Leverage, the great accelerator on the way up and on the way down.

Margin debt is the embodiment of stock market risk. As reported by the New York Stock Exchange today, it jumped 3.5%, or $19.5 billion, in November from October, to a new record of $580.9 billion. After having jumped from one record to the next, it is now up 16% from a year ago.

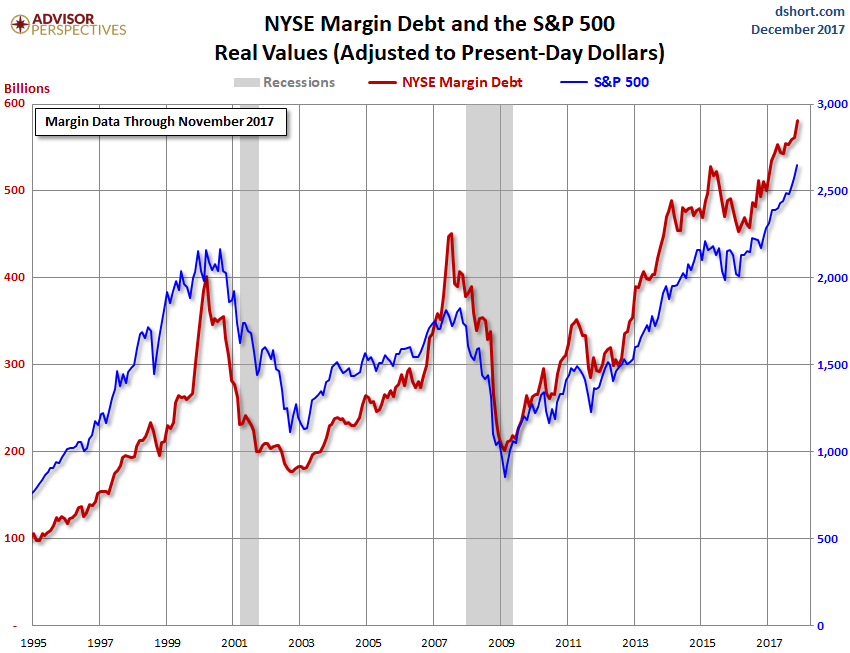

Even on an inflation-adjusted basis, the surge in margin debt has been breath-taking: The chart by Advisor Perspectives compares margin debt (red line) and the S&P 500 index (blue line), both adjusted for inflation (in today’s dollars). Note how margin debt spiked into March 2000, the month when the dotcom crash began, how it spiked into July 2007, three months before the Financial-Crisis crash began, and how it bottomed out in February 2009, a month before the great stock market rally began:

Margin debt, which forms part of overall stock market leverage, is the great accelerator for stocks, on the way up and on the way down. Rising margin debt – when investors borrow against their portfolios – creates liquidity out of nothing, and much of this new liquidity is used to buy more stocks. But falling margin debt returns this liquidity to where it came from.

Leverage supplies liquidity. But it isn’t liquidity that moves from one asset to another. It is liquidity that is being created to be plowed into stocks, and that can evaporate just as quickly: When stocks are dumped to pay down margin debt, the money from those stock sales doesn’t go into other stocks or another asset class, doesn’t become cash “sitting on the sidelines,” as the industry likes to say, and isn’t used to buy gold or cryptocurrencies or whatever. It just evaporates without a trace.

After stirring markets into an eight-year risk-taking frenzy, the Fed is now worried that markets have gone too far. Among the Fed governors fretting out loud over this was Dallas Fed President Robert Kaplan who recently warned about the “record-high levels” of margin debt, along with the US stock market capitalization, which, at 135% of GDP, is “the highest since 1999/2000.”

“In the event of a sell-off, high levels of margin debt can encourage additional selling, which could, in turn, lead to a more rapid tightening of financial conditions,” he mused.

