But many mid-tier markets are red-hot.

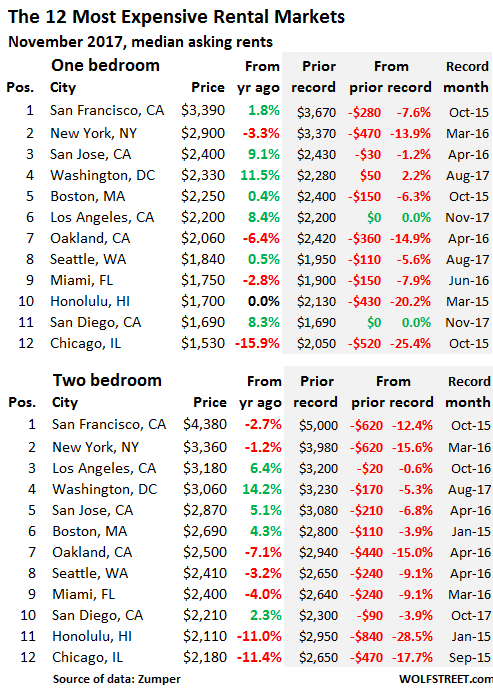

In San Francisco, the most expensive major rental market in the US, the median asking rent in November for one-bedroom apartments, at $3,390, is up 1.8% year-over-year, but is down 7.6% from the peak in October 2015. The median asking rent for two-bedroom apartments, at $4,380, fell 2.7% year-over-year, and is down 12.4% from the peak in October 2015.

In New York City, the median asking rent for one-bedroom apartments dropped 3.3% year-over-year to $2,900. For two-bedrooms, it dropped 1.2% to $3,360. Since the peak in March 2016, asking rents have dropped respectively 13.9% and 15.6%.

Oakland used to be red-hot as it attracted San Francisco’s housing refugees. But in November, one-bedroom and two-bedroom rents have dropped respectively 6.4% to $2,060 and 7.1% to $2,500. Both are down 15% from their peaks in April 2016.

In Honolulu, one-bedroom asking rents were flat year-over-year, and two bedroom rents were down 11% year-over-year. But from their respective peaks in early 2015, rents have now plunged by 20.2% and 28.5%. These are starting to be some serious declines.

The data is based on asking rents in multifamily apartment buildings, gleaned from “over one million active listings” that Zumper aggregated in its National Rent Report. Single-family houses or condos for rent are not included. Also not included are incentives, such as “one month free” or “two months free,” which effectively slash the rent for the first year by 8% or 17%.

The data includes asking rents from new construction, which other rent reports may not include. In many cities across the US – including in San Francisco, New York City, and Seattle (more in a moment) – there has been a boom in construction of high-rise apartment and condo buildings. These units are now showing up in large numbers on the rental market. Most of them are high-end, and landlords might price them aggressively to fill them.

In Chicago, the median asking rent for a one-bedroom apartment dropped 15.9% year-over-year to $1,530, and for a two-bedroom 11.4% to $2,180. They’ve now crashed from their peaks in September 2015 by 25.4% and 17.7% respectively.

In this table below of the 12 most expensive major rental markets, the shaded area indicates peak rents and the changes since then. Note the number of double-digit declines from their prior records:

In Seattle rents have been booming for years. But now asking rents are coming under serious pressure, possibly due to new units flooding the market as a result of an apartment- and condo-tower construction boom that has already become legendary. These landlords are likely feeling pressure to get their units rented out. But suddenly there’s a lot of competition. Zumper’s data includes asking rents from new construction. That might be one of the reasons for the decline in rents, with one-bedrooms down 5.6% from their peak in August 2017, and two-bedrooms down 9.1% from their peak in April 2016.

However, some other cities on the top 12 list saw large year-over-year rent increases, particularly Washington DC, where rents rose in the double digits from a year ago.

