Hedge funds pare back bearish bets “by most since November.”

A surge of the 10-year Treasury yield to 4.5% by year-end “would cause a 20% to 25% decline in equity prices,” and the economy would likely suffer a sharp slowdown but not a recession, according to Goldman Sachs economist Daan Struyven. That’s not his base case, but if it happens watch out below. Whatever might happen by year-end, it’s not happening today.

What happened by mid-morning today is that the 10-year Treasury yield fell to 2.83%, after having reached 2.95% last Wednesday, the highest since January 2014, and tantalizingly close to that ominous or glorious 3%.

Bond prices fall when yields rise. Since October last year, betting against the 10-year Treasury, and thus betting on a rising yield, has become a very crowded and profitable trade for hedge funds and other speculators.

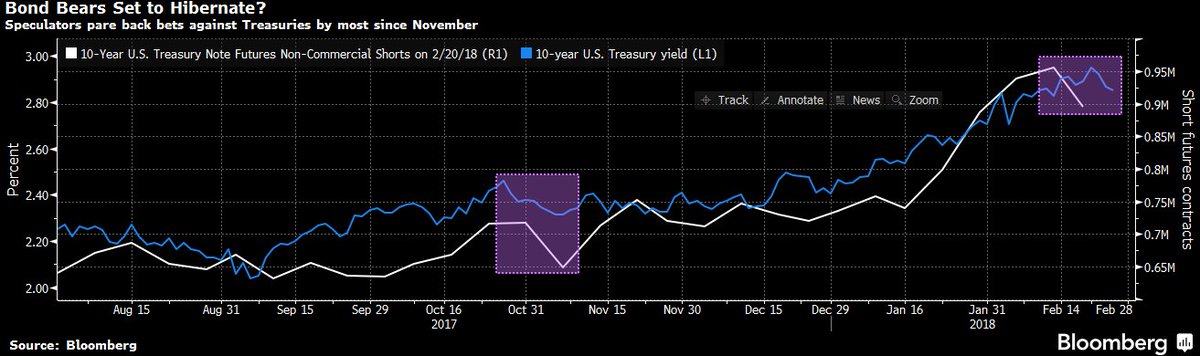

On February 13, I wrote that Record Short Bets against 10-Year Treasury Promise Turmoil. At the time, bearish bets in 10-year Treasury futures had surged to over 939,000 contracts, the most ever, according to Commodity Futures Trading Commission data through February 6.

In the week that followed, bearish bets increased to about 960,000 contracts, another record. By February 21, the 10-year Treasury yield had risen to 2.95%, tantalizingly close to 3%.

That 3%-range is a key level. It renders the 10-year Treasury increasingly appealing and brings out more buyers. And these buyers would likely coincide with short-sellers trying to take profits and get out of a short position. This might work together to put some additional oomph under the price and thus push down the yield, which could trigger a snap-back rally or even a short-squeeze for the 10-year Treasury with sharp declines in the yield.

This snap-back rally could take off even before the 10-year yield hits 3%, I postulated at the time because heavy shorting of any asset tends to have this sort of contrarian effect.

And this seems to have happened. After the 10-year yield hit 2.95% on Wednesday, it plunged, going as low as 2.83% by mid-morning today. This chart shows the daily moves of the 10-year yield:

But now something else has happened. Over the past few hours, the 10-year yield has bounced to 2.86%. Is this the end of the Treasury rally?

This morning, Bloomberg’s fixed-income specialist Lisa Abramowicz reported that bearish bets against Treasuries by these hedge funds and speculators plunged “by most since November,” by about 10% from one week to the next, to below 900,000 contracts (chart).

{kind=link}

So has this washed out the shorts? And can the 10-year yield rise from here on out?

At just under 900,000 contracts, speculators are still very bearish, and that will likely cause any increase in yields to become a profit-taking opportunity for them. In addition, the 3%-range is going to pose a formidable resistance for fundamental reasons as well. This dynamic will stay in place until shorter-term yields rise further in a significant way to where they offer alternatives in yield with shorter duration. At that point, the 10-year yield would have to rise further to attract more buyers. This will eventually happen. And it might happen in a sudden surge. But for now, the 3%-range of the 10-year yield remains a formidable barrier.

