So Sales Finally Tick Up.

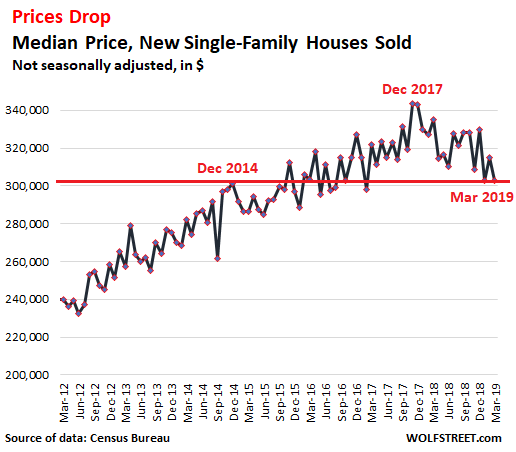

Home builders, the ultimate pros in the housing market, have figured out something after the malaise in the second half last year: Cut prices and buyers will come. The median selling price of new houses dropped 9.7% in March from March last year to $302,700, the Commerce Department reported this morning. This took the price back to about where it had first been in December 2014 ($301,500):

Homebuilders are motivated to move their speculative inventory. They’re making deals at lower prices, and they’re building homes at lower price points. And buyers responded. House sales at the lower end gained market share while houses at the higher end lost market share.

Houses that were sold below $200,000 made up 16% of the mix in March, up from 11% in March 2018. Houses that were sold at prices of $400,000 or higher in March made up 29% of the mix, down from 32% in March 2018.

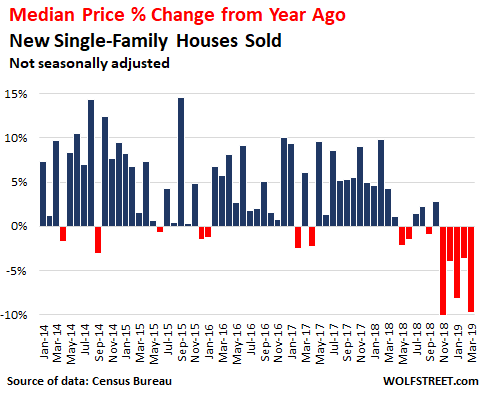

This shift in the market, and the price cuts by homebuilders, has pushed the median new house price down 11.8% from the peak in December 2017. The year-over-year price drops starting in November last year were the sharpest such drops since Housing Bust 1:

The new-house sales data, produced jointly by the Census Bureau and the Department of Housing and Urban Development, is volatile. It is revised in the following months, often quite drastically. But after a while, the trends become clear.

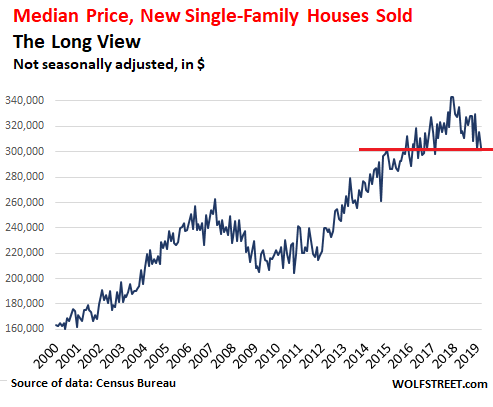

For the long-term view: The median price of new houses ballooned by about 55% from the range in 2011 and 2012 to the peak in December 2017 ($343,300). This peak had exceeded by 31% the crazy peak of Housing Bubble 1 in March 2007. When it comes to price, the sky is not the limit:

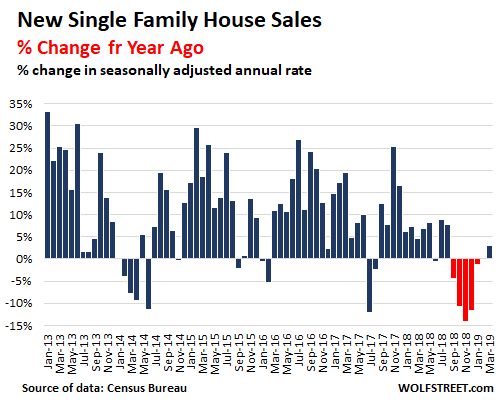

Sales of new houses, in terms of the seasonally adjusted annual rate, had dropped six months in a row on a year-over-year basis, but in March they responded to lower prices and showed the first year-over-year increase, surpassing the strong March last year by 3.0%, with a rate of 692,000 houses, the highest rate of sales since November 2017:

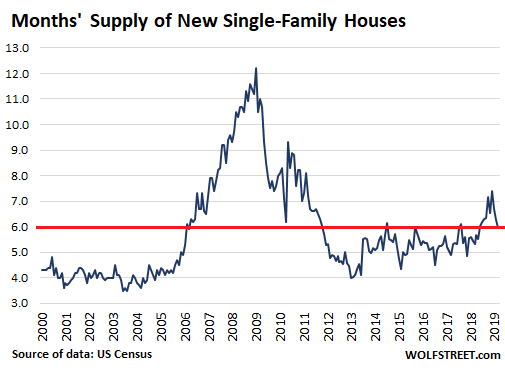

And supply has started to edge down from the peak in January of 348,000 houses to 344,000 houses, a supply of 6.0 months at the current rate of sales. This is still high compared to normal levels, but it’s reversing the spike in supply that had shot past 7 months last year:

All this makes basic sense. Homebuilders are in the business of building and selling houses, and unlike investors and homeowners, they cannot just not sell their houses when the market isn’t with them. So they sharpened their pencils and made deals at prices where the buyers were, and as prices dropped, sales ticked up and high inventories started to shrink a little. Price can fix a lot of problems.

But this is something homeowners and investors haven’t figured out yet. There is plenty of supply of existing homes, but it’s the wrong supply, priced too high, and sales fall. Read… Lower Mortgage Rates No Relief for US Home Sales

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

It’s a good thing everyone who brought new houses the last 5 years put 20% down with 700+ FICO score.

Wolf, I would change the “but” in the subtitle to “so”, to reflect that in a visibly softening market, buyers start actually paying attention to price.

Anecdotally, was in Sonoma for Easter Sunday brunch, saw a veritable shit-ton of For Sale signs on properties along the way there and back. Wonder how many of those folks are still hoping to cash out a the top and resisting lowering their ask. Perhaps WolfStreet reader and Marin county RE guru Tom Stone can give some further insight into the current state of the market there.

Done.

How on earth are there so many houses for sale in Sonoma County when two years ago over 5,000 of them burned up in a fire?

I’m guessing those are empty lots in which the house has been torn down and the lot cleared.

Hey! I’m an Alameda renter too! (But leaving for NC in June). I love Alameda, but with current prices, Alameda has not loved me back…

Dude ! … Those are ‘Tent’ camper’s pads.

No, this was on the way from Marin to Sonoma town center, nowhere near the recent fires, and all the properties were upscale.

This is a good sign as price decreases improve sales until things plateau and another round of prices decreases is needed to bring in the next tier of buyers. A good steady period of price decreases educates those who think they can overpay to get a place on the property ladder because they think they can always sell for more tommorow. Instead, it focus’s buyers on what they can afford over the long term , and whoa be it to the seller who becomes stuck in delusion dreams of the past.

Recently, I read that builders moved downmarket … on average building smaller homes and shifted towards more condos and attached products to get the sales higher. It is likely this explains the drop in average sold price.

Personally, I see the metro Boston housing market is hot. And, I see decent sales in Socal beach communities with limited options below the 2M mark. I also know someone in Detroit that had a heck of a time getting a home after many offers. I just don’t see the problem that the media tells me about. This could be very political.

Thats not the dynamic in the Portland Metro Area. The homebuilders are lowering prices on new homes that they planned and permited two years or more ago. Once these subdivisions are started there is no way they can change the lot size or the type of house that they are building on it, and I imagine the same is true in California. Perhaps they can skimp on finishes and hardware but the discounts Wolf is showing are real price reductions.

