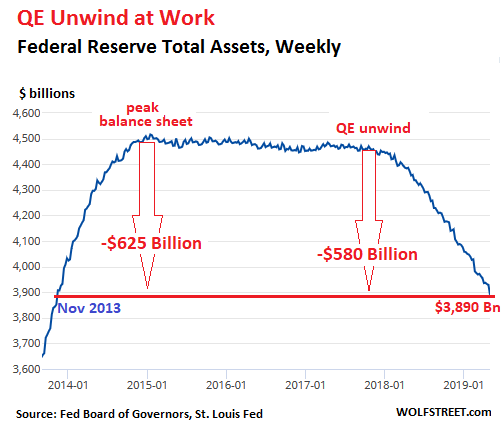

Fed sheds $46 Billion, Total QE Unwind Reaches $580 Billion. Assets drop to lowest level since Nov 2013.

In April, total assets on the Fed’s balance sheet fell by $46 billion, as of the balance sheet for the week ended May 1, released Thursday afternoon. This drop reduced the assets to $3,890 billion, the lowest since November 2013. Since the beginning of the “balance sheet normalization” process, the Fed has shed $580 billion. Since peak-QE in January 2015, the Fed has shed $625 billion:

According to the Fed’s old “balance sheet normalization” plan, which was still on autopilot in April, the QE-unwind would shed “up to” $30 billion in Treasuries and “up to” $20 billion in mortgage-backed securities (MBS) a month for a total of “up to” $50 billion a month, depending on the amounts of bonds that mature that month.

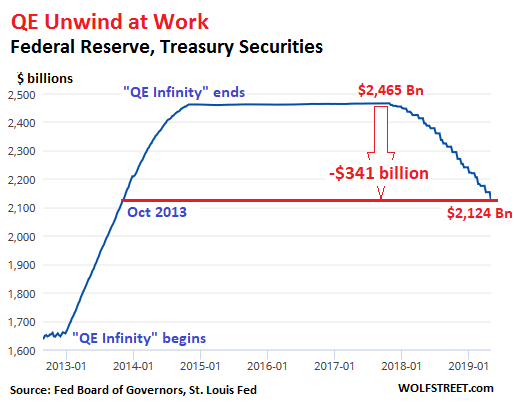

Treasury Securities

The Fed doesn’t actually sell its Treasury securities but allows them to “roll off” without replacement when they mature at mid-month or at the end of the month.

On April 15, $10 million in Treasury Inflation-Protected Securities (TIPS) and $169 million in Treasury securities in the Fed’s portfolio matured. On April 30, two issues of Treasuries matured, totaling $28 billion. Since all of it combined was below the $30-billion “cap,” all of it rolled off without replacement. This brought the Fed’s Treasury holdings down to $2,124 billion, the lowest since October 2013:

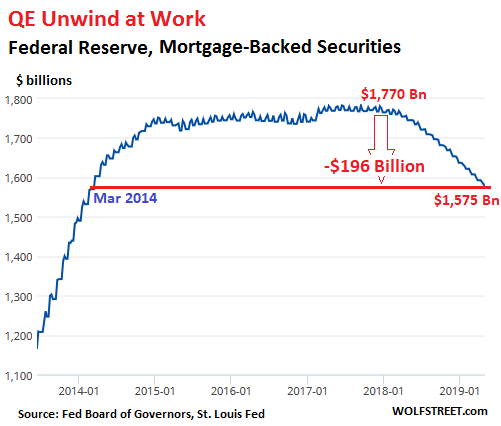

Mortgage-Backed Securities (MBS)

The residential MBS that the Fed still holds were issued and guaranteed by Fannie Mae, Freddie Mac, and Ginnie Mae. All holders of MBS, including the Fed, receive pass-through principal payments as the underlying mortgages are paid down on a monthly basis with each mortgage payment, or are paid off when the house is sold or the mortgage is refinanced. The remaining principal is paid off at maturity.

These pass-through principal payments are unpredictable and can cause the MBS balance in the Fed’s portfolio to decline erratically. To keep the balance steady after QE had ended, the New York Fed’s Open Market Operations continued purchasing MBS in the market, but the settlement lag of two to three months (the Fed books these trades at settlement) caused the zigzag moves in the MBS balance in the chart below.

In April, the balance of MBS fell by $17 billion to $1,575 billion, the lowest since March 2014. Since the QE unwind began, the Fed has shed $196 billion in MBS. But the runoff is nearly all due to pass-through principal payments because 95% ($1,503 billion) of the MBS on the Fed’s balance sheet mature in over 10 years:

The Fed has now outlined its new plan for its balance sheet. April was the last month on the old plan where the asset runoff proceeded on “autopilot.” In May, the transition begins with tapering the runoff of Treasury securities while maintaining the autopilot for MBS.

In October, a new regime kicks in that is intended to keep the balance sheet level, but replace MBS with shorter-dated Treasury securities with the goal of getting rid of those pesky MBS entirely by even selling them outright if the runoff is too slow.

In addition, according to Fed Chair Jerome Powell during the FOMC meeting press conference, the Fed is going to decide later in the year on the details of a huge component in this new plan: How to address the maturity-sinkhole that the Fed has been slipping into.

