House prices set post-collapse record in Miami, flatten out in Las Vegas, Phoenix & once red-hot Charlotte, linger below Oct 2018 levels in Washington, DC & Chicago. Cincinnati & Detroit in a show of their own.

On one side, there are “The Most Splendid Housing Bubbles in America” – the San Francisco Bay Area, the metros of Los Angeles, San Diego, Seattle, Portland, Boston, New York, and others – where home prices have blown past the crazy highs during Housing Bubble 1, which imploded so spectacularly. On the other side are markets where home prices have not yet reached their splendid levels of Housing Bubble 1, or never experienced Housing Bubble 1 to begin with. And this is the other side:

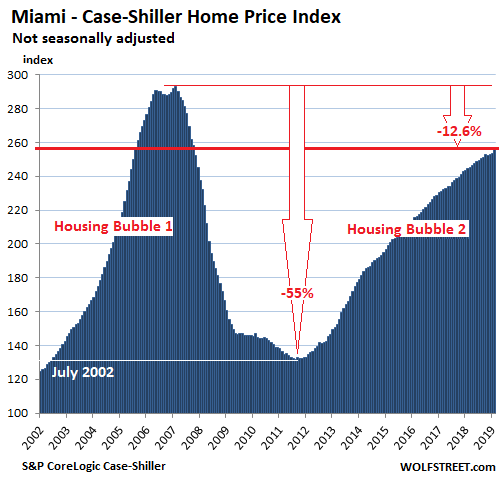

Miami

In the Miami metro, poster child of Housing Bubble 1 and Housing Bust 1, single-family house prices rose 0.9% in February from January, to a Housing-Bubble-2 record, according to the CoreLogic Case-Shiller Home Price Index. They’re up 4.7% from February last year and have risen within just 12.6% of the crazy peak of Housing Bubble 1.

The Core-Logic Case-Shiller Home Price Index was set at 100 for January 2000; an index value of 200 means single-family house prices have doubled since January 2000. In Miami’s chart, the Case-Shiller Index peaked at 293 in February 2007, indicating that prices nearly tripled in seven years. Then prices collapsed, giving up most of those gains over the following years. By August 2011, prices were back where they’d been in July 2002.

Since then, prices have been clambering back up, trying to regain those crazy highs of Housing Bubble 1. The February index level of 256 indicates that house prices are up 156% from January 2000.

Phoenix:

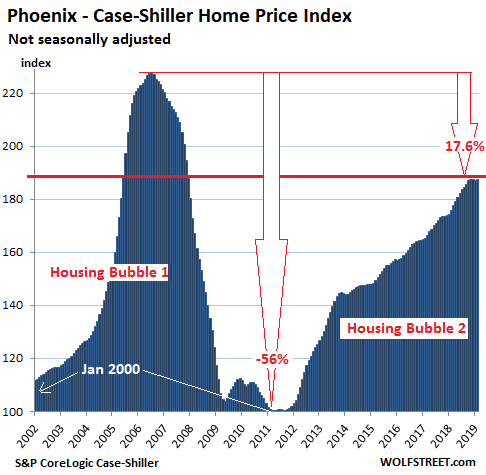

The Phoenix metro, in terms of steepness, was an unparalleled mind-bender of Housing Bubble 1 where the Case-Shiller index exploded by 80% in two-and-a-half years through July 2006 before collapsing back to 2000-levels by 2011. But it has not given up its spirit. Single-family house prices in February were flat compared to the prior three months, but are up 6.7% from February last year and now within just 17.6% of their crazy peak in Housing Bubble 1:

The Core-Logic Case-Shiller Home Price Index is a rolling three-month average; this release tracks closings that were entered into public records in November, December, and January.

It’s based on “sales pairs,” comparing the sales price of a house in the current month to the last transaction of the same house years earlier (methodology). This eliminates the problems of median price indices (changes in mix) and average price indices (a few big outliers). The index tracks how much many more dollars it takes to buy the same house. In other words, it tracks how fast the dollar is losing or gaining purchasing power with regards to same house over time. This makes the index a measure of house-price inflation.

