What’s going on is a sell-off in the Treasury market.

On Friday, the government bond market’s “inflation expectations” rose to the highest level since September 2014. Quite a feat, considering that six months ago, economists were clamoring for the Fed to slow down its already glacial pace of rate hikes – or abandon them altogether – because of “low inflation.”

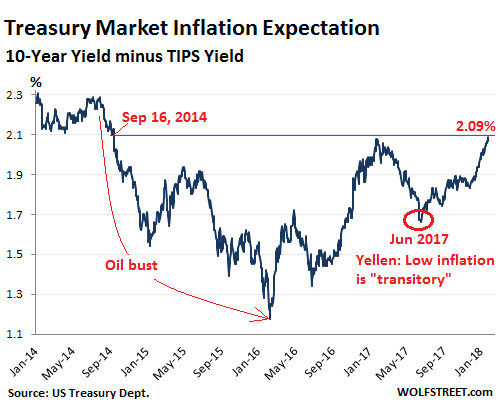

The Treasury market’s “inflation expectations” show up in the premium that investors demand for buying regular 10-year Treasury Securities over 10-year Treasury Inflation Protected Securities (TIPS). TIPS compensate investors for the loss of purchasing power due to inflation. The principal of TIPS increases at the rate of the annual Consumer Price Index, which effectively protects the principal from inflation to the extent measured by CPI.

TIPS holders also receive a small yield, if any. The spread between the 10-year TIPS yield and the 10-year Treasury yield reflects the bond market’s expectation of where inflation is headed over the next ten years.

The 10-year Treasury yield ended Friday at 2.66%. It has been in this neighborhood all week, the highest yield since April 2014 when the bond market was coming out of its “Taper Tantrum” that it had entered into when Chairman Bernanke suggested the unthinkable, that the Fed might someday start tapering “QE Infinity.”

Bond prices fall when yields rise. So what has been going on is a sell-off in the Treasury market. This chart shows the 10-year yield. Note the closing low of 1.37% on July 5, 2016. On an intraday basis, the yield had dropped to 1.32%, an all-time low. Since then, the 10-year yield has about doubled. July 5, 2016, very likely marked the end of the 35-year bond bull market that had kicked off in October 1981.:

The spread between the 10-year Treasury yield (2.66%) and the 10-year TIPS yield (0.57%) widened on Friday to 2.09%, the highest since September 2014. This is what the Treasury market is now pricing in as its expectations for inflation over the next 10 years:

In the chart, note the inflation dynamics. The oil bust started in mid-2014, and the broader commodities bust was going on at the same time. This filtered into all kinds of prices – not just fuel. At the same time, transportation costs collapsed during the “transportation recession” of 2015 and 2016 not only for freight within the US but also for containerized freight across the oceans. And there were other elements that pressured inflation lower.

But then oil prices began to rise and transportation began to recover and other prices moved higher, and inflation expectations surged. The dip last summer that Fed Chair Yellen called “transitory” was in fact transitory. And the bond market is now getting ready for more and is beginning to price this in.

This is one more piece in the puzzle to indicate that the Fed, which watches inflation expectations closely and mentions them specifically, is going to move forward on its path to higher rates.

The economy currently is going through a “spurt,” but nine years of scorched-earth monetary policies are coming home to roost. Read… Why the Next Downturn “Will Not Look Like 2008”

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wow! Wadda ya know. Regression to the mean. i.e, the lowest REAL interest rates in a hundred years (or according to one UK economist, in 5000 years) won’t continue!!!

Who could have guessed.

Stay tuned for a bunch of comments ( I assume from millennials) that since Fed rates have never been above 2 %. like, since THEY’VE been watching, which is after all TEN years, they just can’t EVER be above that.

Nick Kelly – that’s funny!

No, it will continue, because Treasuries continue to be bought, and always will be. And the rise in the market sends more money into Treasuries.

The financial sector in its entirety is not only entirely corrupt, but also, entirely bankrupt. And yet it continues to be a component of GDP. Are you so out of touch that you think the FED, of all entities, will tamper with this? Ridiculous.

It will all collapse at 100% liquidity.

Wolf is whistling past the banquet. Dow 45K, because TINA.

Investors know 2 things by watching Congress: 1.) Bonds are certificates of guaranteed confiscation, whereas when a company goes broke, assets are liquidated and loss is mitigated.

A tiny (and temporary) blip in 10 year treasuries to 2.66% and people start talking about regression to the mean. There will be no regression to the mean (at least not until enough time passes that the mean also drops).

Anything that can’t happen won’t happen. Governments, corporations and individuals have borrowed more “money” then they are capable of paying back at present values. The money can only be paid back (or at the debt serviced) in nominal terms if the currency is substantially debased – so guess what? … the currency will be substantially debased.

