During the selloff in December, the BOJ shed $31 billion, but in January it piled on.

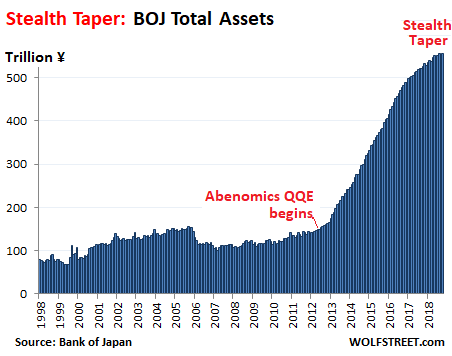

Total assets on the Bank of Japan’s mammoth balance sheet, after a drop of ¥3.4 trillion ($31 billion) in December, rose by ¥4.8 trillion ($44 billion) in January, to ¥557 trillion ($5.1 trillion), the BOJ reported this morning. This shows two things:

One: The balance sheet is now 101.5% of Japan’s nominal GDP (¥549 trillion, not adjusted for inflation), which makes it over five times as large in terms of the economy as the Fed’s $4-trillion balance sheet, amounting to 19.6% of US nominal GDP ($20.6 trillion). This is how crazy the situation at the BOJ has become:

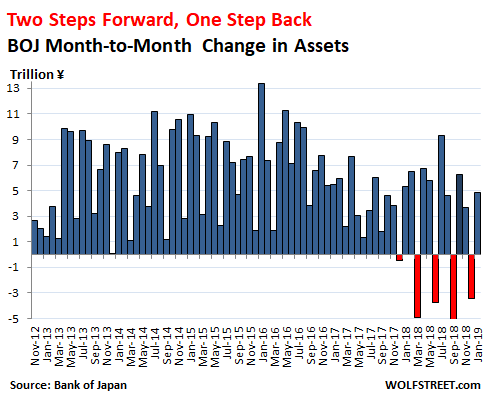

Two: The BOJ is now proceeding with its QQE – “quantitative and qualitative easing,” as it calls this monster – in a special sort of dance: Two steps forward, one step back – increasing its balance sheet two months in a row, then in the third month unwinding about one-third of the increase of the prior two months.

This dance series started in December 2017. December 2018 had been the fifth step back. And January was the next step forward. Among QE-besotted central banks, this dance is unique. This chart shows the month-to-month changes of the balance sheet. Note that the December “step back” was maintained despite the selloff in the markets:

The above chart shows that last December, the BOJ cut its balance sheet by ¥3.4 trillion ($31 billion), a larger cut than the Fed’s QE unwind in December ($28 billion). In September, the BOJ chopped its balance sheet by ¥5.4 trillion ($49 billion), larger than the Fed’s QE unwind in September ($34 billion). The prior two balance sheet cuts (March and June) were also larger than the Fed’s QE unwind during those months.

And each of the BOJ’s reductions undid between 30% (June 2018) and 42% (March 2018) of the prior two months’ increases.

The switch from regular QQE to the two-steps-forward-one-step-back QQE came without any announcement from the BOJ, which continues to say that “QQE with yield curve control” – the BOJ is targeting the entire yield curve, not just short-term yields – will be maintained for as long as needed to achieve 2% inflation.

It did add a couple of rubbery terms in its minutes of the July 2018 meeting: “sustainability” and “flexibility” of QQE. According to the minutes, the BOJ’s staff “proposed measures to enhance the sustainability of the current monetary easing” given, “for example, their effects on financial markets.” And the minutes also said that the BOJ would buy Japanese Government Bonds (JGBs) in “a flexible manner.”

But the minutes reiterated that the BOJ would increase its holdings of JGBs by about ¥80 trillion a year, which the BOJ has not come anywhere near since 2016, as we’ll see in a moment.

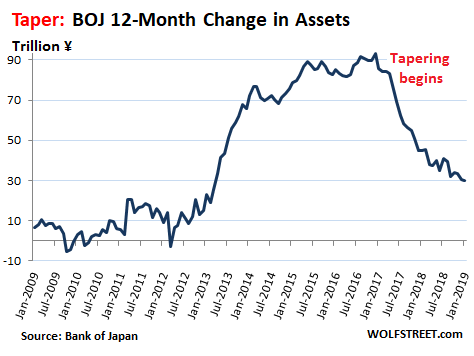

QQE started in December 2012 as part of Abenomics. During peak QQE, in the 12-month period ended December 31, 2016, the BOJ’s assets ballooned by ¥93.4 trillion. Over the most recent 12-month period ended January 31, 2019, the BOJ added only ¥30.2 trillion to its balance sheet, the smallest such gain since March 2013:

In percentage terms, the BOJ increased its balance sheet by 5.7% over the 12-month period ended January 31, the smallest percentage increase since May 2012, before QQE had even begun.

