Market for houses freezes up. House & condo prices drop. High end hit the hardest.

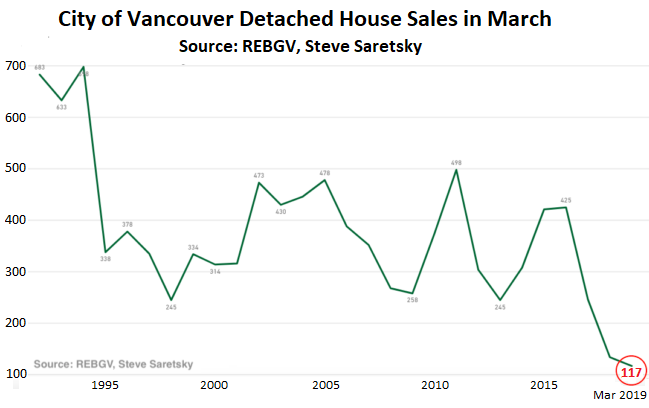

In the City of Vancouver, British Columbia, in March, sales of detached houses fell 14% from March 2018, to merely 117 houses, down 50% from March 2017 and down 74% from March 2016, to the lowest number of sales since 1985, as the market has frozen up. Buyers and sellers are too far apart, and both sides have lost interest in a meeting of the minds.

“It’s hard to imagine sales falling any further from here; what is more likely is that they continue to remain sluggish for a prolonged period of time but increase slightly as prices decline and buyers on the sidelines can be enticed back into the market with lower prices,” says Steve Saretsky, a Vancouver Realtor and author behind Vancity Condo Guide. His chart below shows detached house sales for every March going back to 1992:

Inventory for sale now stands at 12 months’ supply at the current rate of sales. This is still very high, but it’s down 51% from a year earlier, not because the market has improved but because it has essentially frozen up, and some sellers have pulled their unsold units and other sellers are not putting them on the market, hoping for better times.

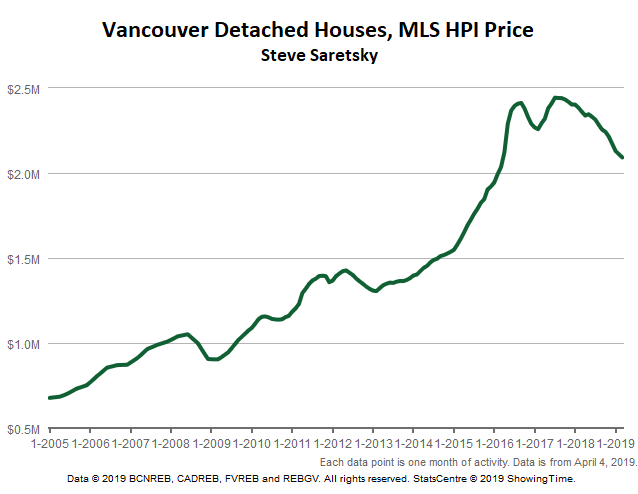

This high level of inventory is likely to put “downward pressure on home prices, particularly at the higher end where Chinese capital flows have hit the brakes,” Saretsky says in The Saretsky Report for March (download the PDF here).” This pushed the MLS Home Price Index down by 11.4% from March last year, “the steepest decline in a decade.”

But the price declines vary across the spectrum: Saretsky notes that house prices “at the higher end have fallen as much as 35% from peak valuations a few years ago,” while price declines are much more moderate at the lower end. “For example, an entry level detached house with a basement suite on the East Side of Vancouver has fallen much less, around 15-20%.” Which is still a steep price decline.

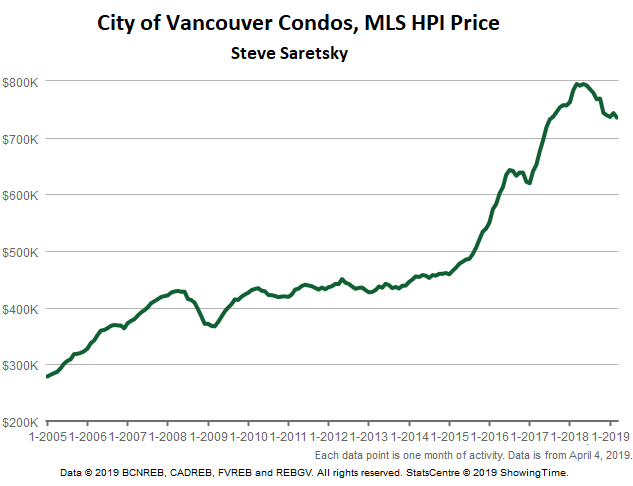

Sales of condos in the city of Vancouver in March have plunged 35% from March 2018, to just 328 units, down 45% from March 2017 and down 63% from March 2016, to hit the lowest level in 18 years.

