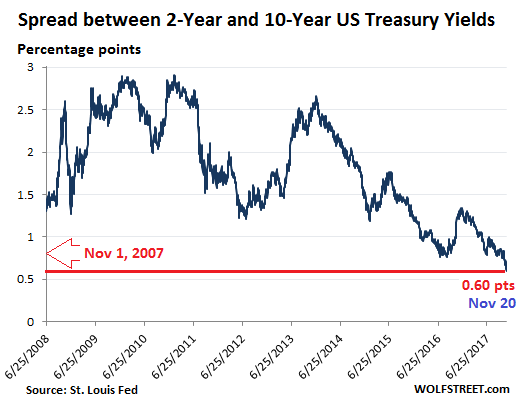

The yield spread collapses to lowest since 2007.

Prices of US Treasury securities fell across the spectrum on Monday, and yields rose. From the two-year yield on down, yields set new nine-year highs.

This sell-off – and the accompanying surge in yields – has occurred for months without downdraft in stocks and without a slowdown in economic growth. It’s a dreamy scenario where the Fed’s tightening has no negative impact on the economy. But the Treasury market at the longer end smells a rat.

Not for this year. But for later.

On top of it there comes a big bout of Fed uncertainty. Janet Yellen, who will be replaced next year by Jerome Powell as Fed Chair, announced today that she would also vacate her slot as governor on the Federal Reserve Board – a job she could have hung on to until 2024 – thereby making room for a fifth Trump appointee to the powerful Board of Governors. In early October Trump nominated and the Senate approved Randal Quarles as a member of the Board. Leaves four slots to fill on the Board of seven members. And no one knows what the Fed will look like next year.

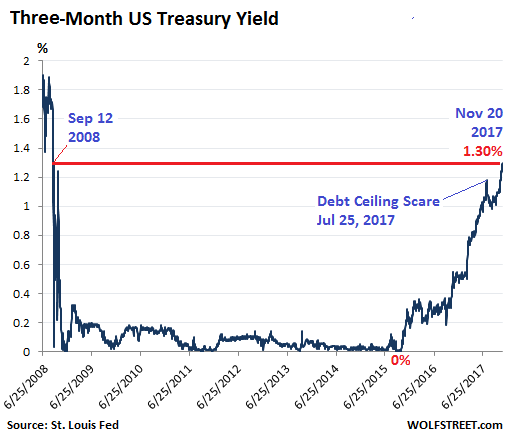

Upon Yellen’s unsurprising announcement on Monday, Treasury securities stayed on trend. The three-month yield is responding nicely to the Fed’s messaging about another hike of its target range for the federal funds rate in December. After hitting 0% in October 2015, the three-month yield rose to 1.30% on Monday, the highest since September 12, 2008. Thus it now exceeds the Fed’s current target range of 1% to 1.25%:

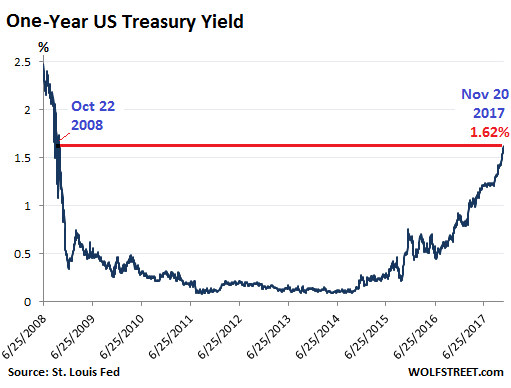

The one-year Treasury yield rose to 1.62% on Monday, the highest since October 22, 2008. It never quite got to zero but fell as low as 0.1% in 2011 and 2014:

