And how would the housing market digest these kinds of mortgage rates?

In this cycle, the Fed has hiked its target range for the federal funds rate only after meetings that were followed by a press conference. There are four of them scheduled this year – the first one on March 14-15. So, next time the Fed may nudge up its target range (currently 1.25%-1.50%) is 6 weeks away.

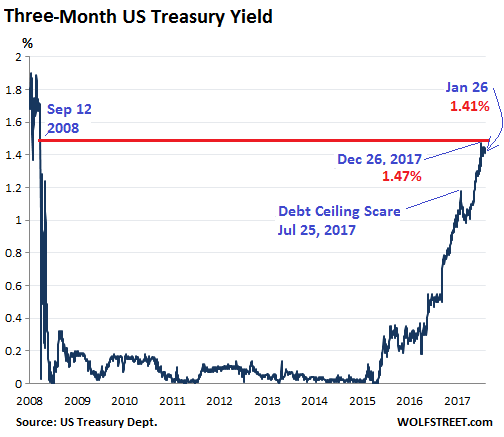

The one-month yield of US Treasury securities has vacillated around 1.25% since the last rate hike in December, closing on Friday at 1.24%. The three-month yield has vacillated above 1.4% for a month, closing on Friday at 1.41%. So this end of the curve is waiting till the propitious decision on March 15 gets closer:

About $14.8 trillion of the US government’s $20.5 trillion in debt is publicly traded (the remaining $5.7 trillion is held by internal accounts of the US government, such as Social Security). This makes the Treasury market the most liquid bond market in the world, and its benchmark yields underpin a number of other markets, including the mortgage market.

And unlike Treasuries with shorter maturities, Treasuries with longer maturities have moved in recent weeks, with prices falling and yields rising.

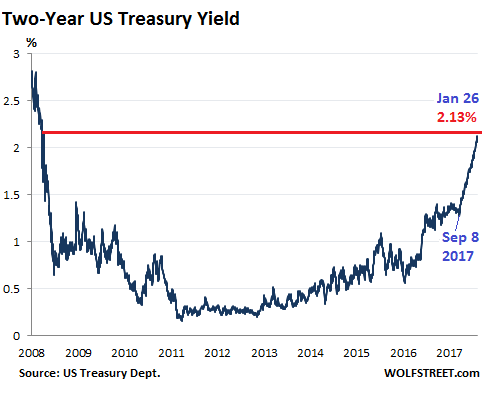

The two-year yield jumped 5 basis points to 2.13% on Friday, the highest since September 2008, continuing the spike that started on September 8, 2017, shortly before the Fed announced the QE Unwind start-date:

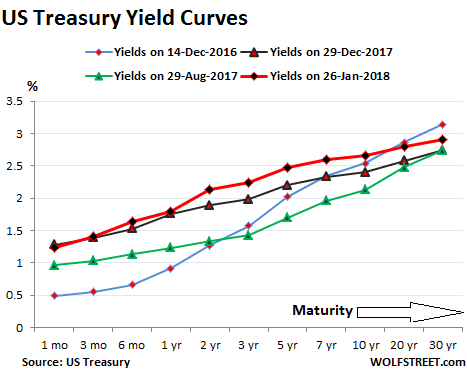

The whole mid-range of the yield curve has moved up. The five-year yield jumped 6 basis points to 2.47% on Friday. The seven-year yield rose 5 basis points to 2.60%, up from 2.33% at the end of December.

The chart below shows the “yield curves” as they occurred on these four dates:

- Yields on Friday, January 26, 2018 (red line)

- Yields on December 29, 2017 (black line)

- Yields on August 29, 2017 (green line) two weeks before the QE unwind was detailed.

- Yields on December 14, 2016 (blue line) when the Fed stopped flip-flopping, raised its rates, and became a clockwork.

Note how the gap has widened in the middle from the green line (August 2017) to the black line (December 29, 2017), and further to the red line (January 26, 2018) – in other words, how the curve has steepened recently from the one-month yield up through the seven-year yield:

The spread between the one-month yield and the five-year yield on Friday was 1.23 percentage points, the widest since March 20, 2017. And the spread between the one-month yield and the seven-year yield was 1.36 percentage points, the widest since May 22, 2017.

