Historic spikes in Seattle and other metros. But New York condos skid.

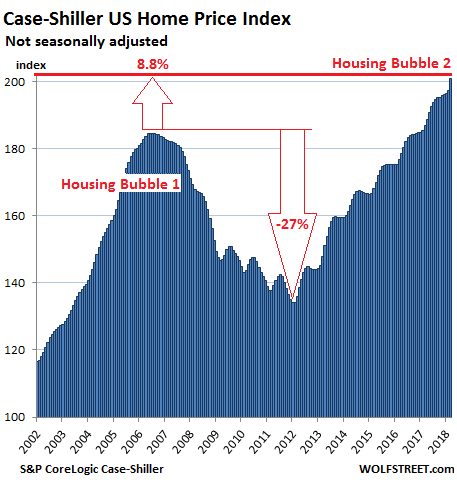

Prices of houses and condos across the US surged 6.4% in April from a year earlier (not seasonally-adjusted), and a sharp 1% from March, according to the S&P CoreLogic Case-Shiller National Home Price Index, released this morning. The index is now 8.8% above the nutty peak of “Housing Bubble 1” in July 2006 just before it collapsed, and 50% above the trough of “Housing Bust 1.” Note the disproportionate spike in April:

That 8.8% increase since the peak of the last housing bubble — “Housing Bubble 1” in this millennium — isn’t an increase over some state of languish that the housing market needed to exceed. It was the peak of the definitive housing bubble that then collapsed and helped push the global financial system to the brink.

Real estate is local though prices are impacted by national and global factors, such as monetary policies and offshore investors for whom “housing” in the US is an asset class and in many cases also escape route. These local and global factors inflate local housing bubbles. When enough local housing bubbles come together at the same time, even as some other housing markets remain calm, they turn into a national housing bubble, as illustrated in the chart above.

The Case-Shiller Index is based on a rolling three-month average; today’s release is for February, March, and April. The index is based on “home price sales pairs,” comparing the sales price of a home in the current month to the last transaction of the same home years earlier. The index incorporates other factors and uses algorithms to arrive at each data point. It was set at 100 for January 2000; hence an index value of 200 means prices as figured by the index have doubled.

So here are the most splendid housing bubbles in major metro areas in the US:

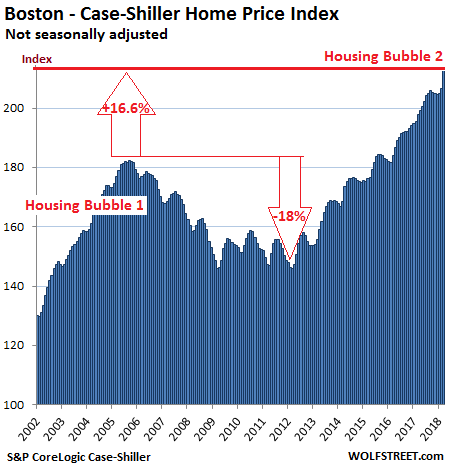

Boston:

The Case-Shiller home price index for the Boston metro jumped nearly 2% from the prior month and is up 6.9% from a year ago. During Housing Bubble 1, from January 2000 to October 2005, the index soared 82% before dropping. It now tops that crazy peak by 16.7%. Note the phenomenal 4-point spike in April, the largest such spike in the Boston data series:

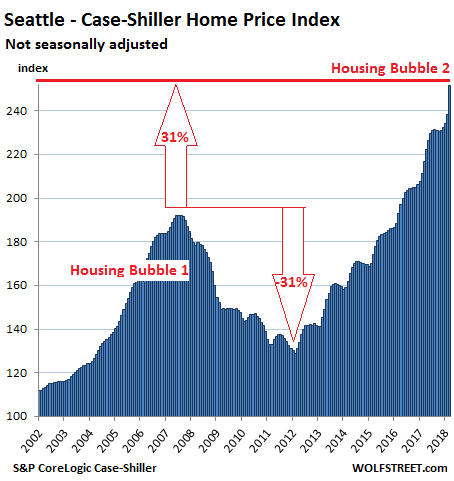

Seattle:

The Seattle metro index spiked 2.5% from the prior month. In terms of points, the index jumped 6.6 points, the biggest monthly jump in the data series. The index has now jumped 13.1% from a year ago and is 31% above the peak of Seattle’s insane Housing Bubble 1 (July 2007). Note the historic spike in April:

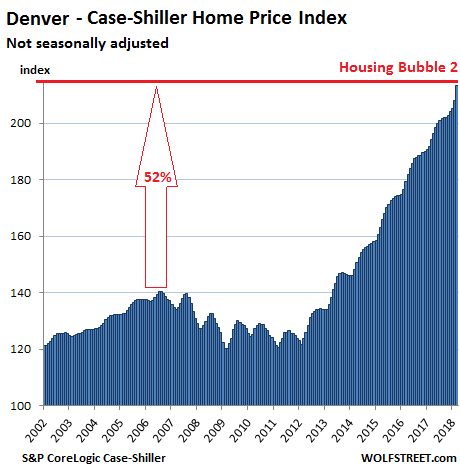

Denver:

The index for the Denver metro jumped 1.2% from March, the 30th monthly increase in a row, is up 8.6% from a year ago, and 52% from the crazy peak in July 2006, with a historic spike in April:

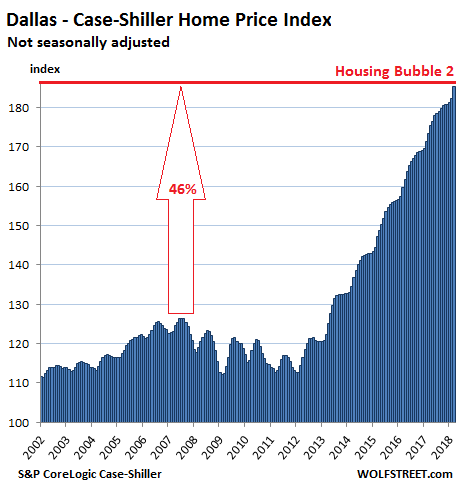

Dallas-Fort Worth:

The Case-Shiller home price index for the Dallas-Fort Worth metro rose 0.9% from March, its 51st relentless monthly increase in a row, and 5.7% from a year ago. Since its peak during Housing Bubble 1 in June 2007, the index has surged 46%:

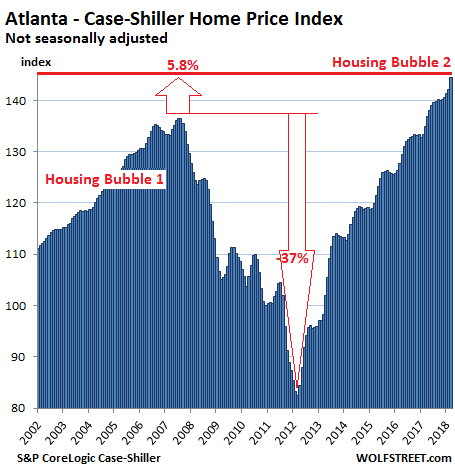

Atlanta:

The Atlanta metro index rose 0.8% from March and 5.5% from a year earlier. It now exceeds the peak of Housing Bubble 1 in July 2007 by 5.8%:

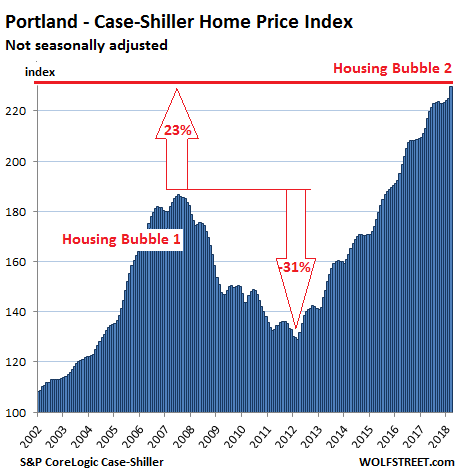

Portland:

The Case-Shiller home price index for the Portland metro jumped 1% from a month ago, 5.9% from a year earlier, and 23% from Portland’s nutty peak of Housing Bubble 1 in July 2007. It has ballooned 130% since 2000:

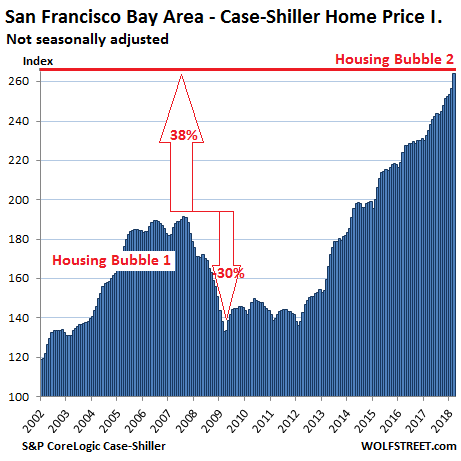

San Francisco Bay Area:

The index for “San Francisco” includes the counties of San Francisco, Alameda, Contra Costa, Marin, and San Mateo, a large and diverse area consisting of the city of San Francisco, the northern part of Silicon Valley (San Mateo county), part of the East Bay and part of the North Bay. The index jumped 1% from March, 11% from a year ago, and 38% from the insane peak of Housing Bubble 1. It’s up 164% since 2000. Note the spike in April:

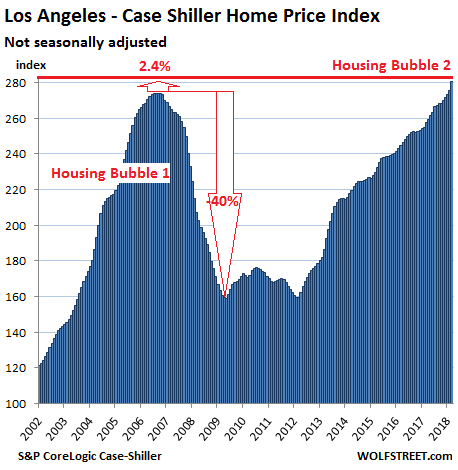

Los Angeles:

The Los Angeles metro index in April rose 0.8% from March and 8.2% year-over-year. Between January 2000 and July 2006, the index had skyrocketed 174%, then it crashed. The index now exceeds the peak of Housing Bubble 1 in 2006 by 2.4%. The index for San Diego is practically a mirror image.

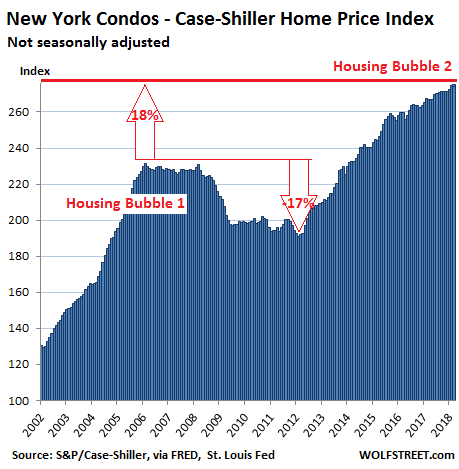

New York City Condos:

Oh boy, no spike! On this page, the index for condos in New York City is the only index that fell in April from March, down 0.5%. With all the spikes in the other metros, this is practically refreshing. But this index has produced many monthly dips over the years, some of them a lot steeper, that turned out to be blips. The index rose “only” 2.7% from a year earlier and is now 18.5% above the peak of Housing Bubble 1, having surged 175% since 2000:

So the index is getting spiky in a number of metros. But Seattle’s beautiful spike is unequaled in the series. These indices get adjusted over the next few months as more data becomes available, so some of the spikes might get toned down a little. This happened before. Or they might get adjusted upwardly. But as it stands, there was a sharp acceleration in some cities over the rolling three-month period for “April” (February, March, April). Some of this may have been driven by home buyers trying to “lock in” mortgage rates before they rise even further.

Despite persistent and false claims to the contrary that are often heard. Read… Why a US-Style Housing Bust & Mortgage Crisis Can Happen in Canada, Australia, and Other Bubble Markets

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

ONOZ teh Seattle luxe apartment bust!

https://www.seattletimes.com/business/real-estate/free-amazon-echo-2-months-free-rent-2500-gift-cards-seattle-apartment-glut-gives-renters-freebies/

I will get the rent data for June in a few days and will cover it, including for Seattle. This should be interesting.

Wolf

I am a builder in south Florida and have been watching things evolve since our bottom circa 2010. The ones you have produced for this article are outstanding.

I see your source is Core Logic for the data. I went to their site but It looks like the raw data only. Anyway you can produce one for Miami.?

Paco Garcia,

I have the CaseShiller data for Miami, but it doesn’t really fit into my theme of the “most splendid” bubble-cities since the Miami index is still quite a bit below its humongous bubble of 2006.

The CaseShiller index for Miami plunged 55% from the peak of Housing Bubble 1. It has been surging again, but remains 19% below that crazy peak.

Yeah, maybe I can move out of my van! Of course the story refers to gift cards and electronics or one free month – stupid gimmicks – not really what I’m interested in. I would need the actual cost of rent to reach an affordable level. What good is one free month if the landlord raises your rent 50% after a year?

From the article you linked:

“A stunning 26 percent of all apartments in the core of downtown Seattle right now are empty, up from just 5 percent a year prior (the number is skewed by brand-new buildings that take a while to lease up, though vacancy rates at older buildings downtown are also rising).”

This indicates there is a HUGE gap between what landlords want and what renters are willing or able to pay. Expect rents to drop quickly from here.

I was at the Fed courthouse today on 2nd, bused past as many cranes as ever with unfinished high-risers popping up like mushrooms. Are we finally seeing the beginnings of a bust? If we are. it’s will be one for the ages..

Hey look, here’s how the other half of the market sees it. Weird.

https://www.wsj.com/articles/case-shiller-home-price-index-loses-a-bit-of-steam-1530018036

I saw that. That’s because they’re not looking at the full data set — and were fooled by the yoy increase of 6.4% in the National Index, though big, was down a minuscule smidgen from the jump in March of 6.5%.

“were fooled by the yoy increase of 6.4% in the National Index, though big, was down a minuscule smidgen from the jump in March of 6.5%”

I don’t think the writers & editors were fooled at all – turning statistical noise – a meaningless 0.1% decrease in the rate of YoY increase – into splashy headlines is one of the MSFM’s favorite sports.

San Diego rose 7.8 percent pricewise from the year ago. Let’s see how long this game continues…

Lots of people working in SD, the freeways are clogged most of the time anymore. Still, the average home price is close to 600K and is still way out of range for the first time buyer. The down payment of over $100K when most folks don’t have enough savings to carry them pay check to pay check is not sustainable. And having two incomes in the family isn’t really helping much. I’m afraid we have created a new underclass generation that may never be able to dig out.

I live in North County San Diego. We have “high” (By my standards and national numbers) dual income with 2 kids. I missed the last dip in purchasing a home and now I am kicking myself. Even though I do believe this is completely unsustainable, I am banging my head against the wall. It is really hard to find nice rental properties in my kids school district. Based on where my kids are, I need some stability that home ownership offers. Even though I generally feel that owning a home is a liability when you have young kids in public schools the factors in the equation changes weights. This is something I am only recently realizing after years of being a real-estate-perma-bear. My wife and I debate this nightly and are very frustrated. The home we had been leasing for years sold for almost 900,000 and the quality was pretty low. Terrible layout, no yard, thin walls, super cheap cabinets despite being in a “premier” neighborhood. I saw some real crap shacks in Clairemont going for 600k and those are cracker jack boxes that are on par with mobile homes in my opinion. So if Clairemont is 600k for a 1,200 foot dump then naturally North County Coastal is much higher. Who are these insane people buying these homes? Where are they getting money to purchase these north county homes that start in the millions? The average corporate worker has to be squeezed to the limit. I can’t figure out if these people are taking home equity lines of credit or if they are fully maxed on the credit cards. Or the bank of mom and dad is kicking in. Having a few kids is expensive if you want to give them a nice life and be able to do sports and stuff and be able to make take a vacation every year. Maybe everyone is pulling in 400,000k or more a year and I am the low income earner. I feel poor living here despite me being in the top 10% of income. I am sure all of Southern California is the same. I just hope me waiting for this second bubble to pop will actually come. I am beginning to consider just moving to a cheaper city. Why do I want to be in debt the rest of my life for a million dollar track home. It would be different if that million dollars bought me my dream home or close but these are just average track home slapped up by builders.

end of my rant..thanks for listening…have a wonderful day.

Most of them are people making a lot of money. They other ones are people who act like they make a lot of money. Then there is a small amount of trust fund babies.

You’d need to wait for some time for things to cool down. This prices are not sustainable in SD. This time may be different, I don’t know but historically, the prices have busted many times in socal for different reasons each time.

I am in the exact same boat you are in, Dude.

I live in Long Beach, CA. Sold my house at the peak in 2007. That bubble was easy to spot. I had some medical issues in the early part of the decade and decided not to take on a mortgage. I figured all the NINJA and crazy loans were gone so house prices would probably be somewhat stable going forward.

Big mistake.

