And where do Chinese consumers fit in?

Americans are infamous for their eagerness to spend money they don’t have. A whole industry has grown up around making that happen, from payday lenders to the government that guarantees or insures a large portion of the mortgages so that lenders and investors don’t have to carry the risk. Consumer debt is turned into asset-backed securities, from government-guaranteed mortgage-backed securities to subprime-auto-loan-backed securities whose top tranches carry an AA-rating or even a AAA-rating.

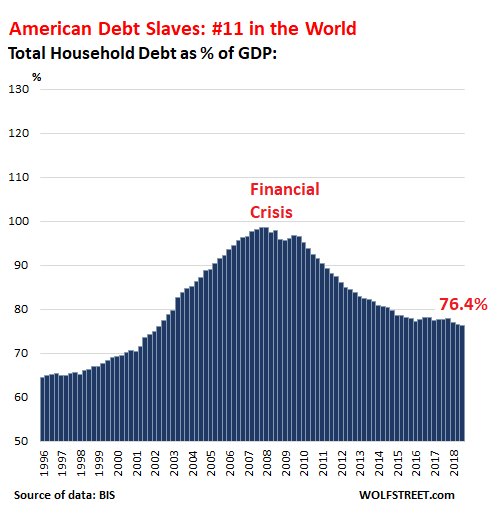

It all worked out. But then came the moment when Americans deleveraged, mostly by defaulting on their debts, particularly their mortgage debts, which triggered the US Financial Crisis and then the Global Financial Crisis. The world should have learned a lesson, but no. Who has learned a lesson? American consumers whose household debt in relationship to US GDP has continued to decline.

US household debt inched down to 76.4% of GDP in the third quarter 2018, according to the newest batch of global data from the Bank for International Settlements. This was the lowest level since 2002. It put Americans in the inexplicably wimpy, and for the finance sector, insufferable 11th place:

Even at the peak just before the Financial Crisis, American household debt never quite reached 100% of GDP. This is important as we move on to the winners on this list.

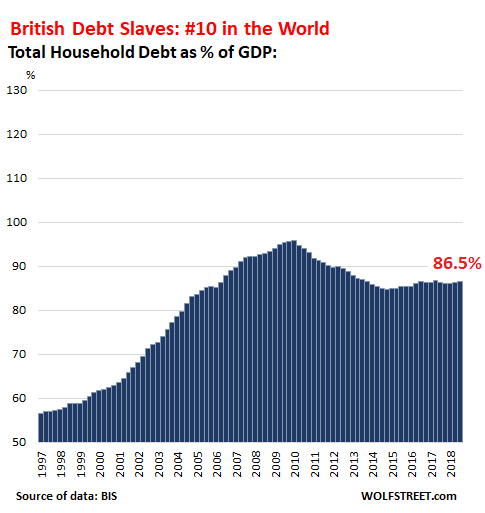

UK households also deleveraged after the Financial Crisis, with the UK banking system kept upright only by massive bailouts and the nationalization of some banks. But recently, household debt as percent of GDP has been ticking up, reaching 86.5%, which put the UK into 10th place:

This ratio is a function of two factors: Household debt measured in local currency and the size of the economy measured by nominal local-currency GDP. This ratio cancels out inflation. When household debt grows more slowly than nominal GDP, the ratio declines. When household debt grows faster than GDP, the ratio increases, and consumers are becoming an ever-riskier part of the financial system.

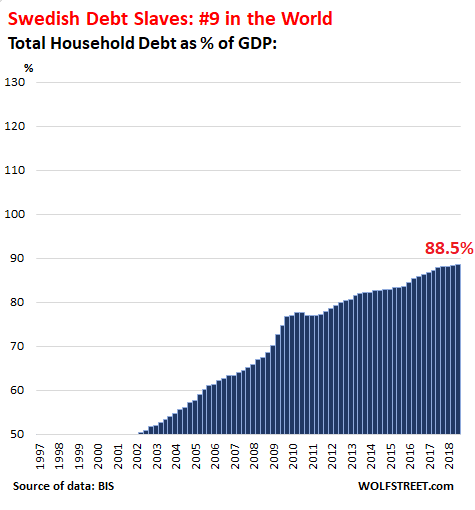

Then there is Sweden. Swedish households used to be notoriously debt-averse, like German households, and their household-debt-to-GDP ratio remained below 50% until 2001. But then someone figured out how to fix that, and suddenly, Swedes went on a phenomenal borrowing binge, and the household-debt-to-GDP ratio nearly doubled over those years to 88.5%, earning them the 9th place in the debt-slave competition:

On this list of winners, the charts are on the same scale, and that’s why there is so much white space above American, British, and Swedish consumers. Consumers that did not do their job in the early part of this century and did not borrow enough fell off the chart entirely, which is a fate that afflicted the Swedes until 2002.

Germans, with a household-debt-to-GDP ratio of merely 52.7%, still, after all these years, would barely register on the bottom of this chart. And Austrians with a ratio of 48.7% wouldn’t even be on the chart. On the other hand, the white space in the charts gets filled in by the winners on this list.

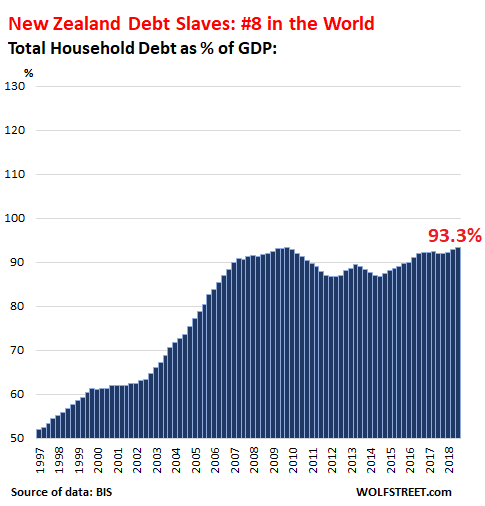

New Zealand, with a household-debt-to-GDP ratio of 93.3% and in eighth place, has been helped along by a property bubble that has been inflating mortgage debts:

Economists love debt slaves.

Household borrowing converts mostly into household spending, which is the biggest contributor to GDP. So economists adore growing household debt because it means growing GDP, and the economic system moves heaven and earth to get consumers to borrow more so that they buy more and add to GDP. And these households become enslaved to their debts and their financiers.

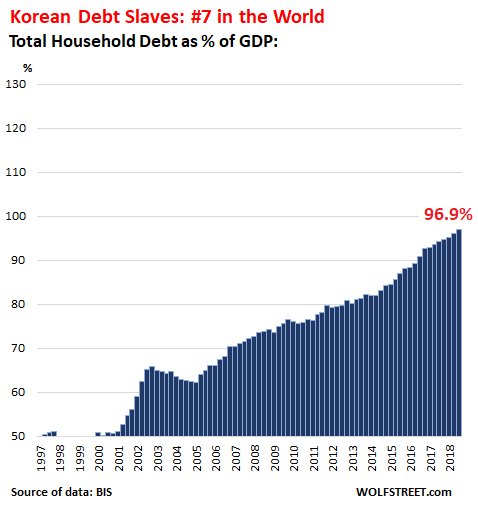

Korean households have made amazing progress becoming debt slaves, now closing in on the glorious 100% line, with household-debt-to-GDP at 96.9%. At the current pace, a couple more years, and they’ll have arrived!