As the yield curve is steepening from the one-month yield up through the middle, it’s slowly pushing up the longer end: even the 30-year yield, after having been stuck for months, has started budging in January and is creeping closer to 3%.

But the 10-year yield on Friday (at 2.66%) was just a smidgen above the seven-year yield (2.60%). So it is from the seven-year yield on up where the yield curve is still relatively flat.

This leaves the closely watched spread between the two-year yield and the 10-year yield at 0.53% on Friday, near the lows of 0.50% in mid-December. In much of 2017, there was a lot hand-wringing about the possibility the yield curve could “invert” – that the 10-year yield could fall below the two-year yield – which was what had happened before the Financial Crisis. This phenomenon has been reliably associated with recessions.

For much of 2017, the two-year yield rose while the 10-year fell. Those were scary moments. But that’s not happening anymore. What has happened since mid-December is that the two-year yield has surged, and the 10-year yield has surged at about the same pace.

The suggestion has been made that the yield curve isn’t out of the woods unless it steepens to where the spread between the two-year and the 10-year yield widens back to some sort of post-Financial-Crisis normal, somewhere between 1.5 and 2.5 percentage points.

But wait… If the Fed nudges up its target range four times this year – a number that keeps cropping up – the two-year yield might rise to about 3% by the end of 2018. And if the spread between the two-year and the 10-year yield widens to 2 percentage points at the same time, it would push the 10-year yield to about 5% by year-end.

And wait… Mortgage rates follow the moves in the 10-year yield. On Friday, the average 30-year fixed-rate mortgage for top-tier borrowers rose to 4.28%, about 1.6 percentage points above the 10-year yield. If the Fed raises rates four times in 2018 and if the 2-to-10-year spread widens to 2 percentage points, then the average 30-year fixed-rate mortgage for top-tier borrowers might have a rate of around 6.6% by the end of 2018.

Would the housing market be able to digest these kinds of mortgage rates – with home prices as inflated as they are in many cities – without an abrupt decline in demand followed by a big adjustment in prices?

That was a rhetorical question.

And wait… At the end of 2018, would anyone still buy junk bonds at current yields (the effective yield of the average BB-rated junk bond is 4.38%), when you can buy Treasuries at a yield of 5%?

This too was a rhetorical question.

A flattish yield curve above seven-year maturities might just be what will make those rising shorter-term rates digestible without causing too much upheaval in the housing bubble, the corporate bond market, particularly the junk-bond bubble, and other parts of the economy. Even if spreads remain where they’re today as the Fed hikes rates four times this year, there will be plenty of adjustments in the markets. But if the yield curve steepens rapidly as the Fed hikes rates, it could get complicated, as they say.

What’s going on is a sell-off in the Treasury market. Read… Bond Market’s “Inflation Expectations” Highest since 2014

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Hmm, what will happen to the service costs on the debt when the government auctions 1.4 trillion in notes this year?

Since this 10-year yield steepening cannot happen (in any significant way), it will not happen. Everyone knows it would be a catastrophe if it went up to, say, 5%.

Unfortunately, every time this rate rises, “forces” (corruption) conspire to push down the yield.

That is not the “real” problem, but it is symptomatic of a “system” which is now so corrupt that it is insane. In an insane world, just remember that 100% liquidity = 0% liquidity.

Twist 2.0!

Potential 6.6% 30y mortgages by year’s end. That’s food for thought. Great article as always Wolf.

6.6% mortgage 30 yr rate would be devastating to housing prices.

Only if the housing was brought with unrealistically low rates and over leveraged/priced.

18% was supposed to be devastating top housing but it wasnt.

The US and other nations MUST STOP using shelter, as a GDP ATM. Or reap the catastrophic social, and political consequences, of that policy.

Moral hazard as far as the eye can see. Surely that $705 million increase in agency MBS last week isn’t an indicator of cold feet.

“Skittish Toombs, Very Skittish”

With MBS, because of their large weekly variations, we look for lower lows and lower highs. And that’s exactly what we’re seeing. This is on track.

The weekly balance you’re referring to was a “lower high.”

