What caused the biggest jump since the Financial Crisis?

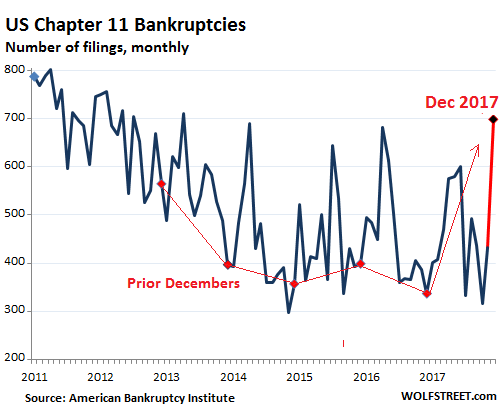

New Chapter 11 bankruptcies in the US more than doubled in December 2017 from a year ago to 699 filings. That jump of 362 filings from December 2016 was the largest year-over-year jump since the Financial Crisis.

This chart shows Chapter 11 filings back to 2011, based on data from the American Bankruptcy Institute. I marked the prior five Decembers with red dots. Note how they’re near the low point of the seasonal swings. That makes the spike in December 2017 even more spectacular:

A spike like this in Chapter 11 filings in a month of December is unheard of in normal times. Normally, bankruptcies jump during tax season, the first four or five months of the year, but not at the end of the year. But these are not normal times.

In December, Chapter 11 filings soared 61% from November. This is also highly unusual, as over the prior five years, presumably the “normal times,” the number of filings from November to December has fallen by an average 8.7%.

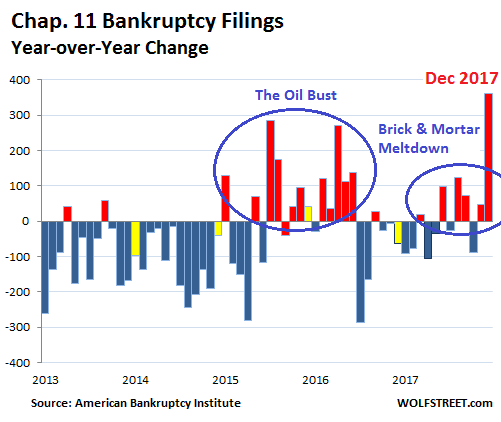

The chart below shows the year-over-year change in Chapter 11 filings. I marked the prior Decembers in yellow. I circled the oil bust and the brick-and-mortar meltdown. But December 2017 was special:

In a Chapter 11 bankruptcy, a company attempts to restructure its debts under the supervision of a judge, and in the process often transfers part or all of the ownership of the company from pre-bankruptcy shareholders to creditors. In many cases, shareholders lose everything, and some creditors too lose everything. But in the end, the hope is that the company can “emerge” from bankruptcy with less debt and keep going, with a reasonable chance the make it. So what is causing this brutal spike in December bankruptcies?

The Brick-and-Mortar retail Meltdown? We know brick-and-mortar retail is suffering, and bankruptcies have piled up in 2016 and 2017, and more will pile up in 2018, large and small, but they’ve been piling up all year, and the holiday shopping season is not the best time to go bankrupt for a retailer. It’s the best time to sell down inventory. The pile-up will happen in the first five months of the year, as it normally does.

The Energy Bust? The energy-bankruptcy wave is largely behind us, as the chart above shows, where the era bristling with red columns was concentrated around mid-2015 to mid-2016.

The horrendous spike in Chapter 11 filings in December had to have another cause. And it’s not that the economy is suddenly and totally collapsing, which it is not.

But I think companies and their owners and creditors know one thing: They can write off losses in 2017 under the old corporate tax rates, at 35%, thus getting the government to pick up 35% of the tab of their losses via lower taxes. In 2018, the new tax law applies and all kinds of uncertainties have yet to be ironed out, and these companies – the owners and creditors – are thinking (I assume) that it’s better to try to recognize the loss in 2017, support it with a Chapter 11 filing, and pull the write-off into 2017 against a tax rate of 35%, rather than 21% in 2018.

A tax-law change of this drastic nature motivates people jump through all kinds of hoops to save some money – including waiting in line for hours to pay property taxes early, a hitherto unthinkable strategy. And I think this is the likely suspect for the spike.

Brick-and-mortar retail bankruptcies will continue to pile up and perhaps pick up the pace from last year, and it will brutal for shareholders and many creditors. Many retailers will not be able to restructure under Chapter 11 and will end up liquidating, and it will be messy. But it won’t look like a continuation of December.

Total commercial bankruptcy filings – not just Chapter 11 but all types, including liquidation and for entities such as sole proprietorships – rose 2% year-over-year to 3,025, in line with recent trends, according to the ABI. But this spike of Chapter 11 filings in December looks to be a tax strategy. It better.

