Condo prices fall year-over-year in New York. In San Francisco, SoCal, & Seattle, year-over-year price gains shrink to nearly nothing. Despite the hype, Boston prices decline. Denver, Dallas & Atlanta eke out records.

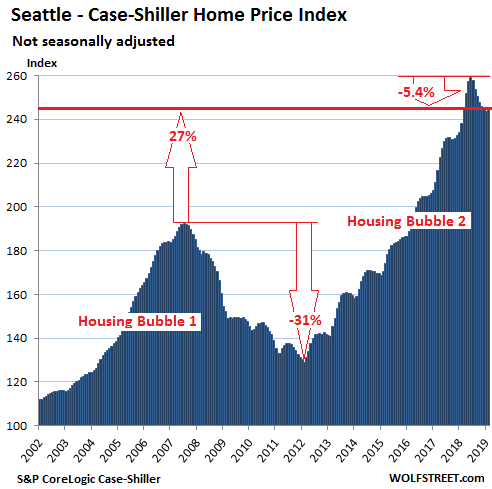

After seven months in a row of month-to-month declines, prices of single-family houses in the Seattle metro ticked up 0.57% in February and are now down 5.4% from the peak in June last year, according to the CoreLogic Case-Shiller Home Price Index released this morning. The index is now flat with March last year, and the year-over-year gain has been whittled down to just 2.8%, the thinnest such gain since June 2012, as Seattle was beginning to bounce off the bottom of Housing Bust 1.

And this monthly increase of 0.57% is merely one-third of the monthly increase in February 2018 of 1.74%. The index remains up nearly 27% from the peak of Seattle’s Housing Bubble 1 (July 2007):

The Core-Logic Case-Shiller Home Price Index is a rolling three-month average; this morning’s release represents closings that were entered into public records in December, January, and February.

San Francisco Bay Area

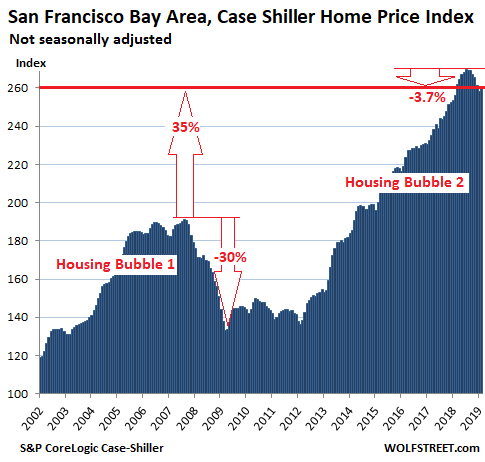

After six months in a row of month-to-months declines, prices of single-family houses in the five-county San Francisco Bay Area – the counties of San Francisco, San Mateo (northern part of Silicon Valley), Alameda, Contra Costa (in the East Bay), and Marin (in the North Bay) – ticked up 0.6% in February.

This leaves the index down 3.7% from its peak last July, and the year-over-year gain shrank to just 1.4%, the meagerest year-over-year gain since April 2012 when Housing Bust 1 had bottomed out. The index remains 35% above the peak of Housing Bubble 1:

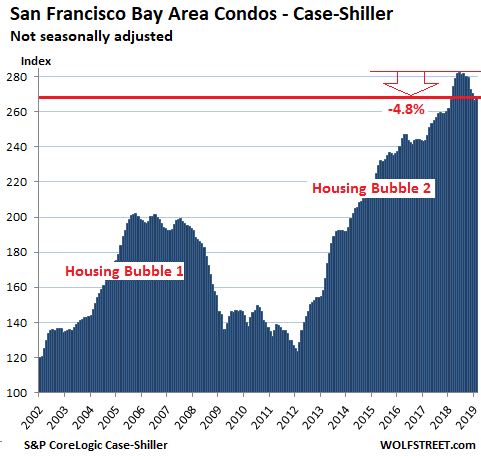

For the San Francisco Bay Area, Case-Shiller also provides a separate index for condo prices, which, after eight months of declines, also ticked up 0.6% in February from January. Condo prices are now down 4.8% from their peak last June, clinging by their teeth to a year-over-year gain of 0.3%:

A measure of house price inflation

The Case-Shiller methodology is based on “sales pairs”: It compares the sales price of a house in the current month to the last transaction of the same house, which might have occurred many years earlier. This eliminates the issues of “mix” that can skew median price indices and the issues of a few big outliers that can skew average price indices. The Case-Shiller index tracks changes in price of the same house (sales pairs) over time, and thereby it tracks how much more dollars it takes to buy the same house: in other words, it tracks the purchasing power of the dollar with regards to the same house over time. This makes the index a good measure of house-price inflation.

The index was set at 100 for January 2000; a value of 200 means prices have doubled since the January 2000. Every market on this list of the most splendid housing bubbles in America, except Dallas and Atlanta, has more than doubled since then.

New York Condos:

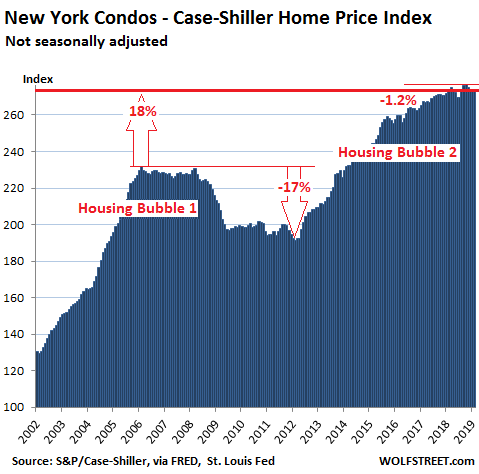

Condo prices in the New York City metro remained essentially unchanged in February, compared to January, are down 1.2% from the peak in October, and are down year-over-year a tiny 0.2% from February last year. This is the first metro on this list of the most splendid housing bubbles in America where prices are down year-over-year:

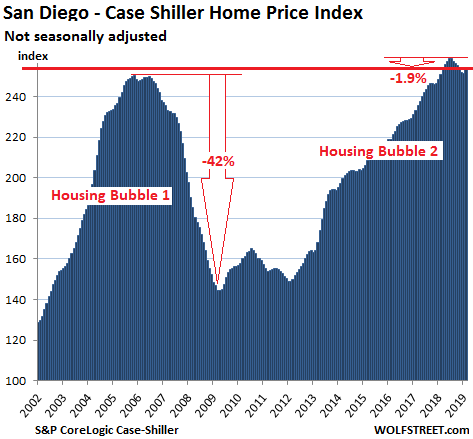

San Diego:

After six month-to-month declines, house prices in the San Diego metro rose 0.9% in February from January and are now down 1.9% from the peak last July. Compared to February last year, the index is up just 1.1%:

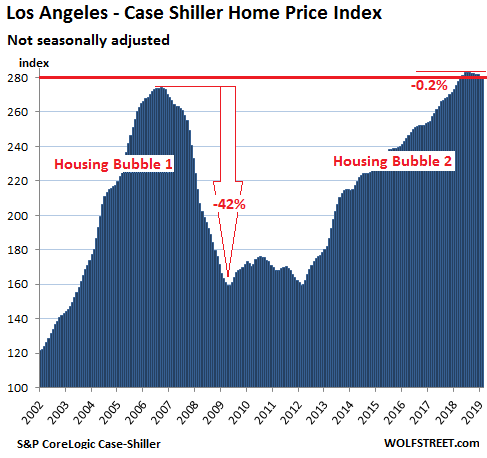

Los Angeles:

The Case-Shiller index for the Los Angeles metro was flat in February compared to January, leaving it down a tiny tad (-0.2%) from the peak in July. The index is up just 1.8% from February last year:

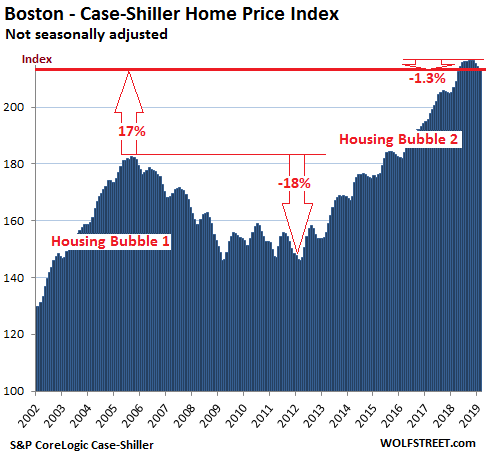

Boston:

House prices in the Boston metro declined 0.4% in February from January and 1.3% from the peak in November. The year-over-year gain eroded to 3.2%:

