There are now many of them. Shoring up the balance sheet is the opposite of “shareholder friendly.” It’s “creditor friendly.”

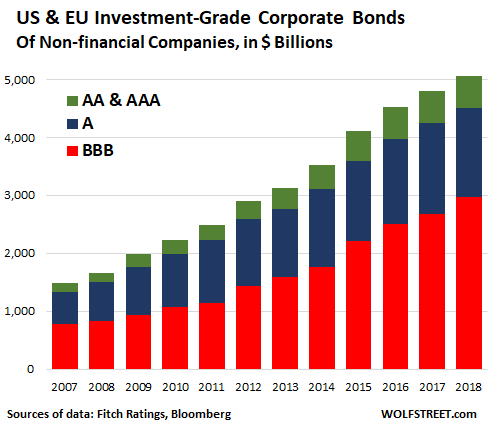

The amount of investment-grade corporate bonds outstanding by non-financial companies in the US and Europe – so excluding bonds issued by banks, insurance companies, and the like – has more than tripled (+204%) over the past ten years, from $1.66 trillion at the beginning of 2009 to $5.06 trillion by the end of 2018.

Split by rating, over the same period, according to data by Fitch:

- The amount of bonds in the lowest investment-grade category (BBB, red in the chart below) has ballooned by 262%, from $820 billion to $3.0 trillion.

- But the amount of higher- and highest-rated bonds (categories A, AA, and AAA, green and blue in the chart below) has increased “only” 147% – though that’s a huge increase too – from $842 billion to $2.1 trillion.

These are investment-grade bonds – the cream of the crop, so to speak. These amounts do not include other forms of corporate debt such as high-yield bonds (“junk” bonds), regular corporate loans, “leveraged loans,” loans by private equity firms, and other forms of debt.

But bonds in the BBB-category are teetering on the edge of “junk.” A rating of “BB+” is already in junk territory (here’s my fancy heat-sheet for the corporate credit rating scales by Moody’s, S&P, and Fitch).

In the next downturn, many bonds in the BBB-category will transition to junk, and many junk bonds but also some investment-grade bonds – if the past is any guide – will transition to default. Two-notch downgrades are not uncommon: one day you wake up, and your “BBB” investment-grade bond is a “BB+” junk bond.

So there has been a lot of handwringing about a future pileup of “fallen angels” as a historic portion of this ballooning mass of BBB-category bonds will be downgraded to junk.

A downgrade to junk makes borrowing more expensive for companies. And for companies that have to refinance debt that is coming due, this could add up. Companies are rated BBB and not A because they have a lot of debt, in relationship to their cash flow. So increasing the cost of this debt can be an issue. A downgrade to junk can also pose other problems for companies, so they generally try to avoid it.

But the strategies used to avoid a downgrade to junk can have a big bad impact on share prices, in the sense of reality coming home to roost.

To avoid a downgrade to junk, companies will try to shore up their balance sheet. This means curtailing or stopping share buybacks and slashing dividends.

This is a process GE went through. After blowing nearly $14 billion on share buybacks in the four years through 2017 to prop up its shares, GE stopped on a dime and transitioned to dismembering itself to pay down debts. The share buybacks stopped cold. Then it slashed its dividends to near-zero. And its shares have plunged.

GE now sports a credit rating of “BBB+” with negative outlook, three notches from junk, after getting hit by a round of two-notch downgrades late last year. Despite having already cut off some major limbs to reduce its debts, GE still has $97 billion in long-term debt. And GE is still trying hard to dodge further downgrades.

When a company tries to shore up its balance sheet by stopping share buybacks and slashing dividends, the result is not fun for shareholders. And even anticipating this process is not fun for shareholders. GE shares went from the $30 range in 2016 to about $9 currently, after having dipped to $7 late last year.

It’s much more fun for shareholders when the company blows billions on share buybacks to prop up its shares, and when it douses shareholders lovingly with dividends.

