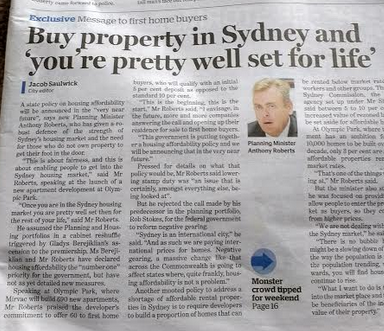

Bitter irony: Government told first-time buyers 5 months before bust began to “get into the Sydney housing market”; once in, “you’re pretty well set for life.”

“Nothing goes to heck in a straight line” because there is always a bounce, sooner or later – that’s my story and I’m sticking to it, but it does get tested from time to time, including in Australia’s housing bust.

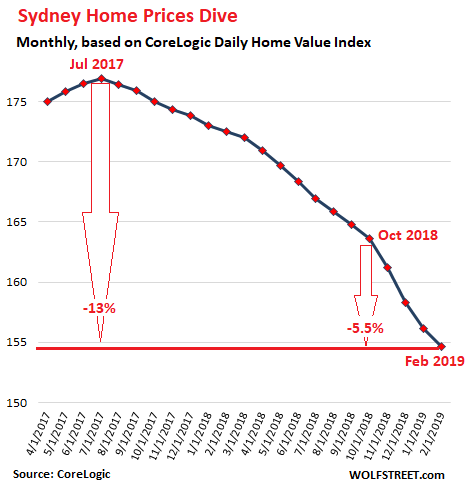

Across the metro area of Sydney, prices of all types of homes combined, according to CoreLogic’s Home Value Index, fell 1.0% in February from January, 10.4% from a year ago, and nearly 13% from its peak in July 2017. Just over the past four months, the index has dropped 5.5%:

The volume of closed sales recorded in Sydney in February plunged 20.6% from the already weak sales in February last year, according to CoreLogic’s report.

Condos, generally the lower end of the market, is where first-time buyers are thought to have a chance, and they were considered the saving grace in this market. But prices continue to drop, and the industry’s hope that first time buyers would bail out this market is now fading.

- House prices dropped 1.1% in February and 11.5% year-over-year.

- Condo prices dropped 0.8% in February and 8.8% year-over-year.

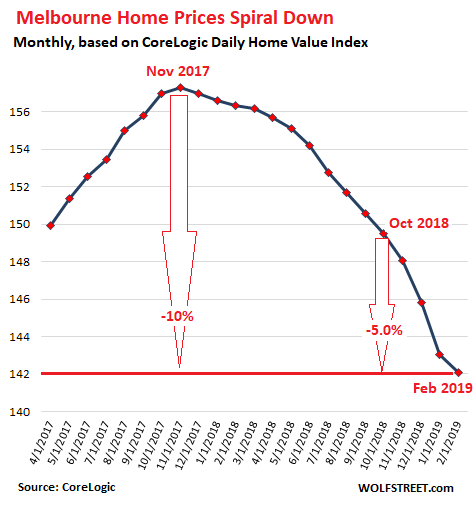

In the Melbourne metro, the second largest market in Australia, prices of all types of homes fell 1% for the month and 9.1% year-over-year, according to the CoreLogic Home Value Index. The index is now down nearly 10% from the peak in November 2017. Over just the past four months, the index for Melbourne dropped 5.0%:

House prices in Melbourne dropped 1.2% for the month and 11.5% year-over-year. Condo prices dropped 0.6% for the months and 3.7% year-over year. CoreLogic estimates that closed sales in Melbourne plunged 22.1% in February from the already weak sales a year ago.

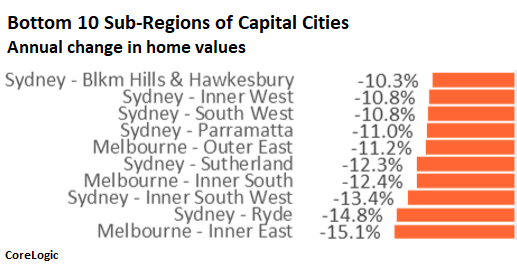

Of the bottom 10 sub-regions of Australia’s capital cities seven were in the Sydney metro and three were in Melbourne (chart via CoreLogic):

There is a bitter irony to all this. In February 2017, just months before the market in Sydney peaked, Anthony Roberts, New South Wales Minister for Planning and Housing, was promoting the launch of a 690-unit apartment development at Olympic Park, a suburb of Sydney, heaping praise on the developer for having reserved 60 units for first-time buyers.