Over the longer term, the Treasury market faces a serious challenge: the flood of supply of Treasury securities being issued to fund the ballooning deficits. And these are the good times. Read… US Gross National Debt Spikes $1 Trillion in Less Than 6 Months

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

You said this “So has this washed out the shorts? And can the 10-year yield rise from here on out?”

I certainly do not know, but I could guess .

Here’s a guess, this can go on indefinitely. One of the writers on an Austrian web site, said this, maybe a decade or more ago, “Interest rates can keep getting cut in half, indefinitely . . .” No one was discussing negative interest rates at THAT time.

He meant this, 4%, 2%, 1%, .5%, .25%, .125% (ad infinitum) with the associated bond prices increasing in a similar way — ad infinitum.

I remember thinking, “Huh, that can’t be so.” And again, I was and am learning just how long markets can remain “irrational” by some external metric.

re: “ad infinitum”….you might like to read this article from way back saying just the opposite:

https://ftalphaville.ft.com/2013/03/06/1412822/the-age-of-infinite-equity/

“Government support for debt markets has gone about as far as it can. From here on the scramble for a finite number of “safe” debt assets becomes self defeating on account of negative rates and the zero bound. What you acquire in safety you must pay for in negative yield.”

(I am just starting looking at Anat Admati’s book, referenced in the article)

Good post, and a very good reference.

QUOTE : “Government support for debt markets has gone about as far as it can.”

To which I would respond, “Yet it continues.”

(Sort of stolen from what Galileo said in 1633)

The Fed is raising rates. This puts pressure on all rates. So, the question is … will the yield curve not reflect the rising cost at the short term end and will the yield curve go flat or negative?

I suspect 3% and more for the 10 year is a given unless the globalists suddenly take over the Fed, again. The next ‘battle’ is at 4%.

The real question deals with creative writing. What will the paper flippers say to sell the rising rates as OK while they sell out to the biggest losers?

I agree with that. The yield spread is very low right now. It would be hard for that to flatten any further. As the Fed does at least three more quarter point increases this year, the 10 year yield will surpass 3% quite easily.

This is speculation on my part but I can’t help but suspect the Powell Fed may have started buying treasuries again. If the Fed started buying unannounced the primary dealers would obviously see this and act on it, buying assets aggressively prior to changes in the balance sheet for February being made public. The Fed may, in fact, have reversed course. As they have stated, they can do as they please without oversight or accountability.

Jerome is beholden to Trump for his patronage and Trump wants to destroy the value of the dollar and also needs a willing buyer to monetize his huge deficits. I smell a rat and I suspect Jerry is buying and will make sure 10 year rates will not go above 3%.

My view of Fed leadership.

Jerome Powel – Coward

Janet Yellen – Coward

Ben Bernanke – Coward (a coward’s coward)

Alan Greenspan – Coward

Paul Volker – Hero

Burns – Coward

Martin – Coward

That’s an awful lot of cowards mingled with only one Fed leader with a spine. You could be correct that this rally was the result of a crowded short trade. I have mostly been wrong about the Fed and markets but you had better bet the dollar is doomed if I’m correct (and doomed if I’m wrong – but on a longer time line).

A Real Man or Real Woman, is willing to be fired for DOING THE RIGHT THING.

Volcker did the RIGHT THING, and thus is correctly called a hero in your list.

The rest dance to their master’s pipe, and are the worst sort of cowards at a time when we need real leaders.

I was kind of joking when I suggested the Fed should make its next bump a whole mind- blowing half a percent, but it is starting to look like the prudent thing to do.

In the history of the Great Crash of 1929, the Fed has come under criticism for cutting rates in 1928 (in response to a plea from Britain and France)

In the words of J.K. Galbraith this was when the market went from being very active to ‘sailing off into the wild blue yonder’.