At the same time, inventory of condos for sale jumped by 96% to 1,905 units. Months’ supply jumped from 1.8 months in March 2018 to 5.4 months now. Plunging sales and rising inventories has put pressure on prices.

The average price fell 12% year-over-year to C$810,934 and is down 25% from the crazy spike-top in January 2018. The average price per square foot fell 11.5% year-over-year, to C$961, “which is right in line with what we are seeing from a feet-on-the-ground perspective,” Saretsky says. The median price fell 9% to C$688,888. The MLS Home Price Index, depicted in the chart below, fell 7.5% in March from a year earlier:

Condos face enormous headwinds going forward, in form of a flood of new supply coming on the market: with impeccable timing, over 40,000 condos are under construction in Greater Vancouver.

Vancouver has joined some of the other major cities around the world with housing bubbles whose duration and magnitude have amazed the world and that were scheduled to inflate further for all times to come – because, you know, you can’t lose money in real estate – but that are now deflating with panache. Among them are Sydney and Melbourne in Australia.

But their housing bubbles were not pricked by the central bank — on the contrary. Read... Update on the Spreading Housing Bust in Australia, and Why it’s Happening

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Big question is the timing and severity of the knock-on effects.

Real estate agents not getting paid, lawyers not getting paid, property transfer tax not getting paid, furniture stores not getting paid, spec builders not getting paid, architects not getting paid, municipal governments not getting paid, etc. … where will the money in the economy come from, foreign money has dried up, and bank’s aren’t lending much into existence.

Permanent QE/ZIRP and government purchase of stocks is the recipe of the day – just like Japan.

A broken, zombie system that needs a complete rethink – globally – but as long as it benefits the already-wealthy so well, as long as politicians are wooed with big-money offers in the world of finance and as along as central banks continue to be staffed by people looking after the interests of their speculator pals, expect no change.

Hence the yellow vests…

exactly….the doomsters are not taking advantage via what the zombie system is giving out, what a ride the market is since the double bottom in December…..and I posted here saying to buy deep…..

2 90% days was the clue……keep running, trailing stops are your friend….now 25% price drops on homes coming by 2021 in a town near you

This has happened before and opened the door for the wage owner to afford a home.

> where will the money in the economy come from

Debt Wazoo, of course!

BitCoin

Spit out coffee funny

I know it was a joke but it could be true. Bitcoin price has been gathering some momentum as of late. It’s part of the money launderers’ collection of instruments.

Like many global cities, Vancouver is a destination for Chinese wealth fleeing the corruption crackdown.

This city has been popular with corrupt Chinese wealth for a couple decades but the inflow really picked up after 2012.

The arrest of Huawei CFO threw some cold water on that, any news on her status in relation to the “Epic” trade deal

It’s been well-documented now that drug dealers have been laundering money big time through Van. real estate and casinos out there. Both have finally been exposed and I’ve my popcorn ready.

Vancouver has been popular with Chinese who have money more than a couple decades. In the 80’s and 90’s anyone who could left Hong Kong and ended up there. One of the more vocal groups I’ve heard against the latest influx were the older (non-communist) expats.

Like in Australia at its peak, (maybe desperate or naive) first time buyers will be eased into the hot seat just as the roller coaster reaches the summit

https://stevesaretsky.com/canadian-government-vows-to-take-equity-position-in-homes-purchased-by-first-time-buyers/

either as a bit of election window dressing… or because a local crowd is needed to do some shrieking as gravity starts talking .

Bankers,

Although the program you link to above was ridiculed as not having much impact on actual sales because of the stipulations involved, I would like to point out that it is a START, and in the future it could be ramped up to a direct “QE” for real estate.

I know that sounds paranoid but it looks like the path.