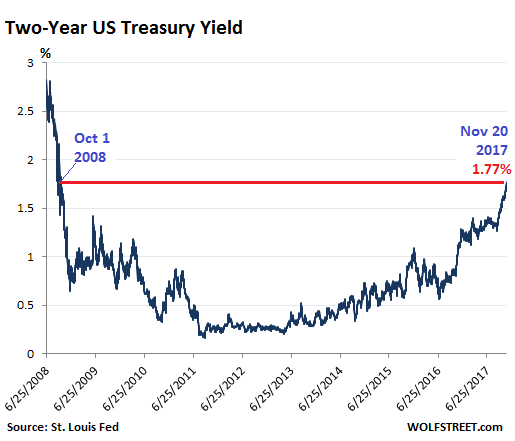

The two-year yield surged to 1.77% on Monday, the highest since October 1, 2008:

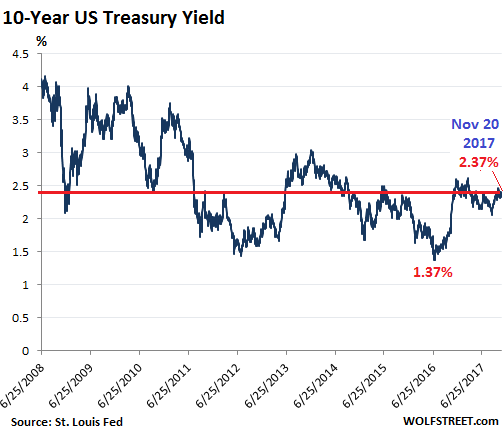

But with maturities of three years and higher, a cacophony has broken out, with longer-term yields jumping up and down energetically. The 10-year yield rose to 2.37% on Monday. That’s still down from earlier in November and down from late last year and early this year. But it’s up a full percentage point from the low of 1.37% in August 2016, the lowest in the data series going back to the 1960s:

The two year yield’s relationship to the 10-year yield has proven to be an ominous precursor in the past. And it’s at it again, to the point where the difference between these two yields – the “spread” – has made its way onto the Fed’s worry list. That spread has collapsed to 0.60 percentage points, the lowest since November 1, 2007.

Back in November 2007, the spread was widening after having been negative in late 2006 and early 2007 as part of an “inverted” yield curve when investors chased after Treasuries with long maturities, and their yields fell, even as they dumped Treasuries with shorter maturities and their yields rose. Not much later, the Financial Crisis cracked the veneer of the banks. So this spread is the bond market’s reaction to something – and it’s not propitious:

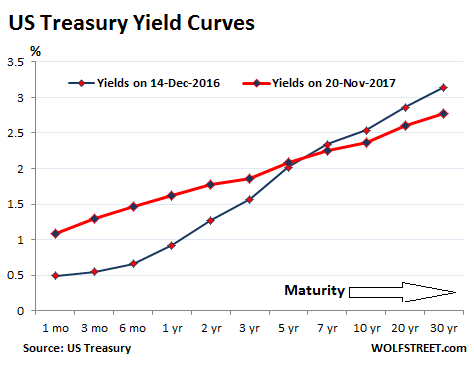

This makes for a peculiar yield curve. The chart below shows Monday’s yields (red line) across the maturities, and the yields on December 14, 2016 (blue line), when the Fed got serious about tightening. Note how the yield curve has “flattened,” with the short end rising and the long end falling compared to December 2016. If yields of longer maturities continue to drop and fall below yields of shorter maturities, the yield curve “inverts.” The last time it inverted was a precursor to the Financial Crisis.

But this time, the Fed has a new set of tools to combat the inversion of the yield curve: its $4.5 trillion balance sheet. The Fed has already kicked off its QE unwind, allowing maturing securities to roll off without replacement, but at an utterly timid pace for now. Its new tool: If it wants to bring up longer yields, it can announce with fanfare that it will outright sell Treasury securities that won’t mature for years and then actually dump them on the market. Watch long-term yields jump — along with the financial fireworks this will create.

