Credit problems always appear first at the margins.

The new Fed remains a somewhat unknown quantity: There are still four vacancies on the Fed’s seven-member Board of Governors that forms the core of the policy-making FOMC. The new Chairman, Jerome Powell, has already shown in his testimony before Congress last week that he may use a little more straight talk than his predecessors, and the markets took notice.

No one knows for sure what this new Fed will look like once the four vacancies are filled. But this new Fed will likely try to push interest rates back to a somewhat more normal level and lighten their balance sheet so that they have some options when the business cycle trips over balled-up credit problems.

With consumers, the credit problems appear first among the most fragile, most at risk, and most strung-out – borrowers with subprime credit ratings, and with lenders that went after these consumers aggressively. And this is happening now.

Small banks pushed with all their might into credit cards, loosening credit standards, lowering credit score requirements, raising credit limits, and offering new cards to people who had already maxed out their existing cards and had limited or no ability to service them from their income, and no way of paying them off – and thus are stuck with usurious interest rates that make these credit card balances impossible to service.

For small banks it was the Holy Grail: to profit from the American debt slave.

There are about 4,888 commercial banks in the US. There are the top 100 banks, and there are the 4,788 smaller banks – those with less than $14 billion in assets. These smaller banks have seen this irresistibly sweet deal. Banks were paying next to nothing in interest to their depositors, but they could charge 25% or 30% interest on outstanding credit card balances. The interest-rate spread between these two products was just too juicy, in this otherwise low-interest rate environment.

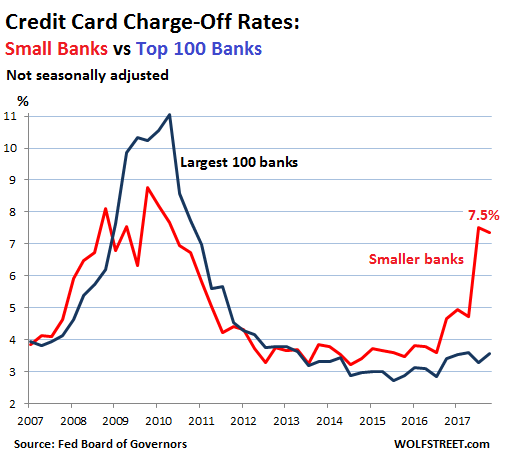

Now small banks are getting their clocks cleaned by these American debt slaves that they have gone after so aggressively and that suddenly cannot make their credit payments. Charge-off rates – the portion of outstanding credit card balances that a bank writes off as a loss – spiked to 7.5% and 7.4% of total balances in Q3 and Q4 respectively, according to the Fed’s Board of Governors. Those were the highest charge-off rates since Q2 2010, up from 4.6% a year earlier, and up from 3.5% two years earlier.

Credit card charge-offs at the largest 100 banks are also increasing, but slowly. In Q4, they were at 3.6%, just slightly higher than a year earlier (3.4%):

During the Great Recession, charge-off rates at small banks had peaked in Q4 2009 at 8.8%. So the current charge-off rates of 7.4% aren’t that far off. Charge-off rates for the largest 100 banks had peaked Q2 2010 at 11% in; but in this cycle so far, they’ve dodged the bullet.

These 4,788 small banks hold only a small portion of all banking assets, including credit card balances. So this won’t jeopardize the financial system. But the surge in charge-offs at these banks does give a glimpse at the credit problems at the margin: And this is a leading indicator for a broader cycle.

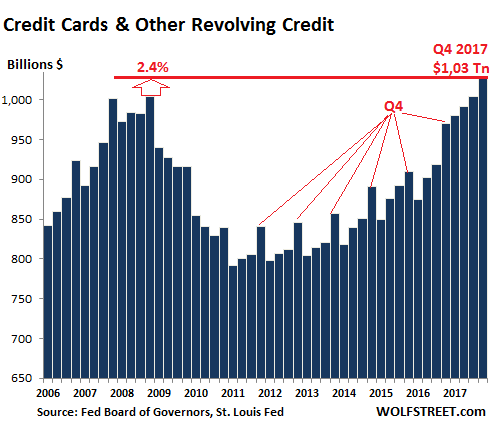

Credit card debt surged recently, starting with a phenomenal spike in Q4 2016 and continued throughout 2017, when credit card balances pushed past the crazy peak at the onset of the Great Recession.

