The fear of becoming a “fallen angel.”

Companies whose credit rating is below “investment grade” can borrow in the capital markets in two ways: by issuing what is lovingly called junk bonds; and by issuing “leveraged loans.”

Leveraged loans are too risky for banks to keep on their books. Banks sell them, and they can be traded; or banks package them into Collateralized Loan Obligations (CLOs), and they’re traded as such. Being loans, they’re not considered securities, but they trade like securities. They’re the booming sisters of the languishing junk bonds.

According to Moody’s, this is what has been happening with junk bonds and leveraged loans:

- Junk bond issuance in the US plunged 52% in May from a year ago, to just $21 billion. Year-to-date, issuance has plunged 20% to $162 billion. The amount outstanding reached $1.27 trillion.

- Leveraged loan issuance in May jumped 37% from a year ago to a record $88 billion. Year-to-date, leveraged loan issuance rose 2.4% from a record in 2017, to $363 billion. The amount outstanding rose to $1.45 trillion. This is the first year that leveraged loans have bypassed junk bonds.

- Combined: As junk-bond issuance fell while leveraged loan issuance rose, combined issuance year-to-date fell 5.7% to $525 billion. The combined total outstanding amounts to $2.7 trillion.

The majority of companies is junk-rated.

About 60% of the US companies that Moody’s rates have a credit rating of “speculative” – otherwise known as “high yield” or “junk,” according to John Lonski, Chief Economist at Moody’s Capital Markets Research.

But these junk-rated companies tend to be smaller. Though they carry a lot of debt in relationship to their size (that’s why they’re junk rated), in aggregate they can’t measure up to the investment-grade giants, like Apple and Walmart that can issue tens of billions of dollars in investment-grade bonds in one fell swoop. For example, Walmart is currently flogging $16 billion in bonds to fund the acquisition of a 77% stake in Flipcart, India’s biggest online retailer.

So in terms of dollars, the amount of junk bonds outstanding ($1.27 trillion) accounted for only 17% of the total amount of corporate bonds. But when the $1.45 trillion of “leveraged loans” are added to the picture, the total rises to 37% — and that’s a lot of high-risk debt.

Future “fallen angels” are in the bulge bracket

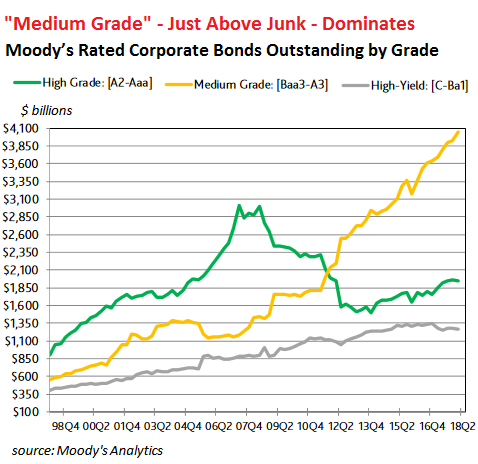

In terms of dollar amounts, 56% of outstanding debt is rated “medium grade” (from A3 to Baa3), according to Moody’s. Baa3 is one hair above junk (here’s my cheat sheet on corporate credit ratings by the three major US rating agencies). A one-notch downgrade pushes a Baa3-rated company into junk territory and turns it into a “fallen angel.” In other words, the majority of companies sit one to four notches above that level.

Since 2009, the amount of this outstanding “medium-grade” debt has surged at an annual rate of 10% to a record of $4.1 trillion, up 120% since the beginning of 2011!

Highest-grade bonds are vanishing

In terms of the dollar amount outstanding, 27% of bonds are rated “high grade” (A2 or higher). Since 2009, the total amount outstanding has ticked up at an annualized rate of 2.6% on average, including a 1.5% year-over-year gain in Q1, to $1.9 trillion.

But this average gain across the category, as puny as it is, hides the actual shift. Since 2009, the outstanding bonds issued by companies rated triple-A or Aa dropped 5.5% a year on average, and now amount to just $628 billion. And this comes despite a surge of mega-issuance by Apple (rated Aa1). The reason: there are fewer and fewer companies with these ratings.

Triple-A is dying out. Only three US companies are still rated triple-A by Moody’s: Microsoft, Johnson & Johnson, and ExxonMobil. And it’s not because the credit standards have become stricter but because companies have taken on more leverage to buy back their own shares and to fund acquisitions in the cheap-debt era, and/or they have run into a buzz saw of problems, such as GE.

By contrast:

- The amount of bonds in the single-A category rose 3.1% on average per year since 2009, to $2.66 trillion.

