The Fed has left the room.

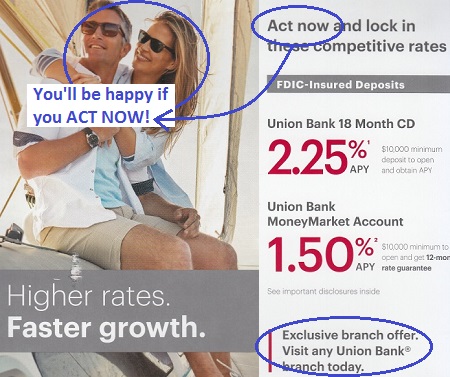

Now banks are sending me expensive fliers in the mail, offering higher rates on deposits, trying to attract my money. This goes way beyond the fliers I’ve been getting for years that offer a one-time bonus for putting a big chunk of money into an account that earns no interest. The photo below is part of a three-section glossy cardboard foldout that I got in the mail. It says that these rates are exclusively available at the local branch. To get this deal, I’d have to go there so they can stare into the whites of my eyes.

“Act now and lock in these competitive rates,” it says. I added the blue marks:

Union Bank, which is offering this, is not huge, with a little over $110 billion in assets. But it’s a storied San Francisco bank founded just after the Gold Rush. It still counts as a local bank, but it’s now owned by Japanese mega-bank Mitsubishi UFJ Financial Group.

It started late last year when I began noticing things. At first, I ran into it accidentally. Some banks were offering higher interest rates on CDs but only through brokers. At first, it was just a few banks, and rates were still low. Then there were more banks offering CDs at higher and higher rates. The other day, I found that Wells Fargo was offering the highest rates for these “brokered CDs,” for example a 13-month 2.25% CD. At the same time, it offered its existing clients near-zero rates.

Wells Fargo, Citibank, Bank of America, Morgan Stanley, and others want to reel in new money, and are willing to pay top dollars for this new money, in competition with other banks, but aren’t willing to raise interest rates for existing customers. Other banks, including American Express Bank and Goldman Sachs’ new consumer bank, Marcus, are offering higher rates to new and existing customers alike.

American Banker weighed in on this topic in its May edition, with an article titled, “The Battle for Deposits Intensifies.” The trade paper has been on top of this trend since late last year, including a video posted on November 2, titled, “‘No question’ the war for deposits is on.”

In its current article, American Banker explains the strategies used by “big banks” to fight this battle the smart way – with Big Data – “ahead of what could be as many as four Federal Reserve rate hikes this year,” without ruining their fat margins and profits.

Over the past two quarters, at least two of the nation’s biggest banks – Wells Fargo and Bank of America – have tinkered with the way they set deposit rates, carving up a handful of key states into smaller markets…. The move will let the two banks more efficiently counter attempts by small banks and credit unions to lure customers away with deposit promotions [such as the one pictured above].

Other banks, meanwhile, are exploring new ways to use data and analytics to adjust rates for lucrative customer segments. For instance, some are offering promotions to affluent millennials who may be tempted to open higher-yielding accounts at online banks, observers said.

Taken together, the moves illustrate how the industry’s biggest players are becoming more precise and tech-savvy on setting deposit rates – and how they plan to respond once the federal funds rate rises enough to spur more intense competition for consumer deposits.

Interest rates offered by banks are on average still extremely low, including those offered by many banks to their current customers, even if the same banks offer much better deals on “brokered CDs” to attract new deposits. And that’s a good thing for profit margins and earnings.

A report by Fitch, cited by the American Banker, estimated if the eight systemically important banks in the US paid their existing depositors an average of only 75 basis points (0.75 percentage points) more on their retail savings accounts, the eight banks’ combined pretax income would drop by 11%.

The percentages may be small, but the amounts are gigantic: There are over $9 trillion in savings deposits at banks and credit unions in the US.