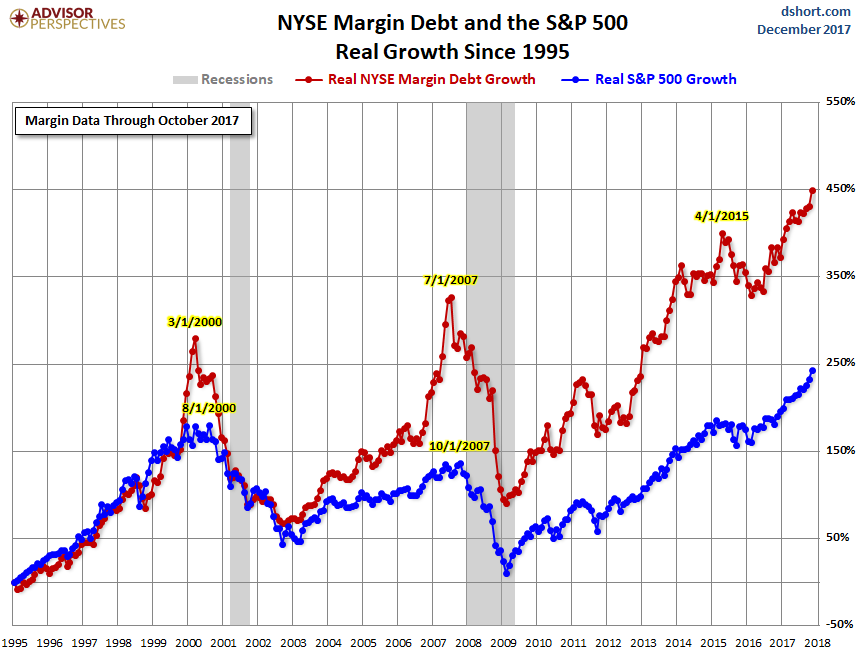

The growth in margin debt has far outpaced the growth of the S&P 500 index in recent years. The chart below (by Advisor Perspectives) shows the percentage growth of margin debt and the S&P 500 index, both adjusted for inflation:

In other words, the stock market is far more leveraged than it has ever been before.

Stock-market leverage, however, is broader than just margin debt. Stocks can be leveraged in many ways. Larger players, such as hedge funds, can borrow at the institutional level to fund stock purchases. Stock market leverage includes so-called securities-based loans (SBLs), offered by financial firms to their clients. These loans can be used to buy anything, not just stocks. But like margin debt, there are margin requirements, and when stocks fall, margin calls and forced selling set in to pay down the debt, which accelerates the rout.

SBLs are called “shadow margin” because they’re not reported in an overall manner and no one knows the overall magnitude. But occasionally, the risks they pose – though they’re considered low-risk – come to the foreground in a most spectacular manner.

This happened when the bankers of Christo Wiese — the former chairman and largest shareholder of Steinhoff International Holdings — suddenly discovered that almost all of their collateral for a €1.6-billion SBL they’d made to him had evaporated as the €3.2 billion in Steinhoff shares he’d pledged had gotten totally crushed, essentially to nothing. Now the banks are licking their wounds. Read… Margin Debt, Backed by Enron-Déjà-Vu Steinhoff Shares, Hits BofA, Citi, HSBC, Goldman, BNP

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Stock buybacks with borrowed money is yet another form of margin debt, and that margin debt is probably not accounted for either by NYSE numbers nore SBL numbers. So we have at least three forms of margin debt:

1. broker margin debt (BMD)

2. stock based loans (SBL)

3. stock buyback loans (SBBL)

Moreover, the NYSE is just one stock market. Does NYSE tally margin debt at all US brokers, or only as pertains to NYSE-listed securities?

Justme

You are seriously misunderstanding the difference between margin-debt and the somewhat less dangerous non-margin corporate debt used for stock buy-backs.

We agree non-margin corporate borrowing for stock buy-backs is generally (not always) a bad practice. If the stock goes south, the corporation can sit on the debt as long as they can service the debt.

The fundamental and material difference with margin debt is the US Treasury defines the required margin (currently 50%); if an account drops below that, the broker is quickly forced to obtain other account-holder funds or to sell some/all the position to restore the margin. Heavy margin selling combined with general price weakness can (and frequently does) vastly accelerate the selling, which generally further lowers the price.

FYI: brokerage houses do not have to allow as much margin as specified in US Treasury regulations. The current margin requirement is 50%, but an individual brokerage house could require a higher margin (ie more than 50%). Brokers generally do not do this for competitive reasons.

It is somewhat difficult for the Treasury to increase the required margin on short notice or by significantly amounts. However, the US Treasury could be much more proactive in slowly increasing margin requirements in obvious times of market stress. Unfortunately, the government hardly ever attempted to do this.

I think the main point was that stock buybacks with borrowed money are also a form of leverage, which further intensifies the fragility of the whole system.

The details you explained are not too relevant, from this point of view.

FYI. The Treasury does not regulate margin. I think It is the FED.

https://www.federalreserve.gov/bankinforeg/regucg.htm

Javert Chip, your response sounded preachy, condescending and was also not very accurate. There is no “serious misunderstanding” on my part. I know how broker margin, works, thank you very much.

That aside, corporate loans generally come with covenants, and a common such covenant is a debt-to-equity covenant that the debt-to-equity ratio must not exceed some number. That is quite similar to having a margin requirement on a conventional broker margin loan: When the stock price of a company is under pressure, so often is the equity valuation on the balance sheet. Hence the similarity between corporate debt used for stock buybacks, and a regular broker margin loan situation.

