Subprime goes to the Toronto condo market.

By Stephen Punwasi, Better Dwelling:

A few weeks ago, a real estate agent told me about his client. Relatively wealthy older dude, closed on not one but two townhouses he plans on flipping. After some questions regarding who financed such a deal, he explains it was a private lender. Right before adding, “don’t worry, it’s not like in the US. This guy has good credit, he just couldn’t get enough money from his bank.”

I realized that people aren’t lying when they say Canadian real estate is nothing like the US in 2006. Canadians just don’t understand what happened during the US subprime crisis. They also don’t really understand subprime lending is alive and well in Canada, we just use different names.

Subprime Borrowers Vs. Subprime Loans

First, a quick lesson on subprime. The S-word is a dirty word in Canada, so there’s little discussion about what it means. Most people think “broke ass borrower” when they hear the term, but that’s not always the case. There’s subprime borrowers and subprime loans.

Subprime loans are any loans that are below prime, as in the typical lending criteria isn’t met. The part that’s poorly understood is a borrower, a loan, or any combination of those can be subprime. A borrower with excellent credit, might want a subprime loan. This happens more often than you think, and is usually because a bank won’t lend as much money as needed. No one thinks of a family in a nice neighborhood with a private loan to buy their fourth or fifth condo as subprime, but they are.

Don’t worry, it’s not just average people that don’t understand this. There’s still a lot of confusion about the issue in the finance community around the US subprime crisis. Most people knew subprime lenders blew up, and naturally blamed poor people and immigrants with low credit scores, as is the way. However, new research shows that the sudden rise in foreclosures during this period were due almost exclusively to investors with good credit. Good credit, but using subprime lenders.

Subprime borrowers defaulted at the same rate they always did. Investors using subprime lenders jumped by a “factor of 10.” When prime borrowers couldn’t get the loans they wanted, they went to the lenders that would. So yes, it was a subprime lending problem – but not due to poor people. These were mostly middle class investors. Whole textbooks will be written on the topic, but what you need to remember today is not all subprime loans are to people with bad credit. However, all have insufficient credit for the size of loan they’re looking to borrow.

Subprime Lending, Private Lenders, and Interest Rates

Canadian subprime lending is often done through private lenders, you access through a mortgage broker. Good brokers always start at the best lender, that usually has lower rates than your bank. When you don’t qualify for these, they move up the chain. If your credit profile won’t even work at “bad credit” lenders like HomeTrust, they’ll suggest a private lenders. Bad credit, no credit, no problem. There’s usually a private lender that’s willing to make a deal.

Sounds great, so why doesn’t everyone use private lenders? They aren’t taking bank rejects as a charitable cause, they’re doing so because they can charge a risk premium. Despite being off of record low interest rates, these lenders charge upwards of 8% and we’ve seen mortgages well into the 20s. The broker also gets 1%-3% of the loan, so there’s little reservation suggesting them. If you can do math, you’re probably wondering how people make money on these deals? They can only do so if they hold it for a short period of time. If you’re bad at math, you may be one of these borrowers not realizing you’re only paying interest on your loan, and not reducing your debt. Regardless, this is where Canada’s subprime borrowers lurk.

Canada’s Subprime Market

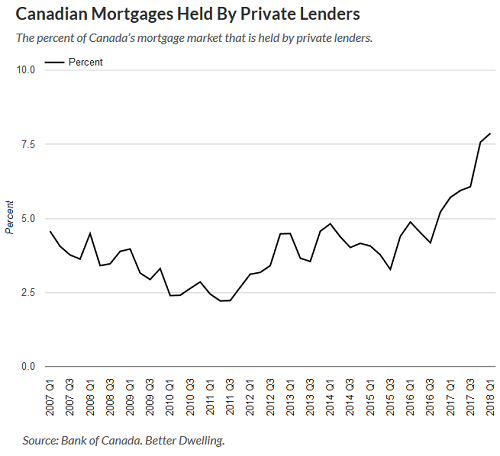

You know that commercial from the Big Six bank, where the borrower goes into a bank and they tell them they’re richer than they think? Well, according to the credit rating TransUnion, over 1 in 10 Canadians probably wouldn’t get that reaction. Transunion estimates that 11.9% of the 28.4 million Canadian consumers with credit profiles are subprime. That’s roughly 3.4 million Canadians, but we can’t be sure these are the borrowers. What we do know is private lenders became extremely popular in Ontario recently.