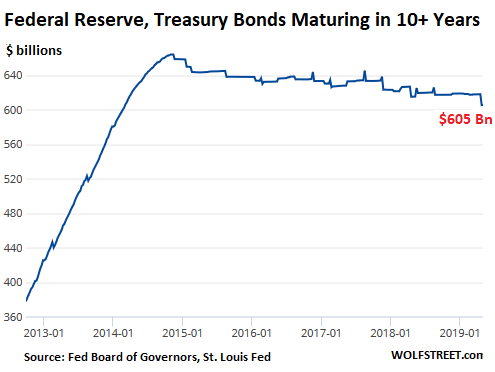

Of those $2,124 billion in Treasury securities, $605 billion are bonds maturing in over 10 years! This amount has not moved much since the QE unwind started:

The Fed has already announced that it wants to bring down the average maturity of its Treasury holdings to the average maturity of total outstanding marketable Treasury securities. This will require that the Fed take on short-term bills, of which it has none at the moment, and get rid of a portion of its long-dated Treasury notes and bonds. The Fed’s stepping away from those long-dated maturities is likely to put upward pressure on the 10-year Treasury yield which would steepen the yield curve a wee bit. Sit tight for details, Powell said.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“Sit tight for details, Powell said.”

Now that’s the fun part, speculating what the details will be. Reverse “Operation Twist”? Use the proceeds of MBS income to buy shorter term treasuries (and what duration? two year? six months?)?

Something else?

In this environment, I’d hate to be a bond trader, or retirement fund manager…how can you make money when your bread-and-butter investment vehicle is being manipulated so? Your returns are at the mercy of monetary interventions.

The Fed with news pieces and desk operations can make markets “jumpy” and hard to trade. But when the curve and spreads become speculative and reverse, there is nothing the senior central bank can do to prevent the reversal.

Otherwise there would be no contractions.

It is worth recalling that the backers behind the Fed knew that financial setbacks preceded recessions.

The theory was that the “lender of last resort” would prevent the setbacks. No recessions.

There has been 18 recession since the Fed opened its doors in January 1914.

While attractive to its proponents, the theory is NOT working.

True, the Fed didn’t prevent recessions in the past or asset prices from falling.

But a look at the last recession shows how the Fed for the first time in history started operating outside her legal mandates by printing trillions to purchase private and government debt, becoming a powerful political entity by choosing to punish savers and reward debtors.

This time is truly different and there are no constraints as to what the Fed can do to surppres interest rates and keep asset prices elevated.

But they also have planted the seeds of their own destruction.

Now that the people have seen how easy it is to print trillions, it’s only a matter of time before we elect a leader to do just that, with a powerful political mandate the people will get their own QE in not the too distant future.

But first let’s take Dow to 30k.

Maybe the FED can add a $1+ Trillion or so in toxic student loans the US Govt has made in the past decade . Have the schools pledge their ivory towers and campus palaces they built with taxpayer obligations as collateral. If that sounds looney, which it is, examine the alternative being offered by the folks aspiring to lead us all.

The Federal Reserve Bank of New York found that colleges raised tuition by 60 cents for every new dollar of subsidized loans the govt makes available. How has this been addressed? More subsidized loans.

Would love to see someone with the guts to examine the impact this has had on the economic well being of the supposed beneficiaries.

As an academic, I can tell you with more credibility and insight than any outsider that the whole system is a joke. That said, it is vital to understand that universities are not run by academics–their presidents are full-time fund raisers, their top advisers are lawyers, consultants, and Business School types, and the boards are completely filled with business men and politicians. Those are the people who run the universities and set the exorbitant prices. The crimes of the academics are 1) living off the exploited labor of grad students and adjuncts, and 2) acquiescing in the whole “corporatization” of the universities so long as their cushy tenured jobs aren’t effected. The educational mission of the university is almost completely lost in the shuffle.

What are the alternatives to those who need a degree in order to access a credentialed job market?

Go study abroad, and then try getting through the domestic degree recognition obstacle course?

You could go to Bangkok, find Khao-San Road, and you could buy any credential paper you wish; For a small price ( <$100 USD) you can get a Harvard MBA ( or MD ), with all the transcripts, and private Prof referral's to boot. For a little more you can buy FB alma-mater and have 1,000's of FAUX alumni friends.

find a diploma mill and use it to get experience

only in 1st 3 years of EMPLOYMENT did anyone care about my degree and what it’s in

after that it was 1000% about WHAT YOU CAN DO

those who CAN’T DO TEACH – which is REAL PROBLEM as our socialism fascist they ‘teach’ kids each day

@James Thank you for honest and concise insights. I have very close relations working at a college and our experience aligns.

The running joke at the technical college where I worked, “This would be a damn good college if it wasn’t for the teachers and the students.” In the twenty years I taught there, the number of administrators and assistants doubled, part-time faculty replaced over half of the full time instructors, administrative salaries went up greatly, and teacher pensions were cut back. Tuition more than quadrupled and donations went up about the same.

thank you for this:

“acquiescing in the whole corporatization of the universities so long as their cushy tenured jobs aren’t [a]ffected.”

I understand the administrative end is often out of touch with stated missions and corrupted, but the professional staff is the backbone of any institution and in more than one industry (I’m thinking medical) there has been too much finger pointing towards paper pushers and law-makers and not enough responsibility demanded from those who act as willing puppets.

=> Would love to see someone with the guts to examine the impact this has had on the economic well being of the supposed beneficiaries.

