Delinquencies soar past Financial-Crisis peak at the ca. 5,000 smaller US banks, and these are the Good Times. What’s going on?

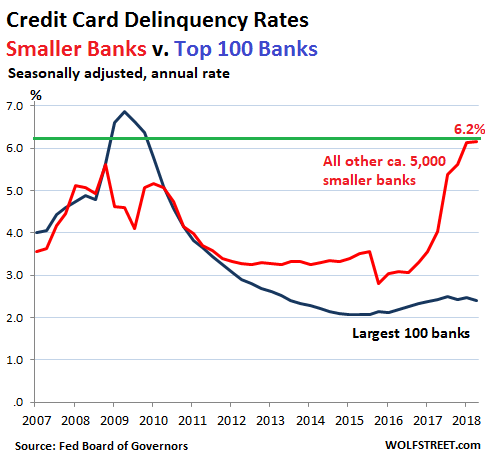

The delinquency rate on credit-card loan balances at commercial banks other than the largest 100 – so at the nearly 5,000 smaller banks in the US – rose to 6.2% in the second quarter. This exceeds the peak during the Financial Crisis by a full percentage point and was up from 4.0% a year ago.

But for the largest 100 banks – which carry the majority of the credit-card loan balances – the delinquency rate was 2.4% (seasonally adjusted), the Federal Reserve Board of Governors reported Tuesday afternoon. So what is going on here?

A bank classifies credit card balances as “delinquent” when they’re 30 days or more past due. The rate is figured as a percent of total credit card balances. In other words, among the smaller banks, 6.2% of the outstanding credit card balances are now delinquent.

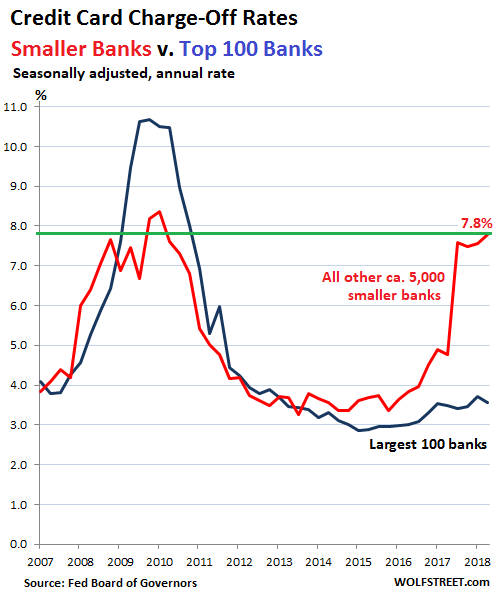

Some customers are able to catch up with their minimum payments, and their credit card balances are removed from the delinquency basket. Others are not able to catch up, and the bank tries to collect what it can. It then moves the balance out of the delinquency basket into the charge-off basket – when the loan is “charged off” against loan loss reserves.

These charge-offs among the largest 100 banks in Q2 rose a fraction year-over-year to 3.6% (seasonally adjusted).

But among the nearly 5,000 remaining banks, the charge-off rate spiked three full percentage points year-over-year to 7.8%, the highest since Q1 2010. The rate among smaller banks had peaked during the Financial Crisis in Q1 2010 at 8.4%:

Note that both charts above are about on the same scale, with the delinquency rates lower than the charge-off rates as delinquencies get moved out of the delinquency basket and into the charge-off basket.

Overall, across all commercial banks, the delinquency rate, at 2.5%, was flat with a year ago, pushed down by the largest 100 banks. The overall charge-off rate for all banks rose slightly year-over-year to 3.7% up. What’s going on is this…

Subprime comes calling.

The charts above show just how badly the largest 100 banks had gotten hit with losses on their credit card balances during the Financial Crisis as consumers, many of whom had lost their jobs, could no longer keep up with their minimum payments. At the same time, the smaller banks had experienced smaller losses.

This was a lesson for those big banks. Since then, their underwriting has become tighter, and their marketing has been focused on the best potential customers that they’re luring with big cash-back offers, juicy frequent flier credits, and other incentives.

Smaller banks can’t offer those kinds of goodies, and cannot compete on that level, and so they marketed to a particularly profitable group, consumers with lower incomes, no savings, and weaker credit – many of them with subprime credit ratings – that they charged stupendous interest rates, sometimes exceeding 30%, creating a situation where consumers can’t even keep up with the interest charges. Profits were initially huge, but so is now the hangover – see the delinquency and charge-off rates above.