Las Vegas:

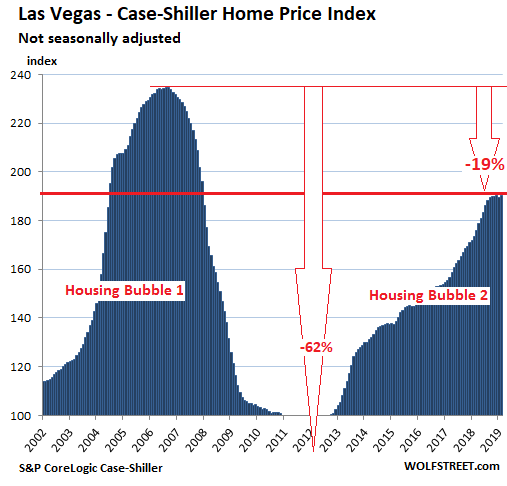

The Case-Shiller index for the Las Vegas metro in February ticked up a tiny bit back to levels where it had been in October, thus expanding its flat spot to five months. However, after sharp price gains mid-2018, the index is still up 9.7% from February last year. During Housing Bust 1, Las Vegas may have set a record for the speed collapse. From peak to trough, the index collapsed 62% to levels last seen in the 1990s. But over the fist three years of the five-and-a-half-year down cycle, they plunged 56%. Now house prices are clawing their way back up toward those crazy highs and are within 19%:

Chicago:

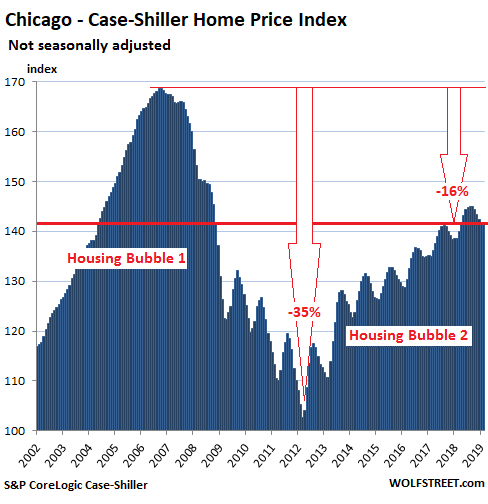

In the large and diverse Chicago metro, house prices were unchanged in February compared to January and remained 2.3% below the post-collapse peak of August last year. This decline is about in line with prior seasonal declines. Year-over-year, the index is up 2.2% but remains 15.9% below its Housing Bubble 1 peak:

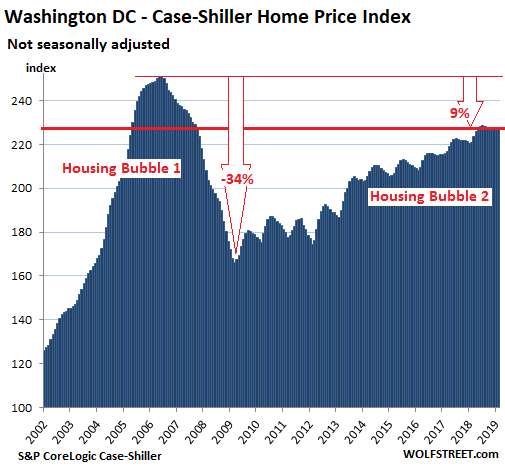

Washington DC:

House price in the Washington D.C. metro ticked up in February from January, which had been the lowest point since May 2018. Due to the price surge in early in 2018, however, the index is still up 3.0% year-over-year. The index has now moved within 9.3% of its ludicrous levels at the peak of Housing Bubble 1:

