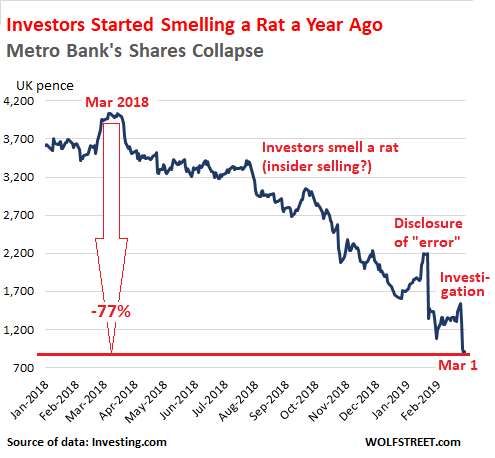

But (well-connected?) investors started smelling a rat 10 months before the first disclosure.

By Don Quijones, Spain, UK, & Mexico, editor at WOLF STREET.

Shares of the UK’s fastest growing high street lender, Metro Bank, are in free fall. They tumbled 16% on Tuesday, 25% on Wednesday and 6.86% on Thursday, to come to rest at a price of 889 pence, the lowest since the London-based bank went public in 2016. In the last five weeks the lender has lost 60% of its market cap and is now worth just £866 million, down from £4 billion a year ago.

The crisis began in earnest on January 22 when Metro’s shares crashed almost 40% — the worst one-day fall suffered by any British lender since the financial crisis — following an announcement by the bank’s management that it had incorrectly classified a huge chunk of commercial property loans and loans to commercial buy-to-rent operators that should have been among its “risk-weighted assets”. The “error” left a gaping £900 million hole on Metro’s balance sheet.

On Tuesday this week, things got even worse when the bank revealed that the Prudential Regulation Authority (PRA), the institution that had first flagged up Metro Bank’s accountancy error, and the Financial Conduct Authority (FCA) are investigating the circumstances behind the error. The bank also announced plans for a £350 million rights issue, after raising £303 million from investors last July. But investors — led perhaps by well-connected investors — have been smelling a rat since March 2018. By the time the initial disclosure whacked the shares on January 22, 2019, they’d already dropped 45%. Now they’re down 77% from March 2018:

Metro’s tribulations are a timely reminder of how important a force trust can be in the financial markets, particularly when it comes to banks. To gauge how much of a credit risk a bank could pose to market participants, including the bank’s bondholders and counterparties, investors rely on the bank’s capital ratio, which itself depends on the amount of risk assigned to each portfolio. By assigning a lower risk weight to its mortgage lending portfolio, whether by accident or intentionally, Metro left investors thinking it was safer than it actually is.

Now it needs to win back the trust it has lost. That could be an uphill slog for a lender that opened for business just nine years ago, becoming Britain’s first new high street bank in over 100 years. Metro is one of a handful of so-called “Challenger Banks” — small, nimble retail lenders created after the crisis to provide a little more banking competition in a country where the five biggest lenders control a staggering 85% of the market. Metro has had particular success at luring disillusioned clients from those banks. More than 100,000 new customers joined in the fourth quarter of 2018 alone.

Part of its appeal is its focus on physical branches — or “stores” as the company calls them — while most large banks are frantically closing theirs. Metro is also open seven days a week, and has longer working hours than other high street banks.

The lender even recently topped a Competition and Markets Authority (CMA) survey based on whether customers at the UK’s 16 largest current account providers would recommend their bank to friends and family, with 83% of Metro customers saying they would. Not one of the UK’s big four banks (HSBC, Lloyds, Barclays, RBS) made it into the top five while largely state-owned RBS came in rock bottom with a 49% customer satisfaction rate.

Unlike RBS, Metro Bank’s big problem is not with its customers; it’s with investors, counterparties and regulators. According to Bloomberg, Fidelity Investments, Metro’s second largest shareholder, has already reduced its stake in Metro Bank from 8.53% to 7.9%. Other big shareholders may follow. Another big risk is that other bank counterparties get cold feet, and refuse to make loans or close out existing credit lines.

Metro says it has already secured a standby underwriting agreement with RBC Capital Markets, Jefferies and KBW for the capital expansion, meaning the investment banks will have to make up the difference if investors are unwilling to pour more money into the lender. Metro also plans to issue around £500 million of bonds later this year to help ease capital concerns.

Metro hopes that this will be enough to calm investors’ nerves and stem the rout. It may be far too small a bank to pose any kind of systemic risk if it does go down, but its accounting blunder should serve as a timely reminder that when it comes to bank balance sheets, what you see is not always what you get. And if Metro does pay the ultimate price for its transgressions, its presence will certainly be missed on the UK high street. By Don Quijones.

The banks claim they’re complying with anti-money laundering regulations, but their customers beg to differ. Read… All Heck Breaks Loose After Spanish Banks Block Thousands of Accounts with Chinese Names & Folks Can’t Get to Their Money

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Yep [deliberately] failing to evaluate and categorize mortgage risk correctly – didn’t take long for one of these ‘new dawn’ challenger banks to adopt the methods used by their predecessors to maximize profits.

It’s endemic, chronic, and the whole industry is incorrigible.