My guts were replaced with IV drips years ago, which minimises any risk to myself, so I’ll give it a shot.

Given present trends the average US college student will be no better off than the average HS graduate within five years, evening things up for those who can’t bribe their way in. Obviously this information must be suppressed, as it could dissuade at least half of college-bound seniors to substitute alternatives, such as multiple part-time grunt jobs or free-lance hunter-gatherer subsistence, causing the salaries of overpaid college basketball coaches to implode and ending civilization as it is understood by US sports fans.

National finances are in no better shape.

Extrapolated Federal Reserve statistics suggest that their assets will be completely unwound by the end of 2027, by which time interest on all US debts will have become unpayable and the dolphins will have departed, thanking you for all the fish.

The banks are expected to survive by making loans to each other at very reasonable rates, assuming they can still get somebody to dole out the Purina Banker Chow between the main martini courses.

It gets worse the more you look at it, so it will only get better if you ignore it entirely.

In 2012 I retired from a large company in Silicon Valley; the last couple years before I left I volunteered to help with college entrant recruiting.

My firm (and most in Silicon Valley) would not even consider new graduates with a BA degree (wouldn’t even interview them). For new entrants, we required STEM graduates with BS degrees; accounting & rigorous business BS degrees were also acceptable.

Graduates with BAs & a couple years good experience were employable, just not as college entrant hires.

Frankly, from what little I know of BA degrees, I found it refreshing that Silicon Valley was that dismissive of the BA degree.

I have a BA in English with a 3.9 GPA and a BS in Computer Science with a 3.98 GPA. I worked a lot harder on the BA. Lots of term papers with a huge amount of time spent on research in the library. I know plenty of STEM grads who are complete illiterates.

And yet, one could easily surmise that you yourself have a BS degree.

Yea, but I wasn’t involved with the thousands of companies who independently made that hiring requirement decision.

Whether either of us likes it or not, at graduation, the market values BS degrees 20-40% higher than most BA degrees. This is relevant because 53%+ of Millennials profess to expecting to be a millionaires (http://money.com/money/5308043/millennials-millionaires-new-research/)

Like I said in my original post, BA-holders with experience were certainly employable. At some point in migration from college graduate to executive, the specific degree becomes subordinate to negotiation, collaboration, business vision and effective leadership skills. However, only about 25-33% will serve as executives because of the limited number of positions.

Students are certainly entitled to earn any degree they can “afford”, and therein lies the rub: The class of 2016 graduated with an average student debt of $37,500. The higher BS salary would seem to come in handy for managing that stunning “just graduated” debt load.

All very nice, Mr. Chip, and possibly true. Not that it matters.

The fact is, US workers are going to get screwed no matter what they do, because the system has been corrupted to guarantee it. And every time they make the slightest peep of complaint about a system rigged against them, the rich and powerful tell them to shut up because it is all their fault.

One percenters instruct them to work harder, pull themselves up by their bootstraps and stop bellyaching. Just get a second college degree, a second skill, a second job. Just send the spouse to work, downsize, take a staycation instead of a real vacation. Or don’t take one at all, just work harder and longer and better. So they do, but no matter what they do, it’s going to be worse for them next year, and the year after that. The solution is to change the system, which is stacked against them.

That’s what all the data says, and there’s a lot of it.

Federal Reserve policies, the subject of the present article, are only important to the 99% as opaque guidance into how much they’re going to be screwed in the future, but it’s a cast iron certainty that they are indeed going to get screwed.

This is one of the most ridiculous things I have ever heard. Math is one of the liberal arts. Economics is also one of the liberal arts. My degree in Computer Science is a BA.

Unamused

(I now understand the derivation of the name).

I’ve never heard any of the 1% (as you call them) say any of what you allege you’re being ordered to do.

Just because the world (well, actually, the US economy) doesn’t work EXACTLY the way you want it to does not mean the system is corrupt, everybody besides you is a crook, or you’re being enslaved or screwed.

However, it does mean you’ve entered the very competitive US job market and are competing against 129 million other full-time employees (plus 28 million part-time) for recognition, advancement and/or money.

There will be no more participation medals here.

Petunia

You introduced the “liberal arts” taxonomy; I never used the term as I specifically referred to STEM (science, technology, engineering, mathematics) with BS degrees.

Accurately describing a new college graduate Silicon Valley hiring practice was intended to enlighten, not irritate.

Median wage for HS grad was $37k in 2017; College grad was $62k (Source = BLS). Wage growth has been strong over the past couple years as unemployment falls to the lowest point in a 1/2 century. Wage growth would be even stronger, especially at the lower end, if not for immigration. So the typical HS grad has a wage problem, which is being made worse.

Increasing govt subsidized loans has resulted in higher cost, which has been met with making more subsidized loans, which drives costs higher. It is circular, self-reinforcing and broken. The issues are persistent enough to lead one to think it has been an intentional political strategy. The amount of pandering that we will likely see on this issue in coming months would strongly support that notion.

Capitalism’s recent corruption through government intervention changed the parameters of the way money flow occurs. Analogous to an old computer where new software is constantly added to fix the chips deficiencies since the initial corruption.(QE)

Ultimately, we need to start over with a new defined meaning of capitalism; where the boundaries of government inflation inducing money creations are not allowed to warp the countries balance sheet beyond accepted standard defined accounting health. What has become innately learned probably can be/was proven mathematically through historical re engineering of what has happened and how the income disparity was induced directly related to QE.