So competition to raise rates is to be avoided. But the Fed – after nine years of controlling the market by lining banks up all in one row behind near-zero deposit rates to avoid competition in order to fatten their profits and build their capital cushions – has now left the room. And instead of keeping competition for deposits down, the Fed has been raising rates.

“There is no way that these rates can remain as low as they are forever. My suspicion is that if one of the big banks broke ranks,” the others would follow, Deepak Goyal, a partner in the financial services practice at Boston Consulting Group, told the American Banker, which added:

Retail deposit rates vary by market, and most big banks are looking at ways to more nimbly respond to changes in consumer demand and competitive dynamics, observers said.

Wells Fargo, which has used regional pricing elsewhere in the country, split up its home state of California into four regions…. That move sets the bank up to offer different rates in each of those regions as needed.

Bank of America split four states… into two markets each.

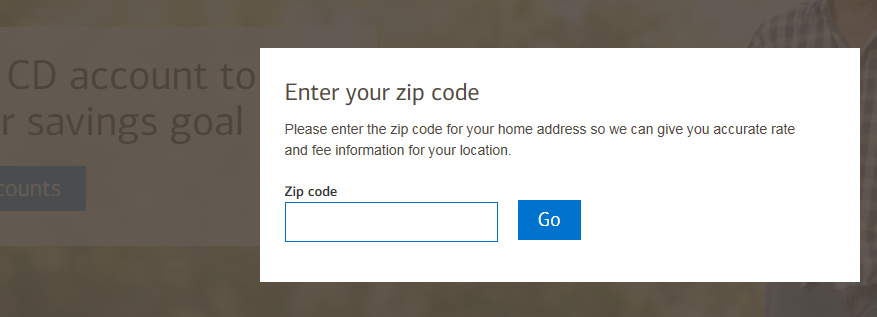

You can tell how this regional pricing works when you look for CD offers on a bank’s website, and the first thing it asks you for is your zip code, “so we can give you accurate rate and fee information for your location,” as Bank of America puts it:

Competitive deposit pricing, after having disappeared under the Fed’s interest-rate-repression rule, is now front and center. Banks are using data and “tech savvy” approaches to try to attract the most amount of money by offering higher rates only to some customers while keeping the deposits of most other customers in the near-zero basement, hoping they’ll never get out. And bank customers and savers have to re-learn to aggressively shop for deposit rates – or else they’ll get stiffed forever.

But it’s a godsend for those savers who are trying. Read… Fight for Deposits Erupts among Banks, with Winners & Losers

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

After I retired I got bored and found a job as a part time teller at a savings bank. They specialize in CDs and Traditional IRAs and offer Money Market accounts as well. I have been with them for a year and a half and we had two rate increases the first 9 months I was there. This year, we have had 5 increases so far and there are rumors of another one. BTW-we currently have 2.25% yield on a 12 month ($500 minimum) CD.

Am I missing something here?

I thought it was an open secret that banks are going to go bust very soon, after years of casino capitalism and paying themselves obscene salaries. Moreover, banks fully intend to “haircut” or “buy in” their depositers of up to 21% of their savings, as they did in Greece.

Who would trust these corporate layabouts to return any of our hard earned savings?

I agree. And 2.25%, nope.

Andrew,

Greece? You are confused. There was no depositor “bail-in” in Greece.

Right. Cyprus had the forcible bail-ins… and set a key precedent of subordinating deposits to other bank liabilities.

But I reckon Andrew was close enough; the Greeks certainly got to pay for the German (and other!) banks’ foolishness as well.

When a bank that owes YOU goes belly-up, “deposit insurance” may not live up to its name.

Best to take other measures for self-protection: diversify accounts so a single bank failure doesn’t ruin you, monitor your counterparties, minimize small-business working credit (I refuse to tall it “cash” or “capital” when it ain’t)…

I was thinking about this today — up here in Canada, my Scotiabank savings account is paying 0.20% . . . It seems like that should be a BIT higher, though the central bank is behind the curve, compared to the US. Maybe I’ll look around . . .