The BOJ has been buying mostly Japanese government securities (JGBs and short-term bills). But it also buys some equity ETFs, Japanese REITs, and corporate bonds. Japanese government securities are the largest asset class on the balance sheet. The amount of these securities rose in January by ¥3.9 trillion from the prior month, to ¥471.5 trillion.

This amounts to nearly 50% of all outstanding Japanese government debt – up from about 14% in late 2012.

For the 12-month period ended January 31, the BOJ added “only” ¥25.4 trillion of JGBs and bills, a far cry from its assertions that it would add ¥80 trillion a year. It has not added ¥80 trillion of government debt since the 12-month period ended April 2017.

Clearly, the “QQE Taper” is well underway, despite whatever the BOJ may proclaim to keep everyone guessing.

The Fed has already reduced its balance sheet by over $400 billion since the start of its QE unwind in October 2017 and for now continues to run its QE unwind on automatic pilot.

The ECB tapered its massive QE to zero as of December 2018 and is currently only planning to replace securities when they mature to keep its balance sheet roughly level.

And in 2019, markets are facing a situation for the first time in a decade where the big three QE’ers – the Fed, the BOJ, and the ECB – will on net whittle down ever so slowly the assets on their combined balance sheets, with the BOJ continuing to add a smidgen, with the ECB maintaining what it has, and with the Fed continuing its roll-off.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Central bankers are without any doubt the most powerful persons in the world nowadays, elections are irrelevant. They can do this because money is not linked to any tangible value.

Clearly there is no restraint to how much money they can print, they can own the world without lifting a finger. Those are interesting times to say the least and I wonder how the monetary experiment will evolve…

Wolf, if the FED increased their balance sheet from 800b to 4.5trillion and only shed 400b, is it correct to say that the FED monetizing 3.3trillon of government debt in less than 10 years ?

Kind of but it’s not that simple because some of it goes back out as “currency in circulation” (the paper dollars in your pocket and stuffed under mattresses in other countries). Currency in circulation is a liability on the Fed’s balance sheet.

So the amount of debt actually monetized in 10 years is smaller than $3.3 trillion, but it’s still big.

In terms of currency in circulation, there is part in this article that explains it, including charts:

https://wolfstreet.com/2019/01/11/feds-powell-balance-sheet-to-be-substantially-smaller-how-small-he-gave-big-clues-my-dive-into-dynamics-w-charts/

Book:

“The Federal Reserve System Purpose and Functions 1963”

THIS fifth edition of The Federal Reserve System: Purposes and Functions commemorates the fiftieth anniversary of the signing of the Federal Reserve Act by President Woodrow Wilson on December 23, 1913.

As with earlier editions, the book is dedicated to a better public understanding of the System’s trusteeship for the nation’s credit and monetary machinery.

This edition, like former ones, is a collaborative product of the Board’s staff. Ralph A. Young, Adviser to the Board, was responsible for coordinating and supervising the staff work that went into its preparation.

Board of Governors of the Federal Reserve System

Washington, D. C. December 1963

“Money and Near-Moneys In the United States circulating paper money and coins of all kinds (currency) and the demand deposits held by commercial banks perform all the functions of money. When a person has $10 of paper money and coin in his pocket and $100 in his checking account in the bank, he is in a position to spend $110 at any time. These two sums represent his active cash balance; they serve the same general purpose, and each can be converted into the other at any time; that is, currency can be converted into a demand deposit by taking it to a bank, and a demand deposit can be converted into currency by taking it out of a bank.”

book page 6/7

pdf page 27/28

https://fraser.stlouisfed.org/title/4518

Good luck with that “demand deposit…converted into currency” regulation. You’re better off raiding the ATM every night, little by little.

I thought the qualitative easing was Abe’s “third arrow”? Looks more like a frickin’ boomerang. This is insanity to the nth degree. We are so screwed.

Increased “currency in circulation”

Sounds like currency inflation to me.

With an official policy of currency debasement and outright monetizing of government deficit spending I don’t know how much longer confidence in these currencies can hold. Once people lose confidence the currency becomes one big game of hot potato and after that happens there is no turning back.

I lived this in Brazil in the 90’s (care for Cruzeiros anyone). The government gets away with printing currency for a time and they believe they have discovered a golden goose, they get lulled into believing there really is no consequence to monetizing debts – but it doesn’t work. People who worked and saved for a lifetime lost everything. Lucky for me I had very little to lose at the time – the same is not true today.

The free lunch politicians and bankers are attempting to steal has made me angry and bitter – this is not my nature they made me bitter and resentful with their massive inflation-tax policy.