Unfortunately, this site does not allow me to post links. However, zillow reports home sizes as well as lot sizes are being reduced. Zillow has also reported this pattern exists in all regions of the country. Here in coastal Southern California, nearly everything being built is either zero lot lines or attached. Not that long ago, single family homes ruled. Times are changing.

It’s the incredibly shrinking house…and lot. Even here in DFW, they are putting up more new homes on postage stamp lots. Unfortunately they call it “real estate” for a reason. Buyers of this recently watered-down product will discover this reality when they go to sell.

For the time being price cures all defects, and builders are making the best of a stagflationary environment.

That’s why there is these large scale surveys, a single persons observations do not tell the whole story. Political? Wolf is just quoting the numbers.

Leave it to SocalJim to bring useless anecdotal observations to discussions based on hard data. Socal is always doing great in Jim’s eyes despite the fact that all data says otherwise and a quick glance at listings shows price slashing pretty much across the board.

With a 9% price drop, renters made out like bandits. Nothing wrong with renting when housing is way way overpriced. People should worry less about gains, and start focusing on potential losses, given the bubbly state of everything.

Also keep in mind this doesn’t include all the free upgrades they had to give. No builder wants to lower the prices. Doing so basically throw the recent new home buyers under the bus. They first try to lure in potential buyers with free upgrades and gifts. Price cut is the very last option as they need to sell but buyers don’t need to buy.

So sorry if you purchased a house in one of these developments over the last few years. Looks like you are underwater now.

#######

“Homebuilders…So they sharpened their pencils and made deals at prices where the buyers were, and as prices dropped, sales ticked up and high inventories started to shrink a little. Price can fix a lot of problems.”

Wolf, I understand the point you are trying to make, but choosing the uptick on the price graph for Dec 2014 and drawing a line to the downtick in Mar 2019, and then claiming that prices have gone back to 2014 is somewhat similar to picking the hottest day in winter and the coldest day in summer, and proclaiming there is only a minor difference is seasonal temperatures over the last decade. Wouldn’t a moving average give a better depiction of what new homes are selling for?

Drew a straight line across, as I nearly always do, from the current data point, horizontally across to wherever it goes. I didn’t “choose” anything.

No offense Wendy, but how else would a horizontal line drawn on a declining market time series look? If a market declines the horizontal lines hits the upper parts of the price increase first… that is just the way it is.

Moving averages are great but they are by definition a lagging indicator, and we know how those do at inflection points!

With government controlled GSE’a and other institutions issuing loans, all guaranteed by the government, at low, low rates there will be no house price correction. I see no dip in house prices here in Seattle, crappy shacks are still selling for a million plus.

I keep hearing about a dip in housing, but I’m not seeing it in the real world – it’s just a mirage, wishful thinking. Houses are assets, not homes, and the Fed gets to decide which direction asset prices go. The Fed has decided asset price will only increase, never drop. There is no free market only a reckless central bank and government inflating assets, and destroying the currency, in perpetuity. Cash is trash. If you don’t have fear of missing out you had better get some fear before you’re left with nothing.

Powell pushed the S&P 500 up over 25% in less then 4 months and he still has the accelerator flat to the floor – need I say more.

You are wearing your glasses backwards. List price (sellers dream price) is meaningless. Pay attention to sold price. The illusion that is painted by all the greedy used home sellers masks reality.

van_down_by_river – Problem is, Seattle prices are down YoY. Even worse, sales are way down and inventory is way up. This means prices are going to continue to drop. The only question at this point is how far will it go in Seattle. 30%-40%+ for $1M+ homes is possible.

The price drop is only based on current market dynamics. What is really scary is the fact that millennials haven’t even started their exodus out of the city centers yet to start families and boomers haven’t started dying out in large numbers in the burbs. Where can you possible buy right now that isn’t going to be flooded with inventory over the next five years?

I think that is a bit pessimistic but certainly possible. However, the large increase in supply in Seattle still has led only to 1 month of supply in King County. The fact that prices fell with such a low MOS shows the fragility of the current market. My regressions show a flat market in Seattle for next 12 months, with a couple percent range on one side or the other. I’m more pessimistic than the regressions but am thinking 10% down.