One way to debase the currency is to keep interest rates low and loosen lending standards – the Fed will do this because the debt situation requires it.

Another way to debase the currency is to create lots more of it and distribute it into the economy through the treasury market – the Fed will do this because the debt situation requires it.

If something must occur it will occur. Loose money is a necessary consequence of loose money policy from the past that allowed unsustainable debts to accumulate. The currency will continue to be debased to the very end – because it is now a necessary outcome.

ATACX is an ETF that tracks inflation from Fidelity Investments, and it is up 13.49% YTD (Daily)*. Thankfully, my investment advisor put a portion of my portfolio into this at the end of October which has returned over 19%.

Inflation has outpaced wages for decades, and this is one metric to measure the decline of middle and working class’ quality of life. A rise in inflation, which we have, will cause a world of hurt to most Americans.

I could be wrong but this looks like a bond mutual fund : heavily invested in the etf TLT .(long term treasuries) . The 13.49 YTD increase is kinda counter intuitive as is the name of the fund.

Hi Wolf,

The one thing that confuses me in this market is the yield variance on government bonds between the US, Germany and Japan. JGBs yield around zero, Germany’s 10 yr bunds yiels about 0.6% while US 10 yr treasuries yield, as you point out, 2.66%. What’s to prevent foreign, yield hungry buyers like European pension funds from purchasing large quantities of US Treasuries and thereby keeping yields depressed regardless of incipient inflationary pressures at home?

Your theory is at work. The impact of foreign buyers is one of the reasons why the 10-year yield has NOT surged as much as the 2-year yield. Without this interest from foreign buyers, the 10-year might have moved up as fast the 2-year and would be now over 4%.

Gundlach addressed this in his early January webcast, either German bund yields go up or Treasuries go down.

Yes, the German 30-year yield has risen from 0.34% in July 2016 to 1.28% on Friday — still ludicrously low since the YOY rate of inflation per CPI in Germany is now 1.7%. So I’d say, German yields are going up now, and will go up a lot more.

Or the dollar drops so violently that the extra yield does not offset the currency losses – in which case foreign buyers will not want treasuries even at higher yields.

The U.S. just doubled down on it’s huge deficits policy – cutting revenues and growing government spending. In the end those deficits need to be paid for with inflation. Everyone in government loves inflation these days, the Republicans used to give empty lip service to avoiding deficits but now they have jumped on the deficits bandwagon Everyone wants to kill the purchasing power of the dollar – why would anyone want to hold long term U.S. debt for a measly 2.5% yield spread after the government has made clear their inflationary intentions.

If I buy a bond at 2.66% and the interest rate goes up to 3% haven’t I lost principle? So why would there be a lot of buyers when expectations are for higher yields? Isn’t the expectations of higher yields sort of like the expectations of higher prices in stock.. Except with stocks it lowers the number of sellers.. With rising interest rates shouldn’t it lower the number of buyers?

I expect higher yields due to the growing demand by the government to finance the growing deficit at the same time the FED is unwinding its portfolio.. Seems to me the tax cuts were a bad idea.

Question 1: yes, but only if you sell. If you hold the bond till maturity, you will get a yield of 2.66% every year and then you will get paid face value when the bond is redeemed. If inflation goes to 4% in the interim, you will still get face value at the end, so the face value of your principal is protected, but its purchasing power will be diminished, and your yield (2.66%) didn’t compensate you for it.

There are many forced buyers in the bond market (bond mutual funds and bond ETFs, pension funds, life insurers, etc.). They HAVE to buy bonds no matter what the yield situation is.

There are also always differing opinions. That’s what makes a market. Many people believe yields will go lower — as you can see from some of the comments here over the past few months. So there are always buyers and sellers because they look at the future differently.

You’re right. I think of tax cuts as stepping on the gas, so to speak, while the Fed is tapping on the brakes.

The general level of ignorance about bonds pretty much reflects the all stocks all the time market. Bonds are after all just a way to GET TO STOCKS. The Fed prints bonds (like money) and the buyers rehypothecate. If you buy bonds to protect yourself, good luck. I bonds are not a bond fund, they are a note, if they fail then zombie apocalypse is the likely cause.

And don’t forget, the rest of the world is a proxie for the Fed. They will buy what they are told to buy.

The exchange rate risk may explain it. Any foreigner that invested in US treasuries lost a boatload lately because the USD has dropped quickly relative to foreign currency. Foreigners may be worried about losing more money to exchange rate variance, so they stay away from US treasuries.

Of course, if you thought USD was going to get stronger, you’d do the opposite. However, the USD is in a downtrend now.