I don’t have the Fed rate for 1928 handy but I’m sure even after the cut it was more than it is now.

The Fed has tried to cool things off with announcements of up to four bumps in 2018 but blowing off the Fed is now a parlor game.

Several old hands have noted the capitulation of bearish sentiment as small retail investors, many of them retired folk, re-enter the market after being burnt in 2008.

The Fed would be doing these retirees a favor by ‘ringing a bell’ at the top, because brokers and financial advisers aren’t going to do it.

The Fed won’t ring a bell at the top but they use ‘mouthpieces’ from CNBC, Goldman and the rest of the overpaid talking heads to “inform” us.

My swag at 3% +/- is just a guess. High enough to start to reward long term savers and instututions but not too high to throw ice water on the economy.

Is suspect there will be a number of these short squeezes by the Fed to flush out the shorts, drop the yield and then let it build back up. Remember, the Fed has infinite currency to play with in the futures market. They control all but a serious and sustatined selloff.

@Mike: I like the way you are discussing the choice of rate. That is what it has become now, a bureaucratic choice, not a “price of money”. Not a “market clearing equilibrium between supply and demand of money” which they teach you in obsolete (and perhaps never true) boring e-CON 101 books far removed. The interest rate has just become manifest as a number to tweak to distribute flows of money. period.

It appears GS is sussing out a maximal “real rate” of interest given productivity and capacity limits, and given inflation projections, that the economy can sustain. So they’re making the claim 4–4.5% is the nominal max limit.

Wolf, is there any way of knowing how much of this treasury shorting is from market neutral strategies? It seems like everybody and their uncle is trying to emulate Dalio.

I don’t have an answer to your question, but check out the chart (number of contracts) that I linked in the article and here…

https://pbs.twimg.com/media/DW-jZV1V4AArsbz.jpg:medium

I think the important part isn’t the absolute level, but the rapid change in level, up and down — for me that change in level tells the story.

Stocks retracing their earlier correction, yields softening from their highs , vix settling down ,no major disruptions/casualties ; except to the short vix crowd . All is good in financatopia. This scenario will embolden the feds to continue their prescribed tightening .

The market continues to diss the Feds rate hike policy, LIBOR is on FIRE and soon the swoosh of funds rushing back out of NYSE EVEN if rates go nowhere. Not sure who blinks first, Powell or the EU, but whoever backs off loses. The(CBs)y printed trillions now the competition for these funds is heating up while simultaneously deleveraging. The trillions they printed was chum, interest rates provide the bait.

“A surge of the 10-year Treasury yield to 4.5% by year-end “would cause a 20% to 25% decline in equity prices,” and the economy would likely suffer a sharp slowdown but not a recession, according to Goldman Sachs economist Daan Struyven.”

Quoting Goldman Sachs (remember muppets?) on a ‘public’ call asserting market behavior is the same as trusting Baghdad bob on the strength of the Iraqi

army. You always do the opposite of what Goldman says.

There is every evidence the market drop was a one off thing.

I have ten years worth of central bank behavior that proves the Fed will continue low rate policy in perpetuity. They will raise this year, but only so they can cut if the stock market or housing (the two pillars of the American economy), show weakness.

You can only stay ahead if you get in now and ride the tiger.

Stock buybacks will hit a record this year. The market is now a sure thing.

Fundamentals.

ROFL.

You have a whole ten years of data?

Many people cannot even imagine what it was like when the Fed raised rates. That last cycle when this happened ended in 2006. So this was over 10 years ago. For today’s generation on Wall Street, 10 years goes back to the beginning of time and is all that is needed for complete historical reference.

In other words, “A surge of the 10-year Treasury yield to 4.5% by year-end would cause companies who invested in those treasure bonds to be quite happy.”

All these debtors crocodile tears are getting annoying. Cheap credit started to end in 2015, the FED has telling what’s gonna do months in advance since years ago.

If you weren’t smart enough to see the waves coming three years ago when costs of debt started to rise that’s too bad.