Ford Motor Company has $100 billion in long-term debt and is rated “BBB,” just two notches above junk. It is desperately trying to dodge those downgrades to junk. Its shares went from the $15 range in 2015 to the $9 range now. Share buybacks are off the table. Its dividend yield is an out-of-whack 6.5%. Bringing that dividend yield back into whack means one of two things: A dividend cut is coming or its shares are going to magically skyrocket.

General Motors has $73 billion in long-term debt and is rated “BBB.” Its shares are still hanging in there, in the middle of their trading range over the past five years. Fiat Chrysler Automobiles (FCA) is rated “BBB-“, one notch away from junk. Its shares have moved from the $23 range in early 2018 to the $15 range now. Kraft Heinz has $31 billion in long-term debt and is rated “BBB-” while its shares have plunged from the $90 range in 2017 to $32 range currently.

These companies have large capital requirements and must be able to refinance a lot of debt when it comes due, and they need to be able to do so without drama. They need the credit market to not worry about their balance sheet, and whether or not they will be able to refinance those debts that mature further in the future. Confidence is everything. Once that confidence begins to wobble, these over-indebted companies begin to wobble. And an investment-grade bond rating is a big factor in that market confidence.

Shoring up the balance sheet is the opposite of “shareholder friendly.” It’s “creditor friendly.” And trying to protect that BBB-rating, after years of debt-binge partying, can have a deleterious effect on share prices, even if the company succeeds in not getting downgraded to junk.

Companies buying back their own shares has “consistently been the largest source of US equity demand.” Without them, “demand for shares would fall dramatically.” Too painful to even imagine. Read… What Would Stocks Do in “a World Without Buybacks,” Goldman Asks

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

So is this the reason the Fed backed off raising

rates ? The inability to refinance corporate debt would have set off a chain reaction that

would have been hard to contain. .

Yes, there was a problem with that, late last year. The junk bond market started getting very cold. No new junk bonds were issued late in the year. Yields were spiking. Leveraged loans took a big dive. All heck was breaking loose in the credit market. I think this spooked the Fed. I pointed out some of the credit-market issues at the time. It spooked me too :-]

Well dont look now, because the statistics on the junk bonds have gotten worse during this distribution rally.

What a way to ‘run’ an economy.

A bit like ‘the tail wagging the dog’.

And a decade of commercial real estate selling at cap rates of 3 to 5%, bank financed, non-recourse.

Yes. The REITs appear to have been hiding quite a lot. There are two strip malls near me. The first closed down completely in 2008. The second has been empty since 2015 except for an anchor grocery store that owns its own property. There was plenty of traffic at both, but the owners would rather collect 0% of high rents than 100% of reasonable rents.

Both are surrounded by million+ dollar homes.

Eventually — maybe! — those properties will be foreclosed, and then rents could come down to the point where going concerns can afford to pay them.

A high unattainable rent keeps up the illusion of a high property valuation for the mall and the surrounding area.

I recently saw a video of a guy walking through a Rancho Mirage, CA upscale strip mall. The narrator was a local guy who hadn’t been there in a while. He was shocked at the desolation of a previously bustling mall. He finished the video at home, none to sure of the economy in upscale CA, and not to confident about the value of his home.

Those retail/residential buildings are popular here, low income housing built over high end shopping. Watts on top of Rodeo Drive…

So either the markets get easy money or

they cease to function. There doesn’t appear to be any middle ground. Capitalism is daring itself.

Hahaha – the joke will be over soon!

Makes sense when a system has evolved for a decade in an artificial environment created to stop a collapse.

And this is playing out with low unemployment and while car companies are raving about how much their average sale price has increased. It all seems so fragile… like one shock is gonna set off a chain reaction.

I feel like the unemployment numbers are tweaked to the sunniest side and might be eliding a lot of people while highlighting replacement of baby boomers who can now afford to retire after 2008’s debacle. Seattle is apparently a Mad Max nightmarescape of junkies and bums. Are they unemployed or are they no longer counted? And what must Portland, SF, and LA be like if rainy Seattle is “dead” per local media?

