Average price of single-family house plunges 13%, or by C$160,000 from peak. Sales of homes priced over C$1.5 million collapse by 63%. Condos still hanging on.

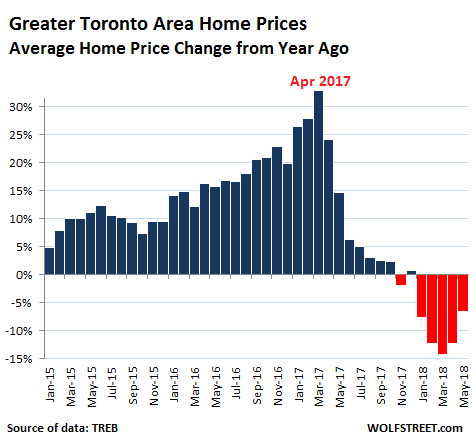

Housing in the Greater Toronto Area is, let’s say, retrenching. Canada’s largest housing market has seen an enormous two-decade surge in prices that culminated in utter craziness in April 2017, when the Home Price Index had skyrocketed 32% from a year earlier. But now the hangover has set in and the bubble isn’t fun anymore.

Home sales plunged 22% in May compared to a year ago, to 7,834 homes, according to the Toronto Real Estate Board (TREB). It affected all types of homes, even the once red-hot condos:

- Detached houses -28.5%

- Semi-detached houses -29.4%

- Townhouses -13.4%

- Condos -15.5%.

It was particularly unpleasant at the higher end: Sales of homes costing C$1.5 million or more plummeted by 46% year-over-year to 508 homes in May 2018, according to TREB data. Compared to the April 2017 peak of 1,362 sales in that price range, sales in May collapsed by 63%.

But it’s not just at the high end. At the low end too. In May, sales of homes below C$500,000 – about 68% of them were condos – fell by 36% year-over-year to 5,253 homes.

The TREB publishes two types of prices – the average price and its proprietary MLS Home Price Index based on a “composite benchmark home.” Both fell in May compared to a year ago.

The average price in May for the Greater Toronto Area (GTA) fell 6.6% year-over-year to C$805,320, and is now down 12.3%, or an ear-ringing C$113,000, from the crazy peak in April 2017.

There are no perfect measures of home prices in a market. Each has its own drawbacks. Average home prices can be impacted by the mix and by a few large outliers – but over the longer term, it gives a good impression of the direction. The chart below shows the percentage change in average home prices in the GTA compared to a year earlier:

Detached houses – generally representing the higher end – got hit the hardest:

- Detached houses: -8.2% yoy to C$1,045,533, and down 13.3% from the peak in April 2017 ($1,205,262).

- Semi-detached houses: -1.2% yoy to C$815,803, and down 3.5% from the peak in April 2017.

- Townhouses: -2.5% yoy to C$640,543, and down 8.7% from the peak in April 2017.

- Condos: +5.7% yoy to C$562,892, and up 4% from April 2017

The TREB’s proprietary Home Price Index is based on a “composite benchmark home” and strips out the impact of changes in mix and large outliers that may afflict the average price. And the HPI Composite Benchmark fell by 5.4% year-over-year.

All home types except condos experienced year-over-year price declines in the HPI, with detached homes also getting hit the hardest:

- Detached houses: -10.2%

- Semi-detached houses: -8.5%

- Townhouses: -4.3%

- Condos: +8.3%

The inventory of homes for sale rose by 13.2% in May compared to a year ago, to 20,919 active listings. At the rate of sales in May, this worked out to a supply of 2.7 months, up from 2.3 months in April and from 2.1 months in March. The average days-on-the-market before the home was sold or before the listing was pulled without sale jumped to 20 days in May from 11 days a year ago.

With some irony, the TREB cited a survey, conducted between May 18 and May 22 in the GTA, that found that concerns about “affordability” — surprise, surprise! — ranked high among a lot of people:

Among 9 listed issues (health care, government spending/balancing budget, taxes, housing affordability, energy costs, economy, transportation/traffic, environment/climate change, enhancing social programs), 25% of GTA residents rank housing affordability in their top two most-important issues for the Ontario election campaign;

69% agree (35% strongly/34% somewhat) that a party’s platform on housing affordability will influence who they vote for on election day.