Bank of Canada (BoC) numbers show that despite a decline in sales, private lending is growing in Ontario. Mortgage originations at private lenders in the Q1 2018 rose to $2.09 billion in Ontario, a 2.95% increase from last year. That should raise a few flags, since dollar volume of real estate sales are down 37.64% during the same period.

The market share of private lending went from 5.71% of originations in Q1 2017, to 7.87% in Q1 2018. While originations at other channels are dropping, private lender originations are growing. The province either has a lot of people with bad credit jumping in, or a lot of over-leveraged speculators. Neither should inspire market confidence.

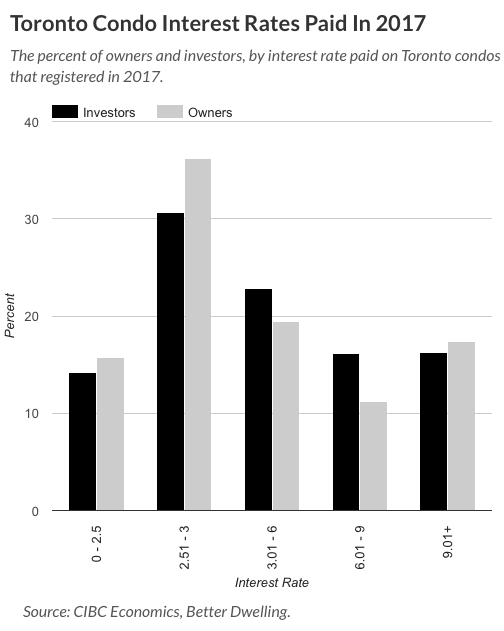

Subprime Goes To The Toronto Condo Market

As a result of apathy (or incompetence), the government doesn’t track subprime lending. Shocker, right? However, if you wanted to see how it contributes to the market look no further than Toronto’s “healthy” condo market. We don’t have the number of subprime borrowers in that market, but we do have the interest rates being paid. Since we know that unusually high interest is charged by private lenders, we at least have a proxy to help us understand condo buyers.

Interest rates are just above record lows, but a lot of people aren’t paying low rates. CIBC Economics numbers show that over 1 in 10 Toronto condos registered in 2017 were attached to astronomically high mortgage rates. Over 17.4% of owner occupied condos registered in 2017 had a mortgage rate above 9%. Over 16.2% of condo investors with units that registered last year were paying more than 9% as well.

That’s a lot of units with unusually high interest rates buying condos – not a great sign of buyer quality. These buyers are likely waiting to flip at the first sign of buying weakness, or don’t realize how difficult it’s going to be to make a profit at that rate.

The government doesn’t track subprime borrowing, but the signs are there. More middle class speculators or broke-ass buyers are going to private lenders. Many of these buyers likely think they’re the only people doing this. The market appears “healthy,” because not a lot of these people understand that a lot of other people are doing this. As rates rise, price growth tapers, and sales decline – this becomes what equity traders call a crowded trade. If you’re unclear what a crowded trade is, there was this thing called the US subprime credit crisis. It’s pretty similar to what’s happening right now. By Stephen Punwasi, Better Dwelling

The average price of single-family house plunged 13%, or C$160,000 from the peak. Sales of homes priced over C$1.5 million collapsed by 63%. Condos are still hanging on. Read… Toronto’s House Price Bubble Not Fun Anymore

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

– I have a question: How much canadians pay only interest on their mortgage ? That can’t afford to pay down principal ?

– I ask because when I look at Australia then some 50 to 60% of mortgage owners don’t pay down principal because they can’t afford it. Real estate prices in Australia are WAY to high. Already this year (and in the coming years) more and more of those “interest only” mortgages are resetting to “Principal & Interest”. In that regard those australian mortgages are also “Subprime”.

– The subprime crisis in the US began when 1) interest rates rose and 2) those mortgages began to reset to “Principal & Interest”.

Hi J M Keynes, good point you make ref interest only mortgages in the UK it’s 19% are interest only mortgages. Wolf what’s the percentage of interest only mortgages in the US and Canada?

As far as I know, and by experience, interest only does not exist. I have had a few mortgages over the years and the blended mortgage is the norm. I suppose if a person was in hot water you could defer and pay interest only? But, I doubt it.

Maybe not for new mortgages, but for people that have an equity line of mortgages, where the original mortgage could be paid off, (such as a reverse mortgage), they need not make any payments monthly, but the interest owing of whatever 200k, 400k, or 75% of the value +/-, is automatically withdrawal every month.

In Australia, until the last few months, 40% of all new mortgages over the last 5 years have been Interest Only and they’re currently resetting at a phenomenal rate. The IO period is between 3-5 years only and then it resets to P+I which is a much higher amount.