Austin, TX is still up ~9% YoY, according to the St Louis Fed.

https://fred.stlouisfed.org/series/ATNHPIUS12420Q

Builders have been in desperation mode for a while. They aren’t building in volume anymore & their profit margins are paper thin. Teetering on the brink of extinction. The only thing going on for the last several years in the residential construction industry has been dense multifamily housing. Single family houses have become an anomaly.

Housing is a leading indicator of what is coming in the not-to-distant-future with the entire economy. What I am seeing here in the East Bay northern CA are more & more existing houses coming on the market & a steady flow of price drops up to 5%. A few of my wife’s nurse friends sold their homes within a few days of list in the last month, so that tells me it can still be a sellers market for those houses priced right in move-in condition, at or slightly above median around $500k. That’s in the near term maybe through the end of this year. I don’t see it lasting much longer before we’re in a similar situation as in 2009.

I typed out a viewpoint earlier, then held back from posting it, but it reached a similar conclusion so I’ll drop it here and here is some of the data on that :

I don’t think new builds are able to build for much less or drop prices much (nahbclassic.org/generic.aspx?genericContentID=260013/) . If you look at new starts (fred.stlouisfed.org/series/HOUST) they drop off just as prices max (fred.stlouisfed.org/series/CSUSHPINSA) but well before recession and it took six years to shake out the market. So we are left asking is it different this time… house prices are maxd out, but rates are still low and mortgages are fixed, there is demand but rental is more common with investor ownership, building costs are high but house size is decreasing (nahbnow.com/2018/11/entry-level-homes-push-down-new-home-size/) which is interesting because builders adjust size to how prices are . So what happens next, housing glut (brookings.edu/research/the-goldilocks-problem-of-housing-supply-too-little-too-much-or-just-right/), or just tapering off?

Like you say DD housing is a large part of the economy and I don’t know what would replace it if large slow down of it were to cause a downturn… more debt, imcrease in services, government spending and subsidy, Japanification? I don’t have any answers to that really as that is as much a policy tune, but like a lot of people just see everything overinflated and wondering what the next big idea is, or how it might all disassemble at some point.

It would not surprise me.

On the other hand we have had decades of war already aimed at shaping or keeping the format in place.

It is something of an irony that globalism both offers one solution to world peace at the same time as both destabilising what there is of it and bringing the prospect of large confrontation closer.

We seem to have a never ending supply of houses going up in my Cordelia/Green Valley area of Fairfield. Most of the new builds that are going up right by my house look to be filling up, I might wander over and what deals they are offering.

Wolf, I’m curious about something: is there any correlation between home price and HOA fees? Down here we see new construction bargains; but the monthlies are often comparable to a car payment, almost another profit center for the builder as long as it controls the HOA. Am I missing something?

I don’t know if “correlation” is the right term. But if you buy into a luxury development with lots of fancy and high-maintenance stuff (gardens, pool, doorman, security folks, health club, staff, etc.), your HOA fees are going to be high. In tough times, high HOA fees can exercise downward pressure on prices.

Check out listings for homes/condos that require an “equity membership,” which can’t be amortized. There are condos in Palm City, FL that are selling for under $1000, w/ HOA fees ~$500/month. At the peak, they were selling for ~150K. Of course, at $1K, those condos would still be a steal, except for the $77K membership requirement… if the seller is desperate enough, they’ll pay much of that from their existing stake.

It is really sleazy that they aren’t required to include that “equity membership” in the listing price. After all if you buy the house and are required to buy a “equity membership” the only person you can buy it from is the only person selling one: the person who sold you your house.

Not requiring that this be part of the listing price is fraudtacular.

Yeah, thanks. After I posted, I realized that what I meant to ask was what you answered in your last sentence.

What’s remarkable to me is the fees in some of these not-particularly-fancy developments, where all you get is an automated guard shack and some lawn mowing. At a $300K house, fees of several hundred are similar to a mortgage rate tick.

Or if you buy in SF, your “HOA” fee is a $500+ Monthly money grab which gets you luxuries like…….the privilege of owning one of three units in a 1910 building.

No parking space, no gardens, no doorman, no pool, no snow removal necessary – it’s just a shakedown.