The irony is that “housing affordability” is fundamentally impacted by prices and interest rates. Interest rates have come up a tiny bit from historic lows and remain historically low. But prices have surged for two decades. What will make the Toronto housing market more affordable for many people would be a substantial decline in prices. So if the TREB wants to enhance housing affordability for folks in Toronto, it should advocate for policies that will bring down home prices – of the kind that the government has been implementing – and not advocate against them. But advocating against them is precisely what the TREB, as real estate lobbying group, has been doing with a passion for a year.

Chicago’s rents are in free-fall, Washington DC’s rent suddenly plunge, New York’s rents fall to third place. But rents soar in Southern California and other parts. Bay Area and Seattle are “mixed.” Read… Update on the Splendid Rental Bubbles & Crashes in the US

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I would like to see a full analysis. Not once did you mention wages. It is the third element ( asset price, interest rates ) affecting affordability. Take a look at the movement of real wages over the two decade period you mention. See?

Sigh they should “advocate for policies to bring down home prices” Seriously this is your recommendation? From a described (yours) lobby group? Really?

How about getting the policy makers (ie govts) to deal with wage stagnation?

Also your analysis of ” Toronto” real estate price trends should either say GTA price trends or break it out into Old Toronto, York etc.– you interchange stats between GTA and Toronto like its the same thing. Nope it isnt! Ask anyone in Vaughn trying to sell a house. And then ask the two houses on my street (Old Toronto) that just sold for over list ( $2.2 m)

Wages are a different topic and are treated separately. One topic at a time.

All data in this article are for the GTA, as you can see from the multiple uses of the phrases “Greater Toronto Area” and “GTA.” Nothing in this article is treating the GTA and the city of Toronto as the same thing.

Getting a little nervous about the price of your home? Asset bubbles don’t last. Everyone knows that.

He’s from Toronto, this comment is what Canadians have to deal with. Don’t blame the bubble(problem). Just fix it buy paying us more to gamble(invest in real estate). People don’t need more money, it would be nice though. What people need is less debt, but inflation in expenses always out paces inflation in wages. If we give you Ontarians more money you are just going to inflate the bubble higher, so no. No more money. Go to bed and think about what you did.

There’s virtually no jobs in the entire greater Toronto area and it has been that way since 1980. Wages will always lag when the job market is this slack. If the Chinese stop buying homes house prices will implode.

We live in a province that has a massive accumulated debt. We pay out just over C$1 billion per month in interest alone: https://www.ofina.on.ca/borrowing_debt/debt.htm –(it’s C$12,543 million per year on the chart, and it’s only going to go up).

We have a provincial election coming up this Thursday. The leftists that created this ripoff are hopefully going to get the boot, but that’s not certain.

in every area of life that is relatively free from government interference, price of goods fall down to average common denominator.

price of clothes, price of cars, computers, food …

problems are not wages, problems are government regulation for buildings, manipulations to interest rate and manipulation of immigration.

no free market in housing that is a problem.

in free market wages would be stable or falling little — because price of goods will be falling faster.

I live in Sydney Australia.

my parents bought 2 bedroom unit in 1999 for $150 000 australian dollars.

price was 5 times his wage gross which was average worker income at that time.

today apparently people are willing to pay $600 000 — $700 000 Average

( good luck to them, I am renting )

Australian Yearly Wage: $60,892.

You Aussies and Canadians are actually lucky, though you don’t know that.

I read the article and some comments, and if I didn’t laugh then I would have cried because basically comments about real estate in Israel look exactly the same!

However here it turned so so crazy that an average apartment (4 rooms about 85 msq) takes over 150 salaries bruto, around 220 salaries neto, and that calculation doesn’t refer to the extra sum of the mortgage interest.

So, I know it awful but I would love to see 100 salaries for a fucken condo here! It would be a dream!

Very few homes in Vaughan sell for over $2 million, those stories used to work in a hot market. Only 3- 5 homes sell for over $2 million weekly out of 200+ homes trying to sell for $1.9 million or more. Vaughan only sells that many over $2 million a week because of the perceived equity in the homes that were sold, most of the people who live in these homes only have family incomes of 100k-200k as shown on realtor.ca

Very few homes in Vaughan sell for over $1.5 million as B20 now forces lenders to verify income and prove people can afford payments at higher interest rates. The number of homes selling over $1.5 million will continue to decrease as interest rates rise.

