It spikes 150% from year ago. Caveats apply. Grain of salt helpful.

So I’m going to quantify the Fed’s increasing hawkishness. This isn’t going to be perfect. Caveats apply. And a grain of salt is helpful. But here we go.

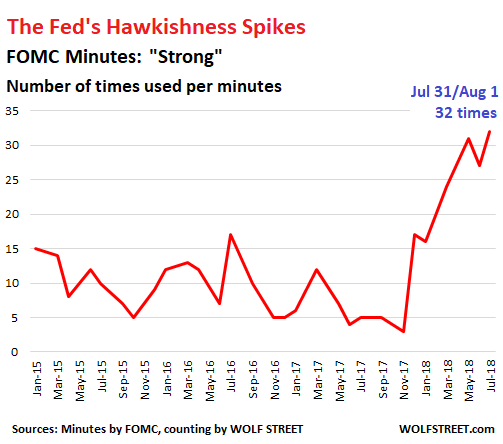

About three weeks after the Federal Open Markets Committee (FOMC) meets to decide on monetary policy – currently eight times a year – it releases the minutes of this meeting. Today, it released the minutes of the meeting on July 31 and August 1. These minutes, which summarize the presentations by Fed staff and subsequent discussions among the “participants,” are purposefully mind-numbing, repetitive, and vague.

But they’re also full of descriptions of how the Fed sees inflation, the labor market, credit markets, the stock market, the housing market, and other things, including the global economy.

And these descriptions come with qualifiers, such as “strong” when things are going well, or “moderate” when things are so-so.

I’m going to track the use of the words “strong” and “strongly” as an indication of what the Fed thinks about the economy. The phrase shows up in sentences like these, gleaned from today’s minutes:

- Asset prices were influenced by a number of factors, including … data pointing to strong growth momentum in the United States.

- Labor market conditions continued to strengthen in recent months and that real gross domestic product rose at a strong rate in the first half of the year.

- Total nonfarm payroll employment expanded at a strong pace again in June.

- Economic activity had been rising at a strong rate.

In today’s minutes, the word “strong” appeared 32 times, 150% more than a year earlier, and the most since perhaps ever: Even in 2005, during the first half of the rate-hike cycle at the time, when the Fed was gung-ho about the economy, the word “strong” appeared between 3 times and 9 times in the minutes.

This chart below shows the number of times that “strong” has been used in the minutes going back through 2015. The spike shows how the Fed’s point of view changed since late last year:

The Fed tapered QE during 2014 and stopped it entirely at the end of that year. The first rate hike in this cycle occurred in December 2015. So this was when the Fed started feeling pretty good about the economy. The oil bust, and the credit squeeze in the oil patch that occurred in early 2016, caused it to flip-flop on rate hikes until December 2016, when the rate-hike cycle commenced in earnest. But now, according to my chart, the Fed sees the economy rocking and rolling.

The current target of a range between 1.75% and 2.0% is way below inflation, with CPI currently rising at 2.9% on a 12-month basis. So the Fed is still highly “accommodative” where its monetary policy stimulates the economy. It is now heading toward “neutral” – and opinions diverge what that means, but it appears to be with the target range somewhere near 3%.

At some point, the Fed might decide to “tighten” – that is, raise rates beyond “neutral.”

If the Fed sees this chart and realizes that there are some “strong”-counters out there, it might do one of three things: Ignore them, use them as additional tool to spread its monetary policy guidance, or trip them up by changing its vocabulary, such as by replacing “strong” with a variety of adjectives:

- Energetic growth momentum

- Employment expanded at a firm pace

- Nonfarm payroll employment expanded at a forceful pace

- Economic activity is rising at a robust rate

- Growth of outstanding commercial and industrial (C&I) loans held by banks was muscular.

- Business fixed investment had grown at a tenacious rate.

Then we’d finally have a hoot reading the minutes. Until then, I’m going to track “strong” and “strongly” to see where they will lead.

The Fed’s QE Unwind is accelerating. The first 12 months are the ramp-up period – just like there was the “Taper” during the final 12 months of QE. The plan calls for shedding up to $420 billion in securities in 2018 and up to $600 billion a year in each of the following years until the balance sheet is sufficiently “normalized” – or until something big breaks. Read… The Fed Accelerates its QE Unwind

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Long end sure doesn’t agree or sees more tightening as a mistake.