The fed is not ready for the change, the bloodletting, the slow down, the smoothing of the income discrepancy curve, the deflation, the recession, the depression, the war, the riots. The last few only happen if they continue to fuck around corrupting the system more and more and more…

They have gone too far, they will have to bail out the student loan generation after they charged that group high interest rates while they got paid by the government for doing absolutely nothing. And I know it is not a true capitalistic proposal, but we stole from their future. Just being as evil as they were:

Quid Pro Quo, Clarice, you ask a question, then I, do. Your question was “What more could you possible want to know?” I answered, now, Clarice, Quid Pro Quo, has the Lamb stopped screaming yet?” he asked, his perverted eyes filled with evil. The fed created the monster, now deal with it.

Deflation would be welcome and necessary for this next generation of GDP participants

The bond experts are puzzled, they predicted interest rates rising. The sheer size of the existing (global) bond market tamps down the value of new issues. The principle value of new issues is lower with higher yields and USG cannot afford to pay those rates anyway. Bond buyers want the collateral value, so it will be interesting to see that play out. Can they still buy on margin, at what rate? How fully can they collateralize?

I fully expect the government to set the yield too low, and the price at auction to be set at a discount. The purchasing power of the dollar has been in a multidecade slide, Fx has propped up the market artificially. That will give out, and the monetary base will contract. JP will be handing out two tens for a five, bail-ins and all that other nasty stuff. Gold will take a hit on that account I am sure. The public will assume everyone is in the same boat and they will go along for the ride.

I would like someone to demonstrate to me that outright forgiveness of these student loans would be worse for the economy than the ex-students paying them back – which means many can’t buy homes or perhaps even a car for as far as the eye can see.

Your proposition is not something that could be supported or undermined with a demonstration. That was clever. You get points.

Your point is quite valid, but loan forgiveness itself, while it does mitigate the situation for its intended victims, does not actually resolve the underlying problem, which is essentially the result of the usual venal corporatist politics. And they’re not about to allow any resolution that doesn’t fatten their bottom lines.

Eric Best,

You don’t need forgiveness of student loans. Just allow them to be dealt with in bankruptcy court, like other debts. If the borrower is able to make payments, the court will see to it that it happens.

And make universities where these people went to school eat the first 30% of the loss.

One of the problems with debt forgiveness (there are many problems with it) is that it is IMMENSELY unfair.

Some poor schmuck, like me, who works full-time (say, security guard at night and weekends) while going to one of the cheap schools full-time, and emerges with no student debt, gets nothing.

And someone who went to an expensive school, didn’t bother with a job, blew a ton of money on electronic devices, concerts, pot, and what is really — compared to the dumps we lived in — luxury student housing, gets his debts forgiven.

And the poor schmuck, as taxpayer, who got nothing from the debt forgiveness, now gets to take the loss on this asset from the guy who went to an expensive school and was too lazy to work while in school.

Remember, student loans are an asset on the government’s financial statement that belongs to the taxpayer. Debt forgiveness destroys that asset. There is no free lunch.

And people need to learn the meaning of “debt.” This meaning is NOT “free money.”

Well said Mr. Richter.

Actually, everybody already has forgotten that in the old days, people with more debt than assets from their student loans could indeed easily default on their loans and walk away scot free just like corporate raiders and PE firms who saddle a company with debt and strip the assets, declare bankruptcy and then walk away not only scot free, but much much richer than before, by using the generous bankruptcy laws of this country

All that got changed with law changes in 1997 and 2005, as bankers howled about having their student loans get vaporized by these irresponsible leeches/former students. The criteria for being able to get out of a student loan were tightened so much as to make it nearly impossible

Hey Wolf! Here’s a Modest Proposal! Let’s apply the same standards to PE firms and other corporate debt holders! Make the CEOs and CFOs and Directors on the Board PERSONALLY RESPONSIBLE for the debt of their company! No more loading the company up to the gills with debt paying themselves off richly and then walking away in bankruptcy court!

Right – people need to learn the meaning of “debt”. This meaning is NOT “free money”

You mean like ZIRP? ZIRP is not free money for financial institutions and corporations?

You are not Irish, but did you know that during the darkest days of the Irish Potato Famine, as the poor were starving by the hundreds of thousands, Ireland remained a NET EXPORTER OF FOOD. The wealthy landlords, mostly English or their Irish favorites, continued to grow wheat and other crops not affected by the blight, and exported it for profit while the little people starved to death

The little people just don’t rate for getting the same breaks, right, Wolf?

Gandalf,

Shareholders of a corporation that defaults on its debts usually lose their entire investment while creditors take over the company.

PE firms play a different game. They might lose their equity stake as shareholders when their portfolio company goes bankrupt, but they strip cash out before that happens leaving the creditors hung out to dry.

Huh?

I think you need to read up on U.S. student debt, Wolf.

Student debt is well known to be riddled with fraud and not feasibly dischargable via bankruptcy.

Fraud = debt forgiveness, which you falsely claim can be had be bankruptcy.

The common sense solution is debt forgiveness for student fraud loans.

Biden and Obamanation and Republicans and Democrats created this debt slavery.