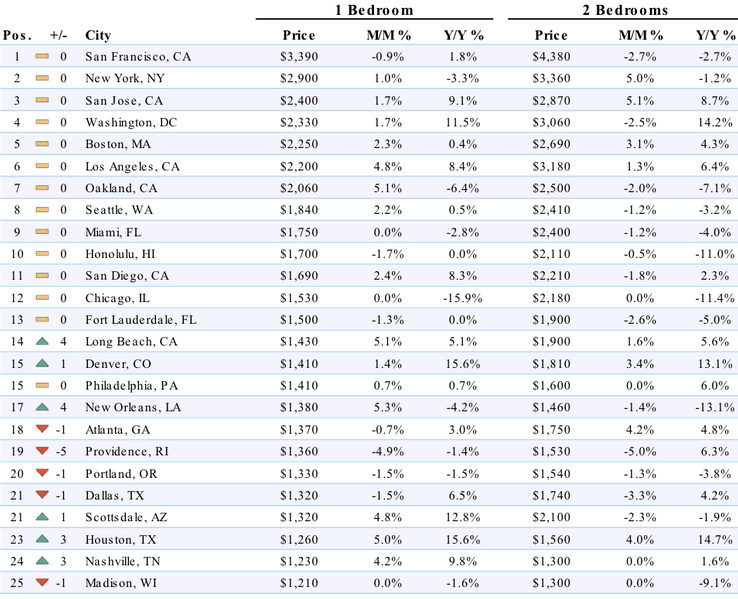

But rents are booming in some “mid-tier” markets – “mid-tier” in terms of the magnitude of the rent. Here are some with double-digit year-over-year rent increases (one-bedroom and two-bedroom apartments):

- Denver, CO (+15.6% and +13.1%)

- Houston, TX (15.6% and 14.7%), likely boosted by demand following the destruction of some housing stock during the hurricane.

- Baltimore, MD (15.7% and 9.4%)

- Sacramento, CA (+15.0% and +15.4%)

- Orlando, FL (+15.0% and 8.3%)

- Gilbert, AZ (+13.4% and 11.5%)

- Tampa, FL (15.8% and 13.9%)

- Or even Toledo, OH (+14.6% and 14.5%)

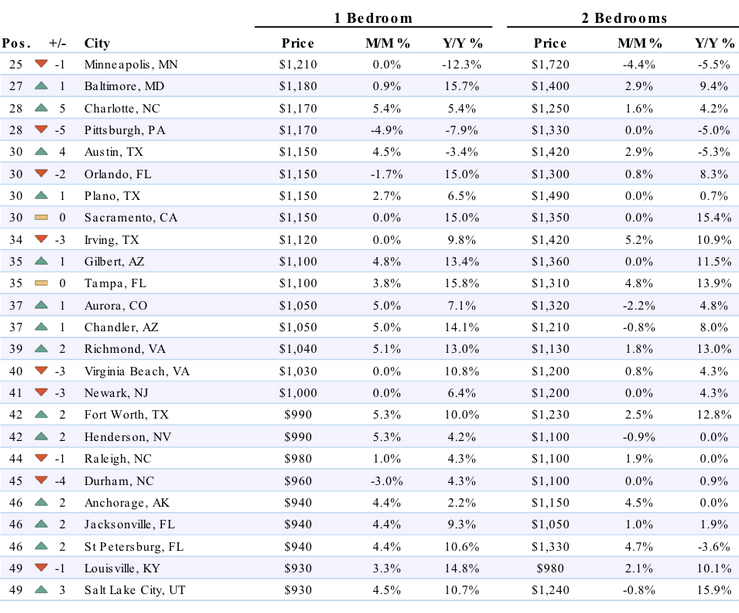

But not all “mid-tier” markets are still seeing rising rents. In some of them, the tide has turned sharply, including Minneapolis, MN (-12.3% and -5.5%) and Lincoln, NE (-15.3% and -12.8%).