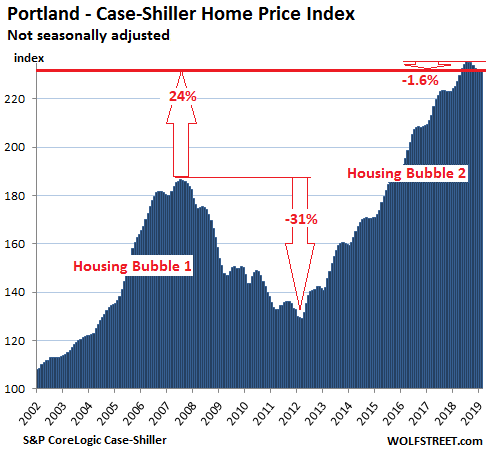

Portland:

House prices in the Portland metro were essentially flat in February compared to January, and remain down 1.6% from the peak in July 2018. The year-over-year gain shrank to 3.0%:

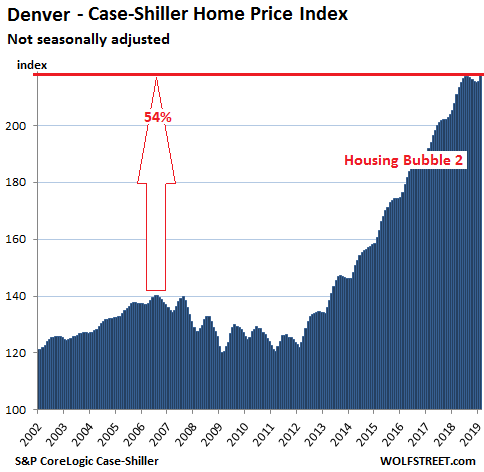

Denver:

After ticking down by tiny increments month after month from their peak in July last year, House prices in the Denver metro rose 0.9% in February compared to January, which made up for the tick-downs of the prior month and surpassed by a hair the prior peak in July. But the year-over-year gain shrank further to 4.7%:

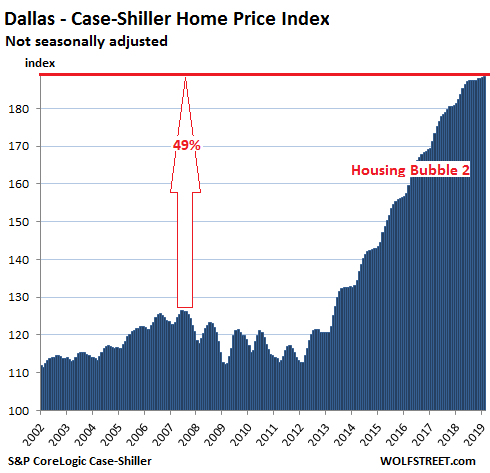

Dallas-Fort Worth:

The Case-Shiller index for the Dallas-Fort Worth metro ticked up in February from January to eke out a new record. Since June last year, the index has inched up only 0.7%. This leaves the index up 3.4% year-over-year, the slowest price gains since 2012:

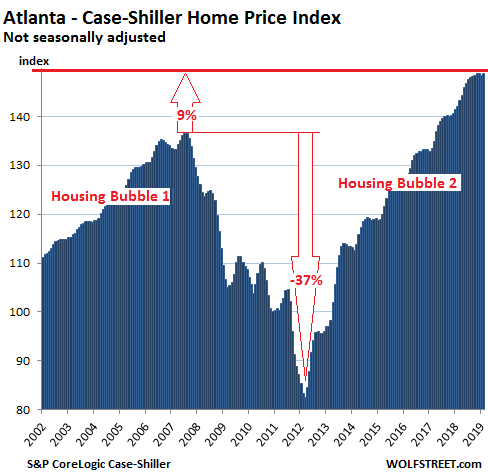

Atlanta:

In the Atlanta metro, house prices ticked up in February from January matching the record levels in November and December for a flat spot at the top. The index is up 4.7% year-over-year:

So finally, sales volume of new houses is ticking up. Read… Cut the Price and They Will Come: New House Prices Drop to December 2014 Level

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The Bay Area housing market is very diverse. Santa Clara county is down 10% I think from last March. The South Bay is reeling from the pullback by foreign investors, while the rest of the Bay Area is not so reliant on them.

The prices in Santa Clara county are so ridiculous. I would not be surprised if house prices down here fall another 40-50%. The growth income for tech workers has been the lowest in the South Bay, but prices are the comparable to the Peninsula. Something has got to give.

The funniest thing is to see all the overpriced houses with the 8’s in the price languishing on the market. Foreign investors can’t hold this market up forever.

I looked up our first house in East San Jose foothills back in 1976, 3/2 slab 1150 sq ft for 27K. Zillow has it now for 851K. the current residents purchased it in 2012 for 258K.

Prices of houses in Bay Area counties vs. the Boston counties

Boston

Norfolk-$503,000

Suffolk-$564,000

Middlesex-584,000

San Francisco

Marin-$1,151,000

San Francisco-$1,353,000

San Mateo-$1,234,000

Alameda-$892,000

Contra Contra-599,000(includes Oakland)

Why so substantial a difference?

Chinese hot money doesn’t want to fly/live in Boston

Silicon Valley bubble is not in their backyard

No Prop 13 keeping people in their houses

More buildable land/geography –

Likely doesn’t have the rampant limousine liberal NIMBYism and zoning laws we do around here. (Remember, everyone here is ultra-progressive until it’s time to build a homeless shelter in your neighborhood or upzone for additional housing).

Adequate mass transit – a big factor that limits where you can live around here.

Snow.

GSW

You make a number of interesting points

Unless I read it wrong Prop13 is not going to be changed . You argument is logical that it will cause people to remain in their houses longer than they might otherwise.But baby boomers will get sick and eventually die and millennials do not have the income to buy their houses. So ironically Prop 13 will eventually cause an increasing supply of houses to come onto the market

No one can doubt that the Bay Area has attracted a good deal of hot Asian money.Some will remain in the Bay Area permanently, buy there is also no doubt that a large amount is subject to political and economic concerns in the FAR EAST. Repatriation of monies can only be bearish on BAY area real estate

Commuting is a problem in ALL major cities. Rte 24 was recently assigned the status as the worst commute in the country., even worse than the roads in LA.

BART is very limited both in the area that it serves and the quality of service that it provides. The NYC tri- state Area mass transit is exponentially better.I have not lived in the Boston area since the 70s, but at the time it was much better than The BAY area is currently.I recently moved to the south Napa area . I was amazed when people told me that they commuted to SF. They did so via using a motorcycle. Commuting to work in SF or LA or Miami or Houston can only be described as a disaster. This can only be considered a negative for real estate prices.Ironically NYC and Chicago faced this issue decades ago ; consequently their mass transit systems are well embedded into the infrastructure of the urban areas

Silicon Valley is obviously the epicenter for tech companies in the US. But Boston with MIT /HARVARD attracts some of the best talent in the world and generates a significant number(while obviously less than SF) of high tech companies.And many of these high tech companies both in SF and Boston are unicorns which generate negative cash flow.Eventually reality will reach even the tech area and such tech stocks will either eventually crash or go bankrupt. And when this happens the underpinning of the real estate market both in Boston and especially in SF will no longer exist.

The really scary thing about real estate in the BAY area is that it faces a confluence of ALL of these factors;tech stock crash,baby boomer dying,hot money from Asia becoming cold money and a general disgust among young people with their lifestyle in the BAY area( because of costs and commuting time)that real estate will be a disaster in the BAY Area for the foreseeable future

Last Sunday I rode the #323 bus from downtown San Jose out to the end of its line in Cupertino to go to the cherry blossom festival held across the street from DeAnza College.

I saw just tons and tons of empty buildings along San Carlos/Stevens Creek, all along it.

Whole Foods there was busy, though, and the cherry blossom festival was fun. I even got to toot a few notes on a few thousand $ shakuhachi.

I remember the days when you were a regular at doctorhousingbubble(dot)com.

Good times, haha! I had begun to think that you got hit by a bus / into a deathly altercation with a Cali-residing (transient) addict / food poisoning at some pseudo-posh dining or grocery establishment / weren’t able to justify the price of internet access anymore.

Where have you been? Your perspective is always a delight to take in!

According to NAR, Boston is the second hottest housing market in the country. This matches what I am seeing … bidding wars. Something is wrong with Case Shiller.

@SocalJim — Its all the children of the 1% (who make up the majority of the college student population) and rich Asians.. If you are single its better to live in a nice area and rent.. I pay $2080 a month for a 2 bed/2bath townhouse apartment outstide of Boston where houses now start in the 900Ks

Either the Boston economy is going great guns or Boston has a serious, serious problem with debt peonage.

