One of the “bigger fears”: dip buyers get burned, turn into sellers, “get an exponential move to the downside.”

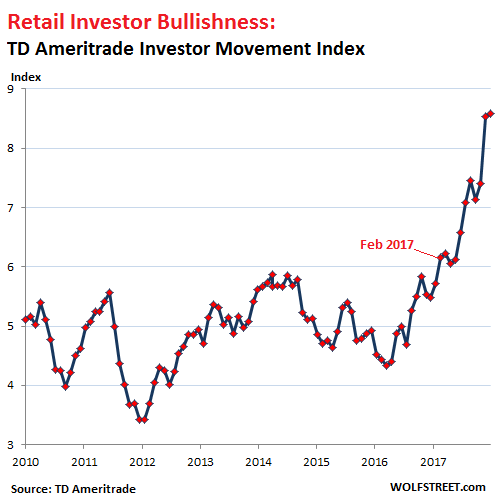

As far as the stock market is concerned, it took a while – in fact, it took eight years, but retail investors are finally all in, bristling with enthusiasm. TD Ameritrade’s Investor Movement Index rose to 8.59 in December, a new record. TDA’s clients were net buyers for the 11th month in a row, one of the longest buying streaks and ended up with more exposure to the stock market than ever before in the history of the index.

This came after a blistering November, when the index had jumped 15%, “its largest single-month increase ever,” as TDA reported at the time, to 8.53, also a record:

Note how retail investors had been to varying degrees among the naysayers from the end of the Financial Crisis till the end of 2016, before they suddenly became true believers in February 2017.

“I don’t think the investors who are engaging regularly are doing so in a dangerous fashion,” said TDA Chief Market Strategist JJ Kinahan in an interview. But he added, clients at the beginning of 2017 were “up to their knees in it and then up to their thighs, and now up to their chests.”

The implication is that they could get in a little deeper before they’d drown.

“As the year went on, people got more confident,” he said. And despite major geopolitical issues, “the market was never tested at all” last year. There was this “buy-the-dip mentality” every time the market dipped 1% or 2%.

But one of his “bigger fears” this year is this very buy-the-dip mentality, he said. People buy when the market goes down 1% or 2%, and “it goes down 5%, then it goes down 8% — and they turn into sellers, and then they get an exponential move to the downside.”

In addition to some of the big names in the US – Amazon, Microsoft, Bank of America, etc. – TDA’s clients were “believers” in Chinese online retail and were big buyers of Alibaba and Tencent. But they were sellers of dividend stocks AT&T and Verizon as the yield of two-year Treasuries rose to nearly 2%, and offered a risk-free alternative at comparable yields.

And he added, with an eye out for this year: “It’s hard to believe that the market can go up unchallenged.”

This enthusiasm by retail investors confirms the surge in margin debt – a measure of stock market leverage and risk – which has been jumping from record to record, and hit a new high of $581 billion, up 16% from a year earlier.

And as MarketWatch reported, “cash balances for Charles Schwab clients reached their lowest level on record in the third quarter, according to Morgan Stanley, which wrote that retail investors ‘can’t stay away’ from stocks,” while the stock allocation index by the American Association of Individual Investors “jumped to 72%, its highest level since 2000…” as “retail investors – according to a Deutsche Bank analysis of consumer sentiment data – view the current environment as “the best time ever to invest in the market.”

So we’re assured that absolutely nothing can go wrong, now that retail investors have become true believers and have put every cent to work in the stock market.

This comes just as the Fed has started to unwind QE, shedding Treasuries and mortgage-backed securities, as the ECB has tapered its QE to €30 billion a month, down from €80 billion, and as even the Bank of Japan, after tapering its purchases for a year, has actually allowed its colossal balance sheet to decline for the first time since 2012. Read… QE Party Over, even by the Bank of Japan

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

– I knew this already by looking at the 3-month T-bill rate (rising since mid 2015), and the yield curve (flattening) and other credit spreads.

– But now the 3-month T-bill rate seems to signal that investors are getting more cautious. It seems it doesn’t rise anymore.

– And it seems silver is also signaling increased (financial) risk/stress.