Get your facts straight, man.

timbers,

You bitch about something I didn’t say. You didn’t even read what I said. I said right up front: “Just allow them to be dealt with in bankruptcy court, like other debts.”

It’s a waste of time to argue with someone who is not even able to read what I said.

I do agree with you about the fraud problem. But the solution to fraud is JAIL for the perpetrators not debt forgiveness for everyone who isn’t even a victim of fraud.

Neither the Fed nor the Government give a damn about fair. They government cares about buying votes and the Fed cares about being richly rewarded from those who have profited from their policies (quid pro quot).

Student debt will be forgiven. The government will forgive the debt and the Fed will monetize government deficits.

When trying to figure out which path humans will follow just look for the easiest, laziest escape route possible – that is the guaranteed course. The debt will be forgiven and the dollar will hyper inflate.

Colleges thrive on the ever expanding student debt. The college towns benefit as well. The government assumes the risk. And the students become debt slaves.

The non-dischargeability of student loan debt is perhaps the most perverse subsidy in all of history.

Bankruptcy would be fine for student loans. It is what the banks should have gone through, but they got the free money.

Agree with the bankruptcy option for student loans, however, if not, then quid pro quo.

@setarcos: Interesting stat “colleges raised tuition by 60 cents for every new dollar of subsidized loans the govt makes available”. Could you please share a link?

I will trade the list of universities with > $1B in endowment funds for that: https://www.nacubo.org/-/media/Nacubo/Documents/research/2018-Endowment-Market-Values–Final.ashx

GP, try https://www.newyorkfed.org/research/staff_reports/sr733.html

or search for Credit Supply and the Rise in College Tuition: Evidence from the Expansion in Federal Student Aid Program

BTW, the IOER thingy didn’t work. The problem today (Friday) is even WORSE than before the tweak. As Jeff Snider of Alhambra, asks, “Where are the dealers?” No economic activity, no loans. Period. Wolf is deluded by the $1.whatever liquidity ” sloshing around” in the system. It is a mirage.

The banks have already sniffed out the repo facility proposal, as well as all other proposals. These are scams. The banks will hold on tight to their money. Meaning a liquidity crisis, which is well under way, meaning an economic collapse, which is also well under way.

Why did you drink the koolaid, Wolf?

“Why did you drink the koolaid, Wolf?”

You said several days ago that I was nuts and wrong with my thinking that the Fed wouldn’t cut its target range by 50bps on Wednesday. You said it would cut by 50 bps, and that it was a fact because Nomura said so, which proved me wrong, you said. You told me to “change your thinking.”

Well, meanwhile, the Fed didn’t cut its target range, neither 25 bps nor 50 bps, and you were completely off the wall with that comment. Now you’re even more off the wall.

IOER replaced the overnight lending business conducted by traders at the banks. When IOER killed that business, those jobs disappeared. Now the banks don’t have anybody who can make those split second decisions with the bank’s money. That’s why they can’t really wind down IOER in a flash, the market for overnight lending was eliminated, those traders moved on.

I think we need to keep this simple.

The market for Reserves are way too small now, about 60-80 billion overnight. Actually it makes the Effective Fed Funds rate rather insignificant.

The tri-party and bilateral repo market which are secured by securities is another thing. Although still smaller than what it used to be compared to 2008, you can see the repo rates are more tied to Treasuries and therefore higher.

The other Fed Market in ON-RRP is there to provide interest earnings to foreign banks and FHLBs.

That said I can’t figure out why lowering IOER a tiny bit should make a difference for the banks who’d rather keep them for HQLA purposes than figure out how to lend them. Maybe they simply want to increase the interest left to give back to the Treasury as the newer rates have dropped.

Worldwide QE is right at record levels, even though the Fed is doing some trimming. Other central banks have picked up the slack. In addition, the Fed told the world that they would stop reducing the balance sheet later this year. No real story here.

The president is lucky. The media triggered a housing price stall by painting the news with house price crash fears ahead of the midterms … clearly, politically motivated. That gave the Fed the room it needs to curtail QT. Eventually, all the house buyers that held their purchase has formed a dam that will break shortly. Get ready for a house price spike … then, we will see what the Fed and other central banks do.

Certainly, because of America first policy from the white house, central banks will tighten ahead of the American election. Face it, other countries do not like the current administration because of new trade policies. They will attempt to unseat him by rocking world markets next year. Get ready.

True. China announced stimulus of $410 billion (tax cuts and Govt. bond issuance) in March of this year.

Valuations will continue to be supported. Heck, Tesla is up 10% n 2 days. These are very good times.

=> The president is lucky.

There are other names for it, any of which would no doubt result in the usual fatuous retaliatory tweetstorm.

BHO was able to ‘fix’ the US economy only by letting hordes of malicious FIC perpetrators off the hook, which allowed them to unleash liquidity sufficent to ensure a reprise of the 2008 downturn before the end of his successor’s first term.

He had political foresight, that one, regardless of how he can be faulted for expanding his predecessor’s heinous imperial policies. For his own part, Trump has quite unwittingly managed to get ahead of this poison pill by loading up on even more irresponsible debt, further guaranteeing an even worse outcome at some future date which I continue to decline to specify because it’s supposed to be a surprise.

=> Get ready.

Get out of range. No telling where that might be.

I’ll believe it when I see it.