I consider HOA to be part of the ‘total home price’. If I see a $300/month HOA, I’ll translate it into ~$120K of home price on top of listing price. My formula is HOA*12*30.

‘total home price’ is determined by market, so yes a higher HOA fee would correlate a lower listing price

Builders I work with are booked well into 2020.

This is flyover country, no coast prices, zoning & permitting

does not add 50,000+ to the lot….yet.

I don’t see the low end crashing. Lived/worked through the housing depression. Rent prices in our area would have to nose dive, to tamper down low end home building. Rent prices have far outpaced construction costs in my area.

tom – I agree that the low end seems to be strong right now but there is a ton of rental inventory available and more to come. In the Northeast, new apartment buildings cannot find tenants and have gone beyond incentives to actually slashing rates. The downturn seems to be impacting luxury housing and rentals first and this in theory should compress prices at the low end within a year or two.

Lending Danger!!!

Ok, I’m a mortgage broker; and just got a new program from a wholesaler which is the first time I’ve had alarm bells going off. Almost all lending up until now over the past 10 plus years has been income and employment based.

It’s an FHA loan whose only income verifiable document is a VOE (written verification of employment/income). This is a typical document used to layout and validate income for a borrower to match pay stubs W-2 and tax returns. so this new program will not require all of the above except for the simple one-page form filled out by a verifiable company.

Think cash earners, 1099, other….

It’s roughly the same FHA guidelines but super duper loose income verification.

I don’t like it!

Thanks for the update. Now add this to the down-payment assistance loans I see advertised all the time…

Wolf,

Actually on Friday HUD issued guidance that was designed to eliminate Down Payment Assistance programs.

What happened was that there were a few “non-profits” offering these programs making a huge profit and HUD became aware and issues a new blanket policy clarifying their position on assistance programs. From grants, to 2nd loans, state and county and city programs.

It was meant to punish a few but has overreaching impact as many of the real down payment assistance programs are now on hold while their lawyers develop their legal opinions.

https://myemail.constantcontact.com/Enews—CalHFA-is-in-receipt-of-HUD-s-Mortgagee-Letter-19-06–ML-19-06–.html?soid=1102887337889&aid=tl-CRvm9vzE

Broker Dan,

I saw your comment on that. But I wasn’t talking about publicly sponsored down-payment assistance programs. The ads I see are from specialty lenders. I’m not sure how they work. I haven’t checked them out. I don’t know that this type of down-payment lending is even disclosed in the mortgage documentation.

I am hearing from an insider that, in some mortgage products, a 60% back end ratios is acceptable. This could backfire in the next recession. In my opinion, they should be held in the 40%s.

Not conventional or FHA.

Actually, conventional has tightened up recently. Above 45% is difficult to get an approval

And this will drive the used house market down because who would buy a used house if a new house is cheaper?

A lot of those production houses may be new, but they’re sick from Day One: plastic moldings, sometimes plastic floors, synthetic carpets, poor materials and workmanship… No thanks, I’ll take something built between 1900-1960- assuming it’s been maintained – any day.

Those 1900-1960 homes will still probably have a longer life span going forward from today than a brand new dreck Toll Brothers house.

I have a bunch of homes, and they are all 1950s. Personally, I think the new homes are superior, but in the areas where I own homes, everything is in the millions, and the newer homes are out of my reach. Nothing like living in 1950s homes … battling termites, unbonded pools, small forced air heating ducts that can’t handle central air, and no ground wires.

I own a few rentals down in Southern California as well and I am lucky to break even after all expenses. Older homes require high maintenance. I’ve had 2 on the market since last November that I have reduced over 20% in hopes to sell. My (1st) realtor priced according to comps that sold earlier in the year but clearly timing is not working for me. My new realtor keeps telling me she thinks we should lower the price even more before the market really takes a nose dive, I guess I missed the golden opportunity to sell and thinking of pulling off the market and continuing renting until this market picks back up.

SocalJim “hooooooold, rent inflation is coming!” I give deflation and stagflation equal probability. At price levels in all assets like today’s level, anything is a gamble. No fundamentals.