I am shocked and quite frankly furious that prices have climbed back into the stratosphere. I refuse to pay $600K for a tiny, ragged, post-war house that was only $400K six years ago. And I thought $400K was too much back then.

What is driving this insanity? Foreign money? Rock bottom rates? Stocks? Investors looking for yield? Probably all of it. I have this vision of a giant Ben Bernanke in the sky with his pants down crapping money all over the land. He’s a hero, in case you were wondering.

My gut tells me this all going to end very badly. But I’m not sure if “badly” means a crash, or if it means an imbedded, landed class that will rule over small, landless plebs like me for the rest of my days.

But renting is about $1000 cheaper a month with no money down. But that becomes moot when prices keep going up and I’m stuck renting for 10 years now.

Furious.

Some Dude,

It’s super tough, I get it; I was in the same position as you. I am in Orange county and was a perma bear from 2010-2016 thinking no way it is sustainable and the bottom has to drop out again. I was renting a nice under market rent condo in Newport, HOWEVER, we had 0 yard. My kid getting older and we just had our 2nd and that was it. I had the down and could afford the payment and after being discouraged by the low inventory found the property we wanted and got it.

The thing to realize is; there are a lot of people out there that make a lot of money. I was talking to 1 acquaintance who said none of his friends make over 100k, and then I was talking to my CPA buddy who said none of his friends make LESS than 100k. It’s a big world with lots of money.

Not sure there is ever a perfect time to buy a home from a financial perspective or market perspective; but, if you get something you can afford and it makes you and your family happy then I say go for it.

My biggest regret is not the massive equity gain and tax breaks I missed out on over the past 5 yrs renting, it was the time “lost” with my kid. Seeing how happy he is now to be in a neighborhood with kids and have a huge yard with grass and a pool to play in; that to me is priceless.

BTW, I am a mtg broker and write a lot of loans and I can tell you that a lot of people can afford the monthly payment but don’t have the down. They get the down from their retired boomer parents; whether it’s 20k or 200k.

Just b/c your parents or my parents don’t have that type of liquidity, does not mean there aren’t thousands of boomers willing to help their kids get into this market.

I think a lot of sane people are in that boat. In Seattle, it’s the same. You pay $1 million for a dumpy house that is in drastic need of improvement and air freshener. Why play that game. Save your money, rent, and move to low cost area eventually. I wouldn’t count on prices rising or falling soon, given the Fed has lost its mind and is unpredictable.

It may be painful to defer a home purchase, but that pain is nothing like the pain of buying at the top and being stuck in a crappy house you can’t sell as the market drops. Better to sit this one out in smart company than be the guy who buys at the top. Mathematics says this will end soon.

If it makes you feel better, break down the price houses between structure and land. The $1 million houses can be rebuilt for about $300-$400k in materials and labor, so that means people are paying $600-$700k for postage stamp size unattractive lots in so-so neighborhoods. Yikes.

Bobber – I read this somewhere; that when buying people are encouraged, or encourage themselves, to buy “as much house as they can buy” so they often end up with a bigger, and more expensive, place than they’d rent. I wonder if I read this in the book “The Wealthy Barber”?

When I was paying $1000 a month for an apartment in Sunnyvale, people I knew were spending that much just to keep the lights on and the water running in their houses.

It’s one thing if you NEED a huge house. But how many people NEED places with “lawyer foyers”, columns galore, a 3-SUV garage, etc?

When people make you think that average people make $100,000, and make it sound as if many are making $400,000 a year, ignore them and go to the numbers. “Search Results

Currently, the median income for a family of four in San Diego is $63,400. ” That’s a f**ing family of 4, and in my view even that is inflated by the government.

Real estate agents and in general anyone in RE industry wants you think that everyone is just signing up and paying these insane prices so that you would be another schmuck signing up for life-time slavery. Look at the numbers; don’t let them make you another statistic in fools who bought into this insane market. A year ago, in Toronto people were lining up and beating each other in the line so that they can get entry into a developer office who was selling apartments. Now, those same people are underwater for at least $150,000, and curse the day they were born.

In the exact same position. Live in NE LA in an admittedly pricey – but really nice – rental. We’d have to put $200K down and pay about $1K more a month than we do now to get into a half-way decent (never mind a nice) house in the area where we’ve lived for years, have friends and where our kids go to school.

Our household income is between $175k and 200K depending on the year (hubby freelances) which is about 4 times the median around here so why do we feel so stuck? We have the $200K downpayment but looking at what we can afford is downright depressing. It seems crazy and scary to consider paying close to $1 million and to scrimp to make mortgage payments in perpetuity for a fairly crappy house that was worth $400K less, just 5-6 years ago.

We go over and over this almost daily. Is it crazy not to buy when technically we “could”? Is it crazy to buy at these prices? It’s endlessly frustrating and frightening,

Great rant. We, my wife and I feel the same way here in Washington state.

Dude,

Just do it. Go somewhere cheaper. I was in the same boat as you during the last bubble. I was in the top 10-15% income wise, yet felt like a pauper seeing everyone around me driving brand new $50K cars and living in $750K+ homes, which I could not afford.

So I said screw this, and moved to one of those icky states that voted for Trump. Life is exponentially better now. Not just financially, but day to day life. Less traffic, nice people. I can go to a public park and not have to worry about bums taking a dump next to me.

Yeah I miss the weather. There’s definitely something to be said about 65 degrees in January. Other than that….not so much.

I can relate 100%. I live in North OC and it has been an endless source of frustration (or depression?) that I can’t get my family into a better home. We’re a single-income family making well into six-figure territory and rent a somewhat crappy condo that we’ve stayed in only because the rent is extremely low (we’ve lived in it a while). To rent a SFR in the local area would add $1000+ to our monthly expenses, which would limit our ability to save and do fun things with the kids. To buy would mean having a monthly payment well north of $4000/month, which is definitely not an option. Just the property taxes alone would be $800 to $1000/month, depending on the price of the property. That’s risky and insane in my opinion.

I’m an OC native, but CA has gotten so ridiculously expensive that I’m envious every time I hear of somebody moving out of state. I would like to leave as well, but I have a good job and our family is here. We’re probably stuck for the moment, but unless home prices get cheaper, we may hit our limit and get out too. It’s just not fun to live in OC anymore.

> a giant Ben Bernanke in the sky with his pants down crapping money all over the land.

Best. Imagery. Ever.

> when buying people are encouraged, or encourage themselves, to buy “as much house as they can buy” so they often end up with a bigger, and more expensive, place than they’d rent.

When renting, you know you’re going to move out of there, and probably soon (a few years).

If you’re buying the place there’s at least the possibility of living there the rest of your life, and if not, a very good chance of living there for at least a decade.

California real estate has many factors why it is so expensive. One, it ranks as the most difficult state to build. When you can’t add inventory, the prices spike. Second, off shore and out of state investors. Several wealthy snowbirds that I know have houses in San Diego. Third, legacy money. Some people have large amounts of equity in their homes already.

California has an affordability crisis for working class and middle class residents. And it isn’t fun to commute to inland subdivisions. The solution is something that California may never do – build higher density housing. Most major cities in the world do not have so many single family detached homes.

Where do you get the idea that the down needs to be 100k on a 600k house???

Nothing could be further from the truth. 3.5% is the minimum down required for FHA.

If you’re a vet (which there are a lot of in SD) you can get in with 0 down.

JJ,

As a fellow OC resident I can relate. There are areas in South County that are nice, with decent sized houses/lots and can get you about 750k.

If you have 20% down; you can get a total payment of around $3800. That’s not “well north of $4,000”.

It’s a tough decision and I was in a similar position last year and got tired of waiting and waiting and waiting for the next pull back or downturn and also was tired of seeing my 6yr old live in a condo with no yard. So; it took awhile and we finally found the house in our price range and went for it and got it. Best decision ever.

So. Cal is being pumped by Asian money. As the Yuan is depreciating, and the trade war continues, I expect So. Cal real estate to go exponential. You have hysterical wealthy Chinese who think their wealth will become worthless.

What happened in Canadian housing over the last 15 years is happening here, and we’re maybe only 5 years into the inflationary cycle.

This is a ‘from the gut’ perspective but I don’t see the money flowing into So. Cal as being, sub-prime NINJA owners. Rather it is established money seeking a long term home. It’s all market by market but LA and San Diego should see about 50% appreciation (at least in new homes that are invesment grade) in the next ten years.

The current rate hike cycle is almost over, and providing the cutting begins next year, then real estate will march higher. If Trump allowed that ludicrous tax cut, I can’t see him allowing the Fed to trash the economy with high rates.