These losses on credit card loans at the smaller banks aren’t triggered because people lost their jobs in a recession. The economy is as strong as it has been in years, and people are working. These losses are happening during good times!

But the subprime segment of credit cards is concentrated at smaller banks because they targeted those customers to maximize their profits, and that subprime segment of customers is running into difficulty not because they lost their jobs, but because they borrowed too much at interest rates that are too high because the banks got too greedy with their most vulnerable customers.

Credit-card loans amount to about $1 trillion. The nearly 5,000 smaller banks hold only a small portion of it. And some of that portion is curdling. This does not jeopardize the financial system. But it does show that among the most vulnerable consumers, the borrowing binge is hitting limits. Credit begins to unravel at the margin.

Total consumer debt, not including housing-related debt, rose 4.8% in the second quarter from a year earlier, to $3.9 trillion, the highest ever. Let the good times roll. Read… The State of the American Debt Slaves, Q2 2018

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Very good article! Especially interesting how the big banks got socked when most of the population lost everything in the crash, and know to stay away from lending to poor people, while the smaller banks don’t seem to know to stay away from this.

Just one indication that it’s the “good times “for the top quintile, not so much for the rest of us.

I didn’t realize that “most of the population lost everything in the crash.”

And so you do want, or you don’t want, systemically critical money-center banks to lend to sub-prime borrowers at better than sub-prime rates?

Which is it? Which choice adds the most grist to your top-quintile mill?

That should be “Systemically Dangerous Money Center Banks”- you know, the ones whose executives criminally drive them into bankruptcy (as acknowledged by the FED) every 20 years or so.

Fixed it for you.

And what “WE” want has little to do with what these banks do.

“the smaller banks don’t seem to know to stay away from this.”

If you have millions of cusomters with smallish $1,000 – $5,000 credit limits paying ~ 25% APR coupled with $25 – $50 monthy late payment fees, etc. etc.

Yeah, they have some risk, but….

Rather, I just read this a another canary in the coal mine regarding the state of the economy / debt slave. Not as a reason to cry for the small banks.

In effect since it is the smaller banks that are affected we need not fear a bail out any time soon.

The bigger banks will absorb them for pennies on the dollar.

Mission Accomplished!

I wonder what % of big bank credit card customers are paying the minimum payment due each month. To me that would provide a better picture of potential future threats to the economy.

I am sure a lot of them pay it off, holding high interest credit card debt is pretty stupid. I have high rewards cards that have huge interest rates. I don’t care because the balance is automatically paid off every month while I cash in the credits.

What percent of the total $1T balance is held by the top 100 banks and what percent is held by the rest?

I can’t give you a precise answer, but you can approximate: the top 15 banks in the US hold about $13 trillion in assets (which include credit card loans). ALL US commercial banks hold about $16.7 trillion in assets. So the top 15 hold 78% of total assets — and by extrapolation about 78% of all credit card balances. Then, take this extrapolation and make a guess out of it: The top 100 banks might then hold about 90% of all credit card balances, give or take a few percentage points, and the remaining nearly 5,000 smaller banks divvy up between them about 10% of all credit card balances.

OK, thanks.

Almost sounds like smaller local banks are a bigger risk for your deposits.

Deposits are FDIC guaranteed, they have been since I was a wee lad.

MC,

What if, during a Bail-in, the FDIC pays you with 250K worth of stock in a newly formed bank designed to absorb the debt of the systemically important bank? Where does it say that you will be guaranteed cash?

Fear-mongering about the FDIC has been nonsense from day one. Some people have fun doing it, so go ahead, have fun doing it. And in the process, you become element of amusement for everyone else.

FDIC is an insurance program, like your auto insurance or home insurance, except its a US government insurance program. It works. I’ve been a customer of three banks that were taken over by the FDIC, including a big one during the Financial Crisis, and never noticed the difference except that the name changed.

Wolf, in a Systemic failure, the money is just not there (FDIC is already in multi billion deficit- correct me if that has changed).. It will then become a Political matter, with an uncertain outcome.

Some people may end up with very nice looking gilt edged “Certificates of Promise” instead of cash. Eventually, they may get there money.

I believe that small depositors ARE likely to get bailed out, but that is far from certain.