Possibly correction needed in paragraph starting “All this makes basic sense…[home builders] cannot just SELL their houses when the market isn’t with them.” Should be cannot just HOLD, or am I misunderstanding something…

It’s a double negative. The actual text says: “…they cannot just not sell their houses when…”

I know double negatives like this aren’t very elegant, but here it serves a purpose, at least in my mind. Maybe I should have underlined the “not.” Might have made it clearer.

Wolf-

Geeky question. Is it possible your series for months of home supply is MSACSR (from fred?) I think that’s overall home supply, not new home supply.

New home supply might be calculated by:

HSN1F / HNFSEPUSSA. Math suggests that’s substantially less than total home supply – but the chart pattern looks very, very similar.

No, it IS new house supply. No, the data is not from FRED, it’s from the Census Bureau (see the link). New House supply in this article = 344,000 houses = 6 months’ supply.

In the article a day earlier, I covered “existing” home supply (houses & condos): 1.68 million homes.

Combined, supply of new houses and existing homes (houses and condos) = 344,000 + 1,680,000 = 2.024 million (which does NOT included new condos for sale).

Thanks Wolf. Your series IS identical to MSACSR, but FRED’s title was confusing (“Monthly Supply of Houses in the United States”), which led me to think it was existing home supply. Which it wasn’t, so, mystery solved.

Related: do you know where I can find a long-lived timeseries for existing home supply? It would be really nice to put your 3.9 figure from yesterday in context.

I really like seeing both new home and existing home activity – as you have explained, the new home sales people will cut prices as necessary to move inventory, while the existing homeowners appear to be much less willing to do so.

I got the time series of existing home sales, prices, etc. from YCharts, which is behind a paywall. The NAR has some time series data that I get from them, but not existing home sales data that goes back years.

I wonder if there’s a CAFK catch a falling knife kafkaesque situation going on. If there’s a bear market rally in the markets, it’s very easy to get out of stocks, but not houses.

Housing markets are local, but the whole world is influenced by the Fed.

In Australia, where the housing bubble is deflating, Martin North is advising straight out to wait for prices to fall if you don’t need to buy now.

Although housing is local but we have seen in general that impact is felt everywhere

For example loose central bank policies have appreciated the real estate all over the world not just one locality

Coincidence? Interesting how the date of March 2017 shows up both in the interesting article on margin debt and as the last point on the price chart that home’s sold at these prices.

New housing developments west of a Palm Springs, CA, where land is still somewhat affordable, has builders popping out “affordable” housing like candy from a Pez dispenser. Problem is, these SFR’s come with a hefty tax bite, as Property taxes, Mello Roos and special assessments can push contributions to the government leeches upwards of 2.5%. So now that affordable $350K house comes with an $8,750 a year ($729/month) fee in addition to your mortgage. For all the talk of “greed” by home sellers and builders, it is unmatched by those who in government who clamor for affordable housing, while simultaneously making housing unaffordable.

Looks like my parents’ house will going on the market. They are getting too old to maintain it. None of the kids need it.

This reminds me that life circumstances continually change, causing home sales. We aren’t in some kind of new reality where nobody has to sell. There will always be supply coming to market. In the current environment, inventory will be priced lower to move. Builders have to keep the transactions moving as well.

In Seattle, in my neighbirhood, I estimate 30% of the homes will come to market in 10 years because the owners are aging out of them.

One important issue, highly impactful to this discussion, is trump’s tax reform that limits SALT deduction to $10,000 per year.

This may not be an issue in, say, Cleveland or West Virginia. But it damn sure puts a cap on how much aspiring country clubbers will pay for million dollar mansions in Fairfield County (CT) or even Silicon Valley. You can only write off so much state taxes and real estate taxes in a given tax year. It’s pure expense beyond $10,000 combined, and especially so at the higher end of the local RE market.

I suppose throwing LYFT and Pinterest options ones way (if one looks the part…) goes a long way towards mitigating this impact in California. After all, it’s not my money and GAAP profits no longer matter, right?