When household borrowing outruns GDP growth for long enough and reaches certain levels, things can get iffy, as US household debt has shown with its starring role in the Financial Crisis though it never even exceeded 100% of GDP. So below are all the countries whose household-debt-to-GDP ratio now exceeds 100%.

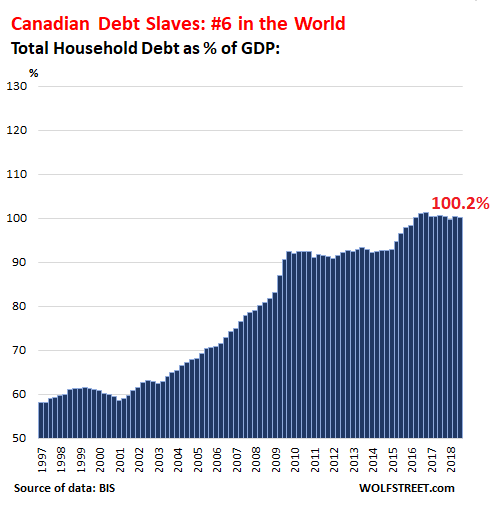

Canadian households have long been making headlines with their top-notch borrowing binge to support their top-notch housing bubble. By other debt measures, such as debt-to-disposable income, Canadian and Australian households have been battling over first place for years. In the debt-to-GDP measure, Canadian households are in a still respectable 6th place: This debt will pose some issues as the majestic housing bubbles in top metros are now deflating:

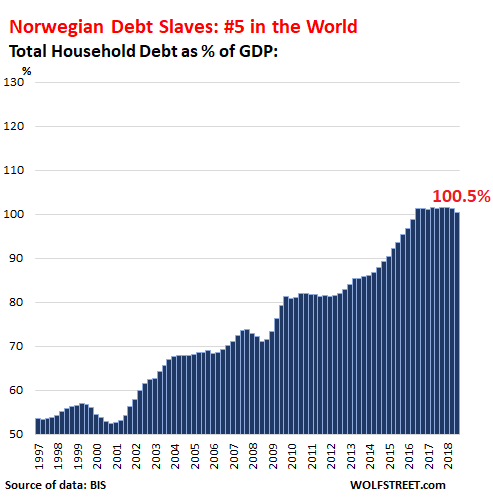

Norwegian households have bravely taken their household-debt-to-GDP ratio from 81% in 2012 to 101% in 2016. But this has since hit a ceiling as even regulators began to fret about the steep ascent, and a down-tick has been observed in the third quarter:

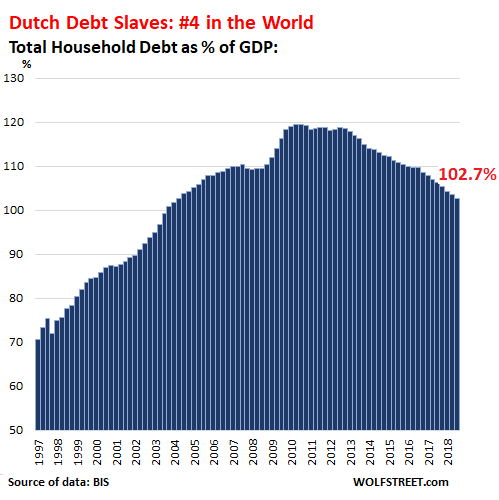

Households in the Netherlands were track to be undisputed king of the hill, with a debt-to-GDP ratio nearing 120%, in part because GDP plunged during the Financial Crisis, which caused the spike in the debt-to-GDP ratio and the collapse of some banks. During the subsequent euro debt crisis, GDP declined again. But since then, the economy has grown, and households have curtailed their borrowing, edging away from the brink, and in the process getting demoted to 4th place:

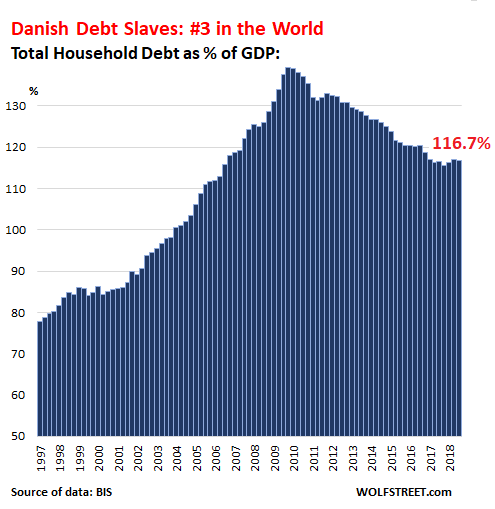

Households in Denmark exploded their debt-to-GDP ratio from an already high 90% in 2003 to nearly 140% during the euro debt crisis as the country went through a blistering recession. GDP still hasn’t recovered to the level before the debt crisis, as households are maxed out and have been whittling down their debts, but at 116.7% of GDP, the household-debt-to-GDP ratio lands them on 3rd place on the list of the biggest debt slaves in the world:

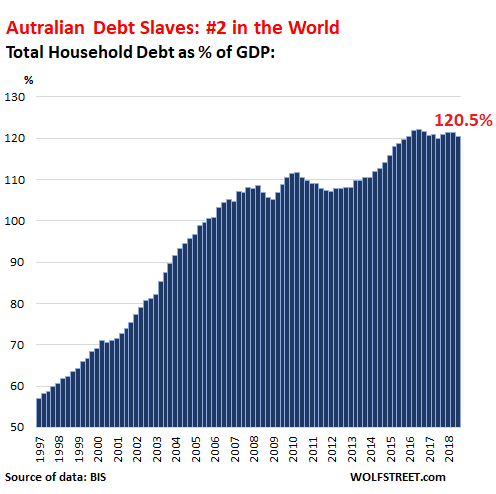

Australian households have been caught up in one of the biggest housing bubbles in the world, financed by debt. The household-debt-to-GDP ratio more than doubled between 1997 and 2016. Now that the housing bubble is deflating at an astounding pace, the debt ratio has begun to tick down, but remains in second place:

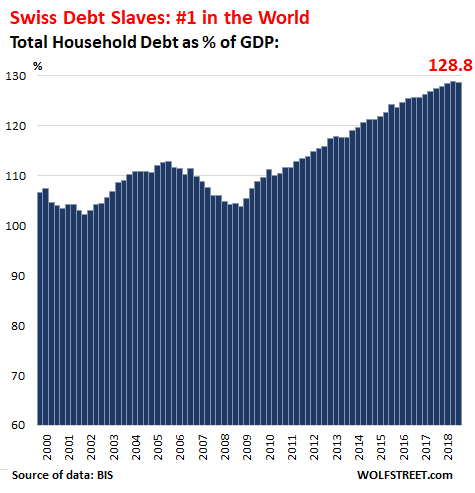

And the #1 debt slaves in the world: Swiss households. This is one of the reasons interest-rate repression remains the rule in Switzerland. The Swiss National Bank has imposed its negative interest rate policy on the country for years, and there have been stories of mortgages with 0% and even negative interest rates. There is simply too much household debt, and no one wants to see it blow up. Hence the negative interest rate policy. But this policy encourages more household borrowing, and the cycle will continue until it can’t:

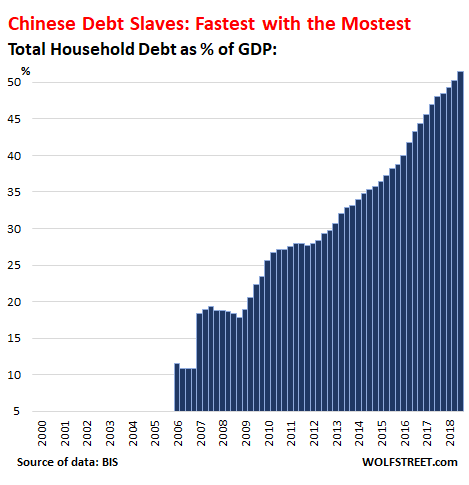

The most explosive household debt: China

China is in a category of its own. And so the chart has a different scale. The household-debt-to-GDP ratio is still in the German neighborhood of just above 50%, but it has quintupled in the 12 years since the BIS data began in 2006. The idea that Chinese households are paying cash to sustain their housing bubble or to buy cars has become a bad joke: Chinese consumers have discovered debt, and they are eagerly turning into debt slaves:

Another Global Financial Crisis, with China at the Epicenter? Here’s my podcast, a 13-minute financial rollercoaster ride…. THE WOLF STREET REPORT

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Switzerland has one of the lowest home ownership rates in the developed world around 44% . The whole country is under rent-control for residential dwellings, meaning that the annual rent cannot exceed a certain percentage of total investment. They are debt slaves but not to their own houses. In contrast, Norway has about an 82% home ownership rate. Quite a difference in the housing markets but both household debt ratios are over 100%. Hard to understand what the Swiss are spending their debt on.

@cesky Yet housing in Switzerland is very expensive. What’s the catch?

There is a 100% capital gains tax in the first years of ownership to stop buyers from quickly selling houses. Swiss law is very strict about the rules of buying and selling because it’s a very small realty market. The longer you live in your house the less capital gains taxes you have to pay on your profits.

Foreigners are very limited in their ability to buy real estate in Switzerland, too. Both factors should act to dampen prices by discouraging speculation and money laundering in real estate.

Does foreigners include EU citizens?

@char According to https://www.ch.ch/en/real-estate-foreign-national/, which is an official site of the swiss government, EU/EFTA nationals are not concerned but you have to live in the country. That still excludes a lot of money.

I am very dubious about the direction of Swiss monetary policy, and in fact fear it may be a trap for Swiss society – this is not the Switzerland I know. Leaving that aside, and it is a very big aside, maybe the experience of Switzerland is an example of some of the limits of being a wealthy and successful service economy, particularly as financial centre in a world of wider monetary expasion that has put the sf and hence the economy under different pressures.

There are three articles I have been reading that give a better description from various sides, but you will have to piece the picture together for yourself. As only one link goes straight through in a post, the other two you will have to add three ws.

https://www.swissinfo.ch/eng/poverty_swiss-take-aim-at-excessive-debt-/44802620

Explains that stats (privacy remember) are lacking, and how socialistic moves are at work in terms of debt relief.

.eiu.com/industry/article/526174436/the-swiss-household-savings-puzzle/2017-11-28

Looks at how Swiss savings and real estate purchase interact.

.variantperception.com/2018/09/09/switzerland-facing-effects-of-consumer-debt-binge/

Focuses on consumer debt level.

You will see an apparent contradiction in two sets of figures in those – Swiss save a high amount of disposable income, yet debt as % of disposable income is high, I leave anyone to figure out for themselves properly how that is.

Low home ownership is primarily a question of prices in my opinion, it is an expensive market with higher lending standards, and as with Germany laws increase incentive to rent.

I’m Swiss, and here is my take on it: I have a mortgage at 1.15%, and I can invest in funds and other instruments with better returns than that. Moreover, my interest payments are tax-deductible.

My savings therefore don’t go into paying back my house, resulting in having both high debt and high savings.

With ultra low interest rates on mortgages since 2008, the home ownership rate has increased markedly, primarily the purchase of condominiums. In the 1990’s, the home ownership rate was around 36%. Now 44%! Lots of million dollar condos that could be interest only??? Individuals that I know personally have opted to take out interest only and at the same time save what they would have used to reduce the principal. So the interesting question is the rate at which new debt has been taken on and how much current interest the typical Swiss home/condo owner has to pay relative to their relatively high income( minimum wage is approaching $20 per hour). The high debt burden would become problematic if interest rates reverted back to the levels that prevailed in the 1990’s ( 3-4%).

I think you are along the right line . I don’t know the methodology used to calculate savings rate in those articles , but have seen principal repayment on assets counted in as savings at other times, in which case what you are saying adds up further. I would have to start looking up debt/disposable income ratio over time, and if possible mortgage vs consumer of that, but the impression overall, if principal payment counts as savings, would be higher debt for property purchase plus higher savings in its repayment, all coming out of a high disposable income. The Swiss property market and its mortgage structure is quite unique

https://www.quora.com/How-do-home-mortgages-work-in-Switzerland

So the level of existing debt will be naturally high given the exceedingly long amortisation accepted and used.

I expect wage inflation before a rise in interest rates so it is not that problematic.

The question of why low/high home ownership has two big answers. Rural or urban and state policy. Price is not important

Thanks, and to B – these are the kinds of small details that often even local people do not know of their own market, let alone of foreign ones. I know in Switzerland in some remoter areas there are state financial incentives to encourage repopulation.

It is still possible to put it all down to price, it depends how you choose to look at it – eg. policy affects price which makes renting/ownership more or less attractive. That people choose not to buy vs. are unable to buy is quite a thin line that is hard to place when there are many variables, including state policy, at work. I won’t guess, but for sure some will think prices are too high while others will think it is soundly managed and that they should be at that level. I won’t argue either way, as that is for the participants to argue out themselves.

#1 Lets not confuse actual home ownership – no mortgage – with debt slave / mortgage obligation.

When I get asked, “Do u own ur own home?”

I reply, “well, I have an obligation…”

And the obligation never ends with HOA fees and property taxes.

I guess it really depends on how you quantify national GDP, take Ireland for example debt to GDP of 43.8% in 2018 – you must be kidding.

as per economy.ie – the 2016 Irish GDP explosion farce.

http://www.irisheconomy.ie/index.php/2016/07/12/the-farce-of-irelands-national-accounts-lets-go-plane-watching/

Wow! Exports are up 34%; Investment is up 27%; imports are up 22%. Wham, Bam, the economy grew by 26%. Sensational. Per capita income per person in employment has increased from a whopping 88k in 2010 to 130k in 2015. I’m sure you can feel the booming economy in your pocket? Of course you can’t, the national accounts are a sham.

It’s large corporations transferring assets and IP patents into Ireland – with no real connection to employment – and then booking it as real investment, for tax purposes.

They don’t call it “Leprechaun economics” for nothing

GDP is a reasonable number to use for almost every country except Ireland.

I am a Dutchman currently living in France. Having spent the majority of my years in the Netherlands before emigrating, I guess that I can contribute something to this discussion without immediately feeling the need to defend myself or my country of birth.

Statistics like “household debt to GDP” can be extremely misleading if they are not placed in context. In this case, it is not only the amount of debt in itself, but also the quality of the debt that must be taken into account. It makes quite a difference if a household goes in hock to pay for a new car, a boat and a nice holiday, or takes out a mortgage to finance the house they intend to get old in. In the former case the debt is not balanced by serious assets, in the latter case it is.

While the naked debt figures for the Netherlands look awful in this article, in reality a significant part of that debt consists of mortgages taken out to finance houses to live in. While one can argue about the current price level of real estate in the Netherlands, fact is that only a small subset of these houses tend to be “under water”, in other words, worth less than the mortgage resting on it.