A lot of people who bought expecting to sell out in the interim at a profit never having to hold the loan till the P+I period are now caught and underwater. True to animal instincts, many of them are freezing in the headlights hoping to hang on until the market recovers instead of taking the losses.

For many, taking the loss would wipe out the nest egg they built over years and so they’d rather go for the long shot of a hail-Mary recovery. Sadly, it’s wishful thinking and they are going to have to go bankrupt or spend the next ten years of their life paying for past mistakes.

So the prices atm are still sticky on the way down due to these “klingons” but plummeting sales and auction data tell the story. On top of this, the Chinese buyers have evaporated and wages (although very high) are stagnant.

The only driver left is the government immigration Ponzi of bringing 200,000+ people per annum into the 2 big cities. But they don’t have much money. They’re just cheap labour and a driver for the rental market. Oz is screwed.

I think we will find out the true health of the Canadian homeowner by next year once the bond interest rates rise more. Even though the Bank of Canada isn’t raising interest rates in step with the US, it’s interesting how most mortgage rates are are still creeping up. My opinion too many fools not to lock in their rates.

In Canada, we really don’t know, most of our stories are hearsay, all levels of governments are afraid to put the puzzle together (at least publically) to find out how bad it really is out there.

For example behind my house are 2 empty homes not for sale and another home a couple houses down the street just went on the market, and that house is also empty. The people in the homes were not foreign buyers, they were locals.

Even if there was a mortgage on all three properties, the mortgage could be paid with a type of credit line called a home equity line of credit (HELOC), where borrowers can make interest-only payments if they want to, but the rate on that loan is variable and increases with every interest rate hike. HELOCs increased in Canada by a $1 billion in April 2018, we only have 35 million people living in the country.

https://betterdwelling.com/canadians-borrowed-another-billion-against-their-homes-over-a-31-day-period/

Question: in Canada can you normally leave the keys to the bank and walk away from ‘your’ morgage? Thanks!

You can’t easily walk away from debt or your mortgage in Canada, very few mortgages are non-recourse mortgages.

We only have 6 large banks in Canada and a handful of smaller credit unions. All institutions that are not a credit union have an account sitting at large bank – e.g. Bank A may look like a local/small competitor to one of the 6 bigger banks, but all of their accounts and your money sits in a large account at one of the 6 big banks.

This makes walking away from your mortgage difficult because in most cases your bank already knows where you went to hide your money. Once you stop paying (e.g. walk away from your mortgage) they can freeze your accounts and cancel your bank credit cards to take as much money as they need to, to make themselves whole again.

If you owe say $15,000 in back mortgage payments, and you have savings of $5000 in their banks, they can take the $5,000 then ask for a court order to go after all your other assets such as investments that are not in retirement funds or garnish your wages until they are completely paid back.

If you emptied your bank accounts before they could do it for your (which is difficult as the banks would probably not let you take money out if you stopped paying your mortgage) and you had credit cards with non-banks e.g. Costco or some other department store or Chase Mastercard (which is from America and has no ties to Canadian banks). The non-bank credit card companies may cancel your credit cards because they get your credit history report which would flag that you are delinquent on your mortgage payment. Then you would have no access to cheaper credit.

You may be able to go to payday loans to pay bills until you figure out if you want to file for bankruptcy or a consumer proposal (consolidate debt and pay off less than you originally owed), but payday loans usually lend less money at higher rates than credit cards.

To be more accurate to the name “simplyput”, everyone in debt can file for bankruptcy. Forfeit the homes and any other items worth any value to cover the debt, then start over with a poor credit score.

Like that will stop them from giving people more credit.

Isn’t an interest only mortgage

Basically renting with the added risk of bankruptcy?

This made me laugh, great comment :-).

In Australia it’s particularly prevalent for a few reasons, the major one being Negative Gearing. Due to the tax write-offs of interest payments, it makes no sense for an investor to have a capital repayment mortgage (as he can’t write that off), his only play is to flip the property in a few years for a nice capital gain (and get the 50% tax discount for owning the asset for over a year). This capital gain over the past few years has been pretty significant – 70% since 2013.

As you can see the tax regime is pretty incentivized towards property investment and its certainly been a factor. Roughly about $120 billion in interest only loans roll over into principal repayment in 2019 if there is any sort of recession or the market has started really falling it could be a bloodbath.

Unfortunately, everyone knows the market is over inflated but politicians here love people feeling rich through the value of their homes!