Tightening wouldn’t be a mistake. The Fed would be forcing the markets to incur some short term pain in exchange for long-term gain. Debt and asset prices are unsustainable right now. You can pop it now and take some pain, or pop it later and maybe die from it.

The Fed has been spineless and feckless the past few decades, but it is now facing the realization that the end of this debt cycle is near. Even a drunk has to quit when he runs out of booze.

Tightening much further will be a mistake if the goal is to allow the current economic expansion to continue. If the market expected to see much additional future growth and inflation, that should reflect itself in the long end. It is not.

Barring unforeseen circumstances, I still see yield curve inversion late 2018 or early 2019 with recession to follow.

Agree, but it’s not a true and sustainable market expansion if it’s fueled by increased debt and deficits. The Fed obviously knows this. The question is whether the Fed will do the responsible thing.

Try to do the responsible thing anyway… no one really knows exactly what they are doing.

The economist post mortums are always interesting.

Why should having the current economic expansion continue be the goal? That seems to assume recessions serve no beneficial economic function, an assumption that would need to be proven before basing policy on it.

As Wolf says:

“The current target of a range between 1.75% and 2.0% is way below inflation, with CPI currently rising at 2.9% on a 12-month basis. So the Fed is still highly ‘accommodative’ where its monetary policy stimulates the economy.”

As such, they have no choice but to keep tightening.

The FED is a mistake.

What I mean is that in stead of respecting and observing the economy like a life by itself, THEY think they can “control” it and make it “do” things. That is a mistake. The end result is that they will benefit a few at the cost of “damaging” the economy under the name of “improving” the economy. In other words, the FED is the dick of the rich to screw the mass. When ever i hear people about TAXing who to balance inequality, my answer is that to simply cut the FED off would be much more effective without using violence against anyone’s property.

The long end is being pushed down by EM bond selling due to shifts in the currency market. The Fed is probably right to assume that the selling is “transitory”, analysts are bullish on the EM, and when it abates that long term rates will rise on their own.

Maybe they should rename the minutes as “The Fed’s Guide to Empty Prose”. On the other hand, I’m hopeful they are at least, on the surface, shedding securities…I say on the surface because how does one know what goes on behind the proverbial curtain. Are the major central banks of the world colluding? So, is another bank picking up the slack so to speak? Hard to know where to go….

Can someone explain the relationship on the yield curve.

U.S. 10 Yr/2Yr Spread is 0.2194 (-0.0096 (-4.1921%))

Who is buying the US10y if the expectation is that rates will continue rising?

Wolf do you have any data on Fed note issuance, the volume, how many shorter term 2y vs 5y vs 7y vs 10y ? Could the 10y be dropping because there is a lower supply of them vs other lengthened treasury offerings?

You had a previous article pointing at domestic treasury consumption, but its not as clear as to why the 10y would drop this drastically.

Have we reached the end of the Fed rate hikes?

I hope not.

Plenty of supply of the 10 yr. This is one of the most shorted trades right now — because it’s so obvious. Like Tesla. It’s hard for the 10-year price to drop (and the yield to rise) when these huge short positions are staked on it. That’s what keeps Tesla propped up too.

Wolf, if possible could you explain this to my ignorant self?

Borrowing shares/bonds to sell then buy back at a lower price. How does that prop up the price?

Bond vigilantes, (efficient market) has been over for a long while. The only way it returns is if supply shrinks enough that buyers once again have a say in the market. The one sure way to shrink supply is to go medieval on the budget and if Dems win this fall that could happen. That is also the case for owning corporate bonds and why (perhaps) the market keeps blowing off the Fed rate hikes.

Shorts eventually have to buy back stocks to close their positions.

They are guaranteed buyers, and, they also must buy “ahead” of the other shorts to profit, so paradoxically, many shorts are buyers when a stock goes down further because they fear getting stampeded if the stock suddenly rises and everyone has to close (or if it goes all the way down to ‘suspended’ and they can’t close).

“Borrowing shares/bonds to sell then buy back at a lower price. How does that prop up the price?”