Always enjoy your comments Van and share your outlook. “Emerging” countries might be a different story but for the Western countries, don’t hold your breath for the populace to wake up anytime soon and see the CB money printing for the root cause of many of their worries.

In conversations with friends about the ills of our time, when I bring up CBs and money printing faces go blank and quiet. And these are often highly educated people with PhDs, uni professors, people with London City jobs, though mostly not economists (for better or worse). The middle and upper middle classes seem most beholden to MSM narratives. They look down on the lower classes with their unenlightened beliefs in “conspiracy theories” and they hold on to that distinction.

As respectfully as I can I want to add to what WR saiid about paper dols – USD – abroad, that I think it’s also about the Fed not having control over electronic USDs abroad . There are many more electronic ones than paper ones.

I’m thinking about the Eurodollar, and I recommend Eurodollar University by Jeffrey Snider. It’s intellectually challenging for a non finance pro like myself, but well worth sticking through it.

I find the term “dollar shortage” a bit curious when just about any bank anywhere outside Iran can print USDs via the keystroke method, but what do I know, a non pro amateur?

Sure, the Fed can create multiple EM currency crises, it has, and can cause a tsunami of USD loan NPLs devastating the world banking system, but I don’t call that being in control.

Then the real doozey, when the Fed does Godzilla QE and you’ll need a a wheelbarrow full of computers and smartphones to buy a pack of gum.

The world will be super happy, its USD debt gone poof!

Wolf, if the $2.4 trillion in circulating currency evolves over the next 5 years as you predict, that’s $11,000 in CASH for every man, woman and child in the U.S. Heck, over half the population couldn’t put up $500 if their life depended on it. That’s probably going to create some inflation, yes? At that point, it would seem rather ridiculous to start any new QE program? Politicians might just become a target….

Much of that cash is overseas. Entire countries run on it. Drug traffickers hoard it, etc.

(also, I said that there might be up to $2.2 trillion, not $2.4 trillion, in five years if the current trends continue).

It’s nuts. These Central banks create far too much liquidity in the Global Financial System. That is one of the main reasons why bond and equity valuations have remained so high year after year.

I wasted my time talking college classes in the Pricing Of Securities. There is no such thing as intrinsic or fundamental value anymore.

Japan buys equity ETF”s. Norway’s Central Bank owns global equity ETF’s with a total value higher than it’s ($400bn) GDP. Other oil rich Arab nations gorge on FAANG stocks.

I honestly believe that the FED will be handed the power by Congress to go in via POMO and buy equities when the next severe recession hits.

The global 1% watch the S&P 500 likie a hawk. It has become a perfect proxy for ALL global assets. All assets are moving in lockstep.

December 2018: >90% of all global assets lost value

January 2019: >90% of all global assets gained value. .

“I honestly believe that the FED will be handed the power by Congress to go in via POMO and buy equities when the next severe recession hits.”

Uh-huh. Of course, what’s to stop the Fed from buying stocks now and maybe they have already?

The law is as the law does, and the Fed is as the Fed does. I could site dozens of things that are illegal that the Govmit is doing right now.

The Fed could have accounts in Switzerland and own lots and lots of stocks for all we know.

And Switzerland government itself buys stock. Think it owns a lot of Apple…and I’m so very sorry for their loss (not).

Yellen proposed buying stock in the next downturn, as I have the quotes posted on my wall to remind me to turn off my logic, and BTFD when “THAT” happens. I’m guessing they will mimic Japan and buy index ETFs at first, then “TBTF” big caps.

Ironic that central banks do not see the unintended consequences of having 0.10% of the world population own 90% of net wealth (per Ray Dalio), or having the top 10% of Americans owning 90% of stocks. For the 99% of the population not living the QE dream, there is no difference to them between Quantitative Easing and “Modern Monetary Theory”, except the easy to understand fact that the bottom 90% will profit from MMT vs the top 10% currently profit from QE. Sure to be a terrifying election cycle for Wall Street in 2020, so enjoy the market Euphoria while it lasts…

Per https://www.reuters.com/article/us-usa-fed-yellen-purchases-idUSKCN11Z2WI

SEPTEMBER 29, 2016 / 3:44 PM

Yellen says Fed purchases of stocks, corporate bonds could help in a downturn

WASHINGTON (Reuters) – The Federal Reserve might be able to help the U.S. economy in a future downturn if it could buy stocks and corporate bonds, Fed Chair Janet Yellen said on Thursday.

Speaking via video conference with bankers in Kansas City, Yellen said the issue was not a pressing one right now and pointed out the U.S. central bank is currently barred by law from buying corporate assets.