In other mid-tier markets, rents are down more or less mildly, including Portland, OR (-1.5% and 3.8%); Madison, WI (-1.6% and -9.1%); Austin, TX (-3.4% and -5.3%).

So depending on where people live, their rents might be soaring. When rent is $1,000 a month, and the renter earns $2,000 a month after taxes, a 15% rent increase is painful and likely pushes the personal inflation rate into the double digits. It also causes the renter to cut spending on other items.

But even in a city where rents are on the decline, renters tend to have a hard time negotiating a lower rent at lease renewal unless they’re willing to move to a different apartment and boldly use that willingness as a negotiating tactic.

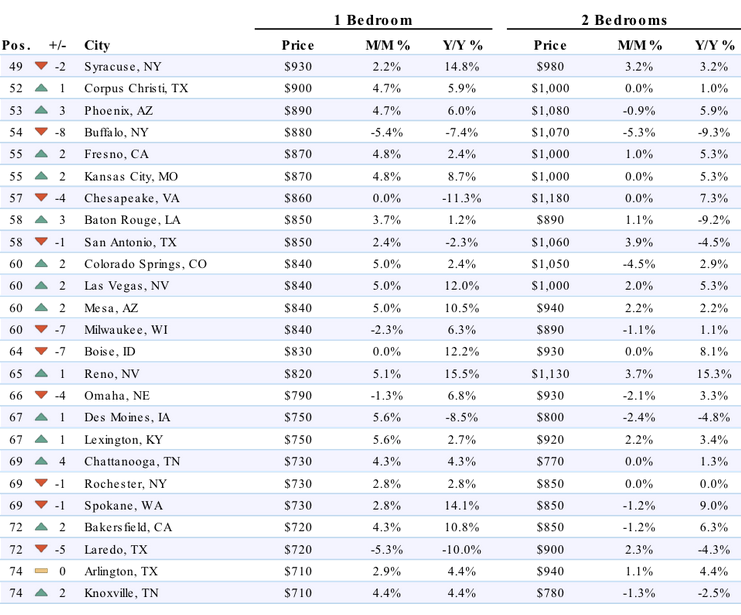

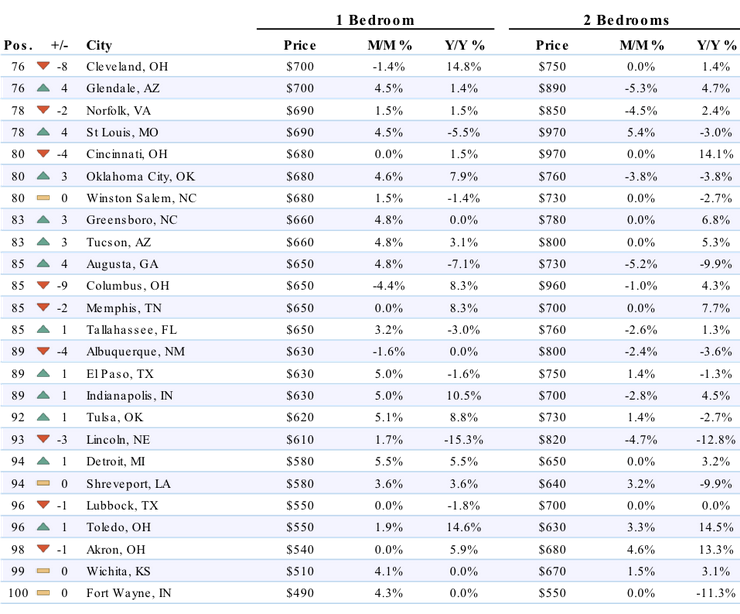

Below is Zumper’s list of the top 100 most expensive rental markets and price movements. Check out your city (click to enlarge).

The Case-Shiller National Home Price Index jumped 6.2% year-over-year. By comparison, disposable income, not adjusted for inflation, rose only 2.9%. This disconnect, year after year, adds up after a while. Read… The US Cities with the Biggest Housing Bubbles

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I just boldly used my willingness to move as a negotiating tactic and made good on the threat. I’m saving $350/month on a larger unit but in a less desirable part of town.

