Or what the averages are hiding.

We will start with income and see what’s left over, and for whom.

Personal income increased by 4.1% in December from a year earlier, the Bureau of Economic Analysis reported today. This includes all income received by all persons from all sources, such as from labor, financial assets (dividends and interest income but not capital gains), business activities, homeownership (rentals), government transfers, etc.

“Real” personal income — adjusted for inflation via “chained 2009 dollars” — rose only 2.37%. This is for the US overall.

Per-capita “real” personal income – which accounts for 0.71% population growth in 2017 and measures income per individual – rose only about 1.7%. If the inflation measure even slightly understates actual inflation as experienced by these individuals, their personal income growth might go away entirely.

Next step down…

Disposable personal income – personal income less personal taxes – increased 3.9% year over year in December. This is the income that folks have available for spending or saving. “Real” disposable personal income rose 2.1%. And on a per-capita basis, it rose only 1.4%. So these are not exactly huge increases.

Not everyone is getting this income growth equally.

The economy can be divided up into layers. Bridgewater Associates founder Ray Dalio sees a split between the top 40% of income earners for whom the economy is doing well, and the bottom 60% for whom the economy is a series of setbacks. Or by it could be 30% and 70%. Wherever the split is drawn, the smaller group of top income earners has had it good while the larger group of income earners at the bottom is struggling.

But consumers, no matter what their income levels, are trying to do their best to prop up the economy, upholding an American tradition. And they’re spending more, the Bureau of Economic Analysis reported today.

Personal consumption expenditures (PCE) – the goods and services purchased by everyone living in the US – rose 4.6% year-over-year. Adjusted for inflation, spending grew by 2.8%.

Personal outlays – PCE plus personal interest payments and personal transfer payments – rose 4.7% year-over-year.

So, with disposable income rising 3.9% (not adjusted for inflation), and with personal outlays jumping 4.7% (not adjusted for inflation), what’s left over and for whom?

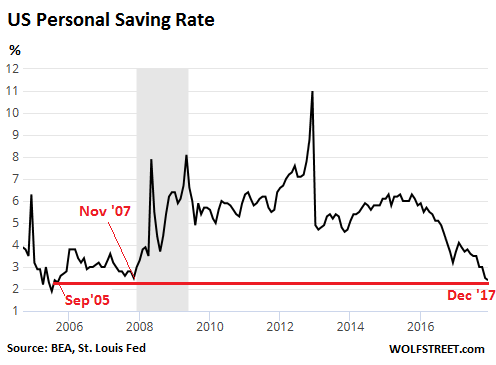

The personal saving rate – disposable income less personal outlays – fell to 2.4%. This was even below the savings rate of 2.5% in November 2007, and the lowest savings rate since September 2005:

In terms of dollars, personal saving dropped to a Seasonally Adjusted Annual Rate of $351.6 billion, meaning that at this rate in December, personal savings for the whole year would amount to $351.6 billion. This is down from the range between $600 billion and $860 billion since the end of the Financial Crisis.

But who is – or was – piling up these savings?

Numerous surveys provide an answer, with variations only around the margins. For example, the Federal Reserve found in its study of US households:

- Only 48% of adults have enough savings to cover three months of expenses if they lost their income.

- An additional 22% could get through the three-month period by using a broader set of resources, including borrowing from friends and selling assets.

- But 30% would not be able to manage a three-month financial disruption.

- 44% of adults don’t have enough savings to cover a $400 emergency and would have to borrow or sell something to make ends meet.

- Folks who had experienced hardship were more likely to resort to “an alternative financial service” such as a tax refund anticipation loan, pawn shop loan, payday loan, auto title loan, or paycheck advance, which are all very expensive.

Similarly, Bankrate found that only 39% of Americans said they’d have enough savings to be able to cover a $1,000 emergency expense. They rest would have to borrow, sell, cut back on spending, or not deal with the emergency expense.

All these surveys say the same thing: about half of Americans have little or no savings though many have access to some form of credit, including credit cards, installment loans, pawn shops, payday lenders, or relatives.

So what does it mean when the “saving rate” declines?

Many households spend more than they make. For them, the personal saving rate is a negative number. This negative personal saving rate translates into borrowing, which explains the 5.7% year-over-year surge in credit card debt, and the 5.5% surge in overall consumer credit.

It boils down to this: most of the positive saving rate, with savings actually increasing, takes place at the top echelon of the economy – at the top 40%, if you will – where households are flush with cash and assets and where the saving rate is very large.

But the growth in borrowing for consumption items (the negative saving rate) takes place mostly at the bottom 60%, where households are living paycheck-to-paycheck even if those paychecks are reasonably large and even if life is comfortable at the moment.

When the overall saving rate drops it means that the surge in borrowing at the bottom 60% or so is no longer outweighed by the growth in savings at the top.

But economic risk lies at the lower echelons – with people who cannot afford to lose their jobs. If something goes wrong in the economy, it’s at there where defaults are happening and where job losses hurt the most. This is why these low saving rates were a red flag before the Great Recession – not because households at the top were saving less but because households in the lower 60% of the economy were stretching further to borrow to fund their spending and to deal with existing debts.

Nine years of scorched-earth monetary policies come home to roost. Read… Why the Next Downturn “Will Not Look Like 2008”

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“Another light on the dashboard is blinking red.”

“Ah, don’t worry about it, those lights don’t mean anything. America is exceptional!”

Well the cure is simple they either change those little bulbs or look into the rear view for some sort of flash.

Just like an analysis:Some 5 years ago my pesky check engine light came on each time i started the engine.I raised the hood and low and behold the engine was still there.Removed the bulb no more problem!!

too much effort … you could just use some matte black model paint and cover up the little light … yup just cover it all up

You obviously live in a state that does not require an emissions test.

Move to California and your on board computer will rat you out to the DMV and you’ll have to fix whatever emissions problem caused the light to come on (that is what that light is for- not necessarily bad engine problems, just emissions related issues in the vehicle- the most common one being a loose gas cap).

OR

Trash the car – the dmv is pitiless.

Check-engine light also comes on when the oil pressure is low. Ignore it, buy new engine.

It’s helpful to figure out what causes the check-engine light to come on (and it’s not because the engine is not there anymore). Be careful ignoring it. It could get very expensive.

Buy an OBD2 scanner, but not the ones which come with bluetooth and a phone app, which was useless in my case. At the very least can tell you what the problem is.

Don’t buy a french car or learn to accept that there is a warning light that cannot be extinguished …

I one had a German colleague who always drove Mazdas.