- The amount of bonds in the Baa category (just above junk) rose 10.5% on average per year since 2009, to $2.69 trillion.

This chart by Moody’s shows how “medium grade” (A3 to Baa3) has come to dominate over the past few years (yellow line), compared to high-rage (green line) and junk bonds (gray line). Note however, that this chart does not include the surge in leveraged loans, the sisters of junk bonds. With them included, junk-rated debt, at $2.7 trillion, would be over halfway up the chart:

One more word about Fallen Angels

About $640 billion in bonds are rated Baa3, one hair above junk, up from $295 billion in Q3 2007, just before the Financial Crisis. A one-notch downgrade of the issuing company would put them into junk territory. This would be the “fallen-angel downgrade.” Moody’s points out that on average over the span of a year — and these have been the good times — 10% of Baa3-rated companies are downgraded into junk . And there are consequences:

In view of how most companies wish to avoid a fallen-angel downgrade, and given the age of the current business cycle upturn, companies having a Baa3 bond rating might opt for relatively conservative financial management. Such companies might be expected to proceed cautiously with capital spending, employee compensation, acquisitions, stock buybacks, and dividends.

This is one of the ways in which debt and credit ratings can impact the stock market: via scuttled share buybacks and dividend, long before the viability of the company is seriously in doubt.

This is one of the biggest such deals ever, happening now: A group of PE firms extracts $3.75 billion from a company after they’d already extracted billions. Read… This Deal Shows How the Junk-Credit Market is Still Irrationally Exuberant

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Where are our worthless regulators and enforcers in all this?

Sleeping at the wheel. After all who can see a debt train wreck coming. Obviously not the regulators and enforcers. Also why bother when assets can be marked to market whenever they want, the Fed’s money spigot is there should it collapse the system, if that is not sufficient acronym money is there to be funneled with no questions asked (after all when the house is on fire), if that is not enough you have savers, prudent people begging to be skinned, and to top it all you have the”sitting ducks” – the tax-payers to bailout the system. Nothing to worry. Make merry.

Regulators? Haven’t we spent the last 40 years voting to put a bullet in the back of the head of gubmint regulation?

Yes, this is an unusual time (my opinion) in the US, where Executive Branch regulators (e.g. SEC, Fed, FDIC, etc.) have failed. The system is supposed to work such that when this happens, the Congress/Legislative oversight function, spanks them. This is not happening. It has to do with ethics, as far as I can tell.

Do an internet search on Greenspan meetings with Brooksley Born and Sheila Bair between ~1999-2007 (something like that). That is how work is (not) being done by the regulators.

Bernanke, Yellen, et. al. are on record as saying they can’t detect a bubble as it is inflating.

Good Luck

Regulators are grease of Wall Street..rather make their money making machine smoother since they are like H2o to drown the market..

Perfect example of Risk Relief Hazard (e.g. if you are insured you take more risks). The sheeple think the regulators have taken the risk out of the markets so they don’t give a thought of where their deposits or 401K contributions go.

The regulators have merged with the regulated into one agency. Why not, when there’re no consequences?

They are doing their job. Democracy works. Communism is bad.

No amount of regulation can withstand the following:

1. Muppets’ greed.

2. Muppets’ cowardice.

They go hand in hand actually.

Sleeping at the wheel is too kind. Utterly corrupt and carefully looking the other way is more likely what is happening. Prepare for another bankster bailout when the price of these debts collapses and banks are not able to get rid of their garbage holdings to gullible investors.

That is what happened in 2007-8. Banks hold trilli ons in deposits but have capital worth on!y 1 to 4% of their holdings. Only a small downturn in investments makes banks become insolvent.

“…This is one of the ways in which debt and credit ratings can impact the stock market: via scuttled share buybacks and dividend, long before the viability of the company is seriously in doubt.”

Share buybacks are rarely used to finance a company’s expansion. They are usually used to pay dividends. Companies that consistently buy back their shares reduce the float and grow EPS at a substantially faster rate than would be possible through operational improvements alone.

Executives and large shareholders usually own the lion’s share of a company’s equity. Therefore, one must conclude that share buybacks is little more than an euphemism for transfer of wealth to the rich, which in itself is an euphemism for legalized theft.

Suppose you own one share of company XYZ and an executive owns a thousand shares. An increase of 10% in the value of a share of XYZ won’t make you any wealthier but it will make the executive a heck of a lot richer when he sells off his shares. Unless you sell when he sells, you will own a share of a company that has been decapitalized in the process of enriching executives and large shareholders.

Correction. I took a shortcut. I should have said “Companies that incur debt (via bonds or loans) to buy their own shares or to pay dividends… etc.”

