Let the good times roll.

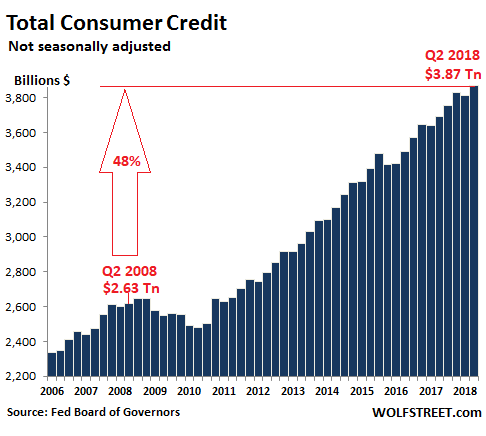

Total consumer credit – or less soothingly, consumer debt – rose 4.8% in the second quarter from a year earlier, or by $176 billion, to $3.87 trillion (not seasonally adjusted), the highest ever, according to the Federal Reserve. This includes credit-card debt, auto loans, and student loans, but not mortgage-related debt. Given how passionate Americans normally are in spending money they don’t have – that 4.8% increase is moderate: In 2011, increases exceeded 11%.

The chart below shows the progression of consumer debt since 2006. After the seasonal hangover in Q1, following the spend-and-borrow party in Q4, consumer debt set a new record in Q2:

To put this 4.8% increase in perspective: In Q2, the economy as measured by real GDP grew 2.8% year-over-year, and inflation as measured by CPI increased 2.7%. In other words, American consumers, among the hardiest creatures out there, have pulled through once again, holding up the economy with borrowed money.

Over the 10 years since Q2 2008, consumer debt has surged 48%. Over the same period, the consumer price index has increased 15.1%, and the economy has grown 17.8%.

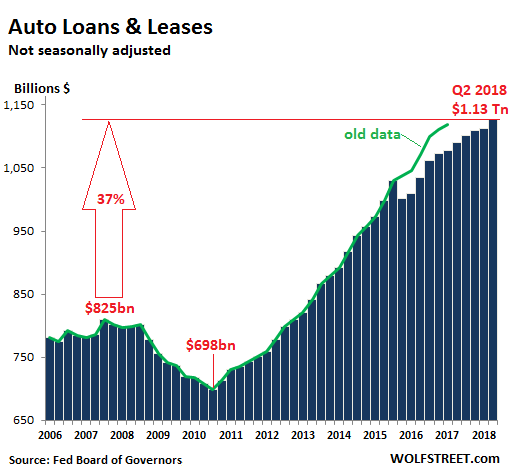

Auto loans and leases

Auto loans and leases for new and used vehicles rose by 3.6% from a year ago, or by $40 billion, to a record of $1.13 trillion.

The percentage increase is in line with the past four quarters, but a far cry from the peak of auto euphoria in Q3 2015, when auto loan balances jumped by 9%. Loan balances are impacted by prices of vehicles, including the mix of new and used, number of vehicles financed, the average loan-to-value ratio, duration of prior loans, and other factors:

The green line in the chart shows the old data. In September 2017, the Federal Reserve adjusted its consumer credit data going back through Q4 2015, based on survey data collected every five years. The adjustments hit auto-loan balances disproportionately, knocking them down by $38 billion retroactively to Q4 2015. To show the distortive effect of the adjustment – and to show that it wasn’t the collapse of the car business – I added the old data in green.

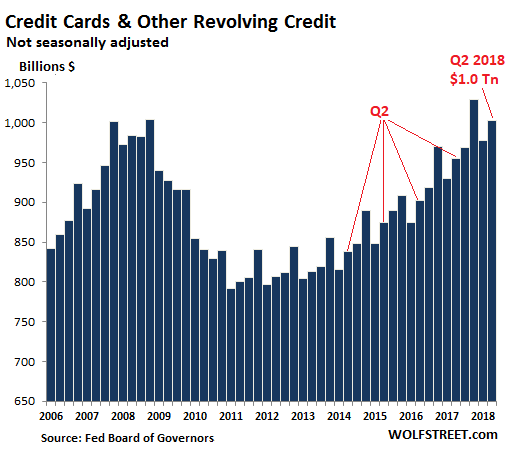

Revolving credit

Credit card debt and other revolving credit in Q2 rose 5% year-over-year to $1.0 trillion (not seasonally adjusted). This growth rate was down from the spectacular 5.6% to 6.8% increases from Q4 2016 through Q4 2017 (the “Trump bump”). But it’s still among the biggest increases since the Financial Crisis. On a quarterly basis, in line with seasonal patterns, it rose by $24 billion from hangover-Q1 that invariably follows the shopping-season debt-pile up in Q4:

A special note about the records in credit card balances: The $1.03 trillion in Q4 2017 had been an all-time record, finally beating the records of the fourth quarters in 2007 and 2008. And Q2 2018 set a record for any second quarter. In the history of the universe, these revolving credit balances exceeded the $1 trillion mark only four times: three of them in fourth quarters (Q4 2007, Q4 2008, Q4 2017) and now suddenly in a Q2.

So Americans are nailing it with credit cards, the most profitable form of lending for banks, where interest rates can exceed 30%, though the average cost of funding for banks is still below 1%. This is a deal made in heaven for banks – until consumers collapse under this high-interest debt.

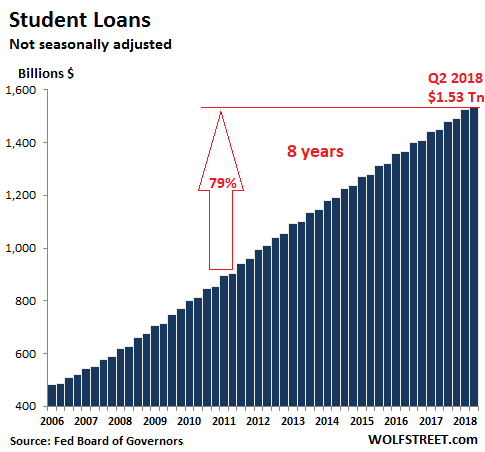

The Student-loan economy

Student loans in Q2 jumped by 5.8%, or by $84 billion, year-over-year to $1.53 trillion (not seasonally adjusted). While this may sound like a shocking increase, it’s among the slowest year-over-year percent increases going back to 2007; up through Q3 2012, year-over-year increases ranged from 11% to 15%!