He never changed / checked the oil, never did any other service on the engine and so on – because: A refurbished Mazda 626 engine would cost about 600 EUR installed at the time. An amount which he (rightly) figured was about the cost of 1 year of authorised BMW/Audi service. As his Mazda’s engine blew up only about once every 3-4 years and he had a good contract with a recovery service to get him home, he figured he was well ahead of his BMW and Audi -driving colleagues.

Avoiding blowing up a perfectly decent machine was too much work.

PS –

When the engine finally blew up, all of the lights would come on at the same time and there would be a hole in the side of the block. Like during the financial crisis, except we didn’t change the engine or fix the hole, we just poured more oil into it after cooling it a bit.

Not just a French car – Volvos were/are always notorious for this!

Check engine light is usually easy/free to diagnose at O’Reilly, Pep Boys, etc. Unless you have a Volvo but maybe this is just my own experience from the past.

What I hate is the tire pressure low sensor, which reliably gives a false alarm on every car in my family!

Bought a used PU and after two weeks the check engine light came on. Went to my auto parts store and he plugged the computer in and told me exactly what was wrong, how much the part cost. It is just a sensor, so I left it for the time being , turns out when something is really wrong happens the check engine light BLINKS.

My retirement may involve creation of a device which constantly sends a reset signal to the car’s computer while simultaneously sending an “Everything’s OK Here!” signal to the emissions testing machine.

I’ve had to scrap a perfectly functioning car due to dashboard lights. Talk about an unnecessary emergency spending burden jammed onto the public. Starve the children to pay to turn that light off.

A piece of tape over the flashing light will fix the whole problem.

Never EVER look at the flash !

The Federal Reserve, by keeping rates below inflation for 9 years, has taught an entire generation to NOT SAVE….and to borrow…

For every “action” by the Fed, there were equal and opposite “reactions”……

Paging Ben Bernanke and Janet Yellen. History will be written and you wont be treated well…

Rents are up, utility costs are up, food is up, gas is up, healthcare is up. Where are the savings suppose to come from when people are barely surviving.

Every time a person gets behind, the system piles on more fees and interest. The entire system is designed to destroy the working class. This can’t last much longer and it probably won’t.

Remember “universal default”? The rule is that your credit card issuer can watch all your payments and if you are late on any one of them, they can raise your rate up to 29% or whatever the max is.

In practice, they don’t watch for the missed payment. They actually watch for accumulated debt on their card and only THEN do they start watching for a missed payment. It doesn’t matter if you’ve had the credit card for 10 years and have never missed a payment.

Bank fees work the same way. They’re inevitably more costly the less money you have.

High fees and high rates used to be outlawed. Probably some states like Minnesota or Iowa or Wisconsin (don’t know about WI anymore, for sure) would still, but the Supreme Court says the states don’t have this power, since the ’70’s or 1980 or so.

One thing I learned quickly while working for wells fargo- wealthy people don’t pay ANY fees on any accounts. All they have to do is say, “Waive it or I walk”. Low value clients, however, are shown no mercy.

Agree. It’s easy to pontificate.

Some people just get by because it’s the best they can do and should feel proud just for doing that.

Others simply can’t see beyond their nose. They won’t stop buying and will pay for it later when they’re enfeebled. Social services and the charity of others are intended for these people.

The evisceration of the savers via central bank policy did not help. There should be a special place in hell for the central bankers and their intellectual support group.

Petunia, you nailed it, the system is designed to destroy the working class. Didn’t Marx institute this thought? Hummm……..

A lot of the working class has been voting against their economic interests for years. Now they are paying the price. Obamacare could have been a better and more cost effective program (including a single payer option) but the votes in Congress just weren’t there. The program could have been improved in recent years, but Republicans wanted it to fail and refused to support any improvements to the program.

The owners need to understand Henry IV of France’s famous warning to the rapacious rentiers of his day:

‘If you crush my people, you destroy me!’

But of course, Wall St thinks that it has decoupled from the rest, and in Europe the EU bosses can boast of ‘ growth’ while the young have 1,000 euro salaries to look forward to….

But were non-profit ‘healthcare’ is concerned, Warren, Jamie, and Jeffrey are riding ino the charge …

YEE-fn-HA !

‘where’… and ‘into’

damned crapified tablet ! .. sigh

I/we are doing well. We went thru the “ crash” with hardly a blip. House lost 40% of worth but when we sold it in 2016 to move to our retirement home we still had doubled our money from when we purchased it in 1995.

We live very nicely. Travel frequently.

However, I am scared sh#tless of the future. I sincerely believe we are in a Depression that no one wants to talk about. If rates 10 years after the crash are still extremely low – – why?? Something is wrong.

I am an old man. I thought I knew a lot. I guess the older I get the more I feel like Shultz, “ I know nothing?”

I was 27 during the crash and just bought my first house. It basically set me and my generation back a decade. I’m in my late 30’s now and make good money but I’ll never be able to make up for lost time and live as well as the baby boomers.

I am sure we could agree that the character “Shultz” feigned his “I know nothing” response as a ploy to avoid being sent to the Eastern Front. Often those in society who have mastered the art of going along to get along, choosing to remain unquestioningly non confrontational, end up being “rewarded” with “nice lives.” Perhaps you have yet to face your personal Stalingrad, Doctor.

If you ever choose to alleviate your ignorance perhaps you might consider reading A Peoples’ History Of The United States, by Howard Zinn as a point of departure. A great read and far less threatening than Das Kapital if inadvertently left on the coffee table during one of your coffee clatch get togethers in that gated security retirement enclave of yours.

Meh, a very biased book that oversimplifies our countries history as the oppressed vs the oppressors.

It does give voice to our national transgressions, but fails to climb above the driving ideological concept of its author Zinn that our history as a nation is one of simple oppression.

You missed half of the equation: oppression, followed by struggle to overcome it…

Michael, I did not miss half the equation…. as I stated “oversimplifies our countries history as the oppressed vs the oppressors”.

This statement encompasses all the struggles which may be inherent in the conflict.

I wholeheartedly agree that “The People’s History of the United States” is a very good book and should be required reading. It has a permanent place on my bookshelf. In college it is often used as an adjunct to a standard U.S. history textbook. Howard Zinn was quite a guy. He was a bombardier on a B-17 during the war, and unknowingly dropped naplam on an isolated contingent of German troops, far behind the lines on the Cherbourg peninsula, if I’m not mistaken, near the end of the war. The USAAF wanted to use up its stock of jellied gasoline (napalm).

Ditto.

If it’s 1960s sitcoms we’re referring to, I would go with Chief Wild Eagle (F Troop) before Sergeant Shultz (Hogan’s Heroes).

