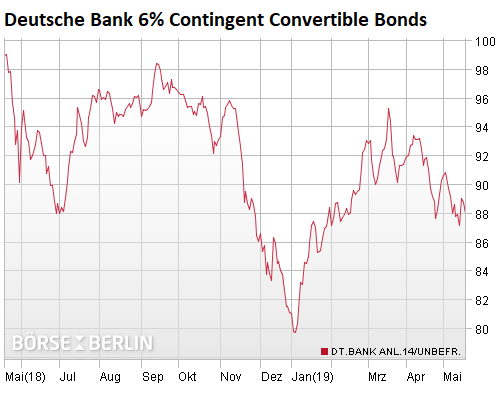

Deutsche Bank’s 6% unsecured contingent convertible bonds — perpetual bonds designed to be bailed in when regulators deem the bank close enough to toppling – are a gauge of what the market thinks the chances are of such an event.

To induce investors to buy these risky instruments, the bonds pay a rich 6% coupon. On Monday, the bonds traded at 88 cents on the euro. Their coupon of 6% (when the bonds were issued at a price of 100 cents on the euro) means that investors who bought them on Monday will earn a yield of 6.8%.

But this is in euro NIRP land where negative yields reign, and where the average junk-bond yield is now just 3.53% (ICE BofAML Euro High Yield Index Effective Yield). In other words, the Co-Co bonds pay nearly twice the yield of the average euro junk bond. Let that sink in for a moment:

But in Europe, it’s not just Deutsche Bank. Part of the situation in the Eurozone is that the ECB’s primary role has been keeping the Eurozone duct-taped together via its negative interest rate policy and bond-purchase program that allows over indebted countries that don’t control their own currency – the euro – to get even more overindebted without feeling the wrath of the bond market. And it worked.

The ECB doesn’t really care about the banks. It cares about the Eurozone. NIRP is not a good deal for the banks, except in the very short term. And that is one of the reasons why the Fed, which is focused on fattening up the banks, has so far had no appetite for NIRP.

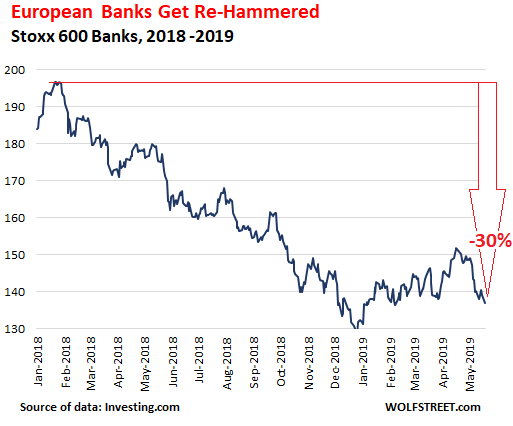

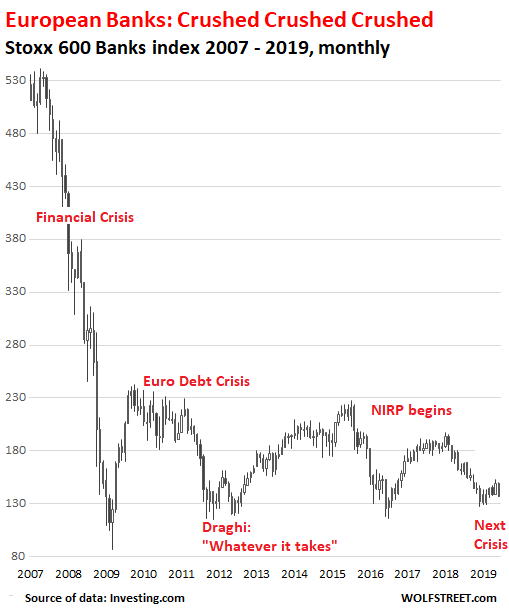

So the stocks of European banks, as depicted by the Stoxx 600 Banks index – which tracks 44 representative banks – dropped 1.6% on Monday to the lowest level since January 9, 2019, and has plunged 30% since the end of January 2018:

But going back 12 years, the plunge takes on different dimensions and parallels that of Deutsche Bank, with the index down 74% since May 2007, just bumping along the bottom, from hopeless to hope and back to hopeless:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

OK ya bunch of pilgrims! Now’s the time to back up the chuck wagon and load up on tons of Deutsche Bank stock at Euro$6.66. Ya got that ya bunch of unwashed, unvarnished cowboys? Don’t let the number 666 scare ya bunch of whimpering hombres. Ya’all savy now?