You really need to read and understand the MBS section in this article where I explain it all:

https://wolfstreet.com/2017/12/07/the-feds-qe-unwind-is-really-happening/

We can all see that the unwind is happening. What remains to be seen is whether it happens the way the Fed was/is anticipating. Seems they don’t fully appreciate the distortions they have caused.

Totally agree with: “Seems they don’t fully appreciate the distortions they have caused.” But I think they’re starting to try to appreciate them :-]

Aaron Layman Properties,

The FED under Yellen has finally found compunction and deserted the carpe diem fostered endlessly by Bernanke.

The ROW follows the FED for the time being.

With the trillions of dollars of QE “printed” by central banks around the world they can manipulate what curve they want. Since they are owned by banksters does anyone think that the yield curve will tighten?

So you’re saying that reinvesting the maturing bonds is easy, but with MBS not so much. Presumably, the MBS are bought again from Fannie, and the reinvested funds are buying less value than the matured ones a.k.a housing inflation 2.

Presumably, the banks are still receiving their cut for bonds, for their gargantuan effort of participating in the auction.

Please review the section on MBS in the article that I linked. It explains the complexities of MBS – including the 2-3 month time-lag to settlement, and the timing differences that cause the large weekly variations. About a month after I published this article, the New York Fed came out with its own article, confirming what I’d said. So we know this is how it works.

Or even better, you can wait until I do my next QE Unwind report either Feb 1 or Feb 8. I will re-explain it then because it’s complex and important and not that many people know about it :-)

Hey Wolf you got a mention in Stockmans Contra Corner, your chart on Netflix. He also has a chart on Bonds Risk Adjusted Return on the 10yr, which I assume might be connected to real interest rates. There are of course three metrics, yield, principle and basis points relative to par. In a fully repressed financial environment the later is probably the one that is out of line.

http://davidstockmanscontracorner.com/flying-blind-part-1-how-bubble-finance-destroys-economic-efficiency-and-rationality/

“Are we there yet?”

A great article.

It’s possible that there will be no inversion if :

1M ==> 1.8%

2Y ==> 2.5%

10Y ==> 2.8%

The Fed will push the front end up.

A stronger $USD, JNK, European JNK, German + Japan govt 10Y, and the diversion of the ad/dec line with the $SPX, will limit the US treasury 10Y from moving up, above 3%.

It seems to me that with a normal yield curve for the 10 year, there will be a RE ‘come to Jesus moment’ on home purchases and a subsequent freeze in sales. What is that magic number? I do know that in our own BC overheated market there was a trend of buying to get ‘into the market’ before mortgages become unaffordable. However, I now hear rumours of people waiting to buy until prices drop to more normal and acceptable levels.

I’ll give you an example. My best friends daughter has saved up $65,000 and wants to buy a home on Vancouver Island. (She has a good job in the trades in the Alberta Oil Sands). He often phones me and talks about it. He has recommended she wait as he believes the market is topping. She put her money in the bank and went on vacation to New Zealand.

4 rate increases this year. (supposedly). And next year? One day the gears are going to lock up. Society has replaced nearly free energy with nearly free debt to perpetuate growth. Unfortunately for the boosters, there are limits in life.

As long as everyone is “waiting to buy”, prices will not go down. Bubbles only really pop once everyone is all in. You guys are also ignoring inflation which will offset the rising interest rates. There is no housing bubble right now. Housing is in a secular market with high prices that are here to stay.

Ever heard of budget constraints? With as many properties being bought under the premise of being able to rent them out then flip how could there not be a panic selloff at some point especially as interest rates are rising and wages are still struggling to make gains.

All it takes is a mild recession and demand dries up. There will be plenty of still “waiting to buy” families converted to “happy we didn’t buy” families six months into an econ blip.

The $USD, last weak, hit a support line : the 2011(L) to 2014(L), also the fangs of 2008, 2009 & 2010 peaks at around 88.

In order to go further down, in order to be defined as a bear market, the USD will have to overcome a tremendous resistance.

Not very likely.

For that to happen (bear) something has to break or be broken.

1) The Fed can’t allow a sell-off in the stock market. That would imply a steepening yield curve not to mention a “no vote” on the forward economy. So they are propping it up with help from money leaving bonds and buying stocks. The challenge of course is “not too hot, not too cold” as Goldilocks would say. But they have the tools and fiat to do it.