(Thanks so much for the link!)

Yes, that is a route that I see as possible also. You would have an economic downturn as the housing bust went ahead, a lot of unhappy owners going into negative equity, a lot of recently finished housing which a lot of first time buyers could not afford, or would not try to afford without some kind of guarantee like the above. Though it aims for the lower portion of the market I think that the top half is already bought out and flippers would not get much sympathy, nor foreign investors and as far as anyone is concerned they have bought to hold, often outright in cash, so tough. That would mean just keeping the market of new property afloat, and that would support both the economy and the price of other property. Well I’m using my imagination there, but I don’t think it is paranoid either to imagine something like that going on, it would be a very logical way for a government to settle the market and smooth out a bust – if there is one thing governments are known for it is intervention to prove their worth as equalisers (or to cover their mistakes). Time will tell I suppose, I would not imagine prices going up further for a long while, just maybe being levelled off somewhere lower, but who knows really.

The only place it can come from, sellers with large multimillion dollar homes in the trendy places of Vancouver, and West Vancouver who want to downsize.

Selling pressure will reduce the volume of money, not increase it.

“severity of knock-on effects”.

The ‘dark’ elephant in the room being –

Mortgage Backed Securities. MBS derivatives.

Specifically, Real Estate Investment Trusts. REIT’s.

I was living in Sonoma County, California when the 1990s housing bubble popped.

One family I remember in particular: He was in the building business (framer, I think), and was making tons of money during the boom. So, he bought a house.

When the bust came, they were having trouble paying the water bill, and had to dump the house, move back to LA, etc.

I always thought of this as the best real-world example of positive feed-back I have ever seen: The guys who were making a bunch of money building expensive houses were using that money to buy expensive houses, which made the houses even more expensive.

Of course, the wheel spins pretty fast when it is going the other way. . .

Construction crews are told to finish asap… Monday To Saturday work weeks is now mandatory by employers in Vancouver for Condo Buildings, although most are pre-sold before even going up for built so housing collapse isn’t affecting the already in construction ones. Would be interesting to see New Building Permits going forward, I wouldn’t be surprised if it literally grinds to a halt by Q3. You are seeing a lot of For Lease signs in Commercial Retail Stores as well, Commercial is doing even worst then Residential in my opinion.

Vancouver is in the lead for biggest drop from Peak, and will likely keep the crown… Sydney might catch up due to OI Mortgages, but Vancouver seems to be way ahead!

They are rushing to finish building homes in Toronto too.

I think they are trying to make sure the buyers can close before banks start saying no to all of these broke speculators. It’s a very expensive process to sue buyers for the outstanding balance. Demanding the buyer to pay the balance outstanding on the home plus legal fees won’t help the developer get their money from the buyer if the buyer never had enough money to get financing on the home the developer is suing them for.

Hopefully, most of the lawsuits will be against rich buyers that refused to pay because they see the home price is less than what they paid for. I doubt that’s the case, many of the 2016 and 2017 speculators were local or domestic buyers hoping to flip a home for a profit without the government knowing so they wouldn’t have to pay taxes on the flip.

Your correct in your comment on presales

On a further note many of these presales in Vancouver were being flipped..with no intention of every completing.

Many presale flippers in Vancouver have as many 6 presale contracts that they have been trying to flip. These presale contracts have been avoiding a number of taxes, including home purchase tax and capital gain tax.

The question is … how many will complete their sales agreements…I’m guessing NONE

“Would be interesting to see New Building Permits going forward, I wouldn’t be surprised if it literally grinds to a halt by Q3”.

There will be no stopping the new building permits, because the corrupt parasites that have infested your council and town hall offices, live off the payback crumbs that the developers, financially enhanced through a corrupt banking system, throw at them.

Existing citizens, natives and taxpayers?. F**k them, their only purpose on this planet is to pay for this mass theft (taxes?).

Our little market town on outskirts of London UK is scheduled to “welcome” a 50% increase in population over the next 10 years. When you ask our “elected” MPs, Ed Davey and Zac Goldsmith, ermm, how comes, nobody asked for this or voted for this, the answer is simple; a brick wall.

Down to your pen, you noughty plebs!!. Pay the pizzo (erm, taxes), or you will meet an accident!