……………………

Last post for me at WS for me. I simply get blocked repeatedly (including my rely above…)…and after reviewing all the rules, I have no idea why. Plenty of smart folks here, yet not as open minded as one might believe…

Good luck in all your investments in life,

secant

secant,

Concerning the comment that was in moderation. It discussed MMT — and thereby automatically goes into moderation.

MMT is an economic religion. If you believe in it, fine. But I don’t allow proselytizing on this site. Hence I review every comment about religion before it is released. MMT trolls are everywhere. And I block them. All they do is promote MMT. Copy and paste. If they want to proselytize, they need to do it elsewhere. However, upon review of your comment, when I finally got to it, I released it as it was borderline proselytizing.

Very true: MMT-ers are the fanatical Vegans of economics blogs…..

No quibble with your “MMT as a religion” stance, but what about capitalism? Most folks here worship at its altar.

Yeah, I try to discourage discussions of these systems (the “-isms”) here too because the discussions are always the same. But at least I have not run into the mob of trolls that I run into with MMT.

Norway’s wealth has got nothing to do with any central bank manipulation – it’s real earned money they are spending, which they gained by keeping over 80% of their oil revenue for the nation and using it to build a vast sovereign wealth fund.

Very sensible move – and spectacularly successful too. Massive wealth created for the benefit of everyone, not for the gilded few.

Proper social democracy in action, rather than ripping up the social contract, glorifying greed and running one’s country as a playground for financial speculators (ie the neoliberal financier ethic).

… but how much did they gain back in Jan.? It happened too fast according to Bloomberg. Markets are falling again. How far this time? That was a bear market rally methinks…

This months Fed roll off (QT) is set to occur on Wednesday the 20th.

Slated to roll off:

$23.3 billion UST

$7.7 billion MBS

Thats only IF the Fed keeps it (QT) on auto.

They’ll probably do it as long as they dare, because if they don’t the shouting WHY!!! will be deafening!

Amazing the BOJ has been able to reduce their balance sheet without affecting interest rates. Is that implied connection in the US Fed roll-off a red herring? By this time next year I think the BOJ will be targeting 2% deflation.

In the last couple of months the BoJ increased its assets by $200B. And the EU picked up some more as well. Pitching in to help. Always more where that came from, apparently.

Just realized my comment regarding BoJ asset purchases was not consistent with Wolf’s report. My comment was based on Yardeni’s report, and Wolf is probably right.

Dale, your number is not far off my number. But this is the gain over the 12-month period, not one month.

The BOJ increased its balance sheet by ¥30.2 trillion yen over the 12-month period ended in January (my third chart). This amounts to about $272 billion over the span of 12 months.

On a monthly basis, go to the first chart. It shows that the BOJ CUT its holdings by ¥3.4 trillion ($31 billion) in December and then RAISED its holdings by ¥4.8 trillion ($44 billion) in January.

That will be a scary poker game to watch, the central banksters raising that target on each other.

The quality of a man’s mind can generally be judged by the size of his wastepaper basket.

José Bergamin

I think we may be near a situation where populations take a close look at all the government debt out there, as well as retirement and health care promises, then realize that a decent share of the debt and promises cannot be satisfied without induced and intentional hyperinflation. At that point, people will not want to own any government debt, especially if the interest rate is low like today. This could force a dramatic worldwide financial debacle that could be devastating to the economy and asset prices.

Interestingly, the problems are apparent through application of simple math. In the US, for example, the booked debt and unfunded liabilities are estimated at $140 trillion. GDP is only $20 trillion, and government tax collections are only $4 trillion annually. Thus, the government has a debt to income ratio of 35 (or 150/4). Would you give a $350,000 loan to another party that had income of only $10,000 per year, during the “good” times?

I think the US total is 200 tn.

Or will the IMF rescue the world with the SDR, and the high-debt developed countries just have multi-decades of no-growth, like Japan?

I keep hearing market commentators claim that the Fed will be more limited in ability to respond to crisis or market dislocation because it will be starting with lower interest rates and a much higher balance sheet. While interest rate reductions will be more limited this time around, doesn’t the example of Japan show that the upper limit to how much QE the Fed can do is very far away? If they want to ease in a big way, they could just expand the balance sheet to something like $25 trillion, right?

Yes you are correct, they can own every single asset in this country because they control the printing press. When all assets are owned by the FED, the only difference between the Fed and the communist party will be a matter of semantics.

What happened to the good old schumpeter’s creative destruction that served our economy so we’ll before?

Suere, and destroy the USD,,,

Sure, but then you need the government to run deficits of $25T so that the Fed has government debt to purchase. Don’t you think printing $25T would create tons of inflation and instability, plus even higher wealth concentration?

If economic distress could be resolved by simply printing money via QE, it would have been implemented centuries ago.