To summarize, in the Netherlands household debt in the form of mortgages is largely canceled out by the value of the assets financed with them. Household debt purely for consumption purposes is not very popular among the Dutch, also because consumer credit interest is not tax deductible while mortgage interest is (with conditions).

I do wonder what a list like the one in this article would look like if not simply the household debt figures, but rather something like “net household asset balance – assets minus debts” were to be factored against GDP. My guess is that such a list would look quit different.

I agree with this analysis.

Our family went heavily into debt to buy a large piece of mountain land TO LIVE ON, forty-two years ago.

We have long since been debt – free, but using debt to acquire the personally used capital (the land) to get that way has been a sound practice, IMO.

Aside: No way I could attack your country of birth and survive, Jos. My wife was born in Tilburg…

[BIG smile]

To your wife: Hartelijke groeten uit Soesterberg…

Love your contributions on Len Penzo’s, by the way.

Though this table has a limited amount of countries, if you read the introduction you will see a maybe more accurate methodology – net assets ppp as % of disposable income (I think !)

https://data.oecd.org/hha/household-net-worth.htm

but we must also remember that national debt is ultimately a private liability, and that national debt is often used to substitute private expenditure, so changing say disposable income as well as expenses. I don’t know if the above OECD figures result in an accurate portrayal of that effect. We could add to that that the level of wealth/debt could change drastically if asset values, currency values, gdp values etc change by much. So any comparison is really just a rough guide to work with, a starting point from which to begin understanding a reality, not an answer to what that reality is.

“the level of wealth/debt could change drastically if asset values … change by much”

Right on. As to disclosing my net worth, I say “That depends on the going price of real estate hereabouts, on the day you ask”.

Bankers,

Any multi-country comparisons of GDP, debt, or whatever based on PPP is a very iffy assumption that produces very misleading results: These Purchasing Power Parity numbers convert local data into US dollars and adjust those US dollars for some hypothetical “purchasing power” differences in the local currency to the USD. This formula is in the eye of the beholder and regularly leads to some astounding results. For halfway accurate results you want to stay in local-currency-only ratios.

For example, China’s GDP expressed in PPP dollars is $27 trillion. That’s about 35% higher than US nominal GDP. This result is totally nuts. PPP is very misleading and should never be used for anything.

The US trade deficit for last year was more than $900 billion if I remember correctly, but Wolf hasn’t commented on that. I’m not an economist, but somehow that doesn’t seem to me to be a good thing.

Here you go, my article on the US trade deficit, including my own blistering charts and all, published the day the data was released (March 6):

https://wolfstreet.com/2019/03/06/good-lordy-what-a-banner-year-2018-was-for-china-other-countries-and-corporate-america/

I sort of agree, at least I don’t attach too much faith to any particular metric, if I could be more vague I would. However China headline gdp is for triple the population, and if you try to convert that into meaningful activity and equivalent values (vaguely) then I would not be surprised if China gdp was higher than US. In reality, what are we to include in gdp – one is able to monetise (ask or impose payment for) well beyond what would seem reasonable or productive, not forgetting the broken window fallacy and endless variations on that. Where does that leave us ? That is why real life commentary like is found here often is very valuable indeed. Thanks.

Wolf, if PPP should never be used for anything. What was its original purpose ?

It’s very difficult to accurately compare economies denominated in different currencies because currencies fluctuate (exchange rates) and lose purchasing power (inflation) at different rates. So one such effort to make economies comparable was PPP.

Bankers

2018 China population = 1,415,000,000 (1,415M)

2018 USA population = 327,000,000 (327M)

Ratio of china to USA population = 1,415 / 327 = 4.24

ie: China population 4.24 times larger than USA (not 3)

China PPP is mostly based on currency yuan) peg of US$1=6.9 Yuan. ( it was US$1= 4.0 Yuan in 1990).

If the peg is US$1= 4.0 Yuan as in 1990, the whole PPP will be greatly distorted and China can sell to US anymore.

I would consider that PPP is a valid way of estimating relative standards of living — but those aren’t quantifiable economic data, they’re more useful for higher-level comparisons.

Hopefully it’s not against the posting policy to link some other site. You can read an alternative view on PPP with lots of real life (non-academic) experiences in the following post:

https://acting-man.com/?p=52263

I feel a big mac attack coming on.

Javert – thanks, I just threw in a rough guess as notion…I was wondering afterwards if it was actually less than three.

MM – even within one country the variability of circumstances is vast. In that article the author focuses on “hedonic comparisons” that set western standards as minimum bar, but I guarantee you you can go and live acceptably and comfortably in these countries at much much lesser cost, this – you would have to leave behind a world of choices and services to do so. You can do the same within a western country, I can find acceptable property in most countries at a fraction of the average cost, where food prices are minimal from local produce. You won’t have a large income like this though, future choices will be more limited, and the social scene would be of a very different nature to that of city, but you would be as well, or better off, in own wellbeing as long as you were able to adapt positively to the change of environment – e.g. some people look for this kind of reality and feel uncomfortable in faster big city life, while others would perish without city constant attentions.

So where anyone places the values, even within national economy, is very personal and subjective. As an extreme take someone who is self sufficient. He/she has no income, he is in utter poverty…he has no debt so is wise to be so….he has no savings worth measuring and yet he seems happy, is active, well fed and dressed and enjoys a level of wealth and security ( to his or her personal view) that cannot be beaten.

So PPP is, and isn’t, a valid comparison. It all depends on where anyone sets their own values and expectations, and it all revolves around the metric of activity having been monetised , in some societies everything has a money price attached and the resulting market is viewed as allowing and achieving progress, in others they just don’t bother so much as it is all more informal as per say within a family is in the west. Neither is nescessarily the better.

Thx for sharing. This makes more sense given that I know conspicuous car consumption is not a big thing there. And their college is paid for by the public.

“…. but also the quality of the debt that must be taken into account. It makes quite a difference if a household goes in hock to pay for a new car, a boat and a nice holiday, or takes out a mortgage to finance the house they intend to get old in. In the former case the debt is not balanced by serious assets, in the latter case it is.”

Yes, sure, but no, the Netherlands is not special; it’s typical.

What blew up in the US during the Financial Crisis were MORTGAGES that then caused the mortgage crisis that then helped take down the banks. The vast majority of US household debt still is and was housing debt (mortgages). The Netherlands is not an exception, but typical in that respect.

Just wait till house prices decline 30% or 40% in the Netherlands — and see that does to the “serious assets,” as you said, that back the mortgages. This happened in the US, and it happened in Spain. In Spain, it toppled the Spanish financial system to where the state and the Troika ended up bailing out some banks and shutting down others.

From my observations, people who see that their ‘serious asset’ has, as happened here in the UK, gone from say 200k to £700k in 10 years, immediately rush get in an architect to design an extension, or even build a second house on the property.

I have been deafened by the sound of drilling, hammering – and squeaky wheelbarrows – all last year.

The words, ‘peak’, ‘asset bubble’ and ‘unsustainable’ seem not to be in their vocabulary.

Feeling serenely happy and even astute about vast debt ‘secured’ merely by bubble asset valuations is a case for seeing a shrink, not a reason to book the architect.

With a risk of repeating myself, those that rushed to buy housing are the dumbest, least financially literate people I have met. Of course, the central bankers made them look like geniuses, and created a moral hazard that will linger for a long time.

Thanks for your comment Wolf.