I was on the third floor. The unit below me has appeared empty for about month, and below that on the first floor, the family was moving out simultaneously with me.

My unit is now being listed for $60/month less than they offered me for lease renewal. I’ve also noticed “now leasing” signs getting progressively bigger and bolder.

East Bay Area here. Bring on the decline.

Can you name the city?

I live in Clearwater Florida which is a suburb of Tampa and I rent. The rent increases are puzzling. You would normally expect to see rent increases when there is a shortage of apartments, but there are a lot of vacancies both in the complex where I live and others around the area. That makes me wonder. It is one thing to set a rate, it is quite another to find tenants who can afford those rates.

I believe that many of the rents cited are in investor owned apartment complexes. The investors or more properly speculators, bought them with cheap loans. Many of those investors paid too much, but at the time it seemed OK especially because there were few other places to invest thanks to the Federal Reserves loony interest rates.

So, the rent increases cited may not mean much. A lot of complexes use teaser rates to fill their units but those are only good for a year. Then they are adjusted to full market rate and the tenants move out again. That leads to vacancies. Apartment complexes live or die on cash flow. Every time an apartment turns over after a year, the owners have to fix up and clean up as well as having a period when the unit is unoccupied and generating no cash flow. That cause me to think that rates will start falling here fairly soon

Just to clarify:

All the rents cited are in multi-family apartment buildings. They exclude rents of single-family houses and condos. So by definition, the rents cited are in investor-owned buildings. And these investors are often “institutional investors” rather than mom-and-pop investors.

The rents cited are “median asking rents”:

– “Median” means half rent for more, half rent for less. So half the units available for rent are listed with asking rents that are below the figures cited, and some of them quite a bit below.

– “Asking rent” reflects what landlords want for their units. They do not reflect what renters who have lived in their units for a while are actually paying.

You can check Zillow for their equivalent rent on a property, and how much it has changed the last month. At least anecdotally it might give you some idea.

JungleJim,

I’m in Tampa and it appears that the craziness may be about to subside. 3 brand new luxury apartment complexes just opened up this year and there are 4-5 under construction currently. These are all massive 500+ unit developments and they’re all over Craigslist advertising 1 month free. I saw 1 or 2 older (built 4-6 years ago) luxury places offering 2 months free just yesterday, so they must be feeling the heat from all this new square footage coming on line. The new med school being built downtown will probably save them if they can hang on until it opens in a couple years…

I know some one who halved his rent payments one month free one month paid then move two blocks over and start again.

When I moved to this area in 03, the free month was the 2nd month, because, they told me, people would live for free the first month then leave.

My rent went down about $50 the 2nd lease-signing, then it went up to the tune of about $400 so I moved to another complex that was walking distance away.

Then the economy crashed, I found someone to take over my lease and I was outta there.

Um, so what happens when that commercial real estate extend and pretend, plus surplus apartments happens?

Oh yeah, and all of those houses bought for rental that are really just disguised real estate speculation?

Just another day with not much progress….

in real inflation. Wages, baby.

Deader than a door nail in most of America.

vent Set Up/Strike Crew needed for Big Special Event in January! (Scottsdale)

compensation: Labor start at $13/hr; experienced rate starting at $15/hr

employment type: contract

Looking for:

Labor Hands

Leads

Minimal Rigging Experience

Labor rate starting at min $13/hr

Experience rate starting at $15/hr

Must have reliable transportation

Resume Required

January 2 through February 2

Send Resume to….

No Phone calls taken

So the big car auction event is hiring minions for the princely sum of $13-15 an hour- notice no overtime mentioned.

Sure going to support huge rents on that money, hey baaaby.