Monday1929,

If, if, if… If every car in the US got into a fatal accident at the same time, all insurers would be instantly bankrupt, and payouts would be near zero. But the chances of that are essentially nil. That’s how insurance works.

FDIC is insurance. The chance of all banks collapsing simultaneously is essentially nil. And if too many TBTF banks are teetering on collapse, the Fed steps in as lender of last resort, as we have seen in the past.

And if a bank collapses, the FDIC takes possession of it. Stockholders get wiped out. The FDIC gets all the assets and takes care of the liabilities in accordance with their place in the capital structure. So far, after the many hundreds of bank failures the FDIC has handled, after secured creditors were taken care of, there were always assets left to cover at least some if not all of the insured deposits.

Not all deposits are FDIC insured (see FDIC rules, including the $250,000 limit). Insured deposits get paid in full. If there are any assets left after that, which there often are, uninsured deposits get covered pro-rata based on what is left.

Mr. Richter,

No, I am not having fun considering what the Bail In law provides for. I do not know how it will be administered, it’s scope nor it’s legal responsibilities vis a vis the FDIC. A question…if all deposits are protected by FDIC, then what actually is bailed in? If all deposits are unsecured, considered loans to the institution in question, but insured, then what was the purpose of the bail-in legislation?

The legislation was enacted in 2010…it has, to my knowledge, not been applied to US Banks…I am unaware of a recent bank failure which could be considered systemically important and have triggered the provisions since the legislation.

If you would accept the Bail-In provisions of the 2010 Banking Act as a viable column topic, I would love to read it. Fear mongering? Please disabuse me….

Start here: https://www.fdic.gov/

Mr, Richter,

Sorry to beat a dead horse…and I can accept that the convoluted laws relating to the Bail-in legislation are above my pay grade. But what does this mean;

3.3 The FDIC and Bail-In

Title II of the Dodd-Frank Act empowers the FDIC to resolve financial conglomerates.54 The FDIC formally adopted the single point of entry (SPOE) approach to implement Title II in a December 2013 release that is currently out for comment.55

This release does not contain all the details, such as: the details of the valuation and equity distribution, or the criteria for recapitalizing subsidiaries. But the outline is good enough. SPOE is a form of bail-in at the parent. Instead of working directly on the parent entity, it uses an intermediate “bridge company.” 56 The FDIC will transfer all or most of the assets of the holding company parent to a bridge company, retaining many or all of the parent liabilities in the estate. It will then issue the stock of the bridge company to estate claimants in satisfaction of their claims. This liquidating distribution in kind is almost identical to a classical reorganization, although it entails a de novo entity.

Their approach should work, if there is enough debt in the parent. (This task is the Federal Reserve’s.) Bail-in requires liquidity support, but the Dodd-Frank Act provides it, through the FDIC and the Treasury.

The economic bottom in our country is getting squeezed unmercifully with inflation. This is just another indicator.

Don’t worry, China isn’t beyond exporting deflation as a means to maintain control.

On Monday President Trump complained about the treatment he was getting from the federal reserve. He complained that the fed is raising interest rates on him but did not raise rates under President Obama. The delinquency data fits into this narrative as they (delinquencies) increased when interest rates increased.

Does the Trump administration see the economy slowing down? Keeping interest rates low will help Trumps economy, but the inflation it would create would devastate the future economy.

Impossible. The savings rate was revised up. Muppets have WAY more money.

This article’s information is not surprising to me. I mentioned last week I changed credit cards due to the reward system. I was shocked the intial sign up was for a $25,000 limit, and it took effort to get it reduced to $10,000. The irony is that the discontinued card sent an offer to me just yesterday, an immediate credit limit boost.

What do they think will happen? In our house we don’t do debt. But I know other people who would say, “Oh boy, look how much more I can now spend”!

The other tell and concern are the credit offering crunches linked to specific stores and products. Things like, “No interest if you charge________amount to your card”, or “No payments or interest free charges for 6 months on outstanding balances”.

But hey, they just charged a sitting GOP congressman for stealing hundreds of thousands of dollars in campaign funds to pay off consumer debts and high living. Even some of the rich and connected apparently live beyond their means and station.

The Congressman is living beyond “your” means

Paulo,

I went through the same thing with my credit card company about 10 years ago. They issued me a card with a $20K limit. It took some real effort to get the limit reduced to $5K. I always pay it off every month and don’t care what the interest rate is.