I remember the late 90’s when I was working in Toronto for an advertising that specialized in real estate development advertising, specifically condo developers like Tridel (the only one still around), cranes were everywhere in the sky. I was fresh out of College and the cost of a 1 bedroom condo downtown was 90k. Then the bottom fell out of the real estate market. I lost my job and got pregnant, and have never really recovered.

When the subprime crisis hit in 07/08 I was a mortgage broker. I was talking talking people out of mortgages because I knew they would regret it.

As I 55 year old, I have hit every downturn at the worst times of my life. I guess that is why I actually feel this coming. It’s burned into my memory. We all forget how things were then, but it’s coming again, only this time things will be much worse.

I’m sorry you didn’t get over your pregnancy Jane!

Chin up, Ms Jane.

First, and in your defence, you are by your stated age at the very tail of the Baby Boomer generation. There has been a pig in the python just ahead of you for your whole life – and those pigs have gotten the spoils of every economic boom before you.

Second, and in support of your awareness, the theory of Adaptive Memory puts you in a better position this time. “An organism with the capacity to remember the location of food, or categories of potential predators, was more likely to survive than an organism lacking this capacity.” Unlike what appears to be 9 in 10 of your fellow citizens who are in denial in this market, the prior negative experiences burned into your memory place you better for survival in the coming downturn.

Remain diligent, frugal, and if you can, ready with a small war-chest. Your best days just might be ahead of you (and your thirty something offspring).

The local speculators and flippers in the detached housing market know there is a problem. Condo speculators are in denial, but sales are down in Ontario so they should get a reality check very soon.

A few more rate hikes should help speculators understand, there are no foreign investors coming to rescue them. Even if the speculation taxes were removed in the province of British Columbia and Ontario: there are more local sellers than foreign buyers still interested in Canada, the government of Canada is going after people for the taxes they owe reducing the net profit of their flip and the government is sharing the information they collect from foreign buyers with the home country of those buyers.

Canada right now is the US circa 2007

The unilateral tax agreement between Canada and China comes into law this September. This is where Revenue Canada will nail every Chinaman that evaded taxes on Canadian properties compliments of the Chinese government.

The REIC in Canada is corrupt to the core, and like its counterpart in the US, its lobbyists have Canada’s politicians, regulators, and enforcers in their back pocket. Since Canadian realtors have a vested interest in keeping the housing bubble from bursting, they’ll find a way to ensure the Chinese embezzlers and money launderers who are parking their ill-gotten proceeds in Canadian real estate are given ways to circumvent any new laws.

The shady loan business will always be an issue, but the increase explains why all the Big Banks that are considered safer are pumping out subprime variable rate mortgages. They must be relaxing their own rules to compete.

Ever since China got serious in cracking down on money flowing internationally the Canadian market has cooled. Vancouver ignored the local tax hikes and regulations that tried to slow it last year but this year the sales finally slowed down.

I may be running low on savings waiting for this bubble to pop, but I have spent it all on popcorn to enjoy the show.

Your last line is hilarious. Made my day :-]

Vancouver and surrounding area house sales have collapsed by 65% in Vancouver proper to as low as 85% in places like Maple Ridge. Prices down hard in some districts, over 30% drop, as well as huge declines in sales.

The crash has commenced.

https://www.zolo.ca/vancouver-real-estate/trends

North Van sales of houses down 72%

https://www.zolo.ca/north-vancouver-real-estate/trends

Richmond house sales down 75%

https://www.zolo.ca/richmond-real-estate/trends

Burnaby house sales down 83%

https://www.zolo.ca/burnaby-real-estate/trends

Surrey house sales down 81%

https://www.zolo.ca/surrey-real-estate/trends

West Van house sales down 79%, prices down 34%

https://www.zolo.ca/west-vancouver-real-estate/trends

Maple Ridge house sales down 85%

https://www.zolo.ca/maple-ridge-real-estate/trends

Like this across the board, buyers are gone, just waiting for the inevitable price crash

Two things move the market: greed and fear. Greed had a good run, thanks to the Keynesian fraudsters at the central banks and their deranged money-printing and credit creation. But the financial reckoning day could not be deferred forever.

The supply of Greater Fools in Canada just dried up, though the reckless and greedy who bought into this insane housing bubble at or near the peak probably lack the intelligence to realize the magnitude of the financial calamity that is in store for them, and Canada, when the bottom drops out.

Got popcorn?

I’ve seen a couple of owners in the very nice Kerrisdale area of Vancouver, multi-million dollar home sort of thing, sporting huge signs in front of their houses decrying the government theft going on with fees and taxes.