Questions about Bonds:

I accept that Bond prices fall as yield increases, including future projections. It seems obvious enough to have this inverse relationship. However, I have a few questions.

Does anyone purchase Bonds anymore with the expectation of holding them to maturity, ever? Or, are they always simply products to be bought and sold as short term investments?

Would the yield offered have to be astronomical to attract stable investor commitment for a particular Bond offering to maturity? (What would you be willing to commit to?) I guess this depends on the industry being financed?

Is everything so shaky and volatile these days that investors are forced to just look at short term returns? Is everything just a bet?

I was reading about some Bond history during the volatile periods of the late ’70s and also ’98-2,000. It appears now that we are still in a very low rate and stable environment and have been since the financial crash. But here is my nagging question. If the economy is supposed to be so great, then why does it seem hard to attract stable investors who are looking for a safe steady return? I just read this:

“Whiting Petroleum, which has hedged 52 per cent of next year’s expected oil production, on Tuesday announced a planned sale of $750m of senior notes maturing in 2026. Later that same day, it increased the sale to $1bn, following strong demand from investors, two portfolio managers following the offering said. The company priced the new notes with a yield of 6.625 per cent, lower than initially expected.”

6.625% seems pretty good compared to Treasuries. Yet the article says the yield is low. It looks like there is a risk that investors could lose every cent, therefore, the risk is priced in. I just looked this up, (sorry, it was from CNBC)

“Rather than look at yield in a vacuum, bond investors use government bond yields as a comparison tool to determine value. Spreads between high-yield and Treasurys now are around half the normal level, meaning that the payoff is lower compared to the risk.”

If Treasuries are at 2.66%, and a Shale company yield of 6.625% is said to be too low, then it seems to me investors aren’t really complacent at all, in fact, they expect a return of 2.5X Treasuries for the risk of investing in Shale, (at a minimum). I don’t see how this is supposedly low if everything is considered to be stable in this low interest rate environment…and the current tapering-based rise is still beyond historical lows, imho.

What would a BB bond rate be in normal return times, 25%?

regards

1) It takes all kinds to make a market. Everyone pursues their own self interest. Therefore, what you or I do with bonds, if anything, is going to be different from many others.

2) The financial markets set rates, except when the central banks act in concert to flood the financial markets with printed money, set up a program to monetize debt, and use the massive amounts of printed money to buy along the yield curve. In the past, supply and demand along with credit risk was used to set rates using an invisible hand. Now it’s mostly contrived. Central bank manipulation is recent, perhaps in the last decade, and corresponds to a belief among economists that the economy can be financially engineered to maximize their version of ‘profit’. Their plan removed income from savings from the world and replaced it with income from asset bubbles. Low wages and open boarders were also supposed to, somehow, make the world better off. That plan actually only made the upper 1% better off and used the savings and labor of others to finance their increasing wealth. The financial media supports this plan. If you were to take an econ 101 class and understand the useful parts, you would know more economics than most pros. Most people with opinions on economics just repeat something they think they heard a while ago. Most of the pros are phonies who sell the book of their employer.

3) There’s no soundbite answer to your questions. You have to read and think.

4) “Inflation Expectations” is another phony concept. It is aligned with “consumer confidence” and “the horror of deflation”, all are tools used to manipulate others into believing that a certain course of action is needed if an oracle pronounces their existence.

cdr,

You said: “4) “Inflation Expectations” is another phony concept.”

It is where the bond market puts its money. This is how the market prices future inflation. The price changes, obviously, as all market prices do. But it is the price of inflation, expressed in dollars and cents, as negotiated between buyers and sellers at a moment in time. It’s not phony at all.

Up until about 10 years ago you would be 100% spot on correct. Then came central bank central planning.

Text books say rates are determined by the general level of rates, risk premium, and inflationary expectations. Debt packaging might add ‘the state of the economic environment’, but that’s fairly esoteric.

Today, there’s no price discovery. Perhaps soon if the Fed actually normalizes. Afterward, the text definition will be the right one again. Until then, inflationary expectations are a memory at best, a distraction at worst.

When you have a central bank, such as the Bank of Japan, buying bonds in such large quantities that “price discovery” is essentially deceased, then the old economics textbooks no longer apply.

In the very long run, this kills currencies as government deficits are monetized almost completely. In plainer English, the government can borrow at almost zero interest rates for as long as the central bank is willing to buy every bond that they issue. This stops once everyone else decides that the currency is worthless, as the government and bank create infinite amounts of money that has a finite economy backstopping the money.

A finite quantity divided by something that grows to infinity goes to zero, and that’s how currencies are murdered by central banks and central governments. That can take a long time, but it does eventually happen.

