There is plenty of supply, but it’s the wrong supply, priced too high.

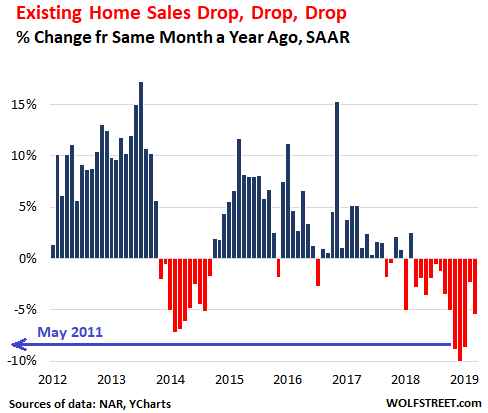

Across the US, hot and cold housing markets all thrown into one bucket: Sales of “existing homes” (single-family houses, townhouses, condos, and co-ops) in March dropped 5.4% from March last year, to a seasonally adjusted annual rate of 5.21 million homes, according to the National Association of Realtors, after having dropped 2.3% year-over-year in February, 8.7% in January, 10.1% in December, and 8.9% in November (data via YCharts):

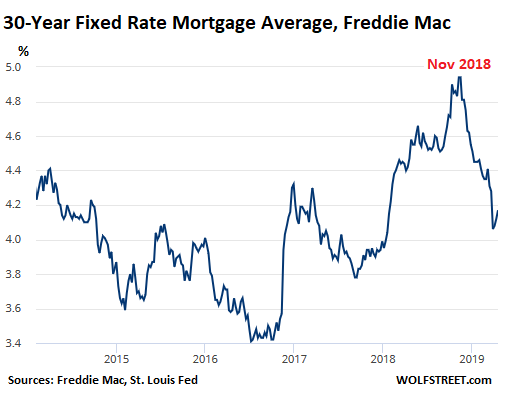

“The impact of lower mortgage rates has not yet been fully realized,” the NAR report said, as the drop in sales volume is occurring despite the fact that mortgage rates had fallen sharply from the November highs.

“According to Freddie Mac, the average commitment rate for a 30-year, conventional, fixed-rate mortgage decreased to 4.27% in March from 4.37% in February,” the report said.

The average Freddie Mac 30-year fixed rate bottomed out in the reporting week ended March 28 at 4.06%, the lowest since January 2018, and down from 4.94% in November. But it has since risen every week. For the week ending April 18, it ticked up to a still low 4.17%:

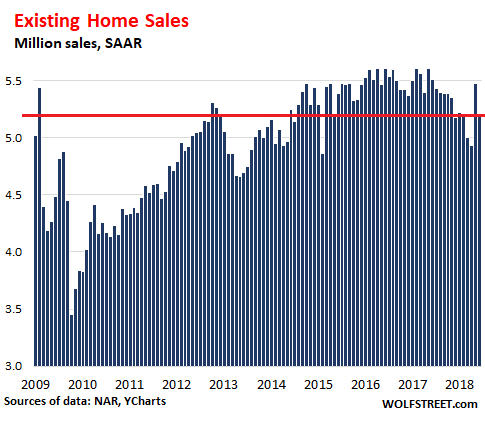

It seems all the lower mortgage rates have accomplished is a slowdown in the decline of sales volume. Even the spike in February, which appears to have been a fluke, was still 2.8% below February 2018. And in March, at 5.21 million homes seasonally adjusted annual rate (SAAR), sales were back where they had been in March 2015 (data via YCharts):

Sales volume by type of home in March, compared to March 2018:

- Single-family houses: -4.7% to 4.67 million SAAR.

- Condos: -11.5% to 540,000 SAAR.

Sales volume by region in March, compared to March 2018, with the West and the Midwest showing the steepest declines. Total sales in SAAR:

- Northeast: -1.5%, to an annual rate of 670,000

- Midwest: -8.6%, to an annual rate of 1.17 million

- South: -2.1%, to an annual rate of 2.28 million

- West: -10.7%, to an annual rate of 1.09 million.

Inventory of for sale at the end of March was up 2.4% year-over-year to 1.68 million homes. At the current rate of sales, this represents 3.9 months’ supply. In other words, there is now plenty of supply, but declining sales volume tells us that it’s the wrong kind of supply, with prices too high for potential buyers.

“The lower-end market is hot while the upper-end market is not,” according to the NAR report. “The expensive home market will experience challenges due to the curtailment of tax deductions of mortgage interest payments and property taxes.”

Alas, in many markets, even the “lower end,” after years of price surges, has become very expensive.

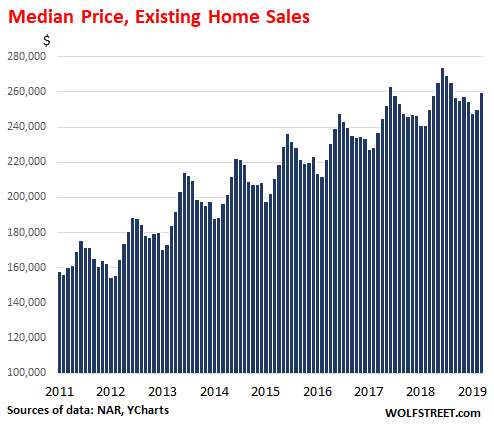

So, with all markets across the US thrown into one bucket, the median price in March rose 3.8% from March last year to $259,400. Prices are subject to seasonality, as the chart below shows. Median price means half the homes sold for more, and half sold for less:

By category: For an existing single-family house, the median price in March rose 3.8% year-over-year to $261,100. For an existing condo, the median price rose 3.6% to $244,400. Median home prices by region:

- Northeast: +2.5% year-over-year, to $277,500.

- Midwest: +4.6% year-over-year to $200,500.

- South: + 2.4% year-over-year, to $227,400.