Yeah, looking around is necessary in all venues. This article reminded me of a mortgage renewal I once endured. The 5 year term was up in 1992 and the Royal Bank of Canada informed me that I would have to pay a $55 service fee to process the renewal forms. I went in and talked to the loans honcho, “Let me get this straight, you are charging me a fee to make a profit on my business”? Soctia bank offered a no charge mortgage processing fee for all new customers at the same time. When I suggested pulling my account they quickly waived the fee. The same day I switched to the local Credit Union due to the RBC dishonesty. Apparently, they only waived the fee for those who protested.

This week I am switching our home insurance to a private non-banking affiliated insurance company after the Credit Union linked agency gave me some grief on a new construction policy for a rental I just built. The new company offers terrific service and follow up, lower rates, and the broker I deal with informed me today by email the best time to come in and see her so we don’t conflict with her lunch break and my travel times, etc. It was professional and thoughtful customer service. Two auto policies, two house policies, and my neighbour has looked into switching over as well. It’s a hassle to switch accounts but I just get tired of being shafted.

I need a new condo Insurance for my rental. I’m getting charged $420/year for a 882 sq ft 1br+loft.

Care to share your new insurance company so I can get a quote?

Hub Intenational: They use the same pool of underwriters, but shop around for clients.

When I built the rental I did not arrange insurance before I began construction as the vacant land was covered by my homeowners policy. When the structure was proceeding and value started to rise I wanted insurance in case vandals lit it, whatever. The company informed me that I had to insure it for $300,000+, when it is in no way close to that value/amount. They wouldn’t budge. I went to 5 different companies that day and Hub International allowed me to insure it for replacement with a pre-fab/modular offering if needed, which is considerably less than the $500/sq foot the previous company was forcing me in to.

The cottage is 640 sq feet with very nice features, and I built it with many left over materials from previous work, plus local milled siding and timber. Underground services including new hydro, post and beam 10′ ceiling with t&g pine, rounded drywall corners, etc made for a nice result. Just one bedroom, but designed for a simple bedroom addition for the right tenant. I have $40,000 into it and now estimate a replacement to be $200,000 if it burned down.

excerpt from email (after I increased the coverage by email request):

“I have requoted the Rented Dwelling policy with the dwelling value of $200,000 and the amended annual premium will be $830 (the prorated amount due will be $152). I can process this change and have the documents ready for when you come by the office.”

The amount isn’t much different that your policy, but the service and attitude is exceptional, and I believe to be honest.

My friend moves in next week. I have one solid day of plumbing hook ups/finishing, and 1/2 day for baseboard and we are done done done.

regards

Low rates imply low risk, you should be only be concerned if they start rocketing higher.

So, is better to wait until rates get higher then?

3 month treasury bills at 1.6%. Envy 3 month, FED raises, so by the time of 18 month, you will be 1.6 + 0.25* 18 / 3 =3.1%.

The banks are using 2.25 to entice the uninformed so that they are better off.

Screw the banks, do 3 month treasuries, that’s my take.

…well said. they always come out ahead.

In my opinion even better….4 week (28 day) t-bills. Auctioned weekly on Tuesdays and yielding 1.65%-1.75%. Beats any bank non-term deposit, and is state tax free if you reside in a taxing jurisdiction.

Where/how does an individual buy t-bills?

go to Treasurydirect. gov

You people must have lots of money, because last time I heard you needed $10,000 bucks to buy T-bills or treasuries plus the commission because you have to buy them through a broker. Over 60% of Americans can’t afford a $1000 emergency–how in hell are they going to buy T-bills? Perhaps my info is wrogn or obsolete, but I do know that the government does NOT sell these things directly–you need a broker, and the vast majority of Americans cannot afford a broker.

https://www.treasurydirect.gov/

Buy TBills through Vanguard and Fidelity and avoid commissions. $1,000 increments. TBonds can be purchased with as little as $50, commission free direct from the Treasury. Must hold 1 year.