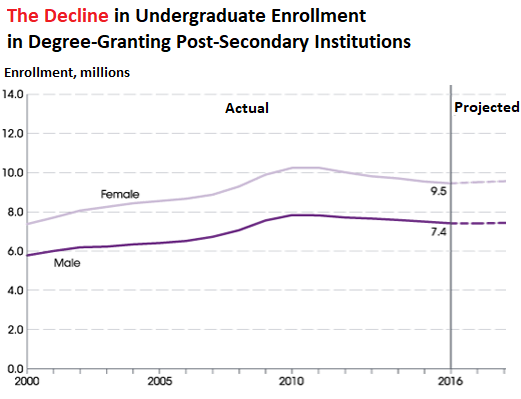

But wait… Higher-education enrollment peaked in 2010. In the eight years since, it has declined for both male and female undergraduate students, according to the latest data available from the National Center for Education Statistics (updated in May 2018). Total enrollment in 2016 fell to 16.9 million, down 6.6% from the peak of 18.1 million in 2010. This chart shows male and female enrollment, actual and projected, via NCES:

And yet, over the eight years since 2010, as enrollment has dropped, student loan balances have soared by a dizzying 79%, or by $976 billion, from $855 billion to $1.53 trillion.

But it’s good for the economy, no? Whole industries have mushroomed around this manna. Investors in for-profit colleges; the student housing industry; companies like Apple that sell students can’t-live-without gadgets and services; the ravenous textbook industry; overpaid top administrators; construction companies building university-owned trophy projects; banks; they’re all getting fat on this manna. It’s just that future consumers and finally taxpayers are now on the hook for $1.5 trillion.

In terms of consumer debt, it’s not those consumers with high incomes and plenty of money in the bank who are paying off their credit cards on a monthly basis that are at risk. It’s consumers who use their credit cards to make ends meet, who carry large balances and struggle to make minimum payments, and who have no money in the bank. That’s where the risks are – with the most vulnerable 25% on the consumer-credit scale, the very ones who carry a disproportionate amount of very expensive credit-card debt that can be devilishly hard to pay off or even service.

This is so thick it’s hard to believe. It’s far beyond just a Brick & Mortar Meltdown. Read… Mattress Firm Considers Bankruptcy to Get Out of its Real Estate Scams

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wolf, thanks for yet another enlightening piece. I can’t stop worrying at what point the burden of debt becomes so overwhelming that Americans transition from a tax-the-rich clamor to a French-style revolution. The Romans had several revolts from debt slaves. The revolts usually ended with a blood bath but sometimes they resulted in blanket debt-forgiveness. But then, they didn’t have the means of control that financial institutions have today. With that level of control there seems to be no end to what financial engineering can squeeze out of debtors.

Is there some sort moral or ethical issue with taxing the rich?

I don’t understand how this is a political talking point… They don’t pay taxes really as is.

Why do we never hear some idiot on TV bringing this issue up with that tone about taxing the middle class?

To ask…

“Socialism never took root in America because the poor see themselves not as an exploited proletariat but as temporarily embarrassed millionaires.”

–John Steinbeck

Exactly. Good Americans who’ve always been exploited by the upper classes have internalized the top-down class war. Any American who covets yet cannot afford three yachts knows it’s the lower classes (especially lower class brown people) who are to blame.

Good Americans always punch down, never up.

Harrold quoting a communist …wow.

Two beers, The powerful have always exploited the weak. However, in the US, there has been the opportunity to strengthen your financial security and even become “rich”. Why spend your time punching up or down, when you can punch ahead? Envy is self-defeating. If someone is poor in the US, there is a good chance their flaws will continue to separate them from any wealth confiscated from others through political force.

In this case/topic, Consumer credit is like food. Manage it wisely and you are strengthened.

All games have always been and are “rigged” and the best example is the game that goes on inside our own heads. Stop ranting about the rich and just go get rich! And help some people in the process if you value happiness.

Thanks for that, Harrold!

I’m going to use it in some of my writings.

How do I credit it – “John Steinbeck by way of Harrold”?

@Setarcos

That social class mobility you are hinting at is a lot smaller then people (including you) think.

Its actually more important to be born by the right parents at the right place if you want to “punch ahead”..

I am not saying it don’t exist, just that for most people it will not make a difference how much or how hard they work.

All we can do is keep trying, just as some buy lottery tickets and hope for the best.

If we all could get rich, we would all be poor..

At Setarcos – First why do you assume people are envious? I think disgusted and outraged at the sense of gross injustice and waste is more to the point. Second, it is a given that the class you are born into is pretty much going to define your position in life and that’s true now in this country than in any time since the 1920s. Third, it is just an absurdity to tell someone to get rich; it’s akin to telling the masses to go eat cake. 3 individuals in the US own 40% of the wealth in this country. 3! The 9.9% of the population is doing great since they toil to ensure their .1% masters accumulate greater wealth, mostly as accountants, lawyers, lobbyists, etc. where they spend their lives wearing down laws and the tax codes written to allow the country to have a thriving middle class. Envious? How about sickened.

Golden Rule : He who has the gold rules.

Correct!

I do have a moral and ethical issue with progressive taxation. And, you’re right that our IRS tax structure is not an equal playing field in terms of taxable percentages on various types of income.

It’s been quite a while since I’ve advocated a modified flat tax here in Wolf’s comments, but I do believe we should have this: A living wage – say $30,000, carries no federal tax liability. All income thereafter should be taxed at an equal percentage – say 20%. This would provide a safety net for those who’re just getting by, it would not financially punish success as progressive taxation does and it would not allow ultra wealthy citizens from paying lower tax rates than workers who’re in the high tax bracket for wages.

Right now, wages are taxed at 10% to 37%, but long term capital gains are 0%, 15% or 20%. Everything should be the same no matter what kind of income and no matter how much income!

Hey look a tax plan that fits on a post card.

We chewed this over in the past. A flat tax with some relief at the bottom. Say the first $20k or $30k not taxed.

I’m paying 20% off the top and make about $15k so yeah, to me this sounds good.

In my humble opinion, progressive taxation is much more fair for a couple of reasons.

First, the use of funds progressively changes from meeting basic needs, to meeting basic wants, then exotic wants, then merely controlling the lives of others with no real gain in personal comfort.

Second, the ease of getting the funds progressively changes. A worker will labor like crazy to meet basic needs, but work that pays more starts involving the powers of privelaged positions, the leveraged resources of others, and the scalable gains from the same work re-sold, none of which should pay as much as the initial hard work.

The plan would work only if applied worldwide; otherwise, capital flight from the U.S. would defeat it.

No chance of such an application, IMO.

Why should capital gains be taxed at the same percentage when investment carries the risk of loss?

Moronic.