Most speculators and flippers who need to sell are surviving on their credit lines, but as rates rise they can only do that for a limited period of time before their lenders come after them for the outstanding loan amount.

I am not quite sure why you are happy to see families making gross incomes of 100k – 200k having mortgages of 800k or more. Those mortgage payments will become more difficult to make in a rising interest rate environment.

The market is slow now and may not recover for years even if the speculation tax is removed in Ontario as there are too many local speculators who needed the high prices from 2017 to break-even compared to the number of foreign speculators who still have an interest in hiding money in Canadian real estate, now that the government is going after tax evaders.

In the first place, profound average wage suppression is a feature of late-stage globalised capitalism.

It is a policy aim and will not be amended.

In the second, it is a feature of an economic system and civilisation in (slow, but steady) collapse mode.

There is nothing at all surprising in any of this, and everyone would be well advised to modify their expectations and decisions accordingly.

Happy endings will not abound: better to toughen up to face grim reality with endurance and determination…..

Agreed. Those who have implemented Chicago/Virginia school economics will not see any sustainable growth (ie economic growth which is not predicated on cheap credit and usurious lending practices) to speak of as they have exported – gleefully – their volume manufacturing base to low-wage economies in search of short-term stockholder returns.

Hence the disappearance of their middle class, and takeover of their countries by the finance sector which has done what the finance sector does – saturated these countries with debt, slowly choking the life out of them.

I grew up in Ontario and have been hearing people in ‘GTA’ boast about their home investments for the last two decades. Unfortunately, the commentor sounds rather bitter at what can only be described as an end to an era in Canadian housing. Between NAFTA negotiations, a trade war with the US, cyclical oil prices, personal debt and stagflation, there are huge headwinds against the Canadian economy that will keep growth and wages depressed for many years to come. Policy changes by the Ontario government such as the 15% foreign home ownership tax will drive away the Chinese, arguably the last thing that is keeping GTA home prices from sinking much further.

Cheap credit turns every reckless chump who lacks the capacity for critical thinking into a financial genius, a guaranteed winner.

Politicos love this because it’s such an easy way to get re-elected. No hard decisions need be made; no industrial strategy necessary. Just cheap loans.

The problem comes for a country once the train hits the buffers, and ‘prosperity’ can no longer be achieved via hordes of amateur gamblers/speculators.

That’s the tricky bit. Japan hasn’t solved that conundrum 30 years on, even though it has a solid industrial base to build on. Much more so than, for instance, the countries that have had Mark Carney as a central bank chief.

Yes, afford-ability is a function of real wages. But to Wolf’s defense, real wages have been eroded by unrealistic low interest rates which have pushed the cost of living and all asset prices upwards beyond afford-ability.

It will get more interesting if the economy turns and mortgage defaults start to show up.

That’s great news! I was hoping to move somewhere that’s even COLDER than where I currently live!

Wolf, As home prices in Vancouver and Toronto decline, do you think shorting the major Canadian banks is a good play? If I shorted them, I would buy long dated, way out of the money puts. I’m thinking mid 2020 puts that are 30% out of the money.

People have been carried out on stretchers after shorting Canadian banks. Fundamentals do not apply in these crazy markets. That’s why I don’t short anything anymore.

If you have a big megaphone, and you can make a stock fall by announcing that you’re shorting it, then it works. But for retail investors, shorting can be a thankless and hazardous activity.

Luck helps a lot, but luck is not a strategy :-]

And remember, RE markets move at snail’s pace. Movements are measured in years not days or weeks. So that’s going to impact your decision about the time horizon.

But if you protect your downside, as you’re suggesting you will, and your horizon is long enough, it might be a fun thing to do.

to Timothy J McLean

These markets are saturated with debt and leverage which should be avoided by any risk averse investor or speculator.

Shorting means borrowing and invariably involves leverage. Beware.

The stock market today is more overvalued than just before the 1929 stock market crash. America is too big for a full scale dollar devaluation. The only thing that could go wrong is helicopter money. The stock market indexes of today would have to drop 80 percent just to revert to the long term mean. If you have enough money to hold out short them and buy deep out of the money puts on the major indexes monthly starting around the middle of 2020. The next crash should eclipse all previous crashes. Remember Brampton and Mississauga were created with welfare cheques back when zero down and a forty year mortgage were possible.