- West: +3.1% year-over-year, to $389,300.

Persistently declining sales on rising inventories and rising prices is the phenomenon of potential buyers and sellers being too far apart, and sellers being unwilling to lower their prices to where the potential buyers are.

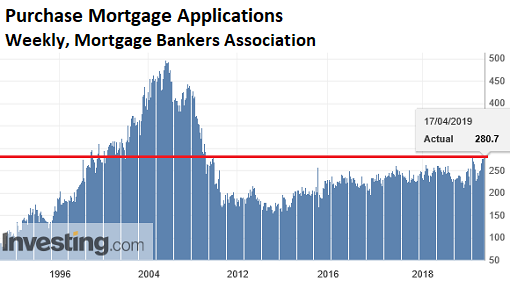

The hope has been that the recent drop in mortgage rates would encourage buyers to step up to the plate. And mortgage applications have risen this year, according to the Mortgage Bankers Association, showing that lower mortgage rates encouraged some fence-sitters to apply for a mortgage to purchase a home. The chart below (via Investing.com) shows “purchase mortgage” applications and not “refinance mortgage” applications:

But many homes are bought by domestic and foreign investors and by other cash buyers that don’t need mortgages. Large investors can borrow at the institutional level. And they’re not necessarily swayed by lower mortgage rates. And this may be the phenomenon we’re seeing here.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wrong supply: overpriced; McMansions; those not conducive to aging-in-place; suburban/gated/golf-course, jumbo loan

Right supply: smaller, transitional, urban, conventional loan

When will they get it. They won’t loosen up on credit scores and half the country are renting for double the price of a mortgage. So you have less tax revenue and houses sitting empty. We need to look at America’s #s and see the real thing. They can afford a mtg of 1000 instead of rent at 1600.

Huh? In most high-priced (meaning: coastal) areas you can rent for much less than the cost of mortgage. You are just spouting propaganda. Never seen you here before.

“They won’t loosen up on credit scores.” I’m a long time realtor and sincerely believe that if you want to see 2007/8 all over again then by all means, loosen up on those credit scores. This current housing market has been goosed along by some of the lowest rates in history.

These are not “free market” interest rates. There’s nothing free market about them. You’ve got a panel of delirious Keynesian phd’s who know how to steer our millions of lives. How does that happen without unintended consequences? And we haven’t had a recession in how many years now? This whole stinkin economy is BS. Trust it at your expense.

Also, when incomes go up 10% year, then people can buy real estate that is going up 10% per year. But last I checked, 2.5% was considered a decent raise, and 1% more typical.

Anybody who had their credit destroyed by unemployment, or lost a home in the financial crisis, will never be able to enter the mortgage market in the US. This group is a permanent underclass in America. As long as that’s the case, you will have an ever shrinking pool of buyers.

Had a neighbor go through bankruptcy.

The kept their house and 1 out of 2 cars.

With 2 years – credit card applications starting flowing to their mailbox. Within three years they were able to refinance their mortgage. They got a new car.

Bankruptcy barely was a speedbump. They got rid of lots of debt and basically kept everything they had. And the credit starting flowing again within a few years.

That’s a very interesting story. I had the feeling that credit offering companies would start overlooking past problems much quicker than we are led to believe. They want the business, any business, so bad.

Fica changed algo to score repos and bankruptcies due to the great recession softer….lots of credit score destruction had to be unwound to create credit push again…..

Same with my sister. Bankrupt, lost her house.. Several years later, new house, car.. She paid the price in interest penalties for a bit, but really not much of a speedbump.

Absolutely correct. Had to go thru bankruptcy. Kept house. Kept cars. Kept sanity. Within a year had 3 credit cards from 3 national banks with $10,000 credit lines. Shed all previous credit card debt plus some irritating other debt. Never, ever heard from a creditor.

Not proud of what I had to do. Either the banks or myself. I chose the banks.

5 years now. New mortgage in new retirement home. Have 0 debt outside of mortgage and one car. One

Credit card is used and paid off monthly. My FICO is 720 per my local bank

Yeah, the system is so corrupt and criminal. Not a surprise if you know how they create the “money”

Petunia — Commenting on your statement ‘ever shrinking pool of buyers’. There exist provisions for anyone in the world who has the wherewithal to take advantage of USA EB5 Visa program. https://en.wikipedia.org/wiki/EB-5_visa

There also exists the O Visas which most Russians use (“who possesses extraordinary ability in the sciences, arts, education, business, or athletics, or who has a demonstrated record of extraordinary achievement in the motion picture or television industry and has been recognized nationally or internationally for those achievements”)

https://en.wikipedia.org/wiki/O_visa

The USA will never ever run out of Cash buyers. The system will not permit this to ever happen! (At the end of the day, The bad guys are caught by our wonder surveillance systems in place).

The cash real estate market is a very small segment of the market. Right now I am willing to speculate that for every buyer who pays cash, there’s a seller taking their money out of the country, and buying overseas.

They dont even need to take their money out, as more and more of these transactions, are being settled outside the US mainland.

Frequently not even in US $ these days.

This is a fallacy

The home sales have stalled becoming of unaffordability.

Get your popcorn and enjoy the show

Government “systems” all fail eventually. To paraphrase the late great Milton Friedman, “Every fiat money system tried in history has failed.”

It’s just a matter of time. It’s like a money addiction (debt) where governments assure themselves that they can break the habit anytime they want to. (Imagine how and what they must cut to balance the budget.) Most government leaders know this but don’t have the nuts to speak up like they did in the 1980’s when our debt relative to revenue was very much lower. For the government to stimulate the economy now, what must they do? Cut rates? Print a few trillions more (debt)? Try to remember that WE must pay interest on the national debt. And by the way, who can we continue to sell this debt to? You may have guessed it. US!!! Happy shopping.

This couldn’t be further from the truth.