You are a genius, and I mean that in a very good way…

The only reason the US can do this is because the USD is the world reserve currency and every potential alternative is more untrustworthy, either because of more debt, e.g. the euro and yen, or an opaque economy, ie the yuen

In the 1980s, the USD came close to losing its status as world reserve currency. Interest rates were still high. Reagan’s tax cuts had massively (for the time) increased the Federal deficit. Funding trillions of dollars every year was not so easy, and paying interest on that debt was approaching ONE THIRD of the Federal budget. Plus the Fed govt had to bail out the Savings and Loans after they got deregulated and went berserk with bad debt.

And so HW Bush had to break his “read my lips” promise and raise taxes. Republicans abandoned him for Ross Perot. Clinton won and raised taxes again later.

Surprise! The economy still boomed like crazy, thanks to the early years of Greenspanomics. With the booming economy and higher taxes, the Federal deficit shrank to almost nothing. So much for the Laffer curve. So much for the worrisome Federal deficit.

The last time the US was truly swimming in such an ocean of debt was WWII. The US govt had to hold patriotic War Bond drives to get ordinary Americans to fund that debt. Rich Americans were already being taxed at 90% marginal rates. The USD was not the world reserve currency.

See how important it is for the USD to be the world reserve currency?

We are living in a bubble created by a confluence of national and world economic policies created over the last decade, Something is going to pop that bubble. Asset inflation (think tulip fever) and mountains of bad debt always end up collapsing.

The crazy Federal deficit will be easy to solve- raise taxes. And that will happen, sooner or later

The more worrisome question will be what happens when that mountain of bad debt finally collapses, taking down pension funds, banks, who the heck knows, maybe even Goldman Sachs.

Despite all the cynicism here, I just don’t see Congress allowing the Fed to bail out an investment bank like Goldman Sachs again.

Having the reserve currency is double edged sword, first good then bad. It would be better, at least as long as we still have the fiat system, to have an international currency like the SDR. Then the reserve currency isn’t tied to the fortunes of one country.

Taxes can’t solve this, and not only because it’s political sucide raising them. You simply can’t raise enough money that way to resolve the humongous imbalances of today. Taxation only steals purchasing power and reduces the ability to invest. Govts can raise money via bonds, and those with excess cash can get a return which then drives the economy.

Tell me what’s the difference between modern day Central Bank QE and the Weimar Republic.

Modern day bankers can purchase treasuries to keep interest rates low, and then let the treasuries roll off the books. The balance sheet is expanded, but there is no hyperinflation.

The Weimar Republic simply printed paper money causing hyperinflation.

As crazy as what the BOJ is doing, it does give one solace that our central bank could continue with QE expansion and still have minimal inflation. Eventually things will end badly for Japan, but we may follow a similar path due to trailing demographics, and although there will be persistent economic pain, it appears a collapse or catastrophic reset can be postponed for decades, by which time, as Keynes has opined, in the long run, we are all dead. Comforting, isn’t it?

In a sense. However the purchase of treasuries by the central bank is monetisation, you only have to look at QE and demand deposit or M1 figures to see this. Inflation follows money supply, interest rates follow inflation, in a traditional model. However you can have increased money supply used to inflate out of deflation only, to say the 2% CPI target…in theory. The suppression of natural rates, where we are talking of the fed controlling rates downwards in an upwards natural environment, is seen in principle to be by reverse QE. That is to say by shrinking the money supply to stall inflation. Now, that that reverse QE actually increases rates points out that the value of money is currently set by control of availability, not so much by increased quantity in circulation. This works by under allocation of supply as compared to that which is already in demand, that being the pre-existing commitments of the financial system, for example, and also using standard fed rate setting measures within the banking system.

Therefore the question arises of how the fed would actually respond to inflation caused by loss of faith in the currency, which could also be understood as “oversupply” or distrust in worth. Would it reverse QE into physical currency for example, or implement other legislative controls. Would it purposefully inflate “out of” the circumstance and then reset. Is it actually doing that now under the guise of a 2% target even, subtly re-concentrating real wealth as society simmers?

For now the management has walked a line that has kept the system somewhat coherent, that has maintained a certain credibility in the whole. However as your or anyone else’s confusion at the above paradox will tell them, it is a very fine line to walk, and one that must be traced out into the unknown with so many parameters that, beyond total control of the whole, it would still remain partly a guess, which therefore it is. A switch of paradigm to rates set by base monetary inflation, or lack of central control of that circumstance, would simply write down all previous effort and success as in vain, in terms of creating some acceptable monetary political economic social order. In fact we do not exactly know what is trying to be achieved, or if we are subject to total improvisation even.