We seem to be enjoying a nice sunset before the “Twilight of the Gods”, a period where Ragnarok is right around the corner but things are not bad at all for the moment, and if you ignore all of the signs of impending doom it’s actually rather pleasant.

I don’t have a good answer to your full question, but I think the Whiting Petroleum notes are rated B3 by Moody’s https://www.moodys.com/research/Moodys-assigns-a-B3-rating-to-Whitings-proposed-notes-offering–PR_376978

That translates to:

Judged as being speculative and a high credit risk.

Remember it is not just return on capital, but also return of capital.

My translation is the same rating agency whores responsible for the subprime CDO tranchmouth epidemic in 2008, is now front running the shale ponzi trenchmouth epidemic in 2018. Whiting’s business model is burning cash to fuel delusions of energy independence, which seems to be working quite well (no pun intended).

Hi Paulo,

In answer to your first question, insurance companies and pension funds typically hold long term bonds to maturity. Their focus is to match the income streams from the bonds in their portfolio with the projected liability claims from present and future retirees/claimants.

As for your question about the “right” rating for a BB rated bond in so called normal times: Personally I think of the relationship between bond ratings and yields as a simple credit continuum. In good times, credit spreads will be “tight” to the underlying risk free rate. In less propitious times, investors will demand higher yields vs the underlying risk free rate. Several decades ago, in a higher interest rate environment, it was not at all unusual to add 10 percentage points (not a typo) to the risk free rate to figure out a particular companies interest rate exposure. In today’s market that would imply a yield of 12.66%. Hope this helps.

Before the financial crisis, when I still paid attention to markets, most large businesses in the US ran on money raised on Wall St. and not in normal operations. This was especially true of big box retailers which is why you had too many of them. Their unending expansion came from money raised in the equities markets.

Now they seem to be doing the same thing in the bond markets. This money being borrowed is funding normal operations. If they are lucky the cost of borrowing can be covered by their margins, and if not, too bad to those that hold on too long.

short answer institutions buy bonds, (on margin) then collateralize them and buy stocks. this is how the central banks have increased the global monetary base by trillions, and stock market averages around the world.

much of it currently going into the US which has the best interest rates. Do foreigners using their own printed money buy US Treasuries because they can collateralize that paper without going through forex, in order to buy NYSE stocks? is the weak dollar policy there to slow them down? is the Fed fighting the weak dollar wonks with its interest rate hikes, therefore propping up the dollar? we will give you the keys to the NYSE if you fund our negative revenue spending spree? is monetizing deficit spending the Feds priority? (rhetorical)

does investing in America mean a global garage sale of assets? is it possible for US corporations (which became multinationals) will find that cheap American labor is the most competitive solution? will a soaring stock market save pension funds for American who don’t have jobs anyway?

Paulo,

Very good questions — in many ways. I’ll take a shot at two of them.

1. “Does anyone purchase Bonds anymore with the expectation of holding them to maturity, ever? Or, are they always simply products to be bought and sold as short term investments?”

Bonds are designed to be held to maturity. So if you buy at face value at the time they’re issued, all you get is the coupon payment for the life of the bond and then you get your money back, hopefully. The coupon payment is supposed to compensate you for the risks you’re taking, including credit risk and inflation.

But the central banks’ efforts to push down bond yields have caused bond prices to rise. For example, 30-year German bonds acquired 10 years ago are worth a lot more today that their face value because yields have plunged, particularly in the Eurozone. So if you sell, you get a big capital gain. And given the ECB’s negative interest rate policy, hedge funds and others have piled into the bond market to buy bonds as short-term investments to be sold at a gain after yields drop further. These are highly leveraged transactions, so small moves in yields can generate big gains.

This has perverted bonds and turned them from income-producing investments to a bet for capital gains – because there is no longer any income form bonds (low yields). But this era is now ending. So bonds that were acquired two years ago will offer the holder neither income nor capital gains. In fact, if sold, these bonds would produce a capital loss. They they’ve become terrible investments.

2. Concerning your point/question about Whiting Petroleum and its high-risk junk bonds… You said, “6.625% seems pretty good compared to Treasuries. Yet the article says the yield is low. It looks like there is a risk that investors could lose every cent, therefore, the risk is priced in.”

You hit the nail on the head. The corporate bond market and particularly the junk-bond market have been in an enormous bubble. Despite the sell-off in the Treasury market, the corporate bond market has not yet followed (topic of another bond article pretty soon). So the spreads in yield between Treasuries and corporate high-yield bonds (junk) and between Treasuries and corporate investment-grade bonds are now the lowest since 2007, just before the Financial Crisis.