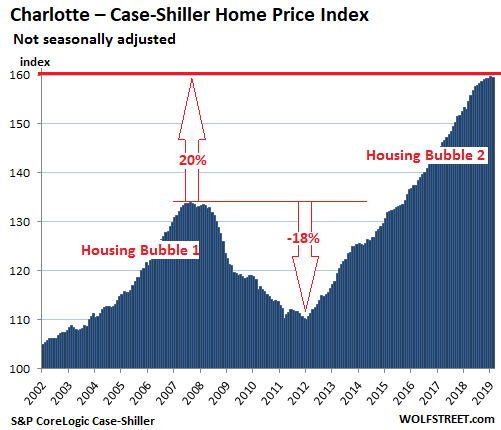

Charlotte:

The Case-Shiller index for the Charlotte metro ticked down a tiny bit in February compared to January, and has now been essentially flat for five months. But until October last year, prices had been on a relentless surge. The index is up 4.2% year-over-year and has risen 19.1% beyond its peak of Housing Bubble 1:

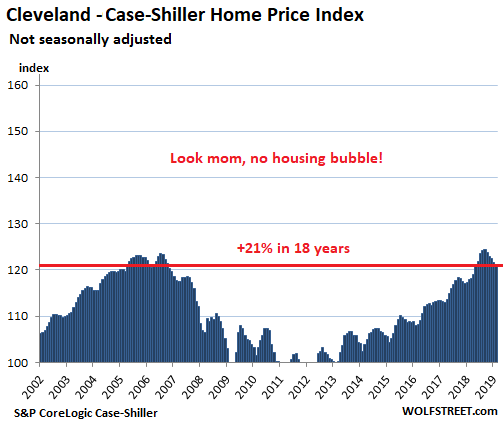

Cleveland:

In the Cleveland metro, house prices inched down again in February from January and are now below where they’d been in June 2018. With an index value of 121.2, the Case-Shiller Home Price Index indicates that home prices have risen just 21.2% since January 2000. Housing Bubbles 1 and 2 have bypassed Cleveland, but not Housing Bust 1. The left scale IS at the minimum range in this series, going from 100 to 160, same as Chicago, while Miami’s scale extends to 300:

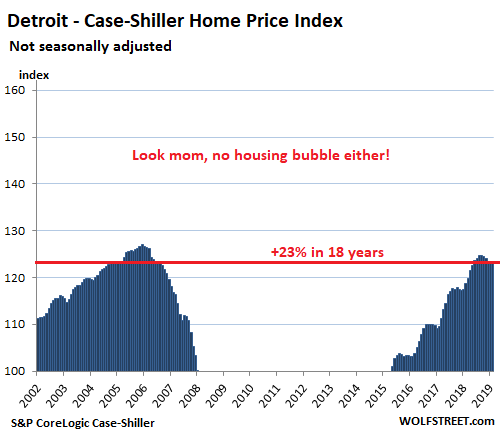

Detroit:

The index for the Detroit metro ticked up again in February from January but remains down a smidgen from the peak in July 2018. Since 2013, prices have risen 47%. But since January 2000, prices are up only 23.4%, and thus Detroit is not the weakest housing market in the Case-Shiller list of 20 cities – that honor belongs to Cleveland (+21.2%):

Condo prices fell year-over-year in New York. In San Francisco, SoCal, and Seattle, year-over-year price gains shrank to nearly nothing. Despite the hype, Boston prices continued to decline. Denver, Dallas and Atlanta eked out records. Read… The Most Splendid Housing Bubbles in America, April Update

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Detroit’s chart is unique with a missing bottom. I saw Detroit as a Third World during that low point.

The question is where was the bottom, 90 or 80 or less. It was pretty dismal from view from 60 miles.

What happened to the $500 houses in Detroit?

It’s costing $2000 apiece to demolish them, and the city doesn’t have the money because it’s desperately trying to manage a losing salvage operation for over 50 years.