There’s no guaranty that stocks will be available at a ‘lower price’. Rising prices in this situation is called a ‘short squeeze’ and results in rapidly rising prices if everyone who sold short needs to buy NOW to cover.

Lots of short sellers having to buy eventually would mitigate price falls since there’s a group of waiting buyers.

I suspect algos prey on short sellers.

ROb D,

Shorts HAVE TO BUY to close out their positions. So they buy to take profits as prices are falling. AND they buy when they’re scared of losing their shirts when prices are rising (“short-squeeze”). Shorting is very risky, with an out-of-whack risk-reward relationship. So shorts are a nervous bunch — and they’re furious buyers during a short squeeze (when prices rise, and when yields fall), thus pushing prices up further and yield down further.

So when very large short positions have already been established (10-year yield, Tesla, etc.), it puts a floor under the asset price and a lot of firepower on the upside.

However, when there are no/few existing short positions, and when then short-sellers START heavily short-selling shares to build their positions, this puts a lot of downward pressure on the price. This is a relatively short phase at the beginning. Then shorts need to get out because all the money has been made, and they get out by buying…

I don’t know which hurts worse: listening to the Fed speak, or tearing my hair out.

I think something is “strongly” stinking at the Fed.

I’d strongly recommend an audit , so the Fed can keep the strong confidence of us all …..

Fiscal and Monetary policy disconnect. The Fed seems to be aiming toward less supply, (you don’t raise rates and then print bonds at record issuance) and so far Fiscal stimulus is dead in the news, and probably in the water. Potus put up a big defense budget and Dems doth not protest one bit. Something has to give.

We got ZIRP as a result of a group of opportunists capturing the Fed after the big recession by popularizing bad economic theory. This bad theory favored Wall Street and those who believe in expansive government borrowing at the lowest rates possible. The theories they used are still widely believed – it’s a career buster to mock them – and could rise again given the opportunity. Fortunately, they are on the way out here, at least for now, and hopefully forever.

The problem the world now faces is that rising rates in the US encourage capital flight from those places where ZIRP/NIRP is still common. This will create a stronger dollar relative to those currencies and somewhat lower rates in the US than they would be if everyone had normalized rates – see the odd yield curve, it’s a reflection of capital flight.

ZIRP/NIRP only work (if you ignore resulting capital destruction) if everyone does it – there’s no reason for capital flight if nobody pays a decent rate of interest. If the US continues raising rates a while longer, all kinds of unknown but probably bad results will occur every place ZIRP/NIRP still exist. Hence my pessimism about the Eurozone existence once Kick the Can becomes much harder to play.

To the good, continued rate normalization in the US means party time here. We have rising incomes, greater capital investment, more and better jobs, and a strong economy. To the bad, asset oriented paper flippers will have less to work with. If it continues for a while longer, the Eurozone could descend into the pit and we will barely notice.

Note to economists: Rates that are too high or too low are bad. Rates in the Goldilocks zone are just right. We’re almost in the Goldilocks zone now … they need to go up a little more – maybe 3% at the lowest end.

All the housing statistics lately have been horrible. They’ll continue raising rates. A recession in 2020. Our long Depression continues. They’ll lower rates to near 0 when a Democrat becomes President and keep it near 0. A Republican wins in 2028(assuming civilization is still here), and rates start going up around this time. Even those who vote third party candidates can figure out the agenda.

Housing is very localized Some areas are booming and others are wallowing in sorrow It’s all about where the jobs and/or the wealth is The trick is and always has been in buying in an area that will be tomorrow’s place to be For me that place is outside the US but I could be wrong

The next few years will be extremely interesting. Debt levels are even higher than they were in 2007. Buisnesses cannot handle the larger loan repayments that higher interest rates bring. Then again, society cannot handle the consumer price inflation that these low rates create or the bubbles they engender. Our only salvation is a debt jubilee or massive wage inflation. The FED simply cannot allow the former and has no power to create the later.

A most coherent comment. What are the possible scenarios, as you see them?

I notice gold bugs are being taken to the woodshed again today.

Gold had gone up about $25 so it was time for it to get beaten down again. At least this allows the Russians and Chinese to get it cheaper.