3 month T-bill doesn’t seem to rise anymore? Not from what I’m seeing. It’s recent trend line has been about 25 basis points every 2 months. Suggesting the Fed will raise the Feds Fund rate at the same rate.

People were saying after 2009 that no one would fall into the stock market casino trap again. They’d gotten fleeced twice and people wouldn’t fall for it again. I’m convinced now people really do have short memories. Assuming the system doesn’t radically change after the next crash I’ll know to buy at the bottom and sell just when everyone else is getting excited about the next bubble since they’re bound to fall for it over and over again.

See cdr’s comment below. It’s just one facet of the Fed’s financial repression. If you haven’t bought the dip since 2008, you’ve lost out. I am certain it will all burn down again, but I am equally certain that this buy-the-dip mentality and record low VIX can be traced back to our central banking masters.

Correct, short memories.

It used to be that the harsh lesson of a CRASH lasted a generation.

Americans have become get-rich-quickers, aided by current fads, such as TV idiocy, cell phones with instant, I mean REALLY INSTANT, communications, and other similar technology-engendered cultural spasms.

Few Americans save to consume anymore ( relatively few, percentage-wise ) and this mentality of “I want it now, without saving and without waiting” is our coming doom, already baked into the completed cake.

https://www.theatlantic.com/business/archive/2016/04/why-dont-americans-save-money/478929/

I’ll take some flak for what I have stated, but the evidence is there, and there are centuries of history proving this “excessive DEBT then BUST hypothesis”.

What lessons used to stick for a generation or more, are not sticking at all, now. Until . . . . .

BTW, the 47% that cannot lay hands on $400 for an immediate and unplanned bill, those were likely the same ones whose votes Mr. Romney conceded, up front. Maybe not.

Robert,

I don’t think that people have changed at all. We had a sweet spot from the late ’30’s up to maybe the mid-80’s, roughly 50 years, of highly regulated financial markets. There weren’t any real financial crises. People left the ’30’s into an era of heavily regulated markets, prosperity, pensions and other aspects of the golden age that gave them the opportunity to save.

We are kind of back in the 1920s now. Folks are working for low pay with little to look forward to in the future. And just like people in the 1920s, your only real hope is to hit it big by speculating. So they do.

Good points, well written. Sound analysis too.

The really bad crash of 1929 to 1933 was followed by America’s Golden Age, perhaps the post-war 40-s through the mid to late 60-s. Perhaps up until the Vietnam debacle.

There is a mega-crash fueled by mega-debt on the near horizon. (IMO, of course). If that is true, will it be followed by another American Golden Age — instead of a Chinese Century ?

The English Golden Age was much later followed by the rather Golden Age of Victoria, a time of relative peace and relatively greater English prosperity, as compared to the world at large.

https://en.wikipedia.org/wiki/Elizabethan_era

Will America follow the English example, or, go into the dustbin of history, like the Portuguese, French, Spanish and Dutch colonial empires, and their associated prosperities ?

History has much to teach us, as always.

Agreed.

The rules have returned to something closer to what they were before the regulatory reforms of the 1930’s. This makes well-placed people money but it’s dangerous for Joe Q Average investor, who won’t get a bailout if he gets too greedy or just incautious.

I agree you’re right on. And like previous forays into the market by the masses, they have bought in when the market is very high, assuming it is going to keep on going to new dizzying heights, and also assuming that it will decline slowly so they can get out before they lose much. I hope it works that way this time.

I suspect a lot more people will lose their retirement nest egg before this is all over.

Guys, I like all your wise comments. The more I see sensible and prudent comments here, the more I know the stock market is still going to go up.

Its like exhorting your teenage daughter not to go out with that douchbag guy; but the more you warn her, the higher the probability she runs away and gets pregnant with his seed. lol.

Its counter-intuitive, but like I said before, there’s still runway left since the masses are in stocks “only” up to their chest.

Think of selling when everyone is in it up to their eyeballs, and then some. Or sell when negativity-biased websites such as ZH or Wolf comments here start to become bullish or go silent.

If ye here, Salt-of-the-Earth types are finally convinced or go silent, THEN the time is ripe.