2) Their goal is a very flat yield curve with low end probably around 2%, 10 year 3-ish and 30 year still under 4%. That is what they’ll be shooting for. Everyone knows the housing markets and other debt-related bubbles can’t tolerate much of an increase in the 10 year on rates.

3) The markets are totally controlled by the major CB’s, Treasury and their minions (GS, JPM,). Obviously, the US CB calls the shots (for now). Everyone sees it and most believe it now, but there is still that plausible denial in all of us that our system could actually be so precarious that our government has to resort to this.

4) All of things economic can go on for a very long time as the CBs control the fiat spigot. The “crash” that everyone has been expecting and waiting for will not come initially in the form economic. It will be social or military or terrorism of sufficient magnitude to convince people that things are way out of control. Of course, the economics will have driven the black swan to that. But it won’t be obvious that the economics was the direct cause, at least to most.

But they’ve put the money supply on an automatic reduction plan. This will force higher yields until there is some calamity.

The ‘yield curve’ is another financial concept that should be useful but is really today a cynical expression. As you discussed above, some of the possibilities can / will be farcical in the coming months.

Operation Twist brought down long rates while continued repurchases from interest payments allow rates to remain low using the same techniques Twist used. Foreign buyers who don’t want Euro-negative rates also see the 2% range for the 10 or 30 year as manna from heaven. Like I said before, the big game central banks planned out for us only works if everyone does it at the same time.

The Fed reducing its balance sheet will allow more competition for funds world wide. However, it will also unbalance the ECB plans and cause even more money to come over here from there, holding long rates down. As The Eurozone looks more and more like a live-off-printed-money scheme, I suspect a BIG flight to safety from there to here will appear after the Eurozone fails financially , keeping our rates lower for longer.

So, what might the yield curve look like? My GUESS still shallow but upward sloping with perhaps 1.5% from bottom to top in range.

Many years ago, you could make decent money in a fund that specialized in the short end. The little extra earned by going into the long end was not worth it. I think those days will return.

The real fun will be with commercial and high yield debt. People will be able to live off of interest income again. Commerce will still prosper. It did it before and only started looking a little shaky after our idiot master economists designed the plan to socialize the world economy using printed money – while making their patrons wealthy beyond imagination.

Or, to put it differently …

1) Interest rates have been and currently are completely manipulated, directly or indirectly. That will/may change when/if the Fed starts and completes normalization and balance sheet reduction.

2) The yield curve is a depiction of interest rates compared to the length of time for the debt’s maturity.

3) If rates are manipulated then the yield curve is a depiction of said manipulation.

4) Conclusion: Analysis of the yield curve and all implications are a cynical farce and will remain so until rates are far more market oriented than today.

EXACTLY!!!!! And thank you. So glad there is one other person that actually gets this. It’s been really freaking me out more and more that no one else has mentioned this. Or maybe they just honestly don’t realize??

People are sheep.

I read a story about sheep psychology recently. Sheep are actually both highly independent while following the herd. Weird combination. Sheep can become mean if you interact with them as individuals. They will do what they want and woe to you if you get in the way. However, that range of freedom starts and ends with the overall herd, which they work hard to stay within.

Thinking more broadly, that’s how people get manipulated. It’s sort of a big game of “Support the Crowd, but Screw Your Buddy”. If you can control the direction of the crowd, you control the whole crowd.

“The Fed’s “balance sheet normalization” will accelerate as 2018 progresses: In Q1, the Fed is scheduled to shed $60 billion in securities, in Q2 $90 billion, in Q3 $120 billion, and in Q4 $150 billion, for a total of $420 billion. This is scheduled to increase to $600 billion in 2019”. – The Dreaded “Flattening Yield Curve” Meets QE Unwind, by Wolf Richter • Dec 30, 2017

Additionally that article points out that the Fed could accelerate its unwind and in so tinkering, steepen the long end. Logical, but as your new insight suggests pushing the long end higher to keep pace with the <10's could have deleterious economic effect IE: RE.