A full service broker I use recently said that CDs would yield more than Treasuries …I said have you looked lately? Must admit, I don’t recall that being case in the past, but maybe I have forgotten.

Looks like the minimum is $100

https://www.treasurydirect.gov/indiv/help/TDHelp/faq.htm

You can buy T bills in $100 increments at Treasury Direct and brokered CDs in $1000 chunks at Fidelity. You won’t get rich in T bills or CDs but at least keep up with inflation to a certain extent.

The bigger issue is, why would anyone in their right mind buy debt that is going to be printed (inflated) away by the Fed?

Gershon, I thought about that question for a long time and the answer is simple. You either loan money to them and hold their currencies or you buy guns and bullets and go against them. I decided to OBEY. All other kind of rhetoric is like jerking off.

Popular direct has a savings account at 2%.

Wolf, thanks to your reporting on this, I too picked up a Wells Fargo 13 month 2.25% FDIC insured CD. I also got a smaller 3 month and 6 month CD from different banks.

My bank did not show up on my broker’s list unfortunately. Wells Fargo is not my favorite bank …

http://www.startribune.com/suit-wells-fargo-endangered-s-minnesota-family-in-state-victim-protection-program/482074921/

Having done business with Wells and BOA over the past forty years, I wouldn’t do business with them at gunpoint. Together they have revived a quaint 19th century word, scoundrel. Its modern synonym, stumpf, meaning to appear before a governmental body and smirk.

Soon banks will have copies of their new book in the lobby:

Mein Stumpf.

Why are cash hungry banks hunting for deposits?

Taking a look at consumer sentiment may provide part of the reason.

The first quarter 2018 consumer sentiment for ages under 35 versus those who are over 50 years of age.

The younger generation has ALWAYS been more optimistic than the older generation. Not anymore. Surprisingly, this has changed.

For the first time ever going back 58 years (length of stats), consumer confidence for over 55 is higher than those aged under 35.

edit: should read –

“35 versus those who are over 55 years of age”.

Why not buy T-Bills instead. More liquid and doesn’t lock up your money like a CD.

T-Bills are great. But banks sell CDs, and this article is about banks and competition among banks for deposits, something we haven’t seen in 10 years. This is a huge shift. It’s not a recommendation to buy CDs.

I would expect 4 week T bill rates and passbook savings rates to track close to one another with somewhat of a lag. 0.01% accounts were possible back in 2009-2015 but not anymore with 4 week bills at 1.7%. Any bank that resists will see a flight of not only deposits but also the revenue streams that come from deposit account customers.

Why is there suddenly a war for deposits? Are the bankers anticipating deposits finally coming back from the stock market? It’s been about ten years now since depositors started chasing yield by withdrawing money from the banks and moving it into equities. I’m wondering if the banks see a reversal coming.

In simple terms, banks are making basic corporate choices in today’s system. To get more loans with higher interest they need bigger depositor stock piles(0.25% is a lot of money when borrowing millions or billions). The current bank machine runs on debt, the more debt they create the bigger the pay cheque. Never paying down principle, they only worry about having enough money to cover interest charges.

Thank you again Wolf!

It is to many numbers for me. I would love to see the migration of money on a big flow chart. Where is it going?

Seems like interest rates are on my mind a lot lately. I like to watch the Treasury Bonds more than stocks (worse than watching paint dry). Stocks are mostly a gamble on the value going up because so few companies actually pay a dividend. I guess it is a gamble on growth of revenues and assets too. But today, so many are tied together with the ETFs. Much of the game in the last decade has revolved around share buy backs and borrowing money.

The cost of money going up should put a damper on most everything going up. It should really inhibit any inflationary tendencies in the economy. It should shift money out of stocks and into Treasuries. It should cut into profits.

So far stocks seem to be disconnected from the cost of money. They did quit their spectacular rise for the first year of Trump’s term. The S&P pushing 2700 again though.. I guess the repatriation of some money is still in play. A big balancing act.