People trust what works, when it no longer works, they don’t trust it and lose faith in it.

Does modern money run on faith alone?

At the expense of over-posting,

“Now, that that reverse QE actually increases rates points out that the value of money is currently set by control of availability, not so much by increased quantity in circulation.”

needs clarification. M1 has been on a tear since 2008. It did not reduce during taper, it has not reduced during unwind/reverse QE . It has its own solid increased rate of change since 2008. M1 is currency and demand deposits, which is cash and “as good as cash”.

In short, we have seen rate changes and market volatility, but we have NOT seen reduction in amount of M1 currency take place anywhere yet that has practiced QE. That is why I have doubts on the actual ability of central banks to handle inflation downwards in certain circumstance, as well as why I question the wisdom of QE or the idea that it represents a kind of solution.

To be clear, the paradox can be summed up as that the idea of issuing more money via debt by the artificial lowering of rates, where when rates are then artificially increased and fed into the market by the weight of new or increased debt, that also brings an increase in money supply as treasuries are both interest bearing and underpin further finance as well as being eventually money spent , that you can expect anything but a marginal ability to only slowdown the devaluation of the currency. It is a paradox because in reality it all seems a one way street, as to go further by actually reducing M1 would appear both confiscatory, as well likely to bring down not only faith in the currency, but its value and that of the economic system, which in other words would lead to further devaluation of that currency, not the strengthening of it that would have been sought.

Yes, the central bank(s) could theoretically continue with QE expansion, even if it never achieves its stated short term goal. In fact in Japan’s case, under its QE policy, the economy continued to contract by ~$1 T in eight short years. Keep in mind that in Japan’s case, the central bank is buying govt debt, PLUS private corporate debt, stocks and (commodities?). Same with the SNB.

Janet Yellen et al suggested a similar path for the FED- to buy stocks, corporate debt, possibly commodities, maybe even goods. But when this policy fails to achieve its stated goal, the next phase would be printing money (currency) outright. Is it unreasonable to foresee “simply money printing”? Not really.

It’s more complicated than just the difference between printing money vs expanding the money supply with QE.

The Weimar Republic was in a hostile and subservient relationship with its primary creditors – France and Britain. Crushed by the burden of war reparations for WWI, the Weimar Republic simply printed more money. If it had done some sort of QE, financiers in France and Britain would almost certainly have viewed it the same way, and devalued the Papiermark. The devaluation raised the cost of imports to Germany and started the hyperinflation.

Had Germany won WWI, its military dominance over France and Britain could have allowed it to force the two countries to accept whatever overprinted or QE inflated currency it wanted to foist on them. That is actually what happened in the early triumphant years of the Third Reich to the countries it conquered

The current situation of the US, which runs perpetual huge trades deficits with countries dependent on the US for their military security or for a huge part of their national economies, is somewhat similar. They have to take our money or else

You gave us the answer, a big, fat, humongous ZERO!!!

Hey Wolf –

What would happen if the BOJ just cancelled the bonds on its balance sheet?

I get that monetizing debt is bad when it causes inflation, but a) here it doesn’t seem to have caused inflation (asset price inflation, sure) and b) they’ve *already* monetized the debt by buying it and parking it, it doesn’t seem to be a large additional leap to simply cancel it out instead of the Japanese treasury department “repaying” the bonds that they sold to the BOJ in exchange for money that they materialized out of thin air. The whole thing is fake so what’s the further harm in right-sizing Japan’s balance sheet while they’re at it? Is there something I’m missing?

No need to cancel them. Interest is close to 0%, plus or minus, so it’s not a big deal. Most of the interest the BOJ earns, it remits back to the government (as does the Fed). So once the BOJ has the bonds, they’re no longer a burden for the government.

So do you see an upper limit on the BOJ’s balance sheet where the end result is a rapid currency depreciation?

nearlynapping,

At this point, what choice does Japan have?

Japan, by far the most over-indebted country in the world in relationship to its economy, has decided that there will be no “debt crisis,” imposed on it by the markets. A debt crisis would force Japan to brutally cut its budget for social services and raise taxes by large amounts to make ends meet.

Japan has decided that it would never come to that. Instead, there may be a currency crisis or an inflation crisis, or both, which would spread the pain more evenly.

Japan can weather this type of crisis better than other countries because it has a large trade surplus and a large pile of foreign exchange reserves, though it would whittle down the wealth and purchasing power of the people. So this type of crisis will be kicked down the road for as long as possible. And that could be quite a while.

What Japan will never have is a debt crisis since the government bond market is in total control of the BOJ and large government-backed institutional holders (pension fund, etc.). Given the extent of its control over the market, the BOJ can now ease up on buying these JGBs. But market forces will never be allowed mess with that market.