Although I would never dare claim that the Netherlands are immune to a housing price crash, the Dutch real estate situation is markedly different from Spain or the USA. The Netherlands are a small country, space is at a premium, and there never seem to be enough houses built. There is an eternal shortage of housing and it doesn’t look like this is going to change anytime soon. Also, non-social rents are high, in some cases approaching mortgage servicing payments.

So, as soon as prices seem to go down, there is a contingent of would-be buyers waiting in the wings to snap up the offers. Be it renters eager to buy, people who want to upgrade or youngsters wanting a place of their own, there never seems to be a shortage of buyers.

Although this does certainly not preclude a downswing in the real estate market with the resulting price correction, a serious crash of 30 to 40 percent does not seem the most likely scenario. Especially if you take into account the latest announcements from the ECB who seem hell-bent on stuffing bags of interest-free money down the throat of everybody who can fog a mirror /sarc.

Jos Oskam

With all due respect, you are perilously close to saying “…this time really is different…”.

@Javert Chip

You’re correct and I noticed this while writing, so I have tried to avoid sounding like that…but obviously not tried hard enough :-)

Although I *do* feel that the Dutch real estate market really *is* different from Spain, the USA or a host of other countries, and that this difference makes a crash less likely, there are of course no guarantees.

The Netherlands are small but not that small and most land around the Randstad (Amsterdam,The Hague, Rotterdam area) is veen. (peat bog swamp) It is state policy to not build on it but use it as (really bad) farmland. Change that policy and there wont be a land shortage. Another issue is that most houses are build before 1990 and as such are not exactly energy efficient. With the new government policy of a gasless country in the near future all those houses need a very expensive refit which in my opinion leads to much lower house prices for those buildings.

ps. Refit is 20% of an average house, land value is 30% so my expectation is that a lot of neighborhoods build in the 20th century will be demolished and rebuild denser. I don’t see how that would be advantages for old builds.

In Japan in the 1980’s an awful lot of the debt in their epic credit binge went towards real estate, where the value of Tokyo was supposedly worth more than all of Canada put together. Then the bubble burst in ’91, asset prices collapsed and at one point Tokyo real estate was down (IIRC) 80%. The banking system never recognized the losses and become zombies for a couple of decades.

What happened in Japan 25 years ago should have been a canary in the coal mine for modern economies, but somehow the lessons were ignored and everyone started thinking this time was different. As Australia and Canada are starting to discover, it isn’t.

I recall that in the 1990s US economists — and the financial sector in general — was openly contemptuous of Japan’s QE, zombie companies, over-reliance on debt, and general desire to eliminate economic cycles. But you won’t hear that today, except in alternative media: the US has become Japan.

https://www.youtube.com/watch?v=IWWwM2wwMww

Dale

Absolutely untrue.

USA may indeed mirror some of Japan’s bad behavior, but US banks are probably among the most aggressive in the western world (includes Japan & Australia) at recognizing & writing off bad debt.

@ Javert Chip

Absolutely untrue? I’ll take exception to ‘absolutely’.

The US has its house in better order than the EU in general (not necessarily including some specific members), the UK, Japan, and (apparently) China. But certainly the US has adopted the Japanese-style QE and low interest rates. And as a result, we have higher debt and — inevitably — more zombie companies than previously. Corporate debt quality in general has deteriorated, even as household debt / income has approximately doubled since the early 1990s. And, of course, the Federal debt / income (tax revenues) has skyrocketed.

So I’ll go with ‘relatively untrue’. The cleanest dirty shirt, right?

THE WORLD, at least where the main central banksters rule, is becoming Japan.

@illumined +1

there is a belief by many in the u.s. that because the money printing hasn’t caused extreme inflation, it’s ok. this is now being packaged as “mmt.”

my first thought is the best we can hope for in this scenario is japan: a slow deflation and gradually lowering future expectations. my second thought is that because we don’t have the social cohesion of homogeneous japan, the more likely outcome is societal collapse and/or war.

safe as milk

“…my first thought is the best we can hope for…slow deflation and gradually lowering future expectations. my second thought…is societal collapse and/or war….”.

You definitely jumped into the deep end of the dystopian pool:

o Japan has been homogeneous for the last thousand years, engaging in 25+ named wars during that time; “Homogeneous” definitely does not mean peaceful

(https://en.wikipedia.org/wiki/List_of_wars_involving_Japan).

o Median ages (half above & half below) of USA males & females are about 10 years younger than Japanese males & females.

o WWII Japanese war deaths – 4.34% of population, (mostly military male); USA – 0.32% (mostly military male).

o Japan does not “encourage” immigration into Japan; USA has been one of the most welcoming & heterogeneous countries since its founding.

o Without immigration & rapidly aging, Japan population peaked at 128M in 2010, declining 1% since then; USA 2010 population 305M, increasing 6% since then

People always talk about the dramatic scenarios like war and hyperinflation etc., but according to some of the best analysts I know about, the depressionary effects of deleveraging is what will be the reality of the next decades. The homelessness and opioid crisis and death of the middle class have led to snowflake AOC, not a Russia 1917 Revolution…

@javert chip – my point is that japan sees itself as a “one blood” society with collective responsibility. the usa does not.

when political elites are in danger of losing control, they often start wars to maintain power. ours have already restarted the cold war. neither party questions it. who knows what comes next.

I totaly agree with Jos and Rd.

The Canadian number is admittedly awful and I have often argued on WS that it does not accurately reflect the Cdn psyche or our history. However, Canada has also become an urban country by % of population, and with that fact has morphed into a hamster wheel society focused on urban consumption priorities; expensive housing, commutes, dining out, ‘activities’ that cost money, etc. While we are one of the largest countries in the World, our population is less than California’s and the majority of Canadians live less than 100 miles from the US border. The stats reflect this situation.

I have lived almost my entire life well outside of these urban centres. I used to know highly paid mill workers that lived like the golden goose would never quit laying, but by and large the more modest the income the more modest the lifestyle and the more likely people would have no debts. All of my friends had their homes fully paid for by the time they hit their forties. Most didn’t have car loans. etc. Nowadays, when I talk to the children of the highly paid miners and millworkers of my past they are often angry that they cannot live the freewheeling consumption their parents enjoyed and could afford. They often expect they should be able to; are entitled to do so. I had a co-worker 20 years my junior ask me to provide a budget analysis for him. He made good money but was sinking ever deeper in debt, by the year. I told him it was a dead snap, and I made a double entry list of needs and wants. And that is where it all fell apart. What I selected/implied to be wants he thought were needs; hockey rep for son, figure skating lessons for daughter, trailer, truck to haul trailer, type of food purchases. I asked him how he shopped and found out they often zipped to the store at 5:00 pm for supper stuff. When I explained the concept of store flyers, and building a week’s menu ahead of time by what was on sale, and buying ahead in bulk, he did not understand the power of saving after-tax-dollars, let alone the need to pay the mortgage off. I tried to make it into a fun game for him, to see how well he could live on less than they used to spend. He didn’t go for it.

My son is 35. His outstanding mortgage is just 1.5 years of his salary. My daughter is 39. Her home will be paid for by age 45. They both are investing in pensions (that are fully funded). As I write this my daughter is just arriving on the Oregon coast for a 1 week vacation at a beautiful seaside ‘suite’. (I used to stay there myself). She is paying for it with ‘points’. My son lives on a river so he doesn’t need to vacation very often, his lifestyle is the vacation people pay for.

That is the Canada rural folks know. Our hobbies used to be free and everyone shopped the flyers and paid off their mortgages. Everyone.