This means investors are not compensated sufficiently for the additional risks they’re taking with corporate bonds. And there will be a reckoning in the corporate bond market, and bloodletting in the junk bond market. You’ll be able to watch it live right here :-]

“… a reckoning in the corporate bond market,”

Corporate stocks are the signposts.

The FANG stocks (Facebook, Amazon, Netflix,Google) seem to garner all the attention as regards to stock “high flyers”. Much of their gains attained by floating corporate bond issues, with which the proceeds are used to buy back stocks. Coupled with an insane reach for yield by investors.

Flying under the radar at the moment are four other corporate stocks that make the FANG gains pale by comparison;

McDonald’s, Caterpillar, Boeing and 3M

Over the past two years, valuations of these corporate’s has skyrocketed, yet their revenues have tanked!

Corporate junk bond issuance, along with very heavy ETF investing.

The margin calls will be epic to behold.

I don’t see much of Buffet’s ‘moat’ around McDonalds.

Sooooooo, bonds are about to enter a long-term bear Market. Bond holders or purchasers have guaranteed (capital) losses… There are some (e.g., insurance companies, pension funds) bond investors that HAVE to buy bonds, but most don´t.

If this analysis holds, there could be some sudden and sharp losses as inflation expectations adjust and ratchet up. There is no reason, law or why these expectations adjustments have to be smooth, predictable or orderly.

I mean, why would you wait ?

Oh, one more thing: the CPI as a measure of inflation is bullshit – actual inflation in the U.S. is 4-5% per year. So, with yields running at under 2% after tax, current (government) bond holders are under water by around 3-3.5%.

Except, of course, if they have loaded up on high yield bonds. In that case, they can still show their clients positive real returns, what with the higher coupons and realized capital gains.

Ok, but what about the risk of high yield ?? Awwwww, ahem, well the FED and ECB et al will make sure that defaults will be contained. No worries, we´re all good.

Of course, things always work out differently from what you expect … otherwise we would all short bonds and we´d all be(come) very rich withing the next 12-18 months.

My point is that now must be the time to buy bonds !!!!

I SAID BUY ! BUY BONDS!

For every bond that is sold there must be a buyer, or else there is no deal, and we have another credit crisis. So yes, investors will and should keep buying bonds, but they may demand higher yields (lower prices), which has been happening in the Treasury market.

A lot of investors, particularly institutional investors, never sell bonds. They hold them to maturity. When these bonds are redeemed, they’ll get face value. Plus, while they were holding the bond, they got whatever yield they signed up for when they bought it.

I buy I-Bonds (directly from TreasuryDirect). Gives you a pittance, but it is supposedly indexed to inflation and each quarter the principal and interest are rolled over to the next. It’s my cash substitute and those are the only bonds I like to buy.

Also, after doing a bunch of backtesting on Portoflio Visualizer, I see that the only bonds that are inversely related to U.S. stocks are long-term Treasuries – 20-30 year – (TLT and VGLT). So if it is a hedge, those are the only ones worth having in your portfolio. Your generic total market bond fund (which usually averages 5-7 years in duration) doesn’t cut it.

Holding Treasuries long-term is risky.

We need to distinguish between holding Treasuries outright to maturity, and holding an open-end bond fund.

Treasuries will always be redeemed at face value (so credit risk is near zero). The US controls its own currency and cannot go bankrupt. The biggest risk is inflation.

Open-end bond funds can blow up during bond sell-offs and you can lose 60% or more of your principal. The problem with them is that they hold illiquid securities (corporate bonds) that they HAVE to sell when they get redemptions, and when the market is in decline, there are no buyers. So these bonds are sold for pennies on the dollar to hedge funds and the like, and you get cleaned out, unless you’re one of the first out the door.

This happened to a number of bond funds during the Financial Crisis, including some of Charles Schwab’s bond funds.

Open-end bond funds are very risky.

His I-bond comment is good though.

All things being equal, as far as I can tell, these are the BEST deal available right now. And the yields lately have been fair (even with the ‘fixed’ interest component hovering around 0% – which I thought were tied to short-term rates, but apparently not anymore).

No risk of principal loss. Pay taxes only when you cash them out. Cash them out anytime after 1 year from purchase. Will bear (and compound) interest for 30 years. Pretty much immune to theft of confiscation. etc.

The only bad things about them are unavoidable anyway – underreporting of inflation, taxes on inflation, etc. The only actual, real, downside that actually crimps your ability to stick your money into them is the $10,000/year purchase limit (although it’s $15k if you file an IRS 8888).

They’re not sexy, but you sure could do a lot worse than I-bonds out in the world..