Timthetiny – Moronic? So you’re saying you can’t expense capital losses at the same rate as capital gains? Capital gains should be taxed a higher rate than earned income. If not then what we’re really saying is that actual real work where real value is created is subsidizing people who create nothing.

To Timthetiny:

Capital gains are just that; hence the word gains. In my ‘investment’ portfolio, I have some winners and a few losers. The IRS is only interested in how much I make from selling stocks, in total, at the end of each year for my capital gains. Gains which Uncle Sam and Minnesota take a portion of.

To MarkinSF:

Owning stocks has a role in a free-market economy: Company X issues stock. Company X now has capital to invest in its endeavors; endeavors which employ people and helps fuel the economy. Individuals buy Company X’s stock hoping the stock increases in value and pays a dividend.

Should capital gains incur a higher tax rate for those who sell Company X’s stock at a profit after holding the stock for over a year than the tax rate for employees’ wages at Company X? Now, the employees can pay up to 37% depending on how much they earn, but sellers of stock pay at most 20% of their profit. Again, I believe the tax rate should be equal for all at 20%.

We all have our own opinion on what is fair and just. Thanks go out to Wolf for letting us state our case(s).

Actually, those making over $100k pay about 80% of the tax paid now.

Did you want to take it all and take away the incentive to build businesses?

demand from customers create jobs, not rich people.

do you not know better or are you purposely gaslighting people?

The incentive is gone now. Small businesses, the kind that grow, are fewer and fewer every year.

…a statistic which amply demonstrates the massive, socially destructive wealth disparity afflicting the contemporary USA (and all other countries that have adopted the same neoliberal economic models).

Also, no-one ever in the whole of human history has ever been discouraged from improving himself by the prospect of having to pay more tax – that’s just one of the myths (lies) that has been peddled to you to ensure the wealth gap keeps growing.

After all, no–one would have done a lick of work in the ’60s if this hypothesis were correct, would they?

Owning stocks has a role in a free-market economy: Company X issues stock. Company X now has capital to invest in its endeavors; endeavors which employ people and helps fuel the economy. Individuals buy Company X’s stock hoping the stock increases in value and pays a dividend.

While this *MAY* have been true at one many year ago, the large majority of stock sales generate nothing for the as these are secondary market or resales.

Even when a stock sold is an IPO, much of the money is skimmed for underwriting fees,etc. and to cover stock options for for the VCs and/or employees who received stock options rather than money during the early startup phase.

Wish it was otherwise…..

chillbro

Calling bullshit on your statement : “…Is there some sort moral or ethical issue with taxing the rich? I don’t understand how this is a political talking point… They don’t pay taxes really as is…”

Top 1% = $458k+: 39.5% of income taxes (20.6% of AGI); avg tax rate 27.2%

Top 50% $38k+: 97.3% (88.3% AGI); avg tax rate 15.5%

Bottom 50% below $38k: 2.7% (11.27% AGI); avg tax rate 3.45%

Other than 6th grade ad hominems, citing your numbers and source would be more convincing.

Source: https://taxfoundation.org/summary-latest-federal-income-tax-data-2016-update/

Wrong. Capital gains rate applies to income of top 1%, not the 39.5% rate. That’s why Buffet pays a lower rate than his secretary.

Bobber:

Nice try at obfuscation, but the above figures are clearly stated as “income tax”.

We could also have a conversation about capitol gains, but that simply skews the tax-paying percentage higher for the >50% earners…

You need to include payroll taxes, or your message is biased. Payroll and income taxes are both federal taxes that have to be paid, so you need to look at them as a bundle. Once you do that you’ll see the tax burden isn’t as progressive as it should be, at this time when wealth inequality is as high as the Great Depression.

…and yet look at how prosperous (real general prosperity – not just the conspicuous consumption of the privileged) the USA was in the ’60s when taxes for the wealthy were massive – and they didn’t all leave.

Exactly why the likes of the Kochs have spent so much money on propaganda to to convince gulls such as yourself that they and their like really should pay less – and lied to you in telling you that all will benefit from their subsequent munificence.

Meanwhile, large parts of your society go to hell in a handbasket, because there’s no money for infrastructure investment or social programs.

Enjoy!

There’s ways for the rich to hide their income from taxes. etc. You are very naive. The Panama Papers scandal just a couple of years ago is just the tip of the iceberg.

https://www.salon.com/2013/04/12/10_tax_dodges_that_help_the_rich_get_richer_partner/

Rates:

Panama papers were great.

Except it didn’t catch very many USA citizens. Got lots of USA names?

Javert. You are right. But that led me to this: http://fortune.com/2016/04/20/panama-papers-us/

Why go to Panama if you can hide your taxes in the US? LOL. And you are dodging my earlier link. No comments on that? Salon is an American website.

Also this: https://en.wikipedia.org/wiki/UBS_tax_evasion_controversies

19K US accounts in Swiss alone for tax evasion.

You are either naive or you are one of them.

It really is appalling to read some of the comments with respect to taxation. First a bit of history.

Yes the marginal rates in the 60’s were close to 90%, BUT the effective rate for the top 1% was around 20%. Today the marginal rates are at 39.5 (well now 37%) and the effective rate for the top 1% is …. what for it… around 21%. So next time someone has the urge to bring up the 60’s and taxes, please for the love of God don’t its embarrassing.

We were prosperous in the 60’s because the US was the only really economy. Not because our tax system was excessively progressive. We struggle now because instead of real investments, we consume, consume, consume. Sheep. Shave them twice a year and feed them and they will buy all kinds of crap a politician tells them.

As for Payroll taxes, again, please know your history. This is not income taxes but a defined pension plan payment, i.e. Social Security. Which if we are lucky and the Government doesn’t total screw it up, not counting on, your SS benefits are a function of what you paid in plus the Corporate match.

who owns the TV networks, chillbro?

The “rich” pay a lot more taxes than you suggest.

And what about the bottom 50% who pay no net income taxes inclusive of EIC?

I don’t think those were “debt slaves” (the Romans), but rather, actual slaves!

I am a big fan of sign up and get lots of points , why yes I would like a free trip to Europe for only spending $3000 and you will waive the fee, Thanks !! .Sure I would love $400 worth gift cards for spending that amount you want , I can’t promise I will be a customer next year but another bank will be happy to oblige me .

Power corrupts in direct relationship to the degree of power.

Absolute power corrupts absolutely.

Plutocracy is a form of control in which a relatively small ruling class of the wealthy, wields extraordinary power over the remainder.

Mingling money and power, politics and business, while bending the rule of law to it’s own self interests.

With all the current information and data available, what are the chances of a recession or depression going forward?

