Cash is less of a threat to central bank policies when interest rates rise above zero.

By Don Quijones, Spain, UK, & Mexico, editor at WOLF STREET.

Sweden’s Riksbank has become the first central bank in the 21st century to take concrete measures to ensure that cash does not disappear as a means of payment from the financial system. To that end, the Riksbank proposes, in a document published on its website, to make it mandatory for all banks and financial institutions to offer cash services.

The pronouncement comes in response to a recent policy suggestion by the Riksbank Committee that only the country’s six major banks should be obligated to continue offering cash services.

That prompted a backlash from Sweden’s competition watchdog, which argued that the plan would distort competition as it would affect only a few of the nation’s banks. In response, the Riksbank has opted to apply the rule to “all banks and other credit institutions that offer payment accounts.”

There was also a difference of opinion between the Riksbank Committee and the central bank’s senior management on the issue of deposit facilities. While the Committee recommended that banks should only be obligated to provide deposit facilities to businesses, the Riksbank believes it is important for banks to also offer deposit services to individual citizens:

“This is a service that consumers can reasonably expect of credit institutions. There must also be symmetry between withdrawal and deposit facilities. In the Riksbank’s view, there is otherwise a risk that the possibilities for individuals to make deposits will decrease even further in the future. For most consumers, it would also be difficult to understand why they can withdraw cash from an account but not make deposits.”

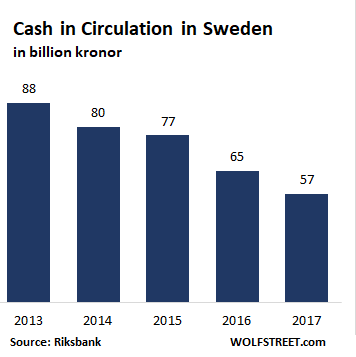

For years, the government and the Riksbank have been pushing for a “cashless society.” The Riksbank has over 1,000 articles posted on its website on the “cashless society“. The emphasis worked: between 2013 and 2017, the amount of cash in circulation dropped by 35%, earning Sweden a reputation as the world’s “most cashless nation”:

Many of Sweden’s bank branches had stopped handling cash altogether. Now, they will have to begin doing so all over again. Many of them are not happy about it. Nor indeed are Sweden’s competition and financial watchdogs, which both oppose the proposal, arguing that access to cash should be the sole responsibility of the state and not private banks.

“To secure access to cash is a collective good that the state should reasonably be responsible for,” the Swedish Financial Supervisory Authority said. It’s an opinion that’s shared by ATM provider Bankomat, which argued that it should be the state’s responsibility to ensure that citizens have access to cash since the handing of notes and coins is such an important — and expensive — part of a country’s infrastructure. Bankomat is jointly owned by the five largest banks in Sweden.

It’s not just banks that are complaining. Shops and restaurants, many of which now only accept plastic or mobile payments, could also be affected by a Riksbank proposal that retail operations deemed important to the public good, such as pharmacies, special transport services, food shops and petrol stations, should also “be included in an obligation to accept cash.”

One likely result of this is that many people who struggle to navigate the digital system, or who don’t have credit cards, in particular the elderly, no longer have to fear finding themselves locked out of the country’s payment system. Sweden’s parliament has also launched a review on the impact of going cashless too quickly as it dramatically excludes the financial needs of the elderly, children and tourists who rely on cash.

It is a dramatic u-turn for a country that not so long ago was further along the path toward eliminating cash than just about any other advanced economy. Sweden was the first European country to enlist its citizens as largely willing guinea pigs in a brave new economic experiment — negative interest rates. But a negative interest rate policy (NIRP) has its limits with consumers as long as cash remains an alternative; hence the efforts to eliminate cash.

But since then, doubts have begun to set in. In a survey earlier this year, 68% of respondents stated that they would not like to live in a fully cashless society. The survey, commissioned by Bankomat, polled over 2,000 people aged 18-65.

Incredibly, the country’s central bank, once at the forefront of the global cashless revolution, appears to agree with them. The Riksbank is now even talking about raising rates either this December or in February 2019, after keeping the benchmark repo rate at minus 0.5% since February 2016.

As the age of NIRP “gradually” comes to a close, much of the excitement about ushering in a cashless nirvana appears to be fading with it. Following on the heels of comments by senior ECB board members in defense of cash as well as an open admission by the European Commission that physical cash is perhaps not quite the source of all evil, the Riksbank’s decision to safeguard the role of cash in the financial economy is the biggest sign yet that Europe is giving up on its war on cash, and is instead allowing people switch to cashless payments systems at their own pace, however long that may take. By Don Quijones.

And in Canada: a cashless society could have “adverse collective outcomes.” Read… Backlash Against War on Cash Reaches the Bank of Canada

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I think they suddenly realized that if they eliminate cash how would you keep secret all the bribes, payoffs and kickbacks.

I `m sure they amount to a tidy sum of global GDP. Sarkozy alone received €50 million in pay-outs. I sure it didn`t go through Visa,Mastercard or SWIFT.