Perhaps the new normal is flat beyond 15 years so as not to shock the economy, gradually letting it steepen after this generation downsizes to condos. Still, the pace of unwind accelerates quarterly through 2019 and if the long end steepens in tandem might the Fed reverse course?

In the face of a Tweetstorm generated by @RealDonaldTrump should the economy crater can the Fed remain truly independent?

That's a rhetorical question.

I don’t think an inverted yield curve will be needed to take the bottom out. Wages from FRED show a larger increase in wages than actual W2 data from SSA, which one you choose still doesn’t catch up to increases in private debt over time. The universal credit card will get exhausted much faster with modest increases in interest rates. The consumer will run out of gas. One reason it looks like good paying jobs are flat (let alone automation) at best and low paying jobs are everywhere, even with all the talk of low unemployment, more like underemployment.

For the first time ever (?) the Fed has control not only over the short-term rates but also the long-term ones via QT (qualitative tightening aka as vaporizing previously printed dollars).

As a result, the 10 year yield is clearly on the move. Up 5 pips to 2.71% this morning. And this with QT just starting to get phased in. Will be interesting to see what happens to the 10 year yield once QT hits full stride later this year.

QT a FAKE term, would be a tightening from a normal, not a re-balancing, or QE unwind, which we are currently undergoing.

If you are going to invent or use the new IT term, So you can think you look informed and important, at least us one that makes sense.

Give the guy a break, QT isn’t a term he just made up – it’s what “they” are calling it. So it’s entirely fine to use, even if you feel its a misnomer. I thought his comment was fine and understandable.

So you think that QT could only refer to something like CB naked short selling assets, then strategically Failing to Deliver them at settlement, and flooding the system with phantom securities to soak up money, then holding these unsettled transactions on their books for years and years?

I’m pretty sure that if they do such a thing they won’t call it “QT” – in fact, they probably won’t call it anything because they wouldn’t publicise it at all..

I am waiting with 70% cash on the sidelines for the housing and stock markets to crash already. Dividends go up, home prices go down. What’s not to like?

Over 90% here, better to be out too early than a minute too late.

Net short position here. The first drop will be a doozie.

What’s not to like?

Well, I guess that depends on the actual outcome.

Do we have a somewhat orderly unwinding or a crash? Have we ever had an orderly unwinding from these extremes? Can that happen?

Will the FED reverse its current direction quickly or at all?

Will interest rates continue to rise? Seems to me a 6% mortgage today would be a disaster.. As would a 4% 10yr Treasury.

It seems to me that we are at extremes in so many things. Our needs and demands as a society are growing as is our debts. While the basic grease that runs our civilization, oil, is getting more expensive. Will higher and higher federal debts be able to be funded or will the government and the FED just make believe until they can’t.

To many unknowns still.

I would personally benefit with a goodly amount of deflation and I think the nation would too.. but I am not leveraged. Those with a lot of leverage want some miraculous solution that preserves the value of their inflated assets while not destroying the value of the dollar and no crash.. They are in charge so we’ll just have to wait to see what happens.

The Fed wants to let the air out of the balloon gradually, but it only has thumbs to work with. Chances are, the Fed will lose control and the balloon will deflate quickly once it starts. There’s a lot of pressure in that balloon. You can’t blow more air into it once it’s lose and flying around the room.

Why do people keep worrying about mortgage interest rates? I say go to the moon and then housing prices will plummet! I’d much rather finance a much lower selling price than a totally inflated selling price with a low interest rate. I’ve been sitting on the side lines for years waiting for this housing bubble to pop and interest rates to rise. Think about this, in the early 1990s the interest rates for mortgages in CA were in the double digits! Housing was affordable and well within means of the average middle class income. The entire problem is debt aka cheap money has completely distorted EVERYTHING in our economy to the point that EVERYTHING is one big racket. Healthcare, colleges, automobiles, insurance, housing, the stock market. It’s going to come crashing down and crash big time………cognitive dissonance is at an all time high. It’s rather scary actually, especially for those of us that have kids. The older boomers and retirees could probably care less about their grandkids. I see it in my in-laws. They are loaded up with pensions, fat returns from the stock bubble, paid off real estate oh yeah but they all pretend they walked to school uphill both ways in 2 feet of snow their entire lives. Gimme a break!