Perhaps, this can be a “Wolf Index”? I won’t be surprised if some hedge fund quants have some algo scanning text here for bullish/bearish/silent consensus, and feeding this into their trading bots. Wolf should try a wicked experiment, and post highly Bullish articles and comments for the next month and then see what happens to the stock indices ;-)

I’ll try my honest best to post prudent words of caution to help everyone protect themselves (because I really care for strangers?) but of course, no one will listen until it is too late; which is not so bad too, since my own portfolio can ride this higher if everyone does NOT listen.

That last sentence is to throw the bots off, or maybe its not? lol

Ok, let me try again. This time for real?:

I’ll try my honest best to post prudent words of caution here to help everyone protect themselves, but of course, no one will listen until it is too late.

Well

U would have had lots points to sell during this run up, no?

That is, Way too early

What makes u think gojng short now is the right time?

Anyway

It’s never that simple

Yes the humans r predictable

But the game is always different

The difference in this game was:

Understanding that the public or funds wouldn’t be scared towards gold / safety when the printing started

The FED wasn’t gojng to settle for anything other than a bubble.

And prolly

Being situated to profit from playing with other people’s money

As per always

I think people do have memories, this time when the sell off happens even your small hap hazard investor is going to run for the exits when the music stops.

1997-2001 bubble was built on tech. Tech is ‘real’

2005-2008 bubble was built on real estate. Real Estate is ‘real’

2014-2018 bubble is built on central bank credit. Guess what, not ‘real’

Rhodium, as a psychologist, I think it is not a memory problem but due to gambler’s fallacy. For example, “Fool me once, shame on you. Fool me twice, shame on me. Fool me a third time – you’re bluffing – I’m due for a jackpot.” There is also the fact that people who gamble vs invest need to get even because their serial losses put them in a deepening hole of growing desperation. Though the odds of a win can often be 1 in 100,000, not hitting the lotto 8 weeks in a row encourages magical thinking that week 9 is their jackpot.

Great news. Looking forward to buying the big dip. Nothing else to add. I’ve already said it all in previous posts. It’s going to be sweet.

Notes on 90’s day trader fad. Then it was essential to have a good (T1) connection, which cost a bit, you often had to go to a store to play, and players were putting up their entire investment capital which many lost doing split second transactions. This current generation of day traders seems far too complacent and while I like my connection I know the HFTs can eat my lunch any time they want. Fortunately for these newbies I don’t think it’s that type of market, but on the downside it will be hard if not impossible. I think the people who buy the dips and who buy the bottom will rue that day. Remember JP Morgan lost a fortune trying to buy the stock market crash in 29. The L shaped bottom, study it carefully.

“The L shaped bottom, study it carefully.”

No, I’ll just buy the dip. Algos won’t let it last long. In fact, the only way we’ll have a respectable dip is if an atmosphere of massive gut wrenching fear tags along. Such as people noticing the ECB is a money printing debt monetizing negative rate machine with no plan other than to keep printing money forever if it can. The Swiss will try to prop up equities with their printed money. They will fail with the big one but will try up to that point. When people notice these details, let the fun begin.

I’m going for distressed debt funds. They will be hit by liquidity issues, not credit issues. I’ll get the high rates and the capital gains upon recovery. My Roth IRA will get the rest, with glee.

Investors like Buffett have been waiting, they will buy the bottom and they will get slaughtered. The government was not nearly so big in 29, no SSN, no DOD, The institutions who are on the short side mostly will be able to call the shots and they will be holding onto what they’ve got as in their death paroxyms the USG vainly tries to claw back something. Or it could be all unicorns and rainbows like you say.

It’s my contention that this is exactly why the “wise money” (if such a term even makes sense) never got up and danced again with Chuck Prince after ’09.

The “L shaped bottom”, the “Bear market retracement bull trap”, the “cascading waterfall to the floor” – whatever term someone likes to use – /someone/ is going to eat losses that’ll end up being intergenerational and it’s the people who aren’t caught up with the noise of the here & now that intuitively know this, even if they cannot frame the situation eloquently.