Because I never really know what’s ahead, I find myself muttering those memorable words: “We’re the Hekawe” *

And yes, before you ask, we all know which current political figure reminds us of Roaring Chicken.

* Apparently the original name proposed – but rejected by the censors –

was the (more apt) Fugawe

This is what happens when so much of the population buys into the big lie of keeping up with the Jones and consumption to fill the empty spirit. I don’t intend to preach, but I do firmly believe that one’s heart is where one’s treasures are. The chickens are coming home to roost – that is what happens when so many dance with the devil. It will not be a pretty sight !!!

Less is TRULY more….mystifies me that more people won’t believe it.

https://moneyish.com/splurge/1-in-3-young-americans-spent-more-on-coffee-last-year-than-they-invested/

I’m not complaining. Folks can keep spending at Starbucks. I just buy SBUX stock.

I have *no* money to invest, but even I can afford a can of ground coffee …

IdahoPotato Then again, the one who laughs last, laughs the hardest. Folks like us tend to stress out working and investing, while those that enjoyed that cup of coffee- well they got to enjoy it and likely with friends. There is always that possibility that neither we nor our loved ones will get to enjoy that cup.

I enjoy great fair trade organic coffee at home made with a $25 stovetop “moka” pot – the type Italian grandmas use. Tastes way better than Starbucks burnt coffee.

Idaho – I just got a “phinn” which is one of those little Vietnamese coffee makers that fits on the top of the cup, it makes a great cup of coffee. And a “phinn” only costs about $3.50 in my neck of the woods.

Although I’d have to say overall that my favorite coffee maker is a “Chemex”, it makes a great cup of coffee and clean-up is super easy.

I haven’t tried a Moka Pot yet but I’ve been curious about them for years.

And to add to this off-topic detour, just made another cuppa in the “phinn” and yeah it’s good coffee but I’m going to look into getting one of the smaller Chemex knock-offs. Actual Chemex coffee makers are expensive, and the original model is big, with a lot of thermal mass – if you’re just making one cup, one of the smaller ones is the way to go. If you look up a Chemex it’s stone-simple, but does it ever work well. Cleaning the “phinn” is kind of a pain. With a Chemex you just gather up the filter paper and toss it (in trash or garden).

All things being equal, saving coffee money will probably only result in being able to buy that same amount of coffee sometime in the future, and no one can retire off of coffee-sized money.

You might, in fact, like this article about precisely this:

https://realinvestmentadvice.com/fpw-5-financial-myths-you-should-ignore/

Did the article mention the star award program? Many of the customers are all about free stuff. It is amazing to watch what data mining can force people to buy. Today only buy two drinks and a sandwich and earn 1,000,000 stars. (jk)

“If instead of buying cups of joe, you invested that $1040 each year from when you were 25 until retirement at 65, you’d end up with more than $170,000, assuming a 6% rate of return.”

The thing is, for 40 years of saving, that’s simply not a lot of money in the grand scheme of things. It’s also overly simplified and unrealistic.

If you’re going to talk utility, I can almost guarantee you that people will get more happiness out of 40 years of some product they enjoy, than foregoing said product in the hopes of having $170,000 saved up at age 65… if you live that long.

Not saying you shouldn’t save, but these examples annoy me.

If I gave up _________, I could be slightly more rich and definitely more miserable by age 70! Wahoo!

The point is not giving up something you like. It is lifestyle creep and the notion of discretionary spending AFTER you have saved and invested.

Agree. I’m in the top 40% with savings rate, probably top 10%, but in the bottom 60% in terms of income. We only buy what we need and always the cheapest product of good quality that we can find. I’d say a good 2/3 of those with a negative savings rate simply need to reevaluate whether they really need all the stuff they’re buying.

Our last large purchase was a trip to the emergency room for our son. Even with insurance that set us back $2K. According to your reasoning, next time we should consider what we need more, the money or the kid.

He did say “stuff” . I would not have put my kid into the “stuff” category, and I doubt Matt P would either.

It’s the stuff, Petunia, it’s the stuff. I will avoid listing the stuff that I see people buying, but I am certain, along with Matt, that so very

much of it is unnecessary. Based on need vs. income vs. debt vs. lack of savings . . . etc.

E-room may be a large purchase, but it surely ain’t “stuff” .

I truly hope your son has recovered fully, and is back to where he needs being. As does Matt I am sure.

Don’t intentionally take things the wrong way. Everyone knows what was meant, including you.

Matt, Robert, Tim,

I have heard incessantly, especially since the financial crisis when working people were blamed for the crisis, how the poor and working class have misused their incomes. People with low incomes are continually dealing with financial setbacks. All the setbacks are mostly associated with items they must have to survive.

You nice middle class people all think that a video game machine is an unnecessary expense for a low income family, because you don’t understand that the machine is considered a lifesaving device in such a family, it keeps the kids at home away from the violence in their neighborhoods. I would challenge any of you to go to a poor neighborhood in your town, knock on a door and ask them about all the unnecessary stuff they have. I doubt you would find any.

George Gilder wrote “Wealth and Poverty” decades ago. I read it as an educated middle class minority woman and knew it was crap. He spent a year living on a minimum income but had the resources of a middle class guy. When we fell into poverty, as a result of the financial crisis, our resources helped us get out of poverty. They included having stuff to sell, having the ability to produce and send a resume. Having the wardrobe to wear to a job interview, etc. All items you nice middle class people would begrudge a low income family as being unnecessary.

This has nothing to do with the fact that you weren’t being criticized for spending money on your child’s health care. And yet — teaching your kid that they need a video game set (which increases the need for more stuff like a large TV, like a fast Internet connection, like fancy gear), doesn’t give them any of the resources that they need to write a resume, find a job, etc. It is not contributing to anything useful.

Teaching them that they can stay home with their family, do things together, read books, talk, does. And all those things are cheap.

My own personal observation is that people with very little money eat out a lot. If you want your kids to be thrifty, help them save money, and improve their health all at once, teach them that lunch is a peanut butter sandwich in a bag, supper is cooked at home, and a restaurant meal is a rare celebration.

Nick,

I knew somebody was going to bring up books in relation to poor people. I grew up as an avid reader in a working class family, for us my reading material was an expensive hobby. All the things I enjoyed reading were not available in the local library. My enjoyment in reading started with Archie and Veronica comic books and later evolved to teen magazines, even the National Enquirer was fun to read. All these were available at the local grocer and not the library. Had I walked into a library and only had Nancy Drew as an option, I would have become a dedicated street kid instead.