Comparing it to the prosperous Hiroshima and Nagasaki, you would think it was Detroit that lost the war and got the worst of it. The greate industrial city that was credited with being decisive in winning two major theatres was deliberately destroyed using ethnic divisions and systematic economic repression for having successfully supported the emergence of labor unions.

It will never be allowed to really recover, and it is a metaphor for America.

Not true, a new bridge is being built. It’s publicly owned, unlike the bridge that is there which is owned by Grosse Pointe billionaire Manuel Moroun. The new bridge is named after the great Canadian hockey player “Gordie Howe”, International Bridge. The Canadian/Ontario governments have thrown a huge amount of money at the bridge and all the infrastructure on the Canadian side. Ford bought the old train station, “Ford Motor Co.’s restoration of the Michigan Central Depot by 2022 would bring 5,000 employees to Detroit’s Corktown neighborhood, where the Blue Oval aims to create what it calls “the next generation” of automotive mobility.”

And really, as a resident of the SF Bay Area, our roads/freeways can only wish they were as smooth as the I-94,96 and 75 in Detroit metro. How about this, DTW in Wayne County airport puts all of our airports to shame. No joke!

2000 is cheap for demo. Probably no remediation of toxic substances. Detroit just vanished like other boom towns.

qt,

It’s now a $0 dollar house or is gone entirely.

Panamabob,

Detroit’s bottom was 68.1 in March 2012. That was about a year before the bankruptcy filing, when everyone had already known for years that Detroit would eventually file.

Detroit is very mixed. The downtown area has been revitalized and is thriving and getting more expensive. But there are many classic neighborhoods that are in terrible shape, with long-time vacant houses needing to be bulldozed to make room for ag land or whatever.

Things in Seattle are looking better, but anything below 450k is still selling fast. Higher end homes are sticking around longer, of course all an anecdotal view of a house hunter. Question is when to buy? Google’s new office complex downtown will open soon, bring more tech rich kids to town.

One thing to remember is the taxes are so high in Seattle…my nephew just graduated from college and works for Google. They gave him a down payment for his condo downtown Seattle (a sweet deal or so it seemed). He lives in the same building as 22 other Google employees (none with families yet, as far as he can tell). He paid close to $2.5 million. The problem is that he just had to pay his first set of taxes. He asked us for a loan to pay them. This is becoming more and more common for younger homeowners. They don’t realize the expenses of owning a home or the taxes. His first mortgage payment to Google is due in June and it’s hefty. His $250k salary ($75k of that is a signing bonus) is heavily taxed in different ways. Also, interestingly enough they’ve been having productivity meetings due to the weed culture there. That’s a different topic but interesting nonetheless. Our home in Bellevue was just appraised for $600k more than our realtor wants to price it. This puts us back at -$112,000 less than we paid for it.

Don’t want to come off rude but If he’s making 250k a year and not able to make payments then there’s something wrong. Also not sure why anyone would buy a 2.5 mil condo, when you could buy a house. I know people make way less then that and able to meet their obligations. Maybe he’s living outside his means.

You think? The problem is employment is tricky. So many great companies are providing incentives (down payments for homes, student loan payback, tons of stock options). But not hard cash up front and when it (such as bonuses), it’s a greater tax burden that they don’t realize. He chose a down payment versus a grad school at Stanford that’s costly. So yes, he bought a Tesla, a new condo, a vacation cabin, has a nice credit card limit…3 weeks vacation but no idea how to manage money. He spends a ton of money on pot. I think the big salaries are fine but at what expense? I lived next to the Google offices in Boulder and the mentality is go big for the newer employees. Many are making $200,000 but are also buying $1,000,000+ homes for their first bachelor/bachelorette pad.

Living outside their means created the large “bubbles” along the west coast. Tech employees are forced to live near work( satellite offices never did work out), being forced to be close to a high demand location forces people into these risky positions.

I think eventually jobs are going to include housing. Because no one who’s not in the top 10% can afford to own a house or condo any more. So like Toyota did at least at one time, there will be worker’s dorms, and higher quality housing for more elite workers, like they do in the Army.