The top-8 countries (US, China,Japan, Germany, UK, India,France and Italy) represent 52% of the 2018 $80B global GDP; effectively, US, China and Germany (which is now in recession) are the major players. In case you’re wondering, Russia comes in about the size of Australia.

160+ of the world’s roughly 200 nations have smaller annual GDPs than the $650B the Fed has taken off its balance sheet since 2015.

I’m unaware of any nation on earth that does not have a explicit/implicit “my nation first” policy (please inform me if you know of one that does not…).

Frankly, it’s long settled that no one gives a crap if international leaders actually “like” each other, including Trump. Toward the end of his presidency, nobody actually trusted Obama (Remember the “red line”? Remember Lybia?). Both the British Prime Minister (Henry Thomas, 1850) and Charles de Gaulle (c. 1968) said “Nations have no permanent friends or allies, they only have permanent interests”.

The global economy goes up; the global economy goes dow. Only a couple nations can even pretend to independently and directly impact it.

– Fed shed, but Warren Buffett add, at the Nasdaq 100(NDX) top.

You have to be an idiot not to buy Amazon.

– The NDX, monthly, linear, in an uptrend channel :

1) the resistance line come from March 2000 top @ 4,275.72

to Apr 2019 top @ 7,851.98, the latest high.

2) Support is a parallel line coming from Oct 2002 bottom @ 795.25

– The NDX was the most oppressed, abused and laughed at

the bottom of 2002.

– Analysts advice was to stay away from the NDX junk, because it was

the weakest.

– But when the DJI & the SPX fell in March 2009 bellow the previous

2002/2203 low, the NDX made a higher low.

–

– The 2 years period between 2014 and 2016 enabled the NDX to breach the March 2000 peak.

– During the 17 months between Oct 2014 to Feb 2016 lows, the

NDX made three higher lows.

– When the NDX jumped, after Nov 2016 election to become the most beloved index, investors moved in, enjoying the bubbly ride.

– Warren Buffett accumulated AAPL first.

– BRK leader decided to shock the world and the most beautiful CNBC girl, like a teenager trying to impress the queen, on a date.

– Grow up Munger & Buffett, after all u are hovering around the 90’s,

the NDX will spin, because the correction will come.

Don’t worry Michael Engel.

I am sure you will have another chance on Monday to figure out the direction of the market. You seem very bright.

Charlie & Warren are fortunate to have such an experienced advisor.

Gobbledygook.

Buffet has been buying tops for a while now, he’s losing his touch.

Buy amazon at 2k? Yeah, what could go wrong there…

Maybe this is superstitious in my part, but my gut feeling says a crash is coming at the end of the year.

It’s just very unlikely to have a crash the first year of a new decade. In the last 250 years, it’s always been at the end of a decade. In 1907, 1929, 1987, 1999,2008-2009.

Many are predicting 2020 for a crash, but I strongly feel it’s more likely to happen this year or not at all. Maybe it’s something about the human psyche and starting fresh in a new decade.

We would need a black-swan event. What could that possibly be at the end of 2019?…

The Fed is trying to juggle twenty balls on one leg, at night, in a windstorm, and on a railroad track, and you want to identify exactly what will cause the balls to drop?

Why does it matter? All we know is that Trump continues to add more balls to the act, and the end is clear and inevitable (i.e., baked in the cake, some would say).

Pretty soon there will be 10 rich people and 10 billion poor people hearing the economy is the strongest it’s ever been.

Alternative view:

“Over the last 25 years, more than a billion people have lifted themselves out of extreme poverty, and the global poverty rate is now lower than it has ever been in recorded history. This is one of the greatest human achievements of our time,”

World Bank Group President Jim Yong Kim, 2018

$580 B seems quite notable to me, must take a lot of catalyst to dry this quantity of paint.

The Fed’s “New” balance sheet plan

Wolf,

Under the old plan, the Fed was slated to shed in May;

UST – 49.5 and MBS – 24.8 for a total of – 74.3

Could you please update the Fed’s new plan?

It will be very interesting, to compare what the difference turns out to be.

A ‘hard’ or ‘soft’ paring back of roll offs.

Under the old plan, the May total would have been “up to” $30 billion in Treasuries and “up to” $20 billion in MBS. So the caps would have kicked in.

Here is the new plan, including the amounts in May, and for each month through September, and the total difference between the old and new plans:

https://wolfstreet.com/2019/03/20/feds-new-balance-sheet-plan-get-rid-of-mbs/

So “roll off” means repay the Bond Holder at maturity, presumably with (newly printed) USDs?

It’s the other direction now. To increase the money supply, the Fed originally bought bonds using printed money. Now, the debtor repays the Fed back with USD, which the Fed essentially “destroys” since it’s not send the USD back into the system by repurchasing replacement securities.

“Roll off” means the US Treasury borrows money from the market (issues new Treasuries) and sends this money to the Fed to pay off the maturing Treasuries in the Fed’s portfolio. The Fed then destroys this money. This is the opposite of “printing money.” Hence “QE Unwind.”

I’m on tenterhooks, waiting to see when the inflection point occurs with Fed unwinding and all other central bankers simultaneously trying to wind it all in. I’d currently place a bet on the Fed reversing course soonish.

Ignorant question from me, though: Why is the Fed now targeting shorter maturites? Currently it would seem in the interest of government to sell long dated stuff whilst they still can at low rates.