Sorry, but yes, you’ve oversimplified and should be less offended that Chip has given you some information you can use.

When a corporation like Boeing buys back a Billion dollars worth of stock to the benefit of its options exercising executives there’s way too many moving parts to the equation than an Occam’s Razor supposition it was margin debt.

justme

With all due respect, speaking as an old retired brokerage CFO, I stand by my comments.

Hi JC – thanks for posting – I always find your writeups interesting and informative! And thank you Wolf for cross posting DShorts graphs. DShort (Advisor perspective) has the clearest presentation of financial data of any style that I have seen on the internet.

think of margin debt as compound interest in reverse. think of zero interest rates of the way the banks gets back at you for leveraging the interest in your account. think of your stock market gains as compound interest you paid yourself as you leveraged up (self in the aggregate) being deposited in a bank account. how are the banks going to discourage you from sucking them dry, when rates are already zero? two answers, one they leverage up your deposits and buy stocks, (the circle widens) or they drop rates further, or they bail you in.

A – I’ve read the Fed has direct control over stock margin borrowing with tools to reduce at a moments notice

.

B – I’ve also read the Fed is concerned about margin levels and stock prices.

The Fed has not used it’s power to reduce margins. Therefore, I believe either (A) or (B) is not correct and can not be supported empirically.

“A” is a myth :-]

Not sure if you’re joking or not. Pardon me if I’m taking you at face value but shouldn’t…I could be wrong but I think the Fed change margin requirement any time I wants:

“That is why it gave the Fed power to control initial margin requirements in the Securities Act of 1934. As the table shows, since that time margin requirements have been changed 23 times. The requirement has been as high as 100 percent, meaning that none of the purchase price could be borrowed. Since 1974, it has been unchanged, at 50 percent, allowing investors to borrow no more than half the purchase price of equities directly from their brokers.

What Does Increasing Margin Requirements Accomplish?

Historically, the Fed has raised margin requirements to curb stock market volatility rather than overall growth of the market. Yet considerable research shows that margin requirements have no impact on volatility. The latest research, by Fed economist Paul Kupiec, concludes “there is no substantial body of scientific evidence that supports the hypothesis that margin requirements can be systematically altered to manage the volatility in stock markets.”

Nevertheless, advocates of higher margin requirements, such as economist Robert Shiller of Yale, argue that they are an significant weapon in the Fed’s arsenal. He feels that higher margin requirements can be an important signal that the Fed is serious about cooling an overheated market.

There are a number of problems with this theory. First, there is no evidence that increases in the stock market portend increases in inflation. As a December 1996 study by the Federal Reserve Bank of St. Louis concluded, “The pace of increase in stock prices is not itself inflationary, nor are stock prices particularly useful in helping to gauge inflation trends.” Indeed, during the 1970s inflation was associated with a stock market that was falling, not rising.”

https://www.frbsf.org/economic-research/publications/economic-letter/2000/march/margin-requirements-as-a-policy-tool/

the Fed used this last in 1974 which is to say it was so long ago it can be defined as “mythic”

timbers

Using Wolf’s charts, with (round numbers) $600 billion of margin debt, regulatory action to increase to required margin must be done in a way that does not unnecessarily set off margin selling. Generally this is done by giving the market significant notice (a year) to adapt to higher margin requirements.

Regulators could also ask for congressional approval to raise margin rates for new investments, while grandfathering in previously existing investments for a longer time to give the markets time to react.

Markets with billons of margin debt and trillions in equity, tend to react badly even to tiny changes. Think of an elephant being spooked by a mouse – the elephant isn’t afraid of the mouse, it’s spooked by what lurks just outside it’s field of view.

No worries . When asked if she has any concerns with flattening yield curve , Janet replied correlation is not causation.

That rejoinder is fine unless your policy is to influence the bond market, and all you have is correlation, and no causation (or efficacy).

Margin dept has been pointed to as the culprit that caused the great depression yet is let to run unchecked still today.A gradual increase in the margin requirements seems long overdue.If margin rates were increased in measured amounts it may ease the coming crash.

This market keeps trying to break and I think there are people behind the scenes trying all sorts of levers to break it. I think this time it’s not going to be margin debt, it’s that good friend of ours, Mr Bitcoin. I think Mr Bitcoin will be where leverage becomes dynamite.

Well done, Satoshi. Your coin’s intrinsic value may be zero, but the entertainment value and everything bubble busting value is certainly not zero.

People may want to think about shorting the market though. Coinbase simply shuts down when it can’t process those sell orders. I think in the next two or three years, the stock market might close for extended periods of time until “the animal spirit” returns.