Warms this old man’s heart to see these values survive here and there ..

@paulo

i spent most of my life living the urban hamster wheel lifestyle that you describe, i have learned the error of my ways. i am still an urbanite but i take pleasure in my family and walking the dog down by the river and chatting with neighbors. we rarely go out for expensive meals, etc anymore.

i have the advantage of an economics education so it was easy for me to understand where i went wrong and develop a strategy for getting my like back on track. most people – even educated people – are functionally illiterate when it comes to money.

there is a great syndicated radio show by dave rasey who gives financial advice in a straight shooting folksy way to people who call in with their problems. it’s simply jaw-dropping when you hear people explain the tragedy of their financial lives. at first i had contempt but now mostly sympathy for the callers. dave’s advice centers around a system he developed (and sells) that’s solid if somewhat simplistic and christian for my taste. it’s based on a system of “baby steps.” i think we all need to take baby steps in the right direction.

dave rasey = Dave Ramsey?

I do absolutely understand your take on urbanization, but there is another important macro dimension to consider: We humans do much better working together, sharing the tasks, than trying to do everything ourselves far away from everybody else. The ills of urbanization are well known, but there’s a lot of thinking and some initiatives going on to make cities more livable.

Harry Dent points out the importance of China urbanizing. That will probably be its greatest challenge in the next decades.

Farming is automated to a large extent already in developed countries, and that will continue worldwide. Even mining, extremely dangerous for humans, is getting automated. Not much for humans to do then in rural areas. That’s good, because then nature can be pristine and healthy and be the Planet’s skin and lungs.

Forestry is also automated with its tree cutting machines.

Dutch housing is way overvalued if you compare it to historic housing values to income. This is mainly due to the tax-code but also because where in the house price cycle we are. Household assets is mainly overvalued home equity which could crash like the 80’s when house prices halved so i find net household assets not a particular useful number

Jos just imagine the mortgage intrest rates we had in Netherlands in the 80,s? It will be a massacre.

Added to the almost 0% rates last 10 years that means that savers been slaughtered terrible. If we account the insane costly immigration and

the very poor future performance of stockmarkets and thus pensions we

have a toxic cocktail of a bloody stagflation scenario. Not to mention the aging population.

What the banksters have done is simply consuming the future by loaning from future generations, hell will be paid one way or another.

This is a bit specious. If there is a high debt to national income in a society, then most like the society is moribund and can’t react well to change. You say that Netherlands has good debt in household debt, but this requires low interest rates, held down artificially and it assumes that people will stay employed and support the long term debt. In a recession this is not true. in the end the debt and the moribund nature of the economy will force either a deflationary recession or significant inflation.

Good traits begin at home. For us intermittent fasting and some good old fashioned deleveraging called savings really works. We look at debt and insulin resistance as the things to avoid. No debt and No Sugar works for us. We’re happy.

Smart!

I just finished reading “Pure,White and Deadly – How Sugar is Killing Us and What We Can Do to Stop It”. We’ve been fooled all these years into thinking it was the saturated fats!

I wonder if there is a good source of corporate debt to GDP? I think this time corporate debt is going to be more important since they went whole hog with ZIRP. Rumor is that they are looking to deleverage in order to deal with BBB problem, but that would be a drag on the economy wouldn’t it?

Yes… coming. Maybe next weekend.

Wolf, how about total net debt, personal, corporate and government against GDP (net of Government.

i.e, the private, tax and interest paying part of the economy that has to carry Government).

Thanks, Lance – I’ve been wondering about this very question! Hopefully Wolf regales us soon with his consummate ability to make very recondite things very clear. I keep hearing about the BBB problem vis-a-vis buyback leverage and on the face of it, the whole thing sounds pretty precipitous.

sorry. yes, i ramsey.

Interesting, China and Germany both at 50% household debt/GDP. Both are export monsters, so in both, consumers might be borrowing to compete with the rest of the world to buy local products. Is that really what it would mean?

Germany’s debt to GDP ratio has been essentially flat for two decades. China’s is shooting up exponentially. HUGE difference.

So is India’s. People now take loans to go on vacations and buy furniture. It’s insane.

Debt is so low in Germany because so many people rent (50%) . Higher home ownership would lead to more mortgages and higher debt.

China was a third world country. Normal people in third world countries don’t bank so no debt.Normal first world people do bank so they get mortgages and car payments

This one he turns it round very simple (is good very simple) so it takes debt (new money) from GDP

http://adjusted-for-inflation.com/

it’s also looking bit like household debt to gdp, why I don’t know.

Like any other balance sheet, households have assets as well as liabilities. It makes more sense to look at net debt rather than total debt. I suspect that households in the Netherlands and Switzerland have a lot of assets to offset their debt.

True. The problem with debt is that the creditor still needs to be paid, while the market value of assets can experience considerable variation.

Certain assets, including equities, bonds, and real estate, are currently at elevated levels by most valuation techniques. If asset values revert to anything like historical norms, a very healthy net worth can quickly become very unhealthy.

One thing that I haven’t seen in commentaries is the fact that, because of inflation, the creditors’ loans will suffer, not the borrower’s debt. Inflation allows borrowers to pay back debt with cheaper money. For long term debt, borrowing most of the property’s value, at what is currently a 4.25% interest rate (+ or -), makes sense to me. Unless we have deflation (which would cause the opposite effect) and if currency stays relatively stationary, at 2% inflation, it will be easier and easier to pay off that debt over time. This assumes that someone has a “fixed” rate, not adjustable. Other debt – credit card, car loans, any short term or adjustable loans – spells trouble if times get tough. Personally I’d want a mortgage at the currently low rates, use available cash for investing, and have the benefit of a “non-recourse loan” (if available) which means that one can walk if the property’s equity disappears.

” One thing that I haven’t seen in commentaries is the fact that, because of inflation, the creditors’ loans will suffer, not the borrower’s debt. Inflation allows borrowers to pay back debt with cheaper money ”

Tst, the debt is the money and the money is always in the lender’s account so he lend again and again and get interest each time. He make inflation for profits. Borrower he must pay more for all else because inflation so he must be hoping he get some inflation in pay too or he is getting poor. But lender he must make sure his money is not worth nothing or he got no job, so he make sure you start in debt with need to pay tax, and he got interest that people like working with his money too so he always pushing it to people “have now pay later”, but not so much that it realised that he just inventing like he want.

vinyl1

Very strongly disagree.

Net debt results in someone with $1M house & $1M mortgage having zero “net debt”. No reasonable loan underwriter would use this technique.

Some jurisdictions (Swiss) may have special legislation/circumstances insulating debt from volatility for a limited period of time, but I can’t think of a single major asset class that has “stable” valuations over the normal business cycle (say, 10-15 years).

Total debt generally retains its amortization schedule regardless of asset value.

I was kind of thinking of myself in 1995: mortgage balance, $50K, cash and stock in brokerage account, $250K.

We get that, ‘what about the assets’ argument all the time in Vancouver.

As in, I make $75k/year, and I borrowed $1mn to buy a 50 year old house way out in the outer rim suburbs, but now I have an asset worth $1.1mn (and real estate prices only ever go up) so everything looks good on my balance sheet…

Surely the problem is obvious though, if the asset values are inflated (and cap rates surely indicate they are in most of these places), then when the asset values fall, the debt remains and everything is frozen, barring some sort of reflation or a mass wave of foreclosure which would threaten the banking system (as in the U.S., U.K., Ireland, Spain, etc.) last time around – this is basically what a debt crisis is, after all.