Shale oil is expensive to extract and thus dependent on energy prices, which are volatile. So yes – risky compared to many other investments. And depending on who you ask, shale is in aggregate burning through investment capital to generate its revenues and will never pay pack its investment capital.

And anyway, treasuries are nearly 0%, so who cares what multiple of 0 this investment is, it’s not really a valid comparison metric. Like Mr. Manly above says, ROI can also mean return OF investment :)

Breakeven price for shale has gone down a very long way since 2014. Just to use a formation most people are familiar with (Bakken in North Dakota), breakeven price has gone from an average $45/barrel in May 2014 to $33/barrel in May 2017. Some Bakken areas, such as McKenzie County, have average breakeven costs as low as $24/barrel as of May 2017. Factor inflation in and that’s really impressive: I know many people here like to diss the US but this is an exemplary case of American enterpreneurship and ingenuity at work.

Both the USA and Russia are expected to overtake Saudi Arabia in oil production in 2018, at least if ARAMCO sticks to the self-imposed production cap. Which will be the great energy story for the present year.

Sticking to them means US oil companies and Rosfnet laugh all the way to the bank while the Saudi government is mired in yet another one of its semi-regular, always self-inflicted, always intertwined budget and dynastic crises.

Unfreezing production could drive down oil prices at a moment when inflation is really starting to bite, cooling it a bit (and hence allowing Saudi foreign currency reserves, mostly composed of US dollars, to breath a little easier) and perhaps driving a few, mostly marginal, US energy companies to the wall, especially if interest rates for junk-rated companies start moving forward somehow faster than a tectonic plate.

I honestly expected people to stop believing all this crap years ago (because the money to be made in shale is off the Wall Street deals, not the oil, similarly to the mortgage underwriting that lead to the housing crash), but the game goes on.

The economics of shale make no sense, outside the frantic attempt to extend an era that has ended (in the words of Warren Pollock). Chris Martenson over at peakprosperity.com has covered this quit a bit. The industry has never had positive fcf regardless of the price of oil, their well production projections are based upon 30-year traditional oil fields even though the decline rates are completely different, long term shale well maintenance is much higher than traditional pump-jacks and accompanied with the decline rates likely make these wells dubiously viable for more than a decade, ‘new and improved’ drilling/fracking techniques do not appear to recover more oil – rather just steepen the decline curve, the existing wells will never be able to pay off the existing debt for those wells, the volitiles and light mix of hydrocarbons coming off those wells cannot really be refined and no one’s willing to spend tens of billions of dollars to build refineries for them (because they know that shale has no future)..

This is, of course, separate issues of externalized costs of earthquakes and turning vast stretches of America into superfund sites (that there will never be the resources to remedy).

The only way that the United States will be able to align energy consumption with domestic production, is when it is too poor to buy other people’s carbon and can’t play any more games. Fracking is one of these games. But instead of using these past 10 years to get our affairs in order we’ve used them to build bigger McMansions further out into the exurbs and buy SUVs and defund public transit.

When choosing what to give up due to energy scarcity, as Kunsler so eloquently stated – instead of giving up SUVs and sprawl, we chose to give up the middle class. Just look around you, it’s obvious.

Art Berman and Chris Martensen have looked at the numbers and claim all the shale oil plays have not generated any profit yet. They’re drilling sweet spots first and claim they may never show a profit. Sounds like Musk may never show a profit as well as Netflix, Uber and other companies. Doesn’t make sense to me. I assume this is sustainable as long as we can keep adding cheap federal and private debt but doesn’t there have to be some reckoning in the future?Modern economics is a mystery to me .

AMZN:

Net profit margin: one-tenth of 3M

Sales: 4 times 3M

Market cap: 10 times 3M.

And hundreds of millions lost shorting this pig.

Thanks to all for your thoughtful and knowledgeable replies/comments on Bonds.

Your replies have reinforced a few things for me.

From good old Clint: “A man’s GOT to know his limitations.” For me that means I just don’t know enough about speculative finance and investing to actually risk the money I have; that I have worked hard for. (Plus, I have no guts for margins).

The other point is the concept of value. To be an investor I would have to risk my assets on what outside forces define, maybe even hype or distort. Or, as some say, on CB shenanigans/manipulation. I would have to play in someone elses sandbox, and they are going to likely be a whole lot smarter than I am.

I know my community, and I know building practices. I have some vacant land, and a bunch of left over building materials from past projects. I also live in a rural area that has little interference or inspection routines other than health and safety (electrical). For 3 hours, starting at 9:00 I will continue taping and mudding some drywall in a small rental I am building. For several years an older friend will live in it for cheap. When he is no longer able to care for himself and moves on the rental will go to a selective tenant at just below local market rate. This will allow me to be choosy, yet will provide an additional monthly income, plus has added a whole bunch of value to our land.