Vancouver volume is in a trading range of 250 to 480/ month

since 1998. Vancouver market is small and very volatile.

The current volume at 117 is at nadir.

Volume will jump back into the trading range, because prices

will fall.

Vancouver and SF will be infected by China malaise.

At this point the Shanghai stock exchange is in the grips of the bears.

China economy is not in recession yet, but it might be soon.

A big correction in the global market will force owners to dump.

If the bear market will be deep and long, pushing the US into a metamorphosis,

==> bankers will dump RE.

The RE market is a pendulum that swing back and forth.

The invisible hands of the RE market strong hands will push it to the

opposite direction, from over extended high valuations to bargains, in order to acquire properties from the weak hands at much lower prices.

Vertical up, vertical down.

the correction needs UE to really ramp up before it happens, think 2006, everyone was still giddy….I sold my home seeing the bubble…..2021 could see 25% home price depreciation by then….

make your money on the blow off top coming in equities……all the doomsters are really bad at making money and timing doom

“all the doomsters are really bad at making money and timing doom”

LOL so true! I nominate for Comment of the Decade.

Well I was using the old method of an RE crash, like from 1991 until 2000.

I bought a house in 1991 (yeah, I fell for the hype, not building more land, prices never go down, get it now, interests will NEVER be this low again @9% mind you, bla bla bla) and was upside down until 2000.

That being said this time the market was NEVER allowed to find a floor IMHO because of the banker bailouts and behind the scene hedge fund deals of whole tracks of homes. Plus I knew some one personally that lived mortgage free for 48 months and the bank paid their RE taxes the whole time………this is insanity AND not a “market”

I failed to see that the banks/government were going to pull out all the stops and collude to make sure RE stayed un-affordable.

“all the doomsters are really bad at making money and timing doom”

The movie “The Big Short” comes to mind. Even if they had all the proof of impending doom before their very own eyes, the shorts still had to endure a period of irrational “normalcy”. And that period can be excruciatingly long. Timing doom is like predicting which snowflake will trigger the avalanche.

You could do a few graphs on the same subject for Australia and you would see a similar pattern (unfortunately).

Here you go:

https://wolfstreet.com/2019/04/02/update-on-the-spreading-housing-bust-in-australia-and-why-its-happening/

Wolf,

What’s your take on this:

I removed the link to the NYT. Too many people clicked on it. The NYT doesn’t pay me to promote their stuff. They don’t even link to my site. I don’t comment on economics stuff published by the NYT. They’re goofballs in their business department over there.

The New Time was once a decent paper…hasn’t been for a long time. Wolf is very kind to only refer to them “goofballs”.

Didn’t know NYT was off limits. Won’t link to them again.

California Bob,

The NYT is not “off limits.” It’s just the way you did this: a one-liner and a link to an unrelated article, asking me to comment on that article that then hundreds of people click on… I generally don’t allow those links.

If you write a couple of paragraphs about something and the NYT is the source, go ahead and link it, no problem.

Good article and comments. A non-fiction horror story and people are wondering if there is a hidden twist in the ending? I don’t think there is, but you never know…….

I saw an interview of Carol James, (BC Finance Minister). This was past Friday evening. Her response to these RE stats is that everything is unfolding as planned and hoped for. Just so readers know where the Govt is coming from.

I look for an accelerating decline, and the reason is this. Would you want to be a buyer today, when the price might/could/will be lower tomorrow? People will start to wait for the bottom, and while I do feel some sympathy for some of the purchasers from a few years back, it is only because they are fellow humans and my parents raised us to not take pleasure in other’s misfortune, even if it was self inflicted.

An add on comment is how this boom has affected my home area. I live 120 direct air miles west from Vancouver on the east coast of Vancouver Island (Sayward). It requires a 2 hour ferry ‘experience’, another form of financial rape courtesy of past Govt interference, and an additional 3 hour drive. The bulge in RE development stops 50 miles east of us, (Campbell River), and that development frenzy is still non-stop. Some rural locals have bought up cheap land/properties around here a few years back, listed insane price askings, and there they sit; for sale at 50% higher than sanity. Due to property price refugees arriving here, an increase in retiree buyers, and a booming logging industry, there are NO rentals available (not one) and almost no houses for sale….maybe 2? People do leave here regularly, in fact we make bets about when? An older spouse often develops a health issue and the partner decides the 1 hour drive to town is too much. Or, usually the female half, decides there are not enough amenities (shopping). If people get past 5 years they usually remain. It takes just a few visits to see how the towns down Island have been ruined by development, and they have nowhere else to run. An aquaintance who rents has been given 6 months notice to move as the property owners have decided to finally move in. They are from Alberta. The renter has already started his search and is networking for leads. That is a tight market, for sure.