But note: There are a large number of consumers who pay off their credit cards every month and just use them as a payment method. They have money in the bank and in investments, and they don’t need to borrow at 25% to buy groceries. The same applies to homeowners: Many of them own their homes outright or have paid down their principal balance by a large amount. These consumers are not at risk. The problems occur at the most fragile 20%.

And this spike in credit card charge-offs at smaller banks – the most aggressive end of the market – is a first sign that the business cycle has started to turn at the margin.

This comes after eight years of the Fed’s easy-money policies. But that era is now drawing to a close. The Fed has been hiking rates and unwinding its balance sheet with clockwork regularity, and with the distinct possibility of speeding up the rate hikes just when – since the Fed is famously behind the curve – the first sign of these credit problems have appeared at the margin: small banks exposed to the most strung-out consumers.

From there, credit problems spread to less fragile consumers, and they’ll spread into the corporate sector and into real estate. But banks are still pushing credit cards, and junk-rated companies are still swimming in cheap liquidity. This tells us that the credit cycle will turn only slowly, and that problems will be visible only at the margins for a while – this could be a year or two – papered over by larger numbers and averages. But it seems the Fed is painfully aware that the cycle is turning, that it waited too long, and that it’s time to create some leeway to cut rates later on.

During the sell-off, the Fed ignored the whiners on Wall Street. Read… Fed’s QE Unwind Marches Forward Relentlessly

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Not ignoring the whiners anymore. At least, we will try not to…

Great Article.

Wolf

Being retired for a few years, I’m somewhat out of the finance loop. However, I thought the following major consumer credit change had been implemented:

Credit issuers had to consider all open credit lines, plus some estimate of income(?) before offering additional credit.

If I am mistaken on this, mea culpa and ignore my question. If I am (somewhat) correct, shouldn’t this new credit-granting process weed out extreme amounts of credit being granted to those with limited ability to pay (example: $30K annual income & 100K of credit line)?

I do understand consumers can get into payment trouble even without extreme amounts of credit.

The FICO score actually “considers” this. But two things:

1. A lot of debt, if it gets paid on time, can RAISE the credit score.

2. To my understanding, there is nothing that forces a credit-card issuer to say “no” when the customer already has certain balances. Its up to the lender to decide.

There was an amendment to Regulation Z tha requires lenders to assess ability to repay, but to Wolfs point, the lender decides their own credit policy on that metric. The ironic thing is, in order to comply with the Reg, most lenders use a debt to income ratio to assess ability to pay and it is a very poor metric at predicting losses in the card industry. Unlike mortgage lending, stated incomes are normally used because income verification is expensive and inconvenient …who is willing to provide a pay stub to get a card? The Reg is basically a new cost to the industry and the consumers it was designed to help.

And things can happen after a person was approved for credit.. They can have an accident, lose a job, get sick, or even fall for a scam. Even an event like a fire or Noreaster can set a person back. There is also the seemingly invisible inflation that continues to eat at many people’s real disposable income which is never taken into account when making them a loan.

Seems to me there are a lot of people living on the edge who seem to be able to buy a decent car and some even a home yet have no money saved for any unexpected event. For many, they are just one unlucky day away from not able to make their payments.

economicminor -Plus the US economy follows a boom-and-crash cycle, and we’re due for another crash (for the top 10%) or a deepening of the ongoing depression (for the rest of us).

2007-2008 was a life changing crash; many have not recovered and the luckier of us have simply adjusted to living on a lot less money. We’re terrified of debt and very cautious financially.