I mean, just go and read Hussman go on and on about how they didn’t properly backtest their data against Great Depressionary outcomes and blah blah blah. The problem is that he’s wrong on this; or more specifically, he’s wrong on the emphasis. He’s wrong to apologize because it was (and still is) a very likely outcome and the gamble isn’t worth the outcome of having to stand in the soup-lines instead of surviving.

And yea, with all of the neoliberal fetishisation of austerity, punishment and allocation of resources such as medical care, education and basic necessities of life dictated by which eschelons of extreme inequality one happens to be (un)lucky enough to reside in – surviving at all is a very real question, fuck “money..”

I’m in your camp Ambrose even if it does feel like anyone out there with common sense keep getting trampled by clueless unicorns..

But one of his “bigger fears” this year is this very buy-the-dip mentality, he said. People buy when the market goes down 1% or 2%, and “it goes down 5%, then it goes down 8% — and they turn into sellers, and then they get an exponential move to the downside.”

Did he have a hammer in his hand when he said that? cause i thought i heard a nail screaming!

https://www.zerohedge.com/news/2018-01-05/its-most-hated-bull-market-my-career-retail-investors-sit-out-rally-pull-1-trillion

Who’s right?

Surely, most retail are now chasing Crypto.

Mutual funds are losing out to ETFs — and have for years — that’s the only thing the data in the linked ZH article confirms though the title and part of the text are misleading because they assume that ETFs don’t exist.

The data in the linked ZH article is about retail investors pulling money out of equity MUTUAL funds. According to the chart in the ZH article, the process started in 2012. And that is true. Why? Because retail investors have been switching massively from mutual funds to ETFs (exchange traded funds).

ETFs have surged because their fees are lower than mutual fund fees and because they can be traded like stocks.

So the data in the ZH article is not a reflection of retail investors pulling their money out of equities, but a reflection of the declining mutual fund industry for the benefit of ETF providers. This has been known for years. The ZH title and some of the language in the article are very misleading because they don’t include what retail investors are now putting their money into: equity ETFs.

Good points. Thanks Wolf!!

Thanks for this!

I’ve some of ZH articles and wondered had I just experienced a “If you can’t blind them with brilliance, baffle them with bullshit” moment? Because the ZH article would say redemptions keep exceeding subscriptions or something like that so why is the market rising, than the figures given showed the opposite as best I could tell…leaving me baffled with bullshit I guess.

They’re at the top of the list on Russian troll sites, they give you a bit of news and a bit of propaganda. Hey we are not alone in the world, but I don’t want Putin paying my rent while I suppose myself to journalism.

TINA must still be alive and well.

I’ll keep riding the wave. I have a long way to go until retirement and if it crashes, it will surely recover before I am of that age and if not, we’re all screwed anyway and it won’t matter.

“We are all screwed”. Surely that’s not true even during the depression. Some people kept on living well. Perhaps because they weren’t 100% invested?

Your entire post can be summarized as FOMO: Fear Of Missing Out. Heard of contrarian thinking and perhaps diversification?

Not FOMO here just staying the course which is the soundest advice for building toward retirement when younger. I max my 401k and Roth and put the rest into high interest savings accounts or more index funds. Even 1929 was ok if you didn’t panic sell.

Dare I mention it …. perhaps just a few bucks here and there put into that yellow shiny metal stuff ….

Good answer. The US economy is nowhere close to a recession by any metric you want to look at. Keep dollar cost averaging into index funds and don’t think about doing anything differently until the yield curve truly goes flat. 2018 will be another good year for equities, but maybe the last in this market cycle. Enjoy the ride!

The yield curve won’t go flat. Yields will continue to rise. Treasury yields have risen sharply at three years and below, and now are rising in the mid-range and at the longer end, with the 10-year closing in on 2.5%. There is talk of four more rate hikes this year. QE is over in the US, Japan, and the Eurozone. Some of the QE is getting unwound. But rising yields sooner or later hit stocks – there’s no need for a recession, and I don’t see a recession.

BTW, in March 2000, when stocks began to crash, the economy was strong. It was the ongoing crash that triggered a recession one year later.