It’s pro sports championships driving up prices in Boston, nobody wants to move away.

nic9075 – The high end of the market in Boston market should be getting clobbered just like the rest of the country’s high end neighborhoods. My observation is that $1.2M+ listings are sitting and going through rounds of price reductions while anything priced under $1M sells fast all across the country. Eventually, the inventory build in the luxury segment should compress prices in the middle of the market.

I’m increasingly hearing people say buying makes zero sense right now with current housing values. Why take on a $4K-$6K mortgage with very little upside in appreciation on a shack when you can rent for $2K-$3K ? I’ll keep renting until prices come back to 2012-2013 levels. If rents rise, we’ll move to a cheaper city. One of the advantaging of renting is mobility.

Back in the Old Days Boston had a respectable Tech Industry as its backbone ( anyone remember Wang or Digital?). Now it is the poster child for the soon to pop bubbles of the Educational Industrial Complex and the Sick Care Industrial Complex. Cash out while you can.

Enforcement of anti-compete clauses lead to the demise of the tech industry along Route 128.

Mass. also had a lot of companies making avionics and microwave/radar stuff. We’ve got a lot of their old catalogs from the 70s and 80s around here.

I have seen a number of the big money Boston homes are going to people in biotech, money management, and law. In contrast, big price LA homes seem to be business owners, athletes, and corporate executives.

In either city, tech people seem to be mostly priced out of the big money stuff. They seem to buy more of the upper middle housing tier.

I agree. These figures are wrong.

I see houses going under agreement in days/weeks at noticeably higher prices for what I paid on my similar split level ranch.

“I see houses” – How many? More than CS uses in their metro calculations? Sorry, but I’ll bet on CS being more accurate than your anecdotal observations.

That being said, it is clear that March has a bump and it is substantial, since CS is a three month rolling avg.. Most of us were expecting it this Spring and the real question is what happens after the two month pop is over. YOY comps get difficult quickly in several major metros..

How many? All of them. Not sorry, I go with my lying eyes over your CS anyday

When did you buy your split level?

timbers – You are probably in the mid to low end of the market. There still appears to be demand for the cheapest houses because the economy is hot. Sales are sluggish for large, expensive homes. It appears that this will be a top down correction. High end houses could go down 20%-30% over the next few years while houses below median could continue to appreciate. The low end of the market will be impacted more during the next recession.

The high COI, high tax Northeast and West Coast could be in for a 25% correction within the next 3-5 years. Flyover will probably fare much better. Boston metro should be close to ground zero for housing price deflation. Only places that are going to fair worse than Boston are NYC, Bay Area, Socal, and Seattle.

Another anecdote… and backing up the very unbiased analysis by Larry Yun. I am in the Boston suburbs and seeing things wildly different. The very hot suburbs are seeing homes sitting on the market. Many turnkey homes having open houses and getting 0 offers. That was much, much different the last three years. Bidding wars are down big time in the stats.

Here some analysis just released by the greater Boston association of realtors:

BOSTON — The number of single-family homes sold in Greater Boston this past February was almost 22% higher than the number of single-family homes sold in February 2018, and the median sales price of these homes was $577,500, a record high for the month of February, according to the most recent housing market data compiled by the Greater Boston Association of Realtors.

There were 586 detached single-family homes sold in Greater Boston this past February, a 21.8% increase from the 481 homes sold in the previous February, according to housing market data updated through March 10 by the Greater Boston realtors’ association. In Boston, there were 53 single-family homes sold this past February, an 82.8% increase from the 29 homes sold in February 2018.

The Greater Boston single-family home and condo market includes 64 communities within the realtors’ association’s jurisdictional area, which includes the Metro Boston region, the Central Middlesex region and three other regions. Please click here to see a map of the association’s jurisdictional area.

Jim Major, president of the realtors’ association and an agent with real estate agency Century 21 North East in Woburn, Massachusetts, said in a March 27 press release that home buyers can expect to see less upward pressure on home prices as the supply of homes for sale continues to rise.

An indicator of the supply of homes for sale is the number of active listings, which is the number of properties available for sale at the end of the month. In the single-family home market, the number of active listings increased from 2,007 in February 2018 to 2,056 for this past February, a 2.4% year-over-year increase.

Also, the same article goes on to note condo prices slipped a little more than 2% over the same time period. Anyone who knows Boston knows the condo price slip is due to the massive massive building of new condo units. But the single family prices rose almost 7%, and since more single family homes were sold than condos, the average price is higher, and it is a record, which directly contradicts the Case Shiller data showing a slight fall. Also note that this data showing record prices with increasing sales is also reported by the National Association of Realtors. So we have two groups of realtors reporting record high prices and increasing sales in metro Boston, we have numerous people seeing that, then we have Case Shiller reporting weakness. Case Shiller is the one that appears wrong.

Look, I’m not one to scream “fake news”, but if there’s a conflict between Case-Shiller, an unbiased economic analysis, and the NAR, which has been caught lying in the past, and has an obvious agenda, which would I listen to?

In the last two slumps impacting Boston, condos were a leading indicator. As the “stepping stone” home slips, those in that stepping stone stop upgrading.

SocalJim – Just as I thought. Luxury properties in Boston are getting crushed. Look for prices to compress over the next two years in the mid and low end. From CNBC:

“Demand for high-end homes is waning in large part due to changes in tax law. The amount of state and local taxes that homeowners can deduct was capped at $10,000, and the mortgage interest deduction was reduced from $1 million to $750,000 in mortgage debt.

“Not only do the new rules make it less desirable to purchase a multi-million dollar home in high-tax states, it has also motivated some people—especially those with big incomes and big housing budgets—to consider moving to places like Florida, Washington or Nevada, which have no state income tax,” wrote Redfin’s chief economist, Daryl Fairweather, in a release.

The shift in the luxury market has been more pronounced, therefore, in certain metropolitan markets. The average luxury sale price fell hardest in Boston (-22.4%), Newport Beach, California (-21.8%), and Miami (-19.3%). Miami’s drop may have been less about tax changes and more about overbuilding on the luxury end in recent years that has led to an oversupply of high-end homes for sale.”

Ed, something is wrong with those statistics. Prices have not fallen 20% in Newport Beach or Boston. All of Newport Beach is high end. And, the high end in Boston is moving. So much bad stats out there

Here is data from Newport Beach from corelogic …

92660 1.6M -18.2%

92661 3.8M 92.2%

92663 2.2M 43.9%

92657 3.9M 38%

92625 2.6M -10.6%

Those are the Newport Beach zip codes in the most recent corelogic report. If you weight all those price changes by the number of sales in each zip, you get a price increase of 8.2%. The -20% number in your post is just garbage.

“Something is wrong with Case Shiller”, nice, when angry, shoot the messenger. Where have I heard that one before.

Who’s angry? Oh – you. Project often? And what does shooting have to do with anything? You really shouldn’t own s gun, it shortens your life expectancy.

Your statement about guns sounds like you are pretty ignorant on the matter.

Unless you also are just scared of living in your city since I could say living in Detroit shortens your life expectancy and you shouldn’t do it, as it has one of the highest murder rates in the country. (See how ridiculous that sounds, as the majority of Detroit residents aren’t constantly scared of being killed in the streets)

Do you realize there are loads of areas in the country where basically everyone owns a gun and the crime rate is WAY lower than Detroit, which has heavy gun control laws?

You sound a lot like someone who is scared of something they don’t know much about since they just believe politicians and shark week stories… The fact you had to latch onto a common saying and derail a discussion about Real Estate with politically charged statements is pretty telling on that fact.

Maybe just relax and try to enjoy life?

Both the NAR and Case Shiller could be right. CS uses the change in price of each house from its previous sale, while NAR just reports aggregate price for those houses that happened to sell in a period.

If NAR price is going up, and CS is going down, then generally that implies that more high-end houses are selling (compared to low end), but they are selling for less.

There are so few homes that are sold and resold that their must be a lot of fixing the CS data to get an answer. And, what about flips … how do they know how much was put in before it was flipped? All secret stuff hidden by the CS team.

Good points.

1. Their methodology uses the word ‘flip’ only in regard to fraudulent transactions. The key word is ‘interval error’.

2. All transactions (price pairs) less than 6 months apart are not included, which would filter out very rapid flips (buy / remodel / sell).

2. Their methodology does assess the impact of remodeling, but only as an error to overall market price, and assumes the variance of this error grows linearly with time, and the latter price of the price pair is discounted according to an estimate of this error. (See page 21, interval error.)

Given this methodology, the price effects of flips that take more than 6 months (but less than several years) will be highly weighted in the index. But if CS is going down, that means it is going down despite the value-added (remodeling) flips, which it treats as a market value increase unless the two prices (sales) are less than 6 months apart.