That’s the argument for theft, ….errr… increased shareholder value.

Yes, most of us are aware that buybacks are used by executives to juice their own compensation. Your explanation is helpful, but where did you get the impression that this articles says buybacks are used to finance a company’s expansion? I don’t see that here or in any of Wolf’s work — he knows very well that buybacks don’t help the actual business of the company.

“Suppose you own one share …and an executive owns a thousand shares …” An increase in the value by 10% will actually make us both wealthier in the same exact proportion.

However, you and i may agree that the system is often played/manipulated and/or corrupted in many ways by people, i.e. who possess “greed”. To that I would add that the people who find the most fault with that fact are the most envious. Pick your vice – envy or greed. Both are similar fruits of a poison tree.

What I find interesting is that there are so many who believe that the greedy people can be overcome by the envious people simply by electing leaders who are supposedly righteous. And the supposed righteous ones possess enough arrogance/pride to think they can and should micromanage everything …and everyone (except themselves).

When we become honest enough to admit that we all possess both envy and/or greed, we begin to understand real potential solutions. If we are not willing to be honest with ourselves, we have little hope that others will treat us honestly either.

I don’t think you can equate CEOs and the rest of us insofar as greed, callousness, insecurity, and paranoia are concerned. They are the cream of the crop in that category, and that’s why they are CEOs.

LOL. Hey I can be greedy and callous as anybody (ask my ex-wife). Where do I apply for one of those CEO jobs!

Greed is NOT the issue.

Let them go for their greed. But they the shit hits the fan, no bailouts, let people go to prison, heads roll.

And no money printing. If their greed tell them to borrow, they borrow from me, or the people who have savings, see what rate I will charge them. In stead, they borrow from the FED, printed papers, at low/no cost.

Yes, there is greed in everybody, but the FED and the treasury encourages and amplifies greed and removes accountability and punishment mechanisms.

JZ, Totally agree.

“Share buybacks are rarely used to finance a company’s expansion. ”

I’d go one step further and say by definition, buybacks are counter to expansion.

As WR points out one dubious domino after another, including the cryptos, I still wonder about the theory that the inevitable credit crunch will be gradual, if not a soft landing.

How could a credit crunch happen gradually with all kinds of traders, human and others, watching screens 24/7?

When ‘deep junk’ falls off the cliff, will the medium junk become more or less desirable? Or will there be a flight to real safety as everyone loses their appetite for risk at the same time?

Will they run for safety in Amazon trading at a PE of 250 (or so) or will they hide in Tesla? (another WR ‘favorite’)

If the Fed is going to ride to the rescue again, they may have to move faster than last time. The last time was close enough and they still haven’t cleaned up the mess from that one.

Has there been enough deleveraging to prepare for the storm, or is the ship still partly flooded from the last time?

From what I can glean, the leverage of the big American banks isn’t nearly as bad as it was in 2007-8, but corporations, households, and the government are in worse shape, as are nations dependent on commodity exports to survive. So, from the point of view of the Fed (which overwhelmingly cares about the big American banks and a very far second about anything else) they may perceive the next crisis in starkly different terms than people in New Orleans or Nigeria or North Dakota do. They’ll likely sacrifice the periphery to maintain the core, but the core is such a small subset of the polity that the results could be ominous.

I would agree that banks are in a much better spot w/r/t leveraged loans; the leveraged lending guidelines are only now being really rolled back and loosened at the bulge brackets and large banks.

I think this next cycle could more acutely affect the unregulated institutions who took a ton of market share since ’09 in this space because the banks were under the microscope and couldn’t make many of these loose/covenant light loans.

So IMO it may not be as deep of a run on FDIC deposit-taking banks like in ’08/’09; however, in this huge chase for yield, you have a lot of investors in corporate debt and leveraged loan funds/ETFs that don’t know what they’re buying, aside from chasing yield, which is dangerous.

50-50 :-]

1. My version is correct: “Majority” = singular; hence, “The majority is….”

2. Your version is correct: “these” — and I fixed it.

Thanks.

The ship is upside down.

https://brians.wsu.edu/2016/05/24/majority-are-majority-is/

DEBT.

Its the debt.

Bonds are just another name for debt.

Be they triple ‘A’ rated or junk. They’re still debt.

Minimizing risk is the smart play and swimming with sharks in the same pool is not only risky but foolhardy. Too much uncertainty around.

So our beloved president wants to slap a 25% tariff on just about everything. My prediction: with a sweet new profit margin available, American corporate leaders will take on massive new piles of debt and jack up prices to pay it. Net effect will be a massive reduction the standard of living of the population.