The rule I have with Japan’s debt situation, is this: so far, so good.

I have no idea how long this can be kicked down the road. I assume the plan is to drag this out long enough for the generation that caused this to peacefully pass away and let the younger generation deal with it. So this could be a while. These folks live a long time.

Wolf,

Would Japanese see any benefit from buying gold prior to the ‘lost decade’ and all the money printing from BOJ?

Back in 1986 the Mint of Japan issued large quantities of “Chrysanthemum” 100,000 yen gold coins which were in super-hot demand. The gold in these coins was worth about 40,000 yen so the Japanese government pocketed a nice profit.

Now, these coins had a peculiarity: they were redeemable at face value.

While the Japanese economy was going from strength to strength nobody cared, but after the Nikkei 225 peaked in early 1990 and the great unwind started, people started bringing their coins at Bank of Japan offices to redeem them for cold hard cash.

I am not talking starving families bringing in a couple of coins to have a little money to buy food, but all sort of characters trying to redeem hundreds or even thousands of Chrysanthemum coins for cash at once.

To make matters worse while gold hadn’t exactly nosedived since 1986 it was still down about 10% in yen terms, meaning each Chrysanthemum coin contained only 36,000 yen of gold against a face value of 100,000 yen.

It was a mess, especially in an image-conscious environment such as the Japanese government and bureaucracy. The Bank of Japan was losing money on each coin but at the same time could not simply stop redeeming coins. That’s where the nastiness started.

The Bank of Japan started accusing foreign brokers and coin dealers, chiefly based in Hong Kong, Macau and Switzerland, of having “flooded the market” with hundreds of thousand if not millions of counterfeited Chrysanthemum coins against an official issuance of roughly 11 million. Fingers were pointed, the Interpol was brought in and lawsuits began flying across borders.

You can well guess what happened next: the Bank of Japan was found to have at best exaggerated wild rumors and at worst to have fabricated charges outright. Brokers and dealers sued for damages. In at least one case in Hong Kong the Bank of Japan paid extra damages to avoid having to publicly issue an apology.

That was the first, and last experience with gold for many Japanese.

So did the Yen appreciate vs USD in Dec 2018 because of the BOJ shedding assets or was it a flight to quality as the US markets sold off?

The yen is at 110 to the USD, same as when I went to Japan for the first time in 1996. The little ups and downs are temporary.

Japan is quite interesting for a number of reasons.

There are a couple of instances which the pundits in the West seem to gloss over or completely ignore when discussing Japan. And I’ll give an example of Japan, Inc addresses a problem by just changing the rules.

Two of these involve flow of funds. I’ll use that ‘110 to the USD’ as an example.

Prior to the big bubble Japan the Yen plodded along at much cheaper values. When I first lived in Japan the rate varied from 260 to 270 yen per dollar which made Japanese exports ‘cheap’ and imports relatively expensive.

It also made purchase of assets overseas quite expensive.

Then you had the huge fall in the US$ and increase in the value of the yen to the mid 80 area before the bubble burst and then a fall and then an increase into the mid to high 70’s around 2011.

This huge increase in the value of the yen created all sorts of distortions and opportunities – remember all the purchase of assets overseas by Japanese?

Some were real duds; others weren’t. The Japanese were able to basically buy foreign assets for 1/3rd of the price compared to the 80’s. I also think this huge outflow of funds also helped alleviate massive inflationary pressures in the domestic economy.

This spike in the value of the yen also led to the bubble and subsequent bust – which IMO was more related to domestic structural problems and tax regimes in Japan than more people realize.

Then along came Abe with Abenomics. Japan was in trouble and Abenomics forced the market to revalue the yen. It went as low as 125 or so to the USD. This made all those wonderful assets purchased with cheap dollars so much more valuable in cheap yen. It allowed repatriation of earned income in interest and dividends at much better rates as well as getting rid of lots of book losses on those assets as the yen increased in value.

This was particularly important for many of the insurance companies in Japan who had piled in foreign bonds and were sitting on massive losses.

(As an aside way back when Japanese life insurances companies used to offer whole life policies with indicated returns of more than 5%. Once the yen exploded in value and the losses amounted to their foreign holdings as well as interest rates falling in Japan, they were no longer able to service these policies. No problem, the government ‘forced’ a unilateral change to allow the insurance companies to void those contracted rates of return. If you had a policy instead of getting 5% you basically got zip. All legal and a huge loss in accumulated wealth for many.).

The next area also relates to the above. When the big earthquake hit Japan it not only affected Japan, but the markets across the world and in particular the energy markets.

All of the sudden the Japanese turned off all of their nuclear plants which caused a huge strain on the domestic economy as well as energy markets across the globe.