Could you translate that in to Chinese? Many of our political leaders here in Europe think they are the answer to our prayers!

It’s more like from hopeless to hopeless-er to hopeless back to hopeless-est.

LOL

Hope-less-ly lost.

“Ashes to ashes, dust to dust”.

Sorry; I’m fully invested in Tesla, Uber, Lyft & Snap…oh yea, and Bitwhatever

German banks have an advantage many other EU banks do not have. Germans save money and keep a lot of their liquid savings in DB and Commerzbank.

DB’s recent balance sheet shows €500 BILLION in Depositors Funds, but if you then go looking around the balance sheet for “cash” it is a different story. The difference between deposits and cash is some €300Bn.

Where is the €300Bn? Mostly, I suspect, supporting the DB Investment Bank. The traditional Wall Street IB model went to the wall in 2008 when IB’s rushed to acquire deposit taking banks because the deposits were a more stable form of “borrowing” rather than relying on inter bank loans.

A solution to DB’s problems might be to split the retail bank from the investment bank, and then wind down the investment bank to a more suitable size to cover their commercial clients needs. However, any split of the bank would require the return of depositors funding to the retail bank which would bankrupt the IB. The Bundesbank could fund the transfer, but the price might include ECB “interference” in what Germany sees as a domestic matter.

My German friends are convinced that the German Government will support and save DB at the end of the day, but if depositors begin to think that their funds are at risk, or not there when they want them, the Government will have to write some very large cheques.

There is also the small matter of ensuring that there is not a Credit Event which affects the derivative portfolio. Unleashing that scenario will reveal who is swimming without their trunks!

Covey

I think the most plausible scenario is that DB will be rescued ,

the government ( the German government that is) sees that Germany must maintain their major bank for reasons mainly explainable as the old copied rule of

“ TOO BIG TO BE ALLOWED TO FAIL”,

So the deposits that the bank hold will be safe ! But guess who’s paying again??

The depositors themselves albeit the German tax payer at large is on the hook,

and the crooks who wasted their money you ask?

Don’t worry they’ll be having champagne and caviar with the pollies !

Same damn scenario repeats itself. This time in German subtitles!!

I had a good laugh when I read your last sentence and the thought came to me that with almost EVERYONE now swimming naked, the revelation will merely mean the whole economy transforms into a nudist beach event.

You know, the odd feeling you get if you’re the only decent one with trunks on, while the entire nudist colony runs around you hanging loose and laughing at you instead?

And then, pretty soon, those decent sensible ones will succumb to the social pressure and throw their caution and their trunks off too.

There’s no shame nor madness when sufficient number of folks are in it together. lol.

Sounds like the episode of Twilight Zone called Eye of the Beholder

In Germany Deutsche Bank may be a legit banking institution. In other countries like the U.S., it is mostly a front for money laundering criminal operations.

As a retail banking customer in multiple countries, I know a shady operation when I see one.

No one wants to say it they two magic words “money laundering”. . Wonder why. Look up “Danske Bank Estonia”.

One branch of Danske Bank in Tallin, Estonia alone laundered $230 billion of Russian money. One branch. That branch chanelled most of it through Deutsche Bank’s U.S. unit, mainly through Jacksonville Florida. These were transactions that went through rapidly daily earning huge fees on both ends.

https://www.bloomberg.com/news/articles/2019-04-03/deutsche-bank-s-u-s-unit-kept-danske-s-shady-billions-flowing

“From 1999 through 2006, it handled almost $11 billion in U.S. dollar transactions for customers in nations under sanctions: Iran, Syria, Libya, Burma and Sudan. Later, it helped rich Russians move $10 billion from their country using “mirror trades” — simultaneous stock trades in separate jurisdictions that bypassed customary hoops for transferring money.”…

“It’s not clear how urgently the Florida team warned executives at Deutsche Bank Trust Co. Americas. But when workers sought broader scrutiny of certain clients, they got a familiar response from some higher-ups, the officer said: Shut up, focus on the transaction in front of you, file your paperwork and move on.