That’s just off the main 49’th/SW Marine Drive strip. There may be more on the inner side streets.

One has two signs about 8’x4′ each in front, bright red and large print.

Not sure what to think. If they’re foreign I don’t really care. If they’re true Canadians then I do have sympathy. Some people just want a place to live.

The government introduced a small property surtax on homes valued over $3mn (the tax can be deferred until the home is sold, typically as an untaxed capital gain in the millions of dollars). People’s mileage for sympathy may vary.

Good post, and I recommend the ‘Better Dwelling’ blog to all, almost as much as I recommend this fine place.

I’ve seen a couple of owners in the very nice Kerrisdale area of Vancouver, multi-million dollar home sort of thing, sporting huge signs in front of their houses decrying the government theft going on with fees and taxes.

Cry me a river, Greedheads. The insane run-up in housing has been driven by one thing: central bank “stimulus” that has fueled the most insane asset bubbles in human history. You certainly didn’t see any signs on their lawns decrying the swindles against savers or future generations being perpetrated by the Fed, BoC, and their ilk, or lamenting that young couples trying to build a household had been completely priced out of the market – at least the prudent ones.

It won’t bother me in the least if the “homeowners” who bought into these housing and stock bubbles end up living in cardboard boxes when fiscal reality finally asserts itself.

I think the last chart is not the intended one.

Thanks. Fixed.

That be a Bubble…a YUUGE Bubble! I wondered how Canada real estate kept going up and up. Enter Private Lenders. Who are the big private lenders besides HomeTrust?

I’m just an amateur with an interest in credit and housing.

My take is that a lot of Canadians with these subprime mortgages will end up as bag holders if the condo market crashes before they can flip.

If they are bag holders, they will probably be forced to sell at a loss by the private lender.

The way Canada works is that the the person holding the mortgage will still be on the hook for the difference. They also (generally) can’t can’t walk away from the house loan either.

The way I perceive this is different from the USA 2008 housing and credit crisis.

1) The private lender has to hold these mortgages on the books.

2) These mortgages are not insured by CMHC

3) If the original lender does not hold the loan and offloads it, I don’t believe they could easily bundle a bunch of subprime mortgages into CDO’s since Canadian mortgages are either variable rate or short term fixed. (unlike the USA)

So if I had to rate likelyhood of contagion if it blows up:

10% for the wider economy and over 60% for the housing market where most of the property types with subprime mortgages. (Completely arbitrary numbers I picked) ?

This notion that Canada is not like the US — because in the US homeowners can just walk away from their upside-down mortgages, and in Canada they’re on the hook for the difference — is often cited but mostly not true. And this is a real lessons for Canadians.

In the US, of the 50 states, only 12 are “non-recourse” states were homeowners can just walk away, meaning that they will lose the house but will not be responsible for the deficiency.

The remaining 38 states and Washington DC are “full recourse,” and the bank can get a “deficiency judgment” and try to recoup the mortgage debt beyond the value of the collateral. Some of the states that had the biggest mortgage blowup, such as Florida, are in this group.

Even in Canada, there are two non-recourse provinces (with some limitations): Alberta and Saskatchewan.

I analyze all this in greater detail here — and everyone who has this misconception should read this (it also lists the 12 lucky non-resource states):

https://wolfstreet.com/2017/04/25/mortgages-u-s-canada-recourse-states-non-recourse-states/

In other words, when there is a massive national mortgage crisis, as there was in the US, and when people have lost their jobs and have no money, banks tend to not go after them because it would be like trying to squeeze blood out of turnip. In the end, if the bank gets too aggressive, the former homeowner can just file for bankruptcy protection. Banks know this. It’s a very costly procedure, and if there are no gains associated with it, banks just drop it. Same in the US as in Canada.

At the time of the early 80’s crash there was a Canadian private mortgage insurer: Insmore.

It was Alberta’s non- recourse law that busted it. The dollar dealers sprang up like weeds. They would assume the underwater mortgage for a dollar, the former owner would walk and the dealer would rent the house for six to 12 months until foreclosure

That’s a very good article!

I’m interested how things turn out.

I guess it’s an impossible subject with lots of possible twists and turns.