What the Fed currently sees – after four rate hikes and a fifth coming, and after kicking off the QE unwind – is an orderly selloff at the short end of the curve that hasn’t caused any kind of market tantrum. Markets are not rattled by this at all. Stocks are riding high. Corporate bond yields remain very low. And this could encourage the Fed – the new Fed next year – to pursue its “normalization” strategy more vigorously, while trying to get the yield curve to tilt up at the long end, and do all this while it still can before the next recession shows up and before markets throw a serious hissy-fit.

Inflation is already moving beneath the surface. Read… New York Fed: “Underlying Inflation” Hits 11-Year High

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I watch the 10s-2s and the high yield spreads as the best indicators of an approaching recession. The 10s-2s spread has flattened some, but is still at +60 basis points, and the yield curve overall remains normally shaped. Sure it’s not as steep as before, but all throughout the mid-late 90s raging bull market, the spread was 60 basis points or less before finally convincingly inverting in February, 2000…

Once the yield curve inverts, I’ll seriously consider lightening up on equities. We are still a long way from that point. There still is no alternative…

If the US Treasury smells a rat it’s got a better sense of smell than Ed Norton did in the “Honeymooners” when he told Ralph Kramden that, “I was down in the sewers under New York in rubber hip waders and couldn’t smell a rat that was two feet away”.

Get ready for this shit show to commence after the first of the year.

Let the American dipshits bleed their least drops of blood on XMAS before they see what the REAL America looks like Third World Style…

Mike,

Why would you celebrate a tragedy? Everyone who isn’t in the top 20% knows how bad things are. What exactly are they supposed to do about it? They work, many multiple jobs, get home exhausted. They are too tired to rant on the internet, too poor to run for office in a rigged plutocracy. So they go to bed and get up and go to work in the morning. That’s all they can do unless you are suggesting a revolution. Maybe that’s a good idea, but historically speaking, most revolutions are a disaster. The resulting government is worse than the last one. Not to mention at this point in terms of power over people’s lives the government is dwarfed by multinationals. What then, people don’t vote about what Verizon or Disney shoves down their throat anymore than they vote about Exxon-Mobile poisoning their water. I understand being frustrated. But consider thinking about things privately.

I’m afraid you’re right. Debt levels are exploding as folks think they deserve it all . Shocking that lower class can have a house in the Keys with a nicely financed boat.

If one plots the Ten year minus the Two year bonds from 2004 to 2009 one sees a massive trough. History looks like it will repeat this time around. Grab your popcorn.

Hi Wolf,

Pardon the ignorance but does increasing yield on a bond or US treasury indicate lowering of confidence?

And who and what determine the yield? Can the yield of a sold product change?

Thanks

Price determines bond yields. In general and simplified terms, a bond has a coupon (unless they’re short-term bills, “zero-coupon” bonds, or similar). This coupon reflects the periodic interest payment that the issuer has to make to the bondholder.

For example, bond X with a face value of $1,000 has a coupon of $50 annually. If you pay $1,000 for it when it is newly issued, you’re getting a yield of 5%.

If the price of the bond drops to $500 the next day (which would be embarrassing), the yield on that bond is now 10% = the $50 interest on a $500 investment.

If the bond doubles in price and goes to $2,000, the yield drops to 2.5% = the $50 interest on a $2,000 investment.

Every time the price of a bond changes, the yield changes in the opposite direction by definition.

Moderate this….bond yields and prices will Both go to zero if the central bank

Lunacy continues, and your Bonds 101 course will do this investor tremendous harm…..don’t you think explaining repudiation like what just happened in Venezuela should also be part of the relationship between price and yields.

Here are some essential basics:

Venezuela’s defaulting debt is in a currency the government doesn’t control (dollars). It actually has to either service this debt or default on it. It cannot deflate it away, and its central bank cannot print dollars and buy this debt and do away with it.

A country like the US that issues debt in its own currency can never default because the central bank (Fed) can and will print money to buy the debt. The Fed’s role as lender of last resort will always be there. So there will be no default in the US, and the credit risk of US Treasuries is therefor near zero. In other words, you will always get your money back and you will always get your interest payments.