I don’t see much scope for price hikes in socal and for sure looking at the Fed’s hawkish tone, I don’t think rate hikes are done. Infact, they seem more aggressive with time to hike rates.

Socal has seen many boom and bust and the bubble bust for many reasons not just because of sub-prime loans.

Are from from the camp: “This time is different” ? I thought the same in 2006-2007 :-)

I think you’re correct with regards to the current rate hike cycle nearing the end. If the Fed allowed any substantial increase in interest rates it would work at odds with their stated policy of devaluing the dollar. The Fed has only two official mandates 1) full or optimal employment and 2) steady dollar devaluation.

The Fed has stated their desired rate of dollar devaluation is 2% per year but, as Jerry Powell has stated, the Fed will let the devaluation run significantly above 2% to make up for years of inflation, they say, ran below 2%. The Fed refers to this as symmetrical inflation policy – I refer to it as a wealth transfer policy.

“they say, ran below 2%”

That really is laugh out load funny. In my real world, inflation is well above 5% and has been for years and years. How anyone can believe that we are in an era of low inflation is beyond me.

interesting,

If you bought a house 15 years ago and you refinanced the outstanding balance a few times (no cash-out) to benefit from falling mortgage rates, your mortgage payments went down. Your property taxes might have increased but not by that much. So housing costs would have been flat or down for 15 years! Meaning for you, zero inflation for housing. For many people, housing costs are 30% to 60% of the cost of living. These people see prices go up on smaller items, such as food and utilities, but the big thing is locked in. This makes a HUGE difference.

Just because home prices and rents go up doesn’t mean that everyone actually experiences that. But everyone experiences things like food price inflation.

But when you rent, and your landlord jacks up the rent 15%, and 50% of your cost of living is rent, you’re really screwed, and you feel the full brutality of inflation.

Also, many things got cheaper for various reasons, including e-commerce and the elimination of middlemen, especially for imports: apparel, consumer electronics, shoes, bed sheets, etc.

Our health insurance premiums have barely budged for the past two years, while for some people premiums have soared.

Inflation is really a mixed bag and everyone experiences it differently.

Actually, I think the FED are loving their rate hike. I think this game is much bigger than just US economy. FED rate hikes are trashing the developing markets, and they are fine with that. So, expect the rate hike to continue aggressively.

Hogwarts,

In other words the “fundamentals” of those earning a paycheck have nothing what so ever to do with the price of RE?

This is going to end just like it did last time, and the time before that and the time before that. Only after the crash will everyone….maybe even you….start with the Monday morning quarterbacking about how “obvious” this bubble was and how and why it popped, bla bla bla …..this happens every single time…..the post crash “experts” come out in droves to “explain” how reality prevailed.

BUT what ever it isn’t this certainly is without a doubt another bubble.

“we’re maybe only 5 years into the inflationary cycle”

I hope you stick around for those 5 years and if you’re correct you will have every right to crow about it. If after 10 years of this insanity leads to another 5 years of this insanity what then? And please don’t tell me a permanently high plateau…..that isn’t how cali RE works.

“The current rate hike cycle is almost over, and providing the cutting begins next year, then real estate will march higher. If Trump allowed that ludicrous tax cut, I can’t see him allowing the Fed to trash the economy with high rates.”

I’m not sure.

There’s a theory that rate hikes are actually driving inflation higher vis-à-vis higher input costs and the like, which in cause will potentially provoke the Fed to continue raising rates. I’m not convinced, but it’s an interesting one, and conventional wisdom about these things has been wrong before.

Powell has also added some additional language to the most recent meeting that indicates he’s much more serious/concerned about financial bubbles, and considers managing these one of the Fed’s mandates (whereas previous Feds have basically taken a “we can’t see bubbles” hands off approach.

As to Trump, in theory he has no control over what the Fed does.

The collapse of Chinese market might cause some of the Chinese sellers to liquidate holdings here to pay debts at home. The CCP is not the dumbest player out there. They have levers to apply at home to force people there to repatriate overseas holdings.

Also, the global market is interrelated. You are talking a Yuan devaluation will not have any impact other than money fleeing from China. That’s not the case because devaluation makes Chinese products even cheaper, and that will export deflation around the world. Debts all over the world will be more expensive and it will cause defaults including companies in America.

“So. Cal is being pumped by Asian money.”

Finally some one gets it!

Wolf, can you help me understand what your definition of a bubble in these cities is? Due to inflation clearly the price won’t be the same as it was 18 yrs ago. Where is non bubble territory on tour index?

This index is a measure of inflation, namely house price inflation, which is part of asset price inflation. There are a lot of types on inflation such as consumer price inflation, wholesale inflation, wage inflation, etc. None of the inflation indices are adjusted for inflation.

Everyone called the last bubble a “bubble.” It was unsustainable and ludicrous. By 2009, everyone agreed. It had been a bubble for years. The peak of the bubble was when it began to implode. There is no disagreement on this. Use that as a base and go from there.

I remember back in 2006-2007 there were a few voices calling a housing bubble, pulling up home affordability charts and such, but it was by no means consensus. Even the all-knowing Bernanke didn’t see a bubble in housing back then.

The only reason there’s a consensus of 2006-7 being a bubble peak now is because it went down after.

The consensus will never agree that we have a bubble in anything that is going higher – that’s just the way things work.

Very true.

>The only reason there’s a consensus of 2006-7 being a

>bubble peak now is because it went down after.

But the fed still felt justified in building a “floor” under inflated housing prices rather than allow a correction toward household income.

Excellent point, Wolf. Most of the financial media takes it for granted that consumer price inflation *is* inflation. How refreshing to see it recognized that consumer prices are but one subset of the whole. Not to mention questioning the accuracy of how the government measures them.

@ Phil. I wish there is a chart that has the authority of defining “bubble”. There never is. The goal of “bubble” is ALWAYS AT ALL TIME wealth transfer. If the definition is clear and everybody can see what it is, the wealth transfer will NOT occur.

What you can do is to “measure” it yourself and have your OWN OPINION so that you can avoid the wealth get transferred OUT OF you. And if you are the 1% kind, you can get wealth transferred INTO you.

To have your own MEASURE and OPINION differentiate you from the rest of the mass. If you do NOT have them, your wealth is likely to get transferred into the hands of Warren Buffet and the likes.

My own opinion for the housing price at current level is the following. It is just an opinion.

“Bubble” means price at this level is NOT sustainable for long term, E.G. more than 5 years.

1. The price/W2 income is 5 to 10 times. NOT 3 or 4. People can “buy” home, but they can NOT “afford”. “Buying” requires your W2 can make mortgage payment. “Affording” means every 3 years, you can save enough for another year if you lose your W2 income. It is called “weak hands” and “strong hands”. The difference is drastic. “strong hands” can hold the home through recession. “weak hands” will lose their home and their savings of previous years during recession.

2. Price/rent > 30. When I bought mine in 2010, Price/Rent is 10 to 15. You can use interest rate to justify this. But to me, getting my investment back after 30 years is NOT attractive to me at all. Then you say price “ALWAYS” rise, and that is crossing the line of being a speculator.

3. Hard to measure flows such as foreign purchase and unstable income such as IPOs. I have NO knowledge how to quantify these. What I do know is the the world is reversing globalization. It will rewind slowly but surely. There is geopolitical tensions rising.

4. The most important parameter. Central banks rate and QE is reversing. No matter how much you look at the past 10 years in AWE, what happened in the past 10 years SHOULD reverse now. It has NOT happened yet and Wolf keeps reminding everybody about it. This is usually the moment of the wealth transfer. The turkeys have been fed FAT and it is getting close to Thanks giving.

The professional money managers will tell you different things about trend and what will happen next year. They risk other people’s money picking up pennies in front of a steam roller. They do have better readings than average folks like me. But buying a house is a 30 year decision. It is NOT next year’s bonus. And it is your own money, NOT other people’s.

I agree with you. There are better measures to tell whether a given market is in a bubble or not than trying to discern things from an index which is only expressed in nominal terms.

Good measures are things like price/income ratio and rent yields in a given market.

What a great comment JZ. Thanks for the ideas.

It was pretty easy to see the end of the last bubble because Phoenix & South Florida began to slide in late 2006 which was way in advance of the collapse for the rest of the country. The radio host Clark Howard who has a personal finance radio show was calling it. My parents in Phoenix began loading up on distressed real estate in Phoenix to use as rentals throughout 2007 and early 2008 in spite of my frantic warnings that “this one is really different.” In hindsight, I think my Cassandra-like warnings stiffened their resolve to keep buying. 30 years of experience in the Phoenix market made them leverage to the hilt in 2007 & 2008 because they were finding what seemed to them like crazy deals to buy rentals. But the market floor kept dropping and renters never materialized as Phoenix became, in my father’s words, “Appalachia with sand.” By 2009 they were bankrupt after a 30 year run of successful commercial construction & my father gave up when confronted with a diagnosis of cancer.