If subprime lenders are dumb enough to hand out loans to people who can only pay off the interest and won’t be able to make payments — things could be interesting. (as you mentioned — they can go to a Trustee and try to re-structure their loans for pennies on the dollar for whatever is owed after the property sales or go bankrupt)

If most of the borrowers are semi well off with savings, good primary income/secure employment and home equity — they won’t find it very easy to go bankrupt without some serious pain. (Canadian bankruptcy process / laws aren’t very friendly if you have a high income or other equity)

Though if they are able to deal directly with the lender — they could probably get a better deal reducing/restructuring any leftover mortgage after their “investment” properties are sold at a loss & and if they pay the difference in one large onetime payment. (it’s cheaper for the lender to do this than get lawyers/trustee’s and courts involved)

Either way, it seems like the subprime borrowers are 100% on the hook if these loans start to under perform, and are pretty much segregated from the wider Canadian economy and “prime” mortgages that require banks to qualify their lenders.

I was also reading that CMHC is reviewing their insured mortgage portfolio for mortgages that never actually qualified and requiring the issuing financial institution to buy back the mortgage (link: http://www.cbc.ca/news/business/laurentian-bank-1.4555286 )

So I don’t think there would be any risk of contagion into the wider housing market or some unexpected domino effect into the prime mortgage lending market too.

I suppose if Canada has a recession where a lot of people in Vancouver, Toronto, etc.. lose their jobs for and can’t find new employment — then all bets are off what will happen to the economy/housing markets.

I guess I’m just pessimistic millennial with an almost 6 figure salary who thinks that prices will ever go down enough for the average person to afford a decent sized 2 bedroom in Vancouver without a 35yr mortgage. ;)

“So I don’t think there would be any risk of contagion into the wider housing market or some unexpected domino effect into the prime mortgage lending market too.

I suppose if Canada has a recession where a lot of people in Vancouver, Toronto, etc.. lose their jobs for and can’t find new employment — then all bets are off what will happen to the economy/housing markets.”

Thoughtful comment, but I think you are underestimating the risk of contagion – the percentage of GDP devoted to residential construction is enormous, then throw in home renovation & maintenance, realtors, lawyers, brokers, furniture stores, the wealth effect on people’s spending as they feel poorer, the oversized Canadian financial sector and the huge percentage of everyone’s retirement funds that their stocks make up, the hit to government finance (provincial property transfer tax revenue), local governments funded by developer fees, etc.), people unable to move for a new job because they are underwater, it just goes on and on.

Throw in China decelerating, Trump’s trade war madness, the unstable Euro situation, growing emerging market chaos and tightening at the FED and ECB and you have an external environment with a lot more downside than upside as well.

No issues then. The lesson is the same. If you are going to be a problem, make sure that it’s a HUGE problem, then you’ll be getting a “bail out”.

Indeed!

First of all, Thank You Wolf for such an excellent definition on sub-prime and private lenders, etc.

It’s been around for a long time, though. I remember my dad 40 years ago ‘buying/carrying’ mortgages for buyers. He was always paid back just fine. He didn’t charge more, but his return beat the savings rate…..in other words he earned the same spread the institutions did. Mind you, he obviously didn’t borrow money to do it, either. He was sitting on it.

As I read your explanation I asked myself, “Why is this a problem”? Plus, it isn’t a Canadian problem if Toronto based lending and buying speculators over extend themselves. They will be a nice reminder for folks about how Canadians used to behave and should conduct themselves. Greed greed greed has a downside. Personally, I could care less if these folks go over a cliff of their own making.

Anyway, I am one of the traditionally minded Canucks with no debt and some cash in the bank. It’s how I was brought up, I guess. I’m still waiting to pick up another neighbourhood property, one that I can keep an eye on. :-)

This winter or next spring you will be in for a treat. All the housing availability and no one left to out bid you. It will be a buyers paradise in B.C. by next spring if the Chinese and Canadian joint effort works out.

Prairies,

I agree, especially if the mobsters all decide to pull out at the same time: read How Chinese gangs are laundering drug money through Vancouver real estate (https://globalnews.ca/news/4149818/vancouver-cautionary-tale-money-laundering-drugs/)

Add to this the fact that the previous provincial government was pretty much “in on the action” in BC and you’re going to see some fire sales.

Beavis and Butthead Do Canada Real Estate.

Uh… yeah …. I’ll buy that. Shut up Butthead, I can use that house to score.

Beavis and Butthead would never buy Canadian real estate because Canada is where Brian Adams comes from.

The Real Tony,

“…Oakville would be number one on the list as the most overpriced city in the GTA.” Now just wait a minute Real Tony, I live in Oakville, I like it, it has paved roads and sidewalks, pretty much all new infrastructure, good parks, reasonable taxes, and. . ., oh, never mind, doesn’t apply to me–I rent :-)

It’s frankly amazing just how much prejudice you can cram into a few words. Chinaman, immigrants, millenials and welfare. That’s just where I stopped counting. I wonder why economics blogs are so attractive to people like you? Does the connection to money somehow paint a veneer of steely realism over your shallow prejudices?