The way the US has dealt with its debt is by destroying the dollar via inflation. But this has been a gradual process rather than a sudden process that has been going on for 100 years. And even if inflation gets to 18% or whatever, you will still get your interest payments, and you will still get your money back when the Treasuries mature. That money will have just lost some of its purchasing power.

That’s why you can read articles here about inflation.

“Repudiation”. The idea that crypto-currencies are not real money is connected to this thought. If a government such as Venezuela repudiates in a currency they do not control, or issue, the same problem rides on crypto-currencies: if a government decides to take tax payments, or issues bonds payable in crypto-currencies, they can by declaration, say they will repudiate payment of interest on said bonds, in said crypto-currency.

Lender of last resort normally refers to central bank lending facility, so called discount rate, to lend to a failing bank that is not able to secure loans from other banks, but we live in a new reality where old notions have been thrown out the window. Plan accordingly.

Don’t you think the current money flows are a flight from public (gov. debt) to private (equities) triggered by a *loss of confidence* in governments?

I don’t see a “flight from public debt” scenario. Not at this point. Yields are still very very low, just not as low as they were a little while ago.

Thanks for the very informative articles, and for the example above.

>> you will still get your interest payments, and you will still get your money back when the Treasuries mature

In the example above, The bond was issued for $1000, so on maturity, the last holder will receive only $1050 regardless of how much they paid to buy that bond, right? Does this not mean there is profit/loss for individuals (who buy/sell at different amounts than the face value) irrespective of the yield being lower or higher than the original 5%? Can you help me understand this?

rv,

At maturity, the holder of this example-bond will receive face value ($1,000) plus any interest due (that could be $50). If it’s a 10-year bond, the holder received $50 every year for 10 years (=$500). When the bond matures and is redeemed, the holder gets her initial investment back at face value (=$1,000). So in total, over the 10 years, the holder earned $500 in interest income and at the end gets her investment back.

The $500 is income. The $1,000 is return of the initial investment and not income (return on capital and return of capital)

This assumed that the bond does not default.

But the important piece is that bond prices drop because there are fewer and fewer buyers correct? Lower demand increasing supply etc. We have so overly complicated the crap out of economics in this country that the only rationale behind it is that it was done for nefarious purposes. This is increasingly panning out as true!

Yes, prices drop because there are fewer buyers at that price. That’s the key. Once the price drops enough and the yield rises enough, it attracts buyers. If the probability of default rises, buyers will demand a lot more yield before they take the risk.

But once central banks get involved, the entire equation changes. And they’re heavily involved.

Yields are normally effected by future inflation expectations (and so short-term interest rate), but whether it’s true inflation or state manufactured inflation, I am not sure. The keyword is “normally”, and I am afraid that refers to a vanishing past.

Bloomberg ran an article a couple weeks ago titled “Treasury’s Surprise Debt-Maturity Move Eases Sting of Fed Unwind” in which they reported that the Treasury is issuing more short-term debt and reigning in long-term debt in order to intentionally keep the long end of the curve suppressed.

I suppose this means that our savvy overlords think a flat yield curve is a good thing? Or maybe the Fed and the Treasury are just piloting from opposite sides of a teeter totter.

At the same time, Mnuchin tested the waters for a super-long-bond of 40+ years. There was little interest in the market for it, but there was interest at Treasury for it. So I’m not sure how to read all this.

Treasury is still issuing plenty of long-term debt … well, let me rephrase this, it’s issuing plenty of debt due to growing deficit spending, and some is long-term. This was a tweaking of the maturity plans, not a drastic change.

This also means that this short-term debt to be issued will have to be refinanced in the shorter term, thus pushing up supply of new issuance at that time, just when the additional deficits from the tax cut (if it happens) need to be funded. So this could get interesting.

US Treasuries are going to continue to nab a bid due to the much larger problems elsewhere (Europe….and to a lesser extent, both Japan & China).