1-7 yrs waiting period depending on the derogatory event

Petunia – This isn’t true. Your credit score should recover within 5-10 years of defaulting on a mortgage.

There is an ample pool of buyers but there is a mismatch between demand and what is actually for sale. All of the listings are oversized, cheaply built 90’s early 2000’s era mcmansions priced way too high. Young buyers want modest sized, affordable homes in walkable neighborhoods.

Since there is a scarcity of modest sized housing in walkable neighborhoods, they get priced at ridiculous premiums. I can’t even find a townhome anywhere I would want to live in the entire country for less than $600K.

Petunia has no idea what he’s talking about with his credit comment.

Credit is available via FHA and Conventional

>mcmansions priced way too high.

The UK had a similar problem in the past. A lot of large old houses were converted into smaller flats, add in a streetcar service, and some design for walkabilty and problem solved.

One of the real estate types that seems to be languishing on the Market here in the outskirts of Portland is the large “country property”. These are usually big rambling houses, with huge yards, 4 car garages plus RV parking big shops and giant patios. They were all the rage with the well to do in the 80, 90’s and early 2000’s but now their owners are aging out. There does not seem to be many people in the market with the money to buy these places, the money (and time) to maintain them and the desire for the long commutes to the type of job that would give you this cashflow.

That’s not just Portland, that’s kind of everywhere. Really big houses in the middle of nowhere/country club that don’t make sense except for retirees that either were able to cash out their first homes at nice profits or have fat pensions/401(k)s.

Not practical for anyone who needs a job to pay for a mortgage into their 60s.

I’d rather go for the land .. plus a yurt, or maybe a modest cob/strawbale/earthen berm abode utilzing passive solar in it’s design — I know .. dream on, right ?

The typical wood-frame balloon construction built is wasteful and inefficient, and is reflective of a ‘high-energy’ energy economy, something of which is out-of-date for the times of scarcity that are looming on the horizon !

Whilst typical stick-framed buildings are wasteful, the problem is with the design, not the building method. I have designed and built a stick-framed home with 40% less energy use than similar homes around, and at only a 3% higher material cost than the typical. Stick frames are easy to build solo, I did, and cheap. There is no need for unusual construction methods, though you can do that if you wish.

Nonsense Polecat. I just built a stick frame house, by myself….last year. I have been building for 40 years and practices are pretty amazing these days. R40 in the ceilings, R20 in the walls, double paned windows, etc make for almost no heating costs. My tenant averages $1.01 per day for heat/lights/hotwater/and all appliances. Stick framing, post and beam design, open concept. My own home, at approx 1500 sq ft doesn’t cost much more. We use a wood stove most of the time for basic heat but when away use in-wall fan driven electric heaters. I also run a full shop with lots of power tools. Last Hydro bill was $1.71 per day.

If labour is free then other methods may save money, but stick frame reduces wood waste and allows rapid quality construction thus lowering costs. Apartments are now going to 24 floors stick framing for all of the above reasons. Furthermore, floor systems can use other products (waste…osb) and post and beam uses glue lam waste negating the need for expensive clear timber.

Senecas Cliff – Yes, this is the exact problem. Baby boomers loved huge houses on huge lots in bad locations that are ridiculously expensive to maintain.

I’m seeing townhomes and condos in new suburban town centers selling for more than the isolated single families on big lots.

“…the phenomenon of potential buyers and sellers being too far apart, and sellers being unwilling to lower their prices to where the potential buyers are.”

I wonder whether these sellers are unwilling to lower their asking because they are expecting a fat check, or they are unwilling because they realize that they will need a fortune to buy their next house.

It could be a combination of the two (and other) factors. Before moving out of CA, I lived in several cities in the Bay Area in the past 30 years and what I see there is beyond insane. I’ve been saying for many years that in the Bay Area, Real Estate as well as life in general, are unsustainable. Yet, prices (and life in general) keep getting more expensive every year. I’ve lived through three busts and I have no doubt another one is coming. I’m just shocked this cycle has lasted that long.

In California, Prop 13 aggravates the reality distortion field in prices. It’s conceivable that your neighbor on the left pays $3k in property taxes while your neighbor on the right pays $25k for an almost identical place. The only reason for the difference is that the left neighbor bought his house in the 80s while the right neighbor bought it last year.

Prop 13 may be one of the main factors behind the sellers’ resistance to lower their prices in CA.

Prop. 13 is encouraging me to stay put. The run up in residential property prices in good neighborhoods over the past four decades means that sellers who have been in their homes since before Prop. 13 passed face huge capital gains taxes when they sell their home.

It seems like those are two separate things. If you’re 55 or older, you can take your low prop 13 tax basis to a replacement home if the home is in the same county or in one of ten participating counties. (The pertinent propositions are 60 and 90.)

I think it’s really the huge capital gains tax that gives people pause to move. It used to be that you could roll your capital gains into your replacement property if you bought within a two-year timeframe, and I wish that law were still in effect. People feel locked into big family homes for life. Easing up on the capital gains tax would create more movement in the market and would bring more efficiency to living situations.

Surely, capital gains tax can’t be the only reason, there must be more to it?

In Sweden, looking for a house some years back, we noticed that one problem seemed to be older people becoming over-invested in their house, lured in by generous tax deductions for improvements, their main mistake being borrowing against the house to pay for the work “to increase it’s value”.

The problem with home improvement is that after some limit depending on the size, vintage and style of the property is reached, then everything that is added is just more shit for the next buyer to rip right out and drive off to the dump in order to restore the property; further improvements detracts from the value!

These people then find out that the offered price, minus the 25% tax on the profits will not cover the mortgage, then they are sitting ducks to be screwed over on the bankruptcy auction.

People clamouring for tax deductible interest on mortgages should expect to pay capital gains. Can’t have it coming and going….just saying.