We owe this wonderful, awe inspiring prosperity to one great man: Ben Bernanke. As he himself has stated many times we are all lucky that he led us, through his wisdom and courage, to previously unimagined prosperity. We should all thank god that he, as he so modestly puts it, had the courage to act.

Where would we be without all the trillions sloshing through the economy to lift ALL boats. Nay sayers shouted “you can’t print prosperity” but Ben knew otherwise and he had the courage to act on his divine knowledge. Now Ben has printed prosperity for all to enjoy without the inconvenience of sweat, toil and labor.

Borrow some money and buy some assets – the Fed says it’s o.k. – they just want you to enjoy a prosperous life. Apply for a 0% airline miles credit card – get a free vacation and use a cash advance to buy bitcoin, sweet prosperity!!! Thank-you Ben.

“economy to lift ALL boats”

That is such bullshit. rising tides can NEVER lift all boats as one side of the boats is on the low tide side.

Underwater mortgages? We know what happens with that. Underwater portfolios? Maybe there’ll be a run on passports.

Me? I’m buying into a concrete block business. I figure there will be a big upturn on those bricks used to break the highrise office windows so “investors” can jump out easier. Oh, I forgot. There will be a bail-in. It’s the modern era. It’s not 1929 anymore, Dorothy.

Just a waiting game… waiting for something to break.

Christmas was wonderful for retail by the reports I’ve read but people have little savings and incomes haven’t been rising.. so I it must be on their cards. More debt to add into the story.

Yet interest rates have not gone up yet as I would have expected with the .75bp raise by the FED and the slow unwinding of QE. Lots of money floating around still.. Easy credit abounds… To easy to borrow against any asset as in not only brokerage margin but also shadow margin fueling all kinds of speculative insanity.

So now we have a 1000 pages of new tax laws… That few if any understand. It appears to be a chaotic change for high tax states. Lots of other changes that there is no time to implement.

And all it will take IMO is almost anything to cause a sell off in stocks and then real estate.. Just a waiting game… waiting for something to break. To much leverage.

All the margin is on the short side, no?

Good commentary here and see the ominous signs of “irrational exuberance” fueled by margin debt, derivatives, and fools getting credit card advances at 22% interest to jump in too.

Any speculations how this unwind will start? – I see lots of scenarios, curious what others see.

Doug Kass has recommended moving to cash.

What kind of strategies are you guys using?

Regards

Full bitcoins and snapchat shares.

No, just joking. My strategy is simply to survive, as anyways my disposable income is close to 0 and I cannot save enough to invest.

I also learn german, a good move as a spaniard I would dare to say.

Difficult times ahead.

One thing to note from the above charts is that margin debt changes tend to predate a corresponding change in S&P 500 index by a number of months. So from a trader’s perspective, no point in trying to predict the market, just do what it tells you. Also of interest, is that in 2015 to mid 2016 – prior to the election, margin debt (as a leading indicator) was pointing to an increasingly imminent bear market. The surprise Trump win caused what might be termed an “extension” to margin debt expansion and to the bull market – which when it unwinds, could make it that much uglier. But at the moment, margin is still climbing strongly and now we have tax reform, like it or not, with the expectation of bumping corporate earnings and investment granting us another “extension”. No apparent end in sight just yet.

Oh, btw – considering the insanity of central bank policies around the globe – don’t assume their reaction to an imminent asset bubble threat will be ramping up margin requirements. They have exhausted most of their kick-the-can techniques, so these brilliant thinkers may go with LOWERING margin requirements! It would be entirely consistent with their 21st century methods.

The networth of the US like all balance sheets compares assets vs. liabilities etc. And while nominal debt in households, credit cards, student loans etc… must judge relative to rising asset base of private citizens.

Similarly, compare nominal margin debt total to total market capitalization of 3-4000 public cos. in US…Then what is your conclusion.

Market cap of the S&P 500 bloats during rallies and withers during selloffs, just like the S&P 500 index itself. By definition (the way the S&P 500 index is set up), they run in sync — and they tell you the same thing when compared to margin debt.

RV sales are peaking also…

http://www.rvia.org/?ESID=indicators

My local dealers are flooding the networks with ads. Deep discounts, plenty of inventory, I think its all real, and maybe its people downsizing to an Airstream. Did you see the CBS feature on Amazon part time workers who live (rent free) in their RVs which they park on the grounds of the fulfillment center. Pay is 10.50 and the seniors and others are lined up for those jobs.

…and property tax free.

While my property taxes have been inflating 5 to 7 percent per year to pay overpaid cops and firefighters and their pensions.

My pay up 0 percent.