I don’t understand begrudging a poor family a large or any TV. It is cheap entertainment and provides some useful information as well. We sit around the dinner table every night and talk, mostly about all the crazy stuff I see on TV. Should all the poor kids and their families sit home staring at walls? If they did they would certainly start resenting people like you. Think about that.

You are in the only developed country without universal medical.

One spend less than one makes. It is the principle to keep you stand. If one violates that, one’s up keep becomes one’s down fall.

The trick is to “label” consumption as “investments” and let consumers “invest” while in reality everybody is “competing each other up death on consumption”. The tough part is to get out of this game, even tougher than to break the habit of gambling and drug use because you are NOT only facing yourself as the enemy, buy also the people, the competition around you, the entire matrix.

I wish i had thought of that 40 years ago.

When I read posts by the righteous smugs on what the poor and working poor are doing wrong I’m brought back to “My Fair Lady” and Alfred P Doolittle (Stanley Holloway) confronting the do-gooders looking for the “worthy poor.”

The smug think that a TV, a video game, even a cell phone are luxuries that simple folk shouldn’t have but they have never shopped at Goodwill or Salvation Army or St. Vincent DePaul where a TV can be had for free, if one qualifies, a video game can cost a buck and a cell phone can be had at Walmart for a few dollars.. They scold because meals are eaten out, but probably don’t realize some fast food joints sell meals that cost less to buy hot than to buy the ingredients and cook them at home.. Too busy wagging their fingers..

I would never argue that a cell phone is a waste of money — that’s a critical part of working today, both for finding a job and qualifying for it. Neither did I mention televisions.

Your statement about fast food being cheaper than home-prepared food is simply wrong. For ten dollars, you can buy a loaf of bread, peanut butter, jam, apples, and some kind of bulk snack, and you have 4-5 lunches. Or, you can eat once at a fast food restaurant. When you look at the expense diaries that people keep, there is frequently a very large amount of food spent on eating out. This is a choice, even if it’s one that you think is a personal right.

I’m not arguing that people are poor because they spend money — I’m arguing that they don’t have savings because they spend money. Poor people can save money too; if they have to have things, put them off for one year and save the money you would have spent, then go to town. Having $2000 in the bank is a lot better than having none. For myself, if I had nothing in the bank, I wouldn’t be eating at McDonalds.

Nick

“I’m not arguing that people are poor because they spend money — I’m arguing that they don’t have savings because they spend money.”

That is a distinction without a difference. Nick, your name was never mentioned nor was anyone else’s in my comment so I don’t know why you would think it was about you personally..

David, sorry if I misread the point of your comment. I am sensitive about this, because I do try to avoid blaming people for things that they can’t control, and I do hesitate to ascribe one or two behaviours that are worthy of scolding. In this comment I may have gone over the line, I’m not sure.

However — I work in public health, and I’m convinced that the habit of eating out is one that is pretty fundamental. It affects health, and it also affects finances (which are probably one of the largest determinants of health).

The distinction between being poor and having no savings is real. Not everyone can cease to be poor — it requires a mixture of luck, help, and planning. Managing to build up a smaller level of savings, though, is a goal that everyone should have. Maybe I’m optimistic, but I believe it’s more attainable, and more amenable to purely personal factors, than actually ceasing to be poor.

Nick

The most wonderful thing about Wolf Street, besides Wolf’s spot-on analysis, is how honest adults try and contribute to a discussion. We all go off on tangents, I’m terrible, but I do try, but genuine nasty trolls haven’t made this a home and I suspect that’s to Wolf we must give credit.

Sort of in keeping with the discussion on savings, which must be directly related to jobs, a friend of mine just wrote that he thinks he’s about to be laid off because orders have been so slow. He runs a machine that makes concrete infused siding, artificial clapboards, in a company just south of Seattle. Maybe this is normal for this time of year but I’ve watched every trade work in all kinds of weather letting nothing stop this madhouse of building in western Washington.. I find this startling news ((and it’s not news as of yet)). The company is calling in their employees either today or very soon..

I agree. The poor are as much victims of advertising as the middle class. In fact, more so. Due to their circumstances, they should be evaluating whether something is truly necessary. Unfortunately, impulse purchases and immediate gratification have become all too common. Frugality and thrift have become dirty words to some. We’ve lost a lot as a country since the 1930s.

Why does everyone have to be a victim? Why can’t people just take responsibility for their actions. Yes advertising can be effective at creating a perceived need, BUT, we as individuals can either choose to purchase or not.

The ad didn’t reach out of the TV and make me buy what I didn’t need or want 10 seconds earlier.

This victim mentality has to stop.

There is a lot of pressure for people to ‘keep up with the Joneses’, which is an acceptable choice if you can afford it. We, both professionals with good incomes, chose to stay in our modest middle class home. We enjoyed creative hobbies, tenting, ate out only occasionally and avoided buying ‘toys’ apart from two kayaks. Others in our street with decidedly lower incomes filled their carports and driveways with motorboats, RVs, ATVs etc.

We were later able to buy a nice home in a more upmarket community and enjoy a comfortable retirement. We have contingency plans and will hopefully be able to hang on if/when the world economy goes into freefall. It is worrying, though.

Why does something have to be “necessary” only when the poor/low income folks are buying? How would the middle/upper income folks react to being told they should only spend their income as someone else defines as “necessary”?

Should poor people never buy a birthday cake for their kids? Should they never eat out? Never watch TV or play video games? Never buy meat and only eat beans and eggs? Why don’t we trust them to make the right decision for their own family, income and resources?

Years ago, a woman was criticized in an advice column by a writer who was deeply offended that she bought a cake while paying for groceries with food stamps. The woman recognized herself and wrote in to say she was the cake buyer. Her child was dying of cancer and this was to be the last birthday celebration.

I never forgot this lesson, do not judge someone else’s choices as you have never walked in their shoes.

Frugal isn’t a choice when you are poor.

Roger,

Wow…seriously? Really, are you out of your mind?

I think we have GAINED a lot since the 1930’s….who would want to go back to days of Jim Crow, women as virtual chattel with limited education or job choices, deep poverty, a nascent union movement where cops beat strikers per their bosses orders, seniors freezing or dying from hunger in the streets, and on and on and on…not to mention the rise of the Nazi’s and looming WWII….and extremely high crime in the cities in the USA.

Of course people were frugal, there was NO BANK CREDIT to the working classes and low income folks are by definition/necessity frugal.

Don’t you think today’s loose monetary policy and easy credit enable “impulse” buying and immediate gratification?

No one I know who lived through the 1930’s would remotely think it better than today. I’ll even take our pervasive advertising, as I or anyone can take it or leave it in the 21st century. No one forces you to buy.

Wise words. Fill the garage to compensate for the empty spirit. Most do that but few admit it.