Another interesting metric might be comparing the increase in consumer debt with the increase in consumer income.

And I guess, why shouldn’t people borrow more? Trump and Congressional Republicans are leading the way!

Kent

Actually, as Wolf pointed out, 50% ($84B of the total YOY $176B) was increased student debt.

Basically:

Roughly 20M domestic college students ran up an additional $84B of student debt

The other roughly 220M adults ran up the other $84B of debt.

Said another way, college students are running up debt 11 times faster than the general population. As Herbert Stein said, “If something cannot go on forever, it will stop”

Not just college students. Many retirees are still paying off (or defaulting on) student debt.

https://www.huffingtonpost.com/entry/student-debt-elderly-poverty_us_58595c6be4b08debb78b2f2a

I also read last week (I think it was the NYT) that a huge percentage of those with credit cards debts landed there because of medical bills.

If you have a $5-10,000 co-pay to access your ObamaCace “insurance”, how do you think people pay it?

What is not discussed much is the aging of debt. True, debt is not increasing by past amounts but that is simply because many are maxed out! It is a little scary that so many people are using credit cards for daily expenses just to survive. The crash will come on Main Street not Wall Street!

Partly true, talking to a lot of my coworkers though, they’re frustrated that every time they make a bunch of money from working overtime with the intention to save it their wives end up going wild at Target when they see the money in the bank and end up overspending on the credit card too. Funny thing is they notice it doesn’t seem like much stuff makes it home before the money is all gone anyway. A dollar doesn’t seem to go that far as guys I know brag about making $150k a year or lesser but still high amounts while in cheap housing situations acquired before the latest bubble, and then have nothing to say for themselves when they realize all that money is gone and they have no idea where it all went. Thrift is dead in many American households (and as a side note if I press them they will admit to some of their own expensive completely unnecessary expenses for stuff they don’t even use, so the wives should not get all the blame).

Yeah only women spend money. Men get showered with their cool cars and electronic gadgets as manna from Heaven.

Target and Amazon are my 2 enemies. Everyday I see a couple boxes from Amazon at my front door or a couple bags from Target, all bc of my wife.

She has 0 spending control. Luckily our overall expenses are below our means, but, that’s about an extra $1k per month used on junk that I could be applying to principal mortgage pay down. I learned a great deal from the 08 crash about saving and living within (and below) my means, amazing more people cannot just delay gratification or value their hard earned money more.

Can relate Rhodium. Sometimes we can get crazy with money especially after a lean snap. Organize priorities first.

Western Capitalist “Market” Economies are Pyramid Scams. The Taxes extorted from the Ignorant Poor Multitudes become Tax Cuts for the Rich. Large Companies get special deals from the IRS, such as Google, Amazon, Facebook, Microsoft etc. Companies fed by the Pentagon get paid whether their Products work or not. The Pentagon`s paid-for Senators and Congressmen vote for useless Missiles to be made in Plants built in their Towns of their Taxed Voters.

You Speak So Much Truth I’m Fine With All The Capitalization.

The system is broken, we all know that. I have often wondered if a fairer system would be no income tax at all, so the harder you work and the more you earn, the better for you. An incentive to work. BUT to balance that, 30% or something similar, sales tax on everything. The more you spend, the more you pay. So the rich would pay more with them buying Lambos and yachts. Yes the poor pay more relatively, but surely it’s an incentive to go out and work, as income is tax free, whereas benefit isn’t (as you spend it and hence get taxed.) And at the end of the day, we all spend it somewhere so in the end it will get taxed.

And if you are smart and save, no tax as you aren’t spending it. Good for you, the economy and (those bastards!) the banks, as they can lend it out to people to invest in businesses etc. So an incentive to work to earn and save and not simply spend.

Or am I missing something here?

Work and save and not simply spend…money has valu e precisely because some people borrow and spend, otherwise your savings will be worthless mr. Scrooge.

There is a third option, which is to invest savings.

Further, it should be obvious that we are discussing a small fraction of most peoples’ discretionary income.

Obviously, everybody cannot save all their money.

Not a constructive comment.

The ultimate goal, in my opinion, is to create an economy where the income of individuals is ranked in a linearly increasing fashion tied directly to their productivity or impact on productivity. So the most productive people make the most and least make the least.

However in modern society things like investments and speculation cause a kind of runaway wealth accumulation effect where a persons money can earn far more than their labor or ingenuity ever would. So at a certain point a person makes enough money to where their ability to generate wealth grows exponentially faster than someone who must rely on labor and good ideas alone for income.

Progressive taxation is an attempt to reign in this run away wealth accumulation and redistribute that wealth in a way that helps increase class mobility.

So that those at the lower ends receive ample opportunities to increase their wealth through hard work and growth. Instead of being squashed by an elite wealthy minority.

Most peoples gripe here is that the money that is confiscated is used extremely poorly by the government.

You could write books about why progressive taxation currently fails to achieve this end. In any event progressive taxation has been undercut systematically for decades by things like the current capital gains tax rates.

Peter, I’m uncomfortable with the idea of someone earning 30K paying nearly 10K in sales taxes. How can someone possibly live on 20K? I’d much rather endorse a flat income tax and except the first 30K.

Make food tax free and that 30k person can have relatively little taxes.

High sales taxes are always great for promoting a huge black market and I’m all for that so yeah.

Yes, because the rich would simply form a limited company some way or another and buy the goodies under the company name and…….wait for it, deduct costs as business expenses. Baseball season tickets, boat for entertaining, business trip to europe, etc.

I know it’s considered maybe a bit, “radical” but why aren’t “families” allowed to deduct their expenses as business does? Yes, many are not very “responsible” with money but so are many businesses.

Why don’t more families “incorporate” so as to take advantage of the corporate money laws? Maybe there are laws that prohibit such action. None of this makes any sense anymore. We are now in a more than 10 years into this so-called “recovery” and too many individuals, families are back in the same old mess……too much debt. The same with the country. We no longer use “billions”; we now talk in “trillions”! Either we have very smart bankers or very dumb citizens. When those citizens wake up and realize that they are being fleeced they will rummage for the pitchforks.

Especially like the comments here; reminds me that there are various slants to how numerous people view our economy and what should be done if anything.

We are really playing “monopoly” with our system. And with “monopoly money”……..

As an extension to your suggestion, eliminate all corporate taxation, as that is a capital base that can create jobs.

Instead, tax ALL income as earned income, including specifically dividends and capital gains, and eliminate the cap on payroll taxes.