When I was working I used to invest through a Financial Advisor. The returns were spotty at best, and pretty much just ended up as a vehicle for deferring taxes for when I retired and ended up in a lower bracket. Now, I just take the money and spend it on building materials, and while the cost of capital improvements are not deductible, it still increases net value and will provide an additional income stream.

Until I read WolfStreet I used to think Bonds were safe. I also used to think my Financial Advisors knew more than they did. Now, I know better. My wife and I were like milk cows to them; a guaranteed income stream. Oh well……. At least we didn’t lose our investments like so many.

As long as the Fed is able to manipulate the market, there will be no true price discovery. Also, bond “vigilantes” are similar to unicorns, often discussed mythical figures, that are powerless against the Fed’s shenanigans. It’s sad that the “Big Mac Index” is a more reliable index of inflation than the “official” fed numbers. I own TIPS, and often think of selling, since their yield is based on made-up inflation numbers. If the temperature outside is 90, but the Fed says its 75, and they control the thermostat, what can you do?

Slight quibble: I would compare yesteryear’s bond vigilates to woolly mammoths. Now extinct but they were once “a thing” as the cool kids say.

Aren’t inflation expectations in the same category as Santa Claus and the Easter Bunny? Or the belief that the snowflakes who run the central banks know what they are doing? It’s funny that we periodically have inflation expectations, but never actually have inflation. At least the kind of inflation that comes from an improving economy. The inflation that comes from cheap money has in no way led to an improving economy. But then again, central bankers can’t tell the difference.

Inflation has been higher than the official numbers for years . Maybe they could come up with a new gauge that includes stealth inflation . How do you gauge getting less of a product for the same price . Too bad the Gold Standard of Ice cream has been debased as the Half Gallon Ice Cream Container is now officially Extinct !

The US economy is heavily indebted. And, importantly, productivity (real productivity) gains are non-existant. If anything, we’re moving in the opposite direction as oil increases in price and crony capitalism continues unabated.

I will be extremely surprised if the 10 year ever gets back to the 4% of 2007. Of course everything economic occurs with a lag, so I guess it is possible 4% may be reached; however, I don’t see how it could “hold”.

I have no doubt the Fed sees this too.

Supply and Demand.. If there is a larger supply of debt instruments than there is demand, or available free cash, the interest rates will raise until the debt is attractive to someone. Is higher interest rates due to inflation expectations or due to the supply and demand imbalances? Is the concept of inflation affecting interest rates still valid? When we have had tremendous inflation of our monetary base and extremely low interest rates?

The Fed is going to have to start surprising the market with rate hikes if they want to put a damper on the inflation that’s coming. If they just keep doing what the market expects they are going to be way behind the curve. For instance, they should hike this Wednesday but they won’t do it. Therefore, I think the next recession is going to be inflationary with higher stock prices and much higher commodity prices.

I have asked this a bunch of times with no response that makes sense.

You look at the saving rates, the data on mortgages, the data on car loans and the data on credit cards and it appears to me that any significant price inflation will just crater the entire economy.

How do we have price inflation when so many are already over their heads in debt?

The slow burn of inflation we’ve had is what, in my estimation, has caused the extreme levels of debt with people trying to maintain the lifestyles they have grown accustomed to with very little increases in their take home pay.. Even these supposedly wonderful tax cuts will only add $100 to most families. That is nothing in reality.

Wolf: On a different but related topic, I know you’re interested in the role skyrocketing debt has played in the current soaring (but now sagging?) auto sales boom. In case you haven’t seen it, I suggest you take a look at today’s article on Zero Hedge which describes the expanding ” negative equity” trade-in game auto dealers are playing these days just as rising used car prices seem to be starting to go the other way (along with bond prices.)

Ah, yes. the fabled consumer, credited for most of the growth of the economy despite a decade of little or no gain in his earnings, knows a bargain when he sees one. And I don’t mean $40,000 gas guzzling pickups and SUVs; I mean free money, stolen from savers and spent by the Great Unwashed.

Interest income is dead.

It is all about capital gains now, everywhere you look.

Cap rates in real estate where I live (southern california) are sub 3%.

Why would anyone buy a sub 3% cap rate building with their cash, when a 10 year treasuary yields 2.6%? Capital gains of course.

How capital gains come about in real estate? Fed QE and easy money of course. It will last until it doesnt.

Inflation expectations are the best contrary indicator for TIP investors. When the number is low these notes often sell at a discount to par, and you always consider the offer of USG to pay you up front to buy their paper. TIPs are a better investment in a low interest rate environment because inflation (despite being stuck at 2%) is fairly reliable.