“Or, usually the female half, decides there are not enough amenities (shopping).”

So you’re saying if I move there, my wife would have nowhere to go spend money?

Note To Self: look into buying property where Paulo lives

Second Note to self: Figure out a way to cut off access to Amazon once we arrive

Betting on house prices is never an advisable idea unless you can reasonably foresee future growth in employment driven demand, population growth or safe haven status.

Toronto has all 3 while Vancouver only the latter. Notwithstanding I would expect Vancouver housing values to be 20% higher in any given 5 year period at the least so buying for investment now if you’re rewarded with some income is not a bad move.

Better change your name to “Your Real Estate Agent”. Vancouver has at least another 50 percent to fall unless the Chinese come back into the market. But the rule etched in stone is the Chinese never buy into falling markets of any type they only buy into markets that are skyrocketing. Looks like a long way down for Vancouver real estate.

Paulo –

Same thing occurring here. South of you among the many small islands of the Gulf. An influx of baby boomers that sell up and move to the west coast for the easy climate.

Arriving with a big bag of cash, buying a home, car, new furnishings, and then signing a petition against any further development! Case in point, a first nations tribe is being sued for clear cutting a large block of land on Saturna Island! Strange times.

Thank you for the perspective from your neck of the woods. I have to conclude that the collusion of the central banks of the world after the 2008/09 fiasco has unleashed a speculative mentality not seen since the 1920’s. I say collusion, because here we are, 10 years later, interest rates are still low and we are even talking about more QE….even though the economy is supposedly so great!!!! So great in fact, that it cannot even pay the same interest rate it paid during the 1930’s. Words/deeds simply don’t line up with reality. I think of the old saying “from sandals back to sandals in 3 generations”. Well, it has been 3 generations since the great depression and I am personally preparing for version 2.0 – since things don’t go to hell in a straight line (per Wolf’s earlier article) it sure seems we are on a slow but consistent march toward that moment of truth which has to be near. I remember Hemingway, when asked how he went bankrupt….he said….” at first gradually, then suddenly”. I truly hope I am wrong. What crazy ass times!!!

Sitting on land you don’t use is no financial picnic. Paying real estate taxes is a burden, and then you have the opportunity cost of having no capital when real investment bargains show up after the next recession.

I have a feeling the local land owners will be dropping prices. If prices are dropping hard in Vancouver, they are likely dropping in the remote areas as well.

I have read most of Wolfs posts for a year. My econo-meter needle was pointing slightly toward inflation a year ago. The needle is now on deflation. Sitting on a depreciating asset does not negate demand . Waiting might be a fools errand. The Invisible Hand of the market is dynamic not static. The doctor says grab what you can and run.

Dr Doom

My sentiments entirely.

Cash in a ‘healthy’ Bank is the best bet if you can’t buy Gold.

As usual, 90% of the peeps always gets it backwards and upside-down.

There are no “healthy” Banks, since all are based on a fractional reserve system and global QE has been running for the better part of a decade and possibly with more coming. lol.

90% still don’t comprehend there are many more things that can go wrong with holding cash than holding RE and/or other assets.

That’s why 90% of the peeps gets ripped-off by inflationary economics,, and then even in an unlikely deflationary correction scenario, that wad of cash is going to be relatively low in value compared to RE.

Just imagine this. In a depression or an extreme deflationary event, do you think those holding RE is going to be willing to exchange their tangible assets for your wad of paper money? lol.

Even if they are willing to exchange their RE holdings with your cash, it will be a VERY thick wad of cash before they will be willing to transact, and that in itself becomes inflationary, right?

No one in a serious depression will sell their land that can potentially become their food farm for any amount of cash.

So in “good” (inflationary) or low IR periods, saving cash is a loser, and then in bad (deflationary) times, it is still a loser.