Europe is a walking disaster…with zombie banks in Spain & Italy (and France) propping us only slightly less zombie banks elsewhere. The European gov’ts are paralyzed by the enormity of the financial problem (i.e. 1) prime cause that the Jamacia coalition talks in Germany fell apart……the German’s refuse to prop up Italy, Greece, and Spain…….2) Spain’s gov’t is falling apart as it cracks down on it largest taxpaying region for its independence movement…..3) Italy’s gov’t can’t put together a ruling coalition)

France escaped from (really delayed) the contagion with its election of Brussel’s puppet Macron….but he is without real allies in the French gov’t….so he will remain ineffective until new elections….though the elitist press will hold him up as the “best” solution for Europe.

The pension crisis in Spain in acute…with their main pension funds (which the central gov’t has been borrowing from for a decade) is expected to go bust next year unless Spain can float some significant new debt….new debt that most of the rest of the continent isn’t going to buy…and debt which the ECB CAN’T buy without the approval of Germany/France….due to lack of ability to issue currency unfettered by the whims of the national gov’ts in Europe.

Is it any wonder why the ECB just reported its recommendation to change the deposit insurance system in Europe? Or do they see deposit insurance as a major problem going forward now that Italy and Spain are collapsing (in slow motion).

This is all true, but European fund managers are moving into U.S. equities more rapidly, signifying a global flow away from public to private investment.

This is all coming to close to the post thanksgiving point where many investment decisions are baked in until January. Post January with a new fed things could get very ugly for the supporters of p 45 in trumpeter land.

There is a remote pool I regularly pass that is home to a Family of Black swan’s (Yes they are native to this country) they were not there last time I passed.

Perhaps they are on their way to the financial districts of some developed nation’s.

This all sounds good in theory. In the real world we have unelected bureaucrats from Japan and Europe buying all along the curve to weaken their own currencies.

Don’t get me started on the Swiss

Nice summary on bond rates Wolf. Thanks for your work.

It is clear to me that the Fed with other CB’s are orchestrating a “no problem” move from ZIRP. They do this by manipulating through sales and purchases of key futures to make it appear that the tightening move is being well received. This explains the stock market move as well (for now).

As they succeed, everyone else falls in and buys/sells to unwittingly support the “image” the Fed wants to promote: That everything is under control with the normalization of rates.

The only problem of course is that the real economy will not respond so well, since “growth” is now solely related to debt creation.

But that is a problem for another day, another Fed Chair, etc.

The obvious solution when things slow (and they are and will continue) and that has been touted excessively is “infrastructure spending”. Watch Congress lay down and vote a trillion in stimulus in this area. The seeds have already been sown as we now all readily regurgitate missives about our “crumbling infrastructure” ….which of course it is not that bad.

It will take to 2018 (mid) for these interest rates to start kicking in and slowing the economy further, I believe.

I think it is important to discuss why the yield curve inverts before a recession.

“Back in November 2007, the spread was widening after having been negative in late 2006 and early 2007 as part of an “inverted” yield curve when investors chased after Treasuries with long maturities, and their yields fell, even as they dumped Treasuries with shorter maturities and their yields rose. Not much later, the Financial Crisis cracked the veneer of the banks.”

This was an indication of a “flight to safety” as bankers started having concerns of a possible crash. I don’t think that is the case right now. I think short term rates are responding to the Fed, and long-term rates reflect an assumption of fairly weak long-term growth.

Yes.

I think it’s almost unimportant to think about all the other macroeconomic data as the yield curve tells you what the “smart money” (presumably with the time and the resources to analyze and understand that data) thinks is going on in the economy.

The short end of the curve is rising to keep pace with rate increases in the Fed Funds rate. The long end of the curve is slowly coming down (with a few bumps along the way) reflecting a future of slower growth and lower inflation.

When the two ends meet and the high yield spread starts rising, I’ll be anticipating some fireworks in the stock market. Smooth sailing conditions prevail at the moment though.