“Housing Bubble 1” started in 1997 with the tax changes & capital gains exemption..

“Housing Bubble 2” is likely going to continue since the unemployment rate is 3.8% (and falling) and we don’t have $100 + oil prices and 6% mortgage rates.

And regarding Boston — is that graph just for the actual city of Boston or the entire part of Eastern Massachusetts east of I-495 which is considered being the “Boston area”.. In this current housing market prices in many cities like Revere, Lynn & Everett which would be considered working class have at least doubled (all are in the $400,000s) since 2012 and these are for properties which look old & shabby (triple decker room framed homes) that need alot of work

The unemployment rate is far higher than 3.8% and it sure isn’t falling. The government feeds the public whatever fairytale statistics it wants to.

“There are lies, damn lies and statistics.” –Mark Twain

But if the Fed starts cutting interest rates again, Housing Bubble 2 might well keep getting even more ridiculous.

Here in the UK we have the highest levels of employment since records began. The weird thing is that at my place of work, which is the largest employer in my town, they have laid off the majority of the lab technicians, got rid of cleaning staff and now the powers that be are removing the water fountain due to costs. We’ve never had it so good ;)

Same in my town low unemployment but everyone that graduates from university or college can’t find work lol

What’s next 0% unemployment with nobody working

nic9075.

The US introduced CG exemptions in 1997? Australia did too. I guess the timing could be coincidental, or competitive…

=>Denver, Dallas & Atlanta eke out records.

These markets can’t support their respective bubbles either, so they will follow the deflation of the others, in their turn.

Lenders avoid developers who want to meet the market with lower-cost housing because they’re out to maximize their rentier margins instead of pursuing normal profit. That will also change, but by the time it does, it won’t help them.

It does not pay a prophet to be too specific, so I’ll just say soon. Always in motion the future is, eh? It’s supposed to be a surprise anyway, and besides, it’s not something to look forward to. When severe distortions unwind it can be hazardous to your economy. People who are waiting for prices to normalise before buying are going to be disappointed by factors other than price.

I suppose the sophisticated audience of this site is aware of these things anyway, more or less. I suppose.

Malformed ‘close italics’ tag. Sorry.

Regarding the Case-Shiller methodology of using “paired sales:”

Is data adjusted for renovations?

Significant and costly improvements may have been made to a unit between sales.

Yes. And also for other things that impact value. The linked methodology is worth looking at.

That’s exactly the issue with CS, among other things. Many people remodeled their own homes and flippers are alive and well in all markets. I’m an appraiser in Oregon and have been watching lumber drop like a rock from last May to December. It is now nearly flat in the wholesale realm and Canadian mills are doing temp closures due to oversupply and decreased demand from the US. Prices in all major west coast cities have corrected at the high end and are continuing to do so, including Hawaii. The correction began last spring imo.

I live in Dallas, there really isn’t a housing bubble. Prices for homes were too low for years and are now reaching the prices they should have been. The Case-Shiller Index was 100 in 2000 and today is only at 188, if you counted inflation alone it would be 148. What is driving the rest of the price is growth, the access to cheap land is becoming harder and harder to find as millions of new people move into the area. If you look at the chart on the FRED which is a larger chart with more space between the years and you don’t see such a dramatic price rise. Can prices keep on rising, yes slowly, or else we would end up in a housing bubble, where one doesn’t exists today.

Unfortunately if you have been waiting for the “Big Crash” your opportunity to enter the real estate market, this is it. Enjoy the endless opportunities. As for the stock market, well your opportunity there would have been back in the Greatest Crash of Nov-Dec 2018. Interest rates, well that boat barely left the dock. Looks to be back at port unloading the passengers.

Sorry folks, but this is as good as it gets. Instead of “this time is different” think of it as “this time is a little different”. The little adds up over time and if you compare over 20, 30, 50 years, you might come to the conclusion that this time is different. Yes folks, things have changed a lot!

This post calls the top. Just like the made up 3.2% GDP prints calls the economy top.

I’ve been in business for 25 years and I’ve never seen such a slow 1st quarter ever. If one is old I hope Tyler is right if one is young and Tyler is right , you’re fucked……..not sure who is going to be buying $1,500,000 started homes in 20 years using their NBI of $1,000 a month.

Low interest rates and QE will not be enough to save the market before it corrects and it will correct.

@interesting-

> I’ve been in business for 25 years and I’ve never seen

> such a slow 1st quarter ever.

+1 This dead calm feels like the eye of the storm.

I don’t know. I have a family of builders in Portland, and close friends in Denver and Seattle. All are reporting not getting paid for their work or being able to pay vendors. I know HVAC, which is in the middle of the chain, is starting to suffer. Friends who are dual-income physicians are trying to release themselves from mortgages $700-$1,000,000 homes. My wife is a physician and had to take a pay cut (in the form of a loan for 12 months, where are supposed to pay her back, no interest, because the network of hospitals she works for is starting to go under; healthcare is a whole other issue). In the world I’m in, there’s more evidence of stealing from Peter to pay Paul.

I’m an appraiser in Bend and agree. We topped out last spring, despite slight increases in certain areas of the US, but even Canada saw things start falling last year, as have many other countries. We learned last time, no one is completely insulated in these corrections…except maybe Texas :-)

yep, the sky is falling, apocalypse is coming…hurry buy some gold and guns.

Trillions of QE have permanently elevated asset prices to levels that are not affordable but in case you are not aware, QE is not being unwound , its here to stay and if anything more QE will be coming our way together with lower interest rates.

Look at a chart of home prices for the last 50 years, they go up and come down to settle at always a higher level than before, so if you cant buy a house now, you will never do. Any decline in home prices will be counteracted by tighter financing conditions , so if you are waiting for houses to crash and are sitting on a pile of cash to buy them for pennies on the dollar, I will make a prediction for you, rather your dollar will be worth pennies than you buying houses for pennies on the dollar. Welcome to our fiat world.

My thoughts, exactly.

But on the other hand, wasn’t it possible in the previous bust?

The economy is so over leveraged the FED is scared of any down turn. They are going to suppress the business cycle indefinitely with lower rates and QE if they can get away with it. Also throw in fiscal stimulus. They can’t allow real estate to fall very far. I think it is going to end badly but I’ve been wrong for 10 years and counting.

Everyone says this is different:-)

We would see

I’m extremely happy to have discovered a very simple musical instrument that I love, hard to learn as it is, and am selling off all my other stuff. I’ve had real trouble getting paid by my boss, and my bank balance got down to $20 a few days ago. I’ve gotten paid, but once scared, twice shy …

I’ve even told my boss, because he’s also a friend, that frankly, I’m preparing so that if things turn to shit here, I can get out quick back to Hawaii. I may be living on the street, but better to live on the street in a place that’s home.

If I can hold out until I’m of the age to collect Social Security, I’ll have a thousand a month coming in, and Hawaii being 1/2 as expensive as San Jose, I think I can live OK.

But I think surviving the future means adopting a very Un-American lifestyle. Own as few things as possible, avoid owning a car if you possibly can, and be very leery of any kind of home ownership (as if you could ever own one anyway) because even if you could start to pay for one, the economy will crash or you’ll get a medical problem or something and lose it anyway. Become as non-materialist as possible.

Wow; this is major doom n gloom here. And how can you possibly live on 1k/mo.? That seems insane.

Another concern of affording a home is the price of maintenance. My mother sold her dream house last month for this reason.

Tyler – This type of sentiment is a prime indicator that the cycle has peaked. When people start believing that markets can never go down is when things start to deteriorate rapidly.

In 2011, we purchased a house because the rental rates were 33% higher than the mortgage payment on the same unit. Add in favorable tax deductions and purchasing made sense. Fast forward to 2019 and I’ve yet to find a listing where the mortgage payment wouldn’t be 25% higher than the rental rate. Investors and logical buyers just aren’t buying at these valuations and this is being reflected in sales data. Virtually every zip code I look at has YoY sales declines and virtually zero price appreciation. Even worse, it appears that rental rates are actually starting to decline as developers have build too many luxury rental units.

Owning a house was one of the more annoying obligations I’ve ever had in my life, but at the time (2011) it seemed like the payoff in 6 years time made a lot of sense. If you remove the potential for appreciation, owning a home makes zero sense. We are at that stage where investors are exiting the market and rational people are getting concessions to move into luxury rentals.

Housing prices, rental rates, and wage increases should all move in tandem over the long run.

In my neighbourhood of Toronto, $2,000,000 – 3,000,000 houses are rented out for $3,500 – 4,000 a month. Mortgage on these is $8,000 – 11,000 + $1,500 in property taxes and maintenance per month with a minimum $400-600K deposit (20%) and also pay $73,000-123,000 for the land transfer tax.