Kentucky fried We will have our day Gold has ore than doubled since I bought some( In Turkish Lira terms that is) Gold and Silver is a total collapse /USD collapse play and that may well be in our future if our beloved Orange Julius has his way Hedge accordingly

If markets panic, I doubt the Turkish Lira is the place to be, $US might be as good as any.

What happens to gold as margin calls for everything under the Sun become a daily pastime? I recall last time this happened.

I read Daneille DiMartino Booth’s book “The Fed”. Wolf, I wonder if you read it. It is scary, a real “what the hell” and it is clear there is total groupthink and they are clueless about the real world. I would like to take them on a tour of my city. They definitely need the 10th man.

In the real world in the USA there is an economic expansion for MAYBE half the population. I know my stocks keep going up but so is everything else that I actually need.

Unfortunately, I cannot statistically lower the costs.

Tuition alone is a nightmare I cannot describe as horrible enough- words cannot express the damage. I’ve met many kids with $200K loans and that is for a psychologist or a physical therapist or doctors with $300K loans or more but at least doctors can pay them back.

If these asset bubbles continue, (I have read about low interest rates and PE as one example of skewed rates, housing too, loans etc. etc.), debt rises (how much more?) , and inflation continues to rise at a hedonically and substistupidly adjusted rate will Hyman Minsky rear his ugly head?

Maybe that is what it will take to end this evil thing and we can go back to some form of capitalism where prices find themselves. Not likely until a crisis.

By the way with inflation at 2.9% (ha ha), what would a normal rate of interest be?

How can they raise interest rates to normal with this debt level?

While school costs can get crazy you can still avoid six figure debt. UCSD tuition was about $9k a year when I went from 2003-2007. I had maybe 5k in scholarships. And had roughly 30k in debt which was managable.

Today’s in state tuition for ucsd is $15k… yes this assuming you live at home. But frankly if people are not wealthy perhaps they can’t afford to go to an out of state college and pay rent and hiked tuition. If you go to a private instituion you are frankly fucking off your money unless you have a rock solid plan as to how it will help you handle the 4x cost.

Grad school is where most of my friends found their real debt. Again most of their prices were aligned with the potential jobs. Some ended up not being worth it. But you can get a cheap masters for or a STEM PhD for free. Or better yet work and get an employer to pay for grad school.

The additional problem with college debt is kids are told its normal to go 6 figures into debt and promised it will be worth it…. if you are a doctor it will be, if you are anything else it wont.

Unless parents are great with money, almost no kid at 18 will make fiscally sound decisions when faced with taking out such life altering amounts of debt. In this regard the lending practices for college are almost predatory.

You are right to a large extent. The kids have no idea what debt is, amortization, interest rates, etc. I volunteer with low income HS students and I try to get some of them to go to Community College instead of 4 year and to apply for scholarships of which there are a good amount out there. Some really want 4 year. I would say the parents should teach them but they do not have a clue either, and a lot of them work 2 jobs, some are immigrants. The students work too, most of them, after school.

I was not any better at 18 (not an excuse).

Kids are encouraged to go Ivy League and I have noted unfortunately for some that they will only be hired for certain jobs if you go to Harvard etc. It gives you upward mobility.

I find it interesting the schools do not teach financial literacy, but have noted a trend in giving classes in financial literacy in HS.

I also tell the students to avoid mocha cappuccinos and new iphones.

“But you can get a cheap masters for or a STEM PhD for free.”

Most of those STEM degrees are worthless and will hurt you more than they help you. The hard sciences are comprised of many Indians and not so many chiefs. Recruiters largely stick to the top ten schools when they do recruit Americans.

By the way, wasting some of the most productive years of your life kow-towing to Professors will be a negative drain on your future earnings. Most studies show B.S level will make as much more than PhD or masters level over time.

If there is a ground zero for fungible, commoditized labor it is in the sciences. Yes, thirty or forty years ago, this was not the case, with ample benefits and pensions, but those days are over.

Universities teach (brainwash?), the population into believing that education is valuable, but today, it is largely for the purpose of placing your money into their pockets.

Here, here. That’s a great post, RangerOne.

I attended my state’s flagship public university the same years you did for a STEM degree. Finished on time, minimal debt at the end, had a great experience, and my career has shaped up great.