What I try to remind myself when listening to the puerile political discourse in America is that all politics in America not practiced among the Power Elite is symbolic, not substantive. If you are looking for coherence or foresight, you can forget about it. There aren’t 10 Senators and 30 Representatives who know what they are doing and take the job seriously. It’s all an exercise in semiotics, and Trump is the Pantomime in Chief. His statements are about ginning up his base and serving his ego (Obama’s were about soothing the elite and serving his ego, which is why he was more popular among the servants of the elite).

Most of what you say is true. However, you don’t give the voters enough credit. Both p44 and p45 were “vote them all out” candidates, one a black guy with no money elected by white people, and the other a billionaire elected by the mostly poor.

We know the system is broken and totally dysfunctional, but cleaning up is a long hard process which may not work. You may think that p45 is in it for the ego trip, but I think he’s in it because the system doesn’t function at the top either. The reason I trust him more than the others, is, because he has real skin in the game. If the system fails, he’s one of the biggest losers.

Created huge dividend with tax cuts ?

Steel and aluminum are tiny portions of the overall economy and 200 billion worth of goods for the Chinese doesn’t even cover half of their trade deficit. The tariffs collected goes to the Treasury, but probably doesn’t even cover the lost taxes on wages and profits that occurs when imports replace domestic production. That is why all other industrial nations utilize VAT taxes, which by the way dwarf what is currently being considered for tariffs.

The only thing massive is the hyperbole of your post.

OK, if steel and aluminum are such a small segment of the economy, why is Trump so obsessed with them? If they are tiny, aren’t there better, more important things for him to be spending his time on, like repealing and replacing Obamacare or bringing back Glass-Steagel which he promised to do or cutting waste and corruption out of our vast military budget? Just asking.

To understand Trump’s MO, study his purchase of the Taj casino.

He did it with 800 million of junk bonds when they were still a fairly new idea. At the time THE veteran casino financial analyst said it wouldn’t be able to pay the interest.

A year later it went bankrupt for the first time.

Then it was re-financed, then went bust again.

Trump had extracted fees every step of the way.

The funny thing is, Trump has bragged about making money while the host died.

By the mid-nineties, no US bank would deal with Trump, so he looked further afield.

actually, it’s Leverage.

Playing out exactly as planned. The whole idea behind record low interest rates was to get people to borrow and spend, and so “reflate” the economy.

Of course what the money was borrowed for and what it was spent on were outside the control of the CBers, And therein lies the real risk: over leveraged companies and individuals and over valued assets.

Implementing the policy as surprisingly easy. Getting back to normal will not be. The Fed clearly now sees at least some of the dangers, and so wants to unwind the balance sheet and raise rates. We will see how far they go before retracing. (The tax cut gave them a bit more short term room, but makes the long term problem even worse).

There really is no safe way back. The reckoning can be postponed for quite a while (see Japan), but ultimately it will occur.

Spend our way to prosperity with borrowed money. Pure genius, Ben and Janet. What could possibly go wrong?

Maybe I am dumb. But I sleep at night

No mortgage. No car payments , no credit card debts. I am loathe with every ounce of my body to take on any unnecessary debt for now

Yep my cash not making much

But I wait as the markets are in long term topping mode. I wait patiently.

In the meantime I work on my cat videos

To monetize on you tube. Sitting on gold there.

Wolf,

These CLOs, they bundle a bunch of different leveraged loans into a CLO; leveraged loans from different companies which means some strong players and some weaker ones? Leverage loans used more by weaker vs stronger players?

If above is correct, the CLO can default or whatever word is used to describe the situation for a CLO when a few of the leverage loans implode correct? So its like Jenga and we could see a domino affect, No?

The CLO needs to maintain its coverage test as a whole; so as cash flows deteriorate and they trip their ratio, they have to reroute incoming cash flows to the most senior tranches out of the lower priority tranches and the equity. Which erodes the yield and the attractiveness of the overall vehicle and reduces its value. It can get messy pretty quickly.

Sprinkle in the fact that many BDCs who have never been regulated have grown to be larger than some of the banks considered SIFIs; no one really knows what bombs are lurking in there.

It’s almost like we’ve been down this road before….

Let me just say this: In the most basic terms, banks bundle loans from junk-rated companies and then slice them into tranches for rating purposes and sell those tranches. That’s why CLOs are called “structured” securities.

So loans by junk-rated companies get packaged and cut into slices where, in case of default, some slices take the first loss (lowest rated slices) to slices that take the last losses (highest rated slices). The highest rated slices of a CLO — backed by loans from junk-rated companies! — may have a triple-A or double-A rating. And the lowest-rated slice that takes the first loss might have a B-rating (junk).