Roberts was hyping new incentives for first-time buyers, including a reduction of the down-payment to 5%, to lure them into the Sydney housing market:

“This is about fairness, and this is about enabling people to get into the Sydney housing market. Once you are in the Sydney housing market, you’re pretty well set then for the rest of your life.”

It induced me to write an article with this headline, obviously: Housing Bubble in Sydney Soars to New High, Politicians Promote Scheme to Bitter End, with this image of the Sydney Morning Herald’s eternally glorious headline:

The metros of Sydney and Melbourne, due to their enormous size and high prices, dominate the national home values, but weakness is now spreading to other capital cities, with only Hobart and Canberra still showing year-over-year gains (in parenthesis, CoreLogic’s measure of “median value”):

- Sydney: -10.4% (A$789K)

- Melbourne: -9.1% (A$629K)

- Brisbane: -0.5% (A$491K)

- Adelaide: -1.0% ($433K)

- Perth: -6.9% (A$439K)

- Hobart +7.2% (A$457K)

- Darwin: -5.3% (A$398K)

- Canberra +3.4% (A$594K)

On a national basis, the CoreLogic Home Value Index dropped 6.3% year-over-year and 6.8% from its peak in October 2017. It’s now back where it had been in September 2016. CoreLogic’s report points out that, despite the decline, the index remains 18% higher than it had been five years ago, “highlighting that most home owners remain in a strong equity position.” Only recent buyers are underwater.

That’s a calming thought, even for the Reserve Bank of Australia, according to the minutes for its Monetary Policy Meeting on February 5, 2019, when it decided to maintain its policy rate at the record low level of 1.5%:

From a longer-run perspective, members assessed that, following such large increases in housing prices, the effect of the recent price falls on overall economic activity was expected to be relatively small.

From a financial stability perspective, tighter lending standards, an improving labor market and low interest rates were all likely to support households’ capacity to service their debt.

Few households were in negative equity positions despite the falls in housing prices, implying that banks’ losses would be limited even if household financial stress were to become more widespread.

The IMF was less sanguine in its assessment of Australia. It found that “the financial sector faces continued vulnerabilities from high household debt, still-stretched real estate valuations, and banks’ ongoing dependence on funding from global markets.”

The assessment “recommended further steps to bolster financial supervision as well as to reinforce financial crisis management,” which might be a good idea.

What banks & housing markets in Sydney and Melbourne are facing in 2019. Read… Forced End of “Ponzi-Like Leverage” & “Fraudulent Lending” Turns Australia’s House Price Bubble into “Property Bloodbath”

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Well, maybe Anthony Roberts (New South Wales Minister for Planning and Housing) was correct in stating “Once you are in the Sydney housing market, you’re pretty well set then for the rest of your life.”

Everybody assumed this was a positive statement; Roberts failed to mention it could also set you up for financial ruin.

Ah yes, big government at its best.

– It shows – IMO – that Roberts was “in the pocket” of the real estate/property boys.

– Similar story for Prime minister Scott Morrison. He worked for one of the real estate/property organisations.

– What do you mean “Conflict of Interest” ?

I was shocked to read that. I have never heard or can imagine a Canadian MP saying anything like that.

To be sure we had a brief spell of 100 % financing but if any member of the govt had advised buying, he would have been in trouble.

A city mayor maybe.

I wouldn’t say Canadian MPs are above this type of nonsense. In 2015, the Liberal candidate in my riding – who ultimately won and is now our MP – promised to “boost house prices in Orleans” by moving more government offices there. Ultimately, he did not move any government offices to Orleans, but prices have exploded in Orleans and across the NCR anyway due to massive increases in government spending.

If the rest of Canadastan (not Ottawa) were to ever visit and see how the government town laughs about their phissing away tax money they would finally get mad. The city is one huge puss filled boil that accomplishes almost nothing while living like over fed hogs.

As yerfij said, many in the West are already mad. If it wasn’t for the BC Govt NDP taking a stand against the Kinder Morgan pipeline, I would expect to see another resurgence of western separatism against Ottawa and Ontario/Quebec for always pulling the strings of those who pay the bills. Unfortunately, I live in the province that disrupts western solitary, BC aka la la land. But….I’ll take the climate and real west coasters as we muddle onwards.

Everybody assumed this was a positive statement; Roberts failed to mention it could also set you up for financial ruin.

I keep saying this: Professional politicians almost* never lie.