Someday this war’s gonna end…

The apartment boom across the US will overshoot; perhaps even significantly. The moral hazard from the last housing crisis (Fed buying up 1.25T in MBS) has changed the whole dynamic in housing.

Fannie/Freddie have been behind the massive amount of lending for these ubiquitous, ugly 4 floor with central garage complexes all made of wood. Developers get in and get out. Who knows who owns them or will be left holding the bag when rents collapse.

My theory (espoused here several times) is that support of this massive apartment boom was in part cooked up by Obama and team. When/if it goes bust, the Fed will again intervene. Only this time, it will be turned over to HUD and made into subsidized/free housing for the growing poor and seniors.

Can you please explain your assertion that “Obama and team” “cooked up the massive apartment boom”? I know a bit about REITs, particularly apartment complexes, and would like you to support your comment with some evidence. What did Obama’s team do here??? Wolf, if he doesn’t come up with any facts to support this, he’s breaking the rules for posting that you set forth, imo. You have an excellent forum with many knowledgeable commentators. I’d hate to see it run into the ground.

“cooked up” is a poor choice of words. After 2007 there were a lot of people thrown out of their homes needed affordable housing. (still do) What Obama did do, was to use HUD, section 8, to place minorities in foreclosed middle class housing, to achieve racial balancing. He also did the same thing with refugees, in places like Temecula CA angry citizens turned away busloads of these people. The housing bubble goes back to the Bush Home Ownership society. That turned out in reverse, while Obama and Holder clearly had an agenda they used housing to further their immigration policies.

I have noticed that new apts tend to be smaller than older apts. If you look at rents per square foot, I doubt the rents are going down. On some new listings the bedrooms are so small you cannot put in a large bed, and the kitchens don’t hold two people at once.

In New Jersey, to be legal, a bedroom for one person must have 70 sq ft of “usable floor area” – about 9 ft x 8 ft. Plus a window and a door.

I’ve rented in Tampa, Denver, Norfolk, St Louis, Washington DC, NYC. I have often wondered why landlords make no effort to retain good tenants. They behave as if tenants are identical interchangeable parts. I have always been an excellent, respectful tenant but landlords never make any attempt to keep me. The lease ends, they jack up the rent, I leave, over and over. They prefer to take a gamble on the next tenant.

Another thought: What is the effect of Section 8 on rents in a community. Cities will pay a landlord up to 3x normal rent. A wage earner can’t compete with that and gets shut out. What role does Section 8 play in rents rising in major cities?

Speaking for So Cal here, section 8 is actually getting shut out of cities where rents are going up. It’s getting harder for people with vouchers to find landlords who will take them. If a landlord has the option for anything near a market rate tenant with a job, they will choose that over a section 8 tenant due to all of the property damage that mysteriously follows section 8.

In a market economy, section 8 only works when landlords have to choose between them and a poor person with no gov’t backed voucher.

Landlords hold all the power that’s why. They can keep deposit money at will for crap they should have fixed during the term of the lease for example. If people started breaking their leases and giving the middle finger to landlords once in a while things would change. Case in point……friend of mine rented a nice 2 BR town home which before her had a tenant that was in there for 7+ years. Before my friend rented it the landlords raised the rent. My friend ended up purchasing a home and broke the lease. The landlords embarrassingly went to their old tenant begging them to come back because having a town home sit empty at $1800 in the middle of winter makes a dent in their profit, especially now that rents are falling here in MN>

In California, the market favors landlords right now but the law has always favored tenants. There are a lot of tenants’ rights and protections that can be abused. For example, the court process for evicting people can be really expensive and take months allowing people to basically live rent free that entire time. Also, it is not uncommon for tenants to use their deposit as last month’s rent which isn’t legal or fair. Basically, there are bad actors on both sides like everything else in life.

You need to find an owner like me with just a handful of rental units. Located 22 miles west of NYC in a good town. I rent at 10% under market and maintain 100% occupancy. Most of my tenants stay for more than 5 years. I know my tenants. If there is a problem, I take care of it immediately. They occasionally contact me with personal problems. I have a 4 year tenant who has been recovering from surgery for 6 weeks. She asked me if she could pay 2 weeks late this month. No problem. No late charge. Very nice family.