In the current context CPI expectations are riding the rise in interest rates, they must correlate is the logic. They correlate best at 5% and above, and we aren’t there and never will be. If we are then you want to buy fixed yield bonds. For CPI buy low sell high, simple. Right now Floating Rate Notes are okay, esp. the ones linked to LIBOR, which is more honest than anything the Fed has. They are planning their own synthetic version. When rate hike hell week is over the Fed will get back to their books, and ZIRP NIRP etc. The goal of owning CPI indexed paper is to earn a return of ex 3.5%, CPI and yield, while fixed rate is below 2% which implies a 100% markup. We’re not suddenly going back to the 1970s. Get over it.

When Janet Yellen first became Fed Head I felt very negative about her and what she’d be doing. I expected her actions would be a continuation of Helicopter Ben’s. Turned out not be so !! The last few months I’ve come to appreciate that Yellen has done a remarkably good job !!! She successfully slowed the QE ‘theft’ by the Banksters, and then very gently raised interest rates up from ‘nothing’ helping to keep Money Market Funds from going ‘negative’ and failing. Now that Trump has got confirmation for a new Fed Head to replace Yellen, I worry the Yellen may be the best Fed Chairman we’ll ever have (since Volker).

Considering she was appointed to address the drastic effects of Fed policy on working people, and she turned out after all to be just a heartless bureaucrat, (since working people don’t know who she is, that gambit was moot) Pay attention she has rebuked Fed policy according to Greenspan, for whom CORE inflation preceded headline inflation. Yellen looks at headline inflation, and she, or the Fed doesn’t form policy, they simply react to headline numbers. At one point she emphasized that reflexive policy decisions were the norm, which means raise or LOWER rates according to their read of the tea leaves. She has since embarked on a rate hike policy, which is just her being consistently inconsistent. Greenspan used the discount window and jawboned markets, she uses RRPO, and other tools of financial repression. She also asked for the power to use Qualitative Easing, buy a broader range of assets. Among the cabal of central bankers the Fed remains something other than a true Central Bank. Brainerd is the globalist and she was Clinton’s pick to head the Fed. Doesn’t it seem odd that with the stock market going double digits, that the real economy is going nowhere? I see the so called normalization of rates as them reacting to speculation and dollar problems. And it won’t work, but she will be long gone.

Well said, clear thinking.

People staying in this inflated market are taking on big risks. The Fed has pretty much guaranteed interest rate increases and asset price drops now that it has initiated an automatic reverse QE program to reduce the money supply. This is an automatic program, and it will not end until asset prices drop so much that there is risk of high unemployment. If you are in stocks, bond, or RE, I hope you can absorb a 20% price drop in those assets for what may be an extended period.

With the stock market booming and oil prices flying, it is a great time for the FED to talk up rate increases. There will never be a better time. It is after all the Fed’s job to take away the punch bowl once the party gets going, and just now it is going gangbusters.

It is the Fed’s job to steal via inflation, but not so quickly that the masses become focused on the rapid loss of purchasing power and abandon the dollar. Hence taking away the punch bowl. FTFY

Things are out of control. The NASDAQ went up 95 points Friday. That’s greater than the entire NASDAQ index in 1977. If you bought the index in 1977, you just got another 100% return on your entire principal in one day on Friday.

Of course the Fed is going to keep raising rates. If not, the bubble will explode in nuclear fashion within a year and the Fed will be accused of standing on the sidelines. We’re in blow off top mode right now. The line will go vertical until the Fed stops it.

To me the QE programs maintained low rates for sovereign issuers, kept MBS holders solvent and generated excess reserves on which financial institutions earned risk free returns recapitalizing their balance sheets. All this necessary in the circumstances following the GFC.

The Euro Zone banks still require recapitalization and the sovereigns still require low bond yields to keep the Euro project alive. Not so in the US. Low corporate tax rates in the US and a declining US dollar only complicates the picture. However despite all this global economic activity is picking up and that will float all boats.

I’m not sure the Fed wants to be behind the curve on inflation. The deflation story appears to be playing out and a smörgåsbord of influences: commodity prices, Chinese labour costs, a tight labour market in the US, declining US dollar, trade restrictions etc. These suggest more inflation.

More treasury issuance keeps the yield curve from inverting as short term rates go up and these combined should be the brake on excess exuberance. The higher rates should also place more limits on stock buybacks limiting stock market valuations expansion. Tricky stuff but it might be pulled off. It might be prudent to get used to a higher interest rate environment in real and nominal terms. Given all the debt out there I see this playing out very slowly and carefully.

Just a little correction in the great bond bull market, we won’t see 10yr@3% but if we do load the truck. In fact, load before then.