Is jacking up ticket prices helpful in this environment? Read… Brick & Mortar Meltdown Reaches Movie Theaters

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Nothing new here

Everything is awesome

Chapter 11 Bankruptcy also includes those individuals who are restructuring. When I used to deal with bankruptcies, there were more individuals filling under Chapter 11 than companies. This is not to say which are the majority, but just what I experienced.

I’m curious now what the historical trends are with regard to with the Chapter 7 numbers. I wish I was back in that world just to get an idea of the amount of relief the petitioners are seeking and what the corporate and individual numbers are compared to the last downturn.

I’m also looking for numbers on Chapter 13 vs 7 but cannot find current information

Chapter 7 filings down 7.6% YOY

Chapter 13 filings down 18.5% YOY

according to the ABI.

That said, chap 13 filings in Dec 2017 were up 17% from Dec 2014, the low point. And Chap 7 filings were up 5.5% from Dec 2014.

What about business trying to rebuild or realizing they cannot rebuild after a disaster ( like the hurricanes and fires in 2017- there were tons of people affected). Could they be filing for bankruptcy? This would cause the unprecedented jump in the end of the year rather than the first few months?

But…but…those corporate media talking heads have been telling us 24/7 that Everything is Awesome! And Janet Yellen and her gang of Keynesian counterfeiters assure us that there will be no new financial crisis “in our lifetime” and that our debt-fueled orgy of market speculation with printing-press “stimulus” is the sure sign of a booming economy.

Please read the article all the way down.

I think the key is here: “But I think companies and their owners and creditors know one thing: They can write off losses in 2017 under the old corporate tax rates, at 35%, thus getting the government to pick up 35% of the tab of their losses via lower taxes.” – Wolf Richter.

Second that. Also, the the curve is noisy, the conclusion would be totally different with smoothing.

Rat$?

Jumping $hip?

Unintended consequences. Now who wants to bet TO TV haven’t thought through many other non-intentional outcomes of QE wind down, balance sheet reduction?

This is probably just tax cut. The others will have bigger outcomes to ripple through the system.

Predict outcomes?

I’ve never been able to understand the term “Death and Taxes”. To me that is back the front. After all once your dead there are no more taxes for you. Maybe the family or relatives but not yourself. So shouldn’t it be “Taxes and Death”.

Even after you die, your estate will be taxed in your absence. So taxes can come before and after death, they found a way to tax carbon emissions.

Some people at least feel like they are immortal, but no one feels like they avoided taxes.

With companies and individuals in debt to such degree , it’s good to be a bankruptcy attorney.A bright future ahead.

I’d love to be basically this:

https://store.nolo.com/products/solve-your-money-troubles-mt.html

in human form. Not an attorney because I could never afford the college, but just an advisor. Sure tons of people buy that excellent book, but tons more people don’t learn well out of books, or they can read the book, agree it’s right, but they won’t actually do things without some sort of a coach. I’d seriously consider working for one of those debt-collection boiler room places if it meant I could advise people how to manage their money better. (I don’t know how that would sit with a boiler room operation though; “stop giving ’em good advice and just badger ’em!”)

A thought: perhaps all these maneuvers and shenanigans and the endless piling up of wealth by the top 1-7% of the population (it doesn’t go any deeper than that as everyone below that threshold is either standing still or falling back) is an unspoken defense against something Americans will not discuss–downward social mobility. Despite the stats that show that America has less upward social mobility than Italy, France, or Germany, Americans want to believe that this is “a land of opportunity” where each generation exceeds the economic standing of its forebears. But I smell a great deal of downward social mobility out there that is both within generations and between generations (that can’t be brushed aside by the age of the up and coming cohort–my dad was better off than his dad by the time he was 30 and that was true of most men who fought in WWII). The disgraceful hording of money and defense of every scheme and gimmick to keep it by those at the top may be an unspoken, desperate attempt to preclude downward social mobility at any cost (and the cost to society is getting prohibitive).

“Every scheme and gimmick” includes actual personal fortification and absconding to save one’s skin from the wrath of the hoi polloi.

Articles abound describing multi-milion dollar underground bunkers and refuges in New Zealand.

Hi Wolf,

Does it make sense to think of a corporate chap. 11 spike in the context of private equity and debt-laden balance sheets plus the impetus provided by tax “reform”?

Yes, it makes sense. It would have to be a corporate entity or a pass-through entity (tax rates shrink to 21%/20% after Jan 1) that takes a write-off from the filing to get the tax benefits. But I don’t know where these filings came from to confirm this. PE firms could have been big players in this.