Question, Wolf-are there any metrics to contrast credit-usage increases vs. amount ‘maxed-out but performing’ vs amount non-performing and in default (although it would seem that the latter two figures are insufficient to seriously worry credit issuers, even if my layman’s instinct is to feel they should)? Thanks again for an always informative site. A better day to us all.

I would love to get such granular data. In terms of delinquencies and charge-offs, I get national averages (I’ll post those when they come out later this month). But I don’t get the granular data a big bank has about its customers.

You can assume that delinquent credit card accounts are probably … mostly … maxed out, for the reason that if you have room left on your credit card, you can get a cash advance on this credit card, put it in your bank, and make the minimum payment on that card and other cards (yeah, people do that!). It’s when the cards are maxed out that the consumer runs out of options and falls behind with minimum payments.

Wolf,

The NCUA filings for credit unions show some more granular data on their quarterly call report data. Credit union loan delinquency has actually slightly declined as a percentage, at the same time as average loan balance is climbing.

https://www.ncua.gov/analysis/Pages/call-report-data.aspx

Surely not the whole picture, but thought everyone might find it interesting.

Interestingly, the savings rate is also going up, and is somewhere from 5% to 7% depending on whose statistics you believe.

However, I suspect that the people saving and the people borrowing are entirely different sets. This means that the actual debt is higher for those who borrow, and the actual savings rate is higher for those who save.

Of course, if nobody saved, there would be no money to borrow.

->Of course, if nobody saved, there would be no money to borrow.

Such sarcasm. Fractional reserve banking guarantees there will always be plenty of bait available for loansharking. Self-financing isn’t profitable to them.

You nailed it. Savings rates apply to people who save, and they’re saving more. But credit card balances apply to people who have to borrow on their credit cards and carry balances, and they don’t save. If they had money in the bank, they’d pay off their credit cards.

These are two different sets of consumers. So savings rates could increase sharply because these consumers are doing really well; and credit card balances could rise at the same time, as other consumers are starting to stretch to buy what they need or want to buy. There are a lot of consumers in both groups.

And in the end, the government nails out the banks who has to write off their loan losses. Then we get rounds of tax increases that are bore by the savers.

I am actually not sure who the real suckers are here as I look around the table. Which means the sucker has to be me, the guy who pays off his credit cards, saves and pays his taxes.

In the name of the immortal Peter Simon Gruber: “God, I love this country.”

Actually, I wouldn’t be surprised if a substantial number of people were both putting money in their 401K every month, and running balances on their credit cards.

You know my first thought is that makes no sense at all. But then, this is the American consumer we’re talking about, sense is out the window.

My parents did exactly that consistently for the last 20 years. Then on retiring, they borrowed on the house (maximum) to pay back the cc’s. They can now enjoy their old age with a freshly minted 30 year mortgage at 3x the 1985 purchase price.

The sheer scale of American financial irresponsibility is truly impressive, particularly the skyward trajectories on all fronts. It’s a real testament to the modern techniques of saturation marketing, mass manipulation, status envy, wage suppression, inducements to profligacy, and animal husbandry. This is the way it is when you’re in the herd.

Soon it will all end and we’ll enter the Much Wailing and Gnashing of Teeth Phase, which hopefully will end, someday. They’ll never know what hit them. They never do.

Don’t worry about me. I’ve arranged things so you guys don’t take me down with you.

There’s the financial system, and then there’s physical reality. We are actually producing all the goods and services we are consuming. Can we ‘afford’ them? In fact, we could produce a lot more goods and services if we wanted to, if the effecive demand was there.

Oh my.

“We are actually producing all the goods and services we are consuming.”

Are “we”?

Who is “we”?

Last trip to Walmart, I couldn’t find anything made in America, and last I knew, there was a half-$Trillion trade deficit.

Something changed?

Likewise – don’t worry about me, I will be fine and I should be able to help my family if needed (but don’t plan on doing such, so they too can learn to take care of themselves). Such antiquated concepts “family” and “parents” and “personal responsibility.”

I generally view the borrower (who initiates ALL loans) as the primary source of the problem. Don’t accept the lenders money. Personal responsibility, discipline, delayed gratification. People are able to withstand the marketing, manipulation and envy and are therefore not doomed to the herd. But people make bad choices — and the question becomes should they bear the consequences of those bad decisions or should I have to pay for the bad decisions of others.

You generally do not have to borrow to “survive.” Most debt is not spent on things needed to “survive” nor on things needed immediately. Stop spending on restaurants (incl coffee), movies, cell phones, cable tv, more than 3 pair of shoes, a living space larger than 1,200 sq ft, a car less than 8 years old, any pets, chewing gum, beer, etc., etc., etc. Stop spending. You don’t need it and can’t afford it (if you have any inclination to take care of yourself and your family). I know — a barbaric existence.

Soon it will all end? I wish that was true but the reckoning seems to keep getting postponed longer and longer. For his believers, Trump has repealed the law of gravity and what goes up can never come down. Hurray!!!

So in a few short years (eight) that the average student loan has gone from about $47k to $90k. Yes, today’s youth are becoming more enslaved to the banking system.

I agree a revolt would be a blood bath, but not for the Elites. They have planned well for this possible situation. They control the food, health care, housing, and have stacked the deck with a huge military.

Giving 18-year-olds the ability to sign up for student loans without parental consent is simply criminal. Period. End of Sentence.

Damn few 18-year-olds can understand $20-30-40+ thousand of debt.

So in the prior crisis, households were so debt burdened that they deleveraged by the tune of a whole $200 billion just so that they could add on another $1.4 trillion in just 8 years?

Yes siree, we learned our lesson alright. Lending standards are so much higher, yada yada yada. And home prices and the stock market can only go up. Yeah, it’s different this time alright.

Sorry Wolf, but comparing nominal debt growth to real GDP growth is pretty meaningless.

You should either compare real debt growth (in constant dollars) to real GDP growth or nominal debt growth to nominal GDP growth.

If you really want to get picky:

1. Consumer price inflation and GDP (nominal or otherwise) are irrelevant in figuring consumer debt burden. What matters is wage inflation.

2. Wage inflation at the top 50% is irrelevant in figuring consumer debt burden where that debt is actually burdensome, which is at the lower 50% of incomes. This is where credit the problems happen.

I added GDP and inflation figures for sense of perspective, as I said – not to analyze credit burden.

Why not a flat 10 percent for individuals and businesses? So the special interest would lose their advantage and politicians would lose all those campaign contribution dollars. But the country would be better for it

Maybe because it would need to be 25% to be revenue neutral?

Although not seasonally adjusted, are the consumer debt charts adjusted for inflation?

I mean, I’d rather owe a million bucks today, than 100 grand 50 years ago.