Instead they lead their victims to form their own, private, understanding of whatever it was they said, which the victims naturally agree with since their own brains came up with it.

Obama was really good at this. He could project a totally blank canvas so every “vision” he “shared”, everyone would naturally agreed since it was their own fantasy projected onto Obama’s canvas.

*)

Gotta make some allowances for, say, Theresa May and Boris Johnson.

Nothing whatsoever to do with ‘big government’ – that’s just your own confirmation bias wishing it to be so, and a classic straw man.

Merely the opinion of one man and far more likely that he himself was ‘calling his book’, being vested himself in the Sydney RE market, and set for a juicy seat or five as an ‘advisor’ or non-exec on the board of finance companies and builders.

Nope – far from being the fault of ‘big government’ it’s all a result of deregulated finance running amok.

The polar opposite in fact of the very well-funded propaganda which has formed your incorrect viewpoint.

Providing taxpayer-financed assistance for homebuyers is absolutely “big government”. Collusion with real estate industry is absolutely “big government”.

Collusion with the real estate industry is practically “every government”.

Small-government “economic freedom” poster boy Hong Kong is notorious for this.

Moar socialism!

Thank you but we already had the “capitalism has failed” speech 12 years ago from Kevin Rudd, the helicopter-money PM.

I like New Zealand’s decision to restrict all property ownership to citizens only. That’s a great government intervention only because it’s in keeping with governments original brief: defending the nations sovreignity. Australias government would never do anything so brash as to look after its own people of course, but it’ll gladly exploit its privilege to exploit its own citizens. Australia is a great example of government intervention of a property market in practically every other way, screwing over its young people and depriving them of any hope in owning a home in their own country.

I think this is smoke and mirrors from the govt. Foreigners can still buy new builds or anything through a trust or company….easy to set up. Well that’s my understanding anyway. Proposed capital gains tax will not lower house prices either and not adjusting for inflation is worse still. In my opinion NZ is in deep trouble. Debt to income is too high…maybe that should be regulated!

“Once you are in the Sydney housing market, you’re pretty well set then for the rest of your life.” But once the Chinese stop buying the house of cards crumbles.

This is what happens when folks think of housing as investments and not homes where one lives, makes a life, raises a family etc….things that are “cacophonous” to someone like SoCalJim…I’ll say it again: people’s hearts are where there treasures are. The proverbial chickens are finally coming home to roost as we know where many hearts are! Wonder how the 50 million or so empty dwellings in China will finally end up? Will be interesting to see how this plays out and if the contagion spreads.

Some idiot said that China was building housing for all the people coming from the country side.

No, they’re just speculation objects, and being unused they’ll crumble, a total waste.

The ginormous malinvestments resulting in mountains of debt, it will take decades to deal with that.

Housing as investment is a symptom of the commoditization of residential real estate, fueled by easy money policies of the world’s central banks and the pathological laissez faire economic strategy. Next is drinking water, then food, then air – if the trend continues unchecked.

Ok I asked for details on loans Broker Dan says don’t exist.

In Bay Area h1b workers get 10-year ARM jumbo mortgages with 5% downpayment.

Not a prudent investment to buy a house in Cal,especially the Bay Area . First there are the fires , now there are the floods after some areas received over 15 “ of rain in 48 hours. Then come the mud slides. Officials are very worried about dam breaks in the LA area when the >45 feet of snow in the Sierras melts this spring

Um, the dams in LA have absolutely nothing to do with snowmelt from the Sierras. The only way water gets to LA from the Sierras is via gov’t run aqueducts. Sacramento on the other hand….

Andy,

That’s a very general statement; do you have specific details on these types of loans?

As someone who got million dollar mortgage being on H1B, I see this as normal.

Banks don’t really care if you are on H1B or you are permanent-resident/citizen..

In 2017, The Sydney Morning Herald was part of a property company with a news problem.

I wouldn’t rely on it if I ran out of toilet paper.

Excellent Article!

Also worth pointing out, the high amount of IO Mortgages becoming Principal and Interest since beginning of year. Australian Banks have been hiding real delinquencies data.

From there export sector slowing down, foreign money inflow grinding to a halt to massive subprime mortgage bubble, everything that could possibly go wrong financially in Australia is happening. By end of year, Australia’s Central Bank will start its first QE I believe or they will face a recession for the ages. At least there CB has the tools to combat it, they have low debt and there population can afford inflation somewhat, once RE deflates.

Can Rate Cuts make them survive the downturn given the amount of Interest Only Mortgages banks gave out or is QE needed ?