Sweden have very little corruption.

https://en.wikipedia.org/wiki/Corruption_Perceptions_Index

Inquiring minds want to know … in a couple more years when they’re again pounding rates down to subzero levels due to the fallout from the Frankenstein monster of debt they’ve nursed into existence, will they do another U and again conclude that cash is the bane of modern finance?

No possibility these central banksters will recognize the “need” for ever more extreme “policy responses” as a glaringly obvious sign that what they’ve been doing for the past couple of decades just isn’t working?

Europe will never reverse NIRP’s, if this is what you mean. This applies to the ECB and the rest of the rotten crew: BNS, Riksbank etc. It’s just a matter of how long it will take for the ECB to blink and start buying securities once again like there’s no tomorrow. The Italian gamble will pay off, and handsomely so.

The US is another matter but let’s just say my previous idea of a decade or more of slow financial tightening is most likely just wishful thinking.

Having said that, this pronouncement by the Riksbank is most likely politically motivated: Sweden is one of the many countries where savers have been willingly sacrificed on the altar of fast economic growth, with nothing but a capricious stock market as a compensation. And 2018 has not been exactly kind to stock markets worldwide.

Savers are just one of the many categories of what Americans would call “bagholders”, and they are all getting angry. Angry and confused, meaning they can vote into office people like the amateurish corner cafe orators ruling in Athens and Rome. Even Emmanuel Macron’s carefully constructed image as a “revolutionary within the establishment” is melting away, with an approval rating already lower than Nicholas Sarkozy’s… quite an achievement.

Giving these bagholding savers something akin to a yield to keep them happy is completely out of question, so let’s keep them happy by throwing them a bone in form of suspending the war on cash… at least until this nuisance can be safely ignored.

yep. Same in the US. Governments are at financial war with their own middle-class citizens. Depositors removing their cash is a threat to failing banks who need to maintain deposits but offer zero to stay afloat. Eliminating the possibility of bank runs becomes a necessity. People must be trapped into obedience. Ultimately that leads to the de-legitimization of the governing authorities and political upheaval. Rinse and repeat. We just happen to be around for this stage of the cycle.

Physical cash and coin is an important difference between currency and something else like cryptocurrency. When people don’t frequently see or have access to currency with the country’s name on it, the system loses legitimacy in the eyes of the public. Psychology is important when it comes to money.

High rates of inflation and hyperinflation have historically been linked to “printing press” economies. Eg Weimar Republic, Zimbabwe and some South American States. However in modern Western Capitalist type economies with more controlled banking and most salaries paid via a Bank Account there is now limited scope for Governments to ‘secretly’ feed the system with paper currency.

If the link between the paper currency and digital payments is gradually being broken by moves towards a cashless society, based on Ted’s ‘psychology’ insight, we might eventually run the greater risk of high inflation coming in through a ‘back door’.

If they keep cash, they can avoid being responsible for illegal money laundering at banks on their watch in places like Latvia, Malta, Cyprus etc. Something the hopeless ECB is wrestling with as we speak.

And maybe when you have no currency, your money devalues.

https://www.xe.com/currencycharts/?from=USD&to=SEK&view=10Y

“But a negative interest rate policy (NIRP) has its limits with consumers as long as cash remains an alternative; hence the efforts to eliminate cash.”

EXACTLY, which is why it should NEVER be allowed. Same for the drive to eliminate large denomination bills “to stop their use in crime” as if that has just suddenly become a problem that hasn’t existed forever.

Isn’t the idea physical cash will prevent negative rates nonsense? For a start cash comprises less than 5% of money in circulation (3% in the UK), so just that 5% would escape negative rates. Secondly, it might be okay to stuff a few grand under the mattress but when it gets to 100s of grand it gets a bit scary – you then have to weight the risks. Is it better to “pay” -0.1% to have the bank look after it or pay nothing and “look after” it yourself. Well, I guess it depends on whether the -0.1% later turns to -1% or to a Cypriot haircut.

An alternative is the likes of bitcoin, of course. But I guess you need to believe in it, as a store of value, long term.

Could cryptocurrencies be a part of this move? Eliminating cash does not eliminate the need for it.

I have to wonder how much “the war on cash” has fed cryptocurrencies, and how much CC’s are a part of this move to back off said war. As has been stated, eliminating cash does not eliminate the niche it serves. What fills that niche? Could be CC, could be precious metals, could be a bag of chickens.

xlnt update, thx, DQ.

and some great commentary above.

i tend to think that some of the recent central bank reversals (wrt the war on cash, ZIRPs, and NIRPs) have come from the slow dawning awareness on the central bankers’ parts to some of the effects that these have had:

> the desolation of pension funds, and other retirement savings, by interest rates obtainable over the past decade (eventually becomes a problem for the government)

> the desolation of any other savings accounts, by interest rates obtainable over the past decade (eventually becomes a problem for the government)

As for motions towards a truce in the war on cash:

On the part of the common man, there should also be alarm at loss of the privacy that use of cash affords. (It has become difficult for me to tell how much the common man cares about privacy any more.)

It would be interesting to have the reasons the 68%, of Bankomat’s survey respondents, would give for not wanting a cashless society.

The moment you lose your physical national currency you invite and give legitimacy to currencies without boarders. Crypto currencies. This is the fear of a cashless society. It’s an erosion of sovrienty.