Wolf, John Mauldin said the following: ” The Stock Trader’s Almanac tells us that if we end up on a high on January 3, an extraordinarily high percentage of the time we’ll be up for the year as well.”

That statement is a bit ambiguous i.e. does that mean high for the year, which is easy to do or more like the stock market ending positive which it certainly did. But looks like the stock market has a good chance of going up again.

Retail “Invstor” stong in Stock’s.

You know what this means.

Deja vu.

Could be a reverse, where a crash in the mark causes the recession.

Yes, agree, and that’s what I said — “It was the ongoing crash that triggered a recession one year later” — and that’s what happened in the 2001/2 recession. Maybe I should have said it more clearly.

10Y yield has been steadily decreasing from 1982, triggered by the change in regime instituted by the Volcker Fed. I don’t see that trend being eclipsed by anything going on now.

Well, it fell as low as 1.37% in July 2016. Now it’s at 2.54%.

The thing is, QE is getting unwound. That is a momentous change that hasn’t fully sunk in yet. But it’s starting to.

“The yield curve won’t go flat. Yields will continue to rise. Treasury yields have risen sharply at three years and below, and now are rising in the mid-range and at the longer end, with the 10-year closing in on 2.5%.”

Let me start in reverse. To be fair, the 10-year has touched 2.5% in 2013, 2014, 2015, and 2017. Only in 2013 did it manage to go appreciably higher, to 3% (Taper Tantrum), before plummeting to new lows.

As for the yield curve going flat, it’s flatter today than it was at the start of the year. So while you’re correct that rates are moving up, they’re moving up faster on the short end than the mid end… which will cause the yield curve to go flat. The 10-2 spread is about 50 bps right now… again, that’s the lowest it’s been since October 2007.

However, I do agree that we’re going higher in the short term at least, probably peaking somewhere above 3%, as long as yields continue to move up in the next few days/weeks. If they stall out, I think we’re going lower. The current narrative is optimistically divorced from real life, and we’ve seen it take multiple years before economic reality reasserts itself in the bond market, the Taper Tantrum in 2013 being the best example.

By the way, here’s some perspective when you listen to how the media talks about the economy– here’s a hint: they’re hopelessly bullish, and anything that is not seen as a major negative is celebrated as a huge positive.

“U.S. Economy Posts Strongest Growth in More than a Decade” – WSJ, December 23, 2014

Excerpt: “The U.S. economy is rounding out 2014 in a sweet spot of robust growth, sustained hiring and falling unemployment, stirring optimism that a postrecession breakout has arrived.”

I don’t need to remind you that a “postrecession breakout” had not, in fact, arrived in 2014. And while Trump is bragging about 1.2%, 3.1%, and 3.2% quarterly GDP numbers, let’s not forget that Q2 and Q3 2014 posted impressive rates of 4.6% and 5.2%, respectively. And yet… here we are today. Still in a malaise. Incomes still stagnant. Inflation still a boogeyman the Fed can’t find, and seems increasingly unaware of where it comes from in the first place.

Irony: almost three years later to the day…

“U.S. Hiring Reveals Sweet Spot For Economy” – WSJ, December 8, 2017

Excerpt: “The U.S. economy is hitting milestones not seen in more than a decade, marked by robust hiring that has led to low unemployment and a sustained pickup in output.”

I don’t think I need to remind anyone here that we are not, in fact, in an economic sweet spot today. But that is the narrative. That and “synchronized global growth” which would be laughable if it weren’t sad that’s we’re celebrating paltry growth worldwide like things are finally back to OK again.

Reality will reassert itself, and rates will go lower, eventually.

The Fed should do these poor frogs in the heating pot a HUUUGE favor and make the next bump half a percent. Then maybe they’ll get it.

I gather that a lot of these buy- the- dip guys don’t know that the Fed has been known to raise one whole percent at one time!!

And then did it again!

I don’t whether the guy who said retail ‘investors’ are chasing crypto was being sarcastic, but they might as well chase crypto as Amazon at its insane PE ratio. As for Tesla….

Yes, I vaguely remember in 1999 Greenspan was raising rates aggressively to counter the dot com crazy, my fear would be the new fed becomes lazy, just to keep Trump’s pro stock market propped up with crazy PE’s.