It’s not (as I noted above), and that’s the problem with this analysis.

Nominal debt growth was 4.8% but nominal GDP growth was also 4.8% so in real terms consumer debt growth is growing at the same rate as the overall economy.

See my reply to your first comment above.

Actually, all such numbers are very difficult to interpret in depth.

As a simple example, please go back to comments about savings and debt, both which are supposedly growing now.

They are undoubtedly two distinct groups of people!

I suggest to you that the 4.8% growth of debt and similar growth of GDP are, again, two distinct groups of people.

Wolf, is the credit card debt adjusted “per capita” for population growth? We probably have at least 30+ million more people in the U.S. now since last peak.

Education and health care are two sectors in our economy that still live in the corrupt shadowy old days and haven’t been modernized and “disrupted”. There are a lot of people getting ripped off so certain folks in those systems can make a ton of money. And the people who make a ton of money in these two sectors will fight like hell and spend tens of millions on lobbying and fake PR/media campaigns to make sure the status quo does not change and they can continue to rob Americans blind.

I got a college degree, and for me college was mostly a waste a time and money. I have had a number of different business careers so far, and have never needed to use anything but basic math, basic reading and basic writing I learned in high school. Everything else I learned was on the job, from books, and my own learning. I wasted a ton of time on stuff I never used and sat in class bored all day. Would have been better off in some program where I actually got skills I could use IMMEDIATELY ON THE JOB. Our universities should be much more closely aligned with skills most needed in society. Too many under water basket weaving majors out there.

Don’t worry about the lack of disruption, Tim, Mark, Jeff, and Sundar will get right on it. Because those nurses, doctors and teachers should all be replaced with robots.

Remember, the only one who should be immune are CEOs and lawyers.

Our universities should be much more closely aligned with skills most needed in society.

Should they, Really?

The first problem is that “society” doesn’t know what skills it wants/needs 5 years in advance. The USSR and China texted this. So we don’t have to.

Second problem is that in a free society, people educate themselves for their own benefit, especially when they have to pay exorbitant amounts for that privilege.

Thirdly, there are not that many skills actually needed. Society )and business) has to do something with the superfluous talent or the economy would go in the ditch.

The “basket weavers” are simply on a special unemployment scheme only for academics. Keeps them busy, the numbers good, prevents social unrest and there is always the possibility that they may come up with something. Scott Adams, f.ex.

I do think we should make most education much shorter, cheaper and accessible – so people could go in and out of education as it was needed. Although For some degrees, there is only the hard long slog.

My grandson is going to welding class it costs $10 per class and there are only 3 students. Tulsa technology center. They also have plumbing and other construction classes. We’re so happy stacking silver instead of debt.

$10 per class hour.

I hear that girl and I’ve been reading that Silver May go lower Say 12 dollars or so It might however be difficult to find at that price Gorgeous cool sunny morning here from Nowy Swiat Street in Warsaw

It’s OK! I’ll just invest in bitcoin …

https://www.cnbc.com/2018/08/08/bitcoin-price-falls-after-sec-postpones-key-etf-decision.html

Waitaminute…

Alright, you will be a billionaire in no time. Hope you will subsidize me.

Debt “slave” connotes someone doing something against their will. Perhaps debt whore is more apropos?

When you are having a conversation about a tycoon from South East Asia one of the questions that will pop up is “Who is his chief slave?”.

This slavery is not of the financial kind: all chief slaves are lavishly compensated for their services. Annual earnings over US $10 million plus perks such as prime real estate in Hong Kong or Kuala Lumpur are not exactly rare.

To an untrained eye, these chief slaves also wield enormous power, being their bosses’ right hand men, tasked with directly negotiating large contracts with foreign partners and taking many other important decisions.

Yet they are more pitied than envied. Why?

Because the high sounding titles and huge financial packages hide a reality of long grinding hours, very little, if any, freedom of action, having to obey often extremely demanding bosses and no prospects for advancement: when the tycoon dies the chief slave can, at very most, be graciously allowed to serve his heirs, but more often than not he’s handed his notice and replaced.

The poster child for “chief slaves” was Richard Liu, who famously broke down in tears during an important business meeting due to the demands of his boss, billionaire (in US dollars) tycoon Robert Kuok, and ultimately died of a stress-induced stroke at the Kuala Lumpur airport. Liu left his heirs an authentic fortune, but had hardly lived the life of the high level executive he was.

That’s the kind of slavery we are talking about here, the voluntary one.

” Total enrollment in 2016 fell to 16.9 million, down 6.6% from the peak of 18.1 million in 2010. ”

I’m not sure what’s going on today but it was once the case that when you were approved for a student loan you were given, say $10,000 and you could do anything with it. ( one guy I know put it all into the stock market, another bought a used Audii)

Since today’s tuitions demand many tens of thousands of dollars, could we not assume whole families are now being supported by these mega -loans? Certainly Apple is being supported. Every kid a the local college has an Apple laptop, and I assume they’re all from student loans.

Shodan

Your local college is sucking upmost of this “student loan” money. The higher the loan amounts, the higher tuition.

Since 1980, college inflation grew 260% while everything else increased 120%.

Depressing. That’s all I have to say. The thing is, my dad told me to establish credit when I was 18. He cosigned on a 1980 yellow long bed Toyota pickup. I lived at home, worked construction and paid it off in less than 3 years. I’ve NEVER carried credit card debt my whole life. Paid it off each month. I’ve never been without a job since I was 151/2 years old. Even though I’ve been responsible, saved and no debt, and worked hard my whole life, my cash savings have been decimated by money printing. All of the greed and entitlement has hurt people like me. Things look bleak for the good old US of A.

Joe Your bio reads exactly like mine but my truck was a 1978 Jeep J10 and I did ALOT of flat roofs in Queens and Brooklyn with that puppy Would do it again No regrets

Yep … you are a prime example of how f’d up things are … being responsible and avoiding debt like the plague and saving … and it all gets trashed by the moneychangers. Both these shitty political parties lie so much it’s mind boggling. Republicans tell everyone that ‘freedom isn’t free’ and spend huge amounts of increasing debt on the military and democrats spend on freebie type shit for slices of the demographic … yet all the big stuff that really matters is jobs and cost of healthcare, education, housing and transportation skyrockets … I’m sorry freedom doesn’t cost a trillion a year and there is no reason any job should leave the US except because politicians don’t give a flying fuck about the people. Govt financing as well as private financing of education debt is WHY the cost skyrockets … greed based (for profit ) healthcare is WHY it skyrockets … it’s all financial engineering and none of it is to make the country better for the citizenry … it’s all for the profiteers in public office and in private sector mega businesses

->Let the good times roll.