Go as far “out of the money” as possible if there’s any trading volume. Aim to make one hundred times your money or more. 30 percent out of the money is a waste of money, not far enough out of the money.

Also reported today :

Vancouver sales volume dropped 35% from May 2017 as Prices are up 11.5% versus May 2017.

Prices follow volume ? Always or just sometimes ?

Read that detached sales in Vancouver in May were the lowest since 1991 … that is a long time ago…

When prices follow volume, they do it with a lag.

Sorry. detached sales in Richmond (Chinese suburb of Vancouver), not Vancouver as a whole – but still.

Who cares? The NDP are in British Columbia now and that will scare off all the Chinese. Also a tax agreement between Canada and China will come into effect this September to catch ALL the tax evaders who bought Vancouver and Victoria real estate.

The Real Tony,

“…tax agreement between Canada and China will come into effect this September to catch ALL the tax evaders who bought Vancouver and Victoria real estate” –really? I don’t think those Macau mobsters care about Cdn tax laws so they’re all gone along with whatever cap gains they’ve made.

I think the importance of linking tax information between China and Canada is that China can now track which chinese has been moving money abroad to invest oversea, as China tries to rein in capital outflow.

Completely absent are the multiple factors driving housing prices down.

An outlyer would be the coming effects from the demise of NAFTA! Nobody in Canada has yet figured out that blinded leftests Trudope and Freeloader have killed NAFTA!

Wait until this new reality sinks in! I suspect there will be much less Chinese money willing to invest in Canadian real estate going forward!

I must say, the use of ‘Trudope’ and a multiple exclamation points give this comment a very high coherence quotient.

Thanks. Slipped through. Now tripwired :-]

If the NDP wins the election this Thursday in Ontario no Chinese money will be coming into Canada.

The slow changing of the mental understanding of what the heck a home is, began about the same time as the beginning of the decline in interest rates (right about the time that Long Term Capital Management bit the dust in the USA and our FED went to work) and the conversation that, like the stock market, the value of a home had no ceiling as the rates dropped. The home, became another investment. Invest NOW, it is low tide…I heard that so many times, that I wondered want shoreline was being sold. Turned out to be everywhere, and everything…homes, stocks, art, jewelry, cars, etc.

You only hear about the decline in ‘assets’ when it is to late. Check out art and cars and jewelry, high end goods, and you will see this began about a years ago or so, but is now spreading out. When you hear it on CNN, you will know it is to late to sell anything. The ‘smart money’ is in a hurry to get there…into CASH, just ask Goldman’s guys.

I only know two high wealth people. Both bought a lot of stuff 2009 to 2014 and then sold off 2015 to present and are now don’t own anything they aren’t actively using or attached to. I think their main motivation isn’t that prices will fall but that there isn’t much upside left. Though one comment was, liquid assets you can make money in a falling market if there is enough volatility. Not really true of real estate.

Rigged. Sad!

OT: From that articles on China the other day – the USA is going down the same road:

https://biglawbusiness.com/homeland-security-to-compile-database-of-journalists-bloggers/

We are all going to be ‘famous’.

I watched the RBC Chief Economist give an “upbeat” talk on housing to the Manitoba Board Of Trade last month. He used terms like “a more balanced market” as opposed to a sellers market.

His voice would almost tremble from time to time as he kept a straight face. The guy was good.

I think that he may use the term “soft landing” in his next presentation to them.

It reminds me of the times i spent listening to Dublin economists waxing lyrical about housing in the summer of 2007. Stamp duty ! Oh, that wretched culprit. Same spiel, different location.

Something may make the market react differently this time* that nobody is talking about. There is fairly high immigration and that makes more people chasing the more or less same amount of houses and condos.

The shortage drives prices up even if wages stay constant.

With the traffic congestion in the GTA moving out to the country is not a good option either.

* I know that this are the most dangerous words in investing

Realtors need closed transactions to make a living.

If prices go up, or down it doesn’t matter much as long as you can close deals.

It’s just a gully. That’s all. Just nerves.