Internal documents, court records and interviews with dozens of people — including more than 20 current and former employees of the troubled German lender — show that its U.S. unit largely resisted strict money-laundering compliance for years. The insider accounts help explain why Deutsche’s U.S. subsidiary kept handling Danske’s business after competitors quit.”

——————————

This is the retail division of Deutsche Bank we are talking about.

We are talking about one branch of one bank here. Multiply that by hundreds and see how these banks make their money. I have had bank accounts in three countries. If you are a U.S. citizen they want FATCA, FBAR and other documentation out of the wazoo. Deutsche Bank is noticeably more lax when it comes to these requirements. I stay the heck away from them.

DB with a 40 to 50 trilliion USD estimated derivatives-book can’t be rescued – not by Germany nor by EU.

Have a look at Markus Krall’s videos on YT. Unfortunatley only in german.

Considering the recent news as a Bank to lenders of last resort, maybe there is a spigot of dirty money that flows into DB, and back out to aquisitions and RE finance operations?

No one will really know how dirty the entire banking industry is/was until the broken pieces are picked up and an attempt is made to fit something workable back together again.

Nice graphs.

But just like Y axis scaling tricks, missing out on X axis range is a bit misleading.

Yes it’s a big drop from the peak, but how much stock was actually bought/sold there?

It could be a tiny volume. Many could have bought in the run up years at half that price.

Still bleak though.

KL

Good points & here’s the DB NYSE stock & volume 10-year chart.

https://www.nasdaq.com/symbol/db/stock-chart?intraday=off&timeframe=10y&splits=off&earnings=off&movingaverage=None&lowerstudy=volume&comparison=off&index=&drilldown=off

Looks like panic broke thru the stupidity when the stock hit $20 in 2017. Material increase in volume since then

Kenny, you should plot that graph yourself before calling Wolf out on it. DB trades at all time lows, so it doesn’t matter when someone bought — they’ve lost money.

DB has traded in the US since late 1996. On a daily OHLC chart including dividends, DB’s current US share price ($7.52 on NYSE) is less than 1/3 of its lowest pre-2007 value ($24.54).

Anyone who bought-and-held prior to 2007 has had their money laundered away…

Not quite true…

…technically, you only make or lose money when you buy or sell. If you were a true believer (there are such things; ref: Uber, Lyft…) and you still hold stock bought at $80, you’re undoubtedly in a precarious position having made some questionable decisions, but you haven’t yet “lost”.

I understood Kenny to be using the technical definition of “loss”.

Right. Thanks for pointing out (even if its nitpicking) because prices are set at the margin. A big decline in thin trading means the entire market cap declines based on what a few players bid. The market is really an auction. No one has money ‘in’ the market. They hold a share and watch identical items sell at auction and imagine theirs is now worth the same. This holds true on the high end as well. Maybe especially on the high end. A lot of savers that own equities dont know how their share gets its valuation. That said im not buying any DB stock!

And whats up with these rating agencies? Is there a rating agency for rating agencies?

Wisdom Seeker,

They dont have money anymore. Those that bought prior to 2007 traded their money for stock. They made a purchase that turned out to be a poor store of value, like a car. Except they cant even use or enjoy it while they own it. :(

In addition, the ECB has destroyed the core business model of the European banks: Using deposits and other sources of finance, European banks borrow short term and lend long term. The flat yield curve has eliminated the margin in this core business. Money printing and manipulated interest rates are killing the savers and the European banks. And we haven’t even seen big credit events yet!

A few days ago there was a very interesting article regarding the long term effects of ZIRP on yields.

https://www.zerohedge.com/news/2019-05-20/how-central-bank-interest-rate-policy-destabilizing-banks

The banks must be really hurting and increases in interest rates don’t help in the short term.

Do you remember the infamous Cabo call by Mnuchin last Xmas? He was calling about liquidity, something like a Lehman moment. The only way to make sense of that call was probably a Deutche Bank moment. Maybe coming soon.

What is the mindset of western political leaders that they refuse to shut down bankrupt banks? To not throw their executives in jail and recapitalize new banks?

Bush Sr. put 1500+ S&L executives on jail.

What changed…?

QE to prevent any recession at all costs. To keep those in power in power.