Yeah, right, living the dream.

But you wonder how many people can’t sleep at night. And you wonder how many wake up screaming.

I can’t be sad for all of them. I get maxed out at a few million. And I’m doing well if I can help out a couple here and there. I can’t change the system, and I can’t help its victims, so they’re just going to have to go down.

Wailing and gnashing of teeth I said, millions of them. You just can’t hear it.

I’m sure there are millions I was one of them back in 1981 with a young bride and baby You do what needs to get done It ain’t easy but it’s called growing up

Great article, Wolf.

Further evidence to prove that moral hazard has been binned.

We have a saying here “eaten bread is soon forgotten”, and this applies to the lessons forgotten from the great financial crisis

The DSR (debt service ratio of debt payments to disposable income) is considerably lower than the pre-crisis period and also lower that the average rate of past serveral decades. The average consumer is in much better shape than 10-15 years ago.

The bosses are hiring…confidence index has increased significantly in past couple of years so the consumer has come out of his/her shell and is fnally spending with a little confidence. After years of paltry credit growth except for student (the new free lunch entitlement) and auto (pent up demand).

Debt slaves is right, but a little less so now than before. My consumer-based hobby business, which is dependent on discretionary consumer spend, increased 60% in 2017 after years of being flat – all consumer demand driven.

Time for a Debt Payoff Lottery where the winner has all of his/her debts paid off in full, tax-free

Excellent analysis & empiricism here, Wolf. Calling peak Apple stock over the last week has not seemed to trickle down to the chattering classes yet but I, for one, most assuredly hear what you are screaming out on stocks & debt. Peak Apple & peak debt will be joined at the bar by peak liquidity too.

Things are going to get very frightening by January IMHO. All the best analysts are attempting to scream as loud as you are too. What scares me right now is that all the analysts are in full agreement but the MSM is ignoring the warnings outright. Denial of what you are stating is to be expected given how frightening it must be to realize that this Global Ponzi is going down for the count.

I am as confused as you are about the lack of professionalism in the industry, Wolf. The MSM has to step up to the plate very soon IMHO.

MOU

Do you have the inflation adjusted charts?

” It’s consumers who use their credit cards to make ends meet, who carry large balances and struggle to make minimum payments, and who have no money in the bank.”

========

I would expand that to nations using debt “to make ends meet”.

Yes, if they still have a credit card, desperate, hungry people will “choose” to use them rather than be homeless and beg and starve to death in the street. This is the lesson of today.

(Desperate, hungry people once “chose” to live in concentration camps and be worked to death rather than “choosing” to remain outside the camps and be shot to death. This is the historic lesson of late 1930s and early 1940s Europe.)

The US government, supposedly on behalf of The People, “chooses” to fund its wars to enforce USD hegemony on the world using “borrowed” — ie printed-out-of-thin-air USD, “backed” by drones — rather than pay for The People’s wars “up front”. Up to today, the one and only entity in the world that can create those USD out of thin air is the private Fed. (It remains to be seen if this situation can be sustained.)

When, not if, the debt slaves (including nations) can no longer pay even the interest on their debt, they either default or go to (most likely private) debt prision. (The prisons are paid for with, you guessed it, borrowed USD.) Rather than let the TBTF banks, that have loaned the printed-out-of-thin air USD to the bankrupt debt slaves, go belly-up, the US government will force the not-yet-born US taxpayers of tomorrow to “bail out” the TBTF banks of today, NOT the debt slaves of today. But from just exactly WHERE will the US government of today get the USD of today to bail out the TBTF banks of today? You guessed it.

The thing that the bewildered herd must some how any way be made to believe is that ANY amount of “money” to keep the TBTF banks from failing is “money” (debt) well spent. Great investments, TBTF banks and war corporations.

Regardless of what you know you know with absolutely certainty, there is absolutely NOTHING wrong with “the fundamentals” of the present economic system. All it needs is a little bit of minor, ’08-type tweaking now and then and everything will eventually turn out just fine for the vast majority of Americans and all the rest of the people of the world who are using the USD to conduct their business. So just give the present arrangement a few more years and everything will be “great”.

Does this number reflect consumer credit card balances, and does it in any way reflect how long those balances have been there, or is it just a case of people using CC to save money, cash back, flyer miles, in store discounts? I also ask where is the number on medical bills? Basically people who were on Obamacare are back to nothing? That apparently was an issue in last nights election in Ohio.

There will be a debt jubilee. There will be no other choice. All Public and Private debts will be canceled. The Greeks did it, the Roman’s did it (this led to the” Pax Romana” 200 years of peace). and the British Empire did it and had 400 years of growth of their empire. However, as long as the bankers run the world this will never happen. It would leave most of them bankrupt and quite a few imprisoned or missing their heads.

Willy,

What “debt jubilee” proponents don’t get is that, BY DEFINITION, someone’s “debt” is another’s “asset.” If you forgive the debt, you will wipe out those assets. If you forgive all debts, you will wipe out a huge amount in assets. In the US alone, you would wipe out close to $100 trillion (with a T) in assets. It means the total collapse of an entire economy. Your ATM card won’t work anymore. Savings are zeroed out. Your bank or credit union shuts down. Your accounts are empty. Your pension is gone. Social Security is history. Stores close. You can’t charge up your smartphone anymore because power-plants shut down…

Debt = credit = lifeblood of this economy.

Sure, you could selectively forgive some small amounts of debt and bail out the banks as it was done during the financial crisis — but that was only a minuscule portion of debt that was shed that way, and look what it did to the financial system.

These “debt jubilee” proponents need to think this through a little.

We have a system of debt restructuring, either in bankruptcy court or outside, that works pretty well. That’s what’s going to solve that problem in those places where it is a problem.

Dr. Steve Keen has proposed that the government give everyone a check for a fixed sum, and if you have debt you must pay it down. It is a modern version of a debt jubilee.

So where is that money going to come from that the government gives out? The central banks prints it, right? Keen has some good ideas, but he is just nuts with his theory on this point. If you give $50,000 to each adult in the US — in many cases not enough to pay off student loans, credit cards, etc.– that amounts to about $13 trillion. That would be about four times the amount of QE. It would wreak four times the havoc that QE wreaked. This is just nuts.

One assumes, then, that Dr Keen is a doctor of medicine?

It can’t be economics…..

Debts that can’t be repaid won’t be repaid. In the old days, banks that lent irresponsibly would experience a run and close down. Modern banks have no “skin in the game” especially in mortgage and student lending. Maybe you can invite Dr. Keen to write a guest post on this idea?