Large companies have many resources. Some of them have gigantic cash flows – this is true of GE and Ford. Ford even has a good earnings, about $1.40 a share. GE has sold off some businesses at a handsome price, and may sell off more. If worse comes to worse, companies in trouble can always sell the shares they bought back!

=> If worse comes to worse, companies in trouble can always sell the shares they bought back!

Unless there are no buyers.

Uh oh.

It will be a long way down. Best to prolong the misery.

As Wolf previously mentioned, “Now some folks in Congress from both parties, who are worried about corporate governance and the like, have targeted share buybacks in some of their speeches and have proposed some legislation.”

Is this new found attention really a ‘play’ on the situation this article and you just mentioned?

In a way.

Share buybacks are intrinsically destructive. But so are LBOs, and so are numerous other practices.

Share buybacks prevent LBOs by making the firm unpalatable to PE pirates. Banning buybacks will make them more palatable. You can’t win this way. If reforms are not sufficiently comprehensive they’re just going to exacerbate other problems while attempting limited fixes.

There are many examples. The distortions are many, and many are extreme.

If you are a large cap with positive cash flow from operations, you can sell stock. They might take a bit of a haircut, but if they really need the money to survive, they won’t care.

“Confidence is everything.”

It sure is. Without it, the bonds of trust dissolve and paper bonds become toilet paper. Which would be a better rating than “junk”.

Speaking of which. What’s with the ratings’ nomenclature? Why don’t the three credit-rating agencies agree on a 0%-100% scale? Would the ratings become too obvious for the hoi polloi?

Ratings are kind of like grades in school — but with a lot more gradation. There is no F. But there is a D. And a paper that is really really really good gets an AAA :-]

I think that internally the ratings companies use somewhat different evaluation methodologies, so it might actually be appropriate for them to use different ratings nomenclature. Fortunately, we have Wolf’s ratings rosetta stone!

The role of ratings companies has confused me ever since S&P acknowledged that their own ratings are ‘puffery’, and not appropriate for investment purposes (at least, by themselves). This is true, of course, but strange that so many trillions rely on ratings that the raters themselves consider meaningless.

https://www.wsj.com/articles/SB10001424127887324235304578439010216689372

Just watch the movie “The Big Short” to see just how reliable the big rating agencies are…

No worries. The Senate will rubber stamp the appointments of Stephen Moore and Herman Cain to the Fed Board and they will make sure the Fed turns the money spigots back on to fire hose volumes. Gotta make sure American Capitalism has all the free money it can pig out on

These two seats have been open for quite some time. Trumps previous nominees failed to pass the the Senate , because hearings were never officially scheduled.

Given the tax and alimony mess that Mr. Moore is in and the sexual allegations that have been made against Mr Cain, there is a good possibility that these two nominees will suffer the same fate as the previous two.

Hi Wolf,

“(here’s my fancy heat-sheet for the corporate credit rating scales by Moody’s, S&P, and Fitch).” Should that be heat-sheet or cheat-sheet?

Either way the link doesn’t seem to be working…

Thanks. Fixed.

The Fed will step in in some manner.

45 pushed an aspiring globalist central banker out of the Fed Chair for a private sector economist. When his pick threw in with continuity at the Fed 45 tried to throw him out as well. If QE is what he wants he could nominate Brainerd, so maybe QE is jawboning, while the Fed PUT gets rolled back.

Now do Tesla’s debt Wolf

If Tesla’s debt was priced based only its balance sheet, it would trade much lower and at higher yields. Tesla’s debt is supported by the concept it could sell stock to shore up its balance sheet . When the stock trades lower , watch out for the debt.

Yes, I think overhyped Tesla is an important canary in the coal mine.

How about NFLX?

Tesla has hard assets. What will be value of House of Cards/NFLX library if put to bid. Ask James Bond/MGM??

Aren’t these the same credit companies that gave an ‘AAA’ rating on subprime MBS tranches? Too good to be true?

But this is actually a good thing, no? Companies *should* prioritize debt holders above shareholders. In the line of claims against a company, equity has the last claim.