College is still a great investment in yourself with an incredible ROI, but like anything else, you have to pay attention to quality and keeping costs down. Unless you’re attending an Ivy, private college is a tremendous waste of money when a flagship public university is just as good. If you can’t get into a competitive to very competitive school, college may not be worth it. A degree outside STEM, business, finance, accounting, or some major with an in demand career at the end also probably isn’t worth pursuing. And finishing in four years or less is a must.

At the end of the day what’s going to matter is not what they say, but what they do.

As of now, as “hawkish” as the Fed has supposedly become, their actions are still following the same policy trajectory that was telegraphed while Yellen was still there. From that perspective there has been no change whatsoever in Fed “hawkishness”.

To me, the more interesting thing is what’s going to happen with ECB actions. Here in the US, the central bank buys bonds of a single entity (US govt.) and hence all bonds tie back to the same credit risk profile. As such, forecasting what Fed actions might have on the bond market is pretty straight forward.

In Europe, the central bank buys bonds of many countries, with varying risk profiles. So when the ECB tapers or stops buying German bonds that might not be a big deal for Germany since there are probably plenty of willing market participants who’d buy those bonds at rates which would not be onerous for Germany. The same however cannot be said with respect to say Greek, Italian or Portuguese bonds. This risk variability could cause unexpected dislocations in the bond market.

German rates are negative out to 7 years. Nobody anywhere would lend their money at negative rates unless they were forced to. Would you lend $100 to a friend if you were promised $98 as a repayment? That is a negative yield. This is what the ECB has forced onto Europe. Several other countries have negative yields. Other high risk countries have yields at rates too low to mention.

This is why capital flight exists. The cure to capital flight is capital controls. The failed EU War on Cash was one capital control. My personal guess is Draghi will stall until his replacement arrives next year. Then, let the fun begin. I personally expect ugliness.

Negative rates are not the point. The point I was making in my post is that if the ECB floor is taken out because of an ECB swing towards hawkishness, German yields will rise but they are not going to rise to a point that’s where they are going to cause a significant hardship to the German government. If the floor is taken off Italian, Greek and Portuguese bond yields however, rates on those bonds may well rise to levels which could be quite onerous for those governments.

“So when the ECB tapers or stops buying German bonds that might not be a big deal for Germany since there are probably plenty of willing market participants who’d buy those bonds at rates which would not be onerous for Germany. ”

As I said, nobody buys negative rate bonds unless they have to. The entire ECB debt environment is an aberration. The entire Eurozone will suffer financially if rates there normalize. Its existence is threatened.

Time will tell for sure … about 6 months max …, but ECB hawkishness is as faux as faux can be.

Is it me, but I fail to see what is so strong about the economy? If there is really 4% unemployment, then why don’t wages rise to attract workers? I fail to see how the stock market represents the Nation’s economic health other than a drop in value would scare people from shopping for awhile. The majority of workers do not own stocks.

My niece and two nephews (who live in the States) all have very good degrees. They all own homes. But from my vantage point it looks like they are barely maintaining. One burp and they are struggling to survive.

Instead of the Fed trying to control everything and save us from ourselves, how about developing a philosophy of the ‘Sweet Spot’ where interest rates might range….say between 1or 2 percentage points? This would allow coherent returns for savers, funds for borrowers with a sound Business Plan or a consumer need to borrow, and provided a slow and steady track. Instead, businesses are propped up and rescued with unintended consequences…..like screwing average workers and increasing inequality. Business and industries that don’t adapt should be allowed to fail, just like what happens to households. We’re careening all over the place and this past 10 year Fed track seems like one big experiment. It certainly does not inspire confidence.

You folks want a trade wind or do you want ‘these captains’ frantically raising and lowering the sails with every gust of wind? Maybe the chairs and officers don’t know what to do, but for God’s sake at least pretend a bit better. Hey, here’s a good idea….let’s not tell the crew or passengers anything until we make our move. Real leadership. sarc/

That is to assume they know what a sweet spot should be. With bad data and sleight -of -hand interpretation, a trillion dollar economy, zones of economies, trillions of dollars of off balance sheet stuff, derivatives up the wazoo, covenant lite loans, who owes what to whom (remember AIG), and who knows what else lurking out there, I wonder how the Fed would know the right interest rate. After all the Fed did not see or react to the emerging housing bubble or 2000 or at least it appeared so.