I get to live in the building I work in, and that plus $300 a week pay means I’m doing better than most do in this area. I mean, $300 a week is pretty good money in Silicon Valley.

I made more begging, back in 2009, but …. it’s begging. I’d rather work. Thank goodness I only had to panhandle for a few months.

$250k doesn’t justify a $2.5 million house. Something more like 3 times income has a better chance of surviving.

2.5 mil on 250k? That’s insane.

The old rule of thumb is to spend no more than 30 percent of your monthly gross income on housing. The housing expense includes mortgage, property taxes, insurance, and maintenance.

Doing a rough calculation, I estimate that your nephew is spending about 152K per year (or $12,700 per month) on housing which is about 60% of his gross income.

It’s criminal that Google steers its employees into such a precarious financial situation. And I’m amazed that these whipsmart young techies don’t seem to have much financial common sense.

I don’t even understand how this shit is supposed to work. I studied digital design, worked out my Karnaugh maps. Propositional logic embodied right there in chips and wires. Earned something like a black belt in soldering. If there was a fault on a board, even in the board itself, I’d find it. I could fix anything. And I never earned more than $30k a year, and only approached that figure by doing tons of overtime. Now my skills are next to useless; they only provide me the ability to better search what this or that used piece of tech junk might be worth on Ebay.

How big was the downpayment? This doesn’t seem to add up. If they gave him 500k then that must taxable income. Even if so, I don’t see how 250k-75k affords a 2 million mortgage. Perhaps a high earning roommate/partner?

I’m sure executive dad over at Amazon helped out. But I wonder if that’s the case for the first they new “Nooglers” living in the building in the similar condo price ranges.

And yes, this mentality is not smart. My point is, are they still showing this generation of home buyers how to manage their money?

I’m sure executive dad over at Amazon helped out. But I wonder if that’s the case for the first they new “Nooglers” living in the building in the similar condo price ranges.

And yes, this mentality is not smart. My point is, I hope they are teaching this generation about the rules of money management.

There is no way you can afford a $2M mortgage on $250K. After maxing out 401K, he is probably left with $15K after tax. A $2M mortgage has to be around $13K alone.

$250K is decent for a single guy without kids, but it’s probably just middle class for a family of four on the coasts these days. A single guy on that salary should be spending no more than $650K, and a family of four should be spending no more than $500K.

People are spending twice as much as they should on housing in major metro areas. Seattle, San Fran Bay, LA, San Diego, Boston, NYC, DC, and Miami are in big trouble in my opinion. With unemployment at 3.6%, all of these areas are having trouble attracting new residents. How much do prices have to drop to be able to compete with 2nd tier cities with housing that costs half as much? 25%? 33%?

Your nephew is an idiot, sorry to say.

Contrast, my millenial sister and husband have a portfolio of four properties, and growing richer by the day. One has a government job, the other is an executive. Their principle home is probably worth around $700K, very reasonable. They have plenty left over for the toys, boat, two loaded SUVs, Multiple trips to Mexico and Disneyland per year…ect.

$2.5 million condo on a $250k salary!. Reminds me of the old stories about company towns.

https://www.pbs.org/tpt/slavery-by-another-name/themes/company-towns/

Gotta watch out for those cranes, Gordon .. they’re dropping like flies ..

I recently moved to the Charlotte area and have some on the ground observations. The Feb (in reality Dec-Jan-Feb) numbers feel right as the market seemed dead. Not much was coming on the market, and not much was selling. Unfortunately, I think you’ll see an increase over the next few months of C-S releases.

To pass the time while house hunting I’ve been rolling my own machine learning/”zestimate” type tool (Mecklenburg County has GREAT open data sources on property characteristics and sales). From anecdotal estimates on houses weve considered, it seems like the farther out, larger-lot Charlotte suburbs have stalled out or are beginning to see slight price declines. But, the closer you get get to “uptown” (ugh) the more the situation changes. Since March, houses in good school districts that are more broadly “affordable” (<$400k) and < 10 miles to the city are continuing the relentless march upward for now. Before this year both segments moved more or less in unison.