My wife’s grandmother once asked, “Have people always lived on Vancouver Island, here, in Saltair? Her son-in-law answered, “Yes, in fact Victoria was established long before Vancouver. It wasn’t until the railroad came that Vancouver was developed into anything more than a collection of shacks”. She thought hard for awhile then asked, “Then why the hell did we ever live in Prince Rupert”?

Fast forward to the late ’60s. My two aunts decided to move out of Toronto to Vancouver and were going to rent an apartment. My Dad talked them out of renting, and fronted them a down payment for a nice little bungalow on 4th and Sasamet. It had a view of the Bay and the North Shore; a good view. They paid $27,000 for it and then asked a similar question. “Why did we ever live in Toronto if Vancouver was here the way it is”?

Sometimes, there are no easy answers. They ended up selling the house and retired in Whiterock. The buyer was a lawyer, and just wanted the lot. Down went the house and up went a trendy box. I think that abomination has also been torn down and replaced this last surge/bubble.

Provincial election in Ontario on the 7th. Wow, the choices for a new leader are astoundingly bad.Hydro privatized by the Libs, paying some producers over 80 cents per Kwh for intemittant solar. Electricity bills have skyrocketed for ratepayers…sometimes in excess of $1,000/month. Gas is expensive, housing unaffordable, the climate sucks year round, crowds everywhere, bugs, and the Leafs still disappoint, just like the Canucks. No wonder housing prices are collapsing.

Anywhere would be better, even Prince Rupert.

Couldn’t have said it better myself. Never thought I’d say this but I’m thinking of leaving Ontario. Quebec is 30 minutes away.

The effects are showing up already. In Sydney, house prices slid 3.4 per cent year-on-year in April. In more exclusive suburbs, the falls are as deep as 10 per cent, according to Business Insider. The share of houses sold at auction last weekend is heading toward the 50 per cent levels typically considered to herald a downturn, according to the Australian Financial Review.

That, rather than bad publicity and headline-grabbing fines, is the real reason Australia’s great banking boom is over. The housing phenomenon that’s sustained profits for a generation is sputtering out, and with interest rates on the country’s hefty household debt piles forecast to start rising toward the end of this year, the worst may be yet to come.

Very true. Stagnation and decline in the high-end art market started a couple of years ago: that’s exactly why they made so much fuss about the silly ‘Da Vinci’ sale – camouflage.

What most experts don’t mention is the fact that most of the price decline was in suburbs. Toronto itself was not really impacted – in fact, prices in downtown continue to climb.

Wishful thinking or propaganda? Well, BS at any rate. The average price in the City of Toronto in May ($861,970) was down 4.2% from a year ago ($899,980) and was down 8.6% from the peak in April 2017 ($942,677).

Well, try to buy a new condo in downtown Toronto and compare the price to a year ago. You could buy a good project a year ago for $900/sqft. Today $1,000/sqft is considered a bargain.

Propaganda? Not really. Just facts.

If you had read the article, or even just the subtitle, you would know that condo prices are up from a year ago. That’s the only exception. Prices of all other dwelling types are down, and the combined total is down too. So do try to read the articles before you post.

Prices are climbing like the Blue Jays are going to make the playoffs.

What about health of folks using home credit lines as ATM or private lending? These people are extremely sensitive and vulnerable to any drop in home prices, a parallel to what happened in US 2007/2008. If these people are forced to sell then prices will only spiral earthwards.

I’ve been waiting for years for prices to collapse in Toronto. For a decade and a half Torontonians have consistently been an arrogant bunch. Reaping the rewards of a huge housing bubble while the rest of the Canadian economy stagnates. Well done tracking the Tornoto housing bubble phenomenon over the years; it been a really long drawn out affair.

lol keep dreaming Wolf! Advocate for the suppression and reduction of home prices? You do realize this is Toronto you’re speaking about and not Windsor, Ottawa, or Timmins Ontario right? lol. Your entitlement mentality does not work in a city like Toronto. Nobody is entitled to cheap housing – it’s like saying “hey guys I don’t like the prices of these new Mercedes, Lexus or BMWs, let’s protest and get the prices down so that EVERYBODY gets to drive one!” Life my friend does not work like that. There are cities that are expensive and there are cities that are cheaper. Believe it or not there are many people who can afford expensive homes. So just because you can’t or the “average” person can’t doesn’t mean you should advocate for policy creation to manipulate the housing market to suit your desire for a cheap home. Remember we live in a free market – if anyone wants a socialist form of government where the apple pie is divided equally across the table then move to a country that adopts such political principals. Free markets and democracy rein supreme and this talk of overly regulating housing wreaks of socialist mindsets!