Holding fiat money (i.e. cash) is therefore, the nearest thing to a Lose-Lose situation for the vast majority; unless you happen to be a Bankster or Politician who get can your hands on those freshly-printed notes and spend them first before the rest of the peeps.

Don’t listen to all the Dr. Dooms’, they are all doomsters who can’t build wealth in up or down cycles. Just look at their performance in any asset class over the last 10 years or more.

If you take the advice of such Dr. Doom, you will be the one to be doomed. Such statements as “The Invisible Hand of the market is dynamic not static” is stating the stupidly obvious and not saying anything useful.

He might as well be saying “The hands on my wall clock is dynamic not static”. lol.

And then “The doctor says grab what you can and run”.?? Really? Run where? To Timbuctoo? lol.

Your best chances of success during bad economic times, is to stay with what you are familiar with, hold onto your assets, keep your (financial) army near you as well as your wits about you.

Not abandon everything and simply just run for the hills, where you become a stranger in a strange land and will most likely be robbed, or skewered financially or otherwise.

i mostly agree, except for the part about people not selling their undeveloped land “that can potentially become their food farm.”

most people have no clue how difficult growing their own food is in the real world. some (most?) of them will eventually come up against some sort of cash shortage/liquidity issue and have to sell. good potentially productive family farmland will be for sale on the cheap, and the usual suspects, those with first access to the printed money, will be the ultimate beneficiaries.

“Control oil and you control nations; control food and you control the people.”

This is quite possibly the worst advice ever.

@nicko

It depends on circumstance/scenario so I think neither are nescessarily wrong. Twice I have had to abandon a home and country, once because of war, the other because of unrelenting open menace from a new bureaucracy. In both we were well connected, in very familiar society. So just to say to Kevin that there are also good reasons to cash out of a market, to hold cash ( or foreign currency or gold etc.), because of the fexibility it offers. Nothing wrong with keeping some real estate if you think it will be useful, but not all eggs in one basket – buy some RE abroad, invest in another passport, get to know another country if you are able, etc. etc. When shtf agility, to have various options, is essential. Pitched battles are for when there is a possibility of winning, or out of desperation, but most people leave when they see that the only other outcome is to end up captive or worse.

Everyone knows their own circumstance better so planning is a personal choice at the end of the day .

I think Vancouver homeowners saw price gains accumulate so fast through 2016, the gains don’t seem real, like in Vegas. People are quick to put their easy gains at risk, like in Vegas. People will likely wind up playing too long and losing it, like in Vegas.

If you think $300,000 to $500,000 is a good gain for a quick condo investment, you should leave the table while you can.

My advice to sellers: sell while you can.

My advice to renter: wait it out.

Bobber nails it, along with everyone today.

Defaltion, inflation, currency debasement, QE, negative interest rates; pick your poison. But think about this little gem. Stephen Moore and Herman Cain have been nominated to the Fed Board. If that doesn’t terrify you, nothing will.

Oh well. Steady as she goes, swabbies. The captain is driving the ship just fine!!

Meanwhile, I’m looking to escape climate change in the Southeast by fleeing to Nova Scotia in 3-7 years. Hopefully, the Boomer demographic bomb in rural Canada opens up some oceanfront acreage.

You’ve got the right idea, here — only go a bit further North . . . Newfoundland might be the best place in North America to prepare for climate change (more accessible than the islands on the West Coast, larger urban centres, fundamentally cool climate moderated by the ocean, cheap real estate). Large enough to produce a lot of what it needs, but still an island when it comes to some of the real effects of AGW.

When Canada’s housing market finally has its long-awaited downturn, I hope to pick up two properties: acreage in the Yukon and a home in Nfld. My kids can decide which strategy they prefer.

And one of the most beautiful, genuine places in North America…

Home prices in Newfoundland likely bottomed out just a few weeks ago. My guess is you’ll never see lower prices there than today.

Maybe . . . I will say this, that every mistake I’ve made in investing has been from buying too soon.

Hey Paulo,

Just thought i would point out Herman Cain past as a federal reserve board member ..Cain was chairman of the Federal Reserve Bank of Kansas City Omaha Branch from 1989 to 1991. He was deputy chairman, from 1992 to 1994, and then chairman until 1996, of the Federal Reserve Bank of Kansas City. So he has already been there so during a Clinton/Bush Time period. This you can see on the federal reserve site its self….