Future job prospects – look where they all go following their political careers. Generally isn’t into manufacturing…

The true answer is Bill Clinton and the K-Street Republicans. Clinton was probably the most corrupt President of the 20th century. Newt Gingrich turned the Republican Party over to lobbyists, forcing incoming members to do whatever was necessary to raise money from them for the party coffers. Democrats do that now too, in a great race to the ethical bottom.

Bush Sr was the last President who fought in WWII. He was the last of the patriotic, patrician Republicans to run the country. He understood that the lower classes consider rising up when it becomes obvious that everything is being run for the upper-classes. It’s been mayhem since then, on both sides of the aisle.

Unlimited donations to PAC?

In Europe at least, the government & regulators are in on the bank heist.

Next question?

Bush Sr. did no such thing. Executive branch agencies prosecuted at the request of regulatory agencies that still had the power and authority to pursue white collar crime. George Herbert Hoover Bush did nothing but arrange for the fines of his son, Neil, to be paid by Republican donors after his Silverado S&L crashed and was prosecuted. The solution was to make criminal conduct legal, which gives us the gangster capitalism we enjoy today.

” The UBS downgrade to sell came just in the nick of time:”

-after the stock lost 94% of its value.

I enjoyed reading that little line of sarcasm. I hope you had as much fun writing it.

What changed…?

Citizens’ united decision…

You may be right. Now the big banks own Congress.

DB has just a sliver of equity now. What’s the strategy for getting better?

Do they relax the bookkeeping so that problems never surface in the financial statements? Do they wait until there is a recession or war that puts DB under, then they recapitalize through a bailout? Do they make NIRP permanent, so that bad bank loans never have to be serviced or repaid?

It is truly is hopeless because of what the ECB has done. When price discover returns, or hyperinflation ensues, heads will roll and central bankers will be the pariahs of society.

In Germany the general expectation is that DB will be bailed out at some point. Same for Commerzbank, which is why the government would have really liked for the two to merge before, reducing them to just one unpopular bailout.

Central bankers be held responsible for their crimes? Dream on, only a tiny fraction of society understands CBs to be the cause of the ongoing mess.

If you look at the liability side of the reported bank balance sheets, deposits are broken down between: Large Time deposits and Other Deposits.

2008 and prior, they used to be: Transactional vs Non Transactional.

Non Transactional was also broken down into Large Time vs Others.

Nowadays, the Other Deposits are more than 85% of deposits.

What can you possibly glean with that? Nothing, but you can expect that when a bank creates a loan (out of thin air), it also deposits that loan in the borrower’s account.

Remember the purpose for classifying these deposits is mainly for Required Reserves purposes. When anyone can just cash in or write a check against his/her balance, you need CASH equivalents for liquidity. Hence these deposits require reserves since they are flighty.

But money that tends to be sticky, not so. So you never know what’s really in the banks’ balance sheet. Probably the real sign of distress is no one bothers to lend them in the Wholesale Funding Market.

Anyone knows where DB gets their money? Maybe China is on the top of my list. Maybe HSBC and Standard Chartered are in the same funding boat, too. Prepare to be amused.

Check out the video on you tube by the Dutch banker.

Sorry at the moment I cannot remember his name but Dutch banker will get you there.

Having lived and worked in Germany, it is almost an article of religious faith that Germans trust their banks, and DB is the biggest and telling your friends that you were pulling your savings out of DB would be verging on treasonous!

Most will leave it too late and where will they move their savings to? Commerzbank (disclosure: I am a customer) has had an unhappy history with shipping and property loans and is still partly Government owned from 2008 and still cannot afford to repay the Government.

Last months idea from the Finance Ministry to merge the two banks was never going to fly as DB would have to open its books and some really severe write-downs would be forthcoming. Those write-downs would take care of the remaining DB market value leaving the Federal Government to re-capitalise. Under the new EU/ECB rules on resolving banks, straightforward nationalization ain’t allowed.

I guess everything is OK in the economy. A quote from Powell’s speech recently:

“today business debt does not appear to present notable risks to financial stability. The debt-to-GDP ratio has moved up at a steady pace, in line with previous expansions and neither fueled by nor fueling an asset bubble.”

Sure Jay, but wasn’t the debt-to-GDP at unsustainable levels before this expansion started? Aren’t debt-to-GDP levels now higher than ever before? Aren’t stock valuations at all-time highs relative to GDP?

Jay Powell is being very deceptive here and not taking responsibility for the broader picture. He’s not doing his job. He focuses on current CHANGES to debt levels without noting the hazardous big picture.