Is that data inflation adjusted?

I am thinking if you inflation adjust the DFW Metroplex, prices will have remained flat or even fallen in bit from 2000-2009.

As I said elsewhere here, this index IS a measure of inflation, namely house price inflation, which is part of asset price inflation. There are a lot of types on inflation such as consumer price inflation, wholesale inflation, wage inflation, etc. None of the inflation indices are adjusted for inflation.

Agreed, I hate seeing inflation adjusted numbers on charts like these because for the most part the adjustments aren’t relevant to housing.

I think rent prices and interest rates are the biggest inputs into deciding whether home prices are rational. If the index was 100 in 2000 and rent has increased by about 3% per year since then, then holding price-to-rent ratio the same the index should be around 170 today.

In 2000, the 10-year rate was between 5 and 6%, now it’s between 2.5% and 3%! That’s a HUGE difference. If the long term rate stays well under 5-6% over the next 30 years, then honestly much much higher valuations can be justified.

I mean, if your best alternative over the next 30 years is earning 6% with an index fund or 3% in treasuries, how much would you be willing to pay for a house that generates rental income that grows by 3% per year?

Assuming half of rent income goes to expenses, I’d be willing to pay upwards of 16 times rent for a place to lock in a 6% return. And that’s all-cash – ignoring leverage!

Now imagine what the people in Europe with negative interest rates are thinking. price-to-rent of 30:1 is still a pretty good deal for them in comparison.

All of these ‘home’ price indices also include the land component on which the ‘home’ is built. Subtract the cost of labor and materials to build the structure(s) on the property and that will show how much property prices are inflated by credit.

I have never seen an index of prices adjusted in such a way, and for understandable reasons. It would point directly at how credit inflates asset prices, and also make obvious how property owners get a “free lunch” of asset price inflation that should be taxed away.

In Hennepin County and Minneapolis there is a distinct breakdown of land market value, building market value and a homestead market value exclusion. So I am taxed on my land, my house and my detached garage combined. There ain’t no “free lunch” for property taxes in south MPLS.

In my zip code, the median price is $254,000 according to Zillow. That’s an 11% increase over the past year with an increase of 6.7% predicted over the next year. My favorite metric to measure homes is price per square foot, and the current median listing price per sq ft is $244.

Property tax assessments are usually broken down in such a way. The “free lunch” is the appreciation in the property price with no input on the part of the owner. In fact, the push to lower property taxes is usually sponsored by the banks and real estate industry because it leaves more money on the table to be pledged to the banks as interest, thus inflating prices.

Whenever I hear an elected official advocate reducing property tax, I immediately know who he or she works for.

Property tax is my single largest expense by far, considerably more than my total energy bill.

I argue that I don’t consume the services I’m paying for, someone else is but I can’t figure out who, maybe some paving contractor company who’s stock is owned by our governor?

Yeah, this is my one pet peeve with attempts such as this to compare the current bubble to the previous bubble – while completely ignoring overall inflation.

That said, inflation is indeed one statistic that the gubbimint loves to play with and as such one might want to adjust by nominal median household income growth with is generally not subject to such gaming (or you can even use actual figures like median SSA wage or IRS income).

In any case, median wages are up about 30% between 2006 and 2018. So, if you want to make an apples-to-apples comparison – it’s pretty easy, just multiply the 2006 value index by 1.3.

If you do that it becomes apparent that the situation isn’t quite as dire as it’s sometimes made to be.

That said, I don’t disagree with the overall premise… house prices are, in terms of the national average, overvalued and are in a bubble in certain regions. On a nationwide basis, I personally expect prices to fall 15-25% in the span of 2-3 years.

The Fed’s preferred inflation index, core PCE, increased by 18.9% from early 2007 through May 2018. As you can see from the charts, the bubble peaked in each metro at a different time, in many cities in 2006, but in several cities on the list in the summer of 2007. So now you can do your math.

You will see that the current index value is above the prior bubble peak in all metros on the list:

In 5 metros, the index is at least 18.9% above and up to 52% above the prior bubble peak.

In 2 metros, the index is nearly 18.9% above the prior bubble peak (16.6% and 18%).

In 3 metros, the index is 8.8% 5.8%, and 2.4% above the prior bubble peak.

But remember, the peak of the last bubble was when everything blew up. This is NOT the ideal state to return to, even if you adjust it for inflation. Unless you want another housing implosion.

And the real median household income is up 1.5% from 2007.

https://fred.stlouisfed.org/series/MEHOINUSA672N

And that includes the top 40% where the median household income has risen sharply, and the top 10% where it has soared, and the bottom 60% where it has gone nowhere.

Core PCE is a joke. It’s just an artificial, cherry-picked excuse for the Fed to keep rates lower for longer. There are too many games being played with inflation metrics. Using median income figures in this context makes more sense becuase 1. Income is what matters when it comes to being able to afford stuff and 2. A lot less games and hedonics go into calculating nominal income.

Real median income is irrelevant to this discussion since the Case Shiller is a nominal index.

All this said, and as I’ve said before, I agree with you in the main… some areas are definitely in a bubble and price declines are coming. It’s a matter of when, not if.

“median wages are up about 30% between 2006 and 2018”

Has your income gone up by 30% in that time span? The only people I know who got that type of increase are minimum wage workers. other than that I do not know a single person whose income has risen by 30%

California:

January 1, 2008 $8.00

January 1, 2018 $11.00

Me? I haven’t been able to raise prices in 20 years……I make the same money as I did in 1997….but then again I have to compete with China. While I still do quite well I can not afford a $600K starter home.

My income today is 50% higher than in 2007. I changed careers right around that time, so it’s a bit of apples to oranges. But yes, people like me are out there who have had a significant “raise” over the past decade.

It’s not just a statistical estimate, the rise in median income is also manifested in a host of actuals measures as well such as the actual change in wages reported to social security and income reported to the IRS from many millions of people over the timespan in question.

““median wages are up about 30% between 2006 and 2018”

Has your income gone up by 30% in that time span? The only people I know who got that type of increase are minimum wage workers. other than that I do not know a single person whose income has risen by 30%”

That’s only about a 2% a year raise each year. It’s not crazy, and while you don’t know anyone who has gotten that (I doubt that, but OK), I would guess most people I know are probably right around there (assuming no job changes), as 2% raises seemed to be the new norm for a while.

Here in San Diego there are few listings and the cash buyers are competing to buy them. In a way, these cash buyers are making their own bloated market. These buyers are hugely foreigners (Buying remotely from China), the Top 10% who have more money than they know what to do with, the flippers and the Hedge Funds like Blackstone, who still buy millions in SFRs for rentals. They all think San Diego is a sure thing with no risk but many of us in real estate thought that in 2008. Unemployment in a recession could kill the rental income many count on to make those huge mortgage payments. This time I’m watching from the sides.

Stan:”They all think San Diego is a sure thing with no risk but many of us in real estate ”

I disagree. I personally know some partners in one of the biggest investment firms buying, fixing up and renting properties across the country. I will not name the company but it has been mentioned on this blog before. Their analytic models say stay the hell away from Southern California. They have bought zero properties in California because the numbers based on income, prices and rent don’t make any sense to them and the myriad of exit strategies they have.

Smart money has already left the California market quite some time back. The numbers in CA just does not make sense for smart money to invest here and it’d be crazy to buy at these valuations to buy in CA for investment purpose. I am also watching from the sideways this time.

Dude, thanks for the “rant”. I feel your pain even though my three kids are now grown. But I feel for them, and other Millenials who can’t get a reasonable start in life due to the new economic ‘normal’. Hang in there, you are not alone!

The only RE investment play in CA is appreciation. Cap rates are microscopic compared to most of the US. So, that’s a big gamble to bet on appreciation.

For primary residence though, I think there’s limited inventory and strong demand both via organic buyer and foreign cash buyers.

The organic buyer qualifies via income verification unlike last decade while cash buyer probably doesn’t care too much if the property falls in value 10 to 20%. All bets are off however if there is a global crisis worse than in 2008.

Amazing to behold, but keep in mind it’s only a bubble if it pops. There still seems to be a lot of money laying around, I hear 10’s of trillions are held by foreigners, and as the Fed holds to its promise of currency devaluation more of those foreign holders of dollars may begin to panic and buy whatever they can lay their hands on – houses.