CA has its problems and it’s an easy scapegoat for certain segments. But the housing market is “crazy” all over. One of my wife’s brothers moved to Oklahoma some years ago. In 2013 the median cost of a house in OK City was about 100K. In 2018 it was about $188K. Median household income was around 50K last year. Almost no one there could afford a house even though they are dirt cheap. You see a hot rental market as institutional investors are eating up the inventory, driving up prices and renting them out. Rental prices are increasing too.

Now they can’t move back b/c there is no way they could buy back into this market. In our neighborhood, the majority of houses don’t make it past the first open house weekend. Before the next weekend is up it’s pending then sold. We are already prepared that we will have to sell our house first then buy.

The billionaire class doesn’t think like you and me. The billionaires are buying everything, not the middle class.

Chinese billionaires don’t care if they take a 10% loss on a home in California because that’s better than a 100% loss if the party decides to nationalize their Chinese property. American billionaires don’t care if the houses they buy and rent don’t appreciate much, they pay in cash and don’t need to pay a bank for a mortgage.

The billionaires around the world are buying up anything valuable in the USA while inflation means the middle class slowly gets stealth pay cuts every single year.

Old dog – The greedy baby boomers realize there is an extreme shortage of land and eventually somebody will cave in and pay the premium. The people that aren’t reducing their prices probably don’t need to sell and have time to test the market. My guess is that these people are in their 50’s and 60’s and are in a strong financial position.

Price cutting is essentially holding up a big sign that says “I need out now, please abuse me however you please”. You are better off delisting than cutting your price. A price cut generally leads to getting destroyed at the negotiation table because you are showing your hand.

I bought 16 acres of residential zoned land 10 years ago for $200K. It has beautiful mountain views, hydro, road access, and I put in a pond, orchard, garden area, etc. Other locals laughed at me until I told them it was the price of two 1/8 acre lots in town, just 45 minutes away, and that all the other land in the valley was tied up in the ag land reserve or designated forestry use, only. Those town lots are now pushing 200K per as of this writing, sometimes more.

Oh, by the way we are not greedy Baby Boomers. Rather, we are boomers who saved, didn’t have nice cars, eat out in restaurants very often, and worked lots and lots, plus live modestly. I just like land and have alwayss believed it was the key in ‘prepping’ for much of what we see unfolding, right here on WS.

My kids will get it, I guess, as we aren’t selling. Ever. We don’t want any development around us which is what has chased us out of everywhere I have ever lived before. My best friend, who lives in a small condo, spent his money on vacations, etc.

Paulo – You sound pretty greedy to me. Buying more land than you need because you “like it” is the definition of greed. You and your fat, greedy baby boomer cohorts have made health care and real estate affordable for your own children. Maybe if you didn’t gobble up all of the real estate your kids could afford to buy their own 12 acre useless plots of land.

Are there any supporting data points that indicate Millennial purchase consumption is less than year before?

Aside from overpriced market, US doesn’t seem to have the same supply of buyers that once filled the gap. With Milennials still paying off loans, they aren’t ready to take advantage of lower interest rates.

All I could find was at

https://www.bls.gov/news.release/pdf/wkyeng.pdf

where usual median wage for to 24s was down over a year. Could not find discretionary income real means by age up to date etc. There are a few sites (trying to) say it’s great for millennials and genx etc. but most are not so positive e.g.

” Millennial spending is actually shrinking, as 18- to 29-year-olds today spend nearly $20 less every day than their counterparts roughly 10 years ago, particularly on items like apparel.

Why?More Debt. Most Millennials come into the workforce carrying a much heavier debt burden than past generations, thanks to the high cost of education. ” Forbes

or for UK which I guess is not too too far off

” The net household property wealth of those aged 60 to 62 is 17 times greater than those aged 30 to 32, according to analysis by the Office for National Statistics….

A decade ago those aged 60 to 62 had just six times the property wealth of those aged 30 to 32 but this gap has since expanded rapidly.

Rachel Griffin, tax and financial planning expert at Old Mutual Wealth, said: “The long-term implication of this wealth inequality should be giving the government sleepless nights. A deadly cocktail of childcare costs, rising tuition fees and unaffordable housing have created a generation who may right feel their outlook is bleak.” ” ftadviser

Obviously many of us are living this reality and have our own real experience to remind us exactly how it all stands .

Correction – for women down a bit, for men up a bit.. so roughly the same.

Also just looking through earnings, the median pretax yearly for 25 yr olds is @ 25k on one site, another site give household for same at @ 50k. Anyone gets to figure out if that is enough to buy a property with I suppose…if not you have half of that age group at least unable to enter the market..if they even wanted to at current prices.

Peter – This is anecdotal but I am a millennial in a relatively strong financial position. We sold our townhouse last year because we hated owning a house and we got lucky and bought at the right time (2012).

We thought we would be the only relatively well off young family that wanted to live in a luxury apartment, but the building we moved into has 20 young families just like us. Doctors, Lawyers, consultants. All young families with sufficient income and capital to buy high end homes but choose to rent. This is apparently happening all over DC and is a significant change from previous generations.

There is definitely a growing sentiment among young professionals that owning a house has major downsides. Again, maybe this is just anecdotal, but based on people we know, it doesn’t seem that finances are the only reason millennials aren’t purchasing houses at the same rate as previous generations. Many people prefer to have the flexibility to move around a lot to capitalize on job opportunities or remote work flexibility.

Interesting, Ed, but the problem with renting is that when you want to take control of your lifestyle or living conditions you have to move. Of course everything is different with adequate income as everything is therefore done by choice. However, there is nothing more sad than talking to a neighbour that is in ill health, has little income, rents, and has decided to move because their landlord is an absolute tyrant. They are now going to move into a fifth wheel RV in a little bogus trailer court and are hoping their new tyrant (landlord) owner allows them to keep their dog. They could have bought around here 30 years ago just like everyone else, they both were working and had good jobs. They also liked to party and smoke; and therein lies the lesson. That is the same story of our tenant, my great friend. Awesome kind individual, who just never bothered to buy a place until it was too late. When the money stops so does the options. One was forced into retirement and the other neighbour’s health tanked.