The end of cheap credit? Just because cheap credit started to end in 2015 it doesn’t mesn the effects didn’t take a while to be noticeable.

It’s NOT a ‘tax strategy’ that allows us to evidence over 100% increases in Chapter 11 Bankruptcies, Wolf. This increase coincides with QE Infinity withdrawal, and the lack of potential to engage in stock buybacks which, as you know, has been the industry wide strategy to maintain share price throughout the Great Financial Crisis bloodletting. This bloodletting will NOT abate until the Second Law of Thermodynamics has processed all the overleveraged deadwood across corporate America. Furthermore, given that Greenspan et al. decided to ringfence all the toxic waste buildup post Bear Stearns & Lehman Bros. Chapter 11 Bankruptcy, we have no recourse but to witness increased filings for Chapter 11 Bankruptcy due to the fact that the Central Banks are no longer engaged in issuance of QE Infinity dollars for buybacks in order to prop up the failing corporate economic system.

It’s unfortunate that Paulson & Geithner failed to let all the deadwood burn off in 08, but they did buy the corporate sector, and BIG Government, time to ringfence their combined toxic waste over the last 10 years.

Now P.T. Barnum in the White House can start the three ring circus to Thermonuclear ‘Hot’ World War Three given that the Treasury Secretary has no more firing power in the corporate bazooka.

P.S. Goldman Sachs & JPMorgan Chase are now believers in ‘Blockchain Tech’, and even Jamie Dimon regrets stating that bitcoin was a fraud.

MOU

If the 100% YOY spike continues in Jan, you’re correct. And there is a chance this is the case. But I have not yet seen credit tighten up to the extent that it would cause that kind of spike. But we will find out in a month.

According to your chart, January and February are bumper months for bankruptcies, at the best of times, so it will have to spike a lot.

Blockchain to the rescue!

Fair enough, Wolf.

MOU

Does entering bankruptcy for a tax writeoff offset the negative effects on your credit?

I think you nailed it Wolf.The Job market is too hot for it

to be much else.

Other than perhaps six cities, the idea that the job market is “hot” defies belief. Where are the full-time, 20+ dollar an hour with benefits jobs that used to exist popping up like mushrooms? I teach three classes a year as an adjunct and they count me as employed. Yeah, right. If you work at Walmart or McDonalds for 20–35 hours a week, you are employed. Try and raise a family on that.

In short, check out the work participation rates, median hourly pay, and hours of work per worker before you tell us that the job market is “hot”.

Make sense. It the first signal before recession hit the economy in full force. Certain sectors always lead the charge.

A retailer will buy a lot of goods with with Jan 10 2018 terms, before the Xmas season.

They can get a lot of memo goods from vendors, to move in Xmas, with return for credit, due in Jan 2018.

When the retail goes busted, he takes suppliers A/R & goods with him ==> to the grave.

Every check they paid, to keep nervous vendors trusting, within 3 month of declaring BK, belong to the estate lawyers.

So, a vendor can lose his A/R, his memo goods and still have to pay

the estate lawyers.

That’s a lot of fun season. From the vendor point of view, entering a season like that require a lot of knowledge !

Banks financing retailers, also get hit. Vendors multi hits start a chain reaction.

The retailer who plan all this, can escape with some goods and cash, in order to start all over again one day.

The root cause is that there are fewer consumers these days. The middle class is dead. The only thing that is left is a small number of wealthy consumers and hoards of people that are barely getting by (or not even that).

There’s a reason why bargain chains like dollar stores are the dominant form of store these days. People have no money. I suppose at the high end there are a handful of booming chains.

Stores that once catered to a thriving middle class have lost their base. In the big cities meanwhile, the hedge funds, private equity, and other large investors keep driving up the costs of rent, which hurts retailer and consumer alike.

ch 11 are up 100%+ from a year ago. maybe it’s brick and mortar…nope. energy prices down…nope. new tax law…maybe influenced some decisions. december is usually one of the slowest months for this type of stuff (divorce, closing businesses, bankruptcies, etc) because most people want the kids to have a nice holiday memory.

why don’t we look at this in the broad context of EM loan defaults also soaring. home equity lines and loans defaults more than doubled in the last two months. subprime auto defaults broke out of their range of 2.5-2.7% and now at 3.25%. and the majority of student loans are not in default yet, but they are on one of several types of deferral (the bank agrees to hold collections until the borrower can prove he is able to pay).

in addition, rates are rising in america, QE is unwinding in EU, BoE is raising rates too, China just announced they might not be too interested in treasuries anymore, and japan is getting ready to slow their QE. take out the floor on the price of debt and remove the ceiling on the rate, and of course defaults and bankruptcies will soar.