There are not a lot of things foreigners can buy with the dollars we send them. They can buy (GMO) food but that’s not a durable asset. They could buy a Ford or Chevy but only Americans seem gullible enough to want one. No, houses seem like one of the best options. Of course, if the country continues its slid, foreigners may rue the day. I’m counting on them to pay property taxes required to pay firefighters to sit around playing cards and lifting weights.

AMEN.

Every car accident around where I live scrambles at least one fire truck, ambulance, and police car. WEEEE OOOO WEEE OOO “That’ll be $1,000 pay in overtime for us having to suit out and drive out there.”

They’ll do the same thing for a homeless person who nods when an officer responds to a loitering call and asks if they “need help”, but no city seems to want to prevent another such performance the following week.

“I hear 10’s of trillions are held by foreigners” stop dreaming; where in Turkey, Argentina, Brazil, India? where do foreigners are holding 10’s of trillions. At least real estate brochures make it sound reasonable; I think you should give your brochure to someone to review before releasing it.

$500 billion annual trade deficit. That equals dollars leaving the country and held by foreigners. The currency is real and it has been adding up for years. Now that currency is starting to flood back, eager to buy assets before the value becomes negligible. Houses are being bought, outright, with cash – doesn’t seem to be any shortage of cash to buy homes.

Money, money everywhere

According to all numbers, we owe about $6 T; it is not 10’s of trillions as you said. So, again, fix your brochures. I don’t see money all around. I see apartment buildings all around with at least 20% vacancy who don’t let anyone to find out that no one is renting their apartments. House prices are gonna tumble whether you like it or not.

Normally, that $500B per year going into foreigners hands would be invested in the foreign countries. Apparently, the foreigners (say Chinese, for example) don’t want to invest in their countries, so they invest in the US, Australia, Canada, and elsewhere. This is the problem. The people in China want out. Perhaps this is the most unstable part of the equation. If so many people in China don’t trust investment in their country, the political environment in that country will likely shift. If so, this could help eliminate the imbalances we’re seeing. Just think how much investment would flow into a free democratic China.

“Amazing to behold, but keep in mind it’s only a bubble if it pops. There still seems to be a lot of money laying around, I hear 10’s of trillions are held by foreigners, and as the Fed holds to its promise of currency devaluation more of those foreign holders of dollars may begin to panic and buy whatever they can lay their hands on – houses.”

You keep harping about this dollar devaluation like it’s something new. Have you not been paying attention for, I don’t know, decades?

Inflation is quite a bit LOWER today than it has been by historical standards.

But no, in your mind, all of a sudden people are freaking out about 2% inflation and panic buying houses? Get real dude. More nonsense.

Foreigners ARE buying lots of housing, but it has virtually nothing to do with “dollar devaluation”, it is in fact the exact opposite: the Chinese are buying because of YUAN devaluation.

Knowing that doesn’t help the average person looking to buy a home, but the least you could do is stop making outright stupid statements.

I sometimes wonder how many inflation % watchers are aware that the ride down is often worse than the ride up. For instance, someone who sees their house value go up 50%, for example, might assume that even if it ever drops 50%, they would break even. When actually, in that scenario, they would actually end up 25% in the hole.

The Bay Area is insanity right now. My wife and I do very well and we still cannot afford a place we would want to live. Even assuming we put down $250K on an average condo in SF, we would have to mortgage about $1 million to afford the damn thing. That is an insane mortgage with a huge payment for a freaking two bedroom condo, and would leave us extremely exposed for the next recession. I would rather just enjoy the freedom of holding cash at this point.

This is the right idea. Lots of us are in the same position. Freedom from worry about the coming recession is worth the frustration in my opinion. Nothing wrong with renting.

This is true. We live in Silicon Valley. Houses in our shitty (and I mean shitty neighborhood, 3 schools, 50% undocumented) are selling for 2 million. I can’t fathom that anyone with 2 million would want to come near the neighborhood much less buy. But, everything gets sold so who knows.

PS Just a fun fact, houses in our city on average went up $400k just last year and they keep rising by over $1000 a day. We will never be able to afford a house here and we make over 400k. Insanity.

Could you please post here once you make the purchase? Then I will know the top is in. If you still have cash and they have NOT managed to squeeze it out and make you a debt slave, this ain’t over.

Somebody please tell me why the exodus of blue collar workers is not happening faster in the high price areas (Seattle, San Fran, LA, Boston, Denver, NY, etc.)

If you have a high paying job, you can barely afford it. So why are average hard working Joes still living in those cities? Teachers, nurses, police, construction, government, etc. Why would they put up with it when they can get so much more in a secondary city? Their jobs are portable.

We know the pay hasn’t been increasing nearly as fast as the costs in the high cost areas.

Perhaps many of them bought houses in these locations a while ago and don’t feel the pain.

There’s quite an exodus going on alright. But there is also a strong influx from the US and overseas. For now, the influx is greater than the exodus. So the net is still a positive number. When the influx slows down, the net will turn negative.

I keep my eye on the population and laborforce numbers in the Bay Area and California. For now there is still more influx year-over-year than exodus, but not by much anymore. When it becomes a year-over-year decline, I’ll post the data.

Anyone who stays and has the profession listed must have already bought awhile ago and are sitting on a ton of equity and low property taxes.

The new millennials coming online in that area that fill those jobs are screwed.

Trump needs to put a stop to the Chinese buying up America with phony Yuan. Simple.

Hey Wolf,

Thanks for the article. I’m having a hard time with the Case Schiller index differences between LA and the Bay Area. I have family in both places and housing in the Bay Area is almost 3 times the amount of LA, yet, if I’m reading the index right, LA is slated as costing more. Can you help me understand the difference in these charts? Also, any info you have on the index would be much appreciated. We’re looking at moving to the PNW from SLC, Utah and are watching this trend closely.

Anne,

1. The index only shows price movements not absolute prices. For each metro, the year 2000 was set as 100 in the index. So they all started out at the same point on the index though their prices might have been very different. Then it measured price changes, not absolute prices.

2. “San Francisco” in the Case Shiller is a five-county area that includes the most expensive parts, such as the city of San Francisco, and less expensive parts such as Oakland. There are large price differencea.

But your point is correct: median prices (not Case Shiller) in the city of SF are much higher than in the city of LA.

I am not worried about this current bubble. I was crushed last go round in South Florida 2006 when my newly purchased home that I put 22% down on (purchased at the peak) lost 64% of its value essentially overnight. I ended up walking after 5 years when my corporation moved operations out of the country and renting the property would have meant $800 a month out of pocket to make up the difference.

I currently live in the Bay Area and rent. I wouldn’t touch this market, even if I had the $140K-$160K downpayment it would take to buy a reasonable home in need of updating in the suburbs. Folks who are considering buying now need to have their heads examined. I hear the same refrain from folks now about how property prices will not drop, how strong the Bay Area economy is, how this time is different. Bunk. The current housing situation is completely unsustainable and is being fueled by VC money and, what will certainly end up as plenty of vapor ware.

My favorite proxy is the number of food delivery apps we have in the east bay. We have 6 services, they all suck, they all spend prodigiously on marketing and discounts to get subscribers, and the real bet IMHO is which two will be around in two years. That would mean that 4 companies with investors, marketing spend, software engineers, office space, AND their respective incomes will evaporate. Silicon Valley is the destination for 75% of Venture Capital in the US, and a great deal of that excess capital was conjured by the Fed and is now being steadily ‘destroyed’ – along with steadily increasing interest rates. So in a very real way, Silicon Valley and the Bay Area is highly exposed to a market pullback.

You could look to all those bike-share companies too. I can’t imagine they are making any money, but lots of investment is going there.

Only 6? You’re slacking….

I use the Scoot app to get around town from time to time; my average cost of my own scooter, helmet and 15 minutes of usage to run errands/get home without looking for parking is less than it costs to ride Muni; it really is remarkable – someone is paying for this, and it ain’t me.

Something will have to give, right? (famous last words)

Obviously, prices are being driven by a shortage of housing and while higher prices and interest rates will dampen demand, supply is still short. I just had one of my rental properties in SoCal go vacant, I flew into town, placed a for rent sign in the front yard @ 8:30AM and by ten AM had received 8 calls, with some offering a deposit without seeing the inside. It has since turned into a frenzy with some telling me they have been looking for months and can’t find anything. I feel bad that I will have to select one family when so many are in need. Affordable housing, which is an oxymoron, is in dire need.