I’m not an expert in currencies, but, I do not think Australia has the capacity to go down the QE path. The AUDUSD might collapse; it simply is not a strong enough currency like the USD.

Like I said, no expert here. If I am wrong I won’t mind being corrected.

You’re wrong. US federal reserve notes have lost 75% of their value since the year 2000.

And, yet, the world still hoards USD. And, yet, USD is still the most trusted currency on the planet.

That’s a ridiculous statement.

AUD is still supported by its UNMINED GOLD RESERVES.

Which are massive, and they still keep on finding more.

Australia is a treasure trove of still undiscovered resources, in a world of declining finite resources.

To date their banks and economy have not been that badly managed that QE has been necessary.

The Aussies just need to ease back the dial on the 5-eyes bullshit a little from ’11’ till ‘2’, accept their Huawei equipment, receive those Pandas and all will be well again. Hell, their coal might even clear Chinese Customs.

It’s not like the US and the UK will return any favours for services rendered!

Not Happening 5 eyes has nothing to do with it.

Keep your pandas, were better off with out them and will be better off when they are gone.

After all they only made a few mining companies rich and caused a surge in immigrant labour, they helped the Aussie in the street not 1 iota

Australia is for Australians, we decide who comes here and when, right now we a deciding, who of the recent arrivals we have, we want to leave. And when they must leave by.

I wish the prices on the north coast of NSW would drop, it’s like a feeding frenzy around here. I think Sydney and Melbourne homeowners might be selling before the price drops too much, and are retiring up here.

Prices are a lot lower than Sydney, so they can buy around here and have a million cash left over.

As for ad blockers, this site is fine, a few ads here and there doesn’t bother anyone, and pays for some interesting reading.

Some sites however run berserk with popup ads all the time, so you simply can’t read the stories.

ZeroHedge is an example of the worst websites for ads, check it out Wolf, and you will understand why ad blockers are popular.

I wouldnt fret too much. Once the sydney prices drop enough it wont make sense to buy outside of sydney for a lot of money considering the paycut sydneysiders will have to take to move there. Only makes sense for a small subset of retirees.

We ourselves were considering moving to newy until last year. Now we think, well, we will just wait it out instead of buying a place for 800k in redhead.. why would i pay that in newcastle when i can get something close enough here and get a higher pay.

Wherever the Chinese have bought will see the steepest price drops.

market is being prepped for next wave of northern hemisphere refugees

NSW government has telegraphed it, ‘we need more nurses’

the majority of which are usually from international labour pool,

You should look at UK immigration stats, they are nuts. You have a solid net 50 000 British leaving the UK each year for the last ten years at least, and over 200 000 net immigrants each year.

https://www.ons.gov.uk/peoplepopulationandcommunity/populationandmigration/internationalmigration/bulletins/migrationstatisticsquarterlyreport/february2019

Oxford university also has a migration observatory that gives percent migrant population, some of the figures there are startling also.

I am not xenophobic or particularly nationalistic, and have lived internationally for a long time, but this level of turnover is just not a very good idea I think :-/ . GDP will be happy I suppose.

Yes, the GDP is yet another number that is commonly used to deceive. If the GDP goes up, all must be well, right? GDP is more likely to rise as population grows.

Look at the GDP per capita. It often tells a different story. This is a much better but far from perfect macroeconomic indicator.

For the developed world GDP per capita has been pretty punk for ~10-20 years. Surprise.

https://www.economicshelp.org/blog/6299/economics/what-explains-differences-in-economic-growth-rates/

Thanks. I ended up looking through different economic indicators on from there and per capita final consumption expenditure is supposed to be as close a measure to wealth as possible. Even the per capita GDP charts have variables included in GDP and PPP which give some way out results depending on how they are assembled – in fact the most positive charts are the standard “fully adjusted” gross measures we are used to . So for UK

https://www.ons.gov.uk/economy/grossdomesticproductgdp/timeseries/crxr/ukea

gives personal spending % change annualised. Looks ok except it is current prices, so add an inflation chart and it takes away a lot of the gains. Then look at personal debt level change that is at a fairly constant positive 4% yearly (HoC briefing paper) and you wonder if that is where that increase in spending comes from… which obviously acts to inflate wages a bit… enough to offset the increase in debt and/or inflation? You might add in government debt somewhere as well, and you could question if you should combine debt and inflation or if they somehow should exclude each other. I am, thankfully I think, not a statistician, so I get to go and close about twenty tabs on my browser now :-). Seems punk to me also.