His position there had zero to do with monetary policy. Just like GE’s CEO Inmelt when he was on the board of the New York Fed during the bailouts, had zero to do with monetary policy, though he did decide on the bailouts, including GE’s bailout. All 12 privately owned Federal Reserve banks have boards whose members are executives of corporations and banks in their districts.

maybe his 9/9/9 plan could expand to include interest rates?

The US is one of few western nations without a Central independent bank. (Cannot think of one)

Even the US dollar is printed by a private comp. (US fed. reserve note).

The biggest surprise to me were the actions of the US Treasury and the Fed bailing out auto comp. insurance comp. and investment banks without Congress approval.

The next surprise to me was the Fed taking junk mortgages , junk notes as security against these bail outs.

Central Banks cannot lend money to Banks unless the loan is secured by a Fed. Bond..

The next surprise was the Fed backing the corporate bond market for at least 5 yrs.

The US needs a legitimate Central Bank.. non partizan.

Take your pick. As part of QE:

The Bank of Japan is still buying stocks (equity ETFs), corporate bonds, Japanese REITs, some other stuff, in addition to Japanese government securities.

The ECB bought corporate bonds, covered bonds, some other stuff plus sovereign bonds of the member states.

The Fed bough Treasury securities and US government guaranteed MBS.

Don’t like people from out of province, country or even your own province investing,don’t like investment from pipelines (gas or oil), Like laundered money from drugs and prostitution. What could be the problem?

Nailed it. The average BCer loves paying carbon taxes too. Amazing people live here but the wine is great.

Vancouver will be just fine. Oil is up, loonie is down. Investment and immigration will continue.

This is how it works without the Chinese in the Vancouver market. The average wage in Vancouver is $39,000 a year. A family would earn $78,000 a year. That means a mortgage at the big 5 banks would be 3 times $78,000 or $234,000. The second tier lenders with much higher mortgage rates would lend out 4 times their annual income. A one bedroom condo starts around $600,000 in Vancouver. Now we can see how far prices need to fall just to put a family into a one bedroom condo of around 500 square feet.

There was no easy way out of the bubble. The whole point is not to get there in the first place. Some of these places opened their arms up to illicit funds. This is what you get. Hurts lots of innocent people in the process. For them I’m sorry.

Chinesse money especially cash in leather suitcases has been the real reason for the stratospherical increase in prices in the last few years here in vancouver.

I remeber we went to an open house near south surrey and one chinese man caught my eye. He was carrying a leather briefcase . I caught a glimpse when he opened it to take out some paperwork and could not believe the amount of 100 dollar bills all stacked up in band new wads. Looked like he had well over million in there.

I walked away disgusted knowing that I had no chance if a chinese was present in the bid for a house in vancouver.

I decided to move despite gaining all the health qualifications to work in vancouver. Infact this talent drive would have been this citys downfall if the goverment had stood back and done nothing . These guys have way oo much money. I looked at chinas GDP and its in trillions.

I don’t see the so called collapse anywhere… just outside Metro Toronto… Pickering… friends townhouse sold in 48 hours for full listing… people are still lining up to get buried in debt… its all good then right…

There is no “collapse” in prices. In Vancouver, there is a collapse in sales volume. And sales volume is down sharply in Toronto as well. In the GTA, prices have dropped from the peak in early 2017. In March, the average price was down 14% from March 2017. So the party is over. But if you’re looking for a “collapse” in prices, you’ll be disappointed. It’s just a downtrend, and the end of a bubble.

Wolf – Any chance you can do a deep-dive into housing markets of Toronto and Barcelona? You seem to always find the right set of macro data. All the obvious signs point to a slow-down but they are still going gang-busters. Now we hear Chinese money is shifting from Vancouver to Toronto so a slow-down is not a given even in a rising rate environment – which we don’t really have much of.

Barcelona is not in my bailiwick. But Toronto is, and I cover it occasionally.

Ennis,

Wolf has a new article that covers Toronto (among other Canadian cities):

https://wolfstreet.com/2019/04/12/the-most-splendid-housing-bubbles-in-canada-deflate-march-update/