What, you thought you were too big to fall?

Well maybe if you are into coal, nuclear and petrol, the current US president seems to favor those.

But even him seems unable to mess with the FED plans. Besides those tax cuts and subsides I mean.

The prize of the dollar worldwide is gonna go up. That’s the plan.

How much upwards will it go by the end of the year?

Eh, no clue.

I would still advice buying gold if your local currency is weaker than the dollar.

The Fed can raise rates, but if the SPX is not able to lift itself, and close the gaps, go for US bonds, the long duration, one step at a time.

The safest vault in the whole world is still the US treasury, don’t hesitate.

The USD in a trading range, pumping muscles.

In a cage, the dollar will beat the Yuan.

The Fed have clues. The Fed have no choices and is out of ammunition.

The US treasury always paid interest rate on debt, that’s why the top rating.

But the US rarely reduced debt.

The principle have shrunk because inflation and GDP growth outpaced the growth of debt.

Since 2000, the Fed is not able to get inflation up.

Without inflation it’s harder to clip debt.

Once upon a time the ratio Debt/GDP was in a trading range, but it’s rising :

Nixon 1970 = 31%, 1981 = after the 70’s inflation, still = 31%,

Reagan era in1986 = 46%, 1990 = 54%, after 8 years of Clinton, in 2001 = 55%, 2005 Bush = 60% & 2009 = 83%.

Currently : $22T debt : $20T nominal GDP.

In the next recession, debt will be rising, while the nominal GDP, declining.

That will make it even worse.

This GS talking head talking about 4.5% on the 10 year is simply setting a limit. It means we won’t reach 4.5%, nowhere close. I wish I could make as much $$ as this patsy for putting out tripe like this. But he’s a mouthpiece for the Fed, et. al.

You have to learn to read between the lines in the “financial (controlled) press”. They are all beholden to the Fed and Treasury.

With the 10 year treasury yield getting high relative to recent history, I wouldn’t be surprised if the Fed has paused its QE tightening. Also, the US treasury probably has issued new debt and done refinancing only at the short end. I am assuming most of the debt sold in recent auctions have been under 10 years.

Felix Zulauf, in my opinion one of the smartest cookies in the jar, has a 4 webpage interview in the German Bizweek (wiwo dot de). It is in German, but worth your time translating if necessary :-). Longer than his usual soundbite. His forecast calls for the 10 year to bump against 3% for a while, until later in 2018 or early 2019. Then when it punches through higher this will cause, err, volatility in the bond markets and stock markets. Look for “Dann gibt es Löcher im Markt”. Also for any Zulauf fans out there, be sure not to miss his audio interview on Bloomberg with Ritholtz (also longer than usual) from Nov 2017.

The financial system has moved way beyond something the Fed can control. The shoe is on the other foot these days, the market tells the Fed what to do and the overall bloated QE system has become adept at self preservation.

Even in the recent Jan FOMC minutes they observed “Many participants noted that financial conditions had eased significantly over the intermeeting period; these participants generally viewed the economic effects of the decline in the dollar and the rise in equity prices as more than offsetting the effects of the increase in nominal Treasury yields.”

In other words: As soon as stocks go down enough we are going to need to do something about those treasury yields.

Interest rates on the 10 year have moved up almost 65 basis points since the beginning of Dec.Can the bond market rest or actually go up in price over the near term.SURE

But the framework of any bond move is dependent on the huge increase in new supply from the Treasury and the Qt by the FED. And this Qt is only going to pick up pace as the year progresses.

The Fed has indicated time and time again that credit spreads are too low,that the yield curve is too flat and that equity and junk bonds are well overpriced.The Fed will not stop tightening until these correct to the point where monetary conditions are no longer loose.

While 3% may cause some panic in certain sectors it is still low on an historical comparison.

A new additional problem has risen for Treasuries.Some rating agencies have downgraded US debt.And a growing minority of participants are pricing in some credit risk to US debt.Now obviously the US will not default on its debt,but increasing amounts of debt can lead to a lower US dollar