In good times, default rates on CLOs are low. And most of the risks are spread among investors, not banks.

In terms of the companies, when one of them defaults, it only impacts that company, not the other companies. But when defaults accumulate, then suddenly the entire industry is impacted (such as energy during the oil bust or brick-and-mortar now), and it’s harder for those companies in that industry to raise money to service or pay off their old debts, and then defaults cascade across the industry. This has broader impacts on CLOs as well.

An interesting side note: I read somewhere that Micheal Milken, the creator of the junk bond industry, put out the word that he would like to be pardoned. Currently, he may be barred from the securities industry. Imagine the possibility, Drexel on steroids, scary.

Ha, good to know…

I hafta tell you a little story. Back when when I was getting my MBA, Milken was huge (unbeknownst to us, just a couple of years away from being indicted). In B-school, he was a hero at the time, and Drexel was hot.

But given his age now (early 70s), I doubt he has the fire left in him to do it all over again. I think he’s trying to polish his “legacy.”

Petunia- previous comment about demographics of the 2016 presidential election. Mostly myth, see:

https://fivethirtyeight.com/features/the-mythology-of-trumps-working-class-support/

Median income of Trump supporters was higher than opponents’.

CLO’s being just one small part of the whole.

ABS – asset backed security

MBS – mortgage backed security

CDS – credit default swap

Collateralized:

CDO – debt

CMO – mortgage

CBO – bond

CLO – loan

CFO – fund

SSL – senior stretch loan

And the best for last – PIK bonds – Payment In Kind

These are covenant-lite bonds with no protections and pay yields not in cash, but with more bonds! Payment in kind.

What could go wrong? lol

Something new thats old.

In 2015 several large Wall street banks began selling billions in something called a “Bespoke Tranche Opportunity”. (BTO)

A BTO is just another name for a CDO.

One person’s opinion; it is different this time because a huge amount (>75%) of these loans are covenant-lite, meaning that while these borrowers go down the tubes, the lenders/CLOs will have to sit idly by watching until they ‘default’, which will only be BK or insolvency because they agreed to no financial covenants.

In the ‘old days’, you would set a leverage or fixed charge covenant so as the borrower struggled, they would trip the covenant and allow lenders to pop in and at least have a say in what to do next or act on their rights; that is effectively gone.

You will have a PE firm whose equity value is severely impaired/gone, has written off the investment and won’t contribute another dime but is still in control while they look for a Hail Mary for a zombie company.

So the actual ‘default rate’ will be lower this time through, because to be in default the company will have to be effectively BK; however, the loss per default is going to be higher because lenders will have had to sit and watch the carnage, and will not exactly be incentivized to cooperate with management/PE firms for a solution.

This seems to jive with your article last week about the ‘smart money’; a lot of the fundraising being done now is for distressed/value investing; aka there will be significant vulture/loan-to-own carnage as lenders try to hit the exits.

Assets will be sold, often for pennies on the dollar. The result being that asset prices collapse. Equity levels drastically decline. This triggers more selling of assets. Credit levels shrink as the value of underlying collateral vanishes. Cash flow dries up and debt service stops, generating more asset sales and bankruptcies become common. This now becomes a self reinforcing cycle of economic negativity. A depression.

GSW,

Yes, the dominance of covenant lite loans will definitely change the equation when these credits get in trouble. I’m not sure that we even know how this will impact the market since we’ve never seen that kind of cov-lite dominance.

You suggested some ways. And I agree. Cov light will slow down the arrival of defaults, with the result that when the companies finally do default, there will be even less left over for creditors.

Cov lite provisions help companies avoid technical defaults and defaults caused by short-term issues (provisions such as PIK go a long way in that direction), but they don’t do much good when credit seriously tightens and companies are looking at years of difficulties, and when they need to raise new money because they’re cash-flow negative.

The charts looks to be saying that high grade and medium grade are exchanging places while high yield stays the same, which is how I see it, lower yielding bonds are going to get hit harder.

So basically, if yoy heard the word “leveraged” run away to the hills because a flood is coming?

Investors are hungry for yield,so they have gravitated toward lower rated credit. The default rate for these securities has been low so buying these credits has proven to be a good investment .As long as the economic expansion continues, the default rate will remain low.But when the economy enters the next recession, defaults on low rated credit will soar.To a very large extent default rates and the NASDAQ are tied together. A recession will cause the prices of these low rated credits to tube at the same time that investors realize that the prices that they have paid for tech stocks is far,far above any rational valuation