I think the market will eventually crash but I think it is more likely to be later rather than sooner. All the offshore money coming back plus the better corporate tax rates will likely keep the market going up for one more year. I fear 2019 more than 2018.

Seems like most investors have forgotten the fact that equities are basically a claim on future profits of a business. With valuations where they are most investors are not understanding that what they are effectively saying is “I am willing to accept in the future the most measly of income from the company I just bought a share of interest in”. So, valuations can not matter for a very, very long time… until that is, all of a sudden, they do! It’s how speculation works and it always ends in tears… eventually.

Now, some might say, “well, I expect earnings to rise robustly and ‘catch up’ with valuations”. Can that happen? Of course it can! But in order for that to occur, strong economic growth is a requirement. Unfortunately, the problem with this thesis is that real long term interest rates are signaling anything but strong growth ahead.

Anyway, somehow this paradox will get reconciled, the only question really is when.

“retail investors are finally all in, bristling with enthusiasm.”

The buy-high-sell-low approach to investing. Never thought I’d see the day when getting mugged on the stock market would become a form of entertainment, and yet, here we are.

Walter Map’s first rule of investing: gamble with other people’s money. Your own is too valuable.

Reminds me of Alan Abelson’s two rules for investing:

Rule #1: Never lose.

Rule #2: Never forget the first rule.

I might be crazy but continuing a crazy bull run does not in anyway make me want to dump all my money into a pure equity investment. At least anymore than is necessary to balance short term emergency funds and savings versus long term investment.

What’s the point of looking at a short-term sentiment chart? Might be nice to have a few recessions in there to get a sense for whether it’s a meaningful indicator. Margin debt, however, which you show a longer timeline – now that’s a nice bubbly indicator.

When it falls, people will be looking for cash. Problem is, people with cash won’t want to part with it. You’ll have to sell your stocks at a 50% discount to pry anybody’s cash away.

Maybe. The following is more likely:

1. Shut the stock market down for a couple of days i.e. the beatings will continue until moral improves.

2. Flood the market with so much cash to prevent deflation at any cost. Hyperinflation? Why not? Protect the wealthy at all cost.

Trump biggest talking point is the DOW.

What can he possibly tell you if the DOW will close Trump election

gap.

I liked Trump better when he was correctly calling the markets “a big fat bubble” and castigating Janet Yellen for the Fed’s monetary malpractice.

percent of americans invested in u.s. stock market is 53% per recent gallop poll, nowhere near the 67% peak participation achieved in july 2002, and up only from 52% last year. I just now looked it up at gallop news online. we are out of a 16 yr bear market [2001 secular downturn, then cyclical bull, then 08-09 secular bear down again, then cyclical bull, then 2011 downturn, then cyclicl bull, thenflat bear for 2 and 3/4 yrs from 13 to 2016, and now a true breakout. look at the long term chart. we only now star increase in the markets.t the clock for a new true secular BULL which began in 2016. [see charts at ciovocca capital on youtube and it will be crystal clear]. the same pessimism occurred in 1982 when Reagan’s new secular bull began, and went unabated for 20 yrs and a 900% gain occurred. the majority calling for a crash will be wrong, right now data shows only normal corrections should occur every now and then [and those are not pleasant by the way as it makes people worry and panic]. thanks, a. bona, m.d.

Unabated? lol Mmmkay…

It seems to me you are not saying anything. The stock market goes up over the long term, with crashes once in a while. That’s why it’s common knowledge that people should invest in index funds. You are nothing saying anything new. The bull has been on the run “unabated” for the last 80 years. lol

Well, probably a lot fewer have any money to invest then in 2002.

“Well, probably a lot fewer have any money to invest then in 2002.”

Invest??????

Customer of mine comes to me half way through a Boat refurb and says. I need you to Stop for a while

So I ask, why?

He says. I had the money to pay for the Job. But my wife took it to the bank of the casino and they wont give it back.

The howls and wails of these reckless and greedy speculators will reverberate off the heavens – victims, each and every one – when the long-deferred fiscal reckoning day shows up with a vengeance and smashes the central bankers’ Ponzi markets and asset bubbles.