I try to keep up with my chickens and bees, but they run and fly faster then I ever could. ‘;]

About The Jones however, I care not ! ..

Does it really matter? I’ve been waiting for the housing crash for almost ten years. Seems the bad times are just a couple years away – always a couple years away. If it is coming, someone is doing a wonderful job hiding it ’cause I can’t see nuthin’ coming for a long time yet.

garner, you said… “I’ve been waiting for the housing crash for almost ten years.”

Housing did crash 10 years ago. Big time. It hit bottom in late 2011 or early 2012. Did you miss it?

And in theory, it would have to boom for a while before it could re-crash.

I started watching real estate crash blogs (Dr. Housing Bubble, the one about clean thinking in a dirty glass, etc.) in the early 2000s. I was well aware it was all due for a fall in 2003.

We had some good times, the DHO Index (number of Dudes Hanging Out in RE listing photos) the number of “Cawlums” (columns) on the fronts of places, number of 8’s in prices, we had all kind of inside, snarky, running jokes. Those sustained us as the bubble went on, and on, and on …. It finally started to deflate a little bit in 2007 and the SHTF in 2008.

How’s that line go, something about the market staying irrational longer than you can stay solvent?

I guess I did miss it or it didn’t crash the same in Canada. I’ve watched the price of houses double in the past 7 years.

Yes, you’re right. You would have missed it in Canada. That should have been my first question: “Do you live in Canada?”

In Canada, there was no housing bust between 2006 and 2011. Canadian home prices just barely dipped for a quarter and then skyrocketed. That’s why the housing markets especially in Vancouver and Toronto are now in such precarious state.

I am also in Canada, when housing didn’t correct here I was both confused and disappointed. I sold my house in 2012 expecting a correction when the oil corrected and it took oil a couple years to pop, yet housing didn’t. All the housing in my area was propped up by oil money, oil money is gone and the housing is still insane. It feels like the moment in The Big Short when Burry is confused when prices wouldn’t correct, all the signs are there but nothing happens. Americans and Canadians now report amazing job numbers in January, yet horrible savings numbers and debt numbers. How? Why? No one knows.

Wolf, a lot of us are waiting for Crash 2 actually. I have two well educated professional millennials living in my basement because they can’t afford the housing in San Diego. They were not in a position to purchase during the last downturn in housing. Now they are ready, and so am I!

If it is coming, someone is doing a wonderful job hiding it

Maybe not very much happening on a global scale, but, Stockholm is going down. Prices have dropped 10% since may 2017. Some experts estimate that the market could go further down – with about 25%.

Iceland is very bubbleicios too. They will manage to pull the same stunt they did last time. Not quite there yet, but soon. My Icelandic barber is talking a lot about investments …

Ever hear of McCaffee computer protection software?

The guy became a multi-millionaire and then just before 2008 he built an estate for about a hundred million or so.

Lost almost all of it in the RE crash. Got out for pennies on the dollar.

Once the infrastructure bill is signed and the Wall gets built, there should be enough money to do extend and pretend for another couple of years.

Anytime Bill Gates walks into a restaurant in Seattle the average net worth of everyone in the room is in the millions.. I’d like to be there just once to feel what it’s like to be rich but I don’t know if I could take the poverty once he left.

The problem with statistics is it takes a statistician to unravel them. If 70% of the people can weather a 3 month financial loss of income, some with their own money and others borrowing it, it seems counterintuitive that 44% can’t raise $400 bucks.

If I looked on the sunny side I might think that with jobs seemingly opening up, people with jobs or the newly hired are borrowing again but from what I’ve seen in the Seattle area, jobs outside of tech are paying less than they did 5 years ago. Friends of mine who were working up to 3 part-time jobs are now hired on fulltime but the pay won’t cover the rent so are doubling or tripling up. Some of them have taken on a bit of debt for car repairs but the idea of savings died long ago..

That is why when it comes to income anyone worth a damn looks to the median as the high earners skew the averages. Give me the median income growth YoY, then let’s talk.

Otherwise, just statistical masturbation.

Wolf, what is the median income growth rates, both gross and discretionary? I would guess that the drop in savings rates should be even worse that the published numbers.

If we listen to Trump on immigration then it should help those workers in the lower echelon, who lose earning power when they have to compete with new immigrants. And on the other end new immigrants in the upper echelon, high tech workers, will make the top earning group more competitive and spread out the wealth a bit more. There is nothing to stop the 1% from moving up log scale, (.001%), and that helps as well. The solution is to emancipate the robots and tax the living hell out of them!!!

We were not in the lower echelon but in decent paying union jobs. My friends and I worked in manufacturing and didn’t lose our jobs to immigrants but to runaway outsourcing to whatever country paid the least. People with capital made those decisions that it was better to abandon the US as a manufacturing base and import back their own finished goods at the same price with a much higher profit margin. Once it became a general rush to the world’s cheapest sweatshops prices did fall but what they are now coming to realize is they not only abandoned US manufacturing but have impoverished their US customers..

As far as foreign hi-tech workers helping spread the wealth, I have to question that. Microsoft programmers, during President Bush’s last run in 1999, were losing their $120,000 jobs to people with better degrees from India Institute of Technology. Some were coming to WA and others got outsourced jobs back home doing the same work for $20,000 and living well. The savings in pay didn’t go to those who punch a clock..

Living well in India is a misnomer. Go there and find out for yourself. It is filthy and crowded and mostly lacks basic infrastructure like clean water. Streets are lined with trash as are the waterways. Even though $20,000/yr in India might be a lot of money, it is still a terrible lifestyle.

The techs living on $20k in India are living in gated communities with servants..

The whole point is the $120K Microsoft programmers in 1999 were replaced by those making 6 times as little.. The Amazon techies today making $60 per hour (on average) will be replaced by those making far less. It won’t matter to them if their replacements live in India, Russia, or wherever. The yuppie kids getting their first taste of real money when they come to Seattle are probably good programmers but have no sense of history. Certainly not economics history because if they did they’d be salting away all that they could because if history has taught us anything is capital is always looking for ways to cut and labor is always the first and easiest way to cut.. Even if it’s intellectual labor because programming can be taught as easily as any other skill. It doesn’t matter where the programmer lives as long as they do it cheaper..

I’m livin the ‘sh!thole’ life, after early withdrawl from the workshift grind (no pen$ion, no perk$ .. but also no MORTgage), as I daily collect the poop from the laying hens … to deposit into the compost bin, collecting honey from my bees, and workin my boney fingers to produce at least some sustainence on ‘ol the suburban farmstead. So as things continue to get hinky, and where other people are jumpin out of tall buildings in a single bound, I’ll only have the single-floor window to negotiate !