Paulo – You don’t really own a home, somebody always has a lien against you. Whether it’s a bank via mortgage, or the gov’t via property taxes.

Add to that the cost of property insurance, maintenance, closing costs, and massive amounts of capital tied up in an illiquid depreciating asset.

If money is a problem, the last thing you want is a huge portion of your wealth tied up in a house. The only time you should ever own a house is if your timing is perfect like it was in 2010-2012 and houses are selling at huge discounts. Otherwise, rent and move around to capitalize on new opportunities.

For centuries, interest rates have gone up in a boom and down in the contraction.

One would not expect that a decline in mortgage rates would prompt strengthening of the housing market.

That would be in boosting sales or raising prices.

3.9 months is a solid sellers market. 6 months is a balanced market. In addition, prices continue to grind higher … up almost 4% year over year at the national level. Nothing to see here except a sellers market where buyers are making the mistake of striking. All they are doing is putting more stress on the rental market causing rents to spike again, and this rental spike has turned home into cash cows … who would sell if they don’t need to? I feel sorry for so many who did not get in several years ago when the getting was good. That 800K fixer in on a large lot in east Manhattan Beach is now a 1.8M fixer, if you can even find one to make an offer on. OUCH.

SocalJim,

“6 months is a balanced market.” Maybe 10 years ago. Given how fast the process is these days, four months is the line, or maybe even lower:

https://wolfstreet.com/2018/10/19/us-housing-turns-into-buyers-market/

Agreed. The Dallas Morning Snooze keeps repeating that nonsense about 6 months being a normal “balanced” market. That’s total bunk. If we had 6 months of inventory in DFW, home prices would be tanking, and we would likely be in a full-blown recession.

Consider this … if 4 months is the line, then you would expect year over year price increases would exactly track inflation. My conclusion is 3.9 months is a sellers market since, according to today’s report, home prices are increasing at nearly 4%, which is higher than the inflation rate. Is 6 months the line? Don’t know. But, it appears the line is definitely higher than 3.9 months.

SocalJim – The 3.9 months supply is including the extremely tight 1st tier or “affordable” homes. There is a much larger supply of homes prices over $1.5M. In California, there is a glut of luxury homes in coastal areas that nobody wants to buy. No end in sight for sales and price declines in Manhattan Beach.

King County (Seattle) had a median price decrease based on NWS year over year in March.

Previous price – 625k

Current price – 622k

Previous MOS – 0.62

Current MOS – 1.15

It seems clear there is significant sensitivity to supply in several of the current high flying markets. 6 MOS does not seem a reasonable line in the sand for them.

I think are a few takeaways from this article and the decline in existing home sales. 1) There’s a large percentage of homeowners who locked in very low rates during the past 10 years. These homeowners will not move unless there’s a family event; 2) All RE is local and local RE varies widely by sub-market. 3) Tax policy is affecting the SALT states

Pretty good summary right here.

“The impact of lower mortgage rates has not yet been fully realized.”

If that’s true, we’re all in big trouble.

Funny that Yun doesn’t seem to understand what’s driving home prices. As Wolf mentioned, even the homes on the bottom end of the spectrum are now too expensive for many would-be buyers. This is what happens when a hyper-financialized housing market detaches from fundamentals like wage growth.

DFW saw respectable sales in March, but April may not be so pretty. Texans are now getting their appraisal notices in the mail from various CADs, and the record-high property tax bills that come with them. As the state legislature looks to reform school finance and reform property taxes, local appraisal districts are putting the screws to homeowners to make up for under-assessing big commercial properties. It’s how our two-tiered “Texas Two-Step” property system works to feed the rich and trample average homeowners. Those record high property tax bills won’t be good for sales.

Pusing on a String — hath arrived.

I’m a young adult engineer – work seems to be only short term contracts, hiring is much less aggressive than a year or two ago in the technology sector. Have personally become hyper-focused on reducing student loans and personal expenditures and saving for next inevitable road bump (personally or macro level). Will take me maybe 4 years to pay off student loans on a very minimal lifestyle and assumes constant work (a big assumption), and another year or 2 to accumulate the 20% down payment on a very modest house. Condos hold no long term appeal personally. Student loans limit bound discretionary income and savings, wage growth is stagnant, and capital accumulation is difficult. Tax code penalizes single renters (~70% of young adults). Macro-level issues really bother me, Social security, debt, unfunded liabilities, declining global economic health, demographics etc…

Housing prices are beyond my reach. The median price has nearly doubled in less than a decade. I may consider looking to buy in about 6 years. No manipulation of interest rate will change my (and many) financial reality – prices too high, income is severely debt constrained, and capital accumulation has outstripped earnings potential and asset inflation. None of this factors in property taxes (likely to increase), poor building quality, infrastructure declines, energy cost(transport and housing) or house location. Only serious student loan Reform/relief or a 50% drop in prices could change my reality. Can’t jump on the property treadmill and “trade up”- and frankly – at this point, I wonder why would I want to?

Not really a dreamer, more the Reality man!

Good Analysis i think.

If you are on the East or West coast, the housing market could change fast, so it seems like a good plan to wait it out.

“Tax code penalizes single renters (~70% of young adults).”

Young adults typically don’t make enough money to pay any income tax.

The poor pay no taxes. The rich have armies of accountants to shield their income. So who is left? The upper middle class. We’re the ones who subsidize all the spending for the free s**t army.

“Young adults typically don’t make enough money to pay any income tax.” I call BS on that, using your own examples from your prior comments.