At this point in time, the Fed’s high wire act cannot handle the slightest shift in winds. Any serious drop in stock prices or rise in LT rates will feed on itself and prick the bubble. For stocks, I’d say anything more than a 5% drop would turn the tide. Once the lemmings see the bigger dip, they’ll run for cover. Many people will start shorting the market with confidence and it is game over.

Of course, everything is accelerated these days. We could wake up to a 7% drop overnight.

Wolf great article. Just had a thought concerning cripto’s:Would it be reasonable to suggest that a crash might occur when there a rush to the exits to cover margin calls.I don’t think the exit is wide enough to handle the flood.

I am quite amazed when I see articles like this one,because they reflect a completely US CENTRIC view of bond markets and neglect the large influence of FOREIGN CENTRAL BANKS.

There are completely different forces that are acting on the 2 year note vs the 10 year bond

The 2 year reflects current and expected action of the US FED to slowly raise the Fed funds rate.There is a very high probability that the FED will raise rates an additional 25 basis points next month .The 2 year and shorter durations are completely dominated by actions of the FED.

On the other hand the FED is no longer doing QE and is not a significant factor in the longer term durations. Instead, the 10 y rate is driven by foreign buying due to the large spreads between US and foreign 10y yields.As long as foreign central banks are huge buyers and as long as US/foreign bond spreads remain high and forward foreign currency rates allow it,this foreign demand for the 10y will continue

The ENTIRE move in world wide equities this year has been driven by huge foreign QE. The bull move will die and crash when foreign QE dries up

https://www.ft.com/content/7c0c2f62-645e-3b04-92c2-d87e36e9695d

Yup, people forget that a flight to supposed safety, and higher yields than European bonds , are the main demand factors for USG debt, and therefore the main reasons that USG long-term yields have been dropping.

Could not read the FT link, it is behind a paywall.

Wolf, you seem to take the FED announcements at face value. In the meantime, a really dangerous brew is brewing. How about the following piece of news?

Fed’s Williams calls for global rethink of monetary policy:

https://www.reuters.com/article/us-usa-fed-williams/feds-williams-calls-for-global-rethink-of-monetary-policy-idUSKBN1DG33N?il=0

As usual, they have only one answer.

“And that means taking into account the nature of monetary policy spillovers.”

Central Banks *fine-tuning* the global economy like a thermostat. Ha!

They seem to be under the delusion that they have fixed the economic titanic, and all is going well.

There may very well be a re-think at the Fed next year, with all the new people coming on board. To be honest, I have no idea where they will take us because we don’t know many of the players yet. Powell and Yellen were close in their pronouncements. But this too might change. I don’t think that San Francisco Fed Gov. Williams will be very influential. He has been talking about letting inflation “overshoot” and targeting higher inflation for years.

I’m going to go way out on a limb and postulate that whoever comes or goes at the Fed, its principle directive will stay the same: to effect the transfer of wealth from the middle and working classes to the Fed’s oligarch patrons.

Workers of the world unite

um, i think the point is being missed. the price of money for short term borrowing is rising.

or, conversely, the price of money for short term lending is rising.

or maybe i am wrong.

Global exports to the US are better sustained if the export

country’s currency does not rise in value, making exports

more expensive to US importers. Foreign purchases of US

stocks, esp. by foreign central banks, tends to regulate a rise

in value of the Swiss franc, So. Korean wan, Norwegian krone,

Japanese yen etc. I rarely see this discussed on CNBC,

Bloomberg, Fox or the print media.

– The 3-month T-bill is now over 1.25%. And that means that the FED will raise rates in December (2017).

– Investors are pulling money out of e.g. the T-bills and pouring that into the stockmarkets. See e.g. the rising amount of account at Charles Schwab.

The Fed has been telegraphing for 11 months that it would raise rates three times in 2017, including in December. I’ve been saying this for 10 months. There is no need to wait for the 3-month yield to move up before you can figure out what the Fed will do. The Fed is telling investors what it will do. And the 3-month yield follows.