In short, to “own” what one can rent for $3-4K, one must:

1) pony up half a million $++ and then

2) pay 10-13K per month

Basic calculation.

500,000 * 5% growth/yr + ($6-10K * 12 months) saved/invested * (some growth).

$25K + $70-120K. That is $100-150K in the first year, then progressively more.

How is this not madness?

Take another look in a year or two when those houses are down by 30-50%. The math will then make more sense.

If they were smart they would rent a slightly smaller place, invest the savings and watch it grow in a REIT then when the market cycle slows turn around and take a loan out against the appreciated asset and be able to buy the home that they wanted without sacrificing their “lifestyle”.

But the problem with real estate (problem for some and benefit for others) is that houses are a pride and pleasure purchase, people get emotional about their house buying, even when they are trying to be impartial investors in a home.

They get caught up in beautifying it, not simply making the numbers work and then making the necessary changes to raise the value. Uninformed people will ALWAYS buy based on emotion and then sell based out of fear, which leaves room for the sharks to come in and feed on the blood of the mistaken.

Um. That’s life. Housing is NOT gonna get cheaper. If Housing goes down, so will employment, so a lot of people who think that they can get a cheaper house, then they might be unemployed when that happens.

It’ a catch 22… no way out.

Ehawk – Unfortunately you have this dynamic backwards. Unemployment will rise because the cycle is coming to an end. As unemployment rises, housing prices will drop. Long term, unemployment will absolutely increase because technology will eventually automate everyone’s job. In 30 years, very few people will be employed and will be on some form of meager gov’t welfare. Who are going to buy all of these $1M houses in 20-30 years or pay off the mortgage if nobody has a job?

I agree with automation being a threat, but as someone who works with the technology “very few people” in 30 years is laughable. In 70-100, I might agree.

sc7 – The breaking point comes as soon as Uber can launch autonomous EV’s. That certainly isn’t 70 years away. Probably closer to 10. What will happen to the labor market when drivers are eliminated, and consumers stop buying cars and oil? The shock waves through the entire economy are going to be staggering. Everyone is going to feel the collapse of the automotive and oil industries and every other ancillary industry that supports them.

OK. I’m no Genius, but in a recession people lose their job and in turn other people get scared, foreclosures rise and home sales drop.

So houses get cheaper, when a lot of people have NO Job or income.

how is this backward. Please explain it like I’m five.

In the San Diego area this doesn’t seem to be the case, at least from personal anecdotal evidence.

House listed on the market last week for 888k just went for 13% over list price, sold for 1m with 19 offers…in Encinitas. We are still increasing rents and operating at zero vacancy in our multi family units. There is a lot of overpriced junk out there and it is stagnating, but I don’t see signs of stress out there, especially real estate that is reasonably priced sells with multiple offers.

I’m glad you mentioned this.

King County home sales activity is humming right along. Anything that is listed close to the Zestimate seems to sell within 1 to 4 weeks.

Mansion first listed for $22 million in San Francisco sat on the market for two years. Price was cut to $16 million last year. It finally sold last week for $15.9 million. So has the market plunged 28%? Individual sales are just that. One sale by itself doesn’t say a thing about the market.

Yes, there are strange things going on that aren’t patterns. For instance, my wife’s family is from China and they needed to get their money out of the country and get their kids into a top school district. Of the twelve family members, they all moved to Orange County CA and paid crazy amounts of money for very mediocre homes. All cash. Now their kids attend college at the UC schools and for them, even those who are international students who pay high tuition rates, it’s still a bargain. It’s money laundering at its finest and we’ve let it happen. The problem is now many need access to money and they don’t have it. Selling their homes for less than they paid has been challenging so far.

I agree with you Wolf, can’t substitute anecdotes for statistics but I think I know a slow market when I see one. Your example is not representative of the typical houses most people buy here. I see strong rental market and real estate is selling no worse than last year for sure, good product is moving at better than decent prices I would say, but real estate is local, maybe it’s just my area that is hot right now

I don’t disagree, but Stephan Punwasi’s recent article comes to mind (on how individual sales, laundering in his case, can wreck the curve).

memento mori – The high end of the market in San Diego certainly feels very weak right now. La Jolla, Del Mar, Carmel Valley all seem to be deteriorating fast. As the desirable areas become more affordable, places like Encinitas will drop.

Houses under $1M in San Diego seem to sell fast but eventually you are going to start seeing $1.2M listings in good neighborhoods chopping prices under a million to get bids.

Also disagree about rental market in San Diego area. The rental rates DO NOT support the housing values at all. I’m seeing $1.2M houses renting out for $3K per month. Of course there is high demand for renting when it’s significantly cheaper than buying a $1M shack.

Again, Stephan Punwasi’s recent article here about money laundering in real estate comes to mind.

Ed. The cheapest house for sale in Del Mar start at $1.5 million. Ten years ago that was $1 million and 5 years ago it was $1.3 million. How is that deteriorating fast?

Your rental data is flawed as well. I put a house on market that I just paid $1.3 for at $5,500 and immediately got 3 qualified people wanting to rent on first day. And I intentionally priced it lower to get it rented quickly. So try again with spreading false data.

I am in San Diego and can easily see the ship is turning..

Although not meaningful price reduction but still the tide is turning ..

A house in my neighborhood is listed for last one year started with 950k.. now at 850k..

Anecdotal: I grew up in Dallas and have known the home prices there since the 1960s. I’ve never seen anything like the current price run up (surpassing the S&L days) and areas that are not great are priced like they are really, really great. Preston Hollow homes that sold in the 200,000s back in 2011 are tarted up and can go into the 700,000 range and higher. Some middle of the road neighborhoods breaking $1M. I thought the property tax assessments would slow this down (2.5%-3% of FMV per year), but they doesn’t seem to be doing so. It seemed like there was a pause in January and February, then back to the races.

– So banks are still willing to lend those amounts of money in dallas, Texas.

The S&L days, that is part of the problem, Dallas home prices never fully recovered, they were selling at loss if you counted inflation and the cost of the mortgage. Additionally, the DFW area has added millions of people. Sure the current price run up has been shocking, but it only takes the prices up to where they should have been all along. I don’t want to see the same shooting to the moon increases in prices, but it is good for long term homeowners to get a positive versus a negative return on equity. We aren’t in a bubble in the DFW area yet, but I am worried one might happen. Are certain neighborhoods in a bubble, yes that happens all the time, it comes and goes.

J.F. – Dallas FW is ground zero for new construction undercutting resale properties. The bubble was driven by Mexican and Chinese money laundering. Sales are dropping off a cliff. If you think Dallas is a good buy right now you are absolutely crazy. At least 25% overvalued.

I want to preface by saying I never mean to be impolite when stating an opposing view. I know it can be difficult to read “tone” in comments.

We were in Phoenix in 2004-2006 and heard repeatedly that Phoenix prices were “just catching to where they should have been, that they were undervalued for years.” We all know how that ended. I could believe one market was unique if this appreciation was only happening in one market. I think people are buying payments in this housing cycle.

Lots of people moving to the DFW area.

I respectfully disagree that Dallas is 25% over priced currently, unless the economy falls off a cliff and people stop moving here. New construction has always wiped out the value in existing homes in the DFW area until recently. There is no more cheap land close into Dallas, you have to move darn near Oklahoma border or halfway to Waco to get reasonable priced land to build upon. If prices keep shooting to the moon we will have a problem, but there are these fundamental factors driving home prices in the DFW area. #1 Prices for homes were until recently below inflationary cost, that is buy and hold of existing home was a negative return in part due to the new construction. #2 Millions of people have moved here and are continuing to move here, the supply of existing homes close to downtown is limited while the demand keeps rising. #3 The cost to construct new is getting more expensive, tighter labor market, higher construction material costs, and rising land values. Sure there are negatives like high property taxes and higher interest rates (which actually have been failing recently) and uncertainty of the future, but these negatives aren’t going to drag down prices by 25% any time soon if forever. I really hope that we don’t end up in a bubble, at present any recession would only have home prices dropping only marginally in the DFW area, that is there was no crash during the last few recessions. You have to go all the way back to massive S&L bubble to see a crash here.

Mean while , out here in flyover country, we have better odds at winning the lottery than finding an employee.

In 30yrs, I have NEVER witnessed this.

So yep..it must mean the top is here. The GDP is fake, unemployment …housing ..trucking…timber…shale…

Its spring: rain & mud. I’ll be working in slop all day. There will be a few youngsters with us. The majority of us will be 50+. Were are the youngsters?

Tom, no youngster today wants to be working outside in rain and mud, let alone have to get up early on a regular basis.