If these small banks are able to charge a 30% interest rate on a decent portion of the loan balances, they may be able to absorb a very high level of charge-offs while remaining profitable.

It’s the borrowers that get shafted by their own doing. A 30% interest rate is something only a chump would pay.

We have one of these cards and were grateful to get it when our credit was destroyed in the financial crisis. There are some things which can only be purchased with a credit card, like a plane ticket, or car/truck rental. It also helps those who use it responsibly to reestablish credit.

When my in-laws were sick in another state, my husband was able to fly to see them. Had he had to drive, he would have needed to take a week off without pay, which we could definitely not afford. When we moved we needed to rent a truck to move ourselves as well.

Things that seem to not make financial sense sometimes are very rational.

You can buy a plane ticket and rent a car with a debit card. I do it all the time.

It may be possible now, with some companies, but it wasn’t back then. I tried signing up for the Hulu “free trial” with a debit card and got turned down, this was a few months ago.

Probably depends on your credit history and debit card provider’s history in dealing with the relevant merchant.

It’s hard to imagine for modern man, but back in the Paleozoic era before credit cards existed, people had to first get actual money in order to buy things. Shocking, I know.

I remember as a small child upon my father showing me his first credit card in the early ’70s thinking how strange it was that things could be bought with money you didn’t have (I was a bright, perceptive child, and it’s made life chronically difficult).

Little could I or anyone have imagined though that credit would become a way of life, enabling employers to pay sub-standard wages.

Little could we have imagined that being – chronically – tens/hundreds of thousands of dollars in debt would become to be seen as completely normal – indeed, as being ‘responsible’; adult.

Strange indeed.

I think someone in a book written 2000 years ago or so had something to say about the money lenders..?

->Credit-card loans amount to about $1 trillion. The nearly 5,000 smaller banks hold only a small portion of it. And some of that portion is curdling. This does not jeopardize the financial system.

If consumer credit collapses it could seriously damage a few million people and a few thousand banks, mostly on the lower, marginal tiers, but it probably wouldn’t be enough to crash the national economy or the global economy.

This could:

“Total global debt is estimated to be $247 trillion. It is a figure that should give us pause. Much of this debt, furthermore, went to finance the expansion of the financial sector rather than develop the productive and socially beneficial sectors. It is a model of economic growth that demands more debt to finance itself. There are few other avenues for this unsustainable model. The trigger that might explode this bubble fully comes in the months ahead as countries such as Argentina, Brazil, South Africa and Turkey will confront the maturation of their $1 trillion of dollar-denominated debt.”

https://www.nakedcapitalism.com/2018/08/turkey-trigger-next-global-financial-crisis.html

That’s nearly six times the global economy. Debt slavery is one thing, but this is human sacrifice. The clock is ticking, but I have seen no initiatives which credibly address the issue. And I am so far unable to come up with a sufficiently expansive metaphor to describe what’s coming.

Note to self: plant potatoes.

Are credit card loans packaged and resold like

mortgages ? Different packages depending on

credit risk , interest rates, etc…?

Yes and they have been since the 1980’s.

Andrew Kahr pioneered this with his “First Deposit” banks, absolutely superb direct mail marketing and a killer collection department.

I keep watching the 10 year treasury and it just doesn’t want to go up. Things like ‘increasing default rates’ don’t seem to be helping.

So the big banks are giving away toasters? Small banks lend to small business and economic policy hasn’t been favorable to them since the crash. The whole system just slipped a notch, but at the top end consumer spending is really a small part of what you do.

///

It is important to note that we discuss the volume, not the number of lenders! Hence if the bottom 50÷ earn 10÷ of income, and Wolf estimated that the bottom 5k banks own roughly 10÷…let’s assume that this is who is defaulting. Though a daring statement it seems half the US population is on the way to default. Scarry.

///

Also, to be a merchant it to sell items to other people which they cannot afford. Dismissing these people from the economy, will have a large impact on consumer spending. No credit, no one to buy the goods.

///

If the cause was really that subprime borrowers are in broad financial trouble (again), we should see it in other data (auto loans, mortgages), not just credit cards at smaller banks.

But there’s nothing amiss that I can see in the delinquency rates for consumer loans or mortgages at smaller banks, nor on “all loans and leases” at smaller banks:

https://fred.stlouisfed.org/graph/?g=kWGF

I think this is more about smaller banks (possibly specific banks specializing in credit-card lending) which have made some poor decisions, or which are no longer able to compete with the big boys. Poor choice of customers due to lack of access to Facebook and Google’s massive databases and profiling capabilities?