The young adults in the Bay Area that you keep referring to in your prior comments to show that rents and housing aren’t overpriced, so folks that work in tech and that can afford to pay $4,000 rent a month without breaking a sweat, according to you, they pay a TON in income taxes. They’re sitting ducks for the taxman.

But sure, the young adult restaurant workers might not pay any income taxes — though they pay SS, medicare, and unemployment contributions, plus sales taxes, gasoline taxes, bridge tolls, and all kinds of other taxes and fees that eat up a big part of their meager incomes.

But according to your own comments, the Bay Area and other parts of California are stuffed to the gills with people that can easily afford those housing costs here. You have used this argument to prove that this housing market isn’t overpriced. But people who can afford the housing costs here, they earn enough money to pay taxes out the wazoo. They’re single, and they’re renting. San Francisco is a city of renters. And they’re paying so much in taxes and rent that they have trouble saving for that 10% down payment that’s now $120,000 (for a median condo).

So if I go with your argument that young adults pay no income taxes because they don’t make enough money, then the California housing market is totally overpriced, which contradicts your prior comments.

And if I can go with your argument that the California housing market, and particularly the Bay Area housing market, isn’t overpriced because young people make so much money that they can easily afford it, then, well, they pay taxes out the wazoo, contradicting your current argument.

You can’t have it both ways. If you can afford to buy or rent a home in California, no matter what your age, you pay a ton in income taxes.

TheDreamer – The new tax code FAVORS single renters. Your tax rate was cut and standard deduction doubled. Homeowners got the shaft.

Where do you live? It’s hard to imagine a young engineer would be making less than $150K these days given how difficult it is to find workers in many cities across the country.

Im a big fan of the tax change as a renter myself, but I wouldn’t say homeowners got the shaft.

Raising the standard deduction doesn’t raise homeowners taxes, it just targets more savings to renters.

I realize that some homeowners got hit with a maximum deduction for property taxes, but the dollar amounts are so high that only really high incomes -at least double the median – pay that much.

Standard deduction doubled, but personal exemptions were eliminated resulting not so much difference to arrive to AGI for most people.

Ed – not sure taxes favor any normal wage earner, but married couples are taxed lower than singles, renters have 0 deductions (which may be less of a thing now but just dovetails into homeownership being unaffordable – and certainly was not retroactive) and no child deductions. The meager student loan deductions basically disappear at ~70k, so it’s a stealth gotcha.

I live in the Twin Cities – I have no idea where you live but engineers, particularly just starting out, make nowhere near that – think half that. When I got started in the aftermath of the financial crisis I was being paid $15 an hour with meager benefits and happy I had anything.

The current national average engineering salary is $95k with little deviation according to a quick google search – across all disciplines. Entry level engineers make around $60-70k nationally nowadays. Most engineers I know are ever aspiring for the mythical and lofty $100k (which seems to require a masters). After that, you can only hope for cost of living adjustments due to commodity engineering corporate thinking. Stock options aren’t a thing anymore and I do not personally know any engineers that get bonuses.

Only 2 metros are anywhere near your 150k, with San Fransico and New York paying on average around 120k, however, a cost of living comparison says 100k in the twin cities needs $261,770 in SF to be comparable (mostly due to housing, but also general cost).

The effective tax rate (fed, state and FICA) in MN and CA is about 30% on the lofty 100k, plus sales tax (6.9%), gas tax and all the other little gotchas. Leaving 70k at best, and more like 60k after tax and fee.

Engineering, as a discipline, basically requires a college education. Average undergrad student loan debt is now $37,121, graduate $57,600. Translating to about $500 to $900 a month or 6k to 11k a year for minimum payments (usually takes 20 years to repay). Interest rates are about 6% and rising, and about 1/3 of your payment services interest. I have a masters and started a Ph.D. so my debt is higher. :(

Take a lofty 60k after tax and fee – 15k for rent (low urban national average) – 10k for very modest living expenses – 10k for student loan minimums. Add a car payment if you wish for another 5k. You are left with 20-25k per year- nothing to sneeze at, but still will take you several years of exclusively paying student loans. Then you will need another year or 2 at least to save that 35-120k downpayment for a median house. Longer if you put anything towards long term savings or a rainy day fund (again most jobs are contracting and eventually there will be a recession). https://www.investing.com/news/economy-news/nearly-95-of-all-job-growth-during-obama-era-part-time,-contract-work-449057

Any job, not an engineer or a young engineer at lower pay will have a substantially lower salary and similar loans. You could save for the downpayment first, but that was not working for me, as I could not keep up with house price inflation. I have been burned already (both debt and high housing prices) and now am embracing debt free lifestyle dream and the debt snowball approach. Never again.

Lets just say the 40 year debt/interest rate supercycle is over. Now assume we have entered the same situation as Japan and you knew for certain that for the next 40 years real estate prices would steadily decline at 2-3 percent per year ( even on the beach). Would it make any sense to buy at all, or just rent and let the landlords become the muppets taking the relentless depreciation.

I view homeownership as a good lifestyle decision rather than a good financial decision at this point.

We are in our mid 30s, make a combined income that puts us in the top 10% of this country, and save aggressively. We’re just tired of renting and ready to have a place we enjoy living in and gives us a good quality of life.

We have no expectation of making anything on the house over the next 5-10 years. If so, great, if not, we can accept that. Our nest egg is in an index fund portfolio, not housing.

Here’s a little secret about RE….. You make the profit when you buy, not when you sell.

That is to say, buy at an appropriate price, you’re set. – cash flow positive.

The sad reality, the vast majority of buyers overpay from day one…hence they will never make a profit.

Yup. Let’s just wait it out, what’s 40yrs?

Lol

Markets tend to go up in an orderly manner and down in a disorderly manner.

At some point prices will go down and at some point there will be panic. I’m prepared to wait for up to 10 years and I’ll be there to take a lovely home off the hands of a family who in a panic desperately needs a cash infusion.