They will work for themselves in the gig economy as Uber, Lyft, Amazon delivery drivers on their own work schedule ;)

I just hope I can hold my job with my current employer until retirement in T-5 years.

Where I am, it’s understood that if you’re working in the gig economy, it’s because you’re desperate. If you’re over 40, forget about working in tech. Jobs are hard, hard, hard to get. But you can sign up for Uber and be working right away. And try not to think about how you’re burning your car up for min. wage.

In the city eating avocado toast.

Although my son is away for his 2 week oil patch job while also running his local electrical company…in the boonies. There are lots of jobs in flyover, just not too many pink hands and clean clothes jobs.

Paulo – Agree. It’s the same problem in the cities though. Massive labor shortage. Never seen so much wealth and confidence in my entire life. I’ve seen many people in their 30’s and early 40’s voluntarily quitting high paying jobs because they have gotten so rich in the past 10 years.

And that doesn’t sound like a top to you? Unprecedented and ultra-fast wealth growth?

Maybe here in LA. We’re at the older end of Millennial and have hired within the past couple of years for both our business and household.

The business hiring seems impossible – there’s no shortage of applicants but none motivated or qualified. This is for a desk job with huge growth potential in a great industry – I would have killed for this job in my 20s. We still have an opening but I think I’m going to outsource some other work and shift things around instead.

We also have two nannies. Every time I post a nanny job, we get over a hundred applicants. Yup 100+. We pay market rate, but from what the nannies tell me, we offer more stability than most other nanny jobs where they are out of work as soon as the kids get off the daycare waitlist. But it’s similar in the hiring process – the number of applicants we get who have visa issues vastly outnumbers those who don’t. Out of those 100, there are maybe 2 qualified, it’s beyond depressing.

I’m sure every generation says this of the next, but I seriously wonder about the work ethic and motivation of the current labor pool. I think a lot of kids with NO qualifications expect 9-5 jobs with full benefits and 3 weeks vacation without having to do anything. Sorry, that’s not how work works!

MaxDakota – It’s simple. You are not paying market rate. Stop being so cheap and then maybe you’ll be able to find qualified applicants.

“Every time I post a nanny job, we get over a hundred applicants. Yup 100+. We pay market rate,”

100+ applicants tells me that Dakota is at least incrementally above market rate.

Most people don’t understand supply & demand.

I’m probably either qualified or trainable for that desk job. And there’s no effin’ way Mr. Dakota would hire me because I don’t go to the same golf club with his nephews, didn’t go to the same high school, etc. I know how this stuff works.

“Out of those 100, there are maybe 2 qualified, it’s beyond depressing.”

What is also depressing is parents who expect to outsource parenting and are shocked and appalled that no one ‘qualified’ wants the opportunity of raising someone else’s children. If the position is so great, you should try it.

I can’t comprehend the fascination with home prices. I bought my home in 1992-93 after working in the Bay Area. I moved across America coast to coast. My hometown became hedge fund capital of the world. It has seen G.E. during its glory days. In the end a home is more important than something you just buy and sell like stocks and bonds.

Immigration Immigration Immigration. The US has had a massive immigration increase over the last 30 years. Go to an open house in these hot markets and it’s people who are 1st or 2nd generation Americans who were not here 20 years ago. It’s all Asians and Indians. There are so many more people competing for the same old housing stock in places like Seattle, Boston and the New York suburbs.

Until employers start moving jobs back into the smaller cities and towns across our heartlands we’ll continue to see this run up.

For the record I have nothing against immigrants but their effect on housing prices should be acknowledged

As a MA native and long term renter/real estate lurker…I can vouch for this phenomenon as I’ve attended open houses sporadically over the last several years in the Boston area. The last open house 5 weeks ago in Medford, MA about 6-7 miles north of Boston I was the only non-Asian person in attendance and in recent memory I cannot recall an open house where there were no people of Asian descent present. As poster George said, I have nothing against Asians but it has been interesting to observe the population changing and how it affects the competition for the available real estate.

Also – anecdotally — I am seeing a fair amount of price decreases in the Boston area and properties sitting longer. A friend’s realtor advised two price decreases in 6 weeks and told him just the other day that the market is “slowing” and that if the condo his family listed doesn’t sell soon, it may take longer as we enter the “soft season”. This particular condo in a desirable area probably would have sold very quickly and possibly over asking price a year ago.

What is interesting is the Los Angeles vs. Boston market.

In the Boston area, sales seem to be brisk across low and high price ranges. Bidding wars are frequent and it appears the new tax law had zero impact.

But, in LA, it is a different pattern. In beach cities, it seems that the below low 2M price level, activity is brisk and bidding wars can happen. But, in the same area, above 3M can be slow with discounts. This looks like the new tax law pushed people into the lower price rungs. So looking at LA, it looks like the new tax law had a significant impact.

In my beach area, realtors are knocking on doors desperate for listings on homes that would price lower than the low 2Ms. They just walk by the 3M and up stuff. About one year ago, the 3M to 5M market was almost sold out.

Also, one more local comment. Right now, within a six house radius of my home, their are 3 spec homes going in. One is well north of 6M while I would guess the other two are in the 4Ms. I can tell the developers are getting worried … construction is slowing. Down the street, I see a 10 year old spec home which is a divorce sale. While not as nice as these new properties, so far it is in the mid 3Ms, and they are sending smoke signals that they will deal, but no bid. But, if something shows up with a lower 2M handle on it, a buyers feeding frenzy happens. If this continues, you will see price compression where their is less of a price gap between the high and low end.

Jim the only “bidding wars” I have seen down here (San Diego) is multiple people offering me 20-50-% less than my asking price. I am pulling off one of my listings Friday after close to a year of no sale although it did get a offer we accepted but the buyer backed out. I suppose real estate is local and perhaps you have dwellings in Beverly Hills or Malibu or some other very desirable neighborhood but from my perspective, this market is drying up.

Here is how I would characterize the LA market. The low end of any high priced zip code is doing very well. But, only if the location is good and the home is well maintained. The other really strong spot is the 700 to 900K stuff in decent areas with good schools. Some really low end stuff is doing well in up and coming areas. But, lots of high priced weakness that is widespread.

SocalJim – In LA it has been a one-two punch of the Chinese economy tanking and curbs being put in place by both the US and China to prevent money laundering in West Coast real estate AND the change in SALT deductions.

SoCal real estate is also ridiculously overpriced right now. Boston real estate is based much more on fundamentals. Rent is X, households earn Y, etc. LA has so much hot international money that prices climbed above what local households can afford.

– Topic: Real Estate in New Zealand.

– New Zealand has a housing bubble as well, especially in Auckland.

– After a blistering run-up in price. real estate prices in the capitol Auckland seem to have “turned a corner” as well. Banks in NZ were (and are ??) willing to lend 6, 7, 8 and even 9 times gross household income and were willing to hand out interest only mortgages. Sheer insanity. But now the chickens are coming home to roost.

– Some suburbs in Auckland have seen price drops of up to some 25%.

– Even people who bought a house as an investment are struggling because the rents are simply too low to make a profit, too low to have a positive cash flow on those investments.

https://www.interest.co.nz/property/99445/latest-realestateconz-figures-show-asking-prices-and-new-listings-are-easing-while

http://digitalfinanceanalytics.com/blog/the-mythology-of-capital-gains

At some point boomer demographics will impact the housing market. I imagine many of the boomers will want to sell their McMansions and downsize. I think we’re all familiar with the generational income and family formation differences between millennials and boomers. Unless we get a large influx of wealthy foreign investors or government backed housing investment, then I expect deflation to hit the housing market over the next few years.

For a true bubble, mania and leverage is required. We saw that back in 2007 when Cocktail waitresses in Vegas owned multiple homes, and lenders could bag these manure-grade, AAA rated loans, and sell them to clueless institutional buyers.

Are we to believe that we are in a similar period?

Are lenders doing liar loans again?

Is zero-down here again, or how about those multiple cash-out re-fi’s?

Has Moody’s or other rating firms relaxed their standards?

Are banks eager to lend to sub-prime customers, and can they package these loans to be sold to a new era of dupes?

Have people who got burned, or those that knew them, forgotten about 2009?

Have those buyers went bankrupt in 2010 come back to the market to do it all again?

Are people lining up to buy multiple condos pre-construction, and having the builder finance them with teaser ARM’s?

Has the Treasury Department dropped its anti-laundering requirement for NY and Miami buyers to list the true ownership of properties?

Have bidding-wars in multiple cities become the norm?

Have the Baby Boomers, who are now retiring, and and living off their savings, suddenly decide speculate on multiple homes, and upsize their housing?

Is the phrase “real estate always goes up!” coming back?