Trickle down… doesn’t

But pumping up does, at least for a while…

The Federal government is the final arbiter of unemployment. [After all, no government = no unemployment]. They simply have to decide what level of unemployment they want. Post WW2 it was 2% right across the West.

Then create the jobs and get people working again. There is never a shortage of jobs and the government can also start projects where the private sector employs more people. More employment means more spending into the economy and more wealth to distribute. This is the best way forward. The money to pay for it comes from spending itself.

Government does not create jobs that create wealth. My father told me “government is just another form of welfare.”

The government creates many jobs that save your life. Without life you cannot have wealth.

How I Learned To Stop Worrying and Love the Deep State….

No, sorry, your Dad was incorrect … government now is a matrix of mafias

People remember the good times as the ’50’s and ’60’s. The government was very active in the economy. The Federal government managed unemployment by increasing spending on infrastructure and the military as needed. Then taxed much of that spending back. The high level of confidence in the future allowed the working class to spend freely, which allowed the entrepreneurial class to flourish by creating new and innovative products.

Exactly the opposite of current ideology, and hence an opposite result.

Granted about he ideology, but all that was 70 years ago, and the global resources available for expansion were almost untouched. We are not so fortunate.

In the 50’s and middle 60’s ALL US competitors were either flattened, broke, or in the UK just broke and partly flattened.

As a result at the high point the US was making over 80 percent of the WORLD’S manufactures.

The largest single mistake made in analyzing US manufacturing losses since then is not realizing that Germany, for one, which invented the 4 stroke gas engine, the car, the spark plug, fuel injection, etc. etc. was not just going to sit there amidst the rubble.

(Although at first many men were so depressed that it was women who first began clearing it)

Similar story with Japan and now South Korea.

The fifties were fun but no permutation of government versus private enterprise can bring back a situation where the US wins because it’s the only player.

Perfectly said. We got lazy and are continuing that long tradition. But now added fat AND lazy. Generally speaking.

Hummm, Did a bit of research Regarding your suggesting the impact on the extension of credit having to do with J6P (Joe Six Pack) chasing boobs and beer … Looking into world wide sales of bras (directly connected with boobs) the world sales of boob supporting devices amounts to over 18 billion per year. Looking at Victoria’s Secret I noted that unit sales per holiday season in USA average 400,000. American women on average own 9 of the devices.

Now unless the transgender phenomenon has progressed far more than I have noticed, I believe it is fair to say that the overwhelming majority of males have no use whatsoever for such devices. Therefore, I am confident that it is fair to state that while I agree with you that there is considerable fixation on boobs in this world, it is not Joe or Jim or Jake inebriated or not, who is responsible for the credit extension you find concerning … it is in fact women. Perhaps you disagree? Then might I ask you to unbutton that blouse now and look at your very own boob supporting device. Did you pay cash or use credit card? Please answer I need the info for further research.

You saying that women are the ones fixated on boobs is like saying that men are fixated on work. Each is a means to an end….or have you not heard of tit for tat?

Hirsute,

It would be more accurate to say that one is the means to the other….

Wolf,

Why do you publish comments like this?

The question really is why would anyone save? It is all about consumption now and savers are treated like village idiots. How many trillions has the Fed taken from savers over the last ten years by suppressing interest rates?

I grew up in Europe where the need to save was drilled into little kids. Banks would hold annual events to encourage savings. Every one had a savings booklet. My grandparents lived through the 2nd world war and the recession before. Everything was saved: big balls of used rubber bands, buckets of old bent nails, etc.

We have come a long way in a couple of generations.

“The question really is why would anyone save”?

Exactly. Thats why the baby boom generation retiring now and soon those coming after, are going to be in a world of financial hurt.

All those with healthy 401K’s expecting to receive 6-8% returns on their pensions during their retirement, are living a fantasy when they think; “So why save”?

After 9 years of zero interest rate policy and stealth inflation, all pension schemes/plans now have very serious unfunded pension obligations. Some estimates as high as $5 trillion! To say nothing of those pension funds investing in high risk assets, as they are forced to chase yield.

When the crunch hits, these so-called “assets” will be among the first to find their true value – zero or close to it. Say; Good Bye pension.

There’s an interesting book out by Jessica Bruder “Nomadland: Surviving the Twentyfirst Century in America” about retirees and near retirees, living in RV’s, Trailers, Vans and cars in the USA. They are houseless, not homeless as Bruder notes.

Their social security and pensions (if any) will not pay for current housing and other costs and many of these folks travel the country from low wage job to low wage job, including Amazon’s warehouses during the holiday consumption frenzy.

This is the new Grapes of Wrath, with 21st century style migrants.

Why? Mostly it is the loss of assets and the inability of elders to get full time permanent jobs, after losing them in the Great Recession. Also, losing houses, and living paycheck to paycheck over the last 7 to 10 years, medical crises as well. After working a lifetime, they are still working, only now at minimum or near minimum wage.

These are not lazy or stupid or uneducated people, however, many are poor, many are women. This is a structural problem due to the insufficiency of income relative to the provision of housing, food, healthcare, and other necessities (cellphones and internet ARE needed to get jobs).

In other words, WAGES/SOCIAL SECURITY ARE TOO LOW to cover minimum living costs, let alone covering savings.

Obviously, these are not big consumers except for gasoline and auto parts.

Apparently, this group of hardworking souls is now considered a wonderful resource for employers as an at-will low wage temporary labor pool, that self-funds traveling to jobs, and with no benefit costs; ain’t America grand?…but for whom?…there’s the rub.

Now if the 75 year old working next to you at Amazon keels over, have a little sympathy, it might be you one day, unless the robots take over too soon.

Personnally, I think I will look into a used Van or Winnebago, just in case.

The wonderful Richard Wolff in his Economic Update (look it up on YouTube) mentioned last month that the sales of camper trailers last year went through the roof – something like 100% increase.

It is not a coincidence, it is a real trend.

Great comment. I grew up in a similar fashion but still live in Europe.

I can’t stop trying to repair stuff that breaks instead of tossing it in the bin. I still save instead of borrow but feel like the last of the mohicans doing so.

I stare in incomprehension at people buying 1000 euro smartphones destined for nothing but the garbage can in 3 years.

I gape when people trade in their car because the built-in onboard satnav no longer receives updates.

I wonder why the foodstuff that I bought in a brown paper bag or old newspaper when I was a kid now leaves me with cubic meters of plastic thrash.

I shake my head at modern cars loaded with electronics that effectively limit the life of the car to the period that the manufacturer deems economical to produce spares.