The new Chase Freedom credit cards are like honey that attracts flies. In addition to now giving 1.5% rebate on purchases, the offering also allows no payments for 15 months with 0% ARP. I switched my Chase Sapphire card to that program to get the 1.5% rebate. I asked the banker what was the logic for such a generous program. He indicated that Chase believes a number of customers will grow their balance up to the credit limit and not be able to pay it off in the 16 month. This would trigger interest rate of 16.24% – 24.99% plus penalty fees.

https://creditcards.chase.com/a1/freedom-unlimited?CELL=6RRW&jp_cmp=cc/Freedom+Unlimited_Brand_Exact/sea/p25773611217/Chase+Freedom+Unlimited&gclid=CjwKCAiAz-7UBRBAEiwAVrz-9VQYruNhRZJtaf3jHZS7YgpEJtTNwgfWzo55GXDT8YsK9T7huT_vsxoCtzgQAvD_BwE

Forgot to add that the balance transfer is only 5% that will cause a number of credit card holders to move to Chase and float their balance up to 15 months. This is highly attractive if the borrower is unable to amortized their current balance with the other credit card issuer.

Isn’t that the point, banks ignore outstanding credit card balance because they hope the new user will transfer the balance to their card? As I understand CC debt is not forgiven in bankruptcy.

I believe credit card debt is written off in most consumer bankruptcies. (Maybe you’re thinking of student loans – those aren’t written off.)

CC debt is unsecured debt and is indeed written off in bankruptcy.

As for transferring debt to a new card, that can only be done once or twice because there are not that many different cards and they’re all in cahoots with each other.

And unless you’re very hard-working and diligent, the lower interest won’t be enough to get you dug out from under. It’ll last a year or so and then you’ll be right back at 39% or so.

Living in the UK back in the heady days of the 120% mortgage (1990’s) some loon (Branson?, HSBC?) offered a credit card where they would give you 20% off the entire balance transferred to them from another card.

So, I bought a new bathroom on my old NatWest MasterCard, transferred the balance to the new “goldfish” card, paid that off and saved 2000 GBP.

A friend did one better – he left with 8K unpaid on his card, two years later the collection people track him to Denmark and threatened all manner of legal action so my friend tells them; “you can get 2K now or you can perhaps try your luck in a Danish court” – they said “Ok, We’ll send the paperwork”.

Turns out someone like Experian buys duff credit card debt in bulk for pennies on the pound, then collect whatever they can. They probably would have settled for 1K.

The CC’companies make their profit on gouging the people who don’t clear the balance with fees and on securitisation of the debt. They’re not really worried about default because it’s priced in and if the debt is securitised and sold it is some sucker who bought the ‘AAA’ High Yield security who has a problem. They rather prefer clients with bad economic sense.

I keep waiting for my credit score to drop below 800. Why? Because I am a “deadbeat”. In CC land, that is someone who pays their balance off every month. I’ve used 0% for 15 months to ease cash flow when a huge expense pops up (car totaled hitting a deer, kid unexpectedly returns to college..). It’s too simple- just divide the amount by 15, and if you can’t easily afford that, then don’t do it. CC1 is reserved for only emergency loans- no purchases, ever, except 2/year to keep it active. So all my loans are free, and my CC2 pays me about 300/year in points- gift cards for holiday shopping throughout the year. My interest rate goes up every year as a result- their optimism I will fail is astounding. That too is simple- if you do not have enough in reserve to pay a minimum of 1 month of credit card purchases, then don’t use one. Should I lose my job, I will pay off the CC, and stick to reserve cash and whatever “filler” income I can earn between good jobs.

I nominate Lloyd Blankfein and Jamie Dimon to take 2 of those empty seats.

Think about it, it’s Greener for the environment. No emails and phones back and forth. Both of them play tic tac toe and that decides whatever rate they want to set.

Isn’t that how the rates are set anyways? Why not just make it official and protocol?

Rates,

Too funny. They are and have been “unofficial” Fed Board members for some time. And certainly from an “implementation” of policies standpoint. These 2 big banks as well as Blackrock and others are boots on the ground in many cases for Fed policy.

Around here (B.C. ) companies that offer credit card junkies ‘get out of jail’ schemes advertise everywhere, including billboards and bus benches.

It’s not bankruptcy. It is cheap or almost free if you do it yourself. It does affect your credit but that can be a good thing.

I know one lady well who did it: she has a good salary owns a house but still did what’s called a ‘consumer credit proposal’

(BTW: this babe had already gone bankrupt a few years BEFORE buying her second house)

In this proposal she took an 85 K debt to 35 K.

Sorry don’t know terms i.e. interest on balance.

She had some advice from a debt adviser (govt?) but did it on her own.