There is much more turmoil in the macro-economy if there’s a wave of defaults than if the stock market tanks (although both have bad effects). Frankly, this is what companies like GE should have been doing for the past decade. Maybe it might have survived if it did.

AAA AA A

Yeah like there’s a difference. It’s all throwing darts by 22-25 year old semi-alcoholic recent college grads.

Source: Was a 22-25 year old semi-alcoholic recent college grad who worked as a research analyst and knew from day 1 it was all bulls*t.

I interviewed with one of the 2 big bond rating outfits (Fitch is kinda a distant 3rd). All day interview. Didn’t even take me to lunch. By 2pm I was starving. Like I’d work for a company like that? Pleaze!! Got an offer but turned it down. Looking back on it, I wonder if I had taken it, would I have been involved in giving sweet A ratings to junk CDOs that nearly blew up the world in 2008? I could have been part of history. Oh well.

JSRG,

You could also be about 20 lbs less obese. Waiting until coming home from work to eat only one meal a day helps keep my weight down by about that much.

And it builds mental willpower- nothing like walking into the cafeteria, taking a deep whiff of all that wonderful food, and saying, nah, I’m not going to eat until later this evening

So, maybe not taking you to lunch was a test of your mental willpower and that company’s contribution to our national obesity crisis

Here is the fundamental flaw.

The day you allowed issuers to pay money to get ratings, you skewed the incentives for rating agencies. Even if they are good guys and dont want to play the rating game, the good guys wont get ANY business.

Wall street model (was part of Dalal Street, if you know it) has flaws but for every 20 dick-sucking Buy analyst, you just need 2 Sell analysts to balance the equation. Let clients pay for research – and let there be competition among a 30-40 firms (and not 3-4 agencies).

The flaw is very fundamental – any and all amount of cosmetic changes wont change the fundamentals.

“Shoring up the balance sheet is the opposite of “shareholder friendly.” It’s “creditor friendly.””

This is spot on. How did we get to this place? Sad.

When good economic news comes out, the stock market tanks in fear of rate hikes. Bad news magically becomes good news for stocks in hopes of cheaper debt. Everyone’s attention is on the FED because they centrally micromanage the most fundamental economic input and measure, the cost/price of money. And they have never failed to fail, until you realize that your bad news is their good news. They are succeeding.

If you planning to build a new factory and an inch or a foot is measured differently based on how those on high say an inch or foot is to be measured that day, it becomes a very difficult exercise.

A precious few have the FED rosetta stone. It is smoke and mirrors for everyone else.

The term “zombie” company refers to companies that generate sufficient cash to pay the interest on their debt , but not enough to pay down principle.

Because of the large number of companies , whose bonds are rated junk, it is inevitable that during the next downturn a multitude of companies will be zombified.

The fed will protect the banks.Distorted and disrupted markets spawn zombie companies. This corporate lip sticking a pig is the un-intended legacy of 2008. I took my money out of these pigs a long time ago. I kept my long held positions in utilities thinking they were immune to this scheme. I now have to over-come cognitive dissonance on those positions,it’s hard to do that when you have held them for decades. Robert Burns poem “TO A MOUSE ” sums it all up nicely. Backward I only see prospects dreary, forward I guess and fear.

I’m curious about GE, which I view as a zombie company. Yet what kills zombies is rising interest rates. Interest rates are forecast to go nowhere but down, which hints that GE will be able to re-finance throughout the next recession.

So the big question is at what point does the music stop for GE? How to the ratings agencies make that decision? Can GE create novel corporate structures to defer paying off debts indefinitely?

So the real problem with these bonds is when they come due. Not the interim. When they come due, the corporation or REIT has to repay the original investor in full.

Borrowing the money while everyone was optimistic and hopeful appears to have been the easy part. Repayment is going to be hell. This appears to many of us that it will start happening during a recession. And could lead us deep into something worse.