Yep, we certainly have come a long way.

And I wonder how much farther we will be going… before the whole edifice comes tumbling down.

I am also in Europe. Grew up in Sweden, then UK and now Switzerland since a long time.

From 1926 to 1963 the had a comic strip in Sweden that was widely read. It was about two girls that was literally named “save” and something that (sort of) translate into “over consume”. Everything always worked out for the girl that saved and went bad for the other. This very much reflected the moral of that time. To not save was really looked down on.

But now everybody has a massive mortgage but no liquid savings. The UK is the same. Switzerland is lagging behind but is also moving in the same direction.

People are also getting fat and unhealthy across Europe. It is depressing. It feels like the West is dying.

Savings?

One local Italian bank (of the effectively bankrupt, most likely deeply corrupt kind) has been plastering its province with advertisements for 1.36% EAPR loans for everything from cars to “consumer credit”. That’s noticeably lower than official inflation.

But look to open a saving account for a small child (be him a nephew, grandchildren or merely a friend’s child) and you get such miserable offers as to be embarrassed: 1.7% is the absolute best you can get, and that’s before “fees” are factored in. You are tempted to gift junk bonds to give these poor little things at least a scrap of yield.

I am not a gold bug and much less so a silver one (albeit I always carry a Spanish silver dollar on me), but in this environment I’ve found coins and jewelry to be the best gift in this “anti-saver” environment.

I tried to do this in Montana — went to the Savings and Loans to see what kind of college account I could open for my kid. Basically, they didn’t exist — I could put something in his name that earned about .9%. Go figure.

I’m curious how the data on savings and debt is compiled. If I save 5% of a $50,000 income for a couple of years I look good to the BEA. But if I then take my $5,000 in savings and and trade in my old car to buy a new one for $35,000 I have amassed a huge increase in debt and may show up as one of those who don’t have even $1000 to cover an emergency. But isn’t this exactly how most people operate? Save for awhile and then splurge on some big purchase and finance it with debt.

Wolf,

1st love your site

Wondering if you can comment on demographics as to how it may impact the savings rate. If Boomers are retiring in large numbers, would the draw from pensions/retirement assets not be expected to overwhelm the young folks savings that are fairly small early in their careers (not to mention the crappy job prospects they have)?

A lot of Boomers are retiring, no?

Demographics play out over decades. So if I comment on demographics once a decade, that will keep everyone up do date :-]

Boomers are now between 54 and 71. Many of them are in the prime of their lives. Many of them keep working. Many of them have recently started new businesses (including me). People who want to see boomers move on to the happy hunting grounds and cause the housing market to crash or whatever need to be very patient.

Not many boomers have pensions in the classic sense (not many people do). Boomers are the first 401(k) generation. And they have IRAs. And bank savings products. If they withdraw money from those accounts to fund their retirement, if they’re retired, this money will prop up the economy….

OK, this was my current boomer update. Next update is due in ten years. Stay tuned :-]

I would hazard a guess that a portion (?) of those boomer’s are what you would call; ‘House rich and cash poor’.

I am a 56 year old boomer who is cash rich and house poor. As in, I am a renter with a substantial nest egg. Not sure if that is a good or a bad thing.

Wolf, as you know I’m old and probably wont be able to update you on my view of life 10 years from now. But I thank you for letting me publish it here, every six months. For the curios one or two folks who can’t wait for the end of this six-month’s hiatus, it’s the same-old, same-old. I’m one of those on a “pension in the classic sense”.

But I talk about how I enjoy what, to me, has been an independent, happy life. Money, credit and banking aen’t prominent.

My Mom is in a static state also. but of a more advanced kind. When she asked me how the view was at the cemetery lot I bought for her, I told her all the lots had the same view from six feet under.

For all the yearning and wrangling about this-and-that, we all end up in the static state, after all.

Last I read savers are seeing very little benefit from the rise in interest rates. Debt up a lot and savings rate crashes around the time interest rates rise. If small rises in interest rates are causing this many problems, even us pessimists may be underestimating just how poor so many Americans are today.

With skyrocketing healthcare/education/housing prices…it isn’t surprising people are poorer than they realize – especially since wages (after accounting for inflation) have effectively been frozen for decades.

Democrats are no different than Republicans. They gave up supporting the working class under Clinton. They are a subsidiary of Goldman-Sachs today.

I’d be curious how the savings rate distribution breaks down by income bracket. For example, how many young couple’s making $130k a year are spending as fast as they are making money to maintain a certain illusion of success.

The US trade deficit have grown to 3/4 of a trillion dollar, half of it

with China, while the USD collapsed in one year from 104 to 88.

How is it possible.

Who are doing most of the buying.

Are the lower 60% – 70% so careless, getting into deeper debt, because the 2008/09 debt forgiveness taught consumers the wrong lessons.

I do not know if you are old enough to have gone to school in the 50-s. I can’t believe I am . . .

The grade school handed out cardboard folders for coins, dimes, I think I remember. Coulda been quarters, too long ago. We were encouraged to fill the folder and then at some point trade in a folder ( or folders ) for a 25 dollar savings bond. The bond cost $18.75 or so, then hold to maturity.

https://forums.collectors.com/discussion/804845/dime-saver-folders-history-of

POINT BEING, America was just transitioning to becoming a nation of “consumers” ( are we not “citizens”?) which necessarily meant a national philosophy shift against the damned savers.

Looking at the children of myself, siblings and friends — it seems that people are born to be savers or spenders. BUT SAVING CAN BE TAUGHT, I am sure of that.

There was a psychology experiment where they put a treat (some kind of reward) in front of young children of various ages. They were told they would get two treats, if they waited some short time, or they could have the ONE treat on the table now. You can guess the results, some were savers, some were spenders.

THE POINT OF THE EXPERIMENT, which followed the children for some years after, that this test demonstrated with some accuracy the arc of the children’s lives. Being able to defer gratification is a strong predictor of overall success. Strong, not 100%.

We no longer teach saving — remember, after the 911 attack, Bush II told the “consumers” to go out and spend. (Boy, have we lost our way ).

I remember those…………

Find “The century of the Self” on YouTube. A 4 part BBC series if I recall correctly. It discusses how corporate think tanks over 50 years or so propagandized the population into being consumers and getting your self worth from the brands you buy.

Thanks, doing so now.

Robert

Here is the description :

https://en.wikipedia.org/wiki/The_Century_of_the_Self

You tube the whole series, separate parts

On Amazon as one DvD, new

I read a Bernays book on this transformation, can’t remember the title at this moment . . .

Marshmallows!

https://en.wikipedia.org/wiki/Stanford_marshmallow_experiment

“Vote in Democrats?”