Well then, if mania, and leverage is back, I guess we are indeed in the midst of Bubble 2.0

In my view, the 2019 Real Estate bubble is not the same as 2005. It is more of an echo bubble. There are hot money markets that may still be rising, but most are flat or contracting. Many markets have never fully recovered and the turn is already probably here.

What seems particularly concerning today is that there are now bubbles everywhere. Subprime Auto, College loans, Stocks, Bonds (Trillions in negative yielding debt). Total credit outstanding is far greater than in 2007. This crash will be worse — but not the same.

Are we to believe that we are in a similar period? – Different. Lots of buyers purchasing at uncomfortable DTI ratios with miniscule downpayments against huge inflated asset prices.

Are lenders doing liar loans again? – There is a NINA loan back

Is zero-down here again, or how about those multiple cash-out re-fi’s? – There are definitely still cash-out re-fis.

Has Moody’s or other rating firms relaxed their standards? – Moody’s was a joke in 2008 and they’re a joke now.

Are banks eager to lend to sub-prime customers, and can they package these loans to be sold to a new era of dupes? – Yes, see BofA pledging billions in sub-prime home loans.

Have people who got burned, or those that knew them, forgotten about 2009? – Yep

Have those buyers went bankrupt in 2010 come back to the market to do it all again? – I know of a few

Are people lining up to buy multiple condos pre-construction, and having the builder finance them with teaser ARM’s? – Not sure I see this as much.

Have bidding-wars in multiple cities become the norm? – Yes

Have the Baby Boomers, who are now retiring, and and living off their savings, suddenly decide speculate on multiple homes, and upsize their housing? – A resounding yes.

Is the phrase “real estate always goes up!” coming back? – Annoyingly, very much so.

Some headlines today:

CNBC: “Private payrolls surge by 275,000 in April, blowing past estimates and biggest gain since July”

CBS: Consumer confidence snaps back in April, pointing to steadily growing economy

CNN: The global economy is suddenly looking stronger

____

But I know, I know. It’s all a fake economy based on fake IPOs and fake Fed interest rates and a fake news data from the government.

I live in the Bay Area selling my house and moving to Sacramento to be closer to my kids so I am getting a taste of both markets. Whats interesting is how little inventory is on either market which creates the herd buying. If you live in the Bay Area selling and moving up is very difficult unless you have a sudden influx of cash so most homeowners are staying put as there are few options. My son calls it homeowner lockdown.

Sacramento has been hit hard by investors from the Bay Area buying up rental and flipping housing as the Bay Area is overpriced for these activities so one always sees flip houses for sale with there laminate floors from one end to the other. Builders are cutting prices now and making deals around Elk Grove but the area has become hot for Asian investors in the resale market as most of the inventory is newer homes.

RE out here on the Olympic peninsula getting hot again. 500k to 800k homes going quickly, anything under 400k faster. it feels like cash slosh from somewhere else. Building lots that have sat for years going quickly now as well. I hear of shortages of construction workers and builders and contractors are backed up bigly Also heard that the crappy subs coming in now to pick up the slack.

Mr. Richter:

=>One sale by itself doesn’t say a think about the market.

The plural of ‘anecdote’ continues to not be ‘data’.

Wendy:

=>Are lenders doing liar loans again?

And worse. “The Big Short Doomsday Machine Is Back.” Reuters dropped a bombshell. Perhaps Mr. Richter will weigh in. Other machines are also churning.

Ehawk:

=>If Housing goes down, so will employment, so a lot of people who think that they can get a cheaper house, then they might be unemployed when that happens.

History repeats itself. GMTA.

tom:

=>Mean while , out here in flyover country, we have better odds at winning the lottery than finding an employee.

If you go to McAllen to offer sponsorship to recruits you risk ending up in a pen with your job candidates. Those guys have no sense of humour.

=>The GDP is fake, unemployment

Volunteers and unpaid family members are counted as employed. As are other unemployed.

nearlynapping:

=>This crash will be worse — but not the same.

Several observers have predicted they’ll have to resort to massive bail-ins. Anything – and nearly everything – to save campaign contributor financiers. Even the most sedate analysts (SWIM) are gobsmacked when they run only the numbers they can see.

Keep in mind that the last crisis was never resolved, only accomodated with liquidity and bail-outs, some of them contradicting the Fed’s mandate, like the billions handed to the insolvent CitiBank, and some of them patently illegal. This has enabled the revival and enhancement of the causative bad practices of the last crisis. The numbers say it won’t be possible to accomodate the coming crisis, and the real numbers are expected to be even worse than the reported numbers. Then things will turn bad, because the financial crisis will precipitate an even worse political crisis, which will be successfully exploited, ensuring the shitstorm endures.

Post lux tenebras.

I do hope the meet-up went well and happily exceeded all expectations. I had other obligations and could not participate.

Well-stated, and kudos for mentioning bail-ins, a taboo subject.

Anyone who thinks bail-ins can’t happen should Google Cyprus, ca. 2013. Some argue it was the “test case.”

FluffyGato,

The US is not Cyprus. People have got to come to grips with that eventually.

No FDIC insured depositor in the US ever lost a dime, period. Not even during the big bad Financial Crisis. People have got to come to grips with that too.

The FDIC is part of the US government, and the US government is backed by the Fed which has unlimited printing powers and it will not allow the US government to go broke. People have got to come to grips with that too.

This nonsense about “bail-ins” of FDIC-insured depositors in the US is fear mongering that is getting very boring after all these years.

=>This nonsense about “bail-ins” of FDIC-insured depositors in the US is fear mongering

True. But not all bank deposits are FDIC-insured.

Opinions differ as to what will happen in the future:

That FDIC-insured depositors have never lost money to date does not tell the whole story, and the parlous state of bank regulation cannot guarantee that it will never happen. Besides, banks have ways besides bail-ins to lose the money of their depositors. There have been other, perhaps indirect types of bail-ins as well, for example, confiscation of pensions in leveraged corporate bankruptcies. Naturally those accounts are not FDIC-insured, but that sidesteps my point: bail-ins will occur, because they can, regardless of FDIC protections.

I don’t mean to argue. I just want to be on the record with this topic when the worst happens.

Unamused,

“…when the worst happens.” Nuclear war and everyone dies? Sun collides with the earth and everyone dies? Sure, there are some scenarios in which FDIC-insured depositors, pulverized by then, would lose their deposits, also pulverized by then.

Otherwise, the Fed, whose job it is to make sure the government cannot go bankrupt, will make sure the FDIC, which is part of the government, has enough to cover all insured deposits when a bank collapses. Period. Everything else is nonsense and fearmongering.

There are over 5,000 FDIC insured banks in the US, and I don’t know how many credit unions insured by the National Credit Union Administration (NCUA), which is also part of the US government. Surely, among these thousands of financial institutions with federally insured deposits, you can find one the suits you.

But if you lend money to another outfit and think it’s a bank with federal deposit insurance, when it isn’t, and it folds, and you lose some or all of your money because it wasn’t FDIC insured, well, there is a price to pay for being stupid. Same is true if you don’t know the FDIC rules and end up as depositor with too much money in an account. They’re not secrets.

If a depositor, instead wasting time with this fearmongering, does some basic reading on the FDIC’s website so that they understand the ground rules, and then follows those rules, they will have nothing to worry about.

If you know the rules, you can have millions of dollars in FDIC insured deposits, using different banks, brokered CDs, etc. It’s just basic stuff. Ignorance is costly.

A company that needs to have $200 million in the bank on payday to cover payroll, that company is exposed to credit risk at the bank. That’s why companies don’t keep a lot of money in the bank except for brief periods. They’ll put their cash in US Treasuries and use small amounts of cash and a credit line at the bank to fund their operating expenses. So they will have some exposure, but it’s small compared to their overall size.

But that’s NOT an issue or savers, and when you talk about uninsured deposits, you’re mostly talking about corporate accounts with cash that exceed the limits. This is not an issue savers have to deal with. Don’t confuse the issues here. This was about savers, not corporate payroll accounts.

Also, “bail-in” means bail-in of investors and creditors according to the credit hierarchy. At the bottom of the hierarchy in the US are common stockholders, preferred stockholders, and co-co bondholders. After they get wiped out, losses move up the hierarchy to other unsecured creditors, such as unsecured bondholders and depositors, and then up to secured bondholders. This is how it has been ROUTINELY done for decades. There is nothing new. What was new during the financial crisis was that this was NOT done for the biggest banks (Citi, etc), and that the stockholders and bondholders of the biggest banks were bailed out.

Even if FDIC-insured deposits get bailed in, they’re STILL FDIC insured deposits and the FDIC will make the depositor whole, and it doesn’t friggin matter to insured depositors what happens to their deposit because the FDIC will make them whole.