The only other scenarios is that the folks defaulting are not really in financial trouble, just sick of being credit card debt slaves at usurious interest rates, and switching to other credit/spending options?

Wisdom Seeker,

Auto-loan subprime is already in trouble. Banks don’t like to handle those loans. But three smaller non-bank subprime auto loan companies collapsed earlier this year. This article also has a chart from Fitch about surging losses on asset-backed securities backed by subprime auto loans.

https://wolfstreet.com/2018/04/08/subprime-carmageddon-specialized-lenders-begin-to-collapse/

Thanks Wolf. Is there an update to the Fitch data from the April article? The data only went thru February 2018… 6 months stale now.

In the April article, of the 3 smaller subprime collapses, one was hurricane-driven, another looked like fraud, and the third was having the plug pulled because they weren’t making money, but that wasn’t exactly a blowup. Have there been more lender bankruptcies since?

So the situation still smells more like lenders that forgot their 5C’s, not necessarily a wave of overextended borrowers defaulting.

All these cars are supposed to be properly insured. They’re collateral, and lenders have insurance requirements that protect the lender. A hurricane would be an insurance loss, not a loss for lenders. Car owners are responsible for any gaps between insurance coverage and loan values, unless they bought gap insurance.

The fraud was about hiding actual loan losses and charge-offs when they tried to get more funding. So this was a sign they their charge offs were piling up, and they tried to hide them.

Here is the latest Fitch ABS chart. It includes July. Look at the multi-year trend of deteriorating subprime v. prime:

Thank you again, Wolf, for your continued reporting on credit card debt. I often wonder if part of the wholesale dive into spending beyond one’s means came from a subconscious generational reaction to the stagflation and end of real-wage improvement of the late ’70’s-’80’s, i.e.: destruction of savings sent a lesson that saving was a mug’s game when any available assets needed to be put into tangible goods to keep any value at all. At the same time, add any number of easily-obtained credit cards, only make minimum payments, then add more of same to maintain our heavily-advertised consumer lifestyle. Bake for a generation+ as the kids watch and learn that this is the normal way towards a comfortable American life (Until the wheels fell off the car of the wealthiest nation the world had ever seen). How many generations does it take for a nation to forget how it got to the dance? May we all have a better day.

sorry, meant to say available cash, not assets. A better day to all.

1stCav, the long-wave credit cycles are typically thought to be about 80 years (4 generations). Could be a bit longer now, since families today have kids later in life. The generation that survived the 1930s learned not to binge on debt. The generation that survived the 1970s learned the opposite, as you said, that savings is destruction of wealth. (Living under threat of nuclear holocaust would also lead to a “live now while you can” mindset.) The next turn in the 80-year cycle would be around 2010. The key metric, Total-Debt-to-GDP, does appear to be past its peak, but it has not rolled over too far yet:

https://fred.stlouisfed.org/graph/fredgraph.png?g=jXZa

I hear that many younger folks today, whose families were wiped out financially in the Great Recession, who are struggling under high student loans, who are facing enormous mortgages on overpriced real estate, are again learning (the hard way) not to binge on debt and to savor deferred gratification.

But a generational credit contraction, although probably a good thing for many reasons, will not come without its own painful costs.

Wisdom-thank you very much for your insight, and your thoughtful reply to md below. May we all have a better day.

The interesting thing in this data is mainly that delinquencies and charge-offs in the subprime credit sector spiked last year.

This could be a warning to something, but I wouldn’t assume the reason for the spike without more data. Heck, it could be an economic shift currently isolated to certain regions of the US.

As for the spread between big vs small banks, all you can really read into this is that the big banks tightened credit, so the smaller banks looked to the market that was still available. Smaller banks have a higher cost of capital making it difficult to compete with the big ones head-on.

Riskier credit is more expensive, and the cost compensates banks for that risk. Higher default rates in riskier credit don’t necessarily mean the small banks are losing here. If the spike in delinquencies and charge-offs continues it could become a problem after a point.

Hi Wolf, is there too many small banks in the US? 5,000 seems a lot.