Dear Mr. Richter,

Tremendous thanks and much gratitude for your so very many years of extremely dedicated works and gifts of knowledge you have so graciously bestowed upon the entire World! Even the esteemed Dr. Paul Craig Roberts, and several silence “others”, consistently concur with your outstandingly brilliantly adept and timely analysis–on a daily basis. If it were possible for me to join all of you in San Francisco, I would in a heartbeat, indeed.

During the entire S&L Crisis of the mid ’80’s, and throughout the entire Resolution Trust Corporation “washout”, I was the regional Controller for the nations’ 2nd largest Real Estate Property Management Company in San Antonio, Texas (yes, THAT one who actually saw some “Big Boys” go to prison, and lots of interesting litigations along the way, as well.) When I used to teach part-time in the late ’90’s, I always used a real-life condo as the prime example of what truly happened when Ronnie Raygun, and his fellow wannabes, deemed it so vital and necessary to change all Tax Laws regarding Real Estate Limited Partnerships, effective during the 1985 tax year. Ha! That was Fun!! Anyways, here’s the example I used: had a LLP purchase a new 1B/1B condo in the San Antonio Medical Center area for $25K in 1983; by 1987 a Texas S&L was holding over $250K on that very same condo; POOF; by the time the RTC was done flushing that entire medical center condo complex out, that particular condo actually sold for $4K (which someone purchased using their VISA card–true story!) A couple of weeks ago, out of curiosity, I looked up that very same condo on Zillow, and even though it’s currently horribly rundown, it has an asking price of $170K. I have been warning people for years, that what we are all about to experience or witness during the next few years with absolutely make the entire S&L/RTC mess pale beyond belief (without you wondrous help, I could not even begin to gauge the ramifications what this will be like. I stopped watching Northern European RE markets back in 2015, as it was way too painful.)

When the esteemed “Wolf-Pups” constantly pester you for enhanced or specialized charts/graphs tailored to their needs (figure it out folks–Wolf’s way too Busy), I almost break my Code of Silence, on the few Excellent Sites as yours, which teach and educate me (and all my Worldwide-Friends/Former Colleagues). I would never ask you this, as it is quite embarrassing for us former CFO’s/Controllers/Economists/”Financial Experts”, but between all of us, we cannot seem to accurately compare the periods of 1985 to 1987 through 1992 (S&L/RTC;) 2005 through 2012 (RE Bubble #1;) and now, say 2015/2019 projected perhaps through 2024 (RE Bubble #2.) We must be getting really old and ignorant, as well! Reminds me of the time I was a Controller taking San Antonio’s “Just for Feet” though it’s audit before the franchise’s IPO back in 1994: 6 of us–all CPA’s with Degrees “Out the Wazoo,” one entire evening (after dinner & drinks, of course) could not for the life of us figure out the classic 5th Grade Algebra problem: when Sally leaves the train-station at 5:00 and Tom leaves at 11:00–You remember the One, right? Luckily enough, one of the IPO Auditors had his son’s 5th Grade Algebra textbook in his Dad’s. We tore through that book and spend 45 minutes figuring out how to solve for “x” or “y” or “whatever,” and laughed until we all realized–maybe it’s not such a good idea that “everyone” knows we’re so very, very dumb!! At the very least, I am absolutely sure, that during the ensuing upcoming years, you shall–once again–enlighten All of Us in your Most Magical and Talented Manner, indeed!!

My friends and I consider you to be the most Superior Supreme Economist who has every graced our Lives, ever–and, we all follow around the clock, all over the World–each and every day. It is such a Distinct Honor to finally be able to let you know how much we truly “Big Like” you, and your entire Universe, which we are so very grateful to visit so very often. I’m emerging from Chapter 7 (Medicare/VA/Big Medicine “back-billing,” so I told all my well-off friends, “If you don’t start filling up Wolf’s Mug with some Big Bucks, I gonna start calling you everyday, as the Sun glides across our Globe; and, even though I live in Austin, Texas–they all know that I actually live on Lhasa, Tibet time–I’ll pester you just before the Sun hits your Country!” We All Owe You, Tremendously!”

Best regards always, Mr. Wolf Wichter! You are a true Gentleman & Educator surpassing Excellence at it’s Finest,

Billy Halgat (512.444.0440)