Alternatively, you keep asset prices high and you are just stuck with zero/negative rates forever and a zombie economy.

Last week I received another offer from a predator lender. Just sign here and deposit this $3500 check. Interest rate was 33.79% and term was about 12-18 months. This is a national disgrace and what is the party that “cares” doing about it, nothing.

I looked in to this in the UK recently, as by chance I’d heard a customer talking at the bank about the behaviour of just such a lender hitherto unknown to me. So I looked at some websites.

Small sums, huge interest and penalties, targeting unsophisticated people.

Hey, Petunia, you got a deal! I’ve heard of APRs as high as 300% on short-term loans :-]

But I agree… Some states have usury laws, but they’re designed to be ineffective with many exemptions, and so they don’t accomplish all that much. There have been some efforts in Congress to pass a modern version of usury laws (including interest and fees), but the financial industry lobby is dead-set against it, and the legislation has gone nowhere.

The Wall street banking/financial community, annually drops one million lobby dollars per congress member, into Washington DC.

I hate to get political here but the Republicans have categorically stopped any legislation to control these predatory lenders (which includes Bank of America!). Same for “for profit colleges” which use federal grants to enroll, in some cases, homeless people who are recruited for programs they won’t be employed from and can’t even finish. They are hell-bent to stop Elizabeth Warren who wants better consumer protection. As I’ve stated in the past, these are people who do not comprehend how interest rates work, can’t calculate worth s**t, and are very, very gullible. I do not know how these lenders sleep at night knowing they’ve ripped off someone who is defenseless against these loan terms. So, when it comes to “family values”… you may want to remember who supports and enables these kinds of thieves.

HowNow,

Don’t get me started on Fauxahontas. Check out what she did with the so called Consumer Protection Board, another farce. The board is a creature of the Fed and she knew exactly what she was doing when she did it. At least the right admits they side with the rich.

Petunia, you’re right. Both parties stink to high heaven. I’m a former Republican, too, sorry to say.

didn’t usury laws used to exist nationally? when did they get revoked?

Please explain how the Consumer Protection Board was a farce. Before it was dismantled by Mulvaney, the agency is estimated to have saved or returned to Americans nearly $12 billion since 2011, while costing taxpayers $2.9 billion to operate.”

https://files.consumerfinance.gov/f/documents/201701_cfpb_CFPB-By-the-Numbers-Factsheet.pdf

Do people simply complain or do they have alternate solutions?

This has some history on US usury law

https://americansforfairnessinlending.wordpress.com/the-history-of-usury/

Idaho Potato,

The CFPB is financed by the Federal Reserve Board and it was sold to the public as a consumer protection agency. After the rape and pillage of the American public during the last 10 years, do you really think the fed protects consumers? The good senator was a major supporter of this travesty, a bank funded consumer protection agency.

@Petunia

The CFPB is funded by the Federal Reserve. The Federal Reserve is mainly funded primarily from the interest on U.S. government securities acquired through open market operations.

The Federal Reserve is funded by you and me – the taxpayers. The Federal Reserve has oversight by Congress through the Government Accountability Office. The CFPB has campaigned and achieved some redress for consumers during its short tenure. There is no agency that has taken its place.

I still don’t understand why it is a “farce”. Not have any such agency in the face of a farcical Congress that lets Wall Street get away with murder is the real farce.

Idaho Potato,

The fed’s profits don’t come from taxpayers, they come from depositors and other banking operations. The US Treasury/taxpayers actually profit from feds operations. The CFPB was a control mechanism to keep consumers from getting redress on major scams inflicted on them by the member banks.

This is an excellent example of how the party of wealth (the GOP) tricks everyday people into turning on policies that would benefit them; the use of the the GOP’s ethnic slur for Senator Warren is a real cherry on the icing.

Seems to me that laws against usury, at the present time after a decade of effectively-Zero, and Negative, IRPs, from the world’s Central Banks, would require defining usury, and would lead to the discovery that a fair rate of interest on a loan, is well above what sovereign bonds have been paying, and well above what savers have received from their banks, as interest on their accounts.

That’s assuming that you start with the Given, that your medium of exchange (currency) has some value.

Apparently there has been recent discussion amongst the Fed members, as to what a “neutral” interest rate is, and apparently their endpoints are, as of now, between 2.5, and 3.00 per cent.

Central Bankers around the world, including Fed members, you started this discussion. It will go beyond your wishes.

thinking about your query re usury laws, safe as milk:

certainly we may look on credit card rates, +/- 19 % per annum, as legalized usury

re usury laws, see for example Officer’s citation of Silberling, 1923, re usury laws in Britain:

“The Usury Laws fixed the maximum rate of interest and discount at five per cent…from 1790 to 1822…”; and this was the rate “… throughout the country”.

(“What Was the Interest Rate Then ?”, Lawrence Officer, University of Chicago, PDF online)

Query “usury laws” on search engine of your choice.

Wolf not so long ago posted an informative discussion re how Islamic states formulate regulations allowing some form of recompense for the use of other people’s money, while outlawing usury, so to speak.

Like the term “junk bonds”, the term “usury” denotes some form of excess.

as usual, thx Wolf

I hope someone else (actually a lot of them) takes the money and runs.

It’s not a crime that you can be charged with anymore than their ‘offer’

There was an anarchist American author who did that just a little before the great financial crisis. One day he decided to make his move. He had good credit so he basically maxed at all the loans he could from normal reasonable sources, got a bunch of credit-cards and maxed them out in withdrawing money, then took out all the shady crooked loans he could … and then moved to China permanently leaving no forwarding address.

It seems that more and more usurious predators have been flooding America with absurd procrustean leveraged credit – one gouging rate rubric to fit all – since the GOPer deregulatory mob got its hands on all three branches again.

My wife has impeccable credit and owns her own small business. For much of the post Bush Recession decade she used to get 0%/balance transfer/gobs of miles offers regularly. In the past year she has been harassed by slimy legal lending shark offers and a paucity of legitimate bank products.

I wonder if real banks are in a bunker mentality about end-of-cycle economy concerns? Or maybe the current legal swindle milieu that emanates from the WH grifter & GOPer goose-stepping kleptocrat capos has free license to flood America with the equivalent of financial Ho-Hos?

Or – and this is an expert’s (WOLF) bailiwick – is there something amiss brewing in the bank-credit-Fed funhouse dynamic that is causing this?

The Information Fountain

Bank of International Settlement (BIS)

Basil, Switzerland based, not too far from Davos.

The central bankers – central bank.

So secretive as to be not even close, to being opaque.

As with all statistics, some degree of a “jaundiced eye” is required.

I agree with other comments made here, that a debt measure of “net” rather than “gross” would provide a clearer financial picture. Just saying.

Nothing wrong with being a debt slave when you are young and the debt is against a well located single family home or homes. Go for it. Inflation will make you look smart. Always does.

The people who bought homes during the 2005 to 2008 time frame in California don’t look so smart. They lost a lot of their savings and their homes to deflation, which is most likely to arise after an extended period of price rises, like today.

Being a debt slave is fine, if you are in debt to buy a good asset and your ability to service the debt isn’t impacted, and the value of the asset doesn’t decline. Over US history, those conditions have been fulfilled more often than not, and people have done well with good debt. The real question is whether that’s going to continue.

You have to distinguish between good and bad debt, whether it’s borrowing to invest or consume. You can probably guess which is the good kind…

Housing is consumption. So all bad debt?