So you don’t need to pay a fee for this unless you owe big time. Or have major assets in which case you need the bankruptcy CA’s. (These guys hate the consumer debt advisers)

Rule one before you start: A new bank account that none of the auto debits can access.

Then comes the proposal which amounts to this: ‘do you (the bank) want something or nothing?’

Is this immoral? In the context of 20-29 percent credit card rates, when base rates are near all- time lows, I would lean towards it’s tit-for-tat.

I have passed this anecdote onto a pensioner who owes 40K, no assets, and has asked unsuccessfully for a rate, not a principal, reduction.

A pension in this jurisdiction (and most likely yours) cannot be attached except in unusual cases ( spousal etc.) but not by a credit card outfit.

I’m not going to say exactly what I said he should tell them, because I didn’t mean it literally (it would be impossible) and it usually doesn’t help to be rude.

But he could say: ‘do you want something or nothing?.’

Sorry: it’s called a ‘consumer debt proposal’ not a consumer credit proposal.

“Is it immoral?”

You don’t owe the money to your Mom. And the bank, at any interest rate, is just trying to get some money out of your pocket and into theirs. Morality has nothing to do with it for them. Nor should it be a consideration for you. It’s just business.

A man is only as good as his word. If you take money from any entity, and promise to pay it back with terms, that is the deal. Thinking that morality has no place in business undermines us all. We use a fiat currency. The entire system is based on trust value. The economy crashes when one side decides to operate contrary to good will and trust- rating bonds fraudulently, selling B disguised as AAA. I am not naïve, but gaming the system only entrenches that culture across the board. The only acceptable reasons to renege on a debt, to me, would be life and death medical bills, threat to basic sustenance, or threat of homelessness. I do not think threat to lifestyle is a good enough reason to diminish the value of one’s word. We choose our character. At its core two wrongs don’t make a right.

As a fellow BCer, I remember a time when our BC Govt. Liquor Stores did not allow the use of credit cards to buy booze. I also remember being horrified, (and still am by the way) when a booze buyer pulls out the CC. Think about it. Talk about encouraging a vulnerable group to get into trouble. Using a CC at a pub is insanity. I remember working up north and a co-worker ran up a $700 tab drinking and playing the wheel. This was in the ’80s. Today it would be a couple of thousand dollars. ( hmmmm, I shut the bar down and paid cash…….smaller hangover, too :-)

Anyway, regarding quote “For small banks it was the Holy Grail: to profit from the American debt slave.” How about consequences for greed and bad decisions? What’s next, let them hire a stable of leg breakers? I say the banks should take their losses and go under if they have made poor decisions on who they extend credit to. Credit should be earned by responsible consumers, and be granted lightly.

I know all the arguments of using a CC for the points, air miles, whatever. I also pay my card off every month. But I hate getting those statements so much I simply try and never use a credit card. Never for food at the grocery store, never for restaurant meals, and never for liquor. Once those limits are breached, (pun intended), it simply gets too easy to run up debt and buy what one wants as opposed to what one can afford. We use our card for two things only. Online ordering and for gas at the self-serves.

meant to say….Credit should be earned by responsible consumers, and NOT be granted lightly.

re: ” I also remember being horrified, (and still am by the way) when a booze buyer pulls out the CC.”

I buy everything I can–including booze, both for on-premises and home consumption–on my Costco VISA card, which I pay off every month without exception. I just spent the CC rebate of $517.47 on a shopping spree at Costco–including buying a couple months’ worth of booze–and, amazingly, got some change back. My credit scores are all over 830.

Still horrified?

Hence my comment in another article here about total consumer debt. Nothing has changed and we fell apart at the margins last time around.

Yes people are screened more effectively for a mortgage. That is superb until they lose their job and their total income is halved if not more then add the large Ford truck payment at 600+ and credit cards etc. Credit worthy becomes worthless in a few months.

Total debt is up and incomes are not rising fast enough with the bills and costs one incurs to simply live.

The most sensible thing to do these days is base the mortgage on single income, in anticipation of eventual job loss by one partner. But a 600+ car payment? Indeed, with income not rising fast enough, the middle class is too precariously perched for car loans. That status symbol has got to go.