Todd H.,

We have bankruptcy courts that put a more or less orderly framework around the issue of debts that cannot be paid. It works. In bankruptcy court, debtors shed some or all of their debts, and investors and creditors pay the price, as they should, since they got paid to take those risks beforehand. The loss is the risk they took, and they know they took it. It’s that simple. There is no reason to get fancy or come up with silly theories.

Wow, if you print that volume of money we could become like Argentina.

Wolf,

So you’re saying that student loans can be discharged in bankruptcy and if I default on a mortgage that Uncle Sam (taxpayers) won’t make the bank whole? Modern neoclassical economics as taught in most colleges today is a silly theory that should be disposed of. Dr. Keen and others who try to develop models that accurately explain the dynamics of the economy should be commended.

Todd,

Student loans that are backed by taxpayers cannot currently be discharged in bankruptcy court — and that’s a good thing, in my opinion. But if Congress wants to change that law, it can. There is zero reason to invent or believe in crazy theories and monetary religions that will destroy the currency even more than is currently the case just to solve a specific and very solvable issue.

When the socialists take over America( which they will unfortunately ) There will be a debt jubilee. Free college, free health care, minimum annual income, etc! This will lead to hyper inflation and then all debts will be worthless. So charge it like there’s no tomorrow!

So then those of us that are paying for our kids to go to school rather than having them take out student loans are the real suckers, yes? I seriously do think about this every time I make that tuition payment (x2)… am I stupid?

As soon as I graduated university the Collection Agents started harassing me via phone & mail every day of the week except Sat & Sunday. I was harassed to the point of complete bankruptcy over the 10 years they had me on speed dial. Take it from a graduate of university that going into Student Loan Debt to fund education is a very serious Economics 101 mistake. Harvey Miller [Bankruptcy Lawyer] stated that Fuld went bankrupt because he leveraged 44:1 and make the rookie error of using Short Term money for Long Term Investment which is a rookie mistake that everyone in Economics 101 is taught.

Long term investment has to be supported for the long term, but if one is short-termist in terms of betting large at the table the whole supporting business model for the long term investment will be useless.

MOU

The sad thing is that when I went to college in the early 80’s when Reagan was President, Community College was free and I paid $500 per year in tuition at a State University while working part-time at a gas station at $4 per hour. At 20 hours per week, I paid my entire tuition bill in less than 2 months.

Now it is 15K per year for tuition and student loans are required since nobody can work part time to pay it.

Why can’t we just work to make America Great Again like when I went to college? Other than Bernie who was a contender, I see no progress in that direction under this administration.

I’m old so I’ve seen it all before. I know I got a good deal back then and I am grateful. I also know other countries like Germany, India, and China currently have similar college plans. We are losing our competitive advantage.

Why is this not a topic to be discussed during elections?

Please note that I don’t agree that any college should be free.

There should be some skin in the game.

When CA implemented free Community Colleges, it was a disaster, since it was free, why not sign up for 10 classes and then not show up for half of them?

They eventually charged $5 per unit ($50/Semester) which kept the abuse down.

State colleges and universities should tie tuition to minimum wage since that is what college students can make. If the tuition is tied to working 20 hours per week for 6 months at minimum wage, we wouldn’t have these student loan problem.

I just want to MAGA.

As some commenters pointed out, Wolf’s analysis above is missing a relevant denominator for the scale of the debt. More people, busier economy, should have more debt. But actually Wolf’s right that the increase is too much, too fast.

Here’s link to graph of total US consumer debt (spelled “credit” by the banks you owe it to), normalized to the overall size of the US economy (nominal GDP). It’s at an all-time high.

https://fred.stlouisfed.org/graph/fredgraph.png?g=kOCA

Never in the course of US history have so many owed so much of what they produce to others…

Is it possible then to see say total household debt as a percentage of total household income on a similar timeline for the US?

I know two people who claimed banckruptcy with over $100,000 each.In about three years they both got a credit card again.Its so easy in Canada!Just buy gold and silver or anything you can and sell it later and voila ,bankruptcy pays.Travel the world,live like a playboy!Garnish wages on credit card debt bankruptcy and we wouldn’t have this problem.

Wolf, 2008 dollars were worth more than today 2018 dollars.

Is the rise so high if you adjust by inflation?

Inflation is loss of purchasing power. Inflation can be expressed as an inflation index such as CPI, which rises; or as a loss of purchasing power index which falls by a similar rate. In this article, I gave you both, and they both say the same thing – one is politically correct (a “goal to achieve,” hurrah, well done, Fed), the other is the painful reality for wage earners whose labor loses purchasing power.

It is important to remember that much of the massive debt load hanging above our heads has not receded or gone away it has merely been transferred to the public sector where those in charge of such things feel it is more benign. By a series of off-book and backdoor transactions those in charge have transferred the burden of loss from the banks onto the shoulders of the people, however, shifting the liability from one sector to another does not alleviate the problem.

Writing off bad debt is usually a painful process and often results in a huge change in what something is worth. The creditor, meaning the person, business, or institution that holds the paper can suffer a huge loss. Defaults generally constitute an unplanned and involuntary financial adjustment. We as individuals should be concerned as to how defaults can spill over and affect our lives.

B Wilds: You have hit the nail on the head.

I don’t understand the aversion to higher tax rates on high income individuals… they don’t ever pay high tax rates … the big CEO and board of directors et al all get the vast majority of their compensation in the form of stock options … their ‘earned ‘ income pay is just walking around money till the blackout signal is given that allows them to sell their stock options exercised at a nickel a share and sold in the open market at whaterever the share price is and taxed at a capital gains rate which is very low like 15%. The stock option thing is a tax avoidance scheme and is akin to a company printing their own money to enrich insiders while fucking legitimate shareholders … as long as they keep the share price high shareholders don’t want to kill them. I’ve never heard an intelligent discussion of executive compensation schemes or of trade policy in over 25 years .. they promote shitty systems with sound bites like ‘well we need trade dumbass!’ Or defending these pay schemes as if the CEO is the only one who makes the company function even if he was never a founder. It’s totally inane .. so little intelligent discussion about it .. this ridiculous system cannot stand in perpetuity and it won’t. If I was a top level ‘executive’ getting paid several million a year with most of it taxed at a capital gains rate thru the stock option scheme .. even if my decisions destroyed the company within a few years I would still float off in a sea of money while everyone else with more invested in the company like a retail type investor, pension fund investor, or hard working employee … they get their ass handed to them … and the people most responsible for the demise of the company are mostly richly rewarded for it