Possibly. But that’s down from 7,200 in 2007, just before the Financial Crisis, and down from 12,000 in 1992. So there is a clear trend :-]

Some of the larger banks, like the CitiBank Costco Visa, are paying up to 4% back on purchases. (4% for gas and 3% for restaurants,airfare,hotels,travel.)

I had heard that Visa charges 1.5% – 2% to the seller per transaction.

Is CitiBank only making money on the people who carry balances at 16% interest?

What if everyone pays their bills monthly?

Credit Cards at 16%-30% interest seem to be one step above PayDay loans. They take advantage of the truly desperate and people without spending control.

I was curious about those figures. I was going to buy a $50 Visa gift card ($5 store discount) until I saw the activation fee is 5$. Ripoff

i’ll give you a real world scenario of how this happens. for me it was sandy but there are lots of ways this happens, medical emergency, divorce, etc.

i had over $100k of damage on my flood insured rental property. the fema guy gave me a ballpark of $75k and a handshake. i started reconstruction on cc cash advances. i had to get the place fixed to get it rented again.

fema screwed me and paid me about $40k in drips and drabs over th next 9 monthes. then they announced that’s it. 2 1/2 years later i got aother &20k out of them by fighting tooth and nail but by then it was too late.

meanwhile, the heloc on the property resets from interest only to a 15 year mortgage. my monthly payments increase by $1500.

so, i start by missing a payment or three on a couple of the cards. immediately, my credit line is cut off on all the cards. in short order, every card that isn’t on an intro rate jumps to over 20% interest including the one’s that i have never missed payments on.

never missed a mortgage or tax payment. in 2016, i sold the place for a decent profit. by then, i had 19 charge offs. my credit is ruined for 7 years not that i care. i have no incentive to pay off the debts. i now live with one $500 c

visa cc for rental cars, etc. i also have a couple of prepaid cards for online shopping. i’ve learned my lesson and plan on living without revolving credit for the rest of my life.

Well stop whining then, and think yourself lucky to have been a real estate speculator and got away with it.

There are many people struggling to put a roof over their heads due to your ‘decent profit’; your paltry, self-inflicted problems pale into insignificance compared to the struggles of many to make basic provision for their families.

MD, you might want to work on your issues. Not everyone wants to own and that means, by definition, that some people will have to be landlords. That alone does not make them evil people.

anon was providing an example of how even a middle-class person can end up in CC default through adverse circumstances.

We get that life is even worse for folks lower down the ladder. If it’s not a hurricane, it’s an injury, car crash, serious illness with hospital bills, loss of a spouse who provided a second income to make ends meet…

We have a system in which people are allowed to make their own mistakes by getting in over their heads without realizing it. Both of you make a good case that anti-usury laws need to be reinstated and lenders prevented from extending as much credit to gullible borrowers. And perhaps the basics of personal finance ought to be a mandatory high school class?

sorry. i didn’t think i was whining. i consider myself financially sophisticated and i have nobody to blame but myself. i was just hoping to give an example of how easy it is to fall into this trap. i went through three years of hell and recovered. if this was the 1930s, i would never have recovered.

the issue is yield vs risk vs LTV was thrown out the door with low rates in 2010, started by Ally formerly GMAC. Subprime only works when yield is correct….which is still not correct….

It is axiomatic. The only way to achieve frictionless financial perpetual motion is to gradually drive the commercial banks out of the savings business. That is exactly the opposite prescription as Bankrupt-u-Bernanke applied to the GFC.

Remunerating IBDDs destroyed money velocity. What he did was destroy the shadow banking system (a misnomer for financial *intermediaries*, non-banks). Thus, the IOeR induced non-bank dis-intermediation (where the size of the non-banks, NBFIs, shrank by $6.2 trillion), but the size of the DFIs remained unaffected, increasing by $3.6 trillion in the same period.

And what Bernanke did was illegal per the FSRRA of 2006 which restricted the remuneration of reserves to a fraction of the level of the prevailing levels in the money market (which funds the capital market).

The remuneration of IBDDs was exactly the opposite of the prescription used to support the thrifts during the administration of Reg. Q ceilings (exactly the opposite prescription necessary to support the MBS market).

All bank-held savings are un-used and un-spent, lost to both investment and consumption. Why? Because DFIs pay for their new earning assets (from the standpoint of the entire economy), with new money. The DFIs do not loan out existing deposits, saved or otherwise.

Only insofar as the owners of savings spend/invest directly or indirectly do their savings become *activated*, i.e., synonymous with income velocity.