His views mirror what our newspapers have been saying for years in Canada, no one wants to believe that locals obsessed with real estate caused this bubble. It’s only in the last 6 months have the media stopped blaming foreign investment from China for the housing bubble, but they do still blame immigrants.

https://www.macleans.ca/economy/economicanalysis/chinese-real-estate-investors-are-reshaping-the-market/

https://www.huffingtonpost.ca/gabriel-yiu/canada-housing-crisis_b_14047186.html

http://vancouversun.com/opinion/columnists/douglas-todd-canadas-immigration-targets-a-form-of-housing-policy-says-study

https://www.ctvnews.ca/canada/wealthy-ghost-immigrants-using-empty-homes-to-claim-citizenship-tax-expert-1.3779906

https://www.macleans.ca/opinion/how-to-fix-canadas-ghost-immigrant-fraud-problem/

SimplyPut7 – “…no one wants to believe that locals obsessed with real estate caused this bubble.”

Not so fast. Locals may have jumped in at the middle or end, but they weren’t the ones who started the run-up in prices. Chinese money did that, aided and abetted by our own government. Canada was up for sale, and a lot of corrupt money ended up buying and pushing up prices.

Once this happened, yes, the locals did get involved, some out of fear of being priced out forever (as every shyster realtor was telling them) and some riding the speculation train.

But to say that “locals caused this bubble” is absolutely ridiculous.

This bubble was engineered and manufactured by politicians and their campaign contributors (the real estate/developer lobbies). Everything that could have been thrown at this bubble was thrown at it.

Canada – one big Ponzi scheme!

Re: backwardsevolution

Foreigners are not obsessed with all of Canada, just like Canadians buying real estate in the US are not obsessed with all of the US.

Bad government policies along with the media and real estate boards and financially illiterate people fueled the Canadian housing bubble.

Let’s pick on British Columbia (BC), the population of BC is only 4.650 million people, the area of Vancouver only has 650,000 people the greater Vancouver area has 2.463 million out of the 4.650 million people in BC.

Below are some size comparisons of how big BC is:

http://www.bcrobyn.com/wp-content/uploads/2012/12/CaliforniaMap1.jpg

http://www.bcrobyn.com/wp-content/uploads/2012/12/UKMap1.jpg

Could the government not build cheap houses in the outer areas of Vancouver? Does everyone really need to live in one or two cities in BC?

Let’s say foreigners make up to 20% of the BC real estate market if BC wanted to let lots of Chinese people buy homes, why wouldn’t they be more like Florida and Arizona which allow lots of Canadians to buy houses and condos which are left empty 6 months of the year, and make sure there is lots of supply for local people as well as foreign investors.

Increasing supply would also weed out the speculators, as people looking for fast gains and steep increases in housing prices would go other cities around the world, where they can make a better return on their investment.

I don’t think Chinese investment in Canada is 20% in Vancouver or Toronto, I think it’s a lot less, which means locals will struggle as interest rates rise, as our mortgage rates reset every 5 years, or sooner for people with mortgage coming up for renewal or have variable mortgages that rise with rising interest rates.

The Chinese people I have met were students who came to Canada to go to university and now they work and rent. They don’t have a long-term plan to stay in Toronto or Vancouver. They came here to get an education and as soon as the economy starts to turn they will be off to the next country or go back home to China.

Canada in larger cities like Vancouver and Toronto have lots of Canadian-Chinese people. They pay income tax in Canada and have no plans to go back to China. Like most Canadians in Canada, they also did not get involved in the housing frenzy in Vancouver and Toronto.

The speculators, flippers and subprime lenders (syndicated mortgage investors) I have met or not Chinese. They are locals who believed there is an investor from China coming to rescue them from their debt as interest rates rise. The problem with that is rich investors don’t like their money tied up in assets that become harder to sell as a housing market slows down.

‘When you raise money from investors they want meteoric growth. They don’t want a small, profitable business. They want to get a steep profit out of it. That’s why they’re investing’

https://www.thestar.com/business/real_estate/2018/06/15/online-brokerage-theredpin-closes-its-doors.html

And then there’s the Irish and Italians. Why can’t we all just be good Dutch?

That last sentence is a quote from an older relative of mine some years back. Lol.