Is it for the same sort of reason as the BoJ, as in a desire to target the yield curve? Or is it all just to let them respond more rapidly when, as they maybe see it, crap unfolds and longer term bonds dive, so they can later switch and heap in on longer term stuff as needed?

If so, doesn’t the whole ‘tightening cycle’ of trying to get rates higher and maturities shorter reek a bit of desperation?

BRILLIANT! With the Roll Off proceeding at full speed we’re looking at a rate cut. Well to this mind, rates should never have been raised until and after the Roll Off sped off to 2009 levels.

Color me concurrent.

“we’re looking at a rate cut”

Not quite. Wall Street is clamoring for a rate cut. You should have listened to Powell. Economy is doing fine. No rate cut needed. No rate hike needed. During the Q&A, he swatted at all the clamoring for rate cuts as if they were pesky flies.

What Powell says should be taken with a grain of salt. As he has shown us recently, he can do a 180 on the turn of a dime.

When the subject turns to central bankers and their schemes color me skeptical.

The central banker’s first job is to sow confusion such that no one seems to be sure exactly what they are up too.

In the interest of maintaining my sanity, I ask myself just what is it that central banker’s do?

Print more money and create more credit out of thin air!

It is the only thing they know how to do!

Central banker’s do not know how to solve problems since none have ever worked in the real world.

The central banker’s solution to every problem they encounter is to throw more money at the problem hoping the money sticks!

Never mind that the current problem they are facing is a creation of their own making!

Just throw more money at the problem and make it go away!

Mr. Richter, good analysis and explanation of the Federal Reserve’s current and future actions. Keep in mind that the treasuries that are set to mature ten years or more were issued before 2009 when interest rates were higher than our current treasury rates-they should be trading at a premium/above par. I have also included a link by Ray Dalio, although I do not agree with his economic theories or way of thinking. Ray’s ideas on monetary policy 3 should be read if for no other reason than this is the current thinking of the Wall Street Elites.

I would also say that J. Powell is probably one of the best Federal Reserve Chairmans we have had in quite a long time.

https://www.linkedin.com/pulse/its-time-look-more-carefully-monetary-policy-3-mp3-modern-ray-dalio/

Ok, lets get this strait.

The Fed increases the balance sheet, and stocks go up, and inflation that was supposed to happen never did.

The Fed decreases the balance sheet, and stocks go up, and deflation that was supposed to happen probably wont.

Got it.

The Fed pumps money into the big banks, and the things the big banks like to buy, like Stocks, have heavy inflation. But of course there is an opportunity cost in that the money doesn’t go to ordinary people so the stuff ordinary people buy doesn’t see inflation. The Fed starts to pull that money back from the big banks, Stocks suffer a bit of a dip, and all the bankers yell in pain. But nobody wants to let ordinary people have any of the money, so there isn’t any big inflation in the things ordinary people buy.

Plain as the nose on your face, now these big banks who levered up with the FED’s help during a crash orchestrated by the usual suspects are again positioning to hoover up assets from weak hands on the next big plunge, however deep and whenever it occurs, is up to the FED’s masters.

Wolf…..what makes you believe that the data coming out from the FED is accurate? There is no real audit of the FED nor any third party verifiable data that is not based on FED numbers. So why do you take their word at face value….

You’re wrong. There is a financial audit of the Fed every year. Those financial audits cover the simple stuff like assets and liabilities — the stuff I’m talking about here. You can check out the audited financial statements here.

When folks talk about “audit the Fed,” they mean a full operational audit about all their dealings, their interactions with other central banks, company CEOs, Wall Street tycoons, hedge funds, etc.

There were already two of those audits. The second one in 2011, I covered”: The GAO Audit of the Fed Doesn’t Call It ‘Corruption’….

I would like to see a full GAO audit of the Fed every year to see what they’re up to. But the financial statements are the easy stuff. The folks at the Fed would be STUPID to fake those. They’re way too smart to try to do this.

An operational audit of the US Federal Reserve would reveal the most intricate insider trading information ever to be known on the planet.

And you believe these “Independent Audits”….almost every Fortune 500 company massages “cooks” its books with these same audit firms. Its these firms that are behind the laws that we enact to allow such misreporting… trust me Wolf…I spent many years at the GAO…there is no such thing as an Audit of any kind of the FED. Its all managed accounting. I am selling a bridge in Brooklyn…interested?

The thing is, once you cook the books, it becomes obvious sooner or later. And it’s documented in writing. People who think the Fed cooks its books don’t understand just how powerful the Fed is. It doesn’t need to cook its books. It doesn’t need to show a profit or earnings per share. No one cares about this. It has bigger priorities. And those priories have nothing to do with its financial performance. You always need ask about the motivation for the crime.

And you cannot cheat with Treasury securities. They’re recorded electronic entries — because that’s the only way they exist.

Thank you! I’m the sort of engineer who always asks why? And I’ve been asking why? about yield curve inversion. You just told me who’s been buying all the 10 year bonds and forcing that end of the yield curve down. Thanks Wolf!

May 1, 2019 Credit Card Charge-Offs Hit The Highest Level In Nearly 7 Years And Credit Card Delinquencies Hit The Highest Level In Almost 8 Years

Red flags are flying in the credit-card industry after a key gauge of bad debt jumped to the highest level in almost seven years.

http://endoftheamericandream.com/archives/credit-card-charge-offs-hit-the-highest-level-in-nearly-7-years-and-credit-card-delinquencies-hit-the-highest-level-in-almost-8-years

Mr. Richter:

=> I said right up front: “Just allow them to be dealt with in bankruptcy court, like other debts.”