Comparing the NSA data for the smaller banks that was linked in the article, I see that current 2017-Q4 credit-card charge-off rates (7.4%) are higher than current (5.77%) and previous quarter (5.73%) delinquency rates. I don’t get that. I would expect that charge-off rates must be some fraction of previously delinquent rates, since a card must go delinquent before it transitions to charge-off.

In order to get the corporate tax deduction they must write-off the debt. So naturally they write off the debt the 4th quarter to get the deduction.

“But it seems the Fed is painfully aware that the cycle is turning….” Perhaps the Fed should begin counting the numbers of the growing army of persons living in RVs instead of homes and apartments. Photos of residential streets in Los Angeles with lines of run-down, parked RVs at the curb are remarkable and the reported stories of the owners often tragic.

Good poi nt! I see the same thing here in Tucson, Az. In faact i am one of them, but i like it ..I feel so free and beating the system. I camp out every day. I feel like a prehistoric creature ehhehe.

This is a great article! good info. It does appear the end is already at hand for the stock market . That sucker can’t get to new highs anymore? Maybe for years! Maybe it will go so low cause no one is counting on that but a few of the mass

It’s better if the Fed doesn’t take into account things like wealth inequality or homelessness unless they change their one-size-fits-all prescription.

There’s no question in my mind that low rates and QE makes inequality and poverty much worse as it merely enables the already wealthy to monopolize more of the nation’s assets, allowing them to force rent and price increases to increase profits without having to lose profits to that pesky “wage inflation.”

Regardless of their reasoning, quantitative tightening and higher rates are much better for the majority in the long term than the current system of re-distribution to the wealthiest via cheap money.

The banks aren’t as loose with their credit cards as they once were. I remember a story of a Burger King cook who had $50k in credit card debt discharged in a chapter 7 bankruptcy. Back when I had very little money in savings, my bank gave me a card with a $15k credit limit. Today, with much more savings, they will only give me a $5k limit. If there are smaller banks that are still playing the easy credit card game, they will pay the price someday.

Drango,

Good insight and I agree. My wife and I have excellent credit scores and so can have cards at 20-25K limits. Sounds like a lot but 20K today isn’t what it was 10 years ago. Funny how inflation subtely blinds you.

The usurious interest rates charged by banks and many other purveyors of credit mean that people who cannot pay at least the monthly interest are capitalizing the debt and increasing their balances, even if making the minimum or higher payments.

This means the lenders are charging interest on any interest not paid when due. Not only that, they are lending fictitious money to start with. No wonder people with the highest interest rates (27%….???) cannot pay.

It is not just the banks. For years, I and one of my very solvent friends have bought appliances from Best Buy or Home Depot at 0%, provided you payoff within 24 months. If not paid in full by the deadline, 27% (annually) will retroactively apply to the full amount borrowed.

In a recent transaction, my minimum payment is $30 per month. The actual payment needed to pay in full within the deadline is $165 per month. In two years, you will pay 50% plus in retroactive interest if not paid in full. Many folks pay on time but I wonder what the stats are for profits generated from these “deals” for those not meeting the deadline.

My friend’s 87 year old brother got taken in by this and paid the minimum thinking he was paying as required as he is somewhat confused by contracts.

My friend got the penalty rescinded for him as he had the means to pay in full and threats of lawsuits for taking advantage of the frail elderly are scary to retailers here in Florida, as the state will back up seniors in many of these situations. Buyers on credit, beware….

I suppose this is Universal Basic Income, especially if the Fed just tops off the banks every few years. Seven lean years for the debt slave, rinse and repeat.

good point! it’s government sponsored UBI – 3 or 4 years on, 5 – 7 off. Lots of juicy profits on the up and down side for banks, attorneys, accountants.

Would be interesting to know more about the drivers behind 1 the increase in charge-offs as well as 2 the bifurcation of rates for small vs large banks. Typically, it would be higher unemployment leading to higher charge-offs, which would be affecting both classes of lenders to some extent. While there is considerable under-employment and many who have simply dropped out of the unemployment rate number, there haven’t been any shocks tha should lead to the spike shown in the graph for small banks.