PIGL – I often wonder how the Chinese would have reacted had the Canadians or Americans gone into Shanghai, for instance, and started buying up everything that moved, pricing out the locals. And then when Shanghai was all jacked up, let’s just pretend that these foreigners then moved on to all the other major cities and bought them out too.

Of course, that’s silly, isn’t it, because, first, the Chinese people would never have allowed foreigners to price them out (their leaders would have been swinging from lamp posts if they tried it) and, second, the Chinese people would never allow a bunch of foreigners in their country to begin with.

backwardsevolution, actually, the Chinese did let foreigners into major coastal cities and it precipitated the Boxer Rebellion. And let’s not forget the colonization of Hong Kong by the British and Macao by the Portuguese. The Chinese have long memories of both.

Regarding their recent activity in Canada and IOUSA, I tend to believe that the 20% of total real estate purchases Asian buyers are alleged to have made is probably low in Hongcouver and Toronto. It was well over that number in California in 2015-2017, albeit, their activity has dissipated since China and Vietnam enacted tighter capital controls.

Look on the bright side: the IOUs that IOUSA and Canada have been wracking up for the past century via national deficits financed with Fed and BoC funny money are now being redeemed. They can’t be redeemed in gold – Nixon put an end to that in 1971 and Canada sold off all of its gold – and control of resource industries is frowned upon in both countries. So, what’s left? Trophy real estate in major cities, and housing in attractive coastal cities, which are also a “get out of jail free card” when things implode in China. And best of all, it can be done with little pain to the public, albeit, some prospective buyers will rent for the foreseeable future.

Bottom line, Asian money is as green as yours or mine, their buyers take a long view of markets (as opposed to many NA natives who’d prefer to speculate) and in the HOAs I’m familiar with in Orange County, most Asian buyers paid cash, and didn’t have to worry about a financial crisis. And, they place a floor under prices that overextended IOUSA and Canadian buyers should be thankful for.

So… Condo owners might get in trouble? That would be hilarious if it wouldn’t help to sink Canada’s economy when the bubble crashes.

I’ve already read this piece twice.

Great information, please keep it coming.

Great article to the author, you’re right on and very smart….the canadian RE market, along with the US RE market, is all built on debt, aka, a house of cards and bigger fool theory. Not to mention their entire economies. Just like Amazon that has 3-4 quarters of profit in 20 years yet the stock is about 100 times PE ratio. Not sure when the damn will break, 1-5 years out, but get your boat and life jackets ready now because the “crash wave” will be big. Car loans, student loans, credit card debt, mortgage debt, unfunded public pensions, unfunded social security, unfunded Medicare/Medicaid, over valued stock market, wages at half the pace of property appreciation, property tax write off capped at $10,000 now, rising interest rates, geopolitical tensions, rising oil prices, birth rate decline eroding future tax and entitlement revenue, inflation, private mortgage lending accelerating due to big bank caution, property tax increases, bloaded governments & debts/deficits, State debt/deficits, municipal debt/deficits, county debt/deficits, sky high health care costs, college tuitions out of control…should I go on? All or any combination of these will be the catalist(s) for the next depression that will make the last great recession look like the “Roaring Twenties”!!! Again, not sure exactly when it will happen, could be 2 or twenty years out, but mark my words and run for cover and start to save, save, save for your emergency fund right now, it’s going to be ugly folks!!!

I agree that this is not a time to be in debt. At least some of your savings should be in physical gold and silver, given that the value of fiat currencies is being eroded. PMs should be kept where only you can get your hands on them.

2 or 20 years…that is a good prediction, eventually we are all dead in the end, that is certain so what good will your savings be? I would say go out and enjoy life, it is such a miracle, and quit worring about anything that could go wrong.

I think Amazon PE is over 200

Very interested to know the funding structure of those private lenders. Do they securitize? For the balance sheet lenders, how much do they leverage? Who own their equities? Who lend to them? Who buys their CDOs?

Thank you for posting this information about the “sub-prime” AKA “private loan” in Canada especially in the so-called “healthy” Toronto condo market.

I’m glad that the Toronto real estate market has been in the start of collapsing in prices and sale volumes for the past one year.

I anticipate that the sale prices will be reduced to about half or 50-60% from their peaks in April 2017 in the next couple years or even sooner when the bubble will be fully bursted.

I am sorry for perhaps hundreds of thousands of the so-called “middle class investigators” who will be hurt financially from their speculation and home flipping practices. However, I will be very happy for people who are looking to buy an affordable home to see the prices will drop in half or little more in the next few years.