Great story; and here in South SF Bay, where all the big companies from Google to Apple, to Tesla, to Facebook, etc. are and have hired tens of thousands who rent, each apartment building depending on the size has from 4-10 apartments sitting vacant. I’ve mentioned this before, but worth mentioning again; the apartment that I currently am at is basically at one of the top locations in Silicon Valley, and a 20 apartment building has 4 vacant apartment. I looked at a paper ad that had been jammed in the door of one of these apartments, and the ad was from February; meaning the apartment has been empty since Feb, and this is supposed to be one of the hottest rental markets. RE guys are so funny and phony at the same time.

Just did a quick search for 2BR/2BA for rent in San Diego over craiglist. I saw 3000 listings.. don’t see any shortage

Jon: Yeah, no shame at all. 3000 listing and the guy comes here with the story of “It has since turned into a frenzy with some telling me they have been looking for months and can’t find anything. ”

Yeah, maybe they were looking for an apartment on Mars, not in SD. There is real shortage of apartments on Mars as you know.

“…prices are being driven by a shortage of housing…”

One issue that I don’t see addressed much is the impact of Prop. 13 on CA real estate. Anyone who has lived in a house long term has every incentive to stay put. I/we know several families who have retired and have no reason to sell and move because of the potential tax impact – not JUST property tax, but potential capital gains impact. If you run the numbers, it quickly becomes clear that it would cost serious $$$ to sell. Retired folks “squatting” in their current digs is one less house on the market. For many, the plan is to leave the property to the kids – the kids get the Prop. 13 benefits based on when the property was purchased.

When the kids get the house after the parents’ death, they also effectively avoid the capital gains tax because the cost basis of the house is “stepped up”‘ to current market rates.

Prior to May 1997, you could roll your capital gains into another house as long as you purchased the replacement house within 2 years. I think if this law were in place – along with the “Proposition 60” (Transfer of Base Property Base) – more people would sell. By incentivizing people to stay in homes, you end up with underuse of the existing stock.

Exactly correct – the kids will have a potentially huge windfall from the “step up”.

One other factor affecting this particular housing pool (stay-put seniors) is that we’re all living a LOT longer. With the tax incentives structured as they are, the cost of selling is just daunting. If you are financially secure otherwise and like where you are, why would you move?

I genuinely feel for those of you with young families trying to get established, and wish all of you the best of luck whatever decisions you make. We have a Millenial son and his struggles hit very close to home.

I don’t think there is any shortage of housing stock. If there is a shortage, it is shortage of affordable housing.

Housing bubbles come and go, but are the GSEs still guaranteeing loans on property in these spiky bubble markets?

As a taxpaying American citizen, is my government participating in this fiasco? It would be wise for them to step back and stop guaranteeing loans in an area once prices rise above a certain benchmark.

@Todd H.

“buttonwood betting on ben” < – – – query

Answer = yes

Is there any correlation between housing and commodities ?

Buy low, sell high. ‘Investing’ in a home shouldn’t be any different. Those who are renting and saving will be laughing when the inevitable correction occurs…..

As always Mr. Wolf, very interesting. However I have a question from the back alleys and empty dumpsters all over America.

Just where will all these immigrants that are ‘flooding’ into the USA going to live….In posh Seattle, Portland, San Francisco? Add to that, all the displaced middle class and border class citizens who have rented all their lives and are being push out? It is not off topic but a real part of the topic.

For every action there is a reaction, we do not live or survive in a vacuum. I suspect these fancy expensive properties will be the new focus of taxes to offset the needs of the less fortunate and if not, then heaven help the people who live there when the rubber meets the road.

Amazon and Starbucks have spoken in Seattle, the poor are not welcome and they don’t get ‘my hard money’.

From recently having to look for an apartment, I can tell you where the immigrants, displaced middle class, etc. will be – crammed five to a room, with 20 vehicles parked outside.

Driving around looking for a place to live really illustrated how the middle class is GONE in this country. You can spot the formerly middle class homes that now only the rich can afford, with a lone Tesla or other expensive car parked outside. It’s either that, or a house/duplex with 20 cars and trucks parked outside, many of the trucks with ladders/construction equipment in back.

Or drive by a “cheap” apartment complex and see the parking lot crammed with cars like it was the slums of Calcutta.

that’s happening here, now, and within a ONE-block span:

MY SF MISSION REPORT

in the condo duplex across the street from the homeless camp

on the sidewalk we have the $2 mil new condo with foosball table in the floor-to-ceiling window on the top floor and cardboard covering the window on the first floor

next door to me the tech couple were paying $3700 for a 1-br and a month ago left for his folks’ home on the peninsula because they were tired of the construction as the woman heading the REIT that owns the building is harassing people out and has already set a couple of fires

former janitor homes have your teslas range rovers and lexuses parked out front and white people like from boston or somewhere so yankee that you expect them to be skulling and off somewhere at big dinner tables doing sarcastic slaps. so white even white folks here would say, “wow…now THAT’s WHITE” are all around

and around the corner the other Chinese investor couldn’t rent out a couple of attached dingy, dark, crappy 2-br bungalows at $3200 each so they rented them to a black family of 7 with some kind of rental voucher, in one bungalow and a black woman in the other one

the guy who told me wasn’t happy with the family of 7 and i had to keep from GIGGLING at how the snake is finally deep throat choking on its own tail, thoroughly confused at its predicament as it was originally trying to figure out how to merely chase its own tail.

you all have GOT to read Charlie LeDuff’s new book, SH*TSHOW. it is the funniest sweetest show of how we’re ALL in the same… sh*tshow.

finally after the cold steely logic of Wolf’s “money” (ha ha) site, i’m seeing the ART coming from this hell. the human scream of OH NO WHAT THE FXCK IS HAPPENING.

here in SF where the counter culture has long since been decimated suicided homelessed exiled… i’m FINALLY seeing the signs of life instead of people trying to merely make a buck off it.

the corner has turned. finally… it’s gonna get good and funny interesting because we’re apparently NOT ALL gonna take this bending over and thinking of england…

you millennials read that book. you all have been FDOB too long as it is. (my filmmaker friend Stephen Sayadian who did CAFE FLESH back in the day, he calls that deep edgy scary artistic despair “face down on bed.” and there are different LEVELS of it. the “no sheets on bed” is particularly bad version of FDOB. we’ve ALL been there too damn long)

let the games begin.

AND check out Mr Fish’s (Dwayne Booth) book from fantagraphics, “AND THEN THE WORLD BLEW UP.”

i myself had long forgotten the value in writing and knowing that at least ONE OTHER PERSON feels the pain as excruciatingly as you do. it makes it more BEARABLE to share the agony. i myself forgot, even as Wolf keeps italicizing that fact to me.

(smile)

thanks for all you who write here and make the comments section as superb and real and HUMAN as it is. and all on a money site. ha. all the charts and graphs that i barely understand and yet it’s been screaming against inhumanity and corporate feudalism and against ignorance since i first stumbled here.

i’m just here to say that i’m no witch. but i’m sensitive from not fitting in and living under the rocks. i’ve been invisible until now. with gentrification nowhere left to HIDE. but i’m good at sensing vibes change and for you lazy shmucks, yeah… soon time to get out the popcorn.

but the rest of us, and it seems to be from age fifty or so on, we’ve no luxury of sitting back because we’re the last generation that actually knows how to follow through, maintain an attention span, and get real actual live things DONE. we have to show them how to take off the helmets and not care about what anyone thinks 3,000 miles away on social media.

they are like factory bred franken chickens with breasts so unnaturally big, they cannot walk on their own feet as their tiny little ANKLES have not kept up with these evolutionary changes and they cannot yet WALK.

Great read Mr Wolf! Having major dejavu here from 2006, I have a gut feeling it’s a repeat. Had this feeling last year and sold my home to rent whilst waiting on the sidelines for another decline. Everything is finally pointing to that now aside from the realtors and mortgage brokers whom will lie and tell you get in now before it’s too late. I talk to every person I can who is envolved in real estate and have noticed a swing in moods during the last couple months. While no realtor is going to tell you not to buy, most do agree the market is cooling and one (whom is a high school friend) is warning me to stand by until the end of the year. Foreign investments seem to have been a key factor here from what I have heard. Median home values have skyrocketed beyond any reasonable doubt. Realtors in the Bay Area have been flying out foreign investors or flying to them and showcasing properties. Foriegn investors are granted permanent visas which is part of some program (forgot the name SB15?). This program is changing in September and I am told it will impact this foreign investment money which in turn could further excillerate the next bubble. These are all observations by me, I have no background in economics or real estate other than experience nor can I predict the future but it feels like a repeat to me. I don’t feel bad selling a year ago even though I could have made another 100-150k, I made plenty and feel fortunate to have got out when I did!

you can never perfectly time the market. It is better to capture your gains bit earlier than being bit late and lose a lot of money.