If I find myself on a cliff, I may not be making any dangerous moves, but I’m still on the cliff. Jay Powell, just standing there isn’t good enough. We need to get off the cliff before the wind blows us over. What is your solution to that? I have a feeling he wants to just stand there or go out farther on the ledge.

Draghi is no different.

They very much ARE doing their jobs – not rocking the boat. No-one ever sees a bubble until it’s burst – then everyone is an expert after the event, all re-inventing a past in which they were trying to warn pre-bubble-burst of the dangers but no-one was listening.

Human greed is incorrigible and anyone who tries to rein it in or even warn of its dangers stands to be branded a ‘crackpot’ or a ‘communist’.

Central bankers always assure you that there are no problems, risks are contained, financial stability tests passed.

I think that’s part of the job description detailed under “forward guidance.”

If you check old FOMC transcripts, you will find that Powell saw lots of bubble activity, even as early as 2012.

What changed? He’s now the Chair. He’s literally not allowed to see financial instabilities. The September-December drop in equities made him see the light (instead of reality).

And now we have high-profile ignorami (aka economists, and more specifically market monetarists) who believe that the Fed should never try to counter financial instabilities. And why try to stop a bubble from forming when by Fed definition a bubble doesn’t exist until it blows up?

> DB’s recent balance sheet shows €500 BILLION in Depositors Funds, but if you then go looking around the balance sheet for “cash” it is a different story. The difference between deposits and cash is some €300Bn.

Where is the €300Bn? <

@covey,

Total Deposits: 564,405 as of Dec 31, 2018 in Million Euros

Non-interest bearing deposits: 221,746

Interest-bearing deposits: 342,659

Cash and central bank balances: 188,731

Total Assets: 1,348,137

Therefore about 14% of its Assets are in Cash of Reserves.

The banks does NOT need to keep a CASH level the same as deposits.

What is interesting is the level of their Derivatives LOSSES.

Negative market values from derivative financial instruments: 301,487

Total Liabilities: 1,279,400

Financial liabilities at fair value through profit or loss: 415,680

So, their own shenanigans comprises about 32.5% of their total liabilities.

I would not put my money in such a bank. Just my opinion.

The problem is that virtually all the depositors money comes from the retail banking side, which if spun off would make a good bank.

The investment banking side is a basket case and makes little money at present. The US operations appear to lose money most years, and may be shut down because Congress does not like DB, and all the US Government lawyers think DB is a cash cow for fines.

You could not split the bank without the depositors money being “returned” to the retail bank, and I doubt the retail bank would want a boat load of derivatives in lieu of cash.

DB at present seems to function as bonus pool for staff, even if those bonuses are for failure.

The sell rating means buy, because the next ratings change will be to neutral. This is like the Trade Wars, a blockbuster movie with lots of sequels. Buy the dip, and Let the force be with you, Luke.

Either that, or they quietly stop coverage and withdraw their rating :-]

> “And that is one of the reasons why the Fed, which is focused on fattening up the banks, has so far had no appetite for NIRP.” <

So well said. I guess you know who butters your toast.

For that reason, we should watch the yield curve closely.

Gosh, I sure hope Turkish developers don’t default on those massive dollar- and euro-denominated loans they took out from (insolvent) Eurozone banks so they could go on a speculative multiyear building binge. Cuz I’m not sure Draghi and the ECB could print away a hit of that magnitude, especially with pissed-off populists and nationalists starting to replace the globalists’ and banksters’ servile toadies in the Establishment parties.

DB finds a “glitch” in its software that (supposedly) sniffs out money laundering.

Behold my shocked face.

Surely this “glitch” was not programmed intentionally, as our ever-vigilant regulators and enforcers would surely not countenance money laundering on the scale that Wachovia, HSBC, etc. have engaged in. That would mean senior banking officials going to prison instead of slap-on-the-wrist fines with no criminal charges, ever.

Oh, wait….

Corporation London is sweating. Just today the Queen asked “You can’t trick it? You can’t cheat?” about a supermarket till system. Oh the irony. The banking cartel is drinking alot of whiskey at the minute.

Bush Sr being a patriot. Not since he was head of the CIA. That changed his perspective. Now he was for the military industrial complex, not out country.

A great post Wolf.