Market participants start moving the 3-month yield higher when a projected rate hike moves into the 3-month window. Sometimes market participants underestimate the Fed’s determination for a rate hike and get surprised, and then a few weeks before the rate hike, the yield jumps suddenly.

– Mr. Market doesn’t “smell a rat”. The yield curve is a “risk appetite” gauge.

– When the yield curve inverts then that’s NOT a “precursor” for a “recession”. Only when inverted curve turns to steepening again then that’s for me a sign for a coming recession.

Much to agree with here.

– When one wants to see whether our US economy is in a “recession” or not then one should be looking at the development of the amount of debt. If the “change in debt” has started to shrink then we are – definitely – in a “recession”.

Source: Steve Keen.

Good article

If the value of bonds increase, yield (interest) decreases

If the value of bonds decrease, yield (interest) increases.

For sovereign bonds any decrease in their value means that more and more receipts from taxes has to be ring fenced to pay the higher yield.

This means (i) higher rates applied to existing taxes, or (ii) imposition of new taxes, or (iii) diverting existing public funds away from public services to pay higher yield (interest).

To complicate matters further, because governments have issued billions of bonds, and these bonds and their yields have to be repaid, even a small uptick in yields (interest rates) could be fatal

With reference to what r cohn and JM Keynes have stated above:

The yield curve “inverts” mostly because short rates spike when banks start refusing to lend to each other (interbank lending), and rarely because the long rates changed drastically (there is a great graph of this that I saw the other day but I can’t find it right now). The underlying interbank lending freeze happens when and because bank debt losses start increasing and become generally known in the banking industry.

So, yield curve inversion is not the CAUSE of recession, it is a SYMPTOM that banks (and their customers, too) are becoming very concerned about the risk involved in making short term loans. Of course, after the inversion happens, banks also cannot lend profitably (remember, banks borrow short, lend long) ,so then GDP will drop, being very dependent on ever increasing debt in order to “grow”. And there arrives the recession,as defined by specific GDP drop criteria. But it is bad debt that causes the recession, not the yield curve per se. The yield curve inversion is a consequence of the debt losses that banks generally keep well hidden but start becoming so high the losses can no longer be ignored, and some weak banks starts to fail because they cannot get credit from other banks except at rapidly increasing short-term rates.

bad debt causes the recession

or the recession results in bad debt?

bad debt causes the recession

or the recession results in bad debt?

This is to simplistic.

You need to define the “bad Debt” as it is a term with many meaning’s.

Is it a “Bad Debt” as the debtor you expected to pay, didnt pay for whatever reason.

Has it become classified as” Bad Debt” as the lender should not have given the credit/loan in the first place. To an Insolvent/Uncreditworthy Debtor. In which case it was “Bad Debt” the second it was issued, (Credit was given).

This is the type of “Imprudent lending” AKA “Bad Debt” that frequently Initiates recession cycles.

Recession Cycles leave Prudent lenders with “unrecoverable Bad Debt’s” due to the failure, of formerly, stable and solvent. Debtors. Frequently as those debtors supplied a good or service to an over-leveraged speculator. Who has not, and will not, pay them.

“A country like the US that issues debt in its own currency can never default because the central bank (Fed) can and will print money to buy the debt. The Fed’s role as lender of last resort will always be there. So there will be no default in the US, and the credit risk of US Treasuries is therefor near zero. In other words, you will always get your money back and you will always get your interest payments.”

Mr, Richter,

Yes, you will always get your money, but maybe not the value. Under the current system, the US is in the happy condition of being the World’s reserve currency, with the house of Saud requiring dollars for payment of oil. A country without that standing, which massively debases their currency to pay their bills, will soon find that their trading partners will not accept those Zimbabwe, Venezuelan, or Weimar currencies for goods and services…and then there are toilet paper riots….

I expect that our free role will soon come to an end…Chinese gold-backed currency to commence 1 January 2018?