As previously discussed, the highly leveraged loans to heavily indebted companies will just never get repaid. $3 Trillion is a lot to write off. And that could actually be low because when the economy goes into recession, after all this pumping, the loss of revenues to many corporations will be significant enough to push them also over the edge. This has broad implications for the overall economy as once the defaults start, few will want to buy into something with falling revenues. Especially in those companies that have NO profits. Or profits derived from others whose business model was to pay Peter with the money borrowed from Paul who got the money from Mary who borrowed it from Debra who’s uncle had a direct line to the FED’s QE or a big pension fund.

I see why many feel the FED will have to reverse gears and go to QE Max buying everything. And that may not be enough to actually create any inflation, just barely enough to stop the world from ending. Again!

How long can this go on?

At what point is everything meaningless and irrelevant? And dollars nothing more than imaginary digits on some computer put there by some robot? What is Capitalism without real price discovery?

Our world is increasingly becoming Bizarroland.

The Fed will protect the economy overall. It will do whatever it takes. Someactions will be communicated, some maybe not.

2008/09 set this moral hazard in stone but the causes were initiated much earlier.

We will be going back and forth between fiscal and monetary stimulus until we can’t. All of this will lead to continued inflation that will manifest in all manner of ways but will grow further in asset inflation and in fits and starts with normal everyday costs.

And the move to raise minimum wage will spur price increases that will move quickly to erase whatever real gains the earners might have received initially.

There really is no other way out at this juncture. Nobody in power in their right mind would want to “lead” over the painful correction (how do you spell depression) that the economy has to undergo to regain normalcy. So the games will continue until they can’t.

Keep this in the back of your mind squarely but live your life.

Mike, Great post. Moral Hazard was indeed set in 08/09 and will only add that the die was being cast earlier. And Moral Hazard was/is often actually celebrated as a political “win”.

Fools who are consistent in their folly have a hard time continuing to evade reality. That’s where the 2 party system in the US comes in … by keeping everyone distracted and in blame mode.

Tyranny must appear as a protector, lest it is exposed.

So 60% of the investment grade bonds of U.S. and European non-financial companies are perched just above junk status. Lovely.

What about financial companies? Why are they excluded from scrutiny? Anyone have any idea about the numbers for banks and insurance companies?

Noteworthy to mention, this today from FCX CEO today:

Freeport-McMoran (FCX) is down more than 2.7% in Tuesday’s afternoon session as Chief Executive Richard Adkerson said the company is planning no dividend raises, acquisitions or debt buybacks over the next two years, according to Reuters.

I thought the whole rating issue lost credibility because they are influenced so much ny the Corporations. I’m thinking of 2008. That is to say, why believe them at all?

AND with International acquisitions of US companies on an expansive trend, does anyone think that is good news for US business/capitalism etc.?

https://www.bea.gov/system/files/fdi0718.png

No longer do we have market cycles but rather credit cycles. In order for the FED to save Main Street and bond investers it will be forced to monetize corporate debt. A lot of debt. They got away with it in 08 and will be interesting to see if they can pull of the same magic. IMO it would be fiscal suicide as bonds are no longer a tier one asset according to the BASIL rule makers.

And these are the good times! When the inevitable recession arrives it’s pretty obvious that both Ford and GM are going to have to declare bankruptcy. Both will reemerge but shareholders will be wiped out, again in the case of GM.

There is some misunderstanding about Ford not needing to be bailed out in 2007-08.

By either amazing luck or amazing foresight, the company did its absolutely last and final, do-or die, massive refinancing just months before the wheels came off the US (and then world) financial system.

For the first time in Ford’s history the business alone could not borrow the money. Everything was mortgaged: the business, the factories, the land under the factories and even the Ford logo (since reclaimed)

But even at that, there is not the faintest chance that Ford could have swung the loan less than a year later. The banks were worried about their own survival and wouldn’t lend to each other let alone.a struggling auto maker.

Although not having to declare bankruptcy, Ford did receive billions in

govt loans, claiming that it would be at a competitive disadvantage if the others got loans and it didn’t.

Today with debt exceeding market cap, it is a question why Ford is paying any dividend let alone a juicy 6 plus percent.

Although minority controlled by the Ford family, it is controlled by them and they have over a billion dollars worth of stock.

Spot on!