You’re being silly, and you know it. Please read the last part of the article again. You will find that it’s the TREB — not me — that is advocating for policies to enhance “affordability.”

What I pointed out was the IRONY in the TREB’s statement.

I also clarified what exactly would increase this TREB-desired affordability: lower prices and/or lower rates. But rates are headed up. Leaves the first. Doesn’t take a genius to figure this out.

I’m just trying help the TREB think through this logically :-]

BTW, for you own edification, I live in San Francisco, whose home prices far outpace those in Toronto. I love Canada, but I have no intention of moving there for now. So I don’t have any skin in the game in Toronto. Just looking at the data.

I wouldn’t have even gave him a response Wolf. The attitude smells of someone defensive of any reports that reflect negatively on someones own investments. Possibly bought property in Toronto and is feeling the pressure as the investment deflates in front of them.

I remember years ago reading advice on buying real estate for rental property. It stated that you should make 8-10% on your investment from the yearly rental income , try that on a $1.5 m detached crack shack in Vancouver. This rule is obviously long been destroyed (did that ever exist?)

My concern is the debt my children have been saddled with (which includes everything not just housing) . I have warned them but none of them have ever lived a real estate correction/crash.

Remember when you could buy a house for buck if you would just take over the mortgage ?

History often does repeat. (sadly)

debtfree,

“My concern is the debt my children have been saddled with (which includes everything not just housing) . I have warned them but none of them have ever lived a real estate correction/crash.”

If they work for the public sector, then they’re set for life; they won a small lottery; they have a meal ticket for life.

But if they work in the private sector, that could be a problem. Do you have a big enough basement? Trade problems and the fact that employers like to shed people as they get in to their mid to late 40s and beyond. And with automation looming, look out.

Thank you very much for sharing this fact of the declining real estate market in the GTA both in sale volume and prices. I have moved to this city for a new job almost a year ago and have had no desire to buy any home in the GTA. I’ve seen homes in the GTA are listing for over one million CAD which to me they are very regular homes and nothing special and are probably listing around $400-$500K elsewhere in Canada.

I’m currently renting a room in Scarborough for $530 a month all inclusive with a covered parking spot. So I’m very happy at where I am at in term of living expenses.

I work from home most of the time so I have no need to be in downtown Toronto for work or school. I may go to the office perhaps once every couple weeks or even a month and many people in my company are also working from home. So the close proximity to the downtown Toronto doesn’t attract me and perhaps other people who are working from home. I believe that working remotely from home now has become a norm in the new economy so less and less people want to live and buy a home in or near the city.

So after the house prices will collapse in the next couple years from the one million range to about $400-$500K, then I may buy one detached home in the GTA. Otherwise, I have no interest in buying a home in the GTA.

Good luck all of the current home owners in the GTA who are banking their wealth and perhaps retirement funding in their home ownership which may not work in their ways.

A lot of people commented that the influx of immigrants drive up the demands of housing and home prices. I am myself an immigrant to Canada and GTA. I also have known many of other immigrants in the GTA. None of us who immigrated to GTA recently and in the past five years buys any home in the GTA. So the comments that immigrants in GTA drive up the demand and home prices is not true.

The reasons that the recent immigrants in the past five years are all renting and not buying any home in the GTA are that the home prices in the GTA are not affordable. Also, most of the recent immigrants cannot get the jobs which they were trained for in their countries and even after they arrived in Canada. So most of them end up working in the jobs which pay a couple dollars above the minimum wage such as cooks and servers in the ethics restaurants, janitor which is now called housekeeper and other labour intensive jobs such as fast food workers. So the recent immigrants within the past five years have no purchasing power to buy a home in the GTA from the incomes of their current jobs.

Of course, the immigrants to GTA for fifteen or more years ago may have capabilities to buy a home in the GTA because the home prices were still affordable back then.