“I expect that our free role will soon come to an end…Chinese gold-backed currency to commence 1 January 2018?”

Try after they have milked dry and imploded the current system.

Which is what they are endeavoring to do, destroying the US $ and economy in the process. (Which they will do to that unpleasant customer, when they no longer need them)

China is selling lots of long term Debt, in US $.

This means:

A, they really need US $, (We know they dont)

Or B, they have no Intention of repaying the debt in anything but CNY/RMB Bonds as they intend to have a selective, or engineered, general, Default,

Or C, they expect US $ to be very cheap when the debt is due.

None of this will take place in Jan 2018.

china intends to Milk the current system, for a considerably longer period of time yet. Or they would not have tried to keep it rolling as fast as possible in 2008/9/10.

China is perfectly happy buying up western assets it wants with printed used CCP toilet paper.

The problems start once china has most of what it wants, and owes everybody huge amounts of money, in non chinese currency.

Yellen doesn’t want inflation to “drift lower.” Never mind that real inflation is much higher than our Soviet-style CPI data indicates, or that the Fed’s relentless debasement of the currency means the 99% are being robbed through the stealth tax of inflation. Never mind that on our incorporated neoliberal plantation, living wage jobs are disappearing and an increasingly pauperized population are increasingly hard-pressed to put a roof over their head, pay for medical care and insurance, send their children to college, buy a new car, etc. This is creating deflationary pressures that the Fed will attempt to counter with yet another round of deranged money-printing for the exclusive benefit of its .1% cohorts.

We are so screwed.

Gershon

Your post has nailed it!

Consider the concept of “Mean Reversion” and apply it to interest rates. We’re 1% at the present and since in the last 35 years we’ve seen 16% on Fed Funds rate getting back to 5-6% isn’t that much of a stretch. That the Fed can always print cash (in dollars) isn’t the issue. The total interest on debt already issued by the US Government is presently $240billion / annum on an average interest rate of 1.8%. Should we get to 5% Uncle Sam would then need to pay $681billion/annum.

http://wealthtrack.com/end-of-an-extraordinary-era-james-grant-declares-the-end-of-the-lowest-interest-rates-in-five-millenia-and-warns-of-the-perils-ahead/#more-16267

At which point the strength of the US currency would come under serious pressures.. Serious pressure..

“Should we get to 5% Uncle Sam would then need to pay $681billion/annum.”

“Uncle Sam” Dosent pay it.

He takes it from the US Taxpayer, and gives it to the lender’s.

So Taxes go up, or a whole lot of other stuff, Taxpayer expect to happen. Dosent happen any more.

I was quoting minute 3 of that video with James Grant. Yes eventually Uncle Sam takes it from the tax payer via printing new bonds that get issued and debase the tax payers current fiat holdings. Which is in part why we’ve $21 trillion of debt ..

I would disagree somewhat with your assumption that the Fed Funds rate rising to 5-6% wouldn’t be that much of a stretch. I think it will be very hard to get inflation back up to levels seen in previous decades, and central banks around the world will continue to be able to maintain very low interest rate policies as a result. Many long term factors are at play including a declining/flat birth rate, obsolescence of entire industries by technology, over indebtedness of the young, and a major shift in wealth away from those who would spend – the working/middle classes and the young.

Mark

We are equally entitled to our opinions. I think everyone will be shocked, with the coming disclosure of inflation. The BLS and all governments intentionally under-report inflation. John William’s Shadow Stats has documented this phenomena.

That you believe that interest rates can’t get to 5-6% (for whatever reasons) will almost certainly be the reason that they will. Yes I could absolutely be wrong. Mean reversal is a natural phenomena. So don’t be surprised when you see $100/bbl for Brent Crude oil!

The government must stop buying 70% of all originated residential mortgages. They must start telling the truth about inflation. They must get out of controlling the economy with there lunatic monetary policies. They must reduce spending almost across the board. They are killing middle America.