We really take them seriously? I guess we have to. After all they have PHD’s from Harvard, Yale, Chicago, Columbia and it costs a LOT to go there.

Msshell…Congrats for summarizing what’s important.

If the financial press continues to distract us,

keep us in the dark, the party is destined to

end badly.

My argument is that the masses want to be kept in the dark. As long as the link between the goal of life is to be happy and to be happy is to consume does not get severed, nothing will ever improve.

The economy is strong at the moment.

The issue with relatively modest pay increases has to do with the overall trend that increased corporate profits have been going to upper management and stockholders. This is plain to see from the perspective of corporate profits as a percent of GDP which is near a peak, as well CEO-to-average employee wage ratio which keeps increasing – while at the same time wages and salaries/compensation as a percentage of GDP has been going down.

So, the economy is strong but this “strength” is being funneled to company owners (in the form of dividends and buybacks) rather than to labor.

No!

The strength is being funneled back to mom and pop as interest income earned on a lifetime of savings. We are spending and, as a group, growing the economy.

Rising rates are disliked by the buyback crowd because it makes it harder to sell borrowing for the buyback.

Umm… Yes.

Corporate profits are very robust right now, which is most definitely a reflection of a strong economy.

However, these profits are not making their way to non-supervisory personnel as compared to the past. That’s suppressing their wages and increasing income inequality.

“If there is really 4% unemployment, then why don’t wages rise to attract workers?”

Some significant percentage of workers are employed by small businesses in the US. At least here in CA, it makes more sense financially for our business to outsource work rather than increase headcount.

Additionally, I’m sure every generation says this, but even as an older Millennial, I find the younger Millennials woefully unprepared for a real job. I approached all jobs in my 20s seriously, there was nothing to fall back on, I had to perform. These days, it seems common for 20-somethings to have Mom & Dad and/or a gig-economy “job” to fall back on, and thus, they are less willing to put in the hard work it takes to build a career. I think they will regret this in their 30s, or maybe not if it is the new norm. Quite sad.

There is a strong possibility that there is a strong bubble in plain site, buy will the Powell FED be as persistent as the Volcker FED? Of course, the circumstances are different. There was high inflation then, while today inflation is “too low”, but we know what many think about it, with housing prices, stock market, and Italian bond yields. Prices didn’t go up, real wages went down.

Correction: …plain sight, but…

Jay Powell stated earlier this year that the Fed would only raise rates at quarterley meetings that have press conferences for transparency.( The one year US treasury looks like it has priced in the next two 1/4% rate increases for September and December 2018. ) The Fed also stated that in 2019 they will reserve the right to raise rates, at their discretion, for ANY monthly meeting going forward without press conferences.

John Mason. Former faculty member of Wharton thinks the 10 year treasury is being supported by international monies. If so, this could influence the yield curve and whether it inverts.

https://seekingalpha.com/article/4197835-safe-haven-u-s-dollar-keeping-us-interest-low-fleeing-international-monies.

Look what’s happening to EM countries and their currencies.

It is the Fourth Turning, the idiots are in charge and it will end with catastrophe. Out of the ashes will rise the innovators who will rebuild and the cycle will repeat.

For the first time forever, I have a terrible time remembering the name of the chairman of the Fed.

That may be a positive indicator.

To me it looks like they are running their meeting by using a corporate speak generator. The more a word gets repeated during a meeting the less meaning it has. Also the more a statement gets repeated by either a corporation or the government the highter the chances of it being false or becoming false in the future.

The only meter is the market. It certainly does not think things are “tight”.

The party goes on. Things are tight when a “crisis” actually matters. Right now the market can survive anything.

The Fed and other market-movers are prone to using simple keywords like “strong”, rather than a richer vocabulary, so that their statements can be read and parsed with some degree of accuracy by AI trading bots.

All the Fed’s statements are tailored to create certain market effects, or at minimum to avoid unwanted effects.

The AI trading bots are programmed to read for hawkish/dovishness and move the bond yields before humans even get past the first paragraph. This delivers first-mover profits to the bot owners.