Notice that nice spike in crude prices in April 2011? So not only did you have the yen falling like a rock, but energy prices spiking to high levels as well which had huge impacts on the flow of funds out of Japan to purchase needed fossil fuel supplies.

(IMO Japan needs to get rid of nuclear plants, but to have undertaken that action to shut them all down at once was IMO one of the dumbest economic moves I have ever seen.)

Anyway that spike in oil prices lasted until about he middle of 2014 and the proceeded to fall all the way down to the mid 30’s in January 2016.

These extra imports of fossil fuels cost Japan an extra US$30 to $45 billion a year.

As these reactors restarted and some investment was made in renewables, it greatly affected those flows of funds and the value of the yen. As more come on line the extra demand for crude and coal will be reduced and impact on the price of oil, coal, and LNG.

Lastly, if you ever get a chance to visit Japan and take the Narita Sky Access Train train (Keisei Line) from Narita to Tokyo, take a look outside as you go from Komuro Station and approach Chiba New Town Chuo Station. You’ll see a 10 kilometer long solar farm along the tracks. This is the SGET Chiba New Town Mega Solar Power Plant”.

As Japan imports most of its energy these type of renewables make a lot sense for them, but unfortunately for most people there the price of panels and systems is ridiculous.

Huge solar farms have been built all over the country as the companies have the ability to source cheap panels and inverters, but individual rooftop systems on houses in many areas lag. In Chiba Prefecture you will see quite a few. In Yokohama, very few.

Japan could reduce its fossil fuel energy imports by huge amounts to reduce its energy dependence on other countries. Why it doesn’t shows how strong the established powers are.

Thanks Wolf. I understand that Japan has chosen its path and that they have no choice but to continue with the can kicking. I just struggle with conceptualizing the pure fantasy and of it all.

This is because long duration bonds mature quarterly. There is no two forward one back, it’s just due to uneven maturities.

Ha, are you saying they just started maturing quarterly on Dec 2017? Look at the chart again: this is a NEW phenomenon.

Japan is analogous to a wildly insolvent bank, funded by wildly asleep depositors. Everything is copasetic right up until the depositor line forms, and then you’re done. They will transition from fine to cooked faster than one of their bullet trains. The question concerns the spark that will summon the phase change.

There’s probably another way to look at this — the other side effects of QE and the Fed (or central banks) large balance sheet.

If you remember during the 2008 GFC the problem morphed from bad mortgage backed securities to inter bank repo freeze then eventually to money market and commercial paper markets dysfunction. Parties didn’t trust the collateral presented them.

Fast forward to today, the big banks are awash with reserves and they are at the Fed — meaning it’s high quality. Same thing, the amount of Treasuries auctioned, they are high quality collateral that can be used for SFOR.

So there you go. Debt is now secured with Fed reserves or treasury. The best collateral (other than physical Gold). You are witnessing a transformation so get used to massive reserves and treasury bills. Actually, this is better than unsecured debt and bs paper. Now, at least the govt backs it. Who knows, maybe we private citizens can also lend our t-bills overnight some day. It’s a brave New world.

The government backs it (debt) ” says it all maybe.

Apart from being allowed to perpetually pay off debt with…wait for it…more debt, which works wonders when it comes to questions of solvency, exactly what does government have that is asset-worthy?

Some real-estate, but that is a national asset not for sale (except in Europe ).

Military assets, but those are not mercenary, at least in theory.

Tax-payers, but those will rebel if used to pay off government debt.

Votes, but even those cost money, your future debt.

The difference between a guarantee of solvency and solvent use probably.

Don’t forget the best trick in the books — inflating off the debt.

Usually that gets a lot of folks borrowing.

Yet another benefit of abandoning the gold standard. System low on reserves because of financial proflifacy? Just manufacture a few trillion $ more from thin air. Problem solved! Until of course the underlying assets of the reserves are no longer trusted.

And meanwhile the Eurozone refuses to do their own unwind and to raise rates… hence why I keep saying Brexit might have good long term effects for the UK but don’t expect anything nice for short and middle term.

The Eurozone WILL have to raise rates eventually unless they want to lose a lot of investors money.

When and how that will happen? I have no clue.

As a general rule what you have seen when QE is in place is debasement and weaker currency and when QT is in place a stronger currency. Thus you should be positioning for a stronger yen, likely through 105 by summer. This is against consensus and thus likely right also. I am positioned for such.

Central Banks playing hot-potato in the financed economy.

Central Bankers are doing the only thing they know.

Create credit/debt out of thin air.

It is their solution for everything!

Wolf, Japan is one country, and they say the world is becoming Japan, IOW stagnant. Isn’t that what total control causes, stagnation?