Money flows are like a ballet with Weird Wally doing the choreography.

For me, I would love to see the rates paid to savers compensate us for being the real honest backbone of the economy. For without savings, it is all just flim flam jim jam..

Seems like banks know something we don’t know. Of course big banks being insiders have the knowledge, or at least better knowledge of what’s to come.

Yep, The big banks are better connected, but predicting Fed moves is never an exact science. We shall see if this “gradual” transition progresses as planned.

I think banks raising rates, should go side by side with FEWER buyback announcements; How can lending be going up in an environment where even banks are announcing buybacks?

(my view of buybacks: (1) not enough demand for corporation to invest plus, (2) not enough competition to reduce corporation profits.)

If you buy T bills or 10 year treasuries through a brokereage and the brokerage goes bust, what happenes to your money?

Which on is safer, a CD or a 10 year treasury if both are held in a brokerage account?

https://www.investopedia.com/articles/investing/050515/what-happens-when-stock-broker-goes-bust.asp

Hey Memento / JZ, I’ve always wondered that as well.

The example given for the difference of insurance between SIPC and FDIC was stock # vs value which could mean a loss in $ amount.

But if you used a broker to buy Treasury bills does that constitute full reimbursement? Or does rate changes effect/nullify original order?

Anyone know if there is a cap or requirement if one was inclined to buy Treasury bills or bonds through TreasuryDirect instead of a broker?

Same (if the CD is FDIC-insured). You’ll be fine either way since you own the actual security. Both have CUSIP numbers.

In New Zealand you can get 3.50% for one year on a minimum deposit of NZ$10,000. If you put the same minimum in for 6 months its 3.25% and 3 months will return 2.65%. Ok for Americans that isn’t feasible to do as the US dollar to NZ dollar will only return approx 70 cents therefore negating any gain on a higher interest rate but once you start turning the NZ dollar into Philippines peso or Thai Baht then those interest rates start to look good.

Incidentally I personally believe that interest rates are going to start increasing for depositors very soon because with the Fed’s hikes they can not go anywhere but up so I’ve only taken out 3 month, 6 month and a max of 1 year deposit lock ins. I can’t see rates returning to 1980’s levels where you could get in the 20% for a return but they will rise hence the banks trying to con people into “locking in” now.

Hey Ricardo,

In New Zealand an ANZ savings account gives you 2.2% return. Prob why people don’t feel squeezed to push for yield in CDs.

Nick the figures I quoted are from the ANZ bank and that is what I am receiving so not 2.2% unless its on short term deposit.

The most recent rate of the US Series I Savings Bonds (inflation protected) is 2.52%.

Minimum purchase is $50.You may cash them in after one year w/o penalty.

https://savingsbonds.com/bond_basics/i-savings-bonds-mobile.cfm

On the link you provided, it says there is a three month penalty if you cash them In before five years.

Guilty as charged.Will pay more attention to details next time.

I just sold a house for my mother in law, and decided to put the 100K in a money market acct drawing 1.37 %. I am not so sure that ANY of these banks will be solvent in 2 years, so I didn’t take the risk for another 1 % of interest. Good Move ?

Assuming your money is in the US: A savings product that is FDIC insured is about as secure as the US government, which guarantees them. Money market funds are not insured and you have to check how risky the securities in the fund are. You can get an FDIC-insured savings account at certain banks that yield more than the MM fund you cited.

I got that same flyer and I live in LA.

Also got a pop up ad earlier today for some bank I never heard of offering 1.95% money market.

Currently I’m in Barclays at 1.5% but if they don’t start moving up, I’m going to have to move it again.

Sad really. I had 4% on savings and 5% on checking (up to 25k) at Central Pacific Bank in Hawaii in 2009 and slowly watched it drop to almost 0. They also used to waive $20 worth of ATM transactions per month so I kept them when I returned to the mainland. That went away in I think 2011 or 2012.