The giant banks own the bots and they also own and control the Fed.

Trading being a zero-sum game after securities are issued, the banks profit at the expense of other market participants.

This is just one more arena where the vampire squid sticks its blood funnel into anything that smells like money, at public expense but without public awareness.

Insightful piece. Fed- speak reduced to a science.

Ought to be picked by MSM.

(Would be harder to do if Greenspan was still in the chair.)

So with all the comments I read here; maybe Wolf could write an article explaining the reason that gold is crashing?

I dont think the thought of an increase in interest rates of 0.25% in the USA would result in a fall in the value of gold on the basis of an increase of 0.25% return on capital in money in a bank?

Cashboy,

I wouldn’t say gold is “crashing” — in terms of the moves of the past few days. It’s just down about 3.5% over the past month, though over the longer term — since its peak in 2011 — it looks a little different.

In my observation over the past few decades, there is practically no correlation between PM prices and interest rates. So I would take that off the table.

I’ve talked about gold and silver on some of the radio interviews I posted here. I have a long-term theory of why gold and silver prices are where we are, and where they might go or not go. It’s just a theory, and I have not tried to flesh it out, but it has held up pretty well.

My first big loss as an investor was with silver in the early 1980s though I did everything that you’re supposed to do, including buying after it had plunged over 30%. But I ended up losing 50% over the next couple of years. Since then, I looked at PMs with a different eye and came up with my theory. The key element in it is time.

Beyond this theory, I think it’s a good idea to have some PMs among your assets, not for the catastrophist reasons many people cite, but because they have proven to be countercyclical since 2011, going down when EVERYTHING went up, thus being among the very few assets that aren’t part of the Everything Bubble.

Today there is very little real diversification possible because almost all assets went up together, and they might all go down together. The exception since 2011 are PMs.

I don’t know if readers here are interested in my views or rather my theory about the movement of gold and silver prices, but it seems to hold up pretty well.

If there is interest, please let me know, and I might write about it.

I’m going to report this under the current article so that more readers can see it and respond to it.

Count me in, Wolf. I’m in my early sixties and still learning. I do hold some physical gold and silver, just in case, and always wondering if I should buy more.

I’m pushing 70 with 80% silver 10% gold 10% re F&C . Personally I like the fact I can put less (strong) fiat into PM’s .Am i going into the bond,stock or current R/E casino? ; I don’t think so !! Let the PM’s roll.

Wolf, I’m interested in your views on precious metals.

Thanks

I’d be interested in such an article.

I would LOVE to hear an in-depth article about Gold and Silver pricing. So much of what I read is conspiratorial stuff about “big boys under-cutting prices on purpose” and such.

While I think that is a possibility, I’d like to hear other ideas and see evidence to support.

Someone made the ob about the loss in value in our currency, and how 30 cents would buy a gallon of gas. I keep a 1944 dime on my desk to remind me, that it still does.

you should.

Label it clearly as theory.

If it dosent contrain concepts the gold bugs adhere to lay in top grade earmuffs before releasing.

We know PM’S are manipulated up, and radically overpriced we frequently dispute why and who.

When governments abdicates power to a private bank guess what happens ?

Freedom ?

Create a web crawler that looks at certified websites for bullish phrases. Then log them to create a real-time Bubble Meter with history. Use Golang.

Don ho!

Given reality is mediated through vision and the EU being comprised primarily of freethinkers, I predict the EU will rescue Turkey from financial duress, conquer the Middle East via making durable treaties with terrorists and pardon Putin for all his sins.

These problems the US has created single handedly, shall be resolved.

Good luck with the Fed Hawkishness-o-meter.

Im not sure you can decipher much aside from whether or not they’re planning to continue hiking. That may be worth something though.

As far as an overall change in direction, it seems to me that the 2 things affecting this most are

#1 the stock market (stocks drop and lobbying for lower rates gets deafening. Wages rise and they get nervous)

#2 politics (fed tightening often waits for presidential elections to conclude, but this affect seems to be temporary. Other political effects seem to vary more on the direct pressure of the president than the party affiliation.)

Well, it is Trump’s Fed, so if the economy isn’t “strong” then it is going to be “tuff”, “big”, “beautiful”, or “very, very tremendous.”