Love your commentaries – very Biblical. I’m reminded of Jonathan Edwards’ fire and brimstone: “their foot shall slide in due time.” Just wish that I knew the “due time”…

Thank you, HowNow. While I have no idea if the Bible is the inspired word of God or Bronze Age mythology, or something in between, I read it regularly and believe that a lot of distilled wisdom of the ancients made it into those pages. I’m always struck, when reading Proverbs or Ecclesiastes, how apt so many of the warnings and admonitions are to our own time.

Be sure to check out “The Epic of Gilgamesh” if you haven’t already. And keep up the good (very eloquent) work! Your words are worth a thousand pictures.

Funny to read all these comments of people who apparently seem to have a deeply informed opinion and/or knowledge of the UNKNOWN. And by looking at the past, no less! Clinging to numbers, data, narratives and whatnot to try and control this lovely unknown. For pride, for greed or (actually more common than you think) for reasons of vanity.

Throw your darts, set your stops. Luck is blind.

Along the same lines:

“Cryptocurrencies are the ‘greatest opportunity’ to get millennials to trade”

https://www.coindesk.com/td-ameritrade-bitcoin-great-opportunity-to-get-millennials-trading

A perfect storm is brewing?

Yes, that was a stunning statement (but not surprising from a trading house).

Great site Wolf, enjoy it much. Thinking back 3 years, I think the comment section was like it is today. If I had taken your DCMFers advice I’d be 400 grand lighter in the shorts. Stockman’s DC all the time advice has got those guys buying in right now. Right when I’m setting my trailing stops much tighter and just surfing that big beautiful wave.

“Right when I’m setting my trailing stops much tighter and just surfing that big beautiful wave.”

Make sure you have a “No debt” account, and a small margin balance, stops cant always catch the knife, when it moves fast.

There is already an excess building up, only the industry refuses to divulge it, because it ruins their ROI. When will they find a solution for this cycle of complicity? Is THAT one of the topics of “behavioral finance” ever addresses? We are already “into” our next crash, but only insiders know it.

What was that quote from Bernard Baruch when someone asked how he got so rich? “By selling too early”, he replied.

I just hope I have the nerve to go against the chorus of the crowd telling me I’m crazy to be selling now.

“I just hope I have the nerve to go against the chorus of the crowd telling me I’m crazy to be selling now.”

If you are selling at a profit over costs and inflation, its never the “Wrong” Time to sell.

“…. retail isn’t even in the stock market yet”

M. Armstrong

Coming in late to this discussion, but just wanted to point out that nobody has brought up the effects of extrinsic disruptions to the economy and stock market as triggers for major stock market valuation drops.

WWII and the postwar period sure had lots of massive economic benefits for the US, too numerous to detail here. But one thing that happened was that marginal tax rates were cranked up to 90% throughout the 1940s and 1950s to pay for the war debt. This no doubt contributed to a prolonged period of mildly depressed (by today’s standards) stock market valuation with PEs in the range of 10-15.

Then in the 1970s, it was the various external disruptions to the US imports of oil from the Middle East at a time when US oil production had declined. The sudden rise in oil prices resulted in stagflation and caused a prolonged period of depressed stock market valuations with PEs dropping under 10! Wow, some of you young’uns probably don’t even remember a stock market like that.

Since Volker’s retirement, however, it has been nothing but easy money and steady asset inflation of the stock market under Greenspan and then Bernanke.

And, it wasn’t just the dot-com crash of 2000 that triggered the recession six months later. Remember September 11, 2001? It froze worldwide travel for months while the world figured out how to deal with the GWOT. That whammy to the world economy sure dropped the stock market, but PEs have still remained inflated compared to 100-year historical norms.

So, what’s next? How about nuclear war with North Korea? Or a Saudi-Iran war? Or a Democratic takeover of the House/Senate with resulting prolonged Watergate style hearings on Trump’s tax returns and Russian collusion? Not directly connected to the economy but very likely to make Trump’s Twitter thumbs get even twitchier.

With Trump and his twitchy Twitter thumbs right next to his Very Bigly Nuclear Buttons, anything is possible.