Nice to see things turning around.

Got a snail mail from Wells yesterday advertising a 3 year CD rate at 2.25% with a minimum $25,000 investment.

Region: East Central Florida. And they know I have a fairly well-heeled checking account with them.

There is no way that these rates can remain as low as they are forever. My suspicion is that if one of the big banks broke ranks,” the others would follow Deepak Goyal said, before screaming randomly “NO COLLUSION! NO COLLUSION!!”

The Fed made this collusion the norm. It created it during the Financial Crisis and enforced it afterwards. I remember Ally trying to offer higher rates to attract deposits, and the Fed smacked it down.

A person/site (not me) who seems to track CD rates daily here : http://cdrates.bankaholic.com/ . Seems not to have any bank near where I live which is what I wanted. Play with the ‘+’ button to see a full list. Somebody puts some work into collecting the numbers, but the display format could use a little work – would be better as a flat chart.

Another rate comparason tool here : https://www.nerdwallet.com/blog/banking/nerdwallets-best-cd-rates/

Why does anyone still do business with one of the TBTF banks? These banks are responsible for the mess that we are in and they all deserve to go bankrupt. If Americans exercised the power of the purse they could kill all of them and free themselves overnight. Imagine if every single American refused to put his or her funds as well as the funds of the businesses and corporations that they own and control in any of these banks. No loans or credit cards from any of them either. It is possible.

All the money would be inside households, unsecured and unguarded households. The safety of transactions done through a bank is the one thing that keeps them in business.

I have no money to worry about being stolen, but I am sure a millionaire would have a hard time stashing cash in a household safe.

There are many places to bank with besides your mattress. Smaller local banks and credit unions. I vote for credit unions.

I am disgusted at what sheep Americans are. The crooks are rampant because nobody will do anything, even the little things you CAN do.

These banks are responsible for the mess that we are in and they all deserve to go bankrupt.

It’s not quite that simple. Everyone who signed on the dotted line for a mortgage they couldn’t reasonably afford because “prices only go up!” is also culpable. So are the captured regulators, enforcers, and legislators who have all been bought and paid for by the financiers and their lobbyists. Those who vote for the Republicrat duopoly’s Wall Street water carriers are also guilty of supporting the corrupt, crony capitalist status quo.

Wolf,

Why all of a sudden are they offering higher rates or said another way, from the bank’s macro perspective, why are they doing this? Is it anticipating interest rates going up a lot more and they want unsophisticated consumers to lend them money for what will be a cheap rate in a few months or are they looking to hit regulatory liquidity requirements or simply looking for more cash to lend off of in anticipation of CapX increasing due to the new tax laws?

This practice reaks of what I hate most in buisness. It’s possible to make lots of money based sheerly off the ignornance of consumers.

Though the numbers from that Union Bank pamflet are accyually competative…

Last year right before I advised my wife and mother in law to pull all their $50k savings out of an account that was in a union bank market rate CD, we sat in a room with a Union Bank employee try to sell her uncompetitive shit CDs with high fees and abysmal rates….

I’ll never keep my cash stash with a brick and motor bank that offers sub oar products again. And I will gladly encourage all my friends and family to do the same.

Within a year in a capital one 360 money market account our rate has gone from 1% app to 1.6% app only lagging about 0.15% behind the highest out there with a month or 2 lag to keep up.

Ignorant maybe, but more importantly LAZY!

Even a small child could do the math.

The only way to eliminate this type of profit is to replace it with something that is much worse. The most evil form of inequality is trying to make unequal things equal.

Wolf-

why do they need these deposits? They still have a trillion in excess reserves parked with the Fed. The Fed currently pays 1.75% on excess reserves. Why would any bank pay a CD holder more than that, rather than just use their excess reserves?