How, exactly, does this help? Democrats and Republicans have more or less run the US identically since roughly the point at which Reagan ditched Stockman and his crew around 1982.

He who looks to politicians/parties for salvation will be endlessly looking in vain, methinks.

One aspect of the savings rate that I’ve never seen quantified lurks in the withholding tables which up to now the IRS has set at levels designed to provide the average taxpayer with a generous refund at tax time. In the process, the treasury benefits from a short term interest free loan. Everybody wins. Uh huh.

Now we read about $30, $40 or even higher increases in pay checks thanks to the new tax law. But what happens in April 2019 when its refund time? Negative refunds for all? And if so, how big? If anyone can some up with an answer, its probably Wolf.

Well, there are two separate issues, (1) is what will happen come tax-filing time, BASED ON THE NEW RATES? And that is dependent on (2) what the IRS has distributed to payroll entities as THE NEW TAX WITHHOLDING TABLES.

If they are in close agreement, and if people’s TAX WITHHOLDING DEDUCTIONS ARE STILL OK, then there won’t be an apparent “giveback” .

If the withholding tables DO NOT MATCH the tax filing reality, then anything can happen.

It’s all up to the IRS.

You are not wrong about the new tax bill having a bit of a surprise ending. I played with a tax calculator and saw some interesting things. If you itemize now, but will be affected by the new deduction limits, you need to adjust your withholding. If you have a lot of investment income you need to adjust your withholding. If you have a lot of kids you need to adjust your withholding downward.

The thing that this analysis doesn’t get at is how soul-crushing it is to live without savings. Here in Canada, I’m part of a housing co-op — to hear about the people who literally live from month to month, never putting anything away, always maintaining a line of debt (credit card, HELOC) that is maxed out, would make your toes curl.

My wife and I only survived the GFC from dumb luck: a combination of $30,000 in savings, AND her being Thai were critical. We lived with her parents in rural Thailand and saved our entire lump of money for emigrating to Canada 4 years later and getting established again. Without both of those we wouldn’t have made it. Now we save obsessively, you never know when something like that will happen again. If we’d been in debt, that would have been it. And, in the process, I learned something else — Thailand is a lot better place than North America to be poor in. It still has structures, family, village, economic, that mean that every person is just a little bit more than their credit score. You can find a place to live on your own, even build one; the weather won’t kill you. You can get a motorcycle and drive it without a license or insurance. There is no building code. To people living on the low end in Canada, these things dominate their lives. In the US, with no health insurance, things are far worse.

People don’t realize how terrible our society is for people with no savings — living month to month is a grinding, nervewracking affair.

And one thing your analysis is lacking in is how soul-crushing it is for these people to not always engage their consumerist instinct. Your case is a bit different I think since you actually HAD savings. 30K? That’s a lot more savings that 50% of Muricans for example. A LOT MORE.

Muricans no 1 goal in life is to live like the Joneses.

I agree — I didn’t say anything about this because I don’t understand it. In the house I grew up in, we had a single car from the time I was three until I was in high school; likewise with a television. Our furniture was minimal. Not buying a lot of stuff was in no way at all a hardship — it just meant we had less stuff. When there was something that we had to have — fridge, lawnmower, piano — my parents would look around and buy the highest-quality, most durable model they could find for an above-average price. Then we would use it forever.

I find constantly buying things, other than books, food, or music, kind of depressing.

The thing is, 30K is not a lot when you are looking at potentially never working again. Or to put it another way, it’s a lot when it’s in the bank and can be the foundation of a plan; but if you start spending it, you’ll find it’s not that much.

Agreed that 30K is not much if that’s your goal, but think about it. Those 50% worked like hell and have negative value to show for it.

A journey of a thousand miles begin with a single step. You have taken many steps whereas for most people, they borrowed the miles and now are so behind they will perhaps never reach mile zero again.

I too live WAY below my means. I save 70% of my after tax income.

>>”Thailand is a lot better place than North America to be poor in. It still has structures, family, village, economic, that mean that every person is just a little bit more than their credit score. You can find a place to live on your own, even build one; the weather won’t kill you. You can get a motorcycle and drive it without a license or insurance. There is no building code. To people living on the low end in Canada, these things dominate their lives”

How well said! Yes, life on the low end is dominated by struggle with those things – licenses, transportation, affordable home…

I also have thought exactly the same thing about Eastern Europe. I am intimately familiar with life with little money in the former Soviet block. What I tell my friends there that if they are going to be poor, it is a lot better to be poor where they are and not in the US.

The Dims are all about one thing only: Who gets to grift the most personal income off the political process. The Republicans are the same, except they care about their political agenda too, which the Dims consider to be totally unfair of them.

Interest rates are starting to climb in the US. Too little too late? Only time will tell.

Conspicuous consumption continues but will slow significantly in the next few years. I too have stories about folks driving cars and living lives than cannot remotely begin to support. Unfortunately, many of these folks today have enough cashflow (paycheck) and debt to support their current way of living but in the next few years, many of these people will transition from their middle class way of life into the lower class. It’s not meant to be an insult, but somewhere in their minds they either live in denial or have the need to have what their neighbors appear to have.

Forget the Jonses as they are up to their eyeballs in debt, fighting daily over the money they do not have and their kids are emotional wrecks due to their parents poor choices.

BTW, if you all want to save a few bucks, no need to purchase the “My Pillow” product that you see on TV. Just save like there is no tomorrow and no matter what brand of pillow (or mattress for that matter) you use while sleeping, that big next egg will improve your quality of sleep immensely.

We will call Janet or Powell and tell them to print more money.. That is what we have been doing since 1998 and creating bubbles – this country loves bubbles and slow and steady is not good enough anymore. Jeff Bezos’ net worth went up by almost 80B in a year – the faster and higher it goes – the faster and harder it will fall. All the gains are coming from stock gains thanks to all the central banks who are printing money and handing it to the rich. It is sad – they say there is no inflation – there is inflation – but they use the wrong parameters to measure it – it is in housing, rents, food, insurance and everything. The Fed and all central banks are blind.

I’m having to spend 25% of income on health insurance in 2018. I’m sure I’m not alone.

Savings?

From the article:

“Many households spend more than they make. For them, the personal saving rate is a negative number. This negative personal saving rate translates into borrowing”

There is another way for spending to exceed income: liquidate assets. That was mentioned in other contexts, but ignored here.

As a retired person, I’ve been doing that since 2013. It is the rational thing to do. It is what I planned to do. I may not the the majority of the people spending more than their income, but with us boomers hitting retirement, I surely am not alone in my behavior.