Your general comments about older boomers and retirees is spot on. Their insouciance is profound.

They took the payoff to calm down in the 60’s. That’s why if you look at what they were fighting for (anti war, anti corporate, anti pollution, anti statism, etc), none of it changed and we’ll have to fight for it again.

That better society they envisioned got traded in for paper bubbles, BMW’s and endless cheap trinkets.

This is why they got a good deal, and everyone else got hosed. The powers that be at the time were legit scared that they were going to overturn the apple cart. And they were, until they decided to take the money instead.

So yea, why would you think they would start caring about the younger generations all of a sudden now? They stopped caring about the future 50 years ago (it’s actually amazing that it was that long ago, time flies)..

Looking at the chart 2yr/10yr since 90 and it was only lower during the stock market crashes, however it was consistently lower at this level and even flatish from the 94′ bond massacre right up until 2000, and there is some reason to think we might in a period similar to that bubble. Yes yields did rise in that period but it was only a counter rally in the bear market. Each time the Fed raised (short term) rates the market crashed, and global liquidity now far eclipses any of those events. The 200ma for FedRates is 1.42.

There’s a lot of ‘cart before the horse’ going on here.

Q4 GDP just came in at 2.6%… well below the Atlanta Fed’s GDPNow estimate of 3.4%. In other words, more mediocrity. For 2017, GDP growth was 2.3%. By comparison, in 2015 GDP growth was 2.9%.

That’s after a huge pickup (re: temporary) in post-hurricane related activity, the savings rate hitting a 12 year low at 2.4%, and credit card balances reaching new record highs.

The Fed can hike to its heart’s content, if inflation and GDP don’t pick up dramatically, the 10-year isn’t going anywhere, apart from perhaps a temporary pitstop north of 3% before coming back down.

To add…

“The savings rate fell from 3.3% to 2.6%. If it had stayed the same, real PCE would have been 0.8% (annualized) instead of 3.8% and GDP would have been 0.6% instead of 2.6%.”

The only reason GDP was even half respectable is that people loaded up on debt and spent down their already low savings… that doesn’t bode well.

Don’t be a party pooper! The stock pumpers are expecting robust earnings growth so that prices can catch up with the levitated PE ratios. Your narrative is incompatible with the plan.

There is that, so I try to think of how inflation might occur if the economy slows but rates go up.

Maybe rising rates will kill off fracking, causing energy to rise, or cause Netflix to go bankrupt causing prices of related services to rise.

Asset prices could fall but the Fed doesn’t count that in cost of living, yet if capital intensive businesses that feed into the CPI go out of business, maybe we will see inflation?

Just a thought.

Mortgage lenders may lend at the 30yr rate but they borrow at the 10yr and 7yr rate. This is because the average home owner moves or refinances before the 10yr anniversary. There is no demand for 30yr money. I doubt the long end will go to 6% unless the fed just sets it there because they know it doesn’t really matter.

Mtg rates have definitely made a move to the upside. 0.375% in 2 weeks is considered major.

///

What I am seeing here is the market preemptively reacting to the prospective FED rate increase, giving me a signal that the FED is determined to pull this through no matter what. And wallstreet is willing to take the hit. (wallstreet is with a small “w” for disrespect, they need to earn their “W”)

///

And that makes me think we are on a cliff of unseen proportions. Think of it…how bad is it, that even wallstreet, the bottom of the bottom of the human race, the people who destroyed the entire economy, sold out their own nation and people, sent people by the thousands to misery…are silently supporting these efforts. What are they afraid of?

///

I have no idea what happens this time. All I can do is look at history. Who best survived the 1930’s ? Those who were debt free and had assets. But where do you park the money. I don’t trust banks. They change the rules when ever it suits them. Close the bank the next day open as another. I live small. Not in debt. I am a boomer and I have a very bad feeling something wicked this way comes. Just when. I agree the markets fall on an outside of us economy event. They have never been as false and manipulated as they are now ….ever

The Federal reserve has a lot of inflation that they would love to forget(mis- remember)……..and massive bubbles easily blamed on the consumer and/or your neighborhood? Stand by ! Note the dollar is responding to the ten year hold your nose and BTFD ?