Maybe the last hurrah for a while? A man can dream. But the sold day-1, multi offer situation from last year (or so I hear from our friends) has at least abated.

The good school districts within 10 miles of the city are brutally competitive in every major metro area in the country. Most of these districts have older housing supply and are all fully built out. The demand from high income families far exceeds the supply of houses on the market in these areas.

Luxury in subpar locations is going to take the brunt of the losses in this correction. The cheapest houses in the best inner-ring school districts show no signs of ever slowing down. Always going to be more demand then supply if the region’s population is growing.

Ed,

Agree 100%. I see the same thing locally as well. Older homes, close to downtown are in huge demand. Used to be turn of the century homes were the hot thing, buy them, gut them. But the supply cheaper homes that need a full renovation has dwindled as everything more or less has already been renovated in the past 5-10 years. Now, homes from the 60s and 70s – Brady Bunch Houses – are going fast. People buy them and gut them. The advantage of these homes is the lot sizes are massive, 1/3 to 3/4 acre lots compared to postage stamp lots that new homes offer. And established neighborhoods with mature trees, landscaping, etc is also appealing and commands a premium.

That Denver chart. My buddy lives out there and swears it’s affordable.

Is down 12% in two years, but up 40% 10 years really crushed? Also, dollar is strong, as is the stock market, and oil is around $70. I gotta say, what, me worry?

What happens to state tax revenues if house prices fall 30-40%? Is it a big part of their revenues?

Wouldn’t it be funny if Powell actually obeyed the voice from on high and the market took off ‘like a rocket’?

I drove into Detroit with a friend one night in November of 2008, at the peak of the financial panic. It was a dark place. The auto execs were testifying that day before Congress. They were actually getting crap for flying to DC instead of driving (!). Anyway, we got lost in a bad area. We pulled over to look at our directions. I accidentally bumped the shifter into neutral as we did so. We figured out where we needed to go, and I hit the gas to pull out. The engine revved loudly to about 6000 rpm before I realized what had happened. With a totally straight face, my buddy looked at me and said: “Oh my God…they stole our wheels already!!!”

We have relatives, an aunt and cousin both retired, who sold two houses in New Jersey. They pooled their money and bought one nicer home in South Florida.

This is an example of how the prices of homes can be up, while the number of sales is down. There’s a lot of multi generational consolidation going on and it’s been going on full blast in Florida for the last decade.

This is an easier link to read:

https://www.federalreserve.gov/newsevents/pressreleases/files/bcreg20190503a1.pdf

between the two, this would be the beginning to allow PTIE funds to be an entrance to allow circumventing “public banking regulations” and really setup a private banking system only for the elite. Now if you support that type of banking structure at even further levels of financial consolidation, where only debt packages are floating around the world, then don’t bother reading any of it…

San Diego is probably the next San Francisco. It is geographically isolated, prevented from any more growth on all sides. Fire danger, ocean, and Mexico. There is an established medtech industry golden triangle. Housing prices are probably held down by the age of existing homes, post W2 ranch style, (which some day may seem as fashionable as a Victorian) and salty no growth constituents, a generally conservative base inside a shifting liberal demographic, which is finding its ethnic roots, Little Saigon, Little Italy, etc. In the 60s SF was the destination of choice for professional panhandlers, and SD has plenty of homeless. Get it now while it’s cheap.

Reminds me of the time a RE agent in Carlsbad told me “real estate prices never go down, they only go up” (said Circa 2018).

San Diego is special

Real estate in San Diego can never go down

So what the median income is just 60k and median home price is 600k..

So what the affordability is pretty low

So what the middle class is moving out

Still San Diego..home prices can never go down

We are special and this time is different

Buy now or be priced out forever