Prepalaw, your management “style” is something of a luxury, for you & your tenants. “Fair Housing” laws greatly restrict any leniency from managers since it can be interpreted as preferential treatment. There are fines, and managers who violate this law can be held personally liable for discrimination along with the corp that owns the complex. Procedures for late payments, eviction, cleaning fees, etc. are ironclad and must be followed to the letter for big REITs (their managers).

RM – I hate that. I’m the kind of tenant I’ve never met; the ideal tenant. Never been late paying rent in my life. I paint. I replace electrical sockets. I repair stuff. I was telling someone yesterday about the small office I rented in a small Arizona town in 1997, that I’d fixed up and painted and carpeted and so on, and 10 years later, in 2007, I visited it – it was a driving school – and marveled at how nothing had changed since I was in there; apparently I’d done a good enough job to last a while.

Is inflation flattening faster than the yield curve? I am getting a sniff of something here which tells me if you lock in the current yield on a ten year you might be very happy six months from now.

Simply change the rules on the fly and anything’s possible.

Banks don’t like lending while prices are falling, so good thing the FED is paying them interest on excess reserves so they have less incentive to lend. Otherwise banks would be forced into competition with cash buyers.

“We’re gonna rock on down to Electric Avenue. And then we’ll take it higher”

A number of Nationalities are out of favor in America

at the moment and are being asked to leave.This creates rental

vacancies and along with a larger supply of housing would

not be good for rents. As well if enough people do leave ,then

do wages increase for those remaining.

is

^^ The world’s most imbecilic haiku.

You obviously don’t know what a haiku is.

It’s a Trumpku!

Still too darned expensive in SF.

Kansas City is on fire downtown 97% occupancy and 4000 units under construction .The high end power light 1 sold rented out all their high end units first then filled up building a second building to quickly be followed by a 3rd .New show on diy called bargain mansions about a woman that flips old mansions in KC and now her biggest problem us finding these homes that 10 years ago you could not give away .

Your first chart shows San Francisco two bedroom with a 2.7% increase from a year ago while the Zumper lists shows a -2.7% decrease Y/Y% for a two bedrooms.

Thanks. Fixed.

Here in South Bay, Santa Clara area, I am far more comfortable with rents from a year ago. Now, there are good one bedroom apartments for under $1500/month. About 18 month ago, you couldn’t even find even an Studio at that price. So, from what I see on the ground, the rents have gone down considerably; so in a sense, Wolf, I disagree with the data, at least for San Jose; the data says San Jose is up 9.1% YoY; that can’t be since about 18 month ago, it was such a disaster. Now, I can easily find decent one bedroom apartments, in good parts of town, even under $1600; 18 month ago, you would have been lucky if you found a decent studio for that price.

Thanks for the update.

I like to say that every time the rent goes up another restaurant goes under. Can you imagine what would happen to this economy if rent on the average started to consume 50-75% of after tax wages, the entire economy would probably collapse as there would be no spare money for consumers to buy anything else.

Contrarily, the more rents collapse the more that stimulates the rest of the economy. So maybe a few investors are hurt by a rent collapse, but the economy as a whole is benefited.

Rents are too high now as a % of take home pay, there needs to be a major rebalancing. I hope that’s starting to happen now, but we’ll see.

Agree!

If rent were 50-75% of salary … there are places like that.

https://smartasset.com/mortgage/the-most-and-least-severely-housing-cost-burdened-cities

Interestingly Newark, NJ was the worst.

Only mortgages might be able to buy, but that depends on people being able to afford a downpayment.

There is also the fallout of the 2008 recession of course, which still affects us today and suppresses wages.

Still, if rents were that high, there would be money for food and not much else. Maybe not even food for many people.