I’ve seen all kinds of theories as to why. If they were really trying hard to sell 5-year CDs, it would answer that question with some clarity. But they’re trying hard to sell 1-year CDs, and at 2.25%, which muddles the water. So for now, I’m not speculating as to why. I’m really fascinated by that fact THAT they’re doing it.

I know little is made of the level of safety between the CU and the retail, or money center bank in the event of a financial crisis, the CU is considered much safer because of their stringent rules on lending. Parsing bits of a percentage point has to be weighed against risk, it still matters. The Fed has convinced investors that banks are in great shape because of reserves (bonds) which has been declining. And Jamie Dimon is going to run for president?

Great post, Wolf, and a service to your readers.

I will add to the data stream here; and yes, I’m ashamed to admit that I have not yet re-deployed these savings:

On accounts at two different credit unions, from end-of-April 2018 statements, both accounts in five figures: one CU has paid 0.25 % interest; the other CU has paid 0.20%.

Must re-deploy; and there is great info for doing so, in post and comments above. As usual, thx all.

I love the not-so-subtle message of the flier: “Act now and you could soon own this yacht! And one of our attractive model-escorts will be pestering you for acrobat sex, to boot!”

Wolf, has any of this rate-hikery spilled over into Muni bond markets yet? That might be a good topic for a future article.

The S&P Municipal Bond Index is down just a tiny bit for the year (less than 1%). This means that coupon payments have not covered the decline in market value. This shows that munis are taking a little bit of a hit, and municipalities have to pay a little more when they sell new bonds, but it’s still barely noticeable.

Hey Wolf, I really enjoy this website and the quality of opinions found in the comment section. This article brings up a question that I asked my parents recently. At what age do you quit caring about making significant returns with your money? Commenters are sitting on $100k in cash and are excited about 1.5% returns with a CD. My parents inherited some land and decided to sell it as fast as possible for about 30% less than it was actually worth. They didn’t need the money, they just didn’t want to deal with the “headache”. Yet, they constantly move substantial savings from CD to CD chasing a fraction of a percentage point each time. People seem lost on what to do with their wealth. I’m 37 and live in Indy. I identify real estate deals that often return 25%+. My biggest problem is obtaining the capital to act on the deals. When you get closer to retirement, do you become ridiculously risk adverse or just blind to the potential out there? Sound advice used to be that you always make sure your savings outpace inflation. Does anybody care about that anymore? Putting cash into CD’s at these rates don’t seem to be doing that, which is why I find the behavior so intriguing.

Good questions, Beck Matthews.

I have traded and invested through three crashes, 1987, 2000-2, and 2008-9. During those crashes, if you had your money in CDs or Treasury bills and made 2% or even 0%, rather than losing 50% or more — the Nasdaq plunged 72% in the dotcom crash — you would have been very fortunate. During the last crash, the Fed undertook extraordinary measures because credit was freezing up. Now asset prices may head lower (some have already started to), but not crash, and the Fed might just let them go.

You need to go through at least one full-scale crash of 50% — this could be a long and slow one that drags out over 10 years or more, and it could include real estate — to cut your teeth as an investor and to know what it’s like. This will give you a physical appreciation of “risk.” And only after that, you will understand the meaning of “risk free” return, and why some people accept losing a little to inflation — rather than losing a whole lot to the market.

If you don’t mind losing most or all of your assets, you’re good to go with taking lots of risk — like chasing after that 25% return on a highly leveraged real estate deal. Once you don’t feel like losing that much, you get more worried about capital preservation. And there are times when capital preservation is very hard to do.

However, if you can figure out how to do it, and find lenders to work with you, you can let them take most of the risk if the deal fails, and you take most of the profits if it succeeds. And if you can find some taxpayers to bail you out, that would even be better. There are a number of people that have done exceedingly well with this strategy. But it’s not easy :-]

It’s a week late but RBC just sent me an offer for a 2.5% high interest e-savings account – regular rate is 0.90% which is why I never used one before. The rate only applies from May 15th until Aug. 15th and is subject to change if rates change. What a crock.