Senecas Cliff – Unless a house is going up at a 3.0% annualized rate, you should never buy. If a house isn’t going up in value you have dead money tied up that isn’t earning any yield. The stock market has historically generated 9% annualized returns.

You also have to overcome the massive hurdles of closings costs, mortgage interest, property taxes, property insurance, and maintenance. You have to also quantify how much being tied down to one location for 10 years will cost you versus relocating to find higher paying work or a better life style.

The initial calculation should be based on the cost of a rental versus the cost of the mortgage less tax deductions. If your mortgage expense is half the cost than your monthly rent, you should consider buying. If the mortgage payment is greater than the monthly rent, you should rent. Anything marginal could probably go either way but from my experience owning is a pain in the butt and any meager savings I would gain from owning would be offset by the headache.

Conclusion: Always rent unless there is a screaming buy signal from your analysis. (Total mortgage expense is half of rental expense)

Tangential utopian dream:

Where house is viewed as a place to live in and raise a family.

not as a retirement nest egg.

not as an instrument for investor speculation.

not as an ATM by the taxing authorities.

Long time commenter and housing market bear – I’m about to snap up a townhome in a 50 unit community that is priced affordably (key words there). With interest rates oddly low, seems like the stars are aligning, if only for a brief moment. Most of the property being sold in my city has been in the high end ($600k+), where a small house with a large yard is torn down to plop two or three giant LONG and SKINNY houses next to each other (horrible for firefighting by the way), with a tandem one car garage – pretty pointless garage setup if you ask me.

The townhome I am looking at purchasing is actually sensible – prices in the high 200s to 300s range, normal two car garage, acceptable level of living space, with an option to bring in a roommate if necessary, 2 minutes from major highways and 10 minutes to downtown core. The good part is they are still building so I don’t feel the need to compete with multiple buyers for a single property – there are always more on the tract to purchase. The price has only increase 1.5% since last year also, down a considerable YoY increase from the 2015-2016 bonanza. That might be the biggest stalling of housing prices I’ve seen in this city.

There is another large approx 40 unit townhome community being built just next to this one with similar pricing and setup. It seems that at least a couple of the builders are realizing that the high-end is no longer feasible and are now pivoting to mid to low range segment. The best part is the HOAs of both communities do not allow AirBnB. I am ready to get out of my current neighborhood which is littered with these types of properties – I essentially live in a hotel district with a hollowed out sense of community.

NotBuying – I don’t like your plan because developers are adding a ton of inventory. If there is available land to build new townhouses you are going to be screwed. Your property will always be competing against newer construction in a neighborhood that permits attached houing/multi-family units.

Always buy in inventory constrained hoods that don’t permit multi-family or attached housing. The best school districts are always great investments because there is no more available land because of inefficient single family zoning.

You can add way more townhouses in a small area then you can single family.

Like I said before, most of the properties getting built are multiple tall and skinny homes in a single piece of land. These homes are selling for over $600k. As far as available land, there are few pieces that have as much space as the two communities being built currently (in an industrial area). It would take a developer a lot of time and money to get the same number of single family residences to move out before being able to build on a large plot of land. As Wolf said in his article, all that inventory is at the high-end, anything lower is still an insanely hot market. The city is already busting at the seams with an influx of workers. Builders can’t build fast enough. The codes department is often allowing the building of multiple homes on a single home residence piece of land without even batting an eye. And these are in the “inventory constrained hoods” that you mention. These areas are ridiculously high priced already, only the top 10% of income earners (most likely need to have dual income in the top 20% at least) would be able to afford in those areas. And it is littered with the aforementioned AirBnB properties. Eventually the area I am looking will also be inventory contrained, but it would be stupid to move into an area like that.

Municipalities have a lock on development costs.Years past developers could go out into non-incorporated areas and apply for a NPDES permit for a waste water plant. No way a developer would do that today the goverment will start issuing fines before you start it up. A municipality cannot be placed under a moratorium for connections to a septic sewer system , but a non-municipality can be shut down for any reason. The average moratorium is at least three years. This is where the armies of bureaucratic regulators justify their jobs. The developer gets fines the municipality issues bonds and debt. The regulators will not take on a municipality because the poltical apparatus will neutralize them. Bureaucratic rent seekers always prey on the political weak. If you are the lucky developer where there is an economy , especially a government supported economy, and you know who to bribe ,You have won the lottery. You will not be shut down no matter if the municipality treatment system is over-loaded and goes into a receiving stream un-treated. Politician will yell taxes, bonds will be issued and the new system will carry their name. No connection will be denied. You will not go outside the municipality and do that.

I can only speak for my little corner of Los Alamos, New Mexico…

1. The number of places you can build is low. County ordinance says nothing over 3 stories without a really good reason (like the Department of Energy says they want a 7-story office).

2. There is almost nothing to rent or buy right now at any price so most sales are going for over asking price. The lab and its various contractors are in a hiring phase and it’s causing problems for those that don’t want to commute.

3. Property values have absolutely skyrocketed. I bought my 2/2 condo just over 2 years ago for what was a fair price at the time — $110K. Condos in worse condition are now selling for $170K+. This isn’t just condos, it’s everything.

4. The thing that MIGHT slow it down is 2 low income properties have been approved (one seniors only, one regular), which will help those not working for the lab; and a standard sales price condo has been approved for a location vacant for a few years now (where the “Black Hole” used to be).

Anything priced under $400K is selling fast. Expensive zip codes in the Northeast and West Coasts are starting to come under pressure. Your neighborhood will remain strong until the weakness in the expensive zip codes drives the unemployment rate up. You are 3-5 years away from your condo going back down to $110K.

In your opinion Wolf, what set of circumstances in this financial market environment lead to the increase in forced selling needed to bridge this gap between the stalemate in the property markets?