A number of Bay Area realtors have told me that the foreign money has left the market. But I still see houses that are selling for relatively high amounts – e.g. 1.3 million – that remain vacant for months. Who can afford to make that kind of investment and not live in it or rent it out?! It’s as though people are buying knick-knacks to place on their shelves.

An almost perfect time to sell.

They’re building a lot of high end senior citizen apartments and nursing homes in my area. But nothing for people who can’t afford to pay a few thousand a month. It’s only a matter of time before only the wealthy will be able to afford to die.

And here in Tucson, the student housing market is on fire. Literally.

https://www.kgun9.com/news/local-news/tfd-cost-of-construction-site-fire-8-10-million

In Phoenix in the condo complex where I rent for the winter for about 2500$/month some dud is asking 6K$ same rental but a little better location. The sale prices are up to the last bubble prices and still selling. I guess boomer are downsizing as I spoke to a few residents.

LoL, once again into the breach we go.

Say again, there is no bubble. Chinese hot money will be here forever….

Gold to the moon, oil will cost $1000 a barrel…etc etc etc.

Wages suck, and will continue to suck until immigration shuts down.

The really funny part is the housing market crashes when a real live owner with legal residency is required, or taxes are triple that base tax.

Splat. No more LLC boltholes, no more criminal laundering.

An America without the crime and lies would be very interesting indeed….

Wages shall continue to ‘suck’ not because of immigrants, but because of investment funds which demand continuous stock price and dividend growth to give their mostly already-wealthy clients even more money.

Hence ever-widening income disparity, and the ever-increasing power of the financial speculator, for whom the economy – and indeed society – must be ordered and run.

For the whims and desires of the wealthy and their stock portfolios, rather than the practical needs of the majority (eg affordable housing for families).

Not the first time in human history it’s happened. Cycle repeating after a brief spell of post-war general prosperity (achieved via progressive taxation invested in infrastructure) which was never going to stand.

Trees don’t grow to the moon, AFAIK.

A few weeks ago my wife and I were meeting with a private mortgage broker just to see what our options are at this point in time. We didn’t really plan to buy anything at this crazy height of house prices, but were curious to see what we quality for (more for planning in a few years out). We live in a nice suburb or Tacoma/Seattle on the Puget Sound side.

After about 15 minutes of the meeting, this broker started to get really honest with us (we were her kind of people) and the meeting became a 90 minutes rant from her of reasons “why in the world would you ever buy anything right now!?”

She survived the last recession (barely) and after riding this back up she’s seeing all the ins and outs of who is buying, why they are buying, the frenzy of it all, and the full details of the qualification process.

She’s 100% certain this is going to end badly again. Like all of us, she doesn’t know when or what specific thing is going to cause it, but it’s coming.

Salacious,

Not sure what type of details you were given, however, I have written loans both in this decade and the run-up and the loan quality is night and day.

There is no comparison to qualifying now vs then; so, the notion that “sub-prime” or “non-prime” loans are back or are contributing to this current market is just not true.

Broker Dan,

I’ve heard anecdotally that most of the current loans are fine in terms of monthly income but the downpayments are an issue, so the bank of Mom and Dad is used extensively. Has that matched your experience?

My impression is that the limited supply of homes is smaller than the size of the two-high-incomes buyer pool plus the foreign-all-cash buyer pool. This causes the bidding wars and it will continue until a recession causes supply to increase and trims the number of high household income families.

Lesson,

Actually I think that is a very good summary. Limited supply/inventory with a good mix of demand from first time buyers, move up buyers, foreign cash buyers and investors.

A lot of the loans I write are 3-5% down; some buyers have the money while others get a gift from family. There is a wide range.

1 day I write a conventional loan with 200k down as a gift from parents (retired boomers) and the next is an FHA loan with 3.5% down with money saved up.

In all scenarios; the buyers must qualify via income verification. So many buyers can afford the monthly, but, don’t have the capital to get in the game.

The kind of income verification that most these mortgage companies do is a joke. People with the know how can easily pass that verification even if they make $40K a year.

R2D2,

What exactly are you referring to? Care to elaborate a little more so people know what you are referring to.

Are you implying that buyers are committing fraud by photoshopping their pay stubs W-2s and/or tax returns?

Don’t spread misinformation please

Broker dan: Real estate and fraud; oh, no way. Real estate is run by nuns; no way, they have massive fraud going on :).

R2D2,

You still haven’t answered my question. How are buyers committing income fraud? Can you cite any examples?

Do you know how the income verification process works with lenders?

Pretty sure your answer is no to all of the above and you are just BSing and making ridiculous statements based on nothing so once again, I repeat stop spreading misinformation.

Real estate has been busted many times in the history of California. This is a fact and documented.

The reasons were different all the time but the effect was same.

The effect was: Housing prices rose to levels which were unsustainable and then fell drastically.

I am not sure what would cause the bubble to burst this time.. As Dan wrote, it won’t be sub prime loans.. then it would be something else.

Jon,

Yes that makes sense, although I would not anticipate a “crash” the likes of 2008 which seems to have been a once in a generation type scenario.

I think there will, at some point, be a pull back but not like some perma bears expect such as a 55-70% drop in valuations/prices.

I say buy if it fits your family situation and the payment is affordable.

I bought last year pretty much the perfect house for my family and something far under what I qualified (myself :) ) for. If the value drops, ya, that kinda sucks; but, as of now I am at 2 yrs reserves and working on my third year so I can take a paper loss as I don’t expect moving in quite a long time. In the meantime; the joy a large house and big back yard with pool (vs nice condo) has brought my kids is priceless.

There are a lot of factors to consider when looking to buy…..

“I am not sure what would cause the bubble to burst this time.. As Dan wrote, it won’t be sub prime loans.. then it would be something else”

The phony baloney Micro-Brew, Designer Coffee, Social Media economy and its collapse is what is going to cause the next crash.

Begbie,

I beg to differ. Microbrews are not “phony baloney.” They make some delicious stuff. And plenty of them fail. It’s a tough business in the real economy.

I have single friend who bought a beautiful 1500 sq home for $185,000 about 1 year ago in small town outside Raleigh, NC. She is a Paralegal and makes about $70,000. She is always negotiating work from home as much as possible to reduce commuting stress and expense. In Raleigh same home $300,000.

LIBOR will be gone by 2021. If you have debt, I highly suggest to research further.

I would love to see your take on the potential repeal of Costa Hawkins in California on the November ballot.

With the repeal, rent control will be possible on single family residences (SFR). I expect (hope) that a repeal will result in the investor class getting spooked, dumping SFR’s like hot potatoes, bringing supply up and prices down.

“Housing as a human right”, ie, the DSA and progressive left platform, is the future. Tenant “unions” are organizing in most major California cities to push for a Costa Hawkins repeal and bring rent control back. Watch this space. Increasingly, local politics will intervene on housing and my gut says this will be the ‘black swan’ that pops housing prices.

I see the statistic thrown around that only half of Americans have at least $1000 in savings. Even less have 6 months living expenses if times get tough.

When we hit the next recession, how many will default because there is no monetary cushion? I am struggling to connect Americans with <$1k saved to the housing bubble we are seeing now. Are these Americans predominantly renting? Or are they taking out mortgages they couldn't possibly weather a storm with?

NotBuying,

You make a valid point and I have seen similar articles. Maybe the divide between those with less than 1k and those with significantly more than 1k is getting larger; and the latter are the buyers?

Maybe some of those with less than 1k are long time homeowners (equity rich, cash poor) boomers that are stuck in their paid off or almost paid off house and unable to move? This further strangulates supply.

A large % of sales are all cash to foreigners so they aren’t in the organic (american) buyer with savings discussion.

I wonder what % of americans with less than 1k now vs during the previous bubble. If similar, then you must look at the loan quality now vs the previous bubble and extrapolate from there.

Maybe it’s a combo of all the above?

I really don’t have any idea and it’s an interesting facet of the overall RE question.

As a broker i see all kinds of loan files come across my desk. 1 day I will get a couple who makes 120k/yr with 20k in the bank, the next day I’ll get someone making 40k/yr with 1k in the bank and the next I’ll get someone making 150k with 300k in the bank. US is a big place with a lot of people that have lots of money and a lot of people that have no money. Guess it’s the stronger hands that are the ones buying…….

Just look what is happening in Toronto and Vancouver. SFR home owner have lost on an average of $150K in last year,

One year back, there were bidding war, people standing in a line to get a house there but now there is 180 degree turnaround in scenery

I am sure one year back very few thought about this and they all thought: we are special , land is in limited supply, and this time is different.

Crazy how time changes things.