These numbers are viewed from the point of view of the BORROWERs.

But I would like to know WHO is LENDING?

They are the ones at risk if something happens and the borrower cannot pay or re-fi.

These numbers are so big that I’m not sure any nation can handle the outsize risks.

We will see how China’s consumers react to the unexpected wafer thin trade surplus in Feb and Friday’s 4 % sell off in stocks (Shanghai)

I see those US numbers as confirmation of the damage done to the middle class. GDP since 2008 has primarily been to the benefit of the 1%, not the debt slaves. To the nature of debt, before 2008 HC accounted for a much a larger portion of debt, since 2008 more people are on medicare, and we had ACA for a while anyway. In 2008 people were going Ch11 over medical bills. The simple reality is that Americans don’t have as much credit relative to GDP as most socialist countries speaks volumes to the decline.

Agree. While I’d like to believe the USA debt slave has learned a lesson and changed their habits, something tells me there MUST be another explanation.

If I may invent an example to make a point. Let’s say in 2007 finance and healthcare combined were 20% of GDP when ratio was 98%. In 2019 let’s say they are 40% when ratio is 76.4%

If we assume (again, hypothetical) that the huge increase went to the top few percent and virtually none trickled down to debt slaves, then where do the debt slaves really stand? If we lop off that additional 20% and take the current ratio 76.4% and divide it by 80% of GDP that actually involves debt slave participation and benefit, we get 95.5% ratio.

BTW really enjoyed the writing style, quite a few laughs. Will try to buy Wolf an extra IPA tonight if does not screw up my monthly auto-beer.

Debt to GDP is a worthless statistic. GDP is unrelated to income, and the ability of debtors to service their debts.

Gross National Income is out of vogue. Eat your GDP before you get down from the table.

Gross Domestic Income (measured by income) is theoretically equal to Gross Domestic Product (measured by spending). Every so often, they get out of sync; for example, just before the GFC.

But not to worry. The US government is now including unreported income in its estimate of total income. Unreported income amounted to about $600B per year, and that was just for proprietorships and partnerships. Good for a nice 3% gain in national income! Naturally, revision was tapered in starting a few years back. And that helps debt / GDP appreciably.

I think that Wolf might be right when he joked that we will soon see prostitution and illegal drug income included in GDP / GDI (as they already are in the UK and EU).

\\\

Wolf,

I know this sounds ungrateful but could you>

1* Plot the debt data in respect to the median brut household income

2* Plot the debt in respect to national foreign debt of each nation

As always, thanks for the great read!

Once the government changes hand down under in May 2019, Aussies will go to No.1 with a bullet, as they say in the music charts.

Household debt in the U.S. is nothing compared to corporate debt. Corporate debt in the U.S. stands at about $40 trillion. Loose monetary policy has allowed for insane overvaluations and fueled out-of-control speculation the world has never seen. More so than even the levels of the Great Recession. When the world makes the final pivot from speculation to 100% risk aversion, valuations on all assets are going to sink like a boulder in a small pond. Add to that the strutural problem of declining demographics only exacerbates the problem.

Those who have shelter paid for & large sume of USD will be King. Those up to their eyeballs in debt with massively deflating assets are in for a very tough ride.

Interestingly, US corporate debt is over 900% of corporate income (pre-tax).

Correction: Total corporate debt is apparently nearly 1300% of pre-tax income. The earlier figure did not include loans.

Please provide link for your $40T number

What I found was $9T at Forbes, which they defined as “alarming’ (https://www.forbes.com/sites/jessecolombo/2018/08/29/the-u-s-is-experiencing-a-dangerous-corporate-debt-bubble/#f837eff600e0)

Javert Chip,

“Corporate debt” is just part of business debts. A broader measure of business debts, including debts by small non-corporate businesses is $15 trillion (“nonfinancial business debt”). This is the number the Fed is using.

But this does not include bank debts. If you add bank debts (which might cause you to double-count since banks lend out the money they borrow), the total goes over $30 trillion.

Then there is total “nonfinancial debt,” which includes non-business debts but does not include bank debts — this is a measure of “core debt” – and that’s around $50 trillion in the US.

So the definitions really matter here.

But in terms of “corporate debt,” your number sounds about right. This includes bonds, C&I loans, leveraged loans, and nonbank credit (by PE firms, etc.)

The $40 trillion number I quoted was inaccurate. That number refers to the Total Market Cap of U.S. Corporate Equities, twice the level of U.S. GDP.

I read the speech that Fed Chair Jerome Powell gave at Stanford on Friday night. It is a shocker. Powell favors consumer inflation, meaning wage inflation. The phrase of the day is “makeup inflation”.

If Powell can manage to instigate more wage inflation WITHOUT associated asset inflation, Wall St will have a cow.

Until the human race addresses the mechanisms necessary to enjoy a level of employment and prosperity for all, rather than meeting the demands of the greedy few for constant ‘economic growth’ and subsequent accelerating wealth and income gaps, then why would you expect anything other than absurd solutions to an absurd way of ordering society..?

Well, I expect the historical norm: a revolution.

I think there were some definite assumptions made (continually over a few centuries) by free market economists about the labor market. When population densities were lower and even most “developed” economies were supported mostly by agricultural labor, the employment markets behaved very differently- e.g. wage markets, what the unemployed did when they lost a job, etc.

This is a very worthy discussion that both sides of the (overly politicized) economics profession should have.

MD you are absurdly , correct .

2 percent yearly inflation halves your purchasing power in just 40 years; that’s why. With this much debt, we’re inflating our way out of it.

Wage inflation for the lower 95% would be a good thing, and not just for the workers but for everyone else too. Higher wages would support higher interest rates (to keep price-inflation contained and house prices reasonable). Higher interest rates would rescue pensions (in the long run) after forcing corporations to deleverage (painful but necessary).

Higher wages would also support substantially higher GDP, since most workers spend almost all their income. Forget about trickle-down, higher worker earnings would be like an economic firehose.

The rich would benefit too – the additional consumer spending would translate into higher corporate profits, albeit at lower margins (higher wage costs).

Since there’s surplus capacity throughout much of the economy, particularly in the things that people want but currently cannot afford. And there’s plenty of headroom for interest rates to rise to counter consumer price inflation.

The more I hear about Powell the more I think he might actually be sensible.

Which Powell was that? The 2018 version or the 2019 version?

That’s why I ask for a big stocks (asset) bear market and a shallow recession. That will go a long way to resetting the many wealth, income, etc. inequalities.

I have read several financial experts explaining how that might come to pass.

There’s so much talk about the US national debt, that huge and growing number, but Steve Keen emphasizes the importance of private debt. Mike Maloney has identified private and corporate debt as the really big bombs of today.

As long as Switzerland is the home for elite money it will never be invaded and it will never crash. Polish up on history to understand that countries place in the world. The policies enacted there are very different from the rest of the world.

Wolf, it is hard to get all the different types of debt/GDP. Does BIS provide them all with a common treatment that allows one to compare countries? For example I live in the US and in Brazil. this BIS household debt makes some sense, although I have doubts as most people pay cash for houses and have very little debt, particularly credit card debt with runs over 50% – 100% per year. I need to check my bank and credit card statements.

Anyway do you know if BIS provides all the different debt slices? household, gov’t, corp / bus, financial If not do you know if anyone does? Even the Fed no longer provides total credit market debt that I am aware of. If it does, and I am mistaken, please tell me.