I can’t speak for the UK but as far as US banks go, as bad as their ethics are (Wells Fargo is one example) they don’t actually seem to be much worse than the ethics of most of their customers. After all the bankers all came from the general population.

Old Engineer

Apparently old engineers not only can’t learn new tricks, they also forgot (didn’t know?) only Wells Fargo Bank managers & employees get paid bonuses for making/taking/stealing money from customers.

One suspects at least one old engineers comes from the “general population” that lives under slimy rocks.

Well, Mr. Chip, I believe you made my point. A society in which personal attack is viewed as an acceptable counter response in an argument or discussion cannot be said to have very high levels of ethics.

Saltcreep, below, however, provides a much more cogent response, and food for thought. I agree wholeheartedly with the first paragraph and with his conclusion. Where I disagree with him, and with you, is that it isn’t, as Saltcreep phases it just “…those who set the path of such institutions…” are totally responsible. Those who set the path don’t operate in a vacuum. And as we in the US are not in a dictatorship, if the the ethical transgressions in the banking, pharmaceutical, or the student loan business, to mention but a few, really bother most of the general population, where is the outcry? Where is the demand for change and correction?

It is this fact which so depresses me. The ethical transgressions of business and others simply don’t seem to bother most of the citizens of the U.S. And again, “…those who set the path of such institutions and who never have to face the consequences of their unethical choices…” have all come from a cross section of the U.S. population. It is an ineluctable conclusion that the ethics of the top is representative of the ethics of the whole population.

Now I’ve got to go catch some flies for supper.

Ethics have nothing to do with personal attacks, and, in limited circumstances, are sometimes justified.

Your stated opinion is there’s essentially no difference between a set of highly paid, incompetent and possibly criminal bank managers and the customers they steal from are laughably without foundation.

Darn right I dispute your personal opinion.

Old bank joke :

A guy walks into a bank and says to the teller at the window, “I want to open a f-ckin’ checking account”

To which the lady replied, “I beg your pardon, what did you say?”

“Listen up dammit, I said I want to open a f-ckin’ checking account right now.”

“Sir, I’m sorry but we do not tolerate that kind of language in this bank!”

The teller left the window and went over to the bank manager and told him about her situation. They both returned and the manager asked, “What seems to be the problem here?”

“There’s no damn problem,” the man said, “I just won 50 million in the lottery and I want to open a f-ckin’ checking account in this damn bank!”

“I see sir,” the manager said, “and this b-tch is giving you a hard time?”

Back off on the personal assaults here, mate. This site is not the place for bad behavior.

Or, OE, does perhaps a lack of self imposed restrictions in terms of ethical considerations allow some people to bypass more considerate and empathetic opposition, especially in industries where very short term achievements in financial terms determine whether you’re climbing or descending?

Anecdotally I know someone who was sacked from his job in London as a trader with a major bank during the 2008 crisis, and after getting back in again after the banks had been properly bailed out, said that during the interviews he did subsequent to the crisis, the one thing that clearly stood out for him was that all the banks he talked to wanted only to hear about maximum risk exposure.

What does that say about the ethical considerations of those who set the path of such institutions and who never have to face the consequences of their unethical choices..?

When is the last time a top level banker went to jail?

The W H Bush administration!

When there is no threat for jail no matter what financial crime you commit, then paying a “fine” (if caught) just becomes another business expense for FRAUD.

But, as an average person/customer, you go try to commit that kind of fraud. You would be in jail so fast it would make your head spin.

The is no moral or criminal hazard in banking with vast amounts of money to be made. What kind of people did they think the industry would attract?

Looks like the derivatives party is on it’s way!

So am I reading this correctly? The stock lost 40%, and then an announcement was made? That would appear to be a lot of insider trading

Countrywide repeat

never mind I read it incorrectly (several times)

Yup, no more Repo 105 for you. It’s not a sale, it stays in your pregnant balance sheet. The old Lehman trick no more.

A small accounting error in a bubbly market where everyone is watching for black swans. No problemo for financial stability, just like Northern Rock.

“the London-based bank went public in 2016.”

Begs the question, are public markets simply a convenient dumping ground?

Does the Uk have insider trading legislation?

Banks are untrustworthy. Maybe they should be regulated.

When the banks are nationalized, then they’ll be regulated.

The spikes just before the announcement of the “error” and of the investigation both look a bit like a pump n dump of someone trying to get out.

Who were the auditors that signed off on the accounts? why aren’t they held to account?

Jason,

1. PricewaterhouseCoopers (PWC)

2. I’ll let someone else answer that.

PWC signed off assurance on the 2018 half yearly report, but the full year report ( Results presentation fy 2018 pdf at https://www.metrobankonline.co.uk/investor-relations/ ) says RWA changes were notified in Dec 2018, and a “big four” company is taking up wider oversight. Dec 2018 saw their shares surge? There have been changes in audit law, some banks have changed auditors, are obliged to now each decade in UK I think, in EU each two decades… so maybe new auditors signalled ?

There is an investigation underway, not that it will nescessarily hold anyone properly to account.

?

what I was told was its a structurally unprofitable business (small retail bank), so they moved the RWA charge on bridge and dev loans down to mortgage level (100-150% down to 20%) so they could lend more of the most profitable area. PRA will just fold them into another bank with equity zeroed. C-Suite are in big trouble.