Just wondering how the current Administration’s efforts to roll back regulations, including financial regs, will impact credit card and other debt delinquency/default rates going forward. Is there an agency that’s keeping track of each and every regulation that’s being rolled back, and what the potential unintended consequences might be? I have to think there’s some watchdog group out there doing that.

Well I guess the CBO’s criticism and warnings about Senate Bill S.2155 (which passed a procedural vote today) goes a ways to answering my question. Not good.

Assuming this spreads to other sectors within say a year, the Fed Funds rate is only going to be around 2.75%. That leaves them very little room to maneuver.

I keep thinking this as well. The Fed starting raising too late to gain sufficient safety margin for the next downtown….unless they go nominally negative….

Some time ago we needed money.We went to a big bank

an applied.At the time we were tight and low on cash flow.The bank

in person went through all our assets etc.They said no.However over

the internet that same bank had offered us all the money we

needed unsolicited. The interest rates were the same.So we

got the loan.I just don’t understand.

I just read the banks with assets under $250B were going to be exempt from Dodd Frank. Kinda funny. Between the subprime credit card charge-offs and defaulting auto loans there seems to be a clear trend that the outer margin is steadily declining, or at least over extended. I see many low end jobs available almost everywhere I go, but $12/hour will only go so far towards monthly payments.

12 dollars an hour? I was making 5 an hour as a part time high school lumber yard worker back in 1968 and gas for my beetle was 25 cents a gallon Ahh the good ole days

Ha. Ha. Down South, few burger flippers make more than minimum. Good thing there’s the EITC, cause that’s all these workers are in it for anyway.

Still wonder if the rollback in HC hasn’t caused the spike in consumer debt, such was the case in 2008. Consumers have more money in their pocket because they no longer have to pay HC premiums, but in aggregate their bottom line is more CC debt. Meanwhile consumer spending is strong, (do they count cancer operations?) adding to that debt, and personal savings is weak. My friend just bought a house, (priced above others on that block) she was the low bid, but the seller chose her because she has cash.

The more money in their pocket is temporarily because all these tax cuts will have to be paid somehow and no, just slicing government budgets is not gonna cut it. Not will a stronger dollar on it’s own. Sure the tax raises and maybe new taxes can be pushed to next year but that will leave such a hole in the budget that I will pity Americans if that happens.

It’s my understanding that the U.S. isn’t the biggest sinner in this regard. We are in part relying on the Super Marios of the world to keep the party going. There is nothing so safe as Italian debt.

That was sarcasm wasn’t it? Italy is about to colapse at any moment and the only reason there has not been a regulatory change to deal with Italy and Spain crisis is due to Brexit fumes.

Spain has such a hole in their budget that they are pulling new taxes out of thin air all the time.

Big tip, Spain and Italy don’t have their own currency, they have the Euro, so the old monetary devaluation recipe is out the table.

Why don’t we all have bank accounts at the Fed?

That would cut out the middleman. The banks wouldn’t make their commission.

I still see lot of money flowing around. Real estate prices are going up and up for years…, stock market is going up and up, consumer spending which accounts for 67% of US economy is going up and up and not weakening..

if people are so vulnerable, weak then they would tighten their wallet. I just don’t see it yet.

People don’t have any discipline. They can’t cut back even if they wanted to.

Fantastically insightful article Wolf. You seem to be suggesting we use the smaller banks here as the indicator that the tide is turning. What I am curious by, as someone from the UK, is that the first graph seems to indicate far more responsible consumer lending from the top 100. Is that fully correct?

Yes, the top 100 banks on average (some exceptions are already known) have used pretty rigorous credit standards in recent years. They make you very enticing offers to get people to apply for their credit cards, but you have to have good credit (high credit score) to get it. Smaller banks cannot compete with the enticing offers, so they take the riskier customers (that the big banks don’t take) to get that business.

The FED has a habit of forgetting the delays in the system.

Alan “Kamikaze” Greenspan demonstrates what not to do.

http://newsimg.bbc.co.uk/media/images/45089000/gif/_45089770_us_rates_oct08_226gr.gif

What have you forgotten Alan?

He’s forgotten the delays in the system.

There were delays while the teaser rate mortgages reset; the new mortgage repayments became unpayable; the defaults and other losses accumulated within the system until everything came crashing down in 2008.