Yes, you did. But you didn’t mention that student loan debt is extremely difficult, but not always impossible, to discharge in bankruptcy court. Such cases are regularly described in evaluations of the case law as “rare”.

For now, most federal courts of appeal, but not most lower courts, have adopted the Brunner test, and very few borrowers have the means to appeal the rejection of their cases. The law in this area might now be changing, precisely because it has long proven to be almost impossible, and in many courts completely impossible, regardless of the circumstances.

The law states that the bankruptcy plaintiff must show that payment of the debt will impose an undue hardship on the borrower and the borrower’s dependents, that the borrower has shown a good-faith effort to repay, and that this situation is likely to continue. In practice, this typically requires showing that borrower has already been reduced to poverty and has been rejected for employment as a result of poverty and student loan debt, and has no prospect of ever being able to repay the loan anyway.

You can find a handful of cases, out of thousands, where the court has been more lenient if it can be shown that the borrower’s circumstances might be salvageable. But I could cite for you many more where courts have rejected claims under any condition at all, including those where people have died of old age and disease and despair, in poverty and with student loan debt unpaid, because their cases were not only dismissed, but dismissed with prejudice, with no hope of any recourse whatsoever. The case law really is that extreme.

Contrary to your assertion, it is not at all “like other debts,” because if that were even remotely true, student loan debts and defaults would not have been skyrocketing for years.

I invite you to reevaluate your opinion.

I believe you misunderstand his intent. He said a solution is to treat student loan debt just like all other debt, i.e. dischargeable and not with a higher burden of proof. He did not say that it is *currently* like all other debt.

That would be a saving distinction, ZB, but the language does not make that clear and allows the statement to be open to interpretation, perhaps unintentionally. French, as the traditional language of diplomatic niceties, can be less slippery than English, much less American English, which may make it unfortunate that this discussion is not in la langue française.

As it is, student loan debt peonage makes for an excellent instrument of class war, which is how it was allowed to evolve, and no doubt why it has been preserved: it’s very profitable, not only for lenders but for the US federal government. That could make it difficult to change as seemingly prescribed. As it is, political machinations are churning to make other forms of debt less dischargeable as well, even heritable, and even assignable if legal pretexts are allowed and can be constructed. Meaning that hardly anybody could escape the risks and that anyone could become a target.

There are reasons why organised crime syndicates have engaged in loan sharking, and it was a grave error to have largely legalised it for corporate lenders. That is, except for lenders and other corporate beneficiaries of the class war, which war, as I stated some time ago, was actually lost by the people by 1987, for reasons directly and indirectly related to these issues.

Unamused, student loans are made by and subsidized by the US govt as virtually all private lenders exited the market a decade ago. Interest rates, if the loans are being assessed interest, are ~5% ranging up to ~ 7.5%. Default rates are double digits.

Explain how these loans are profitable if write-offs exceed interest.

Unamused,

Re-read my sentence. It was a suggestion — grammatically a command — for change of the rules: “Just allow them to be dealt with in bankruptcy court, like other debts.” It means that the established rules governing student debt in bankruptcy proceedings should be brought in line with the rules governing other consumer debts in bankruptcy proceedings. In other words, what’s good for auto loans should also be good for student debt. I’m not sure what’s so hard to understand about this sentence.

I remember the debate during the student loan debt reforms. The corporatists dusted off the “cadillac driving welfare queen” and replaced her with the “european backpacking hippie student loan defaulter.” Like they were really worried about hippies BK’ing en masse, backpacking in Europe, then returning to the real world in 10 years once their credit histories got clean…

While we’re at it, someone want to justify why the primary mortgage can’t be crammed down in BK, but mortgages for vacation homes and investment properties can be? Class warfare is so subtle…

=> Class warfare is so subtle…

So subtle that most people didn’t realise there was one until it had already been lost.

Stop gloating, Chip. It’s rude.

“Like they were really worried about hippies BK’ing en masse”

That is exactly what everyone who could did at the time …filed BK en masse. It was an extremely large consumer credit enema.

Do the numbers. A spreadsheet helps.

For 2019, $382.746 Bil of Treasuries are scheduled to mature.

Before: the amount to be re-invested was only $114.166 Bil.

After the dovish talk: the amount to be re-invested increased to $198.199 Bil. or at least $84 billion MORE.

Next year 2020, the amount (to be re-invested) increased to at least $209 Bil. more than the original $82 billion.

If that is not enough, wait till the Fed actually buys Treasury Bills from the Primary Dealers in the next QE, when they let some MBS mature and buy Treasuries FROM THE OPEN MARKET.

By the end of 2020, the Fed has essentially erased Q.T. Yes, erased.

About $490 Bil. of Treasuries will be re-invested, and Q.T. from the beginning wiped out about $491 billion (including MBS also).

If you add the forthcoming MBS swap to Treasury bills, it’s like Q.T. did not ever happened. Excess Reserves will increase again.

That was the most confusing train of thought I’ve witnessed this week, not saying it doesn’t make sense to someone but it left me with a hole in the head and no idea of what the point was.