Not even half as bad as Vancouver still. Vancouver seeing 40% price drops on luxury homes and minimum 20% drops on mid range homes.

Even condos dropping now, somewhere between 5-10% depending on price point.

At this point, Vancouver is the epicenter of the global housing bust, but I expect Hong Kong to assume that position pretty shortly.

Yes, HK has been a bubble for a very long time, held up by China. That party is ending…

And that housing bubble has generated nice GDP figures (while keeping

officialInflation© low). Now, that the tide has turned, the GDP signals recession. Who would have thought?BoC: do we cut or resort to outright robbery?

Once Vancouver reaches the “ghost city” stage prices will begin to free-fall.

15% increase in supply compared to this time last year was revealed recently on an ABC report. Prices have a little ways to fall still.

It doesn’t matter what Australia’s Central Bank does with the interest rate.

Many of the mortgages written up in the last few years are using foreign funds.

The Reserve Bank has left interest rates at the same level for years however mortgage lenders have increased interest rates and repayments to borrowers based on the overseas funds influence.

Household debt is much too high.

Condo sales are another sleight of hand. Building developers sell apartments to resellers who then on sell to retail buyers.

A sale from a developer to a reseller counts as a sale. Doesn’t actually mean it’s an occupied residence.

A likely change of Government soon will only accelerate the downward spiral of house prices if they get their policies across the line. Australia is no longer the lucky country. It’s stuffed.

Where’s ‘Lee’?

We sold in Melbourne about 3 months after the peak.

Not too bad a drop at that point, but VERY glad we did not wait 12x months.

Our old house is now worth about AU$60,000 less.

Now that you sold…..few tips

Don’t put your money in the stock market…..it will dive along with housing. Keep your powder dry…..Rent!

Check out:

Greaterfool.ca

Canadian Blog, and on the money.

The Big Four will sink along with housing. Gold in Australia does not attract tax if transactions are less than $5000….and for the last ~5 year, gold priced in AUD has not dropped compared to the drop in the AUD to USD….

So what exactly is causing this precipitous drop?

Reality.

In a word, as is often the case, CONFIDENCE!

I think the aussies were dolling out very “creative” loan programs over the past few years, similar to our run up in the 200’s:

interest only

40yr terms

arms

“stated income”

etc….

That coupled with the Chinese probably created this bubble.

Yes, the Crisis of the Third Century was just brutal.

More pump and dump. It’s horrible how “financiers” exploit people……

RBAs view that most people are still above completely ignores the fact that it is the marginal buyer that determines the price.

I read somewhere that during GFC it was “only” something like 5% of buyers that defaulted.

So what does it matter that most people have sufficient equity?

Correct … except the number I remember is somewhere around 10% of mortgages became delinquent.

It’s always good to remember that about 1/3 of homeowners in the US owned their homes outright without mortgages, and about 1/3 had paid down their mortgages so that there was no risk for lenders. It’s the other third … those that had done a cash-out refi or that had bought within a few years of the peak, which included many, many investors.

What if those who own their home outright, decide to take out generous HELOCs. Wouldn’t they be a risk to the housing market? After all the HELOC is backed by the property, and the banks are interested in quick sale rather than maximum profit.

Yes. But in a downturn, for the HELOC to exceed the value of a house that is otherwise free and clear, it would have to be a huge HELOC. Generally, people would rather re-mortgage their home instead of putting a huge HELOC on it. If they just want a normal-ish HELOC and they lost their jobs, they can sell the otherwise free and clear home, pay off the HELOC, use the remaining cash to rent until they find jobs.

Thankfully, HELOCs in the US have fallen out of favor:

Just a side note on HELOCs, you must still qualify via income and credit.

Not like previous decades where HELOC strictly based on equity

In the Financial Review the other day – 40% of Australian purchases in the last 2 years have been speculative short term “flippers” relying on gains to make payments. All of these are, or will be soon, under water.

At least 20% of these people have no chance of repaying and will default. It is believed that this number could well rise massively.

West Melbourne, and the Sandbelt regions as its known, Tarneit are almost entirely speculative land flippers – Uber drivers with 4 houses. The research on this done by Martin North etc is literally terrifying and makes Florida (The Big Short) and the strippers with 5 properties look like a conservative Swiss bank.

The elephant in the room is also speculative investment with superannuation.

Sounds like they made the mistake of the US in the 2003-08 years and look out below.

Thanks for posting all the great info., much appreciated, always a good read.

Reg