Because I can see markets being at a stalemate slow decline for a long time without more forced selling coming through if overpriced RE in EM’s is any clue.

I think we’re far away from forced selling. You would need a surge in unemployment where people suddenly can’t make their mortgage payments, or a big drop in rents where investors start walking away from their rental properties. This scenario is not even on the horizon yet.

Yeah, I don’t think the fall in rents is close to even happening, I think that would spike up first as landlords try to cover any declines in occupancy due to employment pressures.

So for 2019Q1 we have had about 4x the store closures we had from 2018Q1, assuming employment are proportionally tied, when should we start seeing this factor into rent/mortgage payments (to the degree, even if small, will contribute at all)?

What about that recent 52.9 services PMI print (vs 55.3 expected) for march? You see that ship turning around next this month? Seems like we’re threading a fine line here and this is only Q1…

PreWaterfall – Rents already seem to be dropping in major markets that I’m looking at due to oversupply. My guess is the inventory build and sales decline is driven primarily by investors exiting the market as they fail to find good tenants.

Ok, Thanks Ed. So rents are dropping in major markets, and from the recent new home sales data, so are prices for homes that are being sold.

Question is, does this level off or will this accelerate downards?

Baby Boomers dying or forced into assisted living.

Once the homes go into probate, inherited, or foreclosed by reverse lenders, the selling pressure really accelerates. Retiree-heavy areas are already seeing this, since offsetting inflows have significantly decreased.

I guess have a shortage of skills by the …homebuilding CEO’s. How can they have miss-judged the market so much with their teams of economists, and advisors.

This shows another major market failure.

Homes are selling in hours/days in the Boston area I live in. And those homes are similar to mine that I bought 3 years ago – a split level ranch.

The only difference is, the prices these homes are selling for are notably higher that what they were selling for 3 years ago.

Stock prices are hitting new all time highs daily.

Liquidity is in 100% Full Throttle Ultra Dove Deluxe Mode. The Fed is drowning assets in liquidity.

timbers – Affordable suburban real estate seems to be selling fast but the luxury market is getting clobbered pretty much everywhere. Affordable homes are selling because lower income households can finally afford to buy.

Cheap Fed money wound up in luxury real estate earlier this decade which helped lower the unemployment rate. The sales volume in your area isn’t being driven by the Fed, but by a low unemployment rate. The sales decline at the high end of the market will ultimately lead to a higher unemployment rate. That is when your area will start to get hit.

Well this entire thread seems to be about a lot of fish stuck in a small pond.

I think now & forever its all been pretty much the same, buy lots of small homes near a college in a low cost area for that time ( they always exist at all times ), and buy 15 yr fixed, and say you do this at 25, then by 40 you can retire your done.

I think the majority of fish stay in the tank for a variety of reasons, but mainly cuz everybody else is doing same. Life is short, 15 years ain’t that long, say you buy 6+ houses when young, on contract ( no down ), at very low prices, and then sell or just take the income forever you can live anywhere on earth or do anything you wish.

When I reached 40 I bought a sailboat and sailed the world for 10 years, then at 50 I moved to SE Asia and never looked back, now in my 60’s even 10% of my social-security exceeds local spending average.

Long ago Emerson & Thoreau wrote much about this subject, and most men/women truly do take the wrong turn at most junctions.

One last comment when I was in early 20’s all my friends where spending their money on hotels & restaurants; now they’re all still working in their 60’s having nothing except their ‘house’ with max’d out LOC debt.

Buy lots of small houses at 25….? Yeah because at 25 we all have that kind of money sitting around…

Never have purchased a home for “asset” value…..if that came along it was a bonus. The three properties I have purchased I have always never placed more than 50% of the “profits” into the next purchase. We were always lucky enough to be able to find work (raised 7 children all in their mid to late 50’s today) raising the children and keeping a roof over their heads. There is too much talk of “asset value” and “future earnings” from homes today.

Also the environment is changing; several commenters talked about the changing needs, more contained living spaces; close to walking space living (which I am totally for); away from the long commutes to large homes that really isolate families and leave hardly no money for self education, travel, socializing etc.

Retired in 1994 from the greater Bay Area; moved to the Sierra foothills. My home is a modest one but large for me…..but, when my children and grandchildren over those years visited there was really no more room for anything!!

A home should be a home to raise a family. And, close to work. (I’ve done the commuting thing years ago).

Some of my grandchildren that have been lucky enough to attend good colleges (and exited sans huge education loans) live in SF, San Jose, Chicago and I suspect in the future other far-off places. The rents in SF are atrocious (born and raised in SF in the 1930’s); but the jobs available there for some are essential in some fields for example health care research etc….and other highly technical fields……

I don’t envy the young in this “market”….but times are a-changing. They will figure is out and maybe they will realize that a “home” is not always supposed to be a “rising dollar asset”….it’s to live in.

Great article Mr. Richter.

And of course renters are actually paying the real estate taxes through their rent.

Down where I live, the property tax for non-owner-occupied properties are 3X the equivalent homeowner rate, plus no caps on fast the appraised values can rise. So when people talk about “affordable housing”, I always ask, “for whom, homeowners or renters”.

Humans Basic needs food water, shelter, clothing, and sleep. When such needs lacks invasion happens. Law is created to keep stable ground and taxes are collected to provide basic needs as it is every humans right to be provided.

Taxes are ridiculous on property even on a primary residence. Scams of association fees are also ridiculous, if tax are low the association fees makes up it and banks charges much higher interest rate profit on top of fed’s interest charged to banks.

At least a primary residence under certain value should be taxed no more than a $1 to at least show that the land is leased and property of US. And interest rate should be much reasonable. Due to those high taxes the price of a house are sold in market of much more than its worth.

Either the rate and tax should be lowered or the minimum wage should match the cost of living.

But none will happen, it’s all a scam. Big guys looting people.