=> Otherwise, the Fed, whose job it is to make sure the government cannot go bankrupt, will make sure the FDIC, which is part of the government, has enough to cover all insured deposits when a bank collapses. Period.

Which is to say, It Can’t Happen Here.

Perhaps we can agree to having a difference of opinion, and leave it at that.

1) During a bear market there are reactions.

Those reactions are positive, they move up, in a quick upthrust.

The rise from the previous RE bottom, from 20012(L) to

the peak of 2018 took about 6Y ==> its equal to the downdraft

period, that started in 2006 to the 2012 bottom, or the same 6y.

2) When the trend is up, it take 3 to 6 times longer to reach the

same level of the last peak. The big players have to accumulate inventory at wholesale prices and it take time.

3) The SPX : from Sept 2018(H) to the bottom of Dec 2018(L) it took 3.5 months.

After 3.5 months, the SPX have reached the level, as Sept 2018 peak.

Wall street big players have too much inventory on their shelves, they must dump, – at MAX prices, up there in the sky, – before

the next opportunity, at lower prices, before a recession start.

FOMC press release at 11:00 PST

The Board of Governors of the Federal Reserve System voted unanimously to set the interest rate paid on required and excess reserve balances at 2.35 percent, effective May 2, 2019. Setting the interest rate paid on required and excess reserve balances 15 basis points below the top of the target range for the federal funds rate is intended to foster trading in the federal funds market at rates well within the FOMC’s target range.

Whoa. They are setting IOER _below_ the current 4-week T-bill rate of about 2.39%. That seems like a new tack. Am I missing something here. FF rate unchanged range of 2.25-2.50.

“Foster trading in the federal funds market”: Translation: FRB now wants banks to borrow reserves from each other, rather than from the Fed itself at the discount window. Maybe this is what the earlier mumbo-jumbo about “operating in a regime of ample reserves” really meant.

But AFAICT, there is no way to view the above action as anything but a convoluted form of tightening. Basically, when banks now need more reserves, they will pay less if they borrow the reserves from another bank, which will get the word out about who is short on reserves, rather than anonymously at the discount window, which will be more expensive.

Translation number 2: FRB to member banks: Dear member banks, there are weak banks out there that are short on reserves, and therefore we have decided that rather than parking your excess reserves at the FRB, we want you to incentivize you to lend out your reserves to these weak banks.

Looks like Wall st got the message. Main stock indices are now dropping.

That 5-basis-point reduction had the same purpose as the prior two 5-basis-point reductions of the IOER: it’s to keep the federal funds rate in the middle of the Fed’s target range (between 2.25% and 2.50%). The federal funds rate has been closer to the top of the range. For example, last night it was at 2.45%. The federal funds rate should be somewhere in the middle between 2.25% and 2.50%.

I think we are describing the same situation. FFR has risen too high, presumably because some banks need to borrow reserves and other banks that have excess reserves have not been sufficiently willing to lend them, preferring instead just to collect IOER. By reducing IOER, FRB is trying to induce the lending of reserves so that FFR drops to the desired level.

Meanwhile, as assets splurge inflation at a rabid pace hitting daily all time highs, Dat Fed don’t see no inflation and joins dat IMF chic who says it’s just a deep dark mystery Dat shes don’t seeing no inflation, ditto:

“Inflation remains the Fed’s most challenging puzzle, as strong GDP growth appears out of alignment with price increases.”

It’s a puzzle! A deep, dark puzzle!

@Rcohn

One man’s opinion:

re: Prop 13 will allow the hand down to the next generation who will slide into their cushy tax basis and then have the cajones to complain about the school systems being underfunded. You’re right, it definitely holds supply off the market.

I am a transplant here (8 years); watching this bubble, you cant try to rationalize the housing market with median affordability and income calcs/ratios like you can in the NY area or Boston; everyone I know who is in their 30’s (prime first time buyer age) and has purchased a home in the Bay Area since I have lived here has had some sort of tail risk/black swan event, or gotten significant help from the bank of mom and dad while not admitting it.

The buyer population over the last few years: 1) You have those who have hit the stock option/RSU register and monetized, 2) those simply laundering overseas cash through the system, 3) someone cashing out outsized gains from a home sale and recycling into a new home before the cap gains kick in, or 4) someone inheriting a prop 13 handdown. It’s literally impossible to play the “oh just don’t eat out as much and stuff a few hundred dollars a month away and you’ll get there” game with the numbers involved.

I agree with you that with the nosebleed levels comes increased fragility (and I don’t even mean the Hayward Fault, which is another coin flip).

A lot of unorthodox variables got us here; only time will tell if those same variables also accelerate a decline.

It’s kind of a standoff now – not seeing outright pain for sellers yet or motivation to really drop price, but buyers are slowly getting leverage with increased supply and longer listings. And people finally did their taxes and got smoked by the SALT situation, which has to show in prices more than 3-4% IMO but who knows?

{{I am a transplant here (8 years); watching this bubble, you cant try to rationalize the housing market with median affordability and income calcs/ratios like you can in the NY area or Boston; everyone I know who is in their 30’s (prime first time buyer age) and has purchased a home in the Bay Area since I have lived here has had some sort of tail risk/black swan event, or gotten significant help from the bank of mom and dad while not admitting it.}}

Uh no if you go by median ‘income levels’ for NYC & Boston the numbers don’t work not even close. If you go by ‘fundamentals’ like median income / median price the numbers don’t make sense

{{I am a transplant here (8 years); watching this bubble, you cant try to rationalize the housing market with median affordability and income calcs/ratios like you can in the NY area or Boston; everyone I know who is in their 30’s (prime first time buyer age) and has purchased a home in the Bay Area since I have lived here has had some sort of tail risk/black swan event, or gotten significant help from the bank of mom and dad while not admitting it.}}

Its the same here in the Boston area, virtually everyone that is buying now is either trading up or has gotten significant help from mom & dad (like the majority of the student population that are the offspring of the top 1% in America) and of course a significant number of buyers (and workers ) in tech, pharmaceuticals & academia are of indian or chinese descent (similar to a previous comment).

Yep. In the Boston area (I live in Cambridge), most people I talk to who bought at least 10 years ago – owners or those who have mortgages (rent from the bank) – agree that this area is immune from a significant downturn.

If you are a lowly renter sitting on the sidelines, you may be viewed with a sense of pity or a sense of thinly veiled condescension or exasperation “You ‘shoulda coulda woulda’ bought when you had the chance (stupid!!)” or “What are you waiting for, it’s just going to get worse!!”

One does get tired of beating oneself up for not making that decision, for waiting too long and now being a real estate misfit, a pathetic and doomed member of the non-homeowner’s club here in the Boston area.

But, but, but…(I think to myself) that 2016 study that half of Boston residents earn less than $35,000 a year. What about that? “According to a study by the Brookings Institution, the Globe found that Boston has the highest rate of economic disparity out of America’s 100 largest cities.” What about that? What about the report or homelessness increasing by 14% in 2018? Have these low income and homeless people all pulled themselves up by their bootstraps and gotten jobs in biotech earning 200K?

I’ve mostly stopped talking about Boston area home prices with locals who own or have mortgages although I may complain about the worsening traffic from time to time. ;-)

The best part about prop 13 is we’re technically only about half way to the full effect of the law. Since children inherit the tax assessment which does not get reassessed until the property is passed down to their children, we’re looking at I’m guessing an average of 80 years between reassessments. Prop 13 has only been in effect for 41 years. So we still got another 39 or so years until the full consequences of the proposition are realized for residential properties. I wonder if anyone has figured out to put the house under an LLC so they can keep passing it down without ever getting reassessed.

These charts are in nominal dollars correct? I assume if we were to use an inflation-adjusted case-shiller index, we’d be below our 2006 peak. After all, $1 in 2006 is worth about $1.28 today.

As I said in the article, these charts ARE a measure of inflation, namely house-price inflation. They measure how the purchasing power of the dollar with regards to the same house (the index is abased on “sales pairs”) has fallen over time. So if you adjust it for Consumer Price Inflation, it will show you how much bigger house price inflation is than consumer price inflation. That’s all it will show you.

Wolf, it seems that during housing bust 1, the upslope matches the downslope in almost every market. The symmetry is almost perfect in some markets. If you assume the peak of housing bust 2 is today for the sake of argument, I think it would be interesting to see a proforma downslope that matches the upslope once again in each city.

The down-slope in Housing Bust 1 was very steep in most markets. It was a true crisis and panic. I doubt we will see the same kind of steepness this